Food Humectants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.41 Billion |

| Market Size (2031) | USD 7.45 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

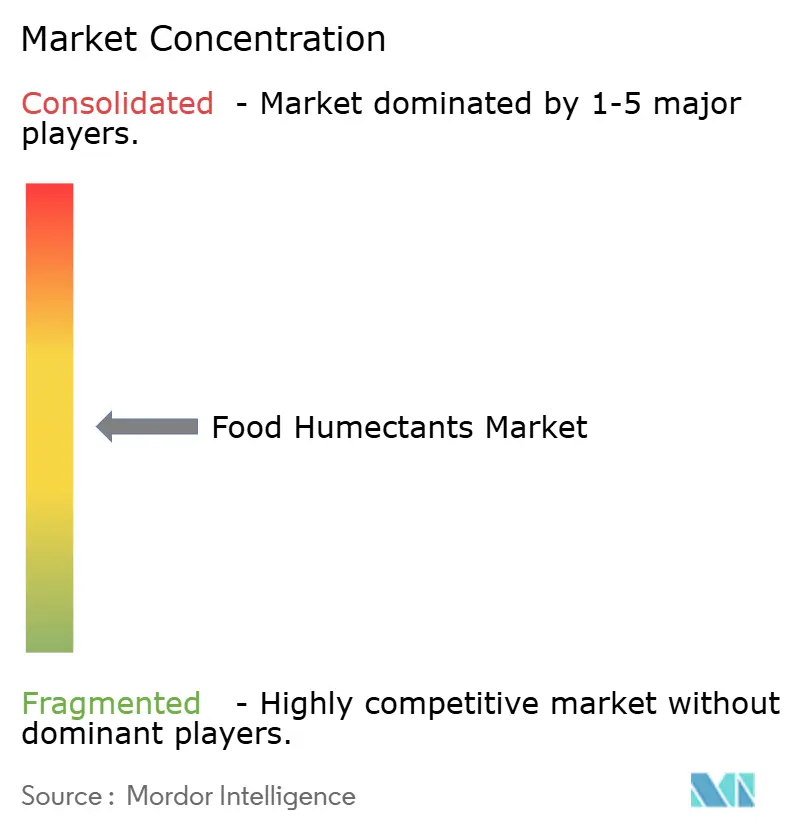

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Humectants Market Analysis by Mordor Intelligence

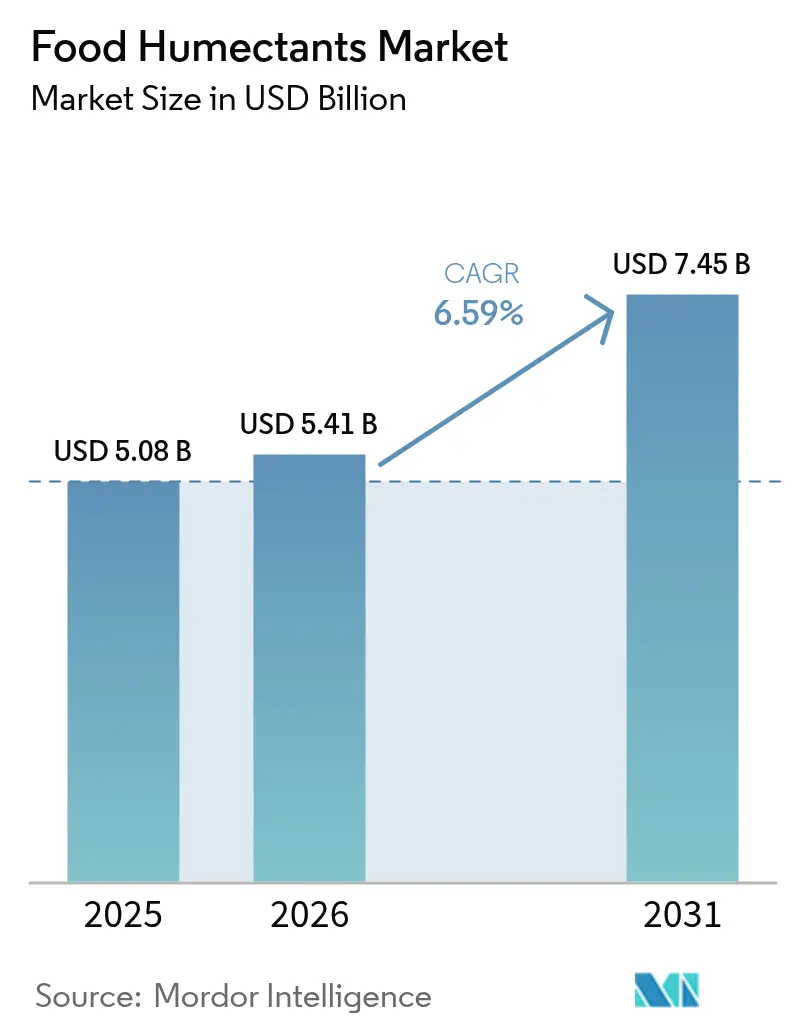

food humectants market size in 2026 is estimated at USD 5.41 billion, growing from 2025 value of USD 5.08 billion with 2031 projections showing USD 7.45 billion, growing at 6.59% CAGR over 2026-2031. Regulatory bodies, notably the FDA and EFSA, are ramping up their scrutiny, pushing the industry towards heightened standards in functionality, safety, and sustainability. In response to this regulatory impetus, the industry is channeling investments into cutting-edge technologies. These advancements not only bolster moisture retention and prolong product shelf life but also align with the clean-label claims that consumers are increasingly prioritizing. To navigate these shifting demands, formulators are turning to innovative solutions. These include bio-based propylene glycol, precision-fermented glycerine, and blends of sugar alcohols. Such choices not only adhere to regulatory benchmarks but also champion environmental sustainability. The competitive arena is witnessing a transformation. Multinational giants are honing their supply chains for enhanced efficiency. Simultaneously, niche suppliers are carving out a larger market share by rolling out natural, multifunctional ingredients that resonate with consumer desires.

Key Report Takeaways

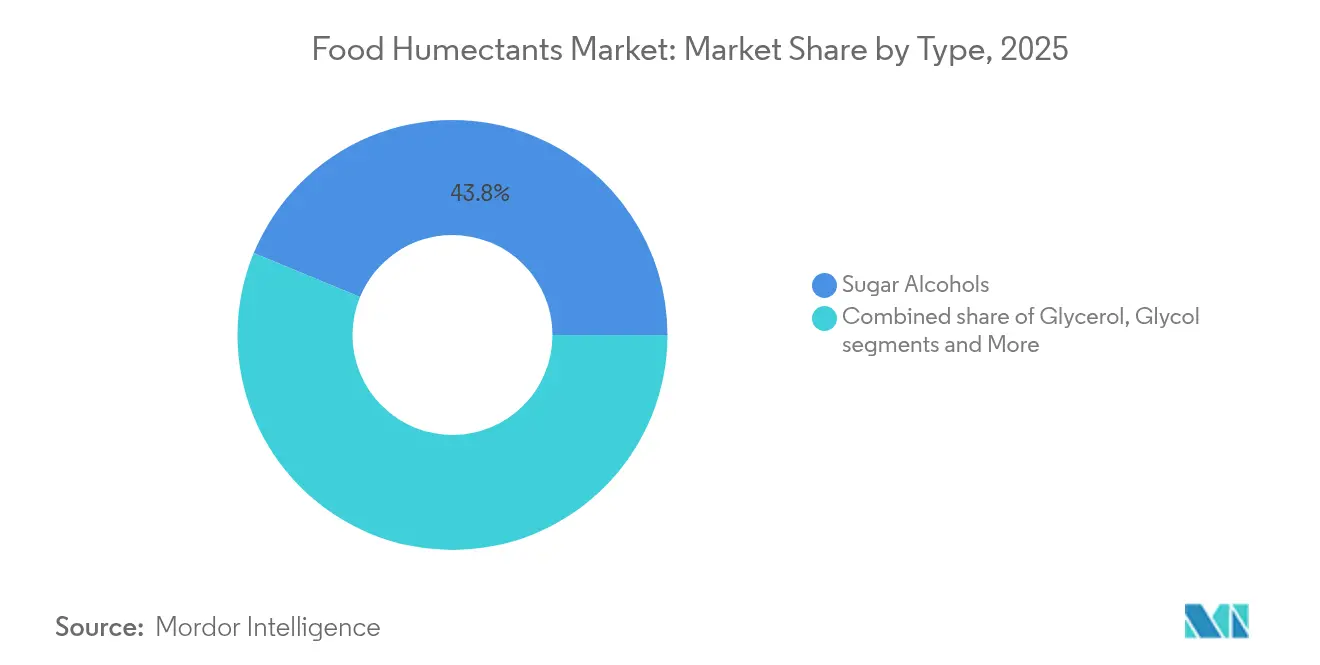

- By type, sugar alcohols led with 43.78% food humectants market share in 2025, while glycols are projected to expand at an 7.78% CAGR to 2031.

- By source, natural ingredients accounted for 70.83% of the food humectants market size in 2025 and are advancing at a 7.55% CAGR through 2031.

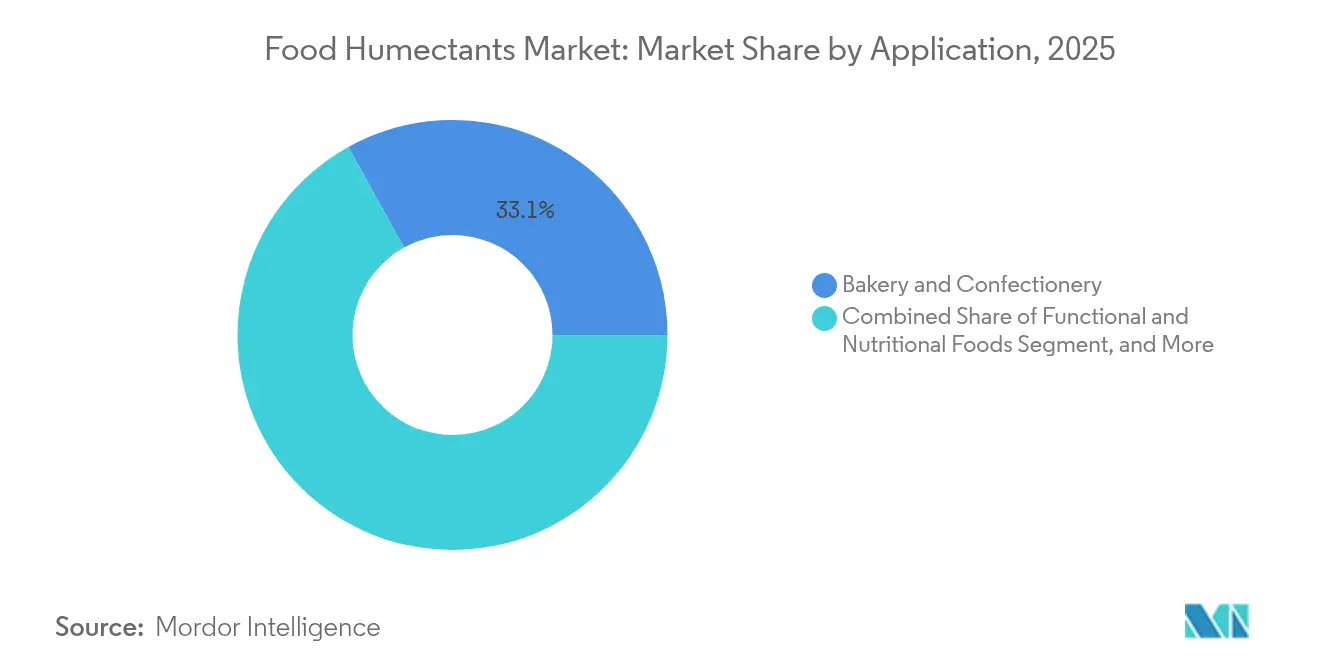

- By application, bakery and confectionery held 33.05% of the food humectants market share in 2025; savory and snacks is forecast to post the fastest 7.1% CAGR to 2031.

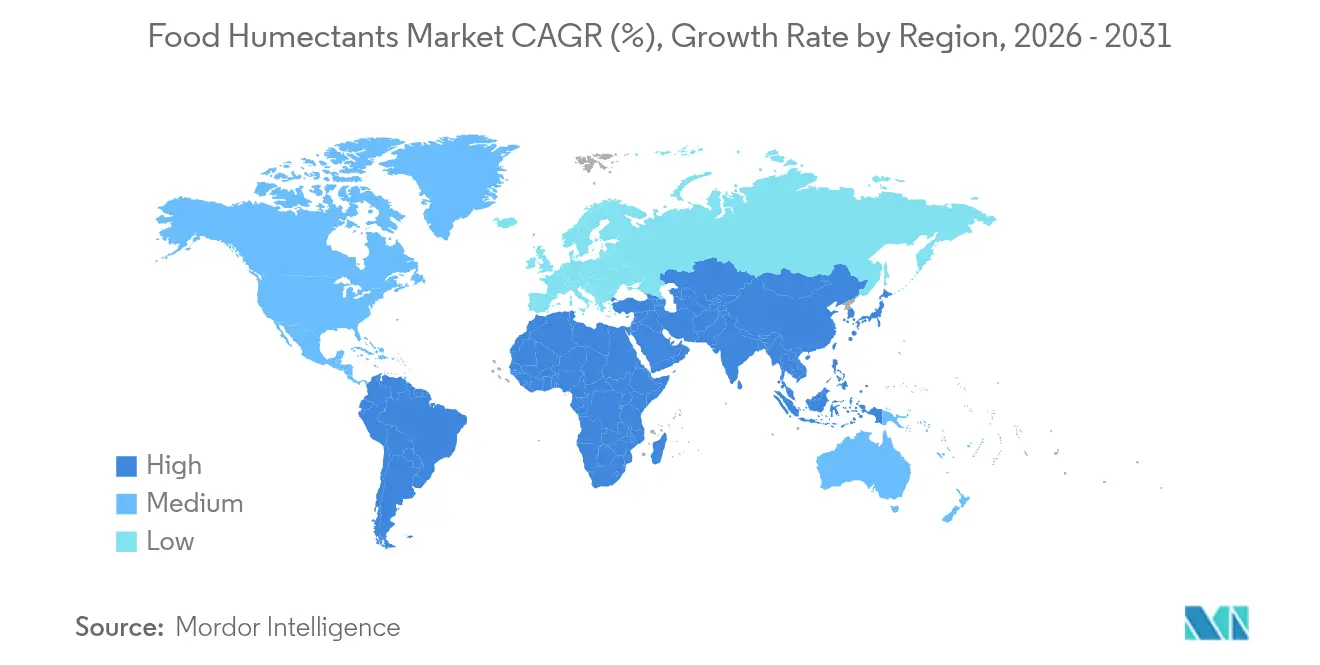

- By geography, Europe captured 32.48% of the food humectants market size in 2025, whereas Asia-Pacific is expected to grow at a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Humectants Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for moisture-retaining ingredients in bakery and confectionary | +1.8% | Global, with strong momentum in North America and Europe | Medium term (2-4 years) |

| Demand from frozen and refrigerated food categories | +1.2% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Use in low-sugar and sugar-free products | +1.0% | Global, led by developed markets | Short term (≤ 2 years) |

| Technology innovations in clean-label humectants | +0.9% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Growing adoption in plant-based dairy alternatives | +0.7% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Development of multi-functional humectants | +0.6% | Global, technology-driven markets first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for moisture-retaining ingredients in bakery and confectionary

The bakery and confectionery sector's transition toward extended shelf-life products is driving significant advancements in humectant selection and regulatory compliance. The FDA's classification of glycerin as Generally Recognized as Safe (GRAS) under 21 CFR 582.1320, when used in accordance with good manufacturing practices, provides manufacturers with a reliable regulatory framework[1]U.S. Food and Drug Administration, "Code of Federal Regulations", www.ecfr.gov. This clarity fosters innovation in moisture-retention solutions, which are critical for maintaining product quality and enhancing consumer satisfaction in bakery applications. Additionally, the Food and Agriculture Organization's Codex GSFA standards for glycerol (E422) establish internationally recognized guidelines, facilitating seamless global trade of bakery products containing humectants. To address evolving moisture management challenges across product lifecycles—from production to retail distribution—manufacturers are increasingly adopting advanced formulations that combine multiple humectants. These formulations are tailored to optimize moisture retention while ensuring product stability.

Demand from frozen and refrigerated food categories

Innovations in humectant technology and formulation strategies are being driven by the unique moisture management challenges posed by frozen food applications. In February 2025, a pilot plant jointly launched by Dow and Evonik, converting hydrogen peroxide to propylene glycol, marked a significant leap in sustainable humectant production. This method slashes water consumption by over 95% when stacked against conventional techniques. Such advancements cater to the frozen food sector's pressing demands: effective moisture retention and a commitment to environmental sustainability. Formulators are honing in on curbing ice crystal formation during freeze-thaw cycles. To uphold product integrity, they're turning to essential stabilizer combinations, notably starches and hydrocolloids. The surge in plant-based frozen alternatives adds layers of complexity. These alternatives exhibit moisture migration patterns that starkly contrast with their traditional animal-based counterparts, necessitating tailored humectant systems.

Use in low-sugar and sugar-free products

The growing emphasis on sugar reduction is driving significant changes in humectant selection, as manufacturers prioritize ingredients that deliver both sweetening and moisture-retention capabilities. Roquette's LYCASIN 80/55 maltitol syrup exemplifies this trend by functioning as a sugar-free sweetener and humectant while effectively preventing crystallization in confectionery applications. This development aligns with increasing consumer awareness of the health risks associated with high sugar consumption, with approximately two-thirds of consumers actively seeking to reduce their sugar intake. The innovation landscape is expanding beyond traditional sugar alcohols to include natural alternatives such as allulose and tagatose. These alternatives not only provide superior moisture retention but also align with clean-label demands, appealing to health-conscious consumers. Regulatory developments further support this shift, as the FDA's recognition of certain humectants as dietary fiber creates new marketing opportunities for manufacturers.

Technology innovations in clean-label humectants

Clean-label initiatives are propelling advancements in the extraction and processing of natural humectants, focusing on maintaining their functional properties while meeting stringent regulatory transparency standards. The FDA's comprehensive framework for food additives, as outlined in 21 CFR Part 172, provides clear regulatory pathways for the development of innovative humectant technologies that comply with safety and efficacy requirements[2]U.S. Food and Drug Administration, "Part 172—Food Additives Permitted For Direct Addition To Food For Human Consumption", www.ecfr.gov. This regulatory support encourages the adoption of novel extraction and processing methods that preserve the natural status of ingredients while enhancing their functionality. Recent research underscores the efficiency of non-thermal extraction technologies in obtaining natural humectants, ensuring the retention of their nutritional value and functional properties. Additionally, the integration of biotechnology, particularly through precision fermentation, enables the production of natural humectants with consistent quality and reliable supply chains, all while adhering to clean-label principles.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory restrictions om usage levels in food applications | -0.8% | Global, varying by jurisdiction | Short term (≤ 2 years) |

| Limited awarness in developing countries | -0.6% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Growing demand for preservative-free and natural products | -0.4% | North America and Europe primarily | Medium term (2-4 years) |

| Adultration risks in unregulated markets | -0.3% | Developing markets, unregulated regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory restrictions om usage levels in food applications

Major markets are tightening their regulatory frameworks, posing compliance challenges that limit humectant usage and complicate formulations. In February 2025, China rolled out its GB 2760-2024 standards, imposing stricter limits on food additives. These revisions not only set new usage requirements for humectants but also banned certain compounds in specific food categories. Reflecting heightened safety concerns, the FDA is consulting on contamination limits for ethylene glycol and diethylene glycol in food additives, a move that could influence humectant sourcing and processing[3]Food Compliance International, "CFSA officially implements the standard for the use of food additives (GB 2760-2024)", www.foodcomplianceinternational.com. Meanwhile, European regulations on mineral oil hydrocarbons in food add another layer of compliance challenges. The EU's guidelines targeting MOAH in foodstuffs have implications for both packaging and processing materials. Such regulatory pressures are inflating compliance costs and extending product development timelines. This is especially burdensome for smaller manufacturers who often lack extensive regulatory expertise.

Limited awarness in developing countries

In developing economies, the adoption of humectants in food processing faces significant challenges due to technical knowledge gaps and infrastructure limitations. According to the USDA's analysis of China's food processing ingredients market, the demand for imported food processing ingredients, including humectants, is increasing as consumers show a growing preference for healthier and premium food products. However, this growth is largely concentrated in developed urban areas, leaving rural and emerging markets with substantial knowledge deficits. Educational initiatives and training programs are primarily focused on developed regions, neglecting areas with rapidly expanding food processing industries. This lack of awareness is compounded by limited access to technical support and application expertise, which hampers innovation and the optimal utilization of humectants in these regions. Additionally, supply chain complexities in developing markets present further obstacles. Inconsistent quality standards and inadequate cold chain infrastructure negatively impact the stability and performance of humectants, creating significant barriers to their effective use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sugar Alcohols Maintain Leadership Through Regulatory Advantages

In 2025, sugar alcohols capture a 43.78% market share, bolstered by global regulatory endorsements and proven safety records. The FDA's designation of sorbitol as GRAS under 21 CFR Part 184 paves the way for its widespread use in food applications. Such regulatory backing empowers manufacturers to harness sugar alcohols across various applications, all while adhering to stringent food safety standards. The segment's stronghold is further solidified by the FAO's Codex GSFA standards, which set global benchmarks for sugar alcohols in food, promoting international trade and consistency. Beyond their roles as sweeteners, sugar alcohols serve as humectants, meeting manufacturers' demands for versatile ingredients that streamline formulations without compromising quality or compliance.

Glycols are set to be the fastest-growing segment, boasting an 7.78% CAGR through 2031, thanks to their enhanced performance in niche applications and a surge in regulatory endorsements. The FDA's oversight of propylene glycol mono- and diesters under 21 CFR 172.856 underscores the agency's acknowledgment of glycol-based humectants in targeted food uses. This regulatory nod fuels innovations in glycol formulations, tackling moisture management in frozen and processed foods. The segment is also reaping rewards from strides in sustainable production, notably the rise of bio-based propylene glycol via eco-friendly processing techniques. These advancements not only lessen environmental footprints but also uphold performance standards. Modern glycol formulations are now equipped with controlled-release features, ensuring moisture retention throughout a product's shelf life, effectively countering quality dips in less-than-ideal storage conditions.

By Source: Natural Sources Dominate Through Clean-Label Momentum

Natural sources hold a dominant 70.83% share of the market in 2025, driven by the growing consumer demand for recognizable and familiar ingredients, alongside regulatory frameworks that actively promote their adoption. The segment's growth is further supported by advancements in natural extraction technologies, which enhance ingredient functionality while preserving their integrity. These innovations allow natural sources to establish sustainable competitive advantages in markets that prioritize transparency, clean-label standards, and ingredient recognition. Additionally, the increasing focus on sustainability and environmental responsibility strengthens the appeal of natural sources, making them a preferred choice for both consumers and manufacturers.

Natural sources are projected to achieve the highest growth rate, with a strong 7.55% CAGR anticipated through 2031. This growth trajectory is driven by the rising consumer preference for clean-label products and significant advancements in the processing of natural ingredients. Biotechnology-driven production methods are leading the way, enabling the fermentation of nature-identical humectants that balance natural authenticity with consistent quality. Recent patent filings highlight innovative approaches in natural humectant production, emphasizing plant-based systems and the use of upcycled materials, which integrate sustainability with high performance. Advanced processing techniques are also leveraging agricultural waste to extract natural humectants, promoting sustainable supply chains and reducing environmental impact.

By Application: Bakery Leadership Supported by Regulatory Framework

Bakery and confectionery applications dominate the market with a 33.05% share in 2025, driven by comprehensive regulatory frameworks that promote the use of humectants in baked goods. Humectants play a critical role in preserving texture, extending shelf life, and preventing staleness in baked products. Tailored formulations are developed to address the specific requirements of various product categories and storage conditions. The industry's progression toward multifunctional ingredient solutions is evident in the integration of natural humectants with antimicrobial properties, which not only enhance moisture retention but also ensure food safety, meeting both consumer expectations and regulatory standards.

The savory and snacks segment is anticipated to be the fastest-growing application, with a strong CAGR of 7.1% through 2031. This growth is fueled by the increasing demand for innovative texture solutions and effective moisture management in shelf-stable products. Anderson Advanced Ingredients' MoisturLOK technology exemplifies the advancements in this segment, offering up to an 80% extension in shelf life while addressing moisture migration challenges in baked goods and snacks. The product's dual availability in powder and syrup forms underscores its versatility, catering to diverse manufacturing processes and highlighting the growing need for adaptable, high-performance solutions in the market.

Geography Analysis

In 2025, Europe holds a leading 32.48% market share, driven by its advanced food processing industries and stringent quality standards that promote humectant usage across a wide range of applications. The region's regulatory framework, particularly the implementation of Commission Regulation (EU) 2023/915, which sets maximum contaminant levels, creates a dual landscape of challenges and opportunities for humectant suppliers. Germany, the United Kingdom, and France dominate regional consumption, supported by their sophisticated bakery industries and increasing demand for clean-label ingredients. Europe's strong focus on sustainability aligns with the growing preference for natural humectants, while its well-established supply chains ensure consistent product availability and quality.

Asia-Pacific is positioned as the fastest-growing region, with a projected CAGR of 7.42% through 2031. This growth is fueled by rapid industrialization in food processing and changing dietary habits that favor convenience foods. Meanwhile, India and Southeast Asia drive volume growth through rising consumption of processed foods, while Australia and South Korea contribute with their adoption of advanced food technologies. The region's diverse regulatory environment necessitates tailored strategies, prompting companies to establish local partnerships and production facilities to address specific market demands effectively.

North America maintains a strong market presence, supported by its leadership in innovation and a well-established food processing infrastructure that enables advanced humectant applications. The region benefits from the FDA's comprehensive regulatory framework, including the GRAS designation for key humectants under 21 CFR Part 184, which facilitates streamlined product development and market entry. Mexico's expanding food processing industry and Canada's focus on natural ingredients further contribute to the region's growth dynamics. In contrast, South America and the Middle East & Africa represent emerging opportunities. In South America, Brazil and Argentina lead the expansion, driven by their growing food processing capabilities. Simultaneously, the Middle East's emphasis on food security and Africa's rapidly urbanizing population are increasing the demand for shelf-stable products, underscoring the critical role of effective moisture management systems in these regions.

Competitive Landscape

The global food humectants market is moderately concentrated, with prominent players such as BASF SE, Ingredion Incorporated, Archer Daniels Midland Company, Cargill Incorporated, and Roquette Frères SA leading the market. These key players, along with other domestic and international companies, are actively focusing on innovation and launching new products to address the growing consumer demand for advanced food humectants while maintaining their competitive edge in the market. The market is witnessing a steady rise in demand, driven by the increasing use of humectants in processed foods, bakery products, and confectionery to enhance texture, moisture retention, and shelf life.

Strategic consolidation activities are significantly reshaping the competitive landscape of the market. For instance, in March 2025, Louis Dreyfus Company acquired BASF's food and health performance ingredients business. This acquisition has strengthened Louis Dreyfus Company's capabilities in ingredient sourcing and distribution, highlighting the industry's increasing emphasis on vertical integration and supply chain optimization. Such strategies are crucial to meeting the rising demand for specialized humectant solutions, which are becoming essential in various food applications. Additionally, the consolidation trend reflects the growing need for companies to streamline operations and enhance their global footprint in a competitive market environment.

Innovation remains a key driver in the market, with companies focusing on clean-label technologies and multi-functional ingredients to align with evolving consumer preferences and stringent regulatory requirements. Furthermore, the rising consumer inclination toward plant-based and organic products is pushing companies to invest in research and development for eco-friendly and health-conscious solutions.

Food Humectants Industry Leaders

-

BASF SE

-

Ingredion Incorporated

-

Archer Daniels Midland Company

-

Cargill Incorporated

-

Roquette Frères SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nexus Ingredient has expanded its product portfolio with the launch of MoistPlus is an innovative allulose-based humectant that outperforms standard allulose by providing superior moisture retention, improved texture, and extended shelf life in food products without adding significant calories or sugar.

- March 2025: Louis Dreyfus Company acquired BASF's food and health performance ingredients business, bolstering its ingredient sourcing and distribution capabilities. This move not only solidifies the company's foothold in specialty food ingredients but also broadens its global presence in humectant supply chains.

- June 2024: Univar Solutions broadened its distribution alliance with Ingredion, now covering Germany, Italy, and Switzerland, with an emphasis on functional ingredients for food and beverages. This partnership boosts the availability of specialty components, such as modified starches and natural sweeteners.

- March 2024: China rolled out the GB 2760-2024 standard for food additives, tightening usage criteria and redefining several humectants. These updated regulations mandate changes in product formulations and compliance measures throughout the food processing sector.

Global Food Humectants Market Report Scope

Humectants are hygroscopic substances. They bind the moisture that is contained in the food and, in addition, absorb moisture from the air and control the moisture. The Global Food Humectants Market is segmented by type into sugar alcohol, phosphate, glycerol, glycol, lactate, and others. By application market is segmented into bakery & confectionery, functional & nutritional foods, beverages, dairy products, and others. By source market is segmented into natural and synthetic. By geography market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Sugar Alcohol |

| Glycerol |

| Glycol |

| Lactate |

| Others |

| Natural |

| Synthetic |

| Bakery and Confectionery |

| Functional and Nutritional Foods |

| Beverage |

| Dairy and Frozen Desserts |

| Savory and Snacks |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Sugar Alcohol | |

| Glycerol | ||

| Glycol | ||

| Lactate | ||

| Others | ||

| By Source | Natural | |

| Synthetic | ||

| By Application | Bakery and Confectionery | |

| Functional and Nutritional Foods | ||

| Beverage | ||

| Dairy and Frozen Desserts | ||

| Savory and Snacks | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the food humectants market?

The food humectants market size is valued at USD 5.41 billion in 2026 and is projected to reach USD 7.45 billion by 2031.

Which segment holds the largest food humectants market share?

Sugar alcohols lead by type with 43.78% market share in 2025, and bakery and confectionery dominate by application with 33.05%.

Which region is growing fastest in the food humectants market?

Asia-Pacific is the fastest-growing region, forecast to expand at a 7.42% CAGR through 2031.

Why are natural humectants gaining traction?

Natural sources command 70.83% of the market due to clean-label demand, GRAS approvals, and advances in fermentation that boost supply and functionality.

Page last updated on: