Food Decorations and Inclusions Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.60 Billion |

| Market Size (2031) | USD 10.10 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

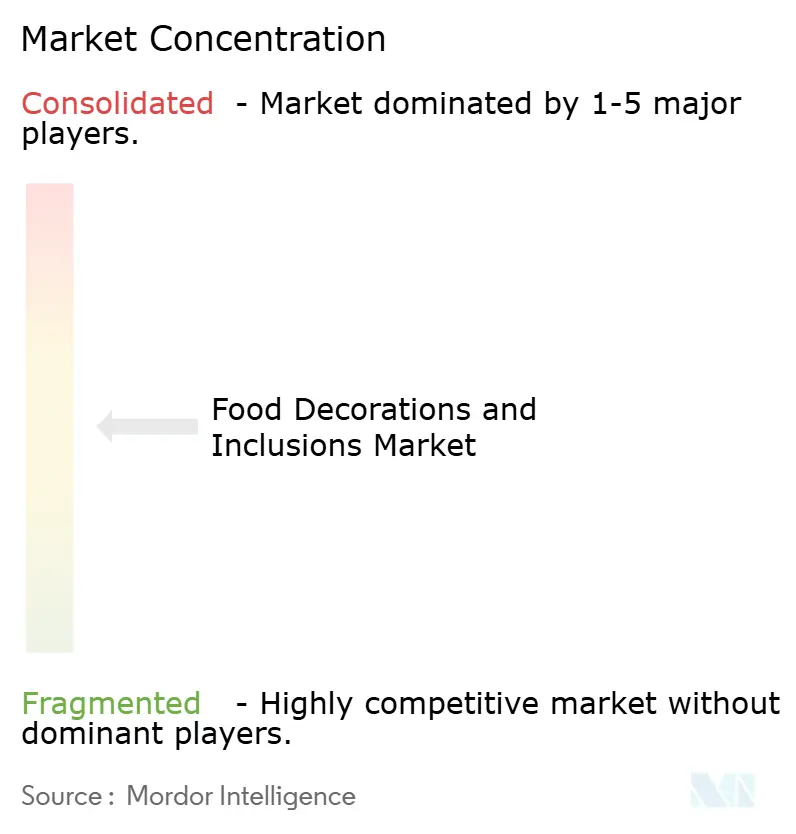

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Decorations and Inclusions Market Analysis by Mordor Intelligence

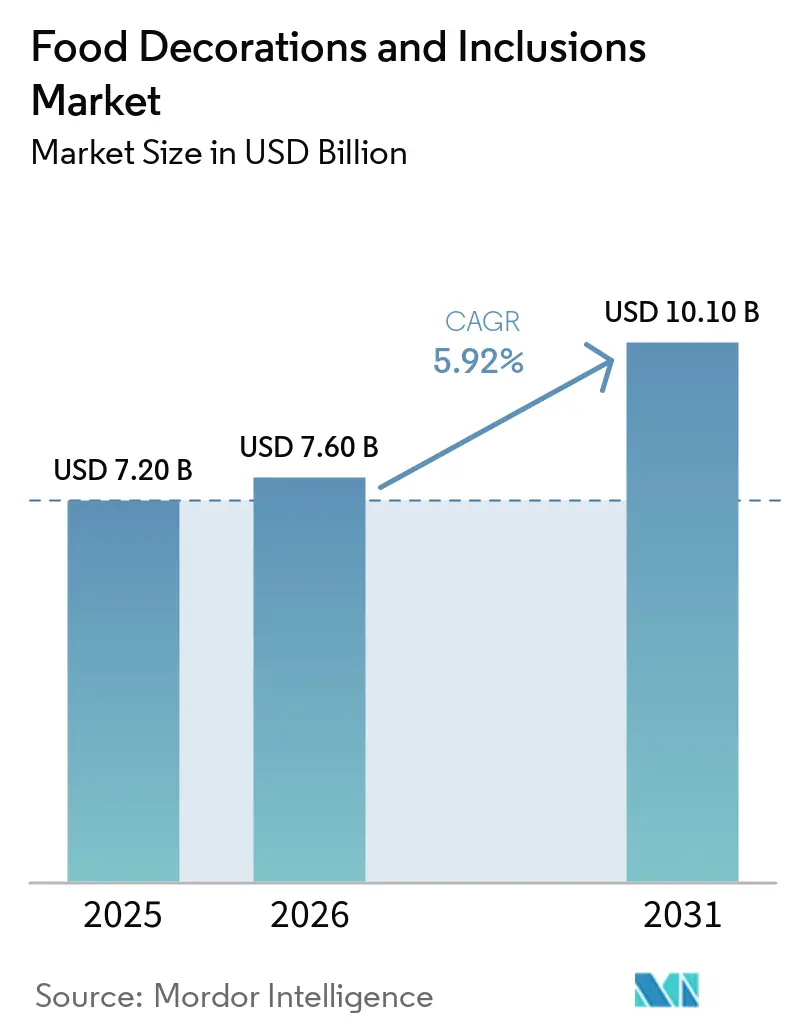

The food decorations and inclusions market was valued at USD 7.20 billion in 2025 and reached USD 7.60 billion in 2026, with an expected growth to USD 10.10 billion by 2031, registering a CAGR of 5.92%. This growth highlights a significant shift, as decoration and inclusion ingredients transition from artisanal luxuries to integral components of mass-produced food products. Industrial food manufacturers accounted for 54.11%. However, the foodservice channel is growing at a faster CAGR of 6.86% through 2031, driven by specialty cafes and premium dessert outlets serving as innovation hubs. These outlets test new decoration formats that are later adopted in large-scale production, giving the foodservice segment market influence that exceeds its current revenue share. Additionally, the rising demand for limited-edition, seasonal, and customized food products is driving innovation in decorative formats across applications such as bakery, confectionery, dairy, and frozen desserts. As competition intensifies in the packaged food market, decorations and inclusions are emerging as strategic components that enable brands to differentiate their products, justify premium pricing, and enhance shelf appeal.

Key Report Takeaways

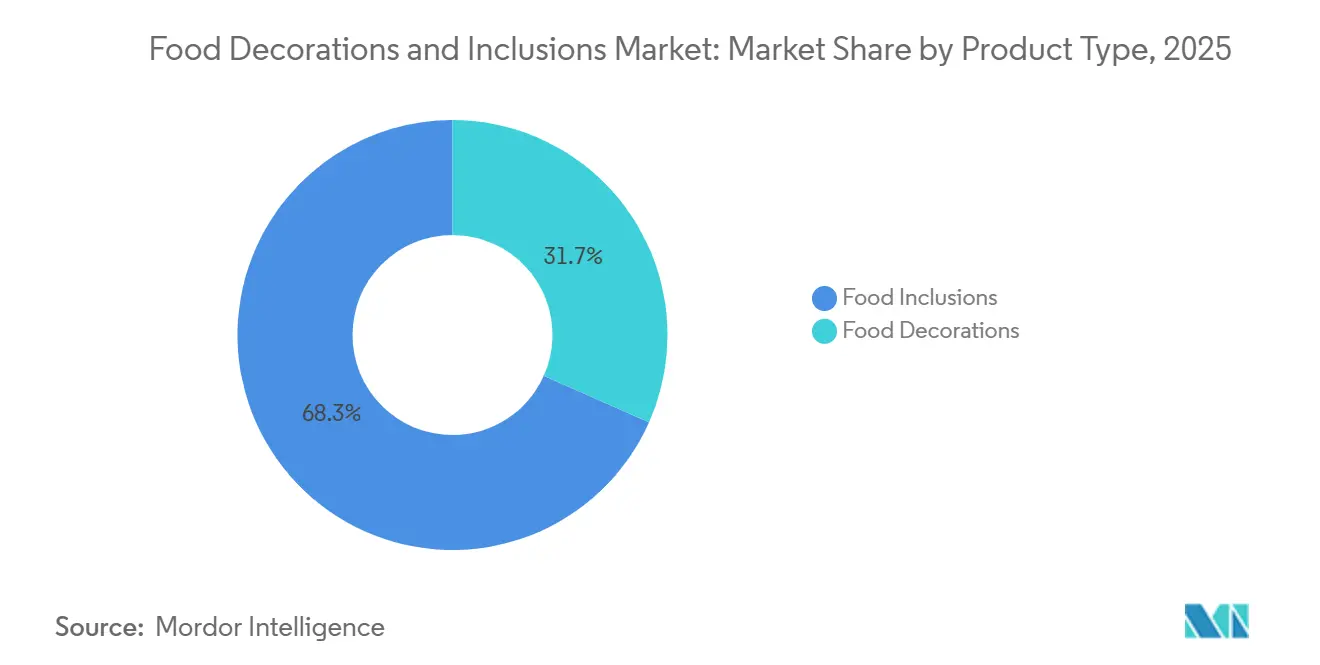

- By product type, food inclusions captured 68.34% of the 2025 market, while food decorations are advancing at a 6.99% CAGR through 2031.

- By ingredient type, chocolate decorations and inclusions retained a 30.19% share of the food decorations and inclusions market size in 2025, while the preserved and freeze-dried fruits segment is forecast to grow at a 7.83% CAGR through 2031.

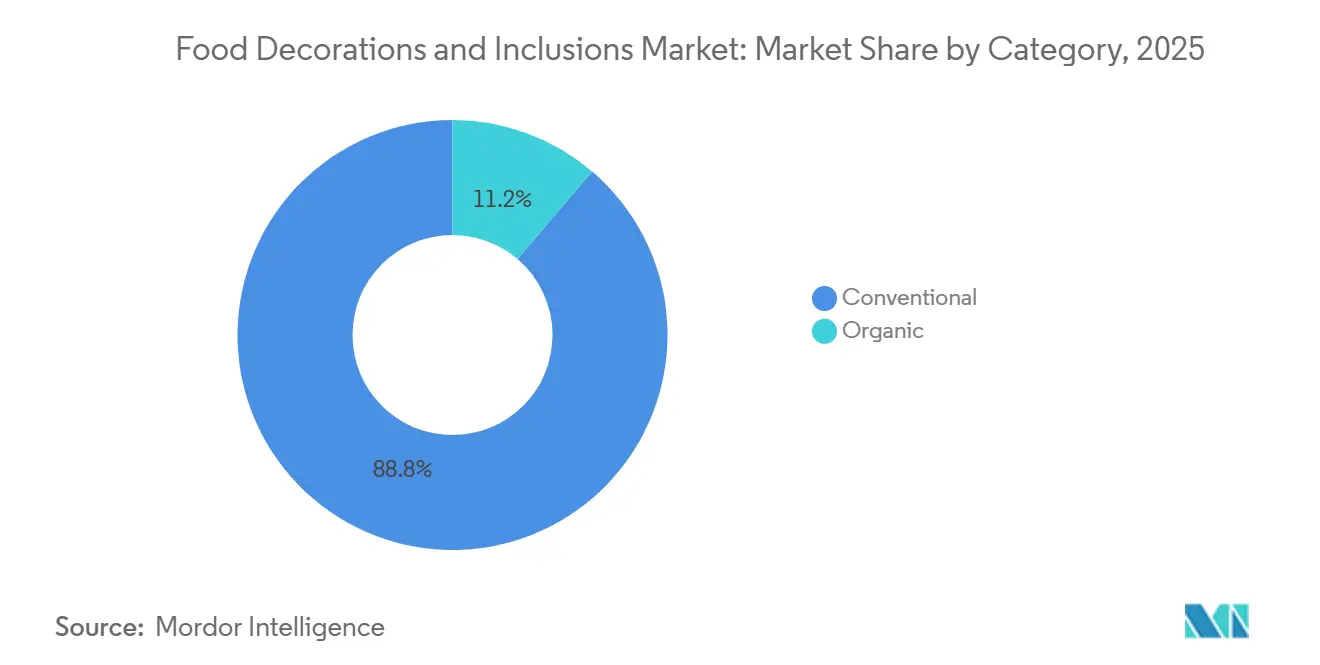

- By category, conventional commanded 88.76% of demand in 2025, whereas organic is expanding fastest at 8.37% CAGR between 2026-2031.

- By end user, industrial food manufacturers commanded 54.11% of demand in 2025, whereas foodservice is expanding fastest at 6.86% CAGR between 2026-2031.

- By geography, Europe accounted for 32.02%of 2025 revenue, while North America is the fastest-growing segment, with a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Decorations and Inclusions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for visually appealing and instagrammable food products | +1.4% | Global, led by North America, Europe, and urban Asia-Pacific centers | Short term (≤ 2 years) |

| Expansion of premium bakery and confectionery products | +1.1% | Global, with stronger pull in North America and Europe | Medium term (2–4 years) |

| Expansion of artisanal bakeries, specialty cafes, and premium dessert outlets globally | +0.9% | Global; North America and Southeast Asia driving fastest network growth | Medium term (2–4 years) |

| Rising demand for clean-label and natural decorations | +0.8% | North America and European Union core; spill-over to Asia-Pacific and Middle East and Africa | Medium term (2–4 years) |

| Innovation in product formats, textures, and flavor combinations creating differentiated offerings | +0.7% | Global; industrial hubs in North America, Europe, and Asia-Pacific | Medium term (2–4 years) |

| Growing demand for customized industrial ingredient solutions | +0.6% | Global, with highest traction in large-scale manufacturing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for visually appealing and instagrammable food products

Social media has significantly transformed the economics of food presentation, with its impact increasing as scale grows. According to industry research by Dawn Foods, 57% of consumers are influenced by social media to purchase bakery items, establishing a direct connection between visual platform engagement and demand for decoration ingredients[1]Source: Dawn Foods, "Dawn Foods unveils Dawn Global Bakery Trends at IBA", dawnfoods.com. This trend accelerates product development cycles, as a single viral dessert format can create urgent ingredient procurement needs within weeks. Suppliers with diverse, ready-to-ship decoration portfolios are better positioned to capture market share compared to those with longer lead-time supply models. This shift particularly benefits products like edible glitters, shaped sprinkles, and vibrant color-inclusion formats, which are visually appealing and perform well on social media. Additionally, platforms such as Instagram and TikTok are driving artisanal decoration standards into semi-industrial production, as commercial bakeries replicate viral designs at scale.

Expansion of premium bakery and confectionery products

Premiumization in baked goods is gaining momentum across both retail and foodservice channels, extending beyond luxury price points. Kerry Group's 2026 Taste Charts highlighted "Swicy" (Sweet + Spicy) flavor profiles and Korean-inspired inclusions as high-growth categories. For example, Gochujang-flavored bakery launches in the U.S. market increased by 120% over the past 12 months, demonstrating how global cross-cultural influences are broadening the scope of inclusion ingredient formulations[2]Source: "Kerry Releases 2026 Global Taste Charts: Defining the Future of Flavour with Data-Rich Insights", kerry.com. Premium inclusions, such as single-origin chocolate chips, caramelized nut clusters, and multi-layer crunch pieces, are increasingly used as price-anchoring tools by manufacturers aiming to maintain higher retail prices without increasing product sizes. This trend positions inclusion ingredient suppliers as key players in margin strategies, rather than solely flavor contributors. For industrial procurement teams, this suggests that loyalty to branded and certified inclusion formats is likely to grow, even as commodity decoration volumes remain cost-competitive.

Expansion of artisanal bakeries, specialty cafes, and premium dessert outlets globally

The rapid growth of artisanal bakeries, specialty cafés, and premium dessert outlets is a key factor driving the food decorations and inclusions market. These establishments heavily depend on visually appealing and texture-rich products to stand out in competitive foodservice markets. Premium cakes, pastries, donuts, cookies, ice creams, and specialty beverages often feature chocolate inclusions, fruit pieces, nuts, sprinkles, glazes, and decorative toppings to enhance both visual presentation and sensory appeal. Additionally, artisanal and premium operators frequently act as innovation hubs, introducing new decoration techniques, inclusion formats, and flavor combinations that are later adopted by large-scale food manufacturers. As consumers increasingly prioritize premium and experience-driven indulgent products, the expanding presence of specialty foodservice outlets continues to fuel demand for high-value decorations and inclusions in global markets.

Rising demand for clean-label and natural decorations

Consumer preference for clean-label food products is driving the demand for natural decorations and inclusions in bakery, confectionery, dairy, and snack applications. Food manufacturers are increasingly substituting artificial colors, flavors, and decorative ingredients with naturally sourced alternatives, including fruit-based inclusions, botanical extracts, natural colorants, and organic toppings, to meet evolving consumer expectations. This trend is particularly significant among younger consumers, who prioritize ingredient transparency and product authenticity. By 2025, shoppers, especially Gen Z and Millennials, are expected to pay 20–30% more for products labeled as organic, natural, high-protein, or free from artificial ingredients[3]Source: "Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. In response, manufacturers are broadening their portfolios of clean-label decorations and inclusions to enhance product appeal and support premium positioning, thereby driving growth in the food decorations and inclusions market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance burden from color, additive, and allergen regulations | -0.5% | Global; strongest friction in North America and European Union multi-market formulations | Short term (≤ 2 years) |

| Supply constraints for specialty ingredients | -0.4% | Asia-Pacific-sourced raw materials (cocoa, tropical fruits); spill-over to Global | Medium term (2–4 years) |

| Rising consumer preference for reduced-sugar products | -0.4% | North America and Europe; early adoption spreading to urban Asia-Pacific | Medium term (2–4 years) |

| High manufacturing costs for premium and organic products impact competitiveness | -0.4% | Global, with highest cost exposure in North America and Western Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Compliance burden from color, additive, and allergen regulations

Strict regulations on food colors, additives, and allergen labeling pose significant challenges for manufacturers in the food decorations and inclusions market. Decorative ingredients and inclusions often contain colorants, flavorings, nuts, dairy components, or other allergenic substances, which must meet diverse regulatory requirements across different regions. Heightened scrutiny of artificial colors and additives is driving manufacturers to reformulate products, conduct regulatory testing, and revise labeling practices, increasing both complexity and costs in product development. Additionally, ensuring allergen segregation and compliance throughout the supply chain is particularly demanding for producers of multi-ingredient inclusions. These regulatory requirements can prolong product development timelines, raise operational costs, and reduce the flexibility to quickly introduce new decoration and inclusion formats to the market.

Rising consumer preference for reduced-sugar products

The increasing consumer preference for reduced-sugar and healthier food options is creating challenges for the food decorations and inclusions market. Many traditional decorative ingredients, such as sprinkles, sugar decorations, confectionery pieces, candied fruits, and sweet inclusions, contain high levels of sugar. Health-conscious consumers are increasingly seeking lower-calorie and lower-sugar alternatives, leading to heightened scrutiny of these products. In response, food manufacturers are being driven to reformulate products by incorporating alternative sweeteners or reducing the use of decorative elements. These changes can affect the appearance, texture, and sensory appeal of the final products. As the demand for sugar reduction grows across bakery, confectionery, and dessert categories, the growth potential for conventional sugar-based decorations and inclusions may face significant limitations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Decorations Lead Growth as Inclusions Anchor Revenue

Food inclusions accounted for 68.34% of product-type revenue in 2025, driven by their essential roles as flavor carriers and textural components in bakery, confectionery, dairy, and frozen dessert products. Items such as chocolate chips, nut clusters, and fruit pieces are integrated directly into product formulations rather than being applied as surface elements. This incorporation into the core product composition fosters stronger supplier relationships compared to decorative toppings, which are more easily substituted across brands. The integration of inclusions ensures consistency in flavor and texture, making them a critical component in product differentiation and consumer satisfaction.

While food decorations generate lower absolute revenue, they are expected to grow at a CAGR of 6.99% through 2031, the fastest among all product types and approximately 1 percentage point higher than the overall market growth rate. This growth is closely linked to visual marketing trends, as the emphasis on product aesthetics driven by social media platforms leads food manufacturers to increase investments in surface decorations, independent of changes to underlying recipes. The rising consumer demand for visually appealing products, particularly in premium and artisanal categories, further accelerates the adoption of decorative elements, making them a key factor in enhancing brand visibility and consumer engagement.

By Ingredient Type: Chocolate's Structural Dominance Under Pressure from Emerging Alternatives

Chocolate decorations and inclusions held the largest ingredient share in 2025 at 30.19%, highlighting chocolate's widespread consumer appeal and extensive use in bakery, confectionery, ice cream, and dairy products. Barry Callebaut's introduction of a dedicated "Cacao Coatings & Inclusions" category and the exclusive commercialization of ChoViva, a cocoa-free, chocolate-like product made with sunflower seeds as the primary flavor component, indicate growing substitution trends within this dominant ingredient segment. Sugar decorations and inclusions, nuts, sugar paste and icing, glazes, and marzipan each serve specific application areas. Marzipan remains particularly popular in European artisanal confectionery, while glazes are increasingly used in quick-service formats that emphasize speed of application.

Preserved and freeze-dried fruits represent the fastest-growing ingredient category, with a projected CAGR of 7.83% through 2031. Unlike sugar decorations, freeze-dried fruits maintain their color intensity and structural integrity in high-moisture applications, offering technical advantages for certain formats. Additionally, their health-oriented positioning enables manufacturers to highlight natural fruit content on packaging, supporting premium pricing that many other inclusion types cannot achieve.

By Category: Organic Segment Signals a Premium Restructuring of the Market

Conventional formulations accounted for 88.76% of the market in 2025, maintaining dominance in absolute volume terms through 2031, driven by established cost structures in industrial food manufacturing. However, the organic segment is expected to grow at a compound annual growth rate (CAGR) of 8.37%, the highest among all segmentation categories. This indicates the emergence of a premium sub-market within decorations and inclusions, which is gradually influencing mainstream formulation decisions. The organic certification process imposes stricter sourcing and processing requirements, serving as a quality indicator for premium retail positioning. This dynamic supports price premiums of 20–40% for organic-certified inclusion formats in specialty retail.

Puratos' "beyond clean label" strategy, introduced at IDDBA 2026, incorporates fermentation science and grain inclusions to bridge organic-adjacent positioning with mainstream baking applications. For ingredient suppliers, the key takeaway is that obtaining organic certification for specific inclusion formats, such as freeze-dried fruits and chocolate, enables access to a higher pricing tier without necessitating full portfolio conversion to organic, making selective certification a cost-effective strategy.

By End User: Industrial Scale Sustains Revenue While Foodservice Delivers the Innovation Signal

Industrial food manufacturers accounted for 54.11% of end-user demand in 2025, driven by the widespread integration of inclusion ingredients across bakery products, confectionery, dairy and frozen desserts, beverages, and other large-scale applications. Among these, bakery products constitute the largest application sub-category, followed by confectionery, dairy, and frozen desserts. Historically, the institutional purchasing power of large-scale manufacturers has led to compressed supplier margins. However, the shift toward co-developed exclusives and proprietary inclusion formats is gradually redistributing pricing power. Suppliers with unique ingredient intellectual property (IP) are able to secure higher margins compared to those offering commoditized formats.

The foodservice channel, which is expected to grow at a compound annual growth rate (CAGR) of 6.86% through 2031, serves as both a commercial market and a source of innovation for the industrial segment. Premium decoration formats that demonstrate success in specialty café settings are typically adopted by mass manufacturers within 18–36 months. The retail end-user segment, while the smallest among the three, is benefiting from the growing DIY baking trend and increasing consumer interest in pre-packaged decoration kits.

Geography Analysis

Europe held the largest share of the food decorations and inclusions market, accounting for 32.02% in 2025. This dominance is supported by the region's well-established bakery, confectionery, and premium dessert industries. Strong consumer demand for artisanal baked goods, chocolate products, and visually appealing confectionery items, particularly in countries such as Germany, France, Italy, and the United Kingdom, drives market growth. Additionally, Europe's mature food manufacturing sector and its culture of product innovation continue to promote the adoption of advanced decoration formats and premium inclusions across diverse food applications.

North America is expected to be the fastest-growing regional market, with a projected CAGR of 6.78% during 2026–2031. This growth is fueled by increasing demand for premium bakery products, indulgent snacks, customized desserts, and clean-label food offerings. Food manufacturers and foodservice operators are leveraging inclusions and decorative ingredients to enhance product differentiation, texture, and visual appeal. Moreover, the rising popularity of specialty cafés, premium dessert chains, and seasonal product launches is driving demand for innovative decoration and inclusion solutions in the region.

Asia-Pacific, the Middle East and Africa, and South America offer significant growth opportunities for market participants. In Asia-Pacific, rising urbanization, growing bakery consumption, and increasing exposure to Western-style desserts are boosting demand for decorations and inclusions. In the Middle East and Africa, the adoption of premium confectionery and celebration-oriented bakery products is increasing, particularly in urban areas. South America is experiencing growth due to the expansion of food processing industries and rising consumer interest in value-added bakery and snack products, contributing to the global market's overall expansion.

Competitive Landscape

The food decorations and inclusions market is moderately fragmented, with multinational ingredient suppliers, specialized inclusion manufacturers, regional bakery ingredient producers, and niche decoration specialists contributing to the competitive landscape. Competition is primarily driven by product innovation, application expertise, and the ability to deliver customized solutions for bakery, confectionery, dairy, and snack applications. Leading companies are focusing on expanding their portfolios of chocolate inclusions, fruit preparations, sugar decorations, and clean-label ingredients to meet changing consumer preferences and strengthen partnerships with industrial food manufacturers.

Market participants are increasingly investing in research and development to enhance the functionality, stability, and visual appeal of decorations and inclusions under various processing conditions. Product differentiation is increasingly focused on clean-label formulations, natural colors, organic ingredients, sugar reduction, and improved texture solutions. As food manufacturers aim to accelerate product innovation cycles, suppliers offering application-specific inclusions with superior processing performance and consistent quality are gaining a competitive edge.

Strategic partnerships, acquisitions, and geographic expansion remain critical competitive strategies in the market. Companies are expanding their presence in high-growth regions and increasing production capacities to meet the growing demand from industrial food manufacturers and foodservice operators. Additionally, suppliers are collaborating with bakery chains, confectionery brands, and premium dessert manufacturers to develop customized decoration and inclusion solutions, thereby reinforcing their market position and fostering long-term customer loyalty.

Food Decorations and Inclusions Industry Leaders

-

Barry Callebaut AG

-

Cargill, Incorporated

-

Tate & Lyle PLC

-

Archer Daniels Midland Company

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CSM Ingredients has introduced Creami, a range of premium indulgent fillings tailored for bakery, pastry, and confectionery professionals aiming to enhance taste, texture, and overall product experience. Developed by leveraging CSM Ingredients’ artisanal bakery expertise and Sipral’s high-quality filling capabilities, the range includes smooth, creamy, structured, and crunchy textures in flavors such as pistachio, hazelnut, cocoa, and white chocolate. Suitable for filling, layering, and decorating, Creami features bake-stable solutions and innovative options like Crunchy Pistachio and Crunchy Hazelnut, which incorporate caramelized kataifi inclusions.

- April 2025: Dawn Foods has expanded its decorating ingredient portfolio with the introduction of Dawn Balance Cleaner Ingredients Colorful Buttercream Style Icings. These icings, made with plant-based colors and natural flavors, offer vibrant decoration options while aligning with clean-label requirements. This launch enables bakery manufacturers and decorators to produce visually appealing cakes and pastries with cleaner ingredient declarations, addressing trends in premiumization and transparency within bakery products.

- March 2024: Cargill has launched a new range of NatureFresh Professional chocolate chips, block chocolates, and cocoa powders at AAHAR 2024, targeting bakery and confectionery manufacturers. The chocolate chips are designed to provide bakers with premium inclusions that enhance cocoa flavor, creamy texture, superior mouthfeel, and visual appeal in products such as cakes, cookies, muffins, and other baked goods. This launch addresses the increasing demand for indulgent bakery products featuring premium chocolate inclusions and decorations.

Global Food Decorations and Inclusions Market Report Scope

| Food Decorations |

| Food Inclusions |

| Chocolate Decorations and Inclusions |

| Sugar Decorations and Inclusions |

| Nuts |

| Preserved and Freeze-Dried Fruits |

| Sugar Paste and Icing |

| Glazes |

| Marzipan |

| Other Product Types |

| Conventional |

| Organic |

| Industrial Food Manufacturers | Bakery Products |

| Confectionery Products | |

| Dairy and Frozen Desserts | |

| Beverages | |

| Other applications | |

| Foodservice | |

| Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Food Decorations | |

| Food Inclusions | ||

| By Ingredient Type | Chocolate Decorations and Inclusions | |

| Sugar Decorations and Inclusions | ||

| Nuts | ||

| Preserved and Freeze-Dried Fruits | ||

| Sugar Paste and Icing | ||

| Glazes | ||

| Marzipan | ||

| Other Product Types | ||

| By Category | Conventional | |

| Organic | ||

| By End User | Industrial Food Manufacturers | Bakery Products |

| Confectionery Products | ||

| Dairy and Frozen Desserts | ||

| Beverages | ||

| Other applications | ||

| Foodservice | ||

| Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the food decorations and inclusions market?

The market was valued at USD 7.20 billion in 2025 and is projected to reach USD 10.10 billion by 2031, growing at a CAGR of 5.92%.

Which product type dominates the market?

Food inclusions held the largest share in 2025, accounting for 68.34% of the market.

What is the fastest-growing segment in the market?

Food decorations are expected to be the fastest-growing product type, registering a 6.99% CAGR during 2026–2031.

Which region holds the largest market share?

Europe led the market in 2025 with a 32.02% share, while North America is forecast to be the fastest-growing region through 2031.

Page last updated on: