Food Processing and Handling Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

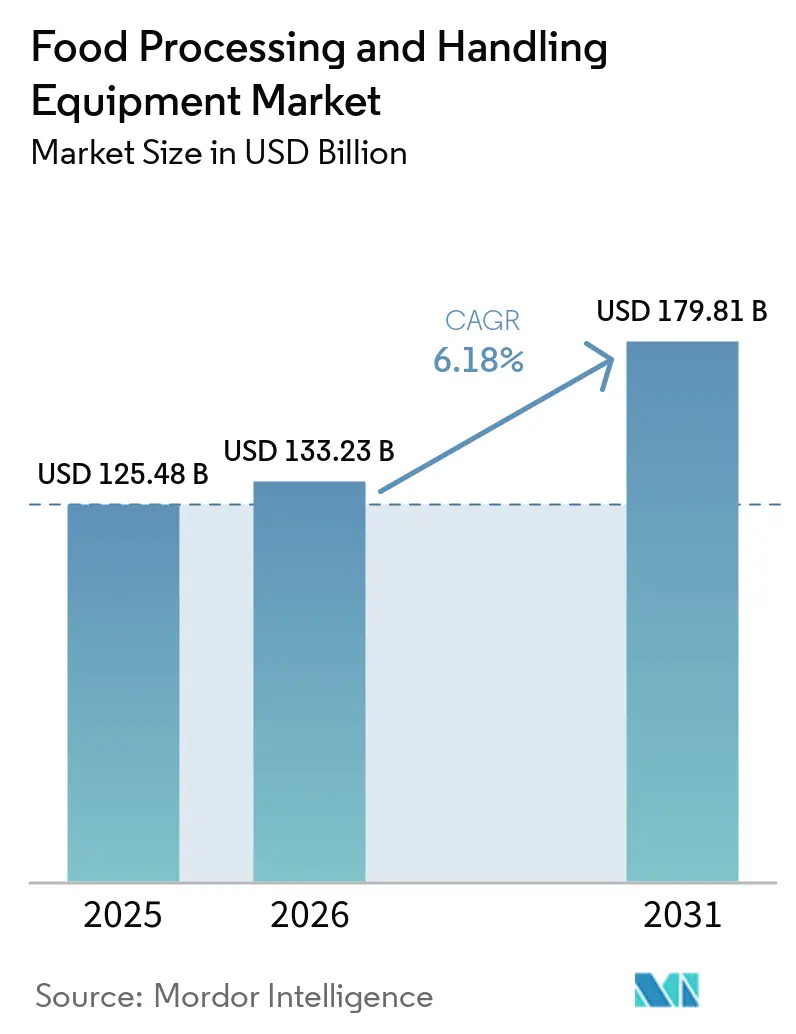

| Market Size (2026) | USD 133.23 Billion |

| Market Size (2031) | USD 179.81 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

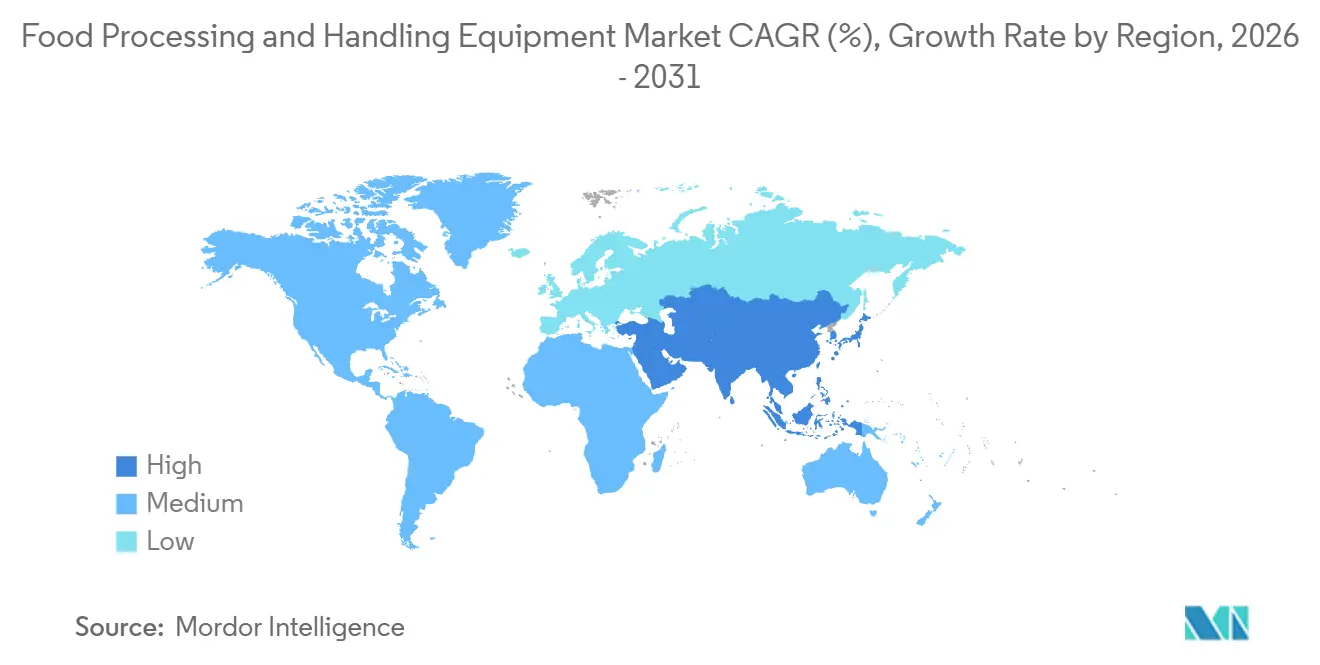

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Processing and Handling Equipment Market Analysis by Mordor Intelligence

The food processing and handling equipment market is projected to grow from USD 125.48 billion in 2025 to USD 133.23 billion in 2026 and reach USD 179.81 billion by 2031, with a CAGR of 6.2% during 2026-2031. Rising demand for processed and packaged foods is driving manufacturers to improve throughput, diversify product formats, and enhance plant efficiency. Stricter hygiene and traceability standards are accelerating system upgrades, while automation investments address labor shortages, inspection accuracy, and line consistency. Energy efficiency has become a key factor as processors weigh costs, emissions, and compliance. Despite short-term input cost pressures, steady food demand, faster automation payback, and regulatory requirements support long-term market growth.

Key Report Takeaways

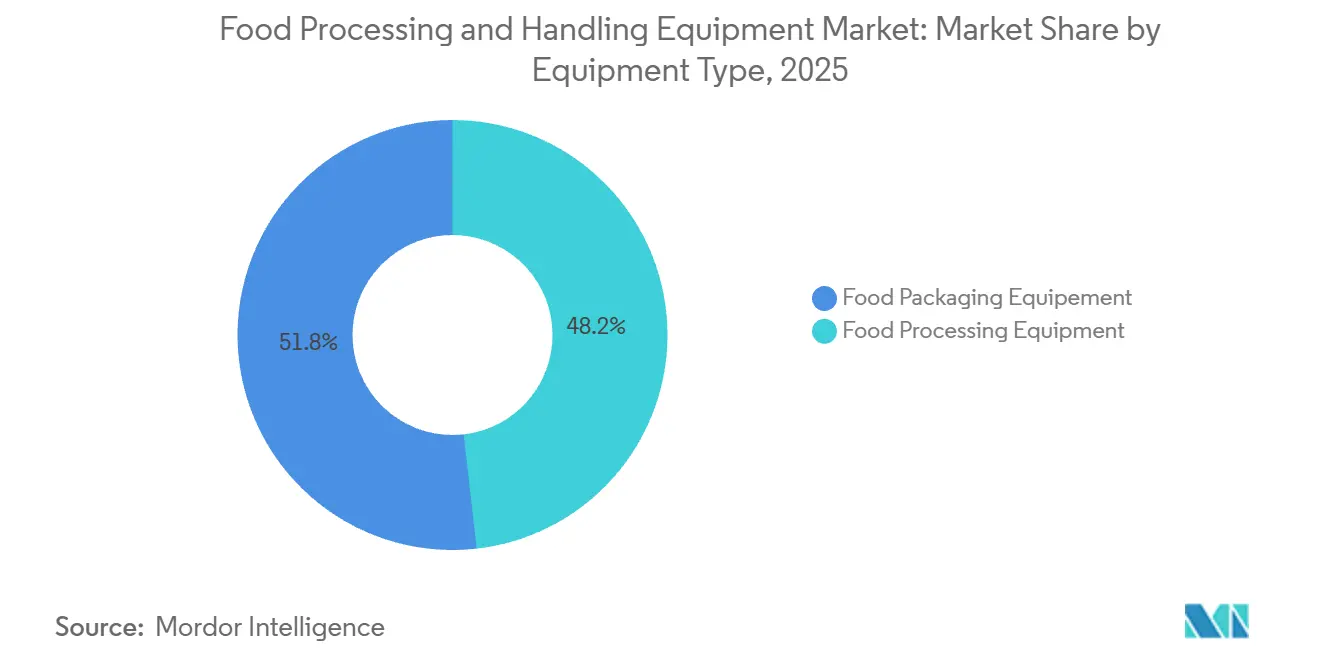

- By equipment type, food processing equipment held 48.21% of the food processing and handling equipment market in 2025, while food packaging equipment is forecast to expand at a 6.7% CAGR through 2031.

- By end-product form, solid products accounted for 53.12% of the food processing and handling equipment market in 2025, while semi-solid products recorded the highest projected CAGR at 7.3% through 2031.

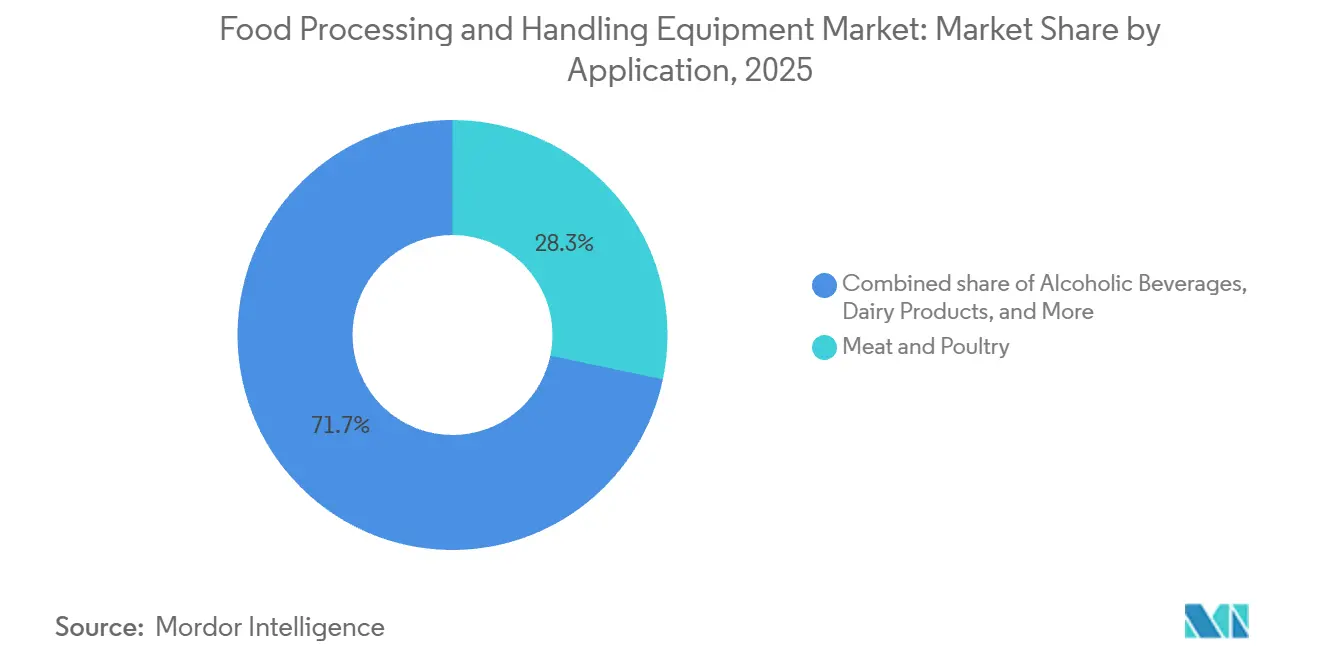

- By application, meat and poultry held 28.31% of the food processing and handling equipment market in 2025, while alcoholic beverages is projected to grow at a 6.5% CAGR through 2031.

- By geography, North America held 32.11% of the food processing and handling equipment market in 2025, while Asia-Pacific is projected to advance at an 8.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Processing and Handling Equipment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed, packaged, and value-added food products | +2.0% | Global, concentrated in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Integration of automation and robotics in food manufacturing | +1.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing focus on food safety and hygiene regulations | +0.8% | Global, highest regulatory intensity in Europe, the United States, and China | Medium term (2-4 years) |

| Emphasis on sustainability and energy efficiency in food processing | +0.6% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Expansion of cold chain infrastructure and refrigerated logistics | +0.5% | Asia-Pacific, with spillover into Middle East and Africa and South America | Long term (≥ 4 years) |

| Technological innovation in processing and packaging equipment | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed, Packaged, and Value-Added Food Products

The food processing and handling equipment market is growing alongside the rising demand for packaged and value-added foods in developed and emerging markets. In 2025, the global packaged food market experienced growth, with the Asia-Pacific region holding a significant share. This reflects the regions expanding manufacturing capacities and increasing equipment demand. The focus is shifting beyond volume, as categories like functional foods, plant-based proteins, and premium ready meals require advanced systems for handling, mixing, thermal treatment, and filling. Older production lines, though mechanically functional, are becoming less suitable, shortening replacement cycles in the market. Investments are now directed toward flexible platforms that support frequent changeovers, stricter quality controls, and complex product requirements within the same plant footprint.

Integration of Automation and Robotics in Food Manufacturing

Food manufacturers now prioritize labor efficiency and line consistency as essential operational needs rather than improvement goals, driving growth in the food processing and handling equipment market. By 2026, PMMI and FPSA identified AI-assisted inspection, HMI knowledge transfer, and digital tool adoption as key investment areas for U.S. food and beverage processors[1]Source: PMMI, “Processing State of the Industry 2026”, pmmi.org. Processors no longer view robotics as standalone purchases but integrate automation into systems connecting inspection, data capture, machine response, and output quality. This approach shortens the return window on automation projects, especially in regions with labor shortages and limited skilled operators. As payback periods shrink, demand for food processing and handling equipment is expanding, now including more mid-sized processors.

Increasing Focus on Food Safety and Hygiene Regulations

Stricter hygiene regulations are reshaping the design, operation, validation, and maintenance of food processing and handling equipment. In 2025, ISO 22002-1 revised its prerequisite program requirements for food manufacturing, emphasizing equipment capability and hygiene-related maintenance. Also in 2025, EHEDG released the fourth edition of Guideline 8 and Document 58, steering the conversation towards a risk-based hygienic design from the initial design phase. These concurrent updates shift the focus of compliance: it's now more about the design and documentation of equipment rather than its usage. As a result, there's heightened pressure to replace systems in the food processing and handling equipment market. Many of these systems, while still operational, fall short of today's stringent hygienic design standards.

Emphasis on Sustainability and Energy Efficiency in Food Processing

Energy performance is increasingly influencing procurement decisions in the food processing and handling equipment market. In 2025, Tetra Pak unveiled a pioneering integrated heat pump system for pasteurization, achieving an impressive 77% reduction in energy consumption by adeptly capturing and reusing process heat. SPX Flow, in 2026, highlighted the prowess of its APV Infusion UHT system, equipped with SteamRecycle, which not only recycles 100% of process steam but also boasts the potential to cut CO2 emissions by a staggering 1,000 tonnes annually per installation. The EXQUISHEAT initiative, rolled out in October 2025 as part of the European heat pump ecosystem, underscores a pivotal shift: the adoption of standardized industrial heat pumps is now intertwined with policy-driven strategies for food manufacturing. This trend amplifies the value of premium equipment in the market, as processors weigh the long-term utility savings and compliance benefits against the costs of clinging to outdated systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety regulations and compliance costs | -0.6% | Global, most acute in Europe and North America | Medium term (2-4 years) |

| Equipment maintenance complexities | -0.3% | Global, with higher effect in SME-heavy South America and Middle East and Africa | Medium term (2-4 years) |

| High maintenance and operational costs | -0.4% | North America and Europe | Medium term (2-4 years) |

| Supply chain disruptions and raw material price volatility | -0.5% | Global, concentrated in North America and East Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety Regulations and Compliance Costs

The food processing and handling equipment market benefits from stricter standards, but the cost of meeting them still acts as a restraint for smaller processors. Compliance work often requires equipment redesign, additional validation, more structured change control, and broader documentation, which stretches procurement cycles and limits discretionary spending on performance upgrades. Large processors can spread those costs across higher output volumes, while small and mid-sized operators face a narrower margin for replacement decisions in the food processing and handling equipment market. This creates uneven order patterns for OEMs because some customers move quickly to replace lines, while others delay purchases and focus on minimum viable retrofits. The result is a market where regulation supports long-term replacement demand but can also slow short-term conversion of interest into finalized orders.

Supply Chain Disruptions and Raw Material Price Volatility

Fluctuations in steel, aluminum, freight, and input prices continue to affect the food processing and handling equipment market, impacting OEM cost structures and customer capital budgets. PMMI's Q1 2026 tariff survey revealed that companies are increasingly adopting dual sourcing and diversifying supply chains geographically, though this requires time and capital that could otherwise support modernization. In May 2026, Purdue University's Center for Commercial Agriculture reported a 105.9% year-on-year increase in diesel prices and a 16.1% rise in industrial chemical costs, with these pressures typically appearing in food manufacturers' profit and loss statements after a 3 to 6 month delay[2]Source: Purdue Center for Commercial Agriculture, “The May 2026 CPI and PPI Reports The Food Price Pipeline Is Loading at Record Rates”, ag.purdue.edu. As processors redirect working capital to inventory buffers, sourcing changes, or margin protection, they tend to prioritize brownfield upgrades over full-line replacements. This shift does not reduce equipment demand but changes the timing, order mix, and pace of higher-value project execution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Processing Complexity Anchors Food Processing Equipment Leadership

In 2025, food processing equipment held a 48.21% share of the food processing and handling equipment market. This dominance highlights essential operations like cutting, grinding, mixing, and thermal treatment, which are crucial for product transformation. These processes result in a larger installed base and higher replacement needs compared to other equipment categories. Additionally, hygiene, automation, and productivity upgrades often start in primary processing before extending to other plant functions.

Between 2026 and 2031, the food packaging equipment segment is expected to grow at a 6.7% CAGR. This growth is driven by rising demand for flexible filling, sealing, labeling, and end-of-line systems as manufacturers adopt recyclable materials, diversify formats, and shorten production runs. Krones AG reported EUR 5,663.8 million in revenue in 2025, a 7.0% increase from EUR 5,293.6 million in 2024, reflecting strong demand for packaging technology. VDMA reported that packaging machines accounted for nearly 70% of Germany's food machinery exports in 2025, emphasizing their global importance. As a result, packaging lines are evolving into strategic assets, improving launch speeds, material adaptability, and labor efficiency.

By End-Product Form: Solid Products Lead; Semi-Solid Gains Driven by Formulation Premiumization

Solid products accounted for 53.12% of the food processing and handling equipment market in 2025. This segment covers a wide product base, including bakery, cereals, frozen proteins, confectionery, and several dairy formats, which gives it a larger aggregate equipment footprint across preparation, forming, heating, cooling, and packaging stages. Solid product lines also tend to involve multiple equipment families in sequence, which lifts capital intensity and supports sustained replacement demand in the food processing and handling equipment market. The segment remains important because production efficiency and hygiene upgrades across solid foods often require coordinated investment across several process steps rather than a single machine change.

The food processing and handling equipment market size for semi-solid products is projected to expand at 7.3% CAGR between 2026 and 2031. Growth is being driven by products such as cultured dairy, dips, spreadable proteins, and nutritional formulations that require careful mixing, homogenization, and filling performance under high-viscosity conditions. Cleaning difficulty is a major part of the segment story, since semi-solid materials are more likely to cling to surfaces and demand validated cleaning performance rather than basic washdown capability. ISO 22002-100:2025 strengthens the relevance of common prerequisite food safety requirements in these settings, where consistency in hygienic operation matters alongside process control. This means the food processing and handling equipment market is assigning more value to semi-solid lines that combine product integrity, validated cleaning, and stable output across more demanding formulations.

By Application: Protein Processing Anchors Demand; Alcoholic Beverages Outpaces the Market

In 2025, meat and poultry represented 28.31% of the food processing and handling equipment market. This segment requires high capital investment per facility, as modern automated lines integrate processes like killing, scalding, evisceration, chilling, deboning, portioning, inspection, and packaging. Its complexity makes meat and poultry a key demand driver, especially with priorities like hygienic design, yield control, and labor reduction. JBT Marel’s 2025 results highlighted a recovery in poultry demand, reinforcing the segment's importance to integrated processing solution providers.

From 2026 to 2031, the food processing and handling equipment market for alcoholic beverages is projected to grow at a 6.5% CAGR. Growth is driven by craft brewing, premium spirits, and rising demand for low-alcohol and non-alcoholic beverages, which require advanced blending, stabilization, and filtration processes. Germany’s machinery exports, supported by VDMA data, play a crucial role due to strong packaging and beverage equipment capabilities. Companies like Krones are well-positioned as the segment grows in volume and complexity, enabling alcoholic beverages to outpace the overall market growth despite a smaller base compared to protein processing.

Geography Analysis

In 2025, North America accounted for 32.11% of the food processing and handling equipment market. The U.S. led the region, with food and beverage machinery shipments reaching USD 6.2 billion, a 3.2% increase from 2024. The focus has shifted to brownfield upgrades over new plant construction, driving demand for automation, traceability, and throughput improvements. Suppliers specializing in retrofitting existing lines, enhancing digital traceability, and improving labor efficiency are benefiting. Replacement demand, driven by operational pressures, sustains North America's market growth.

Europe remains the second-largest market and a key export hub for food processing and packaging machinery. Germany's food and packaging machinery sector reached EUR 17 billion in 2025, with 84% exported, totaling EUR 11 billion. European suppliers are closely tied to global capital spending trends. Policies like the Green Deal and EXQUISHEAT program are boosting demand for energy-efficient systems and optimized process layouts. The market leans toward premium systems offering energy savings, hygiene readiness, and compliance durability, justifying higher upfront costs.

Asia-Pacific is the fastest-growing region, projected to grow at an 8.34% CAGR from 2026 to 2031. Growth is concentrated in China, India, and Southeast Asia, driven by rising processed food production, export activities, and cold chain investments. India's Ministry of Food Processing Industries allocated INR 6,520 crore (USD 785 million) for cold chain and value addition infrastructure under PMKSY through March 2026. JBT Marel's Global Production Center, launched in Pune in September 2025, highlights the region's growing manufacturing importance. While South America and the Middle East & Africa hold smaller shares, Latin America contributes 25% to global food exports. Abu Dhabi Food Hub's 37,000 sqm cold chain infrastructure deal in May 2026 signals expanding market potential for food processing and handling equipment.

Competitive Landscape

The Food Processing and Handling Equipment Market is moderately fragmented, driven by technological advancements, automation, diverse product portfolios, and global service networks. Key players like JBT Marel, GEA Group, Bühler AG, Tetra Laval International, and The Middleby Corporation dominate by offering solutions across sectors such as dairy, meat, bakery, beverages, and prepared foods. These companies invest in R&D and partnerships to meet growing demands for efficiency, food safety, and automation.

JBT Marel and GEA Group excel with comprehensive equipment portfolios for meat, poultry, seafood, dairy, and prepared foods. Bühler AG focuses on advanced grain and cereal processing technologies, while Tetra Laval leads in dairy and beverage processing and packaging. The Middleby Corporation expands through acquisitions and innovative foodservice equipment.

Market players emphasize automation, digitalization, energy-efficient systems, and integrated solutions to stay competitive. Strategies like mergers, product innovations, capacity expansions, and smart manufacturing are reshaping the market. While global leaders leverage their reach and expertise, regional manufacturers compete effectively with customized solutions and localized support, maintaining the market's moderate fragmentation.

Food Processing and Handling Equipment Industry Leaders

JBT Marel

GEA Group Aktiengesellschaft

Bühler AG

Tetra Laval International S.A.

The Middleby Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Tetra Pak expanded Product Development Center at its US and Canada headquarters in Denton, Texas. The investment doubles current production capacity and integrates processing, packaging, formulation, testing, and scaling support within a single co-creation facility.

- January 2026: SPX Flow's APV Infusion UHT system featuring SteamRecycle™ received the 2026 SEAL Sustainable Product Award for its closed-loop steam recovery design. The technology recycles 100% of process steam and is documented to reduce CO2 emissions by up to 1,000 tonnes annually per installation.

- September 2025: JBT Marel launched its Global Production Center (GPC) in Pune, India, establishing local manufacturing to serve Indian and Asia-Pacific food processing markets and positioning Pune as a regional export base.

Global Food Processing and Handling Equipment Market Report Scope

| Food Processing Equipment | Cutting and slicing equipment |

| Grinding and milling equipment | |

| Mixing and blending equipment | |

| Homogenizers | |

| Extruders | |

| Cooking and heating equipment | |

| Pasteurization and sterilization equipment | |

| Drying and dehydration equipment | |

| Evaporators and concentrators | |

| Fermentation equipment | |

| Food Packaging Equipement |

| Solid |

| Liquid |

| Semi-solid |

| Bakery and Confectionery |

| Meat and Poultry |

| Fish and Seafood |

| Dairy Products |

| Alcoholic Beverages |

| Non-alcoholic Beverages |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Equipment Type | Food Processing Equipment | Cutting and slicing equipment |

| Grinding and milling equipment | ||

| Mixing and blending equipment | ||

| Homogenizers | ||

| Extruders | ||

| Cooking and heating equipment | ||

| Pasteurization and sterilization equipment | ||

| Drying and dehydration equipment | ||

| Evaporators and concentrators | ||

| Fermentation equipment | ||

| Food Packaging Equipement | ||

| By End-Product Form | Solid | |

| Liquid | ||

| Semi-solid | ||

| By Application | Bakery and Confectionery | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy Products | ||

| Alcoholic Beverages | ||

| Non-alcoholic Beverages | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for food processing and handling equipment?

The sector is projected to grow at a 6.2% CAGR, with value rising from USD 133.23 billion in 2026 to USD 179.81 billion by 2031.

Which equipment category leads current demand?

Food processing equipment led with 48.21% share in 2025 because it covers the core transformation steps that most plants cannot avoid.

Which category is growing the fastest by equipment type?

Food packaging equipment is forecast to grow at a 6.7% CAGR through 2031, supported by format changes, recyclable materials, and higher end-of-line automation needs.

Why are semi-solid products drawing more equipment investment?

Semi-solid products are set to grow at a 7.3% CAGR because they require more specialized mixing, homogenization, filling, and validated cleaning performance.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region with an 8.34% CAGR through 2031, supported by manufacturing expansion, cold chain investment, and rising local production capacity.

Page last updated on: