Synthetic Media Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

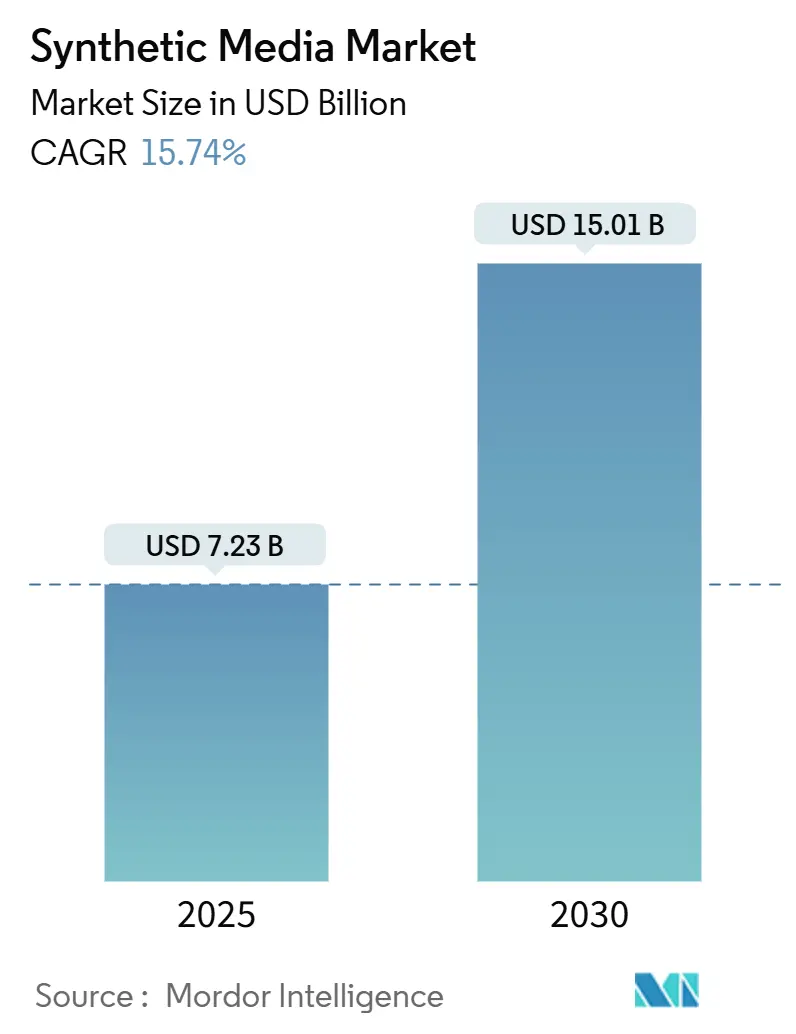

| Market Size (2025) | USD 7.23 Billion |

| Market Size (2030) | USD 15.01 Billion |

| Growth Rate (2025 - 2030) | 15.74% CAGR |

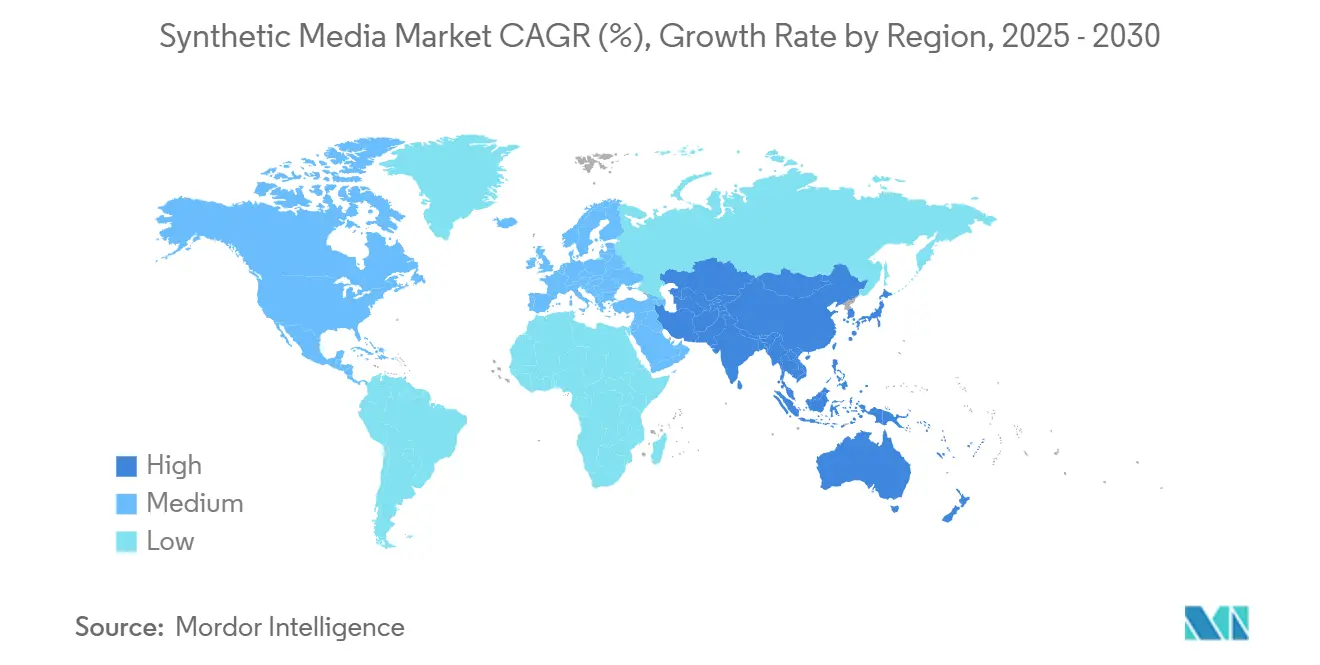

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

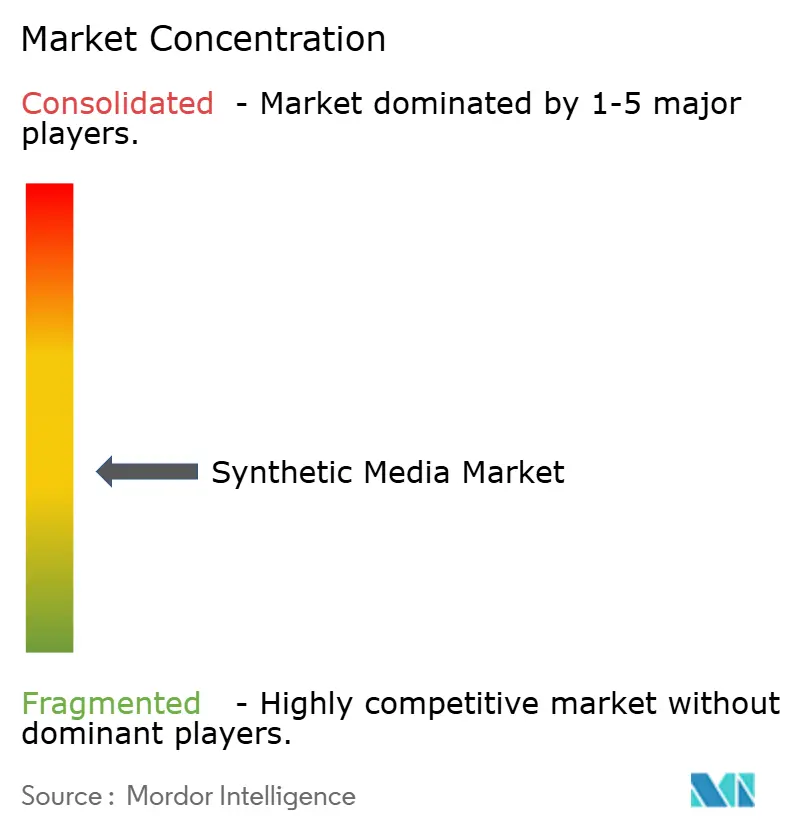

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Media Market Analysis by Mordor Intelligence

The synthetic media market size stands at USD 7.23 million in 2025 and is forecast to reach USD 15.01 million by 2030, reflecting a 15.74% CAGR during the period. The expansion is attributed to multimodal AI breakthroughs, lower GPU-hour costs, and edge-device acceleration that enable real-time content generation. Integrations with enterprise creative suites reduce adoption friction, while regulatory mandates for accessibility reinforce steady demand. Competitive intensity is sharpening as incumbents and startups compete on model efficiency and ethical AI positioning. At the same time, copyright liability exposure and deepfake-driven trust erosion temper near-term uptake.

Key Report Takeaways

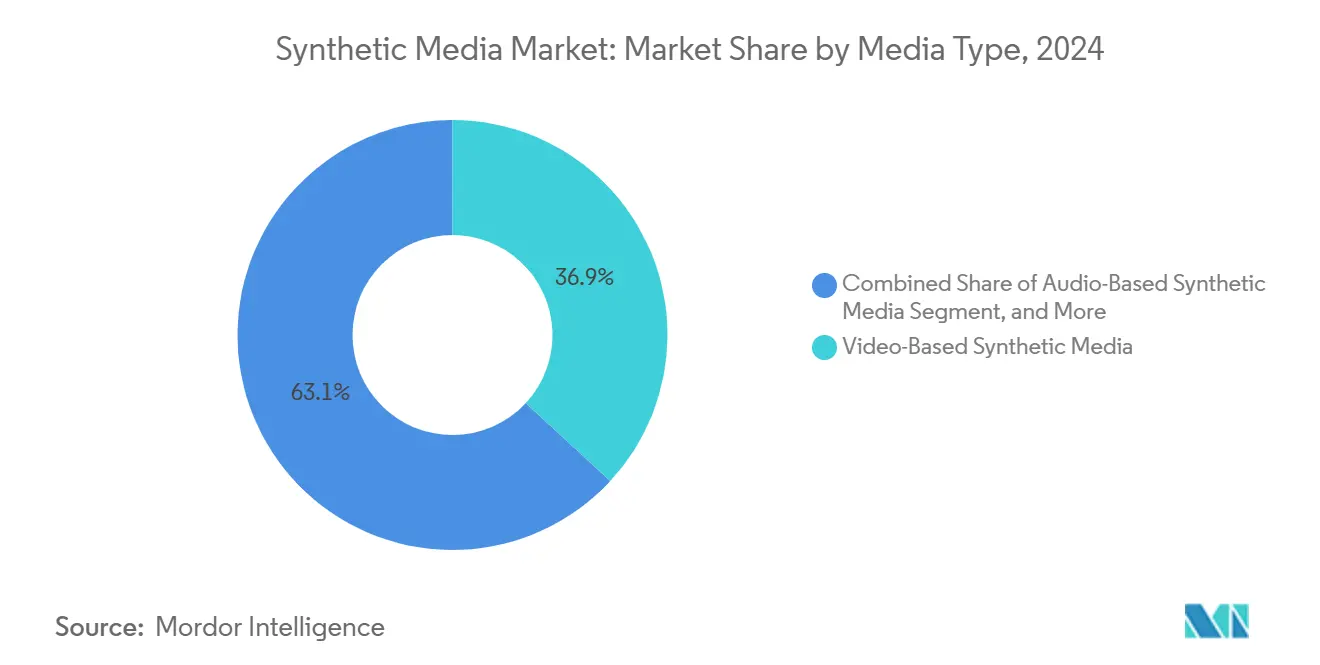

- By media type, video-based solutions led with 36.89% of synthetic media market share in 2024; audio-based applications are growing at 14.85% CAGR to 2030.

- By technology, generative AI commanded 42.48% of the synthetic media market size in 2024, while natural language processing is advancing at 15.92% CAGR through 2030.

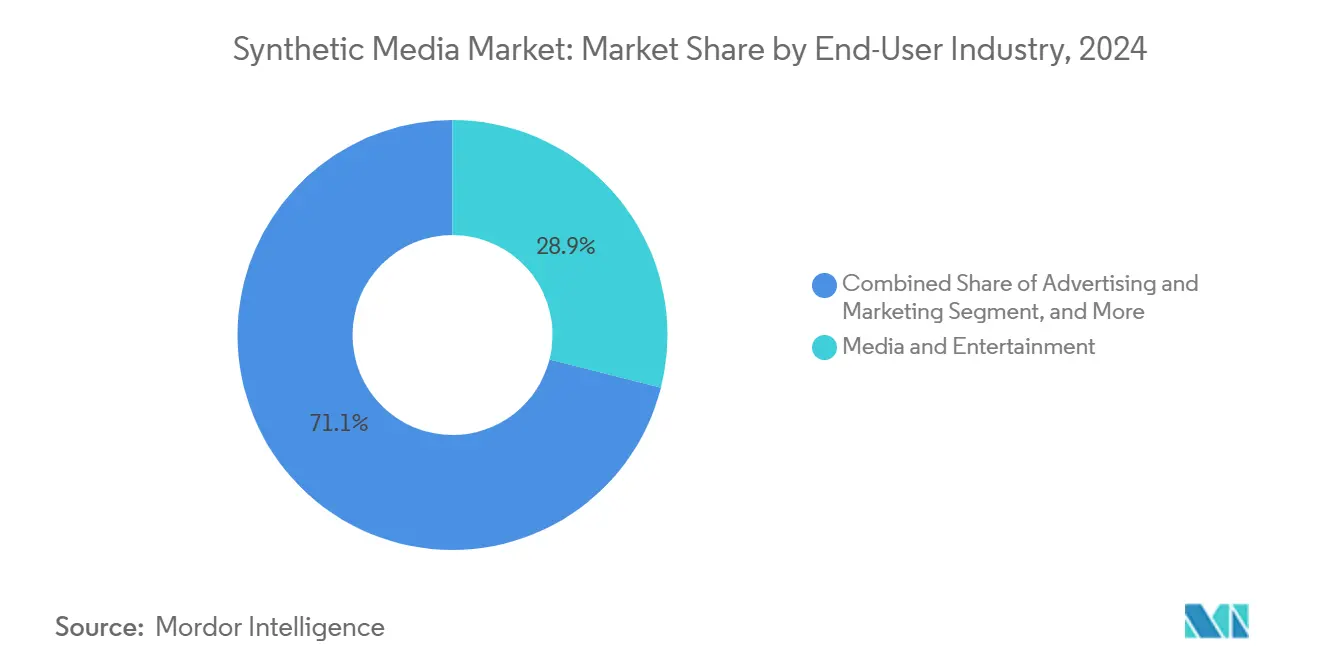

- By end-user industry, media and entertainment held 28.94% revenue share in 2024; gaming and metaverse applications exhibit the fastest expansion at 16.34% CAGR to 2030.

Global Synthetic Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring multimodal-AI model accuracy | +3.2% | Global, concentrated in North America and Asia Pacific | Medium term (2-4 years) |

| Falling GPU-hour inference costs | +2.8% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Enterprise-grade creative-suite integration | +2.1% | North America and Europe core, spill-over to Asia Pacific | Medium term (2-4 years) |

| Regulatory tailwinds for accessibility content | +1.4% | North America and Europe, gradual Asia Pacific adoption | Long term (≥ 4 years) |

| Edge-device generative-AI acceleration | +1.9% | APAC core, spill-over to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Multimodal-AI Model Accuracy

Unified architectures that combine text, image, and audio reasoning are closing the quality gap between AI-generated and conventional content. GPT-4.5 and Gemini 2.0 now produce coherent narrative sequences across media formats, elevating synthetic output to professional standards.[1]Genspark Team, “AI Image Model Features and Capabilities 2025,” Genspark, genspark.ai Higher fidelity reduces reliance on human post-production, accelerating enterprise adoption. Better models attract additional users, creating feedback loops that supply more training data. Companies investing early in multimodal capacity are positioned to gain disproportionate share once quality thresholds cross mainstream acceptance. In net effect, multimodal accuracy raises competitive barriers for late entrants and drives premium pricing for top-tier platforms.

Falling GPU-Hour Inference Costs

Annual declines of roughly 40% in video inference expense are widening access to advanced generation tools.[2]Nathan Benaich, “Your guide to AI: August 2025,” Air Street Press, airstreetpress.com Meta’s USD 105 billion infrastructure program underscores the scale investment behind these reductions. Lower unit economics empower small businesses and solo creators to experiment with synthetic media, enlarging the addressable user base. Edge computing further trims bandwidth overhead, making real-time applications viable for consumer devices. Platforms that design inference-efficient architectures gain cost leadership, allowing aggressive pricing while preserving margins. Overall, decreasing costs democratize the synthetic media market and sustain high growth momentum.

Enterprise-Grade Creative-Suite Integration

Embedding AI generation inside familiar software converts synthetic media from a standalone novelty into invisible infrastructure. Adobe GenStudio and Microsoft 365 Copilot let marketers build campaigns without leaving Outlook or Teams, compressing content cycles and slashing learning curves.[3]Melissa Heikkilä, “How Adobe's bet on non-exploitative AI is paying off,” MIT Technology Review, technologyreview.comIntegrated experiences increase user stickiness and raise switching costs, advantaging vendors with entrenched enterprise footprints. Cross-suite workflows expand usage beyond creative roles to sales, HR, and operations, supporting broad-based seat growth. As integration depth intensifies, pure-play AI startups must differentiate on specialized performance or niche use cases to remain competitive.

Regulatory Tailwinds for Accessibility Content

Accessibility mandates in the EU and North America reclassify synthetic media from optional enhancement to compliance requirement. Voice synthesis, multi-language dubbing, and automated audio descriptions enable organizations to satisfy legal obligations on a scale. Predictable, regulation-driven demand underpins long-term revenue visibility, justifying continued R&D investments. Vendors emphasizing licensed data and transparent model governance are favored in procurement, reinforcing a quality-over-quantity dynamic. While compliance budgets do not fluctuate with economic cycles, they encourage recurring subscription models that smooth cash flow for providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copyright-liability exposure | -2.3% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Deep-fake driven trust erosion | -1.8% | Global, pronounced in developed markets | Medium term (2-4 years) |

| Scarcity of synthetic-content watermark standards | -1.1% | Global, early impact in enterprise segments | Short term (≤ 2 years) |

| GPU supply-chain fragility | -0.9% | Global, concentrated in Asia Pacific manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Copyright-Liability Exposure

Unsettled case law on AI training data puts enterprises at risk of infringement claims. Recent U.S. court decisions sharpen scrutiny of unlicensed datasets, prompting legal departments to vet vendor provenance more rigorously. Adobe’s policy of sourcing only licensed or public-domain assets illustrates a defensive strategy but limits model breadth. The market bifurcates between “safe” yet narrower tools and higher-performing platforms that carry legal uncertainty. Extended procurement reviews slow sales cycles, dampening short-term revenue realization for providers that cannot demonstrate clear licensing lineage.

Deep-Fake Driven Trust Erosion

Financial-crime incidents, including the USD 25.5 million Arup deepfake fraud, damage public confidence in AI-generated content. Media outlets fear credibility loss when synthetic elements are undisclosed. Consumers grow wary of visual or audio authenticity, pressuring brands to adopt watermarking or disclosure labels. Compliance mechanisms add cost and complexity, offsetting some efficiency gains. Negative publicity can trigger reactive regulation, raising barriers for legitimate applications and potentially slowing market expansion in sensitive sectors such as journalism and finance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Media Type: Video Content Drives Market Leadership

Video-based solutions accounted for 36.89% of synthetic media market share in 2024. Enterprises adopt AI-generated video to bypass location shoots and post-production overhead, transforming marketing, training, and entertainment workflows. The video segment of the synthetic media market will continue to expand as edge GPUs enable real-time rendering, supporting interactive ads and personalized streaming. Runway AI's USD 308 million funding validates investor belief in scalable video generation models and underscores capital requirements for compute-intensive media. Adoption accelerates in social platforms where short-form video dominates user engagement, creating demand for automated, context-aware clips.

Audio-based content, while smaller in 2024, is projected to grow at 14.85% CAGR through 2030 as voice cloning and multilingual dubbing gain traction. Lower computer loads make audio ideal for edge deployment, powering real-time conversational agents and accessibility overlays. ElevenLabs' USD 80 million annual recurring revenue signals commercial viability for subscription voice platforms. Healthcare use cases such as voice restoration strengthen trust narratives, contrasting with deepfake misuse and helping to normalize synthetic audio in everyday applications.

By Technology: Generative AI Foundations Enable Market Expansion

Generative AI retained 42.48% of synthetic media market share in 2024 and continues to anchor platform capabilities. Its scalability across media types creates network effects as user feedback refines model performance. Continual increases in model parameter counts strengthen generative AI's position in the synthetic media market, as illustrated by Meta's open source Llama 3.1 with 405 billion parameters. Open sourcing attracts developer communities, broadening integration points and accelerating innovation cycles.

Natural language processing registers the highest forecast CAGR at 15.92%, reflecting its role in converting text prompts into coherent multimedia packages that streamline campaign orchestration. NLP-driven solutions benefit from simplified interfaces that let non-technical users submit plain-language briefs and receive brand-compliant video, imagery, and audio assets. As prompt engineering techniques mature, reliance on specialized design talent declines, shifting budget allocations toward AI subscriptions over agency fees.

By End-User Industry: Gaming Disrupts Traditional Media Dominance

Media and entertainment accounted for 28.94% of market revenue in 2024, while gaming and metaverse segments are growing the fastest at 16.34% CAGR through 2030. Procedural generation allows endless virtual environments and personalized story lines without ballooning development budgets. NetVRk and Meta are embedding generative pipelines into immersive worlds, making synthetic media foundational infrastructure rather than a production add-on.

Advertising and marketing teams leverage AI for hyper-personalized campaigns, dynamically adjusting messaging by audience cohort. E-commerce retailers deploy synthetic try-ons and 3D product renders, cutting studio costs and boosting conversion. Healthcare and education value propositions center on accessibility and training scalability, respectively. As sector use cases diversify, the synthetic media market becomes less dependent on any single vertical, distributing revenue risk and reinforcing long-term growth resilience.

Geography Analysis

North America leads the synthetic media market, underpinned by enterprise software penetration, high cloud spending, and accessibility legislation that mandates inclusive digital experiences. Creative suite vendors headquartered in the region offer direct integration paths, shortening deployment cycles. Venture funding concentrates in Silicon Valley, with OpenAI, Runway AI, and ElevenLabs collectively raising multiple billion-dollar rounds that finance talent acquisition and compute procurement. U.S. regulatory clarity on AI watermarking is progressing, offering businesses a roadmap for compliant rollout and encouraging further adoption.

Asia Pacific is the fastest-growing geography, propelled by sovereign AI initiatives in China and India that channel public funding into model development and GPU fabrication. China’s Deep Synthesis Regulations define liability frameworks while providing technological autonomy, catalyzing corporate investment in domestic platforms. India’s multilingual digital ecosystem stimulates demand for voice synthesis across 22 scheduled languages, aligning synthetic media adoption with government digital-inclusion goals. Hardware manufacturing clusters lower component costs, enabling regional providers to offer price-competitive solutions that challenge Western incumbents.

Europe balances innovation and regulation, with GDPR and forthcoming EU AI Act requirements directing purchasing toward privacy-preserving and explainable systems. Vendors that can demonstrate robust data lineage and watermarking protocols find receptive enterprise buyers. Mid-size creative agencies capitalize on AI tools to offset high labor costs, while public broadcasters pilot synthetic translations to expand audience reach within linguistic boundaries.

Middle Eastern economies invest in AI for diversification, with UAE retail adopters showing high consumer acceptance of AI shopping assistants. African opportunities are emerging but remain constrained by bandwidth and GPU availability, concentrating deployments in Tier-1 cities.

Mordor Intelligence provides coverage of the synthetic media market across other key regional markets, including North America, Europe, Asia, South America, and Middle East and Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The synthetic media market remains moderately fragmented but shows signs of consolidation as players pursue vertical integration. Adobe leverages entrenched creative suite to bundle AI agents, providing end-to-end production and distribution workflows. OpenAI capitalizes on foundational models, partnering with Microsoft to capture enterprise channels. Meta invests heavily in compute infrastructure and open-source strategy, aiming to seek an ecosystem that feeds back into its platform moat.

Specialists such as Runway AI differentiate on video generation fidelity, while ElevenLabs leads in voice cloning realism. Their growth underscores the market’s appetite for best-of-breed tools even as suites expand. Ethical positioning gains prominence: Adobe trains on licensed data, while Synthesia ai invests in disclosure technology to counter deepfake stigma. Antitrust scrutiny of NVIDIA, Microsoft, and OpenAI introduces regulatory uncertainty that could reshape partnership dynamics and acquisition strategies.

Startups occupying niche verticals legal document automation, healthcare voice restoration, localized education content find runway by addressing domain-specific compliance and workflow nuances. Acquisition interest from platform players is rising as they seek to plug feature gaps and accelerate expansion into regulated industries. Pricing competition centers on compute pass-through rates and storage efficiency, with model optimization emerging as a decisive margin lever.

Synthetic Media Industry Leaders

Adobe Inc.

NVIDIA Corporation

Runway AI, Inc.

Synthesia Limited

Meta Platforms Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Adobe launched Experience Platform Agent Orchestrator and AI agents for Microsoft 365 Copilot, bringing automated content production into familiar enterprise environments.

- January 2025: OpenAI partners with Axios to support local journalism and now works with nearly 20 media organizations, enhancing over 160 news outlets globally. These collaborations integrate AI tools into newsrooms, improving workflows, content accessibility, and user engagement.

- March 2025: Stability AI announces a strategic partnership and investment from WPP to integrate generative AI into marketing and entertainment production, accelerating innovation in visual media, immersive storytelling, and enterprise-grade creative tools.

Global Synthetic Media Market Report Scope

| Audio-Based Synthetic Media |

| Image-Based Synthetic Media |

| Text-Based Synthetic Media |

| Video-Based Synthetic Media |

| Generative AI |

| Computer Graphics and Visual Effects |

| Natural Language Processing |

| Voice Synthesis and Recognition |

| Others (AR and VR, Generative Adversarial Networks, and others) |

| Media and Entertainment |

| Advertising and Marketing |

| Gaming and Metaverse |

| E-commerce and Retail |

| Education and Training |

| Healthcare and Life-Sciences |

| Other End-user Industries (Real Estate, Hospitality, and More) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Media Type | Audio-Based Synthetic Media | ||

| Image-Based Synthetic Media | |||

| Text-Based Synthetic Media | |||

| Video-Based Synthetic Media | |||

| By Technology | Generative AI | ||

| Computer Graphics and Visual Effects | |||

| Natural Language Processing | |||

| Voice Synthesis and Recognition | |||

| Others (AR and VR, Generative Adversarial Networks, and others) | |||

| By End-User Industry | Media and Entertainment | ||

| Advertising and Marketing | |||

| Gaming and Metaverse | |||

| E-commerce and Retail | |||

| Education and Training | |||

| Healthcare and Life-Sciences | |||

| Other End-user Industries (Real Estate, Hospitality, and More) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| South Africa | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of the synthetic media market by 2030?

It is expected to reach USD 15.01 million, reflecting a 15.74% CAGR between 2025 and 2030.

Which media type currently leads in adoption?

Video-based solutions hold 36.89% market share due to cost savings in production workflows.

Why is audio-based synthetic media growing rapidly?

Voice cloning and multilingual dubbing needs push a 14.85% CAGR through 2030 as compute requirements are lower than video.

Which region is expanding the fastest?

Asia Pacific, driven by sovereign AI initiatives, domestic GPU production, and multilingual content demand.

Page last updated on: