Sugar Decorations And Inclusions Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

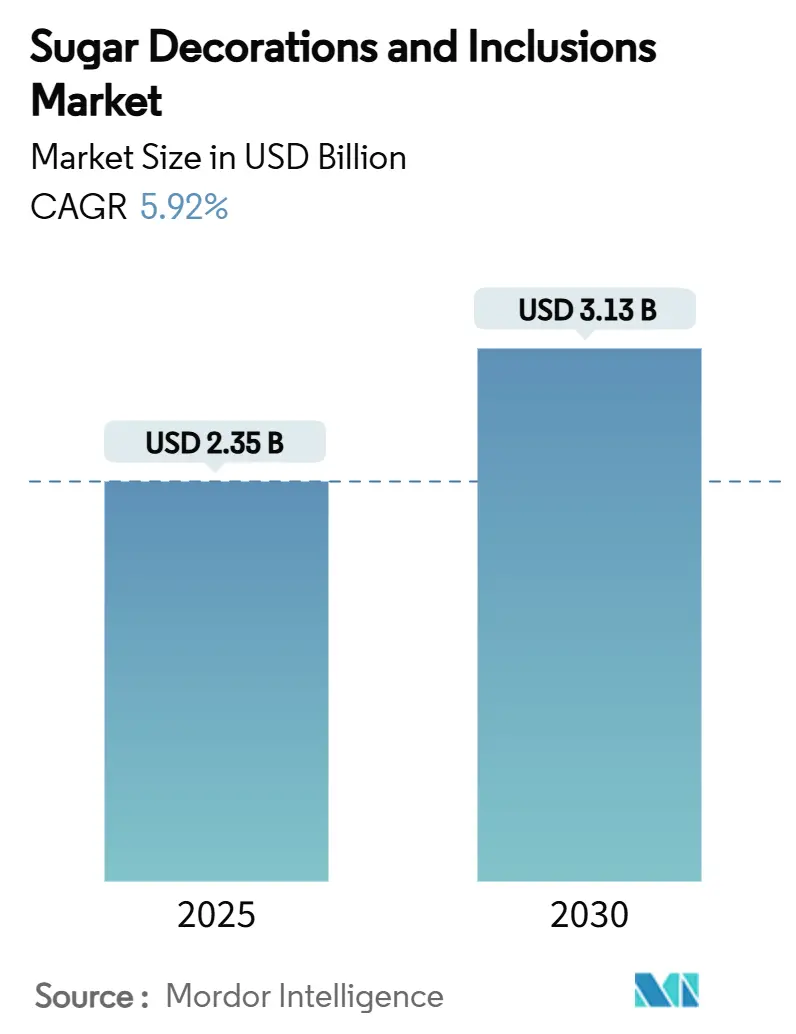

| Market Size (2025) | USD 2.35 Billion |

| Market Size (2030) | USD 3.13 Billion |

| Growth Rate (2025 - 2030) | 5.92% CAGR |

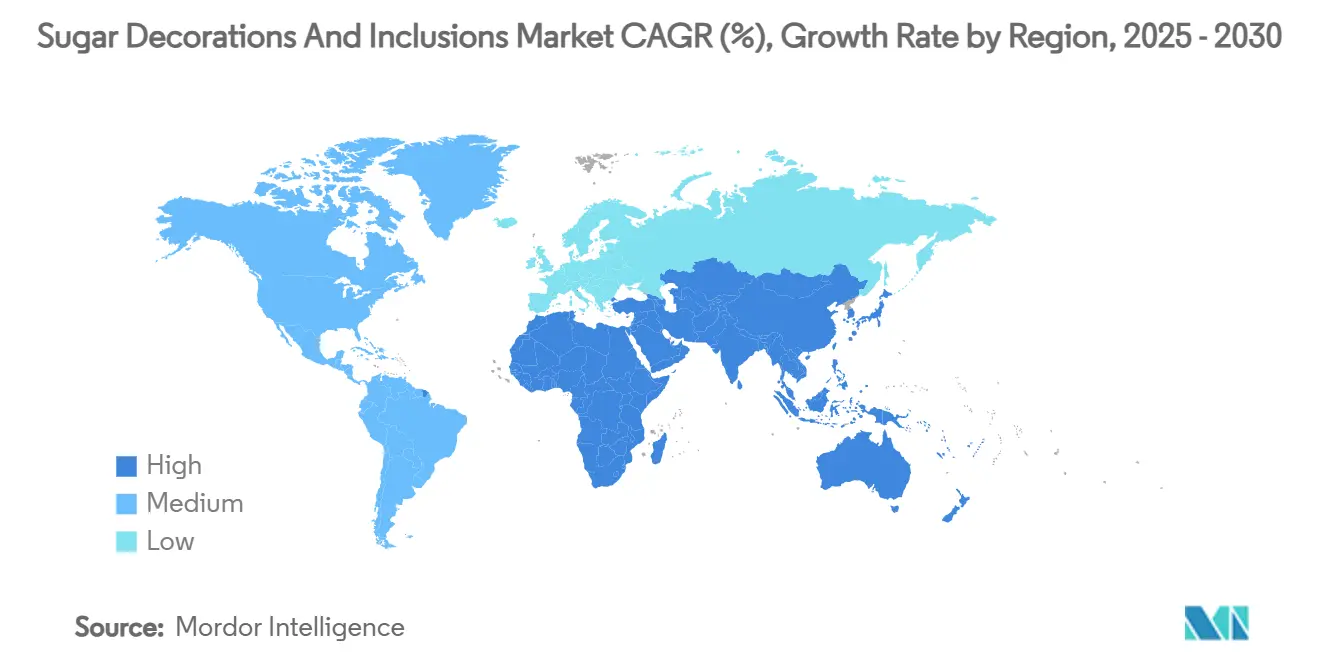

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sugar Decorations And Inclusions Market Analysis by Mordor Intelligence

The sugar decorations and inclusions market size is estimated to be USD 2.35 billion in 2025, and it is forecast to advance at a 5.92% CAGR to reach USD 3.13 billion by 2030. The demand for sugar decorations and inclusions has increased due to social media platforms, particularly Instagram and TikTok. These platforms showcase elaborate cake designs, edible glitter, shaped sprinkles, and colorful toppings, influencing both home bakers and professionals to focus on presentation. The transformation of desserts into social media content has elevated consumer expectations for decorated treats in bakeries and cafés. Europe keeps the lead through strong baking traditions and strict quality rules, while Asia-Pacific records the most dynamic gains on the back of rising incomes and modern retail expansion. Moreover, natural color adoption accelerates as regulators push synthetic dye withdrawal and consumers favor clean labels. Industrial manufacturers remain the largest demand pool, yet commercial bakeries and pastry shops capture the fastest revenue lift as premium craft offerings multiply.

Key Report Takeaways

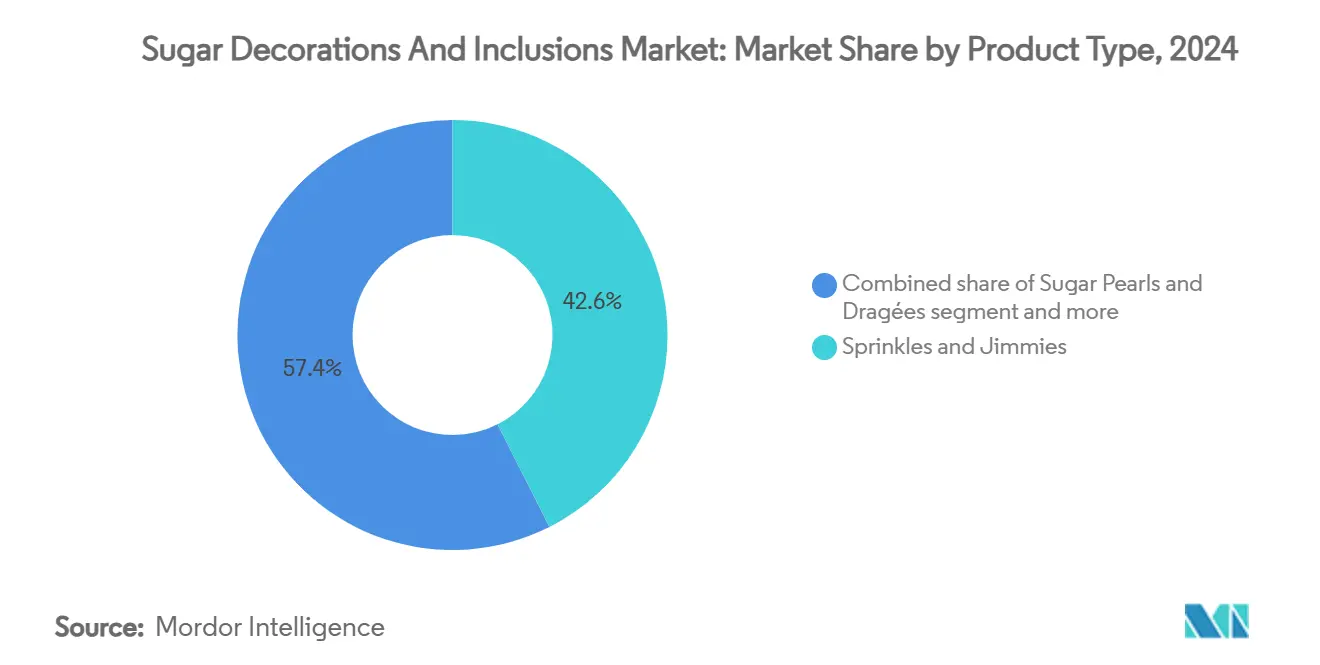

- By product type, sprinkles and jimmies held 42.56% of the sugar decorations and inclusions market share in 2024, whereas functional or reduced-sugar decorations are projected to post a 6.31% CAGR through 2030.

- By form, solid particulates accounted for 67.18% of the sugar decorations and inclusionsmarket size in 2024, and semi-liquid inclusions are anticipated to grow at a 7.69% CAGR by 2030.

- By colorant source, artificial colors led with 61.35% share in 2024; natural colors remain the fastest-expanding group at a 7.25% CAGR to 2030.

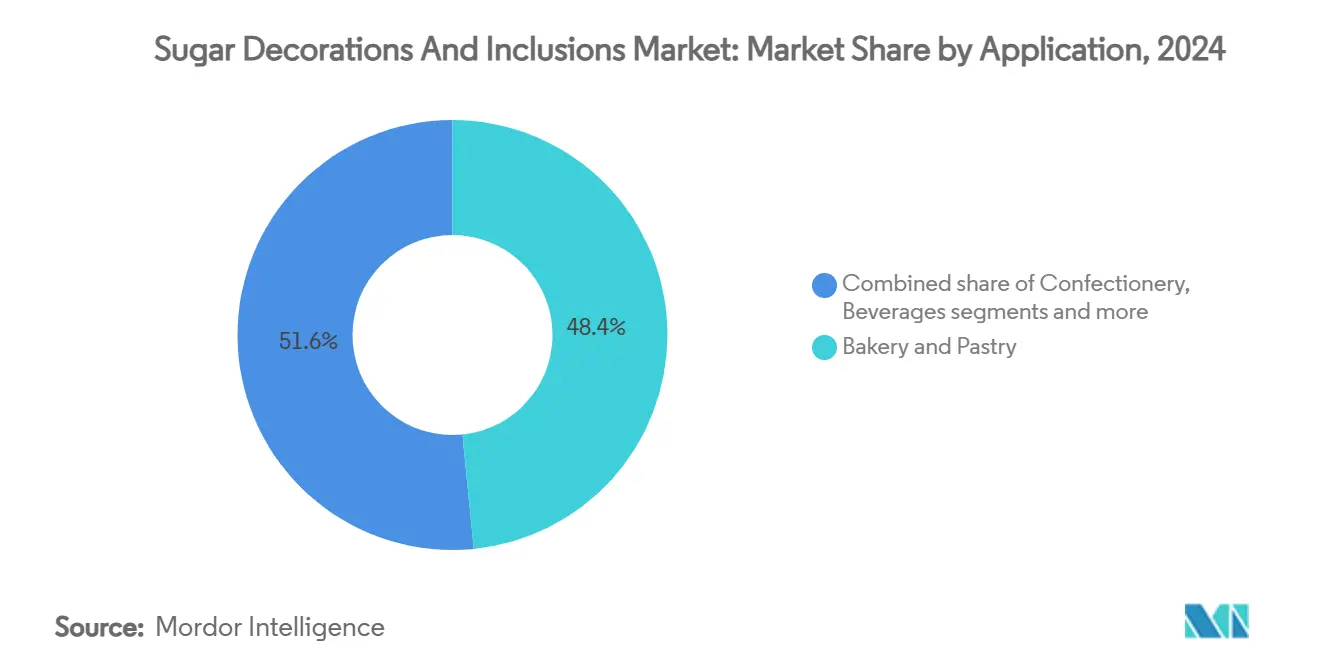

- By application, bakery and pastry dominated with 48.42% share in 2024, while dairy and frozen desserts are on track for a 6.67% CAGR during 2025-2030.

- By end user, industrial food manufacturers captured 54.27% of 2024 revenue, and commercial bakeries and pastry shops are forecast to register a 6.90% CAGR up to 2030.

- By geography, Europe contributed 34.67% of global revenue in 2024, whereas Asia-Pacific is expected to post a 6.08% CAGR through 2030.

Global Sugar Decorations And Inclusions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of bakery and dessert aesthetics | +1.2% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Social-media driven "Instagrammable" desserts | +0.8% | Global, led by Asia-Pacific urban centers | Short term (≤ 2 years) |

| Introduction of health-oriented innovations | +0.9% | North America and European Union regulatory focus, Asia-Pacific adoption | Long term (≥ 4 years) |

| Growth of home baking and DIY culture | +0.7% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising demand for customized/festive offerings | +0.6% | Global, seasonal peaks in all regions | Short term (≤ 2 years) |

| Advancements in food decoration technology | +0.5% | Industrial hubs in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization of bakery and dessert aesthetics

Consumer demand for sophisticated and unique bakery aesthetics is driving innovation in the sugar decorations and inclusions market. Companies like McCormick & Company are capitalizing on this trend, exemplified by their 2024 launch of "Holiday Finishing Sugars" in six festive flavors, which taps into seasonal premiumization. Also, advancements in decoration technologies, such as AI-enhanced design tools and precision application systems, enable mass customization while maintaining artisanal quality. These innovations allow producers to meet the growing demand for intricate, themed, and personalized decorations, particularly for high-end, Instagram-worthy bakery products. The integration of natural colorants and clean-label ingredients further appeals to health-conscious consumers seeking premium and transparent offerings. Besides, influenced by baking shows and social media, consumers increasingly favor elaborate and artistic cake designs, prompting continuous product innovation. Brands leveraging advanced decoration technologies and focusing on customized, festive concepts are well-positioned to gain a competitive edge in a market poised for robust growth. This evolution elevates bakery decoration from a secondary detail to a key factor in consumer decision-making.

Social-media driven “Instagrammable” desserts

Social media giants TikTok and Instagram have significantly influenced consumer behavior, driving demand for visually captivating, "Instagrammable" desserts that shape purchasing decisions. As Gen Z and Millennials embrace the "little treat culture," there is a rising preference for mini desserts and intricate sugar designs that photograph well under various lighting conditions. This trend has compelled manufacturers to innovate, resulting in advanced sugar decorations and inclusions featuring color-changing and thermochromic effects that enhance digital shareability. The National Confectioners Association reported a 12.1% growth in non-chocolate candy sales, with freeze-dried candy leading the segment, reflecting youth-driven preferences shaped by social media [1]Source: National Confectioners Association, "State of Treating 2024", candyusa.com. Industry leaders such as Wilton and CK Products are heavily investing in packaging and presentation to optimize the "unboxing experience," encouraging consumers to share their dessert creations online. Additionally, advancements in 3D printing and AI-driven designs enable producers to deliver customized, detailed decorations that align with social media aesthetics. This combination of evolving consumer demand, technological innovation, and media influence is reshaping product development cycles and driving sustained growth, where visual appeal plays a critical role in market differentiation and premiumization.

Introduction of health-oriented innovations

Health-oriented innovations are reshaping the industry by addressing the growing demand from health-conscious consumers and regulatory compliance. Sugaright is at the forefront with its L350 RBU liquid sucrose, a dual-purpose solution functioning as both a sweetener and colorant, offering a clean-label alternative to synthetic dyes. Also, startups like Michroma and Chromologics are introducing fermentation-derived pigments with superior stability and coloring strength compared to traditional plant-based options, enabling manufacturers to maintain visual appeal while meeting clean-label requirements. Regulatory measures, such as the EU's restrictions on sugar-rich products and the FDA's phase-out of synthetic dyes, are accelerating the shift toward healthier decoration alternatives. In 2023, Puratos, a leading global bakery ingredient supplier, achieved a 2% sugar reduction across its product portfolio, with 32% of sales stemming from health-focused products [2]Source: Puratos Group, "2023 Puratos Sustainability Report", puratos.com. This underscores the commercial viability and increasing consumer acceptance of these innovations. These developments align with broader industry trends emphasizing reduced-sugar, low-calorie, and natural ingredient formulations, driven by heightened awareness of sugar's health impacts, including obesity and diabetes. By adopting these innovations, the sugar decorations and inclusions sector enhances product differentiation and premiumization, focusing on both visual appeal and health attributes. Ultimately, these health-driven advancements are expanding market segments by introducing functional and reduced-sugar decoration alternatives, addressing evolving consumer preferences, sustainability objectives, and regulatory demands, thereby strengthening growth opportunities in the global market.

Growth of home baking and DIY culture

The rise in home baking and DIY culture influences the demand for sugar decorations and inclusions. Consumers increasingly seek decorative, easy-to-use, and visually appealing products for their home baking activities. Social media influence and digital sharing platforms have transformed home baking into a popular creative and wellness activity, increasing demand for premium and customizable sugar decorations. The market expansion is supported by the widespread availability of baking kits and ingredients through online channels, enabling novice bakers to create professional-looking desserts. Companies such as Wilton and CK Products capitalize on this trend by offering innovative products that align with clean-label preferences. The growth of home-based baking businesses and seasonal baking activities contributes to increased sales of specialized sugar decorations. The home baking ingredients segment shows strong growth potential, indicating sustained consumer interest. The trend has also influenced bakeware development, with new materials and designs complementing sugar decoration applications and supporting premium home baking aesthetics. The DIY culture continues to expand the market by combining artisan-quality decorations with accessibility and personalization, addressing consumer demands for creative expression and enhanced food experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price fluctuations | -1.1% | Global, acute in sugar-dependent regions | Short term (≤ 2 years) |

| Stringent food safety regulations | -0.8% | North America and European Union compliance costs, Asia-Pacific adaptation | Medium term (2-4 years) |

| Cross-contamination recalls linked to allergen traces in sprinkle plants | -0.6% | Global, stricter enforcement in developed markets | Medium term (2-4 years) |

| Shelf-life and storage challenges | -0.4% | Global, more critical in humid climates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw material price fluctuations

Raw material price fluctuations, particularly sugar as a primary input, create operational challenges for manufacturers in the sugar decorations and inclusions market. According to the USDA, global sugar production decreased from 194.22 million metric tons in 2017/2018 to 183.5 million metric tons in 2023/2024, indicating supply tightening [3]Source: United States Department of Agriculture (USDA), "USDA - Sugar: World Markets and Trade (May 2024)", usda.gov. This reduced production volume creates upward pressure on sugar prices, impacting the cost structures of sugar decoration manufacturers who depend on sugar, starches, and natural/artificial colorants. Also, market reports indicate that despite strong demand, fluctuating raw material costs limit profit margins and create product pricing volatility. In the U.S., sugar prices are expected to remain at approximately 38.4 cents per pound in 2025, maintaining a stable but elevated level following earlier volatility from supply chain disruptions and inflationary pressures. Industry participants, including major bakery ingredient suppliers and sugar decoration manufacturers, must carefully manage these cost fluctuations to remain competitive. Supply chain uncertainties and geopolitical factors increase complexity, requiring adaptable procurement and pricing strategies. Despite strong consumer demand for premium, innovative, and health-conscious sugar decorations, these challenges affect market growth. Hence, raw material price volatility continues as a significant non-economic restraint in the sugar decorations and inclusions market, requiring industry collaboration and innovation in raw material sourcing and product formulation.

Stringent food safety regulations

Food safety regulations are creating compliance costs and operational challenges for manufacturers of sugar-based cake decorations and confectionery inclusions. The FDA's ban on synthetic dyes, including Red No. 3, effective January 15, 2027, requires manufacturers to reformulate products and adjust supply chains. State regulations in California, West Virginia, and Virginia further restrict synthetic additives, particularly in school food services, creating a complex regulatory environment. These regulations heighten the focus on allergen cross-contamination in sprinkle and decoration production, requiring increased testing and separate manufacturing lines. While natural colorants align with consumer preferences for clean labels, they present technical challenges in matching the vibrancy, stability, and cost-effectiveness of synthetic alternatives. The regulatory landscape for new ingredients and processing technologies, including fermentation-derived pigments from companies like Michroma and Chromologics, creates additional compliance considerations. Companies like Sugaright and Puratos are adapting to these standards through product reformulation and enhanced quality control measures. These food safety policies impact innovation, costs, and product development in the sugar decorations and inclusions market, making regulatory compliance essential for market growth and consumer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Innovations Drive Diversification

The sprinkles and jimmies segment accounts for 42.56% of the market share in 2024. Their widespread use across cakes, pastries, ice creams, and confectionery products makes them essential for both commercial and home baking applications. Major manufacturers such as Wilton, First Street, and Mariano's maintain market dominance through product innovations in shapes, colors, and formulations. The popularity of these traditional decorations remains strong, supported by social media trends that emphasize visually attractive desserts, even as new decoration categories enter the market.

Meanwhile, the functional and reduced-sugar decorations segment is growing at a CAGR of 6.31% through 2030, driven by increasing health-conscious consumption patterns and stricter regulations on sugar and synthetic additives. Companies like Sugaright and Puratos are developing clean-label products with natural colorants and reduced sugar content to meet new regulatory requirements. Traditional decorations such as sugar crystals, sanding sugars, pearls, and dragées continue to serve premium bakery and celebration markets. Furthermore, shaped sugar toppings gain popularity through social media-driven customization trends. The market expansion of flavored sugar inclusions combines visual appeal with enhanced taste, creating premium product opportunities.

By Form: Semi-Liquid Innovations Challenge Traditional Formats

The solid particulates segment accounts for a 67.18% share of the sugar decorations and inclusions market revenue in 2024. This dominance stems from their practical benefits, including easy handling, extended shelf life, and compatibility with existing production equipment. Sugar crystals, sanding sugars, and sprinkles are widely used in bakery, confectionery, and dessert manufacturing, providing consistent texture and visual enhancement. The extended shelf stability of solid particulates benefits manufacturers and retailers through simplified inventory management. These traditional decoration formats maintain steady consumer demand, aligning with established preferences in the market.

Semi-liquid inclusions, such as icing bits and fudge components, are growing at a CAGR of 7.69%, making them the fastest-growing segment in the market. These inclusions enable bakers and product developers to create desserts with multiple textures and enhanced flavors, meeting consumer demand for unique treats. Companies like Puratos are expanding their semi-liquid inclusion offerings to address the market need for texture variety. Moreover, powdered and dusting sugars serve primarily professional and artisanal bakers who require precise application for detailed decorative work on pastries and cakes. The growth in semi-liquid inclusions, alongside the established solid particulates segment, indicates market diversification through both innovative and traditional product formats.

By Colorant Source: Natural Transition Accelerates

Artificial colors hold a 61.35% market share in sugar decorations and inclusions in 2024. However, regulatory changes and consumer preferences are shifting the market dynamics. The FDA's initiative to eliminate petroleum-based synthetic dyes by the end of 2026 requires manufacturers to transition to natural colorants. This regulatory change, combined with increasing consumer demand for clean-label products, drives the natural color segment's growth at a 7.25% CAGR. Natural colorants require higher quantities and specific handling procedures to achieve the intensity and stability of synthetic dyes, creating operational and cost challenges for manufacturers.

The sugar decorations and inclusions industry is experiencing advancements in fermentation-derived pigments that address the limitations of traditional plant-based colorants. Companies like Michroma and Chromologics have developed fermentation-based red pigments that offer improved stability and color intensity, helping products maintain their appearance for longer periods. The FDA's approval of natural color additives from algae and flowers has expanded the available options for sugar decoration manufacturers. California Natural Color has introduced crystal color formats using red radish and spirulina, which provide concentrated pigmentation and improved shelf stability. These biotechnology advancements are transforming production processes and supply chains while meeting market demands for sustainable, health-focused, and compliant sugar decorations and inclusions.

By Application: Dairy Segment Drives Growth Diversification

The bakery and pastry segment accounts for 48.42% of the sugar decorations and inclusions market value in 2024. The segment's dominance is attributed to established distribution networks across professional bakeries and home baking channels. Bakeries and pastry manufacturers use sugar decorations, including sprinkles, sanding sugars, and jimmies, to enhance product appearance and consumer appeal. Companies like Wilton, Cake Craft, and Barry Callebaut maintain strong market positions by offering diverse decoration solutions for bakery applications. The segment's growth is supported by social media trends and consumer demand for customized, visually appealing baked goods.

The dairy and frozen desserts segment leads market growth with a 6.67% CAGR, driven by product innovation in ice cream, yogurt, and frozen treats. Temperature-stable sugar decorations and cold-chain compatible formulations enable manufacturers to create durable visual embellishments that withstand freezing and thawing cycles. Companies such as Puratos and Cargill have developed stable inclusions to address the increasing demand for premium desserts. The beverage segment presents new opportunities, with sugar decorations being used as cocktail garnishes and drink toppers. The confectionery and cereals/snack bars segments continue to grow as manufacturers use decorative inclusions to enhance product appeal in competitive markets. The market demonstrates consistent expansion across multiple product categories.

By End User: Commercial Bakeries Lead Growth Acceleration

Industrial food manufacturers command 54.27% of the sugar decorations and inclusions business in 2024. These manufacturers utilize economies of scale and standardized production processes to serve mass-market bakery, confectionery, and snack producers. Their optimized procurement and quality control systems enable consistent product delivery. The industrial segment maintains extensive portfolios of sugar decorations that fulfill functional and aesthetic requirements at competitive prices. While their focus on standardized formulations and high-volume production sustains their market dominance, increasing demand for premium and customized products is influencing their product development strategies.

The sugar decorations and inclusions market shows commercial bakeries and pastry shops as the fastest-growing segment, with a projected CAGR of 6.90% through 2030. This growth is driven by increasing consumer demand for premium, artisanal, and customized products. Equipment manufacturers like Unifiller provide decoration systems that enable commercial bakeries to produce high-quality products efficiently, with the capability of decorating up to 12 cakes per minute. The HoReCa and foodservice sector focuses on visually appealing presentations to increase customer engagement, while the household/DIY segment maintains steady growth through home baking activities. The market's expansion is supported by adaptable manufacturing systems and continuous product development, enabling sugar decorations and inclusions manufacturers to meet diverse consumer preferences.

Geography Analysis

Europe accounts for 34.67% of the sugar decorations and inclusions market in 2024, supported by its established bakery traditions and quality standards. The region's market features high per-capita consumption and consumer preferences for premium and artisanal products. Germany, the United Kingdom, and France represent significant markets, driven by their pastry heritage and robust distribution networks. Besides, European regulatory frameworks ensure product safety and quality, fostering consumer confidence and product development in natural colorants and healthier alternatives. Companies like Puratos and Bakels Group have developed decoration portfolios aligned with regional preferences and regulations, reinforcing Europe's market position.

The Asia-Pacific region is projected to grow at a CAGR of 6.08% through 2030, driven by urbanization, changing consumer preferences, and increasing demand for Western bakery and confectionery products. China represents a key market, with sugar confectionery growth supported by cultural festivals and seasonal demand. E-commerce platforms Tmall and JD.com have expanded retail accessibility in urban areas, increasing the availability of specialty sugar decorations among younger consumers. In India and Indonesia, health-conscious consumer preferences are influencing the market, particularly for low-sugar, natural, and functional decorative products. Barry Callebaut's growth in these emerging markets, despite supply chain challenges, demonstrates the region's market potential and increasing consumer acceptance of premium sugar decorations.

North America represents a mature and stable market for sugar decorations, with significant focus on natural colorants and health-conscious products. The region's stringent food safety regulations and regulatory initiatives have established it as a pioneer in clean-label products and the reduction of synthetic dyes, which influences product development across regions. Consumer awareness regarding ingredient transparency and sustainability has increased demand for premium, natural, and organic decorative alternatives. The Mexican market shows growth potential through its expanding middle class and integration with North American supply chains. Furthermore, Canada's strict organic certification requirements drive demand for high-quality, environmentally responsible sugar decorations. Companies like Sugaright and Michroma leverage North America's position in health and sustainability trends, contributing to market expansion.

Competitive Landscape

The market structure remains moderately consolidated, with major multinational companies maintaining dominant positions while new entrants target specific market segments. Companies like Barry Callebaut, Dr. Oetker, and Werner GmbH & Co. KG maintain strong market positions through vertical integration, from raw sugar sourcing to finished decoration manufacturing. Their established global distribution networks and diverse product portfolios provide market stability and protection against raw material price fluctuations. New market entrants such as Sugaright, Michroma, and Chromologics focus on specialized segments, developing natural colorants, fermentation-derived pigments, and functional decorations that align with consumer preferences for clean-label and reduced-sugar products.

Market participants expand their presence through horizontal acquisitions and strategic partnerships. Barry Callebaut's targeted acquisitions have strengthened its confectionery ingredients and decoration offerings, enabling innovation across product categories. Companies implement vertical integration to secure sustainable raw material supplies and manage sugar price volatility and regulatory requirements. Industry players partner with technology providers to implement automation, AI-based design systems, and precision application equipment. For example, Unifiller's decoration equipment enables commercial bakeries to achieve high-speed production while maintaining artisanal quality, demonstrating the industry's shift toward technology-enabled manufacturing.

Technology and innovation remain critical competitive factors in the market. Emerging opportunities include biotechnology-based fermentation-derived colorants, supported by FDA patent developments in natural pigment extraction and stability enhancement. AI and 3D printing enable personalized decoration solutions, supporting product differentiation and premium pricing strategies. Environmental considerations drive sustainable packaging development, creating opportunities for market differentiation while maintaining product quality and shelf life. Companies that implement these technological advancements position themselves for market share growth in an industry where health considerations, visual appeal, and sustainability intersect.

Sugar Decorations And Inclusions Industry Leaders

-

Barry Callebaut AG

-

Dr. August Oetker KG

-

Hanns G. Werner GmbH & Co. KG

-

Omnia Ingredients GmbH & Co. KG

-

Orkla ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Mix, a prominent company in the confectionery market, launched 39 new products across its portfolio, strengthening its position in the Brazilian confectionery industry. The company introduced 65 products to the market in recent months. The latest 39 SKUs spanned nine product categories: powdered chocolate, homemade ice cream, toppings and fillings, creams, oven-friendly fillings, fat-soluble flavors, sugars, flake toppings, and confectionery supplements.

- October 2024: Dr. Oetker implemented an expansion of its seasonal 'The Taste of Christmas' range through the introduction of three decorative products. The portfolio incorporated Rudolph Mix, Sugar Decorations, and glitter sugar writing for application on cakes, pastries, and desserts. The products demonstrated efficient application methods for festive decoration requirements.

- September 2024: McCormick introduced six limited-edition Holiday Finishing Sugars. The collection comprised Candy Cane, English Toffee, Salted Caramel, Hot Cocoa, Gingerbread Spice, and White Frosting flavors, designed for baking, decorating, and beverage garnishing applications.

Global Sugar Decorations And Inclusions Market Report Scope

| Sprinkles and Jimmies |

| Sugar Crystals and Sanding Sugars |

| Sugar Pearls and Dragées |

| Shaped Sugar Toppings |

| Flavored Sugar Inclusions |

| Functional/Reduced-Sugar Decorations |

| Solid Particulates |

| Semi-Liquid Inclusions (icing bits, fudge) |

| Powdered/Dusting Sugars |

| Artificial Colors |

| Natural Colors |

| Bakery and Pastry |

| Confectionery |

| Dairy and Frozen Desserts |

| Cereals and Snack Bars |

| Beverages |

| Others (e.g., Edible Cutlery) |

| Industrial Food Manufacturers |

| Commercial Bakeries and Pastry Shops |

| HoReCa/Foodservice |

| Household/DIY |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Sprinkles and Jimmies | |

| Sugar Crystals and Sanding Sugars | ||

| Sugar Pearls and Dragées | ||

| Shaped Sugar Toppings | ||

| Flavored Sugar Inclusions | ||

| Functional/Reduced-Sugar Decorations | ||

| By Form | Solid Particulates | |

| Semi-Liquid Inclusions (icing bits, fudge) | ||

| Powdered/Dusting Sugars | ||

| By Colorant Source | Artificial Colors | |

| Natural Colors | ||

| By Application | Bakery and Pastry | |

| Confectionery | ||

| Dairy and Frozen Desserts | ||

| Cereals and Snack Bars | ||

| Beverages | ||

| Others (e.g., Edible Cutlery) | ||

| By End User | Industrial Food Manufacturers | |

| Commercial Bakeries and Pastry Shops | ||

| HoReCa/Foodservice | ||

| Household/DIY | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the sugar decorations and inclusions market in 2025?

The sugar decorations and inclusions market size is USD 2.35 billion in 2025 and is projected to reach USD 3.13 billion by 2030.

Which region is growing fastest for sugar decorations and inclusions?

Asia-Pacific posts the highest forecast growth at a 6.08% CAGR, driven by urbanization and rising disposable incomes.

What product segment leads revenue?

Sprinkles and jimmies generate the largest share at 42.56% in 2024.

Which colorant category is expanding quickest?

Natural colors hold the fastest trajectory, advancing at a 7.25% CAGR as regulations limit synthetics.

Page last updated on: