Film and TV Production Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

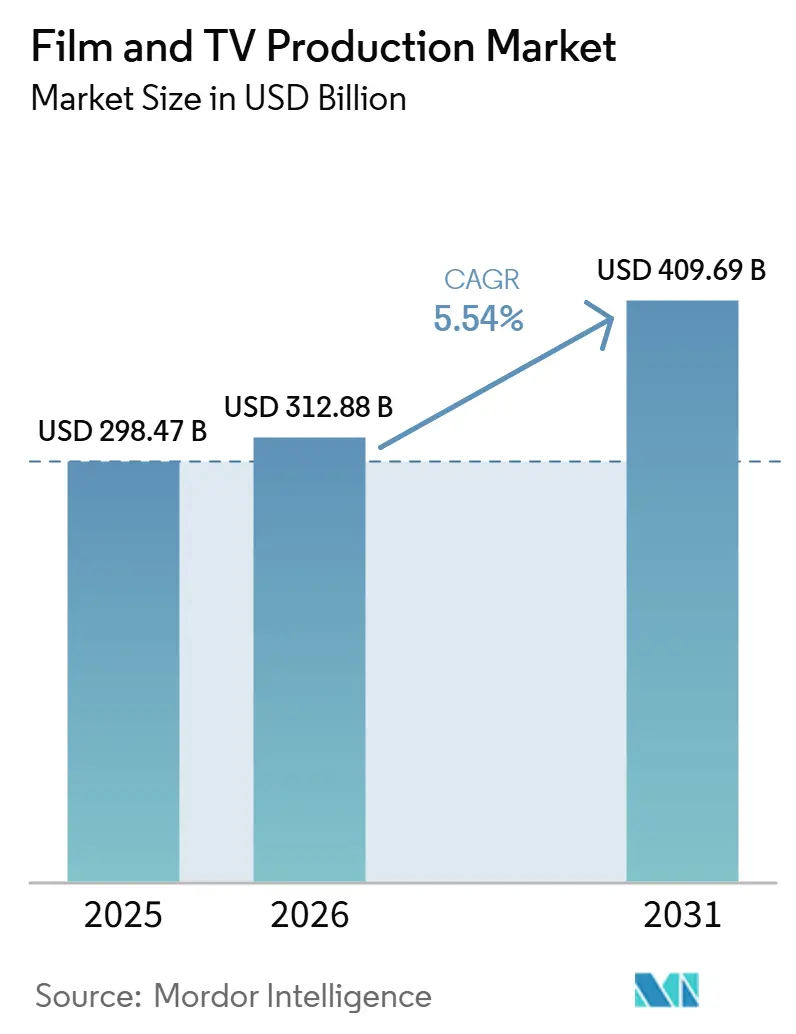

| Market Size (2026) | USD 312.88 Billion |

| Market Size (2031) | USD 409.69 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Film and TV Production Market Analysis by Mordor Intelligence

The Film and TV Production Market size is expected to increase from USD 298.47 billion in 2025 to USD 312.88 billion in 2026 and reach USD 409.69 billion by 2031, growing at a CAGR of 5.54% over 2026-2031. The film and TV production market enters 2026 with stronger visibility on commissioned content pipelines as financing and rights ownership continue to shift toward platform-led ordering models. Feature output remains supportive because global title production stayed above the pre-pandemic baseline, which keeps crews, facilities, and service vendors active across more territories. The film and TV production market is also drawing more value from post-production workflows as finishing, visual effects, and delivery complexity absorb a larger share of project budgets. Corporate consolidation is reshaping the film and Television production market as major media groups pursue scale, library depth, and tighter control of production infrastructure. At the same time, the film and Television production market continues to face pressure from multi-year wage escalation and uneven financing access for mid-budget projects, which raises execution risk even when underlying demand remains intact.

Key Report Takeaways

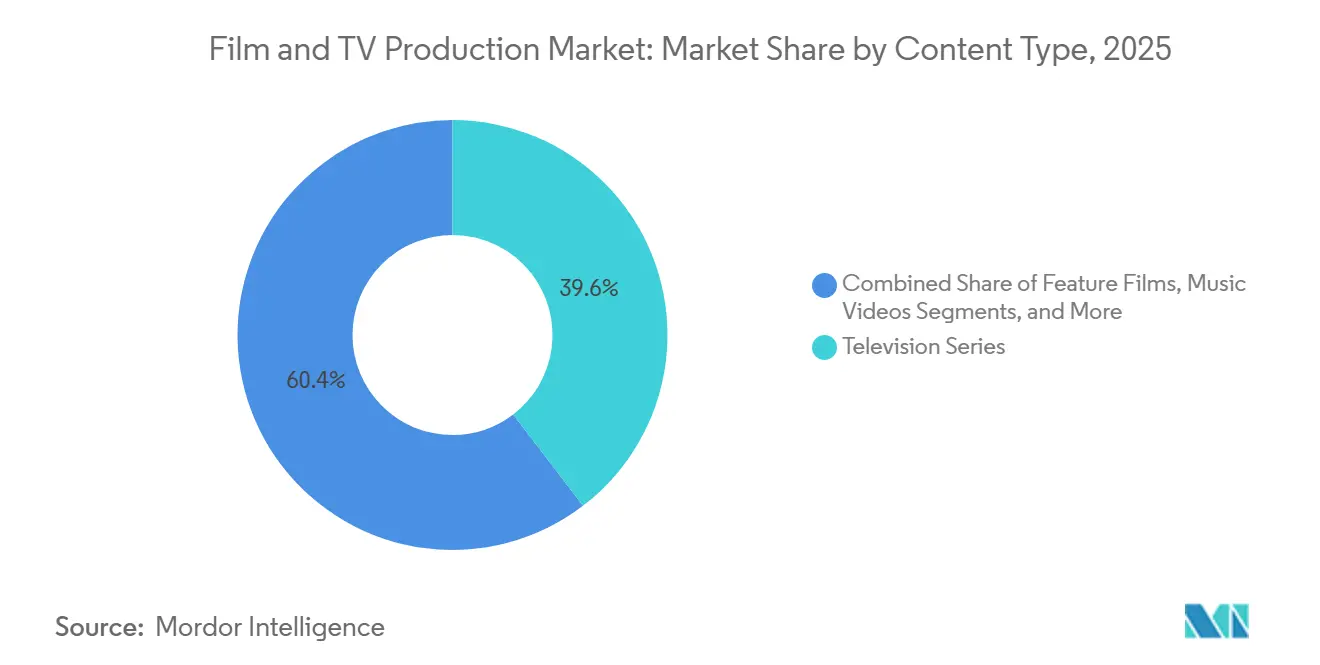

- By content type, television series held 39.62% share of the film and TV production market in 2025, while documentary and non-fiction is projected to expand at a 9.87% CAGR through 2031.

- By production stage, production accounted for 53.22% of the film and TV production market size in 2025, while post-production is projected to grow at an 8.76% CAGR through 2031.

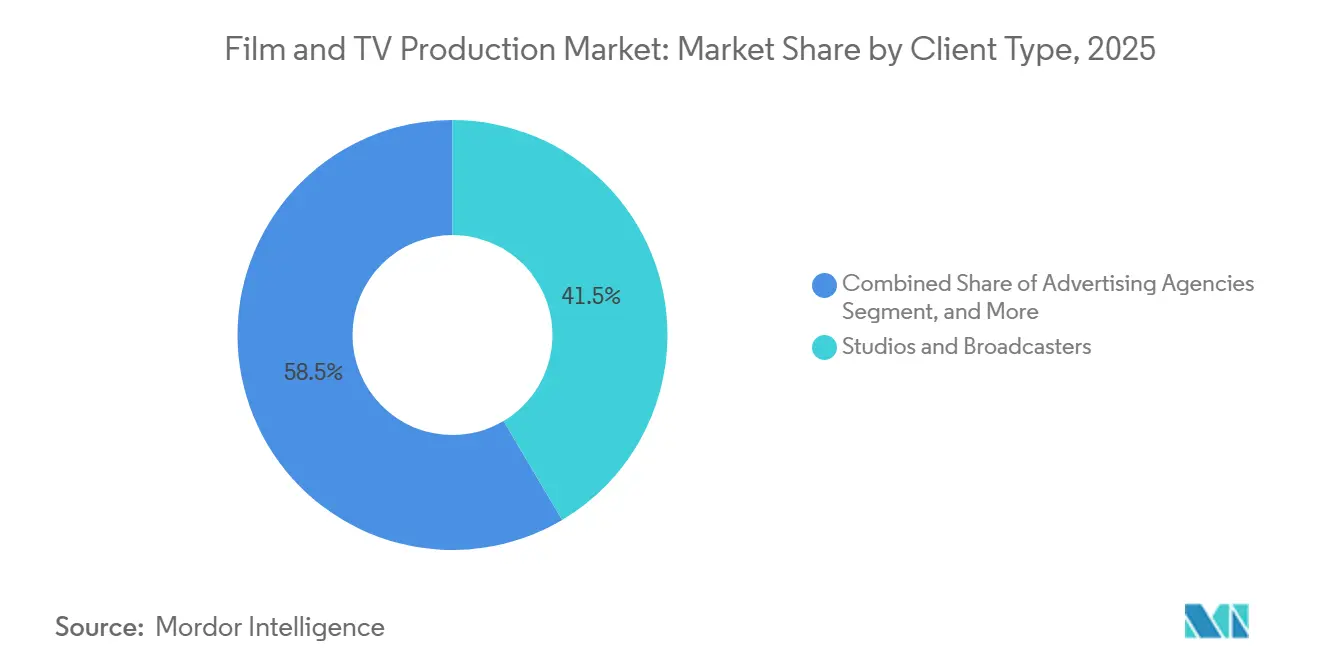

- By client type, studios and broadcasters held 41.48% of the film and TV production market share in 2025, while streaming platforms are projected to expand at a 9.29% CAGR through 2031.

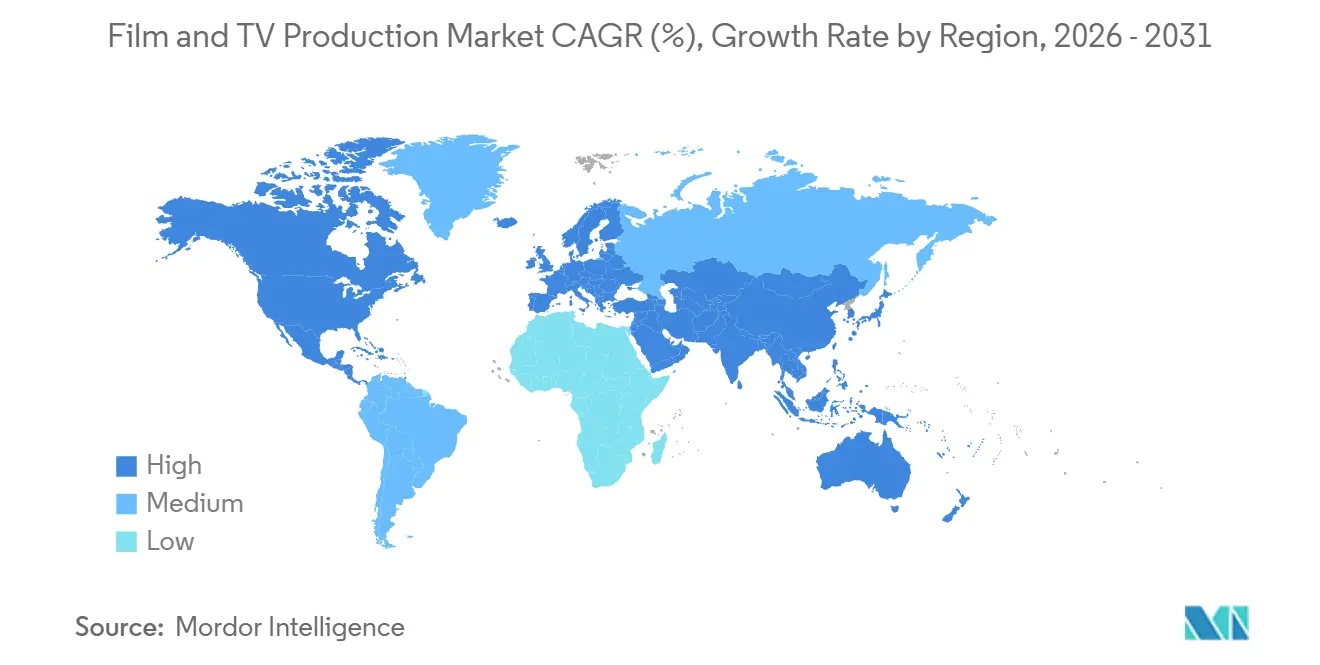

- By geography, North America accounted for 37.21% of the film and TV production market size in 2025, while Asia-Pacific is projected to advance at a 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Film and TV Production Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Streaming-First Commissioning | +1.5% | Global | Medium term (2-4 years) |

| Rising Demand for High-Value Localized Content | +1.2% | APAC, South America, Middle East | Medium term (2-4 years) |

| Virtual Production Adoption in Studio Workflows | +0.9% | North America, Europe, APAC | Medium term (2-4 years) |

| Growth of Premium Post-Production and VFX Outsourcing | +0.7% | India, UK, North America | Medium term (2-4 years) |

| Faster Greenlight Cycles Enabled by Data-Driven Development | +0.4% | North America, Europe | Short term (≤ 2 years) |

| Demand for Cross-Platform Content Packages | +0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Streaming-First Commissioning

The shift from broadcast-first to streaming-first ordering has created a steadier base of demand for the film and TV production market than existed before 2020. Large platforms increasingly commission titles with global rights from the outset, which lowers sales-market uncertainty for producers but gives buyers stronger control over pricing and ownership. That model supports earlier budgeting decisions and keeps crews, facilities, and post houses engaged across longer planning cycles. It also favors producers that can deliver consistent execution across several territories and across repeat seasons or linked franchises. Independent production companies still benefit from clearer funding visibility, but they now operate in a system where more of the long-tail value sits with the commissioning platform. In the film and Television production market, this commissioning structure has become a durable growth support even when individual platforms adjust title counts from one year to the next.

Rising Demand for High-Value Localized Content

Demand for localized titles is rising because audiences stay engaged longer with stories that reflect language, culture, and regional context. That shift has widened the addressable base of the film and TV production market beyond legacy English-language production centers and into regional commissioning hubs. South Korea's audiovisual sector generated KRW 23,080 billion (USD 16.8 billion), across television, film, and VOD in 2024, which shows how local IP can support both domestic scale and export reach.[1]Motion Picture Association APAC, “The Economic Contribution of the Audiovisual Industry in South Korea,” MPA APAC, mpa-apac.org The same pattern strengthens co-productions, rights partnerships, and repeat work for regional suppliers that can deliver culturally specific content at a premium standard. Localized production is no longer only a market-entry tool for distributors because it now supports subscriber retention and catalog depth over time. As that shift continues, the film and TV industry gains a broader and more resilient pipeline of commissioned content.

Virtual Production Adoption in Studio Workflows

Virtual production is moving into standard studio workflow because it improves schedule control, reduces location dependence, and supports more predictable shoot planning. Producers are increasingly designing new facilities around LED volumes instead of treating them as experimental add-ons. Entertainment Partners noted in 2026 that the Council of Europe's co-production treaty created the first legal framework tailored to international TV and streaming series, which helps streamline multi-country production structures across many participating nations.[2]Entertainment Partners, “Film and TV Production Outlook 2026: Tax Incentives, Audience Demand and Where Production Is Heading,” Entertainment Partners, ep.com That legal clarity matters because virtual production often links financing, talent, design, and delivery work across several jurisdictions at once. Newer content hubs can integrate these capabilities from the start, which reduces the retrofit burden that older studio lots often face. In the film and TV production industry, adoption is strongest where new infrastructure, public incentives, and cross-border production rules are aligning at the same time.

Growth Of Premium Post-Production and VFX Outsourcing

Post-production is taking a larger share of project value as premium titles rely on heavier VFX, more finishing work, and tighter delivery standards across release windows. The film and TV production market therefore rewards companies that can combine scale, specialized talent, and pipeline efficiency in editing, grading, and visual effects. Framestore's 2026 rollout of its Futon platform shows how major vendors are embedding generative AI and machine learning into production pipelines while preserving provenance tracking for clients.[3]Framestore, “Theo Jones Promoted to Creative Director, AI,” Framestore, framestore.com That kind of integration helps post houses improve throughput without losing the auditability and accountability that large studios and platforms increasingly require. It also raises the competitive threshold because service partners must now pair creative capability with process control and technical transparency. As this work becomes more complex and more central to title quality, post-production capacity continues to gain strategic importance within the film and TV production market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Talent, Union, and Location Costs | -1.3% | North America and Europe | Long term (≥ 4 years) |

| Financing Volatility for Mid-Budget Projects | -0.9% | Global, most acute in North America | Medium term (2-4 years) |

| Regulatory Fragmentation Across Rights, Labor, and Content Rules | -0.6% | Europe, APAC | Long term (≥ 4 years) |

| Schedule Risk From Weather, Permits, and Production Interruptions | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Talent, Union, And Location Costs

Labor inflation is becoming a structural cost issue rather than a short-term disruption in the film and TV production market. SAG-AFTRA members ratified the 2026 TV/Theatrical Agreement with 91.42% approval, and the agreement set 3% annual minimum wage increases through June 30, 2030.[4]SAGindie, “NOTICE: SAG-AFTRA TV/Theatrical Contract Updates (2026),” SAGindie, sagindie.org These increases raise base budgeting needs for scripted projects and make established production hubs harder to justify smaller slates. Location, legal, and compliance expenses also remain elevated in Los Angeles, New York, and London, which pushes more producers toward incentive-backed secondary markets. New obligations tied to AI and digital replica usage add another layer of administrative work for productions that rely on performer-likeness tools. The result is that mid-budget titles face tighter margins even when end demand for filmed entertainment remains healthy.

Financing Volatility for Mid-Budget Projects

Financing volatility remains most severe in the USD 5-50 million budget range, where projects often depend on pre-sales, gap lenders, and staggered rights deals. In that part of the film and TV production market, buyers have become more selective on license commitments and producers face more pressure to secure meaningful attachments before final closing. The practical effect is slower deal timing and a narrower path to greenlight for projects that are too large for independent self-funding and too small for franchise economics. This pressure is reshaping development pipelines, with more producers prioritizing formats, cast packages, and territories that can travel earlier in the financing cycle. It also makes capital planning less predictable for independent companies that rely on several financing sources instead of one anchor buyer. Unless financing conditions stabilize, the pinched middle will remain the most exposed part of the film and TV production market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Television Series Anchor Value as Documentaries Accelerate

Television Series held 39.62% of the film and TV production market size in 2025, reflecting the format's central role in subscriber retention and repeat commissioning. Studios and platforms commit multi-season packages because they support steadier use of writers, cast, sets, and post-production teams over longer cycles. That continuity makes series work the most dependable volume anchor within the film and TV production market across development, principal photography, and finishing. It also gives service vendors better planning visibility because returning titles typically carry established creative teams, recurring locations, and known delivery requirements. Feature Films remain a separate value pool, and global theatrical revenue reached USD 32.8 billion in 2025 even as viewing time continued to shift toward digital platforms.

Documentary and non-fiction segment is projected to expand at a 9.87% CAGR through 2031, making it the fastest-moving content category in the film and TV production industry. For buyers, the appeal is clear because documentaries usually require lower spend per hour than premium scripted drama while still supporting strong audience engagement. The category also fits well with current platform strategies because it can address crime, sports, music, celebrity, and current affairs without the full cost structure of high-end fiction. European catalog requirements keep documentary commissioning relevant for services that need a minimum share of regional works in market-facing libraries. Commercial and branded content, music videos, and other formats round out the film and TV production market by supplying steady short form demand from advertisers, labels, and smaller content owners.

By Production Stage: Post-Production Gains Ground on the Production Core

The Production stage accounted for 53.22% of the film and TV production market size in 2025 because principal photography still absorbs the largest share of labor, equipment, and location spending. That position reflects the basic economics of filmed content, where shooting days remain the cost center that producers manage most closely. The scale of cast, crew, travel, set construction, and on-set technical support keeps this stage firmly at the center of budget planning. Even when workflows become more digital, the physical act of capture still drives the largest direct outlays across most genres. For that reason, the Production stage should remain the largest value pool within the film and TV production market through the forecast period.

Post-Production is projected to grow at an 8.76% CAGR through 2031, making it the fastest-growing stage in the film and TV production market. Growth is being supported by heavier VFX use, remote collaboration, cloud-based finishing, and the need for multiple delivery versions across platforms and territories. Pre-Production is also gaining strategic importance because data-led greenlights and virtual previsualization shift more decision-making forward before cameras roll. Framestore's AI-enabled Futon workflow illustrates how vendors are building more automated and auditable finishing pipelines for studio and streamer clients. The UK's Audio-Visual Expenditure Credit also increases the appeal of qualifying local VFX work, which supports continued outsourcing and specialized post-production investment.

By Client Type: Studios And Broadcasters Hold Share as Streamers Drive Growth

Studios and Broadcasters held 41.48% of the film and TV production market share in 2025, showing that conventional studio slates and broadcast obligations still represent the largest client pool. These base keeps demand intact for theatrical tentpoles, episodic orders, and long-cycle franchises that need full-service production support. The largest incumbents also provide a measure of continuity because their libraries, release schedules, and established distribution systems support recurring production activity through changing audience cycles. Independent Producers add meaningful volume through mid-budget films and art-house projects, even though financing conditions remain uneven in that layer of the market. Advertising Agencies also remain relevant because branded content and campaign-led production still require fast-turn creative, studio, and post-production resources.

Streaming Platforms are projected to expand at a 9.29% CAGR through 2031, making them the fastest-growing client group in the film and TV production market. Their commissioning model keeps pipeline visibility high for suppliers, but it also concentrates intellectual property ownership and pricing power with the platforms themselves. This creates a different operating logic for producers because upfront funding improves certainty, yet backend rights participation becomes more limited than in older distribution structures. The Council of Europe's 2026 convention for international TV and streaming co-production should make cross-border deal structures easier to execute for many participating countries. As that framework spreads, producers with multi-country legal, financing, and delivery capabilities will be better positioned inside the film and TV production market.

Geography Analysis

North America accounted for 37.21% of the film and TV production market size in 2025, which kept it the largest regional base by value because of studio depth in the United States and incentive support in Canada. Entertainment Partners reported that U.S. domestic ticket sales in 2026 were running more than 20% ahead of 2025, and it projected domestic box office could reach USD 9.9 billion for the year. California, New York, and New Jersey continue to underpin production planning with large annual tax credit allocations, which gives the region a durable floor for studio and location spending. The region also benefits from dense finance, agency, union, and post-production networks that are difficult for smaller ecosystems to replicate quickly. South America is building a more diversified production base, and Mexico's 2026 EFICA launch shows how the region is using fiscal policy to strengthen domestic and co-production pipelines.

Europe remains one of the largest and most structured regions in the film and TV production market, supported by dense production ecosystems and formal regulatory frameworks. The European Audiovisual Observatory reported a record 2,523 feature films across 36 markets in 2024, which confirms the region's depth of active production. The same source valued the European audiovisual market at EUR 142 billion (USD 160 billion), which keeps Europe central to financing, commissioning, and rights activity. The UK's Independent Film Tax Credit has reinforced London and nearby studio infrastructure as a preferred setting for U.S.-funded co-productions. The Middle East is moving beyond service production as Saudi Arabia and the UAE expand infrastructure and incentives. Africa is still earlier in its development curve, yet Nigeria, South Africa, and Egypt remain active hubs, and Uganda's entry into the WIPO dataset with 63 film titles in 2024 shows that regional measurement and formalization are improving.

Asia-Pacific is projected to grow at a 10.12% CAGR through 2031, making it the fastest-growing geography in the film and TV production market. South Korea's audiovisual sector generated KRW 23,080 billion, USD 16.8 billion, across television, film, and VOD in 2024, highlighting the strength of local IP and export-ready production systems. AVIA expects SVOD subscriptions in Asia-Pacific to exceed pay-TV by more than 5 to 1 by 2031, which supports a longer shift of commissioning power toward digital buyers. Taken together, India, South Korea, China, and adjacent hubs are pulling more production capital eastward and steadily expanding the geographic weight of the film and TV production market.

Competitive Landscape

The film and TV production market remains broad, but competition is tightening as capital concentrates around platforms, major studios, and scaled content groups. Netflix, Disney, Amazon, and Apple now influence commissioning, production, and distribution at the same time, which gives them stronger negotiating leverage across the supply chain. Paramount's February 2026 agreement to acquire Warner Bros. Discovery for USD 31 per share shows how major companies are pursuing scale in libraries, distribution, and production capability. Banijay Group and RedBird IMI also moved in March 2026 to combine Banijay Entertainment and All3Media into a larger global production platform with operations across many territories. These deals point to a competitive structure where scale matters more because buyers want deeper libraries, broader format capacity, and stronger delivery coverage across regions.

Competitive advantage in the film and TV production market is increasingly shifting toward companies that control specialized infrastructure and workflow tools. Pinewood reported studio occupancy above 90% across its portfolio for the nine months ended December 2025, underscoring the value of scarce production real estate as demand continues to cluster around proven facilities. Google DeepMind's USD 75 million investment in A24 in June 2026 demonstrates that proprietary production tools are becoming strategic assets rather than merely back-office support functions. Framestore reinforced this trend by formalizing AI leadership around its Futon workflow and receiving its fourth Scientific and Technical Award in 2026 for its rendering ecosystem. In the film and TV production market, these developments highlight how technical execution, auditability, and turnaround speed are increasingly influencing client selection alongside creative reputation.

Regional expansion is also becoming more strategic as companies try to place capital where localized commissioning is rising faster than legacy infrastructure. Mediawan finalized its acquisition of North Road Company in January 2026, creating a wider international production footprint backed by nearly 100 companies across 15 countries. Reliance Strategic Business Ventures Limited strengthened its position in India in February 2026 through a 50.1% acquisition of Sikhya Entertainment, linking distribution scale with documentary and narrative production capability. The film and TV production market therefore still has room for regional specialists, but companies with cross-border financing, infrastructure, and rights management are setting the pace of competition.

Film and TV Production Industry Leaders

Netflix, Inc.

Warner Bros. Discovery, Inc.

Paramount Global

NBCUniversal Media, LLC

The Walt Disney Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Google DeepMind announced a USD 75 million investment in A24 as part of a first-of-its-kind AI research partnership to develop new AI-powered filmmaking tools and workflows. The deal grants DeepMind access to A24's production process, while A24 retains full creative control and no AI training on its content library is permitted. The transaction marks Google's first equity stake in a film studio, signaling broad technology-sector commitment to production tool innovation.

- March 2026: Banijay Group and RedBird IMI announced a strategic partnership to combine Banijay Entertainment and All3Media under the Banijay brand. The merged company, jointly owned by both firms, aims to strengthen its global content portfolio, expand streaming partnerships, and accelerate IP growth across multiple platforms.

- February 2026: Paramount announced an agreement to acquire Warner Bros. Discovery, creating a major global media and entertainment company. The merger aims to combine leading film studios, streaming platforms, and iconic content libraries to strengthen competition in the evolving entertainment market. The transaction, valued at approximately USD 110 billion, is expected to expand consumer offerings, enhance creative opportunities, and drive long-term growth.

- February 2026: Reliance Strategic Business Ventures Limited, Jio Studios, acquired a 50.1% equity stake in Indian production house Sikhya Entertainment for INR 150 crore, approx. USD 17.5 million. The acquisition combines Jio Studios' distribution scale with Sikhya's internationally acclaimed documentary and narrative film pipeline, reinforcing India's growing stature in global content production.

Global Film and TV Production Market Report Scope

The Film and TV Production Market is Segmented by Content Type (Feature Films, TV Series, Documentary and Non-Fiction, Commercials, Music Videos, and Others), Production Stage (Pre-Production, Production, and Post-Production), Client Type (Studios and Broadcasters, Streaming Platforms, Independent Producers, and Advertising Agencies), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Feature Films |

| Television Series |

| Documentary and Non-Fiction |

| Commercials and Branded Content |

| Music Videos |

| Other Content Types |

| Pre-Production |

| Production |

| Post-Production |

| Studios and Broadcasters |

| Streaming Platforms |

| Independent Producers |

| Advertising Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Content Type | Feature Films | |

| Television Series | ||

| Documentary and Non-Fiction | ||

| Commercials and Branded Content | ||

| Music Videos | ||

| Other Content Types | ||

| By Production Stage | Pre-Production | |

| Production | ||

| Post-Production | ||

| By Client Type | Studios and Broadcasters | |

| Streaming Platforms | ||

| Independent Producers | ||

| Advertising Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the film and TV production space?

The film and TV production market stood at USD 298.47 billion in 2025, reaches USD 312.88 billion in 2026, and is forecast to reach USD 409.69 billion by 2031 at a 5.54% CAGR.

Which content type leads global production spending?

Television Series led by value with a 39.62% share in 2025 because recurring seasons support steady commissioning across writing, shooting, and post-production.

Which content category is expanding the fastest through 2031?

Documentary and Non-Fiction is projected to grow at a 9.87% CAGR through 2031, supported by lower cost per hour and strong engagement value for streaming services.

Which production stage is growing the fastest?

Post-Production is the fastest-growing stage with an 8.76% CAGR, reflecting heavier VFX use, cloud workflows, and more complex delivery requirements across platforms.

Which client group is creating the strongest growth opportunity?

Streaming Platforms are projected to grow at a 9.29% CAGR through 2031, making them the strongest client-side growth engine even though Studios and Broadcasters still held the largest 2025 share.

Which region offers the fastest growth outlook?

Asia-Pacific is forecast to expand at a 10.12% CAGR through 2031, while North America remains the largest region with a 37.21% share in 2025.

Page last updated on: