Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 112.92 Billion |

| Market Size (2031) | USD 180.97 Billion |

| Growth Rate (2026 - 2031) | 9.89% CAGR |

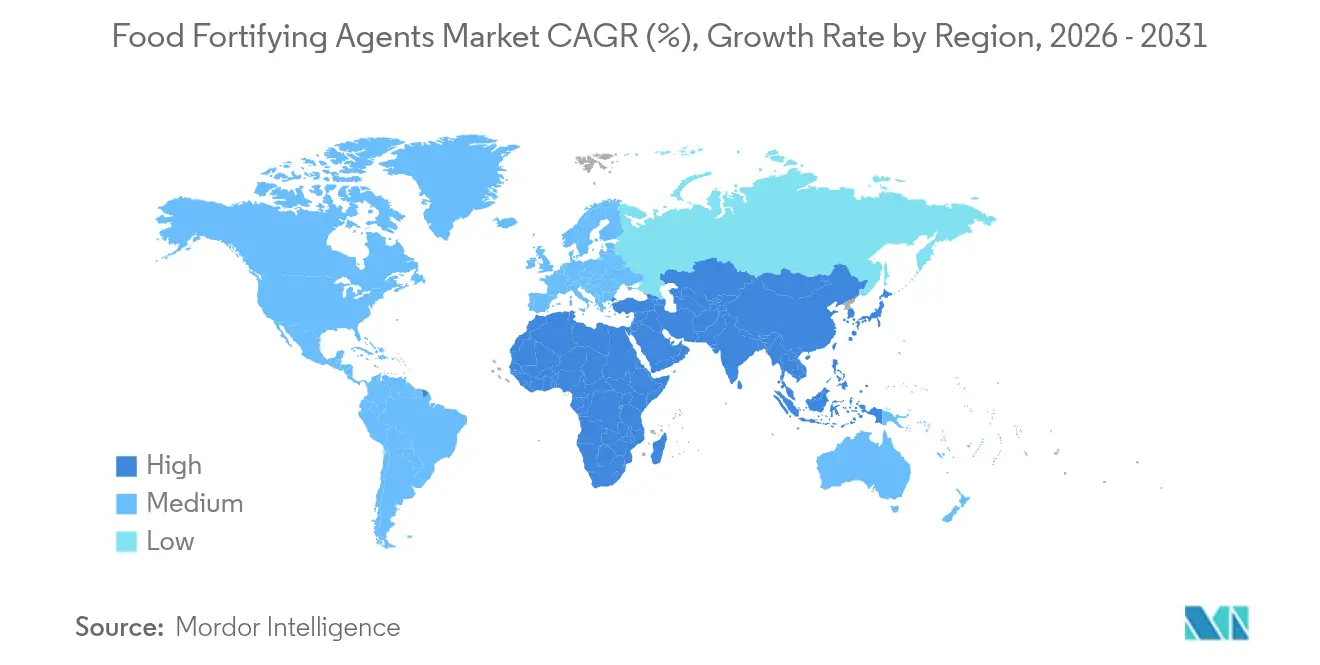

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

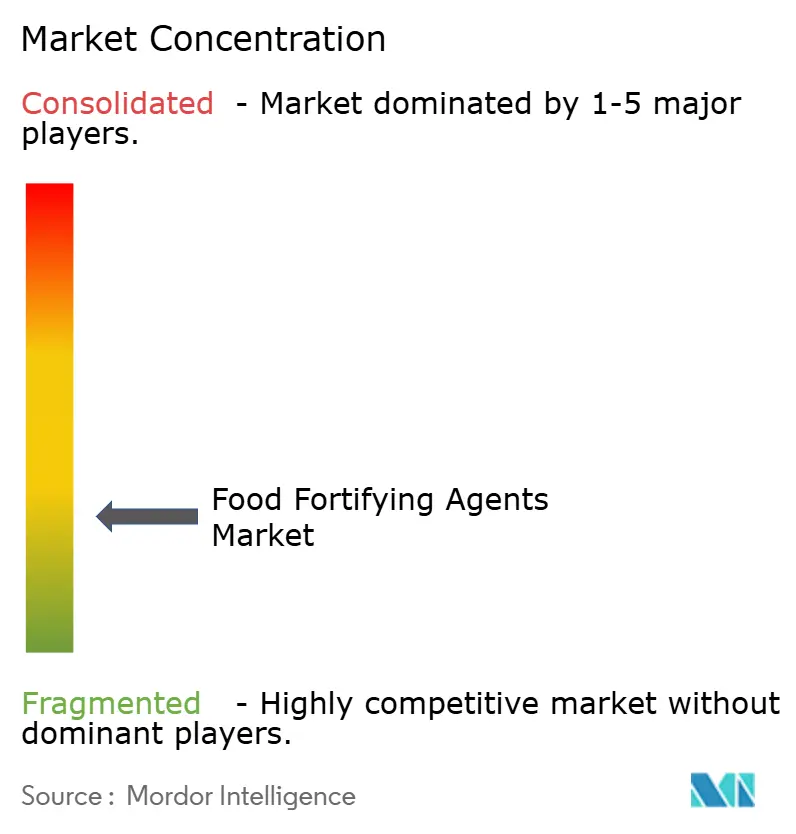

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Fortifying Agents Market Analysis by Mordor Intelligence

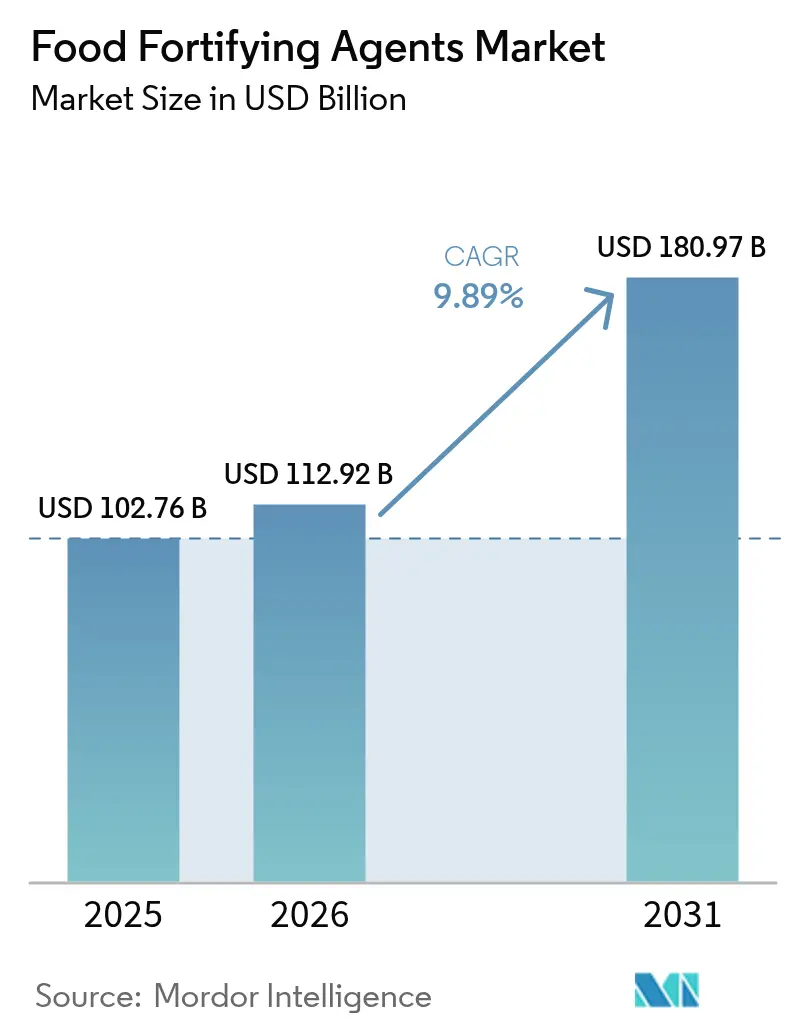

The food fortifying agents market size in 2026 is estimated at USD 112.92 billion, growing from 2025 value of USD 102.76 billion with 2031 projections showing USD 180.97 billion, growing at 9.89% CAGR over 2026-2031. The market growth is driven by rising micronutrient deficiencies globally, especially in developing regions with persistent nutritional gaps. Mandatory fortification regulations in various countries and increasing consumer demand for nutritionally enhanced functional foods support market expansion. The consolidation of ingredient manufacturers has improved operational efficiency and reduced production costs. Advancements in precision fermentation and microencapsulation technologies have enhanced nutrient stability and bioavailability in fortified products. In January, 2025 FDA proposed front-of-package labeling regulations that are shaping product development strategies and fortification processes. Market dynamics differ by region, with North American demand driven by health-conscious consumers, while Asia-Pacific experiences rapid growth through government food fortification programs addressing nutritional deficiencies.

Key Report Takeaways

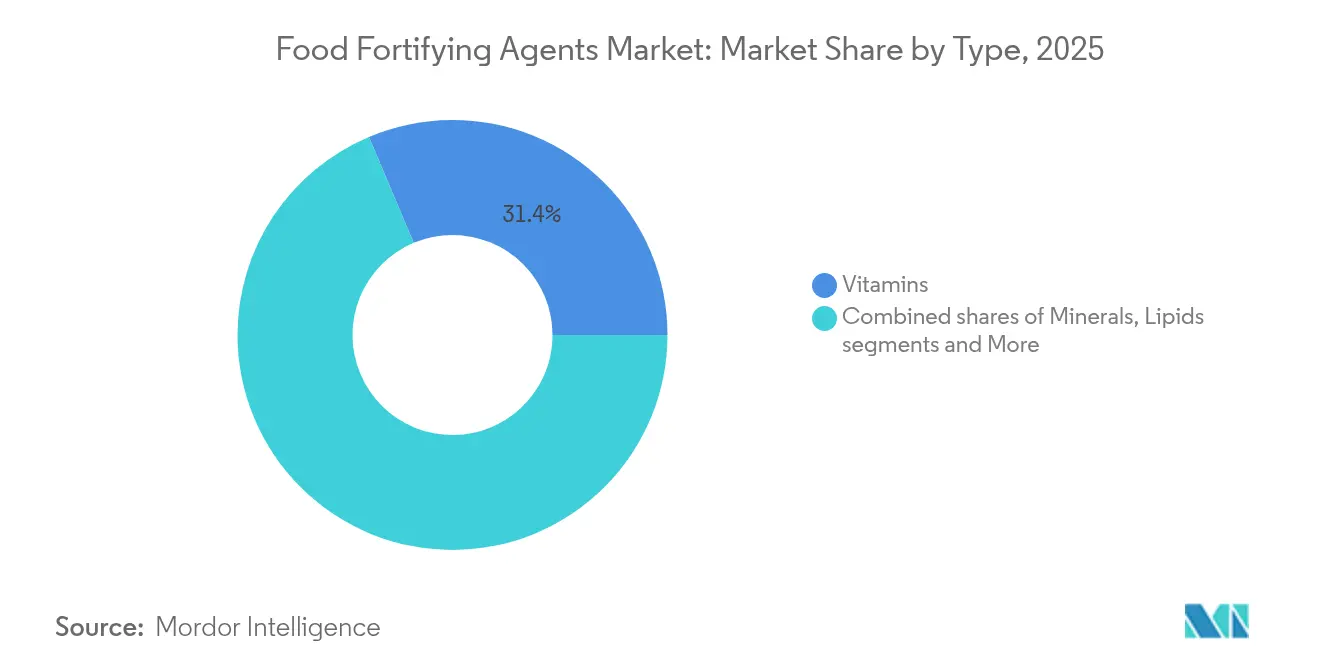

- By type, vitamins led with 31.35% revenue share in 2025, whereas prebiotics and probiotics are advancing at a 12.11% CAGR through 2031.

- By application, dairy and dairy-based products captured 30.10% of the food fortifying agents market share in 2025; beverages recorded the fastest expansion at 12.74% CAGR through 2031.

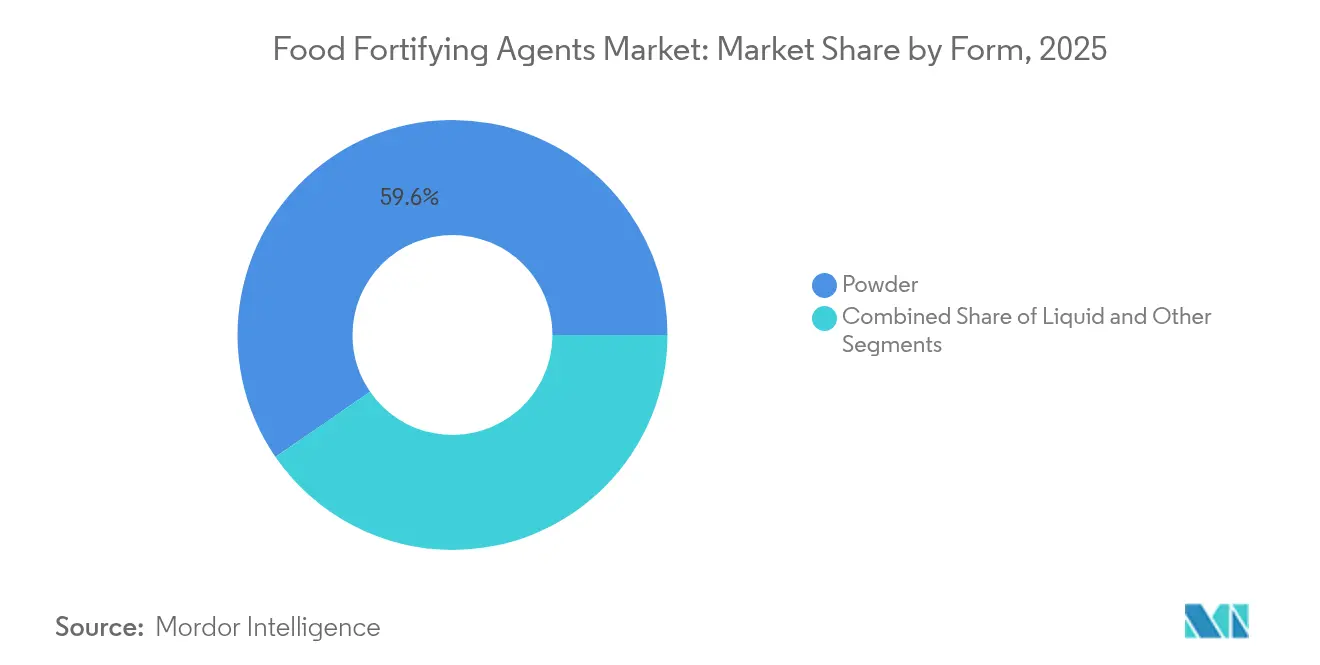

- By form, powder formulations commanded 59.60% of the 2025 food fortifying agents market size, while liquid formats grew at 12.22% CAGR on superior bioavailability.

- By geography, North America held 32.60% of 2025 revenue; Asia-Pacific is set to grow the fastest at 11.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Food Fortifying Agents Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing prevalence of micronutrient deficiencies | +2.8% | Global, with highest impact in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Expansion of mandatory fortification regulations | +2.1% | Global, with early adoption in North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing consumer demand for functional and fortified foods | +1.9% | North America and Europe core, spill-over to urban Asia-Pacific centers | Medium term (2-4 years) |

| Rising need for fortified foods in child and maternal nutrition programs | +1.6% | Asia-Pacific, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Increased fortification of staple foods in developing economies | +1.4% | Asia-Pacific, Sub-Saharan Africa, with focus on India, China, Nigeria | Long term (≥ 4 years) |

| Advancements in fortification technologies | +1.2% | Global, with research and development centers in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing prevalence of micronutrient deficiencies

The global micronutrient deficiency crisis continues to grow, with populations worldwide experiencing inadequate intake of essential nutrients. Iron, vitamin A, and iodine deficiencies are most prevalent, particularly affecting children and pregnant women, with low- and middle-income countries facing the highest burden. According to the World Health Organization, 30.7% of women aged 15-49 years suffered from anaemia in 2023, highlighting the persistent need for fortification programs.[1]World Health Organization, "WHO Global Anaemia estimates, 2025 Edition", who.int The economic impact of these deficiencies, including reduced productivity and increased healthcare costs, has prompted governments to implement large-scale fortification as a cost-effective health intervention. As staple foods serve as the primary nutrient delivery vehicle for vulnerable populations, ingredient suppliers that meet public-sector procurement standards can secure substantial contract volumes. The significant economic burden of micronutrient deficiencies on developing countries has made food fortification a priority public health initiative.

Expansion of mandatory fortification regulations

Many countries have implemented mandatory fortification programs to address widespread nutrient deficiencies. These initiatives, particularly in developing regions, require food manufacturers to incorporate fortifying agents into staple foods, increasing the demand for fortified products across various demographic segments. In March 2025, Tanzania introduced comprehensive regulations mandating all flour millers to fortify their products with essential vitamins and minerals by December 2025. The Ministry of Health, supported by partners like Sanku, launched this initiative to improve nutrition access and combat malnutrition in vulnerable populations. Similarly, Mauritius enacted mandatory wheat flour fortification legislation in 2023 to address micronutrient deficiencies, particularly iron deficiency anemia, which affects a significant portion of its population. This legislation resulted from extensive collaboration between the Government of Mauritius, FFI, the Food and Agriculture Organization of the United Nations (FAO), and the Southern African Development Community (SADC).[2]Food Fortification Initiative, "Mauritius Mandates Wheat Flour Fortification to Combat Micronutrient Deficiencies", ffinetwork.org These mandatory fortification requirements are driving the substantial growth of food fortifying agents in the global market.

Growing consumer demand for functional and fortified foods

The increasing consumer understanding of diet's role in maintaining health drives growth in the fortified foods category. This shift aligns with the broader trend toward preventive healthcare through nutrition. According to the IFIC Food and Health Survey 2024, protein consumption awareness among U.S. consumers has steadily increased from 59% in 2022 to 67% in 2023, reaching 71% in 2024.[3]The International Food Information Council, "2024 IFIC Food & Health Survey", ific.orgMoreover, plant-based fortified products continue to gain market share among flexitarian consumers, while clean-label claims strengthen consumer trust in food fortifying agents. The market demonstrates significant innovation in functional beverages containing vitamins, minerals, and gut-health ingredients, offering convenient nutrition solutions for urban consumers. Meal replacement beverages with comprehensive vitamin and mineral profiles address busy lifestyles and nutritional needs. Consumer willingness to pay premium prices for fortified products, especially those with proven health claims and transparent ingredient sourcing, indicates a clear premiumization trend. Advanced delivery technologies, including liposomal encapsulation, improve nutrient absorption and support higher price points.

Rising need for fortified foods in child and maternal nutrition programs

Government feeding programs are expanding the use of nutrient-enriched staple foods to address malnutrition in early childhood. Through targeted interventions and comprehensive nutrition strategies, these programs aim to improve health outcomes in vulnerable populations. The Mission Poshan 2.0, a flagship program of the Government of India, addresses malnutrition challenges and promotes improved health, wellness, and immunity through community engagement, outreach, behavioral change, and advocacy. The scheme focuses on maternal nutrition, infant and young child feeding norms, treatment of Severe Acute Malnutrition (SAM)/Moderate Acute Malnutrition (MAM), and anemia. It implements a multi-faceted approach, incorporating dietary modifications and nutritional education alongside fortification efforts.[4]Ministry of Health and Family Welfare, "Details of Anemia Mukt Bharat", pib.gov.in These contracts include performance metrics and quality assurance protocols to maintain consistent fortification standards. Moreover, in May 2023, delegates at the Seventy-sixth World Health Assembly adopted a resolution to accelerate efforts to prevent micronutrient deficiencies through safe and effective food fortification.[5]World Health Organization, "New WHA resolution to accelerate efforts on food micronutrient fortification", who.int The resolution urges Member States to make decisions on food fortification with micronutrients and supplementation while considering ways to strengthen financing and monitoring mechanisms.

Restraints Impact Analysis of Food Fortifying Agents Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High costs of fortification ingredients and processes | -1.8% | Global, with highest impact in price-sensitive developing markets | Short term (≤ 2 years) |

| Low awareness of fortified foods in rural and underserved | -1.2% | Rural areas in Asia-Pacific, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Lack of specialized equipment and skilled workforce | -0.9% | Developing economies, particularly small-scale manufacturers | Medium term (2-4 years) |

| Inconsistent quality and standardization among ingredient | -0.7% | Global, with concentration in emerging supplier markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High costs of fortification ingredients and processes

Supply chain disruptions and production constraints are causing significant cost increases across vitamin categories, with vitamin A and carotenoids facing severe price pressures due to production facility incidents. A fire at BASF's plant in Ludwigshafen, Germany, in late July 2024, resulted in a force majeure declaration for specific vitamin and aroma ingredient products. The incident, which occurred at a facility manufacturing vitamin A, vitamin E, carotenoid precursors, and aroma ingredients, led to a production shutdown and supply disruptions. BASF estimated production of vitamins A and E, and carotenoids will not resume until early 2025, creating potential shortages in the global vitamin supply chain. Small food manufacturers face financial pressure from capital requirements for blending, dosing, and quality-control equipment, which often requires substantial initial investment and ongoing maintenance costs.

Low awareness of fortified foods in rural and underserved regions

Limited consumer education and traditional dietary habits restrict the reach of voluntary programs in rural markets. High logistics costs from distribution challenges, including poor road infrastructure, inadequate storage facilities, and unreliable transportation networks, discourage market entry, even with regulatory support. While health workers and extension agents are essential for community engagement, gaps in their training, resources, and deployment remain widespread across rural regions. Traditional marketing channels are less effective in areas with limited media access, requiring direct outreach through village fairs, school demonstrations, door-to-door campaigns, and community meetings. Success in these markets depends on culturally appropriate communication strategies, comprehensive stakeholder engagement, and substantial joint investments in rural supply-chain infrastructure development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Food Fortifying Agents Market Segment Analysis

By Type:

Vitamins Lead While Probiotics Drive InnovationVitamins held the dominant position in the market with a 31.35% share in 2025, driven by established regulatory frameworks and economical premix solutions. The vitamin segment is expected to grow consistently, supported by mandatory fortification requirements for flour, rice, and oil. Prebiotics and probiotics are experiencing rapid growth at a 12.11% CAGR, supported by research demonstrating the relationship between gut microbiome balance, immune function, and metabolic health. Manufacturers are implementing microencapsulation technology to achieve 85-86% viability under thermal and acidic conditions, enhancing stability in shelf-stable beverages. The protein and amino acid segment benefits from growth in sports nutrition, while omega-3 lipids contribute cardiovascular benefits to conventional food products. Minerals, particularly iron and zinc, remain crucial for public health programs targeting anemia and growth deficiency.

The market demonstrates ongoing innovation in delivery systems. Carbohydrates are gaining renewed interest through prebiotic fiber additions, responding to increased consumer interest in digestive health. The "others" category includes emerging compounds such as polyphenols and plant-based proteins, creating opportunities for specialized manufacturers. The anticipated streamlining of probiotic strain registration and postbiotic approval processes is expected to transform market competition and increase formulation requirements in the food fortifying agents industry.

By Application:

Dairy Dominance Challenged by Beverage InnovationDairy and dairy-based products hold 30.10% of the market share in 2025, driven by established fortification protocols for vitamins A and D. This segment maintains its position through widespread household consumption and government-supported school milk programs. The beverage category is projected to grow at 12.74% CAGR (2026-2031), driven by ready-to-drink products that incorporate comprehensive micronutrient profiles, electrolytes, and live cultures. The food fortifying agents market in beverages is expected to surpass traditional categories due to increasing consumer preference for convenience and portable nutrition.

The market sees technological advancements such as liposomal vitamin C in isotonic beverages for enhanced absorption, while plant-based meal replacements combine protein, omega-3, and prebiotic fibers. Mandatory flour fortification sustains demand for bakery products, though increasing consumer preference for clean-label products drives interest toward minimally processed grains. The infant nutrition segment maintains strict regulatory standards, requiring suppliers to use high-purity, pharmaceutical-grade ingredients. The expansion of fortification into meat alternatives, snack bars, and ready-to-eat meals indicates growth beyond traditional products, creating opportunities for manufacturers to develop premium offerings.

By Form:

Powder Stability Versus Liquid BioavailabilityPowder formats accounted for 59.60% of the food fortifying agents market revenue in 2025. This dominance stems from their thermal stability, extended shelf life, and compatibility with dry-mix processing lines. Quality assurance tests, including loss-on-drying and accelerated-aging protocols, confirm that vitamin and mineral powders maintain their potency under ambient conditions, making them suitable for bulk distribution.

The liquid format segment is growing at a CAGR of 12.22%, driven by increasing demand for fortified beverages and shots. Liquid formulations, including suspensions, emulsions, and nano-dispersion technologies, demonstrate enhanced nutrient absorption and higher bioavailability compared to powder formats. In June 2024 Singapore has established a USD 14.8 million precision fermentation center, signaling strong institutional commitment to microbial production of vitamin-rich liquids. The remaining market segment comprises tablets, gummies, and encapsulates, with emerging technologies like self-assembling nanoparticles offering controlled release properties. While powder formats maintain their market position due to cost-effectiveness, heat resistance, and bulk transport advantages, the nutritional benefits and convenience of liquid formats continue to reshape the food fortifying agents market distribution.

Geography Analysis

North America Food Fortifying Agents Market

North America held 32.60% of global sales in 2025, supported by FDA guidance on nutrient addition and labeling requirements. The United States maintains high volumes through flour, cereal, and beverage fortification, while Canada's standardized regulations facilitate ingredient trade. Mexico's participation in USMCA enhances regional sourcing capabilities and provides scale benefits to processors. The region's growth focuses on personalized beverages, brain-health formulations, and vegan fortification blends.

APAC Food Fortifying Agents Market

Asia-Pacific shows 11.95% CAGR through 2031, supported by government initiatives and increased health awareness among middle-class consumers. India's rice fortification program targets 65% of the population with vitamin B12, iron, and folic acid supplementation to address anemia. China develops biotech capabilities for omega-3 and vitamin production, while Japan's FOSHU system validates probiotic and prebiotic applications. South Korea utilizes its dairy and fermented-food expertise in lactic-acid-bacteria fortification, as demonstrated by LG H&H's FGO-based children's product launch in June 2025. ASEAN countries implement unified fortification guidelines for noodles and edible oils.

EMEA and LATAM Food Fortifying Agents Market

Europe maintains moderate growth based on clear regulations and consumer preference for natural, sustainable ingredients. Latin America, the Middle East, and Africa show gradual growth through public-health initiatives and NGO-supported staple-food fortification programs. These regional developments contribute to the food fortifying agents market's global presence with distinct regional growth factors.

Competitive Landscape

The food fortifying agents market demonstrates a fragmented competitive structure, where both established companies and new entrants compete for market share through product differentiation and technological innovations. Companies are increasingly focusing on technological advancements, particularly in microencapsulation, precision fermentation, and delivery systems to improve nutrient bioavailability and stability. Major players in the market include BASF SE, DSM-Firmenich AG, Cargill Incorporated, Archer-Daniels-Midland Company, and Kerry Group plc.

Major players are implementing vertical integration strategies to maintain supply chain control and ensure consistent quality standards. In contrast, smaller companies concentrate on niche segments, including organic fortification, plant-based nutrients, and personalized nutrition solutions. The complex regulatory environment surrounding fortification creates entry barriers that benefit established companies with proven compliance track records and technical knowledge.

The industry is witnessing an increase in innovation partnerships, as exemplified by Cargill and ENOUGH's expanded collaboration in February 2024. This partnership aims to develop nutritious and sustainable alternative meat and dairy products, with Cargill investing in ENOUGH's Series C funding round and securing a commercial agreement to utilize and market its fermented protein. Innovation through partnerships, including university collaborations and supplier-manufacturer development projects, helps companies manage risks and accelerate product launches.

Food Fortifying Agents Industry Leaders

-

BASF SE

-

DSM-Firmenich AG

-

Cargill, Incorporated

-

Archer-Daniels-Midland Company

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Food Fortifying Agents Market Companies Covered in this Report

- BASF SE

- DSM-Firmenich AG

- Cargill, Incorporated

- Archer-Daniels-Midland Company

- Kerry Group plc

- International Flavors & Fragrances, Inc.

- Ingredion Incorporated

- Tate and Lyle PLC

- Nestle S.A.

- CHR. Hansen Holding

- Kalsec Inc.

- Eastman Chemical Company

- Kemin Industries

- Glanbia PLC

- Univar Solutions LLC.

- Corbion NV

- Stern-Wywiol Group

- Arla Foods Ingredients

- Givaudan SA

- Prinova Group

Recent Industry Developments in Food Fortifying Agents Market

- May 2025: Xampla developed a plant-based microencapsulation technology for Vitamin D fortification in food and beverages. The technology utilizes pea protein to create microscopic capsules that protect Vitamin D from degradation during processing, storage, and digestion, maintaining its stability and bioavailability.

- December 2024: Bühler has joined Millers for Nutrition, a coalition that helps millers fortify staple foods. The company provides technology, expertise, and training to support customers in wheat flour, maize milling, rice, and extrusion with fortification solutions. The coalition assists millers in Bangladesh, Ethiopia, India, Indonesia, Kenya, Nigeria, Pakistan, and Tanzania in fortifying wheat and maize flours, edible oil, and rice.

- September 2024: dsm-firmenich launched dry vitamin A Palmitate NI a stable, clean-label solution for addressing vitamin A deficiency through flour fortification, highlighting the industry's focus on stability and bioavailability improvements.

- January 2024: Evonik Industries introduced VITAPUR, a new range of water-soluble vitamins for food and beverage fortification in the Asia-Pacific region. The product aims to enhance the nutritional value of various food products, addressing the increasing demand for fortified foods to combat micronutrient deficiencies and improve health outcomes in the region.

Global Food Fortifying Agents Market Report Scope

Fortifying food agents include vitamins and minerals and, in some cases, essential amino acids and proteins, which help boost their nutritional value and benefit health. The global food fortifying agents market has been segmented by types, which include proteins & amino acids, vitamins, lipids, prebiotics & probiotics, carbohydrates, minerals, and others. Based on application, the market is segmented into infant formula, dairy & dairy-based products, cereals & cereal-based products, fats & oils, beverages, dietary supplements, and others, and by geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers market size and forecasts for food fortifying agents in Value (USD million) for all the above segments.

Segmentation Overview

By Type

| Proteins and Amino Acids |

| Vitamins |

| Lipids |

| Prebiotics and Probiotics |

| Minerals |

| Carbohydrates |

| Others |

By Form

| Powder |

| Liquid |

| Others |

By Application

| Dairy and Dairy-Based Products |

| Beverages |

| Infant Formula and Early-Life Nutrition |

| Cereals and Bakery |

| Dietary Supplements |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Proteins and Amino Acids | |

| Vitamins | ||

| Lipids | ||

| Prebiotics and Probiotics | ||

| Minerals | ||

| Carbohydrates | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Application | Dairy and Dairy-Based Products | |

| Beverages | ||

| Infant Formula and Early-Life Nutrition | ||

| Cereals and Bakery | ||

| Dietary Supplements | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the food fortifying agents market?

The market is valued at USD 112.92 billion in 2026 and is projected to reach USD 180.97 billion by 2031.

Which ingredient type holds the largest share?

Vitamins lead with 31.35% of 2025 revenue, driven by longstanding regulatory adoption in staple-food programs.

Which application segment is expanding the fastest?

Beverages are growing at 12.74% CAGR through 2031 as consumers seek on-the-go nutrition in ready-to-drink formats.

Why is Asia-Pacific the fastest-growing region?

Large-scale mandates such as India’s rice fortification and rising middle-class health awareness are pushing Asia-Pacific to a 11.95% CAGR.

Page last updated on: