Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 27.88 Billion |

| Market Size (2031) | USD 35.17 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Flavors And Enhancers Market Analysis by Mordor Intelligence

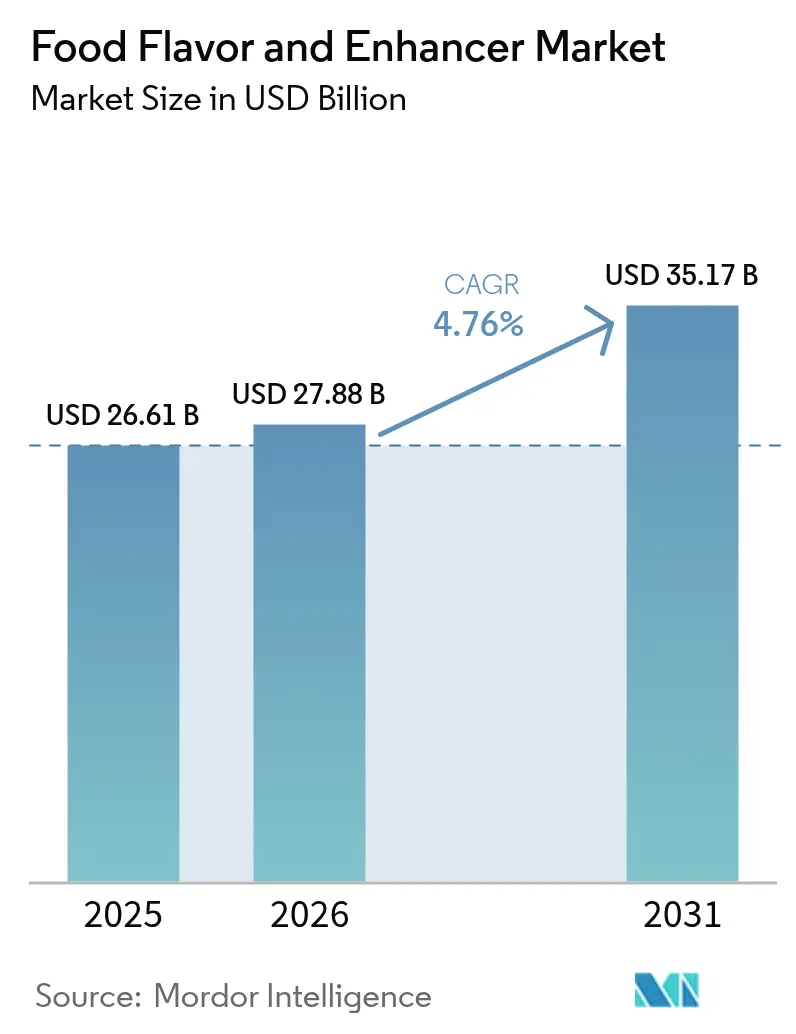

The Food Flavors And Enhancers Market size was valued at USD 26.61 billion in 2025 and estimated to grow from USD 27.88 billion in 2026 to reach USD 35.17 billion by 2031, at a CAGR of 4.76% during the forecast period (2026-2031). Strong demand from beverage, snack, and ready-meal manufacturers, coupled with precision-fermentation breakthroughs, continues to offset raw-material volatility and rising regulatory scrutiny. Leading firms are deploying biotechnology platforms to secure reliable supplies of natural vanillin, citrus, and botanicals, while brand owners pursue novel fusion flavors to differentiate on crowded shelves. Urban lifestyles, especially in Asia-Pacific and South America, sustain double-digit growth in convenience foods, encouraging producers to scale local flavor production and shorten supply chains. Consolidation is accelerating as larger players acquire specialty-ingredient innovators to gain clean-label capabilities and absorb escalating GRAS-notification costs.

Key Report Takeaways

- By product type, food flavors controlled 78.12% of the Food Flavors And Enhancers Market share in 2025, whereas food enhancers are projected to log the fastest 6.08% CAGR to 2031.

- By type, synthetic flavors held 70.85% share of the Food Flavors And Enhancers Market size in 2025, yet natural flavors are on track for a 6.35% CAGR through 2031.

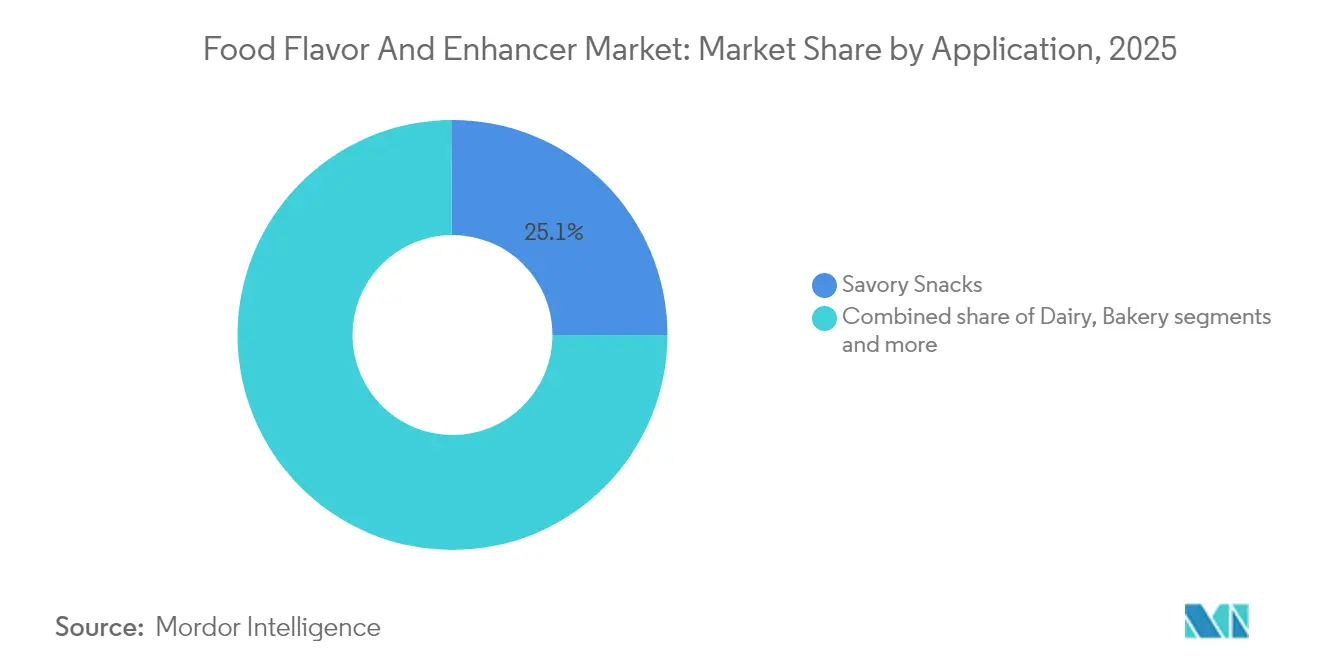

- By application, savory snacks retained a 25.10% revenue share in 2025.beverages advanced at the highest 5.92% CAGR through 2031.

- By form, liquid formulations led with a 38.95% share of the Food Flavors And Enhancers Market size in 2025, whereas powders are expanding at a 6.74% CAGR.

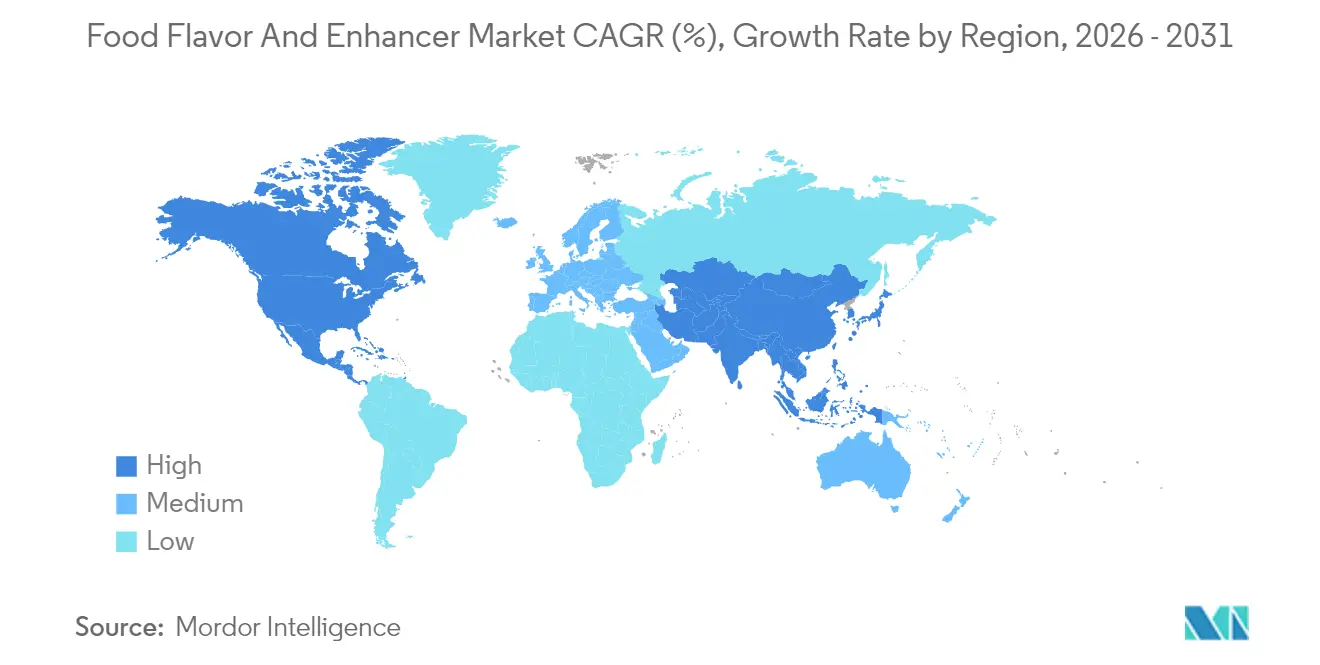

- By geography, Asia-Pacific commanded 29.10% of the Food Flavors And Enhancers Market share in 2025 and is registering the quickest 6.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Flavors And Enhancers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Demand for Processed Food and Beverages | +1.2% | Global, with strongest impact in Asia-Pacific and South America | Medium term (2-4 years) |

| Consumer Preferences for Novel Flavor Combinations | +0.8% | North America and Europe, expanding to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Innovation in Flavor Development and Manufacturing | +0.9% | Global, concentrated in Research and Development hubs across US, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Growing Demand for Clean Label and Sustainable Flavors | +1.1% | North America and Europe primary, Asia-Pacific emerging | Medium term (2-4 years) |

| Urbanization and Busy Lifestyles Boosting Ready-to-Eat Meals | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Short term (≤ 2 years) |

| Increasing Popularity of Exotic and Ethnic Flavors | +0.6% | Global, with early adoption in North America and urban Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in Demand for Processed Food and Beverages

The increasing demand for processed food and beverages is a significant driver of the Food Flavors And Enhancers Market. As consumers continue to seek convenience and ready-to-eat options, the processed food industry is experiencing substantial growth. This trend is further fueled by the rising urban population, changing lifestyles, and the growing preference for packaged and shelf-stable products. To meet consumer expectations for taste and quality, manufacturers are increasingly incorporating food flavors and enhancers into their products. These additives play a crucial role in improving the sensory appeal, enhancing taste profiles, and ensuring consistency in processed food and beverage offerings. Additionally, the growing influence of Western food culture in developing regions, coupled with the increasing penetration of international food brands, is further driving the demand for processed food products. The rise in disposable incomes and the expanding middle-class population are also contributing to the consumption of processed foods, which, in turn, is boosting the demand for food flavors and enhancers.

Consumer Preferences for Novel Flavor Combinations

Consumer preferences for novel flavor combinations are driving growth in the Food Flavors And Enhancers Market. As consumers increasingly seek unique and innovative taste experiences, manufacturers are focusing on developing diverse flavor profiles that cater to these evolving demands. This trend is particularly evident in the growing popularity of fusion cuisines, which blend flavors from different culinary traditions to create distinctive offerings. Additionally, the demand for exotic and unconventional flavors, such as floral, spicy-sweet, or umami-rich combinations, is gaining traction across various food and beverage categories. Companies are leveraging advanced flavor technologies and natural ingredients to meet these preferences while ensuring product quality and safety. Furthermore, the rise of health-conscious consumers has led to a surge in demand for flavors derived from natural and organic sources, as well as clean-label products. This has prompted manufacturers to innovate and experiment with plant-based ingredients, spices, and herbs to create flavors that align with consumer expectations.

Growing Demand for Clean Label and Sustainable Flavors

The growing demand for clean-label and sustainable flavors is a significant driver in the Food Flavors And Enhancers Market. Consumers are increasingly prioritizing transparency in ingredient sourcing and production processes, pushing manufacturers to adopt natural, organic, and eco-friendly flavoring solutions. This shift is fueled by rising health consciousness and environmental awareness, as consumers seek products free from artificial additives, preservatives, and synthetic chemicals. According to research by the CBI Ministry of Foreign Affairs, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, increasing from 52% in 2021 [1]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities,"cbi.eu. This substantial growth highlights the accelerating consumer preference for clean-label offerings, further compelling manufacturers to innovate and align their portfolios with these evolving demands. Additionally, the emphasis on sustainability has led to the adoption of flavors derived from renewable resources and sustainable farming practices. These trends are reshaping the market landscape, driving companies to adapt and meet the rising expectations for transparency and eco-consciousness.

Urbanization and Busy Lifestyles Boosting Ready-to-Eat Meals

The increasing pace of urbanization and the prevalence of busy lifestyles are significantly driving the demand for ready-to-eat meals, which, in turn, is influencing the Food Flavors And Enhancers Market. This shift has led to a growing reliance on convenient food options, such as ready-to-eat meals, which require minimal preparation time. According to a UN-Habitat report, Asia accounts for 54% of the world's urban population, equating to over 2.2 billion individuals. Projections suggest that by 2050, Asia's urban population will increase by an additional 1.2 billion, representing a 50% growth [2]Source: UN-Habitat, “Asia and the Pacific Region”,unhabitat.org. This rapid urbanization in Asia is expected to further drive the demand for ready-to-eat meals, as urban consumers increasingly prioritize convenience and time efficiency. To cater to this demand, manufacturers are focusing on enhancing the taste and quality of these meals by incorporating advanced food flavors and enhancers. Additionally, the rising number of working professionals and dual-income households has further amplified the need for quick and flavorful meal solutions, thereby boosting the growth of the Food Flavors And Enhancers Market. According to the European Commission, approximately 65.4% of all parents in the EU were in active employment in 2023 [3]Source: European Commission, “Household Consumption Statistics”, www.ec.europa.eu .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Quality Standards and Regulations Impact Market Growth | -0.9% | Global, with highest impact in Europe and North America | Long term (≥ 4 years) |

| Flavor Inconsistency Challenges Market Growth | -0.6% | Global, particularly affecting emerging market operations | Medium term (2-4 years) |

| Fluctuating Raw Material Prices Impacting Production Costs | -1.1% | Global, with severe impact on vanilla, citrus, and cocoa-dependent products | Short term (≤ 2 years) |

| Consumer Awareness of Potential Health Risks From Artificial Ingredients | -0.7% | North America and Europe primary, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Quality Standards and Regulations Impact Market Growth

The Food Flavors And Enhancers Market faces significant restraint due to stringent quality standards and regulatory frameworks. Governments and regulatory bodies worldwide have implemented strict guidelines to ensure food safety and quality, which directly impact the production and usage of food flavors and enhancers. Manufacturers must comply with these regulations, which often involve rigorous testing, certification processes, and adherence to permissible limits for additives. These requirements increase production costs and can delay product launches, thereby hindering market growth. Additionally, variations in regulatory standards across regions create challenges for global market players, as they must adapt their products to meet diverse compliance requirements. This regulatory complexity not only affects operational efficiency but also limits the entry of new players into the market, further restraining its growth potential. Regulatory authorities are increasingly scrutinizing synthetic additives and artificial flavors, which are commonly used in the industry. As a result, companies are compelled to invest heavily in research and development to create innovative, natural, and compliant alternatives.

Flavor Inconsistency Challenges Market Growth

Flavor inconsistency remains a critical restraint to the growth of the Food Flavors And Enhancers Market. The inability to maintain uniform flavor profiles across batches can significantly impact consumer satisfaction, leading to diminished brand loyalty and reduced market demand. This issue arises due to several factors, including variability in raw material quality, differences in production processes, and fluctuations in storage and transportation conditions. For instance, natural ingredients, which are increasingly preferred by consumers, often exhibit variations in taste and aroma due to differences in cultivation practices, climatic conditions, and harvesting methods. Such inconsistencies make it challenging for manufacturers to deliver a standardized product experience. Moreover, the global nature of the food industry adds another layer of complexity. Regional differences in consumer taste preferences, ingredient availability, and regulatory standards further complicate the task of achieving flavor consistency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Flavor Dominates While Enhancers Gain Momentum

Food flavor commands a significant 78.12% share of the food flavors and enhancers market, highlighting its crucial importance in diverse applications. This dominant position reflects its widespread adoption across various industries, including beverages, bakery, confectionery, dairy, and savory products. The extensive use of food flavor is driven by its ability to enhance taste profiles, meet consumer preferences, and align with evolving trends in natural and clean-label ingredients. Its pivotal role in product innovation and development further solidifies its leadership in the market. Additionally, the growing demand for customized flavor solutions tailored to regional and cultural preferences has further propelled its adoption.

Meanwhile, enhancers are set to experience the swiftest growth, with a projected CAGR of 6.08% from 2026 to 2031. This surge is driven by processors seeking cost-effective intensity boosters. The trend is especially pronounced in meat-analogue recipes, where umami enhancers adeptly mask the beany off-notes of legume proteins. Manufacturers enjoy an added edge: using lower inclusion rates not only optimizes flavor but also liberates label space for nutrient fortification claims, a burgeoning point of differentiation.

By Type: Natural Flavors Outpace Synthetic Despite Market Dominance

In 2025, synthetic formulations dominated the food flavors and enhancers market, accounting for 70.85% of the market share. Their widespread adoption is attributed to their ability to deliver consistent and reliable performance at lower unit costs. These formulations are preferred by manufacturers due to their cost-effectiveness and scalability, making them a popular choice in various food and beverage applications. The synthetic segment continues to benefit from advancements in technology, enabling the production of diverse and stable flavor profiles that cater to consumer preferences. Additionally, synthetic flavors offer extended shelf life and uniformity, which are critical for large-scale production and global distribution.

Natural flavors, although starting from a smaller base, are projected to grow at a CAGR of 6.35% during the forecast period. This growth is driven by increasing consumer demand for clean-label products and wellness-oriented choices. Retailer mandates restricting artificial additives further bolster the adoption of natural flavors. These flavors are perceived as healthier and more sustainable, aligning with the rising trend of health-conscious consumption. Manufacturers are responding to this shift by investing in research and development to enhance the extraction and preservation of natural flavors. Furthermore, the growing popularity of organic and plant-based products has amplified the demand for natural flavors, as they align with consumer preferences for authenticity and transparency.

By Application: Savory Snacks Leads, Beverages Accelerate

In 2025, savory snacks accounted for 25.10% of the food flavors and enhancers market. This significant share highlights the growing consumer inclination toward enhanced taste experiences in snack products. The increasing demand for convenient, ready-to-eat options has driven manufacturers to experiment with bold and innovative flavor combinations, catering to diverse palates. Additionally, the rising trend of premiumization in the snack segment has encouraged the adoption of unique and exotic flavors, further strengthening the segment's position in the market. The focus on clean-label and natural ingredients in flavor enhancers is also gaining traction, aligning with consumer preferences for healthier snack options.

Meanwhile, beverages are projected to achieve a CAGR of 5.92% during the forecast period. The surging demand for flavored beverages, including functional drinks, carbonated beverages, and non-alcoholic options, fuels this growth. Consumers are increasingly seeking healthier alternatives and diverse flavor profiles, prompting manufacturers to innovate with natural and organic flavor enhancers. The segment is also benefiting from the rising popularity of plant-based and low-sugar beverages, which require advanced flavor solutions to meet taste expectations.

By Form: Liquid Dominates While Powder Forms Emerge

In 2025, liquid formats accounted for 38.95% of the food flavors and enhancers market share, primarily due to their ease of blending and uniform dispersion. Liquid formats are widely preferred in various applications, including beverages, dairy products, and sauces, as they integrate seamlessly into formulations without compromising texture or consistency. Their ability to deliver consistent flavor profiles and enhance the sensory attributes of food products has driven their adoption across the industry. Additionally, the growing demand for ready-to-drink beverages and convenience foods has further bolstered the use of liquid formats in the market.

Powders, on the other hand, are projected to register the highest CAGR of 6.74% during the forecast period. Their longer shelf life, ease of storage, and transportability make them a preferred choice for manufacturers and end-users alike. Powdered flavors and enhancers are extensively used in dry mixes, bakery products, and snack items, where moisture content needs to be controlled. The rising demand for processed and packaged foods, coupled with the increasing popularity of plant-based and functional food products, has contributed to the growth of powdered formats

Geography Analysis

In 2025, the Asia-Pacific region claimed a 29.10% share of the food flavors and enhancers market and is on track to expand at a 6.88% CAGR through 2031. This growth is fueled by swift urbanization and a burgeoning middle class's appetite for convenience foods. Multinational corporations are establishing innovation hubs in cities such as Shanghai and Bengaluru, customizing formulations to cater to regional tastes that often harmonize spicy heat with umami richness. Additionally, government initiatives promoting food technology exports bolster regional investments, positioning Asia-Pacific as a prime testing ground for scalable clean-label innovations.

In North America and Europe, mature consumption trends emphasize the importance of authenticity and provenance in purchasing choices. The rising demand for plant-based dishes in North America has sparked a pursuit for smoke and grill flavors reminiscent of barbecue, leading suppliers to hone their thermal reaction techniques. Meanwhile, European producers, navigating stringent additive regulations, are shifting towards fermented or biovanillin alternatives. These not only meet natural labeling standards but also align cost-wise with their synthetic counterparts.

South America and the Middle East, and Africa are emerging as demand hotspots, where Western dietary trends meld with rich indigenous culinary traditions. Quick service restaurant chains making inroads into cities like São Paulo and Nairobi frequently modify their offerings, blending local ingredients with familiar global flavor profiles, necessitating the use of hybrid flavor systems. Flavor companies in these regions note a growing preference for spicy-sweet blends among younger demographics, suggesting a promising export avenue for products initially crafted for local markets. However, infrastructure hurdles, particularly in cold-chain logistics, are steering innovations towards shelf-stable powder flavors, which are more adaptable to fluctuating climates.

Competitive Landscape

The Food Flavors And Enhancers Market demonstrates moderate fragmentation. This indicates a market environment that allows room for growth through mergers and niche expansions. Several prominent players, including Givaudan, IFF (International Flavors & Fragrances Inc.), DSM-Firmenich, Symrise, Kerry, Sensient, ADM, and Cargill, shape the competitive landscape. These companies have established themselves as market leaders by leveraging their extensive scale, diversified product portfolios, and strong regulatory expertise.

Despite the dominance of these key players, the market remains open to new entrants, as their combined market share has not yet reached levels that would create significant barriers to entry. However, the rising costs associated with regulatory compliance and the increasing need for advanced technology investments are gradually tilting the competitive landscape in favor of enterprises with substantial financial resources.

The competitive dynamics of the market are further influenced by the strategic initiatives undertaken by leading companies. These include mergers and acquisitions, partnerships, and investments in research and development to enhance product offerings and expand their market presence. For instance, the focus on natural and clean-label ingredients has driven innovation in the sector, with companies investing in sustainable and health-conscious solutions.

Food Flavors And Enhancers Industry Leaders

-

International Flavors & Fragrances Inc.

-

Givaudan SA

-

Symrise AG

-

DSM Firmenich AG

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Galactic launched a new natural oregano flavoring ingredient aimed at enhancing the taste and extending the shelf life of both meat and plant-based protein products. Debuting at IFFA 2025 in Frankfurt, Galimax Flavor O-50 joins the company's Galimax range.

- January 2025: FlavorSum, a flavor producer based in North America, broadened its portfolio to introduce flavors with modulating properties (FMPs). These FMPs are designed to tackle specific taste challenges in various food and beverage items. The newly introduced flavor systems possess the capability to mask bitterness, elevate mouthfeel, and reduce undesirable off-notes in products.

- October 2024: Edlong Corporation's acquisition of Brisan Group, a company with 30 years of operations in dairy and sweet flavor markets, expanded Edlong's dairy taste technology development capabilities.

- February 2024: Brookside Flavors and Ingredients completed the acquisition of Sterling Food Flavorings, a manufacturer of flavoring systems for the food and beverage industry. The acquisition strengthens Brookside's product portfolio and expands its offerings to current and potential customers.

Global Food Flavors And Enhancers Market Report Scope

Food flavors and enhancers are compounds that enhance or intensify food taste and aroma. These additives include natural and artificial flavors, along with enhancers such as monosodium glutamate (MSG), which amplifies existing flavors without contributing its taste. Manufacturers incorporate these ingredients into packaged foods to enhance their sensory characteristics.

The Food Flavors And Enhancers Market is segmented by type

of food flavors and enhancers. Food flavor is sub-segmented into natural, synthetic, and natural identical flavors. By application, the market is segmented into dairy, bakery, confectionery, savory snacks, meat, beverage, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Food Flavor |

| Food Enhancer |

By Type

| Natural |

| Synthetic |

| Nature Identical |

By Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverage |

| Other Applications |

By Form

| Powder |

| Liquid |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Egypt | |

| Nigeria | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Food Flavor | |

| Food Enhancer | ||

| By Type | Natural | |

| Synthetic | ||

| Nature Identical | ||

| By Application | Dairy | |

| Bakery | ||

| Confectionery | ||

| Savory Snack | ||

| Meat | ||

| Beverage | ||

| Other Applications | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Egypt | ||

| Nigeria | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Food Flavors And Enhancers Market?

The Food Flavors And Enhancers Market size reached USD 27.88 billion in 2026 and is projected to achieve USD 35.17 billion by 2031 at a 4.76% CAGR.

Which region is growing fastest for food flavors and enhancers?

Asia-Pacific leads with a 6.88% CAGR through 2031, backed by urbanization, rising disposable incomes, and strong local flavor preferences.

Are natural flavors overtaking synthetic ones?

Synthetic flavors still dominate with 70.85% share in 2025, but natural flavors are expanding faster at a 6.35% CAGR as clean-label demand rises.

What application drives the market’s growth?

Beverages exhibit the highest growth rate at 5.92% CAGR, propelled by functional drinks and hydration-focused launches that require sophisticated flavor systems.

Page last updated on: