Food Texture Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

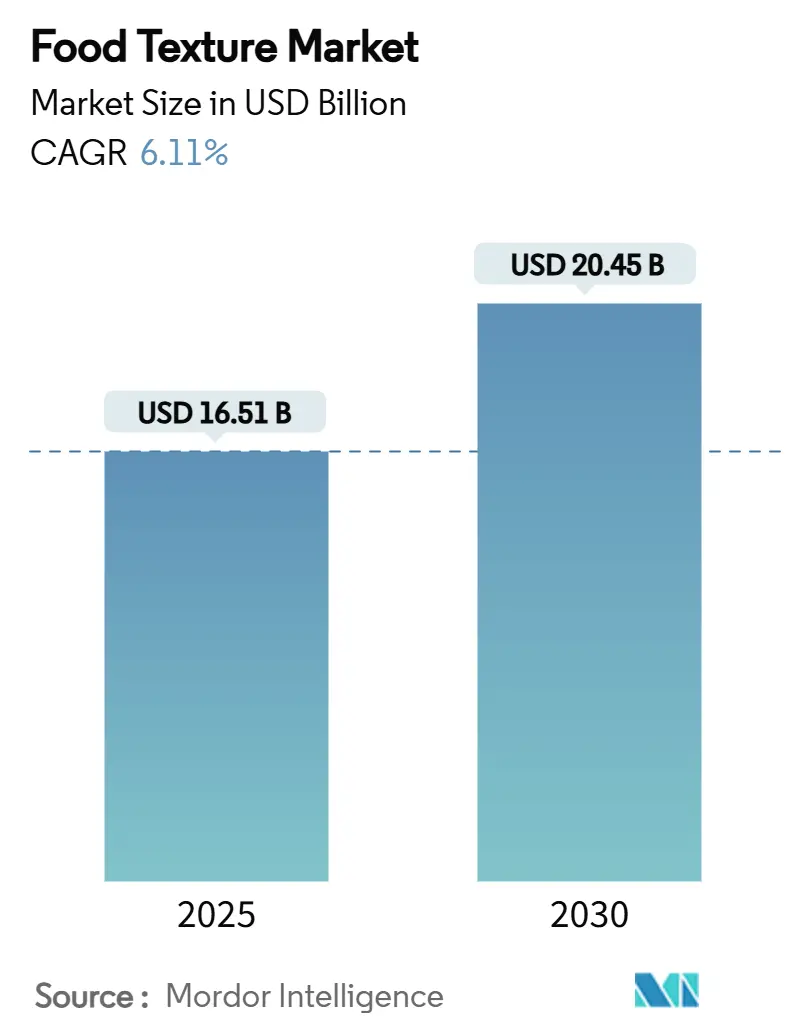

| Market Size (2025) | USD 16.51 Billion |

| Market Size (2030) | USD 20.45 Billion |

| Growth Rate (2025 - 2030) | 6.11% CAGR |

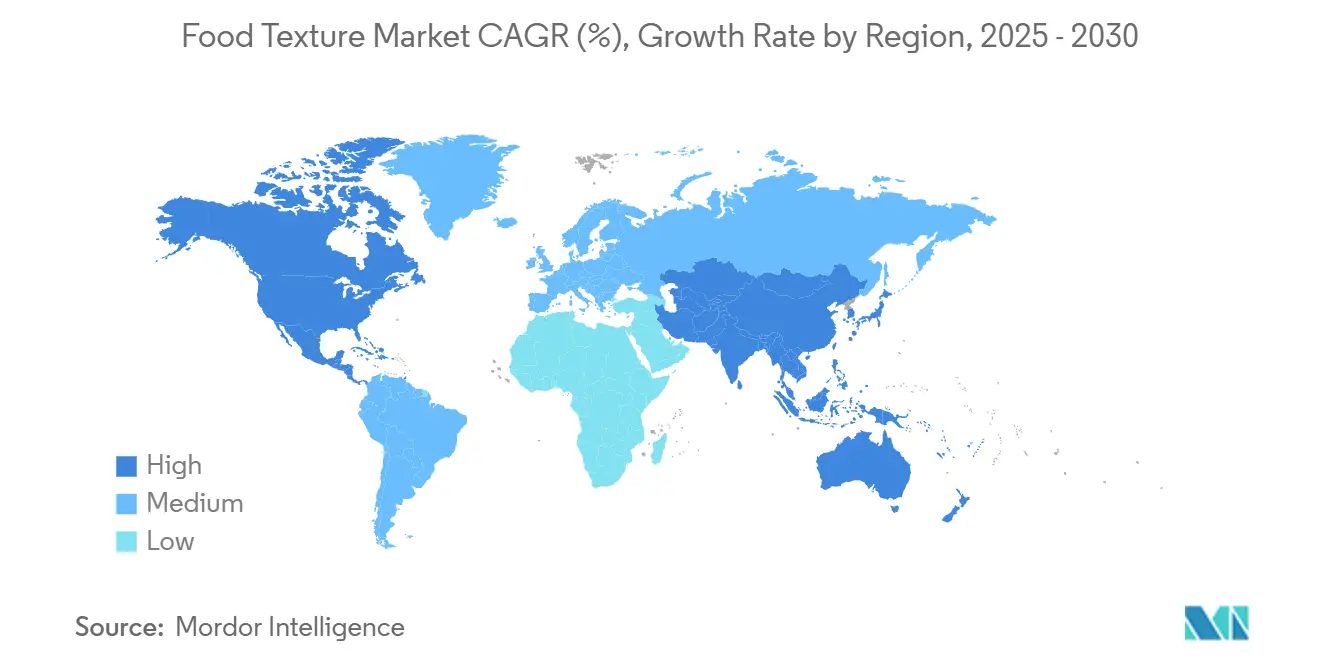

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Texture Market Analysis by Mordor Intelligence

The food texture market size is valued at USD 16.51 billion in 2025 and is forecast to climb to USD 20.45 billion by 2030, reflecting a 6.11% CAGR during the period. Clean-label reformulation, bio-synthetic production methods, and precision-engineered texture systems underpin this expansion, as manufacturers align portfolios with consumer demand for recognizable ingredients and premium sensory experiences. Regulatory approvals for natural alternatives such as fibrillated cellulose demonstrate how novel texturizers gain entry into multiple food categories while supporting fiber fortification and sustainability narratives. Strategic investments in AI-driven formulation platforms shorten development cycles and enable rapid customization, providing a competitive edge to suppliers that combine data science with ingredient expertise. At the same time, climate-driven shortages of seaweed extracts amplify interest in precision fermentation, where controlled microbial processes deliver consistent quality and mitigate raw material volatility

Key Report Takeaways

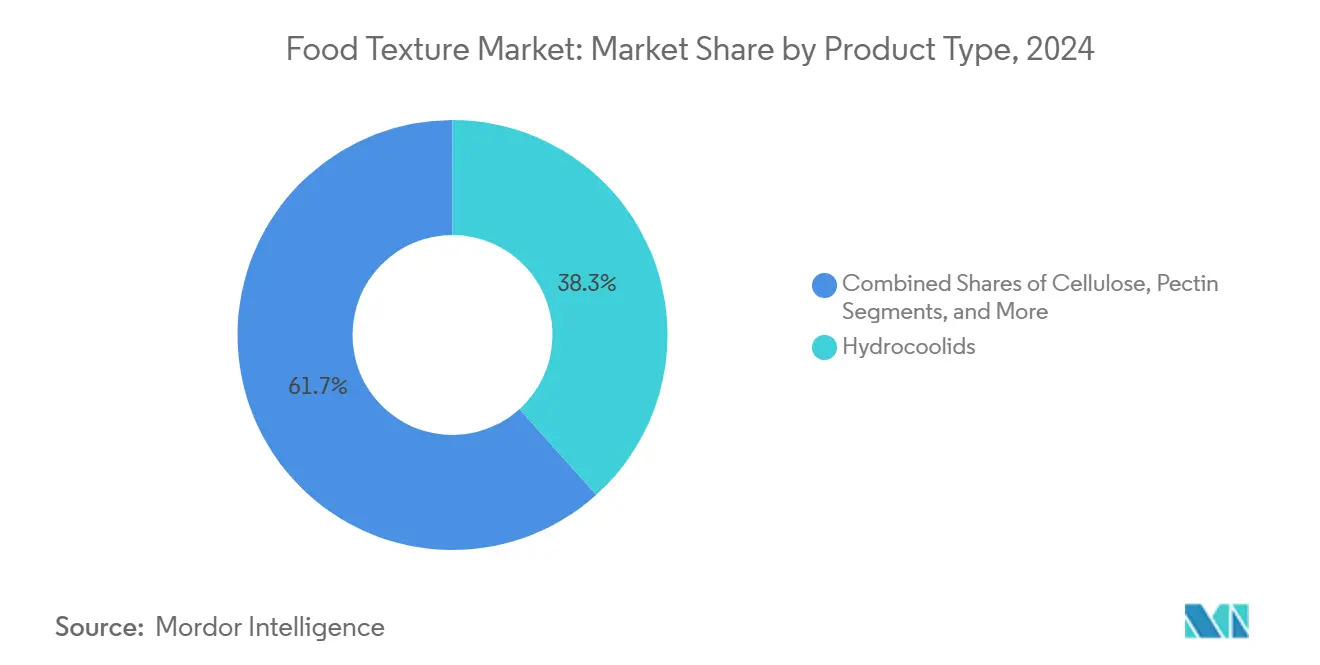

- By product type, hydrocolloids led with 38.34% food texture market share in 2024 and starch and derivatives are projected to post the fastest 7.12% CAGR through 2030.

- By source, plant-based ingredients accounted for 53.89% of the 2024 market while bio-synthetic and precision-fermented texturizers are poised for the highest 7.50% CAGR from 2025-2030.

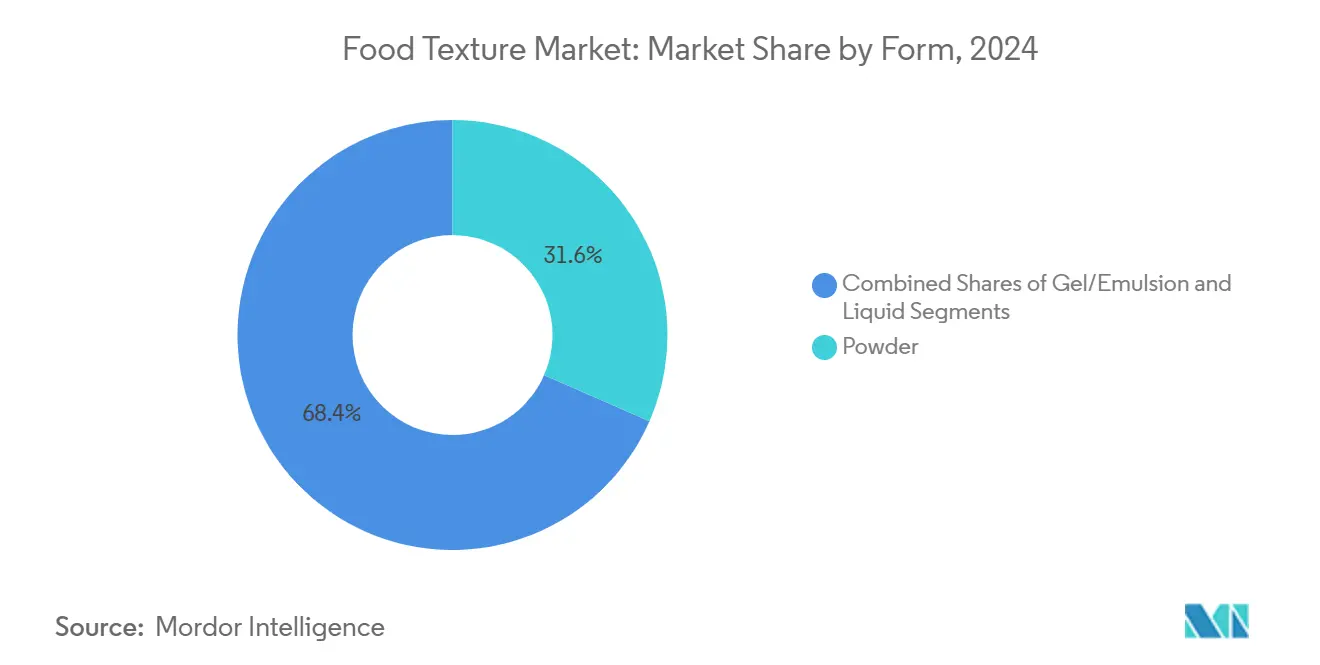

- By form, powder captured 31.57% share in 2024; gel and emulsion formats are forecast to expand at 7.11% CAGR to 2030 in response to ready-to-use processing advantages.

- By application, bakery and confectionery held 34.44% of the food texture market size in 2024 and is advancing at a 7.23% CAGR through 2030, sustaining dual leadership on both metrics.

- By geography, North America dominated with 53% share in 2024, while Asia-Pacific is expected to log the fastest 7.89% CAGR between 2025-2030.

Global Food Texture Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean label and natural ingredients | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Growth of convenience and processed foods | +1.5% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Growing awareness of sensory experience in food | +1.2% | Global, particularly premium segments in developed markets | Short term (≤ 2 years) |

| Functional benefits in shelf-life and sensory appeal | +0.9% | Global, with emphasis on emerging markets | Medium term (2-4 years) |

| Enzyme-enabled in-situ texture modification | +0.7% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| AI-driven formulation platforms shorten research and development cycles | +0.5% | North America and Europe, early adoption in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean label and natural ingredients

The shift in consumer preferences toward recognizable ingredients has changed how manufacturers select texturizers, leading to a transition from chemically modified starches to native alternatives that provide similar functionality. Under current Europe and United Kingdom regulations, any substance classified as a food additive, including natural plant extracts with technological functions, requires authorization. This regulatory framework has increased the adoption of established natural texturizers. Companies such as Beneo-Remy and Cargill have developed native rice and corn starches that match the performance of chemically modified variants. The trend has expanded to include hydrocolloids, where manufacturers use enzyme-assisted extraction methods to enhance functionality while maintaining natural ingredient status. The GRAS (Generally Recognized as Safe) approval of fibrillated cellulose demonstrates how natural texturizers can function as rheology modifiers, stabilizers, and fiber supplements while meeting clean-label requirements.

Growth of convenience and processed foods

The growth in ready-to-eat meals and packaged food segments drives consistent demand for texturizers that preserve product quality during extended shelf life periods and various storage conditions. The Asia-Pacific region demonstrates significant growth in convenience food consumption, driven by urbanization and lifestyle changes that increase processed food demand. Hydrocolloids, including xanthan gum and pectin, are crucial for maintaining texture and stability in dairy and frozen food products, particularly where temperature variations can affect product quality. The expansion of the processed food industry creates opportunities for specialized texturizers that address specific challenges, such as preventing ice crystal formation in frozen desserts and maintaining emulsion stability in shelf-stable sauces. The microbial gums market has developed to meet these requirements, with growth potential in traditional applications and new uses, including biodegradable packaging and prebiotic ingredients.

Growing awareness of sensory experience in food

Manufacturers recognize that texture perception involves interactions between mechanical properties, temperature, and flavor release, increasing the demand for texturizer combinations that enhance sensory experiences. Research shows that mouthfeel includes attributes perceived through physical and chemical sensations, with cultural backgrounds influencing consumer preferences. The implementation of AI-driven sensory prediction models helps manufacturers optimize texture formulations using consumer preference data, reducing development time and improving market acceptance rates. Food companies use robotic sensing systems to evaluate gel-like food textures through convolutional neural networks, achieving correlation coefficients above 0.92 with human sensory evaluations. This technological advancement demonstrates the industry's shift from basic stabilization functions to engineered sensory experiences that differentiate products in the market.

Functional benefits in shelf-life and sensory appeal

Texturizers serve multiple functions by extending product shelf life and enhancing sensory attributes, enabling manufacturers to command premium pricing in competitive food categories. Hydrocolloids are particularly effective in fruit-based products, where they improve textural stability, thermal properties, and nutritional retention while providing thickening, gelling, and encapsulation functions. The FDA's approval of various hydrocolloids as safe food additives enables their use across multiple food categories, allowing manufacturers to achieve functional and sensory goals with individual ingredients. Enzyme-assisted extraction methods for seaweed hydrocolloids improve quality and functionality while reducing chemical usage. Modern texturizer formulations help maintain product quality through retort treatment and extended storage periods, with transglutaminase-treated products exhibiting only 20% reduction in breaking strength compared to untreated alternatives after thermal processing.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of hydrocolloids & starches | -1.4% | Global, with acute impact on cost-sensitive segments | Short term (≤ 2 years) |

| Stringent regulatory approvals for novel additives | -0.8% | EU & North America, expanding to APAC markets | Medium term (2-4 years) |

| Climate-driven shortages of specialty seaweed extracts | -0.6% | Global, particularly affecting agar and carrageenan supply | Long term (≥ 4 years) |

| Consumer push-back on mouthfeel enhancers in sugar-reduced SKUs | -0.4% | North America & EU, emerging in health-conscious segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile prices of hydrocolloids and starches

Raw material price volatility creates significant margin pressure for texturizer manufacturers, with agar prices reaching USD 35-45 per kilogram due to supply restrictions in Morocco, nearly triple previous pricing levels. The Moroccan government's reduction in legal Gelidium seaweed harvest from 14,000 tonnes to 6,000 tonnes annually, combined with export limitations of 1,200 tonnes, has created acute shortages affecting both food and laboratory applications. Major suppliers like Thermo Fisher Scientific have suspended raw agar sales, prioritizing other products due to competition from food companies that consume several thousand tonnes annually. This supply-demand imbalance forces manufacturers to seek alternative texturizers or accept higher input costs that reduce profitability. The Indonesian seaweed supply chain faces additional challenges, including poor quality of raw dried seaweed, currency exchange rate fluctuations, and uncertainty in seaweed yields, creating compound volatility effects.

Consumer push-back on mouthfeel enhancers in sugar-reduced SKUs

Sugar reduction significantly alters texture, melting rates, and overall product quality in categories like chocolate, ice cream, and bakery products. This necessitates the use of texturizers, but consumer resistance to artificial mouthfeel enhancement in sugar-reduced products creates formulation challenges. While pectin can enhance mouthfeel in sugar-reduced beverages without affecting taste or aroma, its effectiveness varies by beverage type and consumer acceptance remains variable. The challenge is particularly significant in confectionery applications, where sugar provides essential functional properties beyond sweetness, including texture, structure, and preservation. Manufacturers must balance technical requirements with consumer preferences, often implementing gradual reformulation strategies to maintain product acceptance while meeting sugar reduction goals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hydrocolloids Lead Despite Starch Innovation

Hydrocolloids hold the dominant market position with a 38.34% share in 2024, due to their versatility in creating stable emulsions, gels, and foams across food applications. The starch and derivatives segment is projected to grow at 7.12% CAGR (2025-2030), supported by innovations in clean-label formulations that maintain functional performance without chemical modifications. Companies such as Ingredion and Cargill have developed native starch blends that provide functionality comparable to modified variants, meeting consumer preferences for simple ingredients.

While gelatin experiences competition from plant-based substitutes, it remains essential in premium applications requiring specific gel strength and thermal reversibility. Pectin continues to grow in fruit-based products and sugar-reduced formulations, where its natural gelling properties support clean-label requirements. Protein-based texturizers are increasing in plant-based meat alternatives, with transglutaminase enabling improved texture and water-holding capacity through cross-linking. Cellulose derivatives have expanded their application range following FDA[1]U.S. Food and Drug Administration, "GRAS Notice for Fibrillated Cellulose", fda.govapproval of fibrillated cellulose as a multifunctional ingredient that serves as a rheology modifier, stabilizer, and fiber supplement.

By Source: Plant-Based Dominance Challenged by Bio-Synthetic Innovation

Plant-based sources hold a 53.89% market share in 2024, driven by consumer preference for natural ingredients and well-established supply chains for seaweed, plant gums, and starch derivatives. According to the United States Department of Agriculture data from 2023[2]United States Department of Agriculture, "Plant Based Food Consumption in Germany", fas.usda.gov, 1.58 million people in Germany adopted plant-based diets, reflecting a significant shift in dietary preferences. Bio-synthetic and precision-fermented texturizers are emerging as the fastest-growing source category with a 7.50% CAGR (2025-2030). This growth stems from technological advancements that enable the production of complex molecules without traditional agriculture. Companies are developing precision fermentation systems to produce ice-structuring proteins and specialized texturizers that offer enhanced functionality compared to plant-derived options.

Animal-based sources experience declining demand due to dietary restrictions and sustainability concerns, though they remain important for specific applications requiring distinct functional properties. Microbial and fermentation-derived texturizers offer advantages in scalability and quality consistency, addressing supply chain vulnerabilities that affect seaweed-based hydrocolloids. The industry's transition toward bio-synthetic sources responds to climate-related supply disruptions while meeting consumer demand for sustainable production methods that minimize environmental impact and maintain product performance.

By Form: Powder Convenience Versus Gel Innovation

Powder form maintains the largest market share at 31.57% in 2024, driven by handling convenience, extended shelf life, and cost-effective transportation that appeals to food manufacturers seeking operational efficiency. Gel and emulsion forms emerge as the fastest-growing segment at 7.11% CAGR (2025-2030), reflecting demand for ready-to-use solutions that simplify manufacturing processes and reduce formulation complexity. These pre-hydrated forms enable precise dosing and immediate functionality, particularly valuable in applications requiring consistent texture delivery.

Liquid forms serve specialized applications where immediate dispersion is critical, though they face limitations in shelf stability and transportation costs that constrain broader adoption. The gel and emulsion segment benefits from advances in stabilization technology that extend shelf life while maintaining functional properties, addressing previous limitations that restricted market penetration. Manufacturers increasingly offer customized form factors that match specific application requirements, with some developing hybrid solutions that combine powder convenience with liquid functionality through innovative packaging systems.

By Application: Bakery Dominance Across Metrics

Bakery and confectionery applications dominate the market with a 34.44% share in 2024 and are projected to grow at a 7.23% CAGR from 2025 to 2030. This growth stems from continuous innovation in texture enhancement and clean-label reformulation. The use of transglutaminase in bakery products improves dough rheological properties and final product quality. The segment's growth is supported by consumers' willingness to pay premium prices for enhanced texture in indulgent food categories. Dairy and frozen desserts utilize hydrocolloids to prevent ice crystal formation and maintain smooth mouthfeel during temperature changes.

Meat and poultry alternatives incorporate protein-based texturizers to replicate animal protein textures through cross-linking mechanisms. The beverage industry requires texturizers that maintain stability across various pH ranges and storage conditions while preserving flavor profiles. Snacks and ready-to-eat meals need texturizers that preserve product integrity throughout shelf life. Sauces, dressings, and condiments use emulsifying texturizers to prevent separation and ensure consistent texture. Infant and clinical nutrition products require texturizers that meet safety and nutritional standards while providing appropriate texture for specific dietary needs.

Geography Analysis

North America holds 53.00% market share in 2024, supported by robust regulatory frameworks that enable innovation while maintaining safety standards, as shown by the FDA's GRAS notification system for novel texturizers like fibrillated cellulose. The region's advanced food processing infrastructure and consumer acceptance of premium texture-enhanced products create optimal conditions for high-value texturizer applications. Ingredion's USD 100 million Indianapolis facility expansion reflects industry confidence in the North American market, with strong performance in its Texture & Healthful Solutions segment throughout 2024. The region's focus on clean-label products drives demand for native starches and natural hydrocolloids that provide functionality while meeting consumer preferences for recognizable ingredients.

Asia-Pacific exhibits the fastest growth rate at 7.89% CAGR (2025-2030), driven by increased processed food consumption, urbanization, and improved regulatory harmonization. The region's nutraceutical market, expected to reach USD 441.7 billion by 2026, presents opportunities for functional texturizers that combine sensory and health benefits. Japan's Foods with Function Claims system demonstrates regulatory progress that supports innovation while protecting consumers. China and India emerge as key markets due to their large consumer bases and expanding middle-class populations seeking premium processed foods with advanced texture solutions.

Europe maintains a strong market position through strict regulatory standards that support established natural texturizers while regulating novel additives. The EFSA's[3]Centre for the Promotion of Imports, "Natural Food Additive Sourcing Trends", cbi.eu food additive re-evaluation program sets international benchmarks while ensuring market confidence in hydrocolloid safety. European purchasers demand sustainability certifications and traceability, creating opportunities for suppliers demonstrating responsible practices. The region's focus on sustainability and clean-label products aligns with developments in precision fermentation for texturizer production. South America and Middle East & Africa offer growth potential through developing food processing industries and increasing consumer sophistication, though regulatory complexities and infrastructure limitations affect market development and cost efficiency.

Competitive Landscape

The food texture market shows moderate fragmentation, enabling both established companies and new technology specialists to gain market share through differentiated positioning. Major companies such as Ingredion, Kerry Group, and dsm-firmenich maintain their positions through vertical integration, global distribution networks, and comprehensive product portfolios serving multiple food categories. dsm-firmenich's Taste, Texture & Health segment achieved 6% sales growth in H1 2024, reflecting successful merger integration and expanded technological capabilities.

The industry continues to consolidate, as evidenced by Tate & Lyle's USD 1.8 billion proposed acquisition of CP Kelco, which aims to strengthen capabilities in sweetening, mouthfeel, and fortification solutions aligned with health and sustainability trends. New market entrants differentiate themselves through precision fermentation and AI-driven formulation platforms that improve product development efficiency while reducing costs and environmental impact compared to conventional extraction methods. Companies implementing machine learning in food product design gain competitive advantages by using genetic algorithms and mechanistic modeling to predict sensory characteristics and optimize textures.

Market opportunities exist in bio-synthetic texturizers, particularly as alternatives to seaweed-based hydrocolloids affected by supply chain vulnerabilities. These vulnerabilities, driven by climate-related shortages and regulatory restrictions, have increased agar prices to USD 35-45 per kilogram. Companies that integrate traditional expertise with digital capabilities gain advantages in rapid formulation development and customized solutions while maintaining regulatory compliance across global markets.

Food Texture Industry Leaders

-

Cargill Inc.

-

International Flavors and Fragrances Inc.

-

Tate and Lyle Plc

-

Ingredion Incorporated

-

Kerry Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: At the Frankfurt IFFA trade fair, Sarda Bio Polymers introduced clean-label, plant-based hydrocolloid solutions for meat and alternative protein applications. Their offerings include guar gum, cassia tora gum, konjac, xanthan, carrageenan, tamarind xyloglucan, and CMC, designed to enhance texture with minimal processing while emphasizing sustainability and performance.

- March 2025: Cargill opened a new corn milling plant in Gwalior, Madhya Pradesh, operated by Indian manufacturer Saatvik Agro Processors, to meet increasing demand from India's confectionery, infant formula, and dairy industries.

- March 2025: Ingredion partnered with Austrian company Agrana to increase starch production in Romania, expanding its manufacturing presence in Eastern Europe to address the rising regional demand for specialty starches.

- February 2025: Linqing Deneng Golden Corn Bio Limited, a subsidiary of China Starch Holding Company, expanded its operations by opening two additional starch processing facilities. The company operates two cornstarch production lines at its existing facilities, with annual production capacities of 550,000 tonnes and 450,000 tonnes, respectively.

Global Food Texture Market Report Scope

| Hydrocolloids |

| Starch and Derivatives |

| Gelatin |

| Pectin |

| Protein-based Texturizers |

| Cellulose Derivatives |

| Plant-based |

| Animal-based |

| Microbial and Fermentation-derived |

| Bio-synthetic/Precision-fermented |

| Powder |

| Liquid |

| Gel/Emulsion |

| Bakery and Confectionery |

| Dairy and Frozen Desserts |

| Meat and Poultry Alternatives |

| Beverages |

| Snacks and Ready To Eat Meals |

| Sauces, Dressings and Condiments |

| Infant and Clinical Nutrition |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Hydrocolloids | |

| Starch and Derivatives | ||

| Gelatin | ||

| Pectin | ||

| Protein-based Texturizers | ||

| Cellulose Derivatives | ||

| By Source | Plant-based | |

| Animal-based | ||

| Microbial and Fermentation-derived | ||

| Bio-synthetic/Precision-fermented | ||

| By Form | Powder | |

| Liquid | ||

| Gel/Emulsion | ||

| By Application | Bakery and Confectionery | |

| Dairy and Frozen Desserts | ||

| Meat and Poultry Alternatives | ||

| Beverages | ||

| Snacks and Ready To Eat Meals | ||

| Sauces, Dressings and Condiments | ||

| Infant and Clinical Nutrition | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the food texture market?

The market stands at USD 16.51 billion in 2025 and is projected to reach USD 20.45 billion by 2030.

Which product category holds the largest share?

Hydrocolloids lead with 38.34% share in 2024 due to their versatility across multiple food systems.

Which region is growing fastest?

Asia-Pacific is forecast to record a 7.89% CAGR between 2025-2030 as urbanization drives higher processed-food adoption.

Why are precision-fermented texturizers gaining attention?

They offer consistent quality and reduce dependence on climate-sensitive crops, supporting a 7.50% CAGR for the bio-synthetic segment.

Page last updated on: