Movie Theatre Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 85.47 Billion |

| Market Size (2031) | USD 106.71 Billion |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

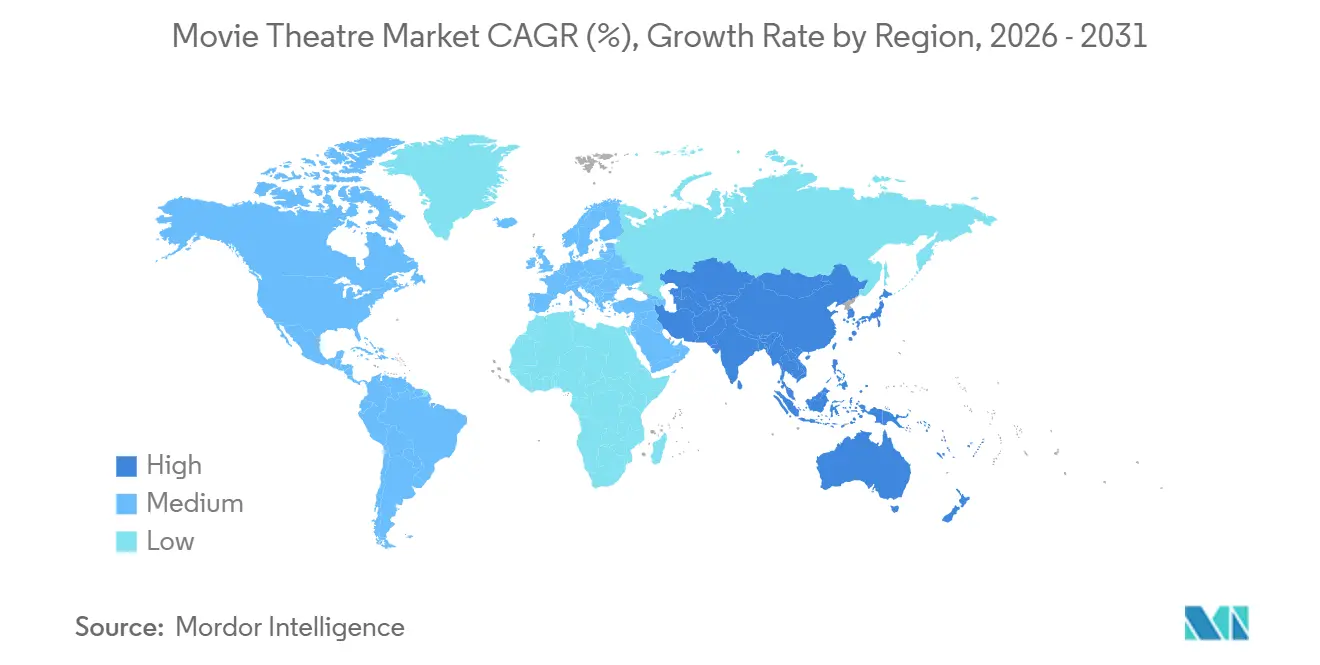

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Movie Theatre Market Analysis by Mordor Intelligence

The movie theatre market size is projected to be USD 81.33 billion in 2025, USD 85.47 billion in 2026, and reach USD 106.71 billion by 2031, growing at a CAGR of 4.54% from 2026 to 2031. Demand is rebounding as premium-large-format (PLF) screens lift per-patron spending, while exhibitors counter streaming competition through event-driven programming and loyalty subscriptions. Operators are prioritizing capital toward immersive technologies that widen ticket price bands, although high interest charges limit smaller chains from matching upgrades. North America remains the revenue anchor but is losing relative weight to Asia-Pacific, where China and India are adding screens in tier-2 and tier-3 cities. Sovereign-backed investment in Saudi Arabia and the United Arab Emirates is accelerating regional supply, and studio pipelines returning to pre-pandemic cadence are reinforcing the box-office recovery.

Key Report Takeaways

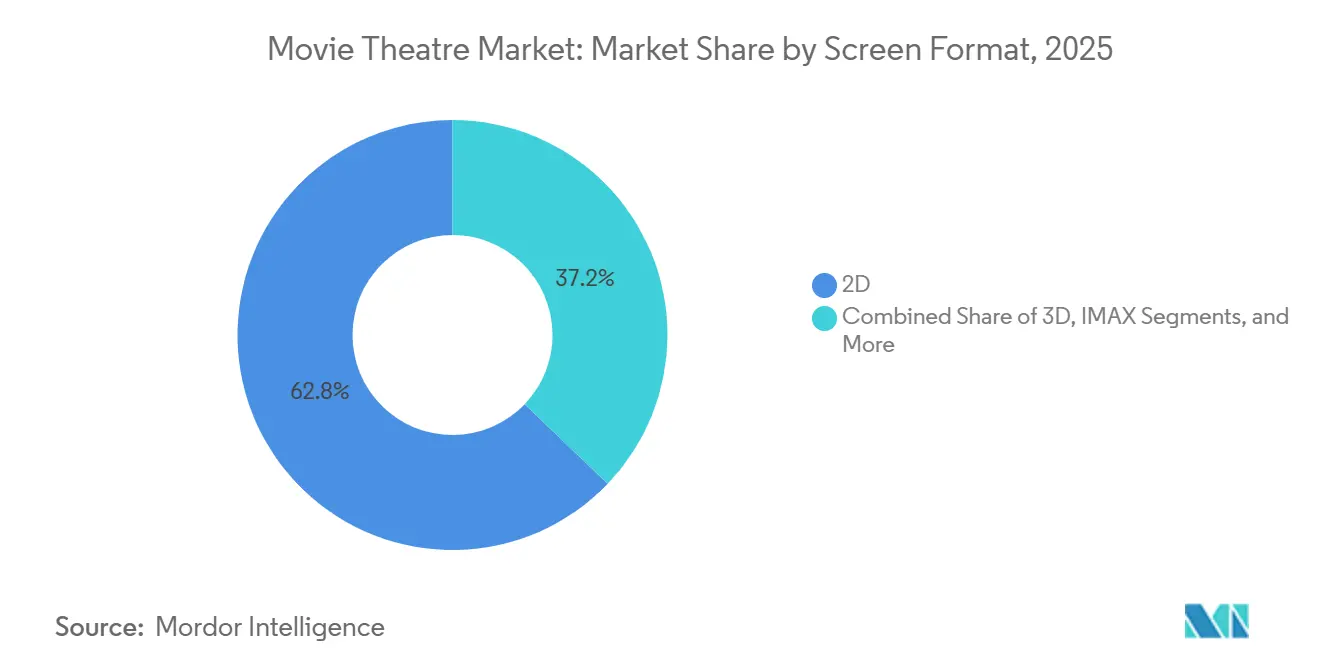

- By screen format, 2D retained 62.83% revenue share in 2025, while ScreenX and other PLF formats are forecast to expand at a 4.61% CAGR through 2031.

- By theatre type, multiplexes held 56.91% of the movie theatre market share in 2025, whereas luxury boutique venues are projected to grow at a 4.66% CAGR to 2031.

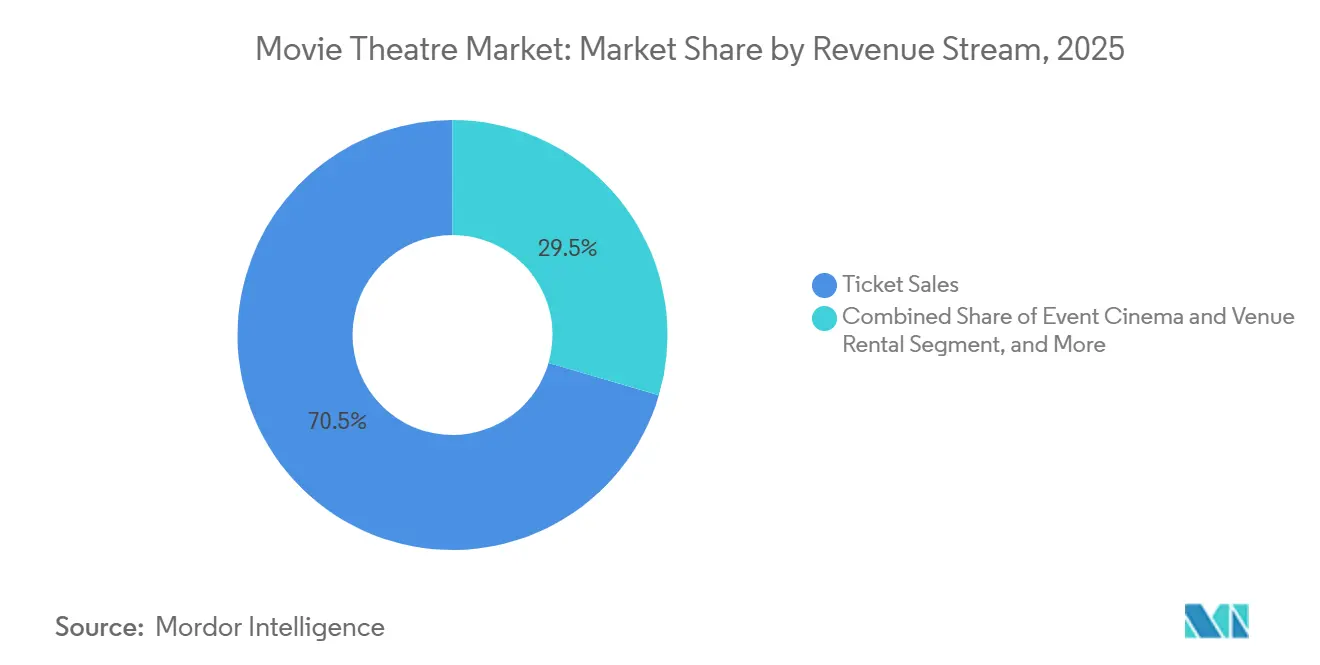

- By revenue stream, ticket sales accounted for 70.47% of the movie theatre market size in 2025, and event cinema and venue rental are advancing at a 4.72% CAGR to 2031.

- By ownership model, publicly traded chains controlled 45.58% of 2025 revenue and private chains are set to post a 4.58% CAGR to 2031.

- By geography, North America commanded 45.38% of the movie theatre market share in 2025; Asia Pacific is advancing at a 4.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Movie Theatre Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Premium Large Format (PLF) and Immersive Technologies | +0.8% | North America, China, Middle East | Medium term (2-4 years) |

| Rising Disposable Incomes in Emerging Markets | +0.9% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Recovery of Tent-Pole Blockbuster Release Schedules | +0.7% | Global | Short term (≤ 2 years) |

| Growth of Event Cinema Programming | +0.5% | North America, Europe, Australia | Medium term (2-4 years) |

| AI-Driven Showtime and Content Mix Optimization | +0.3% | North America, Europe, selected Asia-Pacific | Medium term (2-4 years) |

| Blockchain-Based Loyalty Tokens and Micro-Rewards | +0.1% | Pilot markets in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Premium Large Format and Immersive Technology

Exhibitors treat PLF as a margin-defense play rather than a novelty. CJ 4DPLEX agreed to install 115 combined 4DX and ScreenX auditoriums across AMC Entertainment and Cinépolis during 2025, extending its global footprint past 1,200 screens.[1]CJ 4DPLEX, “Global Box Office Reaches USD 458 Million,” cj4dplex.com In North America, PLF tickets command USD 5-8 premiums that translate into 40-60% higher revenue per seat. IMAX added four new U.S. locations with Regal and signed for 20 additional screens in Saudi Arabia and India, confirming exhibitor willingness to co-finance high-capex systems that justify elevated pricing.[2]IMAX Corporation, “Investor Presentation Q3 2025,” imax.com

Rising Disposable Incomes in Emerging Markets

Middle-class expansion is redrawing investment maps. PVR INOX added 200 franchise-and-management-contract screens in Indian cities of 100,000-500,000 residents for fiscal 2026, minimizing capital exposure while expanding its footprint.[3]PVR INOX Limited, “Annual Report FY2025,” pvrinox.com CJ CGV’s Vietnam revenue climbed 42.2% year-over-year to KRW 253.6 billion (USD 190 million) as premium-format adoption spread in Ho Chi Minh City and Hanoi. These patterns indicate that emerging markets will contribute a disproportionate share of screen additions and concession growth.

Recovery of Tent-Pole Blockbuster Release Schedules

Studio pipelines normalized in 2025, with domestic box office surpassing USD 9 billion, driven by Avatar: The Way of Water and Avengers: The Kang Dynasty. The 2026 slate is expected to top USD 9.8 billion domestically as major studios schedule 12-15 wide releases apiece. Exhibitors benefit from this cadence because tent-pole films generate opening-weekend surges that justify premium pricing and fill auditoriums during peak Friday and Saturday evening slots, when labor and occupancy costs are already sunk. The risk lies in over-reliance; a single underperforming franchise installment can erase quarterly revenue gains, as evidenced by the 2024 shortfall when several anticipated sequels missed box-office targets.

Growth Of Event Cinema Programming

Alternative content is scaling from experiment to structural hedge. Fathom Events’ revenue exceeded USD 145 million in 2024, up 45% year-over-year, by programming concerts, operas, and anime premieres. Taylor Swift's Eras Tour concert film opened to USD 34 million domestically in October 2023 and grossed over USD 260 million globally, demonstrating that music-driven content can rival traditional theatrical releases, while Cinemark reported its second-highest non-traditional box office in Q3 2025, driven by anime titles such as Demon Slayer and Chainsaw Man, which attracted younger demographics. This diversification reduces exhibitors' exposure to studio release-date volatility and opens incremental revenue streams that require minimal incremental marketing spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift Toward Over-the-Top (OTT) Streaming Platforms | -0.9% | North America, Europe | Short term (≤ 2 years) |

| High Capital Outlays Required for Premium Technology Upgrades | -0.5% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Escalating Insurance Premiums for Venue Security and Health Protocols | -0.2% | North America, Europe | Medium term (2-4 years) |

| Tightening Green-Building Finance Rules Raising Cinema Real-Estate Costs | -0.3% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Over-The-Top Streaming Platforms

Theatrical windows compressed to an average 45 days in 2025, with some Universal titles moving to Peacock after 17 days. Netflix, with 282.7 million subscribers as of Q3 2024, released The Electric State in March 2025 with a limited theatrical run of fewer than 500 screens, prioritizing streaming visibility over box-office revenue. This strategy fragments audience attention and conditions consumers to wait for home availability, particularly for mid-budget dramas and comedies that lack spectacle to justify a cinema visit. Exhibitors counter by emphasizing event-driven releases-films like Wicked received 90-plus-day windows in 2024 due to strong opening performance, but the structural shift toward day-and-date or shortened windows is irreversible for most titles.

High Capital Outlays Required For Premium Technology Upgrades

Installing IMAX costs USD 1-2 million per screen, and retrofitting 4DX averages USD 500,000-800,000. North American exhibitors committed USD 2.2 billion over three years, starting in September 2024, to upgrade projection, seating, and concession infrastructure, but this investment is concentrated among the top five chains-AMC, Regal, Cinemark, Cineplex, and Marcus Theatres-leaving independent and regional operators unable to compete on experience. The financing challenge is compounded by elevated interest rates; AMC Entertainment's weighted-average cost of debt stood at 8.5% in Q3 2024, making incremental borrowing prohibitively expensive AMC Entertainment 10-Q Q3 2024. Operators that cannot invest in premium formats risk margin compression as audiences migrate to competitors offering superior experiences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screen Format: Sensory Differentiation Drives Yield

2D screens comprised 62.83% of 2025 revenue because of widespread availability and lower operating costs. Premium formats are expected to capture incremental share as ScreenX and other PLF formats advance at a 4.61% CAGR to 2031, reflecting exhibitor focus on per-patron yield. IMAX, holding roughly 5% of screens, delivers ticket premiums of USD 5-8 above base prices and maintains strong occupancy, underscoring its moat against home theater substitution.

ScreenX installations, costing USD 300,000-500,000 each, provide a lower-capex entry point for mid-tier exhibitors, while 4DX appeals to 18-34 demographics seeking heightened immersion. CJ 4DPLEX’s 2025 box office of USD 458 million verifies monetization effectiveness. The screen-format mix illustrates how the movie theatre market size evolves through technology segmentation rather than pure volume expansion.

By Theatre Type: Luxury Boutique Gains Share

Multiplexes delivered 56.91% of total revenue in 2025 by leveraging eight-to-16-screen footprints that maximize showtime flexibility and concession throughput. In contrast, luxury boutique venues are growing at a 4.66% CAGR, attracting affluent patrons willing to pay USD 25-40 per ticket for recliners, gourmet menus, and 21-plus environments. Single-screen independents continue to shutter due to capital constraints, although art-house outlets in urban centers survive through community programming.

Sony Pictures’ 2024 acquisition of Alamo Drafthouse illustrates how content owners value boutique chains for controlled distribution and premium economics. Open-air and pop-up venues serve seasonal demand in Australia and the Middle East, but drive-ins that boomed during 2020 social distancing are plateauing as indoor venues resume normal capacity. Theatre-type bifurcation underscores segmentation of willingness-to-pay within the broader movie theatre market.

By Revenue Stream: Event Cinema Diversifies Income

Ticket sales accounted for 70.47% of 2025 revenue, yet event cinema and venue rental are projected to expand at a 4.72% CAGR, demonstrating a strategic pivot toward seven-day auditorium monetization. Concessions generated USD 8.20 per patron in the United States and 33% of PVR INOX's total revenue in India, revealing geographic differences in price structures.

On-screen advertising delivered a 3-4% margin lift through pre-show campaigns sold by National CineMedia, while subscription programs such as AMC Stubs A-List generated recurring revenue and increased visit frequency. The movie theatre market size benefits when operators balance blockbuster weekends with mid-week alternative content that fills unused capacity, translating to steadier cash flows.

By Ownership Model: Private Chains Outpace Public Peers

Publicly traded operators accounted for 45.58% of 2025 revenue but carry pandemic-era debt burdens, limiting capex flexibility. AMC’s USD 4.2 billion debt load limits premium-format rollouts despite recent restructuring. Private chains, exemplified by Cinépolis and CJ CGV, are moving faster in South America and Southeast Asia, deploying screens in underserved cities and integrating PLF through strategic partnerships.

Independent owners operating fewer than ten sites struggle to finance laser projection and recliner retrofits, though some persist in rural regions. Government and nonprofit entities in Europe leverage cultural subsidies to maintain arthouse screens, preserving diversity in content. The ownership structure thus shapes strategic options, as the movie theatre market increasingly rewards balance-sheet agility.

Geography Analysis

North America accounted for 45.38% of 2025 global revenue, driven by the highest average ticket prices and robust concession spending. Box-office recovery to USD 9 billion reflects resilient demand for tent-poles, yet per-capita attendance trails 2019 levels as streaming entrenches at-home viewing. Chapter 11 exits by AMC Entertainment and Cineworld closed underperforming sites, tightening supply and lifting utilization. Canada’s Cineplex contends with rising labor costs, while Mexico gains from Cinépolis’ expansion into lower-rent tier-2 cities.

Asia-Pacific is forecast to grow at 4.70% through 2031, the fastest regional pace. China’s screen count reached 90,968 in 2024, and box office climbed to CNY 48 billion (USD 6.78 billion) in 2025 despite domestic-film quotas limiting foreign titles. India’s PVR INOX added franchise screens in secondary cities, keeping average ticket price at Rs 260 (USD 3.12) while lifting food and beverage revenue per patron. Southeast Asian growth is anchored by CJ CGV’s Vietnamese operations, which rose 42.2% in fiscal 2025, demonstrating middle-class buying power.

Europe remains fragmented. Western markets such as the United Kingdom and Germany face attendance declines amid intense OTT penetration, whereas Eastern markets expand from lower bases. Kinepolis’ EUR 242.8 million (USD 274 million) Q3 2024 revenue highlights selective growth via premium formats. Green-building mandates under the EU EPBD raise real-estate costs by 15-25%, favoring chains with stronger balance sheets. The Middle East surges on sovereign funding, VOX Cinemas pledged SAR 2 billion (USD 533 million) to install 600 Saudi screens by 2028, signaling state-driven capacity creation.

Competitive Landscape

The top ten global chains control a considerable share of screens, indicating moderate concentration. Competitive positioning revolves around three levers, premium-format partnerships, geographic infill in high-growth cities, and diversification into event programming and subscription products. IMAX secured 20 additional installations across Saudi Arabia and India, while CJ 4DPLEX locked in 115 combined 4DX and ScreenX deals with major exhibitors, underscoring supply-chain collaboration rather than in-house R&D.

Studio vertical integration adds a new competitive dimension. Sony Pictures’ purchase of Alamo Drafthouse grants it a captive, premium distribution outlet, foreshadowing further moves by content owners to secure exhibition margins. Subscription programs, now exceeding 1.1 million AMC A-List members, create switching costs and data advantages but cannibalize some full-price tickets.

Regulation shapes regional strategies. China’s quota system reserves about 80% of screens for domestic films, shielding local exhibitors while capping the potential for foreign revenue. In Europe, stringent energy-performance rules elevate capex, punishing independents that lack financing capacity. The balance between capital intensity and market access will define winners as the movie theatre market evolves.

Movie Theatre Industry Leaders

Wanda Film Holding Co., Ltd.

AMC Entertainment Holdings Inc.

Cinépolis de México S.A. de C.V.

Cinemark Holdings Inc.

Cineworld Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cinemark Holdings announced plans to install Dolby Cinema technology in 25 additional locations across the United States and Latin America by Q4 2026, representing a USD 37.5 million investment.

- January 2026: IMAX Corporation announced agreements with exhibitors in Saudi Arabia and India to install 20 new IMAX screens by 2027, expanding its footprint in high-growth markets.

- December 2025: Vue International announced a GBP 50 million (USD 63 million) investment to upgrade projection systems to laser technology across 100 screens in the United Kingdom and Germany by mid-2026.

- December 2025: PVR INOX Limited announced plans to add 100 to 200 screens in fiscal year 2026 using franchise and management-contract models, targeting tier-2 and tier-3 cities in India.

Global Movie Theatre Market Report Scope

A movie theatre has an auditorium where individuals can watch movies for amusement. Theatres are commercial facilities that cater to the general public and are available by ticket purchase. Some movie theatres are operated by non-profit organizations or institutions that charge members a fee to watch movies. Movies are cast onto a giant projection screen at the front of the cinema via a projector, and many wall-mounted speakers broadcast sound and music.

The Movie Theatre Market is Segmented by Screen Format (2D, 3D, IMAX, 4DX, ScreenX and Other PLF), Theatre Type (Multiplex, Single-Screen Independent, Drive-In, Luxury Boutique, and Open-Air/Pop-Up), Revenue Stream (Ticket Sales, Concessions and Food and Beverage, On-Screen Advertising, Event Cinema and Venue Rental, and Subscription and Loyalty Programs), Ownership Model (Publicly Traded Chains, Private Chains, Independent Owners, and Government/Non-Profit Operators), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 2D |

| 3D |

| IMAX |

| 4DX |

| ScreenX and Other PLF |

| Multiplex |

| Single-Screen Independent |

| Drive-In |

| Luxury Boutique |

| Open-Air / Pop-Up |

| Ticket Sales |

| Concessions and Food and Beverage |

| On-Screen Advertising |

| Event Cinema and Venue Rental |

| Subscription and Loyalty Programs |

| Publicly Traded Chains |

| Private Chains |

| Independent Owners |

| Government / Non-Profit Operators |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Screen Format | 2D | |

| 3D | ||

| IMAX | ||

| 4DX | ||

| ScreenX and Other PLF | ||

| By Theatre Type | Multiplex | |

| Single-Screen Independent | ||

| Drive-In | ||

| Luxury Boutique | ||

| Open-Air / Pop-Up | ||

| By Revenue Stream | Ticket Sales | |

| Concessions and Food and Beverage | ||

| On-Screen Advertising | ||

| Event Cinema and Venue Rental | ||

| Subscription and Loyalty Programs | ||

| By Ownership Model | Publicly Traded Chains | |

| Private Chains | ||

| Independent Owners | ||

| Government / Non-Profit Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the movie theatre market become by 2031?

The movie theatre market size is forecast to reach USD 106.71 billion by 2031, reflecting a 4.54% CAGR from 2026.

Which format is growing fastest across auditoriums worldwide?

ScreenX and other premium large formats are projected to post the quickest expansion at a 4.61% CAGR through 2031.

What drives the surge in event cinema?

Concert films, anime premieres, and live broadcasts fill mid-week slots, boosting event-cinema and venue-rental revenue at a 4.72% CAGR.

Why are private chains gaining share over public peers?

Lower debt levels and flexible capital allocation let private exhibitors open screens in underserved tier-2 cities while public chains service higher interest burdens.

How are green-building rules affecting European operators?

The EU EPBD raises construction and retrofit costs by 15-25%, increasing capex hurdles for independents yet benefiting larger chains with stronger financing.

Page last updated on: