Satellite TV Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 91.46 Billion |

| Market Size (2031) | USD 100.98 Billion |

| Growth Rate (2026 - 2031) | 2.00% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

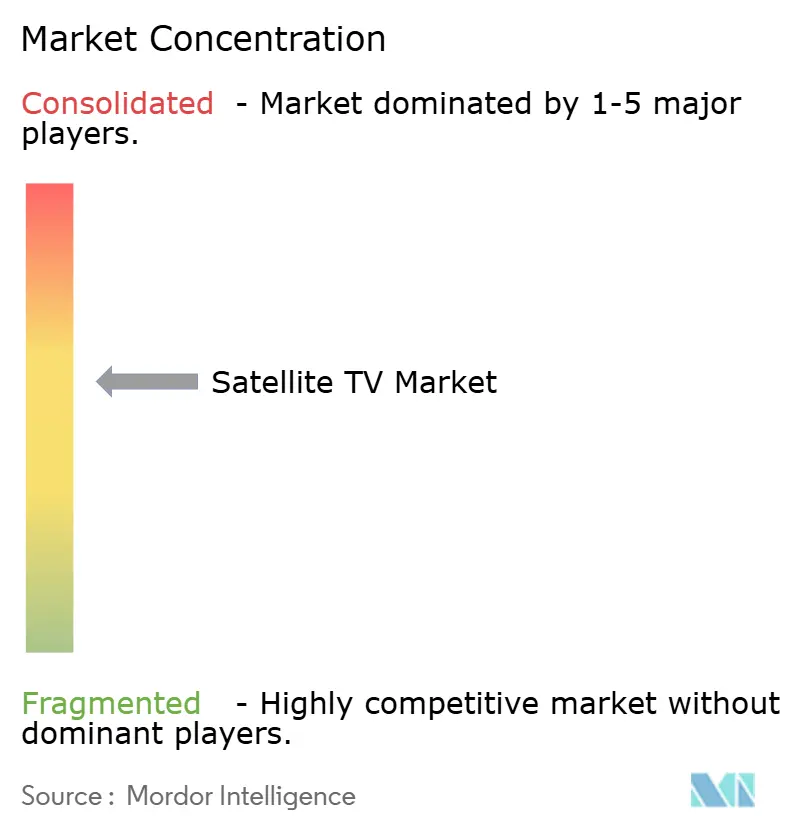

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite TV Market Analysis by Mordor Intelligence

The Satellite TV market size was valued at USD 89.08 billion in 2025 and estimated to grow from USD 91.46 billion in 2026 to reach USD 100.98 billion by 2031, at a CAGR of 2.00% during the forecast period (2026-2031). The satellite TV market continues to benefit from broad geographic reach, which still matters in rural and remote areas where fixed broadband coverage, service quality, or affordability remain uneven. Premium live sports, large event viewing, and established household reception habits are helping the satellite TV market preserve a meaningful user base even as consumers cut back on oversized channel bundles. Free-to-air reception is also keeping satellite viewing relevant in price-sensitive countries, which helps preserve installed equipment, viewing behavior, and future upsell potential for paid services. The satellite TV market is also moving toward hybrid delivery models in which operators combine linear channels, on-demand access, and app-based content within the same customer relationship. Competition is therefore shifting toward content rights, retention tools, selective bundling, and platform integration rather than depending only on subscriber scale.

Key Report Takeaways

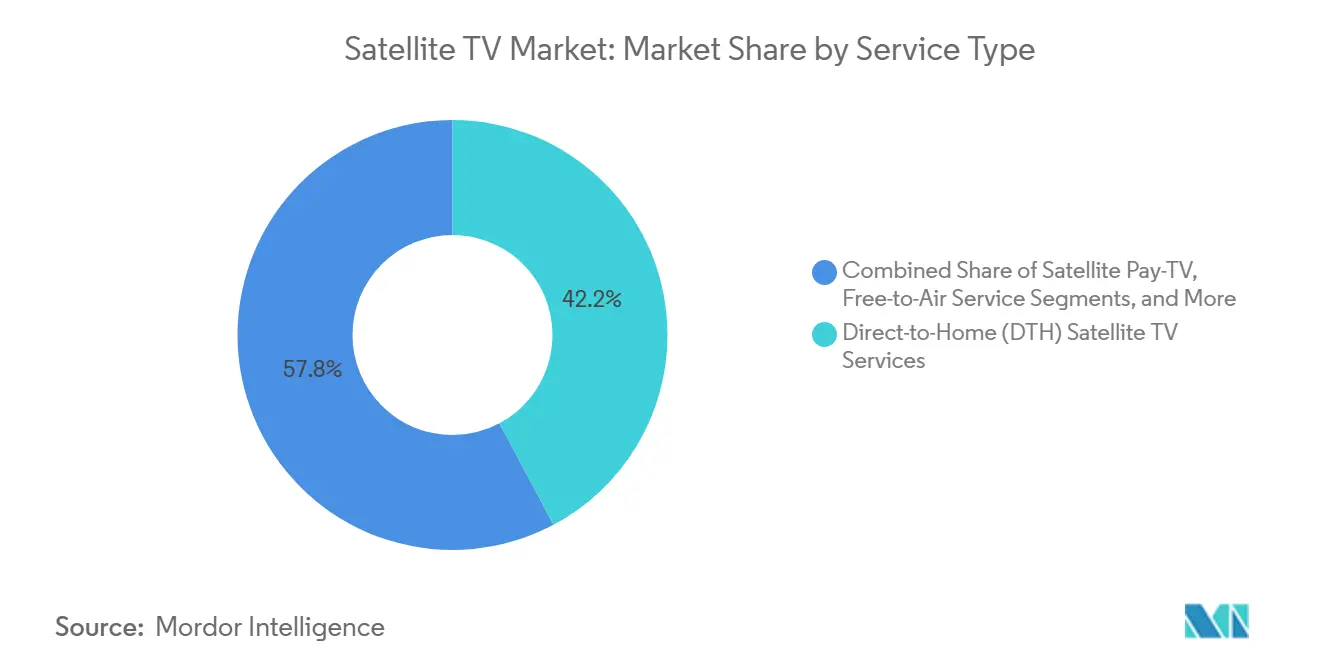

- By service type, DTH Satellite TV Services held 42.22% of the satellite TV market share in 2025, while Hybrid and Value-Added Satellite TV Services is projected to expand at a 5.11% CAGR through 2031.

- By revenue model, the subscription-based model accounted for 63.47% share of the satellite TV market size in 2025, while transactional and pay-per-view is projected to expand at a 4.62% CAGR through 2031.

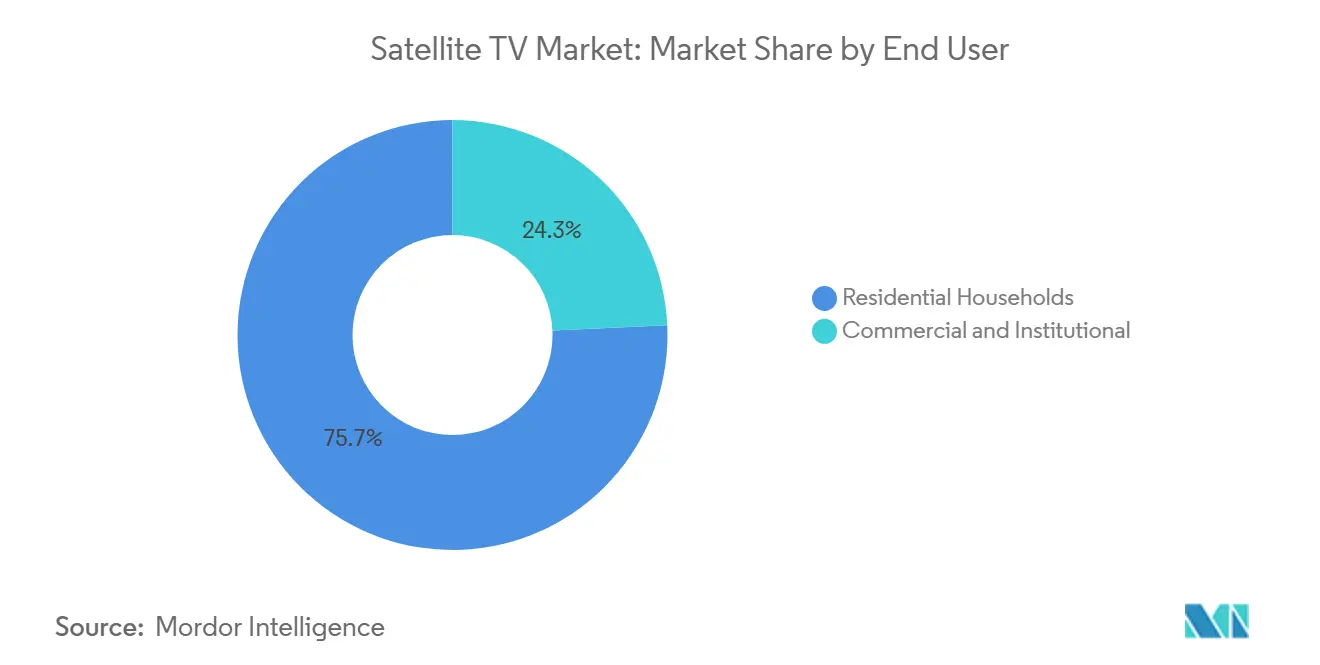

- By end user, residential households accounted for 75.72% of revenue in 2025, while commercial and institutional users are projected to grow at a 3.81% CAGR through 2031.

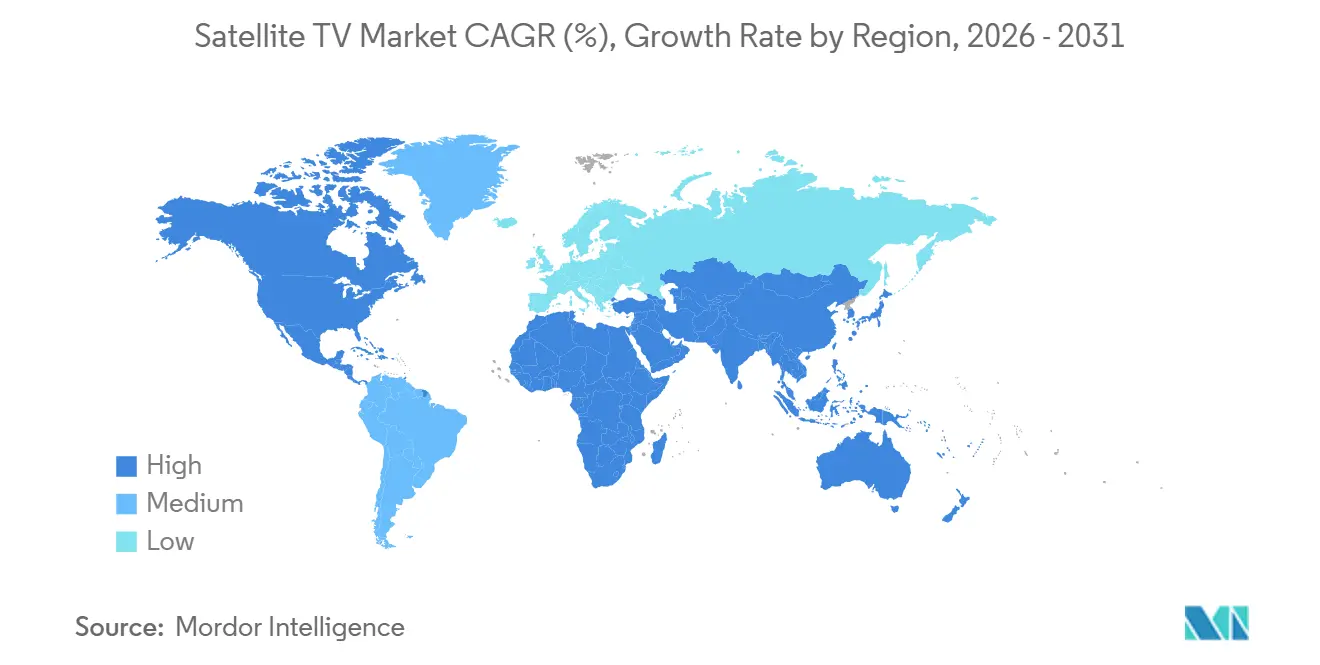

- By geography, North America held 26.11% of the satellite TV market in 2025, while Asia-Pacific is projected to record the fastest CAGR at 3.42% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Satellite TV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Sports and Live Event Viewing Fueling Subscriptions | +0.8% | Global, with concentrated relevance in North America, Europe, and Africa | Short term (≤ 2 years) |

| DTH Penetration in Rural and Infrastructure-Underserved Areas | +0.6% | Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Rising Demand For HD and UHD Linear Broadcasting | +0.5% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Hybrid Satellite-OTT Bundling Improves Retention | +0.4% | North America, Europe, and Southeast Asia | Medium term (2-4 years) |

| Spectrum Reuse And Beam-Targeted Capacity Expansion | +0.2% | North America and Europe | Medium term (2-4 years) |

| Set-Top Box Renewal Cycles Create Upgrade Opportunity | +0.1% | Europe, Asia-Pacific, and the Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Sports And Live Event Viewing Fueling Subscriptions

Premium sports remains one of the clearest retention tools in the satellite TV market because viewers still place high value on reliable live event access. DIRECTV launched its MySports Genre Pack at USD 69.99 per month, which showed how operators are separating sports from the full channel bundle to better match current viewing behavior. This move matters because many households no longer want large entertainment bundles, but they still pay for live sports when the offer is simpler and easier to justify. The FCC also sought comment in February 2026 on sports broadcasting practices and marketplace developments, which highlighted how fragmented access to premium sports has become for consumers.[1]Federal Communications Commission, “FCC's Media Bureau Seeks Comment on Sports Broadcasting Practices and Marketplace Developments,” Federal Communications Commission, fcc.gov In that setting, the satellite TV market benefits when operators can reduce service complexity and present sports viewing in a more unified way. This driver also supports package stability because major tournaments and league rights continue to bring back occasional viewers who may not otherwise retain a broad pay-TV subscription.

DTH Penetration in Rural and Infrastructure-Underserved Areas

DTH access remains a basic structural support for the satellite TV market in areas where television coverage still depends more on signal reach than on household broadband capability. In many rural locations, satellite reception remains easier to scale than dense terrestrial network expansion because one platform can serve a wide footprint without local last-mile duplication. This allows the satellite TV market to remain present even when consumers move between paid and free viewing options over time. The continued importance of dish-based reception also means that the installed base of equipment, viewing familiarity, and channel navigation habits does not disappear quickly. That matters because operators can use this installed base to defend household relevance while they reshape offers around value, content, and flexibility. The strongest benefit from this driver remains concentrated in Asia-Pacific, Africa, and South America, where geography and affordability still shape television access more directly than in mature broadband markets.

Rising Demand For HD and UHD Linear Broadcasting

Picture quality continues to support the satellite TV market because live television is one of the formats where HD and UHD differences remain easy for viewers to notice. Sports, major entertainment events, and high-profile broadcast programming all benefit from stable high-quality distribution that works across large territories at the same time. This gives the satellite TV market a practical advantage in households that still value linear viewing quality and predictable reception during peak events. Upgrades tied to HD and UHD also help operators refresh receivers, reposition premium packages, and encourage hardware replacement without fully changing the service model. These upgrade cycles help preserve customer relationships because households often reassess the value of their television service when equipment quality improves. The effect is especially relevant in Europe and North America, where mature viewing bases can still generate value from quality-led differentiation even as streaming alternatives keep expanding.

Hybrid Satellite-OTT Bundling Improves Retention

Hybrid bundling has become one of the most practical responses to changing customer behavior in the satellite TV market because many households now use both linear television and streaming services. Astro Malaysia extended its Disney+ collaboration in 2026 by integrating Disney+ content into Astro TV, Astro GO, and NJOI, while also placing selected local Astro stories in front of Disney+ audiences.[2]Astro Malaysia Holdings, “Astro and Disney+ Bring Global Hits and Malaysian Stories Closer Together,” Astro Ulagam, astroulagam.com.my Astro also stated in 2026 that local content and streaming activity supported resilient momentum, which showed that mixed viewing models are shaping service retention. This matters because the satellite TV market no longer serves households that choose only one screen environment, and operators increasingly need one interface that combines channels, apps, and on-demand access. Hybrid offers also make it easier to defend monthly value because customers can see both scheduled programming and app content inside a single paid relationship. That makes hybrid service design an important retention tool as the satellite TV market moves away from the old assumption that households will accept separate, large, channel-only bundles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cord-Cutting and OTT Substitution | -0.8% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Declining Pay-TV Willingness in Price-Sensitive Markets | -0.6% | South America and Southeast Asia | Medium term (2-4 years) |

| Satellite Capacity and Launch Cost Pressures | -0.3% | Global, with near-term relevance in North America | Medium term (2-4 years) |

| Content Rights Fragmentation Raises Costs | -0.2% | Global, with concentrated relevance in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cord-Cutting and OTT Substitution

Cord-cutting remains the strongest structural restraint on the satellite TV market because it affects both subscriber counts and the amount households are willing to pay for broad television packages. Nielsen reported in 2025 that streaming exceeded the combined share of broadcast and cable viewing for the first time, which marked a clear change in everyday viewing behavior.[3]Nielsen, “Streaming Reaches Historic TV Milestone, Eclipses Combined Broadcast and Cable Viewing for First Time,” Nielsen News Center, nielsen.com Once streaming became the larger viewing destination, the satellite TV market faced more pressure to justify package breadth rather than only content availability. The problem is not limited to technology substitution because on-demand viewing also changes how households think about timing, control, and entertainment spending. That leaves general entertainment bundles more exposed than sports-led, hybrid, or event-focused offers. The satellite TV market therefore needs narrower packaging, clearer value positioning, and stronger service integration to slow the loss of viewers who no longer see daily value in large traditional channel lineups.

Declining Pay-TV Willingness in Price-Sensitive Markets

Affordability pressure is another major restraint on the satellite TV market because many households in developing countries judge television spending against other basic digital needs. In these markets, consumers often compare a monthly satellite bill with free-to-air access, mobile data use, or lower-cost app viewing rather than with another premium television package. This makes the satellite TV market more vulnerable when large channel bundles feel too broad for the amount of content the household actually watches. It also limits how far operators can increase prices even when content, technology, and customer service costs continue to rise. The result is that value perception becomes as important as channel count, especially where family budgets are tight and viewing habits are becoming more selective. This restraint is strongest where free reception remains available and where mixed mobile and streaming behavior reduces the number of households willing to commit to a traditional paid television structure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: DTH Leads While Hybrid Services Shape the Next Revenue Layer

DTH Satellite TV Services held 42.22% of the satellite TV market share in 2025, which kept it as the leading service type by revenue. This position reflects years of investment in direct household delivery, receiver ecosystems, installation networks, and branded subscription relationships that remain difficult to replace quickly. The satellite TV market still depends heavily on DTH because it is the service format most closely tied to broad household familiarity and national coverage. DTH also remains important because it works across premium urban users, mid-income families, and remote households that do not have the same broadband options as large cities. Even in slower-growth conditions, this segment continues to anchor the satellite TV market because it holds the widest historical installed base and the clearest connection to monthly subscription billing.

Free-to-air, commercial, and other satellite-led service types remain meaningful because they preserve audience reach in places where price, institutional use, or universal access matter more than deep premium bundling. These categories keep the satellite TV market connected to public viewing needs, business environments, and lower-income households that may not enter through a traditional premium DTH plan. Hybrid and Value-Added Satellite TV Services is projected to expand at a 5.11% CAGR through 2031, making it the fastest-growing service type in the satellite TV market size. That growth reflects the shift toward integrated services that combine dish-based reception with internet return paths, app aggregation, and on-demand features inside one interface. The satellite TV industry is changing most clearly at this edge of the service mix because the future revenue layer will depend less on dish-only viewing and more on how operators package linear television with digital convenience.

By Revenue Model: Subscriptions Anchor Earnings While PPV Captures Event-Led Demand

The subscription-based model accounted for 63.47% share of the satellite TV market size in 2025, which confirmed that recurring monthly billing remains the main financial base for operators. Subscription revenue still matters because it supports content acquisition planning, customer service, device deployment, and package structuring in ways that ad hoc spending cannot fully replace. The satellite TV market continues to rely on this model because predictable payments help providers manage a business that still depends on scale, content rights, and service continuity. Subscription structures also remain useful for households that prefer one broad television relationship rather than several small app payments spread across different platforms. That is why the satellite TV market still treats subscription billing as the base layer, even when customer expectations around flexibility and bundle size are changing.

Transactional and pay-per-view is projected to expand at a 4.62% CAGR from 2026 to 2031, which makes it the fastest-growing revenue model in the satellite TV market. This pattern reflects the continued power of event-based spending, especially around sports, tournament viewing, and other time-sensitive premium content. DIRECTV's 2026 sports-focused package launch showed that operators are reshaping monetization around clearer content value and shorter decision paths for customers. The FCC's 2026 proceeding on sports broadcasting practices also reflected growing attention to how premium access is being segmented across platforms and price points. In practical terms, the satellite TV market is moving toward a structure in which subscriptions hold the relationship, while pay-per-view and event-led upgrades capture extra spending from moments that still drive strong viewer urgency.

By End User: Residential Households Remain Core While Commercial Demand Broadens The Base

Residential households accounted for 75.72% of revenue in 2025, which confirmed that home entertainment remains the core demand base of the satellite TV market. This segment has long defined the business because satellite television grew around family viewing, broad channel navigation, premium live sports, and fixed monthly plans tied to home devices. The satellite TV market still depends on residential users because they represent the largest installed base, the highest volume of recurring subscriptions, and the clearest legacy connection to linear television habits. At the same time, this segment is also the most exposed to streaming substitution because households compare monthly bills more directly with app bundles, free video, and mobile viewing options. That means operators in the satellite TV market need residential plans that feel more selective, more integrated, and easier to defend on value than older large-bundle structures.

Commercial and institutional users are projected to grow at a 3.81% CAGR from 2026 to 2031, which makes them the faster-growing end-user group in the satellite TV market. This segment includes hospitality, aviation, and other managed viewing environments where service reliability, content rights, and broad screen distribution still matter. United Airlines and DIRECTV launched live TV streaming on Starlink-enabled seatback screens across up to 150 aircraft in June 2026, which showed how satellite-linked television services can extend beyond the home into mobility settings.[4]United Airlines, “United Airlines and DIRECTV Team Up to Stream Live TV Including Live Sports on Starlink-Enabled Seatback Screens This Summer,” United Airlines Media Room, united.mediaroom.com This development is important because it gives the satellite TV market another route to growth that is less dependent on household bundle retention alone. As a result, commercial demand is broadening the business base of the satellite TV market by creating value in environments where managed content distribution remains more important than low-cost individual streaming.

Geography Analysis

North America held 26.11% of the satellite TV market in 2025, which made it the largest regional contributor by revenue. The region remains important because premium sports, established DTH brands, and high-value television habits still support paid services even as streaming gains further ground. The satellite TV market in North America is also under the most direct pressure from cord-cutting, which means operators need sharper product definitions than they did in earlier years. DIRECTV's launch of the MySports Genre Pack in January 2026 reflected this change by moving toward a narrower, event-led offer instead of relying only on the traditional full channel bundle. This regional shift matters because North America often sets the commercial pattern that other mature markets later adapt in more selective form.

Europe remained a major pillar of the satellite TV market because satellite reception continues to coexist with strong fiber and IPTV infrastructure rather than disappearing under it. The region benefits from long-established orbital distribution, strong public and private broadcast traditions, and households that still use linear television at scale. Eutelsat renewed its long-running partnership with Polsat Plus Group in January 2025 for video distribution from the HOTBIRD neighborhood, which reinforced the continuing role of satellite in European television delivery. CANAL+ also reported combined 2025 revenue of EUR 8,665 million (USD 9,402 million) after completing the MultiChoice acquisition, which highlighted the value of scale across mature and growth-oriented territories. Europe therefore remains a region where the satellite TV market preserves strategic relevance through distribution reach, portfolio scale, and continued broadcaster commitment.

Asia-Pacific is projected to grow at a 3.42% CAGR through 2031, making it the fastest-growing regional part of the satellite TV market. Growth in this region is supported by uneven broadband penetration, large rural populations, and continuing demand for mass television distribution across diverse income groups. The satellite TV market in Asia-Pacific also benefits from operators that are adapting quickly to mixed viewing behavior rather than defending legacy television formats without change. Astro's 2026 Disney+ integration and broader local content positioning showed how regional providers are blending global streaming access with local television relationships. South America, the Middle East, and Africa remain smaller in overall value, but they continue to matter to the satellite TV market because broad coverage, sports viewing, and price-tiered reception models still support ongoing relevance across those regions.

Competitive Landscape

The satellite TV market is moderately concentrated at the global level, but competition is still shaped more by strong regional leaders than by one dominant worldwide operator. This gives the business a layered structure in which a few large platforms control meaningful territories while national and sub-regional brands remain important within their own footprints. The satellite TV market, therefore, behaves as a connected set of regional contests rather than as a single uniform global battle. Content access, bundle design, geographic reach, and service integration continue to shape competitive outcomes more directly than price alone.

CANAL+ made the largest scale move in the recent period when it completed the MultiChoice acquisition, creating a combined subscriber base of 42.3 million across around 70 countries. This move matters because scale helps spread content costs, support cross-market distribution, and strengthen negotiation capacity across both mature and developing regions. The satellite TV market also saw product repositioning from DIRECTV, which used a sports-specific package to respond to consumers who wanted premium live content without a large traditional bundle. Astro strengthened its own position through deeper streaming integration, which showed that regional operators are increasingly competing through platform usefulness rather than through channel count alone. These examples show that the satellite TV market is being reshaped by scale-building, selective unbundling, and hybrid aggregation at the same time.

A second competitive layer is emerging around commercial deployment and mobility-linked viewing. United Airlines and DIRECTV launched live TV streaming on Starlink-enabled aircraft in June 2026, which demonstrated that managed live television can move into aviation and other non-residential settings. Eutelsat and Anuvu also signed a new multi-year agreement in May 2026 for high-throughput capacity on EUTELSAT 10B for in-flight connectivity services, which showed continuing investment in mobility-linked video distribution. These developments matter because they broaden where and how the satellite TV market can create value beyond the home. Operators that align linear television, hybrid interfaces, and managed commercial use cases are likely to defend relevance more effectively than providers that remain tied only to the older residential bundle model.

Satellite TV Industry Leaders

DIRECTV, LLC

Dish Network Corporation

Sky Group Limited

Tata Play Limited

CANAL+ S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: United Airlines and DIRECTV launched a live TV streaming service on Starlink-enabled seatback screens across up to 150 aircraft through July 20, 2026, covering the FIFA World Cup 2026 with over a dozen live TV channels. The initiative represents a commercial template for satellite TV operators extending services into the aviation vertical via hybrid Starlink/DIRECTV content delivery.

- May 2026: Eutelsat and Anuvu signed a new multi-year agreement for Ku-band high-throughput capacity on EUTELSAT 10B for in-flight connectivity services, including for a major global airline. The deal extends Eutelsat's footprint in the aviation sector and reinforces commercial satellite TV's integration into mobility platforms.

- January 2026: DIRECTV launched its MySports Genre Pack at USD 69.99 per month, a contract-free, sports-only streaming bundle targeting cord-cutters who prioritize live sports but reject the full pay-TV channel bundle. The launch formally transitions DIRECTV into a genre-segmented commercial model.

- September 2025: CANAL+ completed its acquisition of MultiChoice Group, creating a 42.3 million subscriber combined base across approximately 70 countries. Combined 2025 revenues reached EUR 8,665 million (USD 9,402 million), establishing CANAL+ as the world's largest satellite pay-TV operator by geographic footprint.

Global Satellite TV Market Report Scope

The Satellite TV Market Report is Segmented by Service Type (DTH, Satellite Pay-TV, Free-to-Air, Commercial, and Hybrid and Value-Added), Revenue Model (Subscription-Based, Advertisement-Based, and Transactional/PPV), End User (Residential Households, and Commercial and Institutional), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Direct-to-Home Satellite TV Services |

| Satellite Pay-TV Services |

| Free-to-Air Satellite TV Services |

| Commercial Satellite TV Services |

| Hybrid and Value-added Satellite TV Services |

| Subscription based |

| Advertisement Based |

| Transactional / Pay-Per-View |

| Residential Households |

| Commercial and Institutional |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Direct-to-Home Satellite TV Services | |

| Satellite Pay-TV Services | ||

| Free-to-Air Satellite TV Services | ||

| Commercial Satellite TV Services | ||

| Hybrid and Value-added Satellite TV Services | ||

| By Revenue Model | Subscription based | |

| Advertisement Based | ||

| Transactional / Pay-Per-View | ||

| By End User | Residential Households | |

| Commercial and Institutional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the satellite TV market?

The satellite TV market size was USD 89.08 billion in 2025, is estimated at USD 91.46 billion in 2026, and is projected to reach USD 100.98 billion by 2031 at a 2.00% CAGR.

Which service type leads the satellite TV market today?

DTH Satellite TV Services led the satellite TV market with a 42.22% revenue share in 2025 because of its long-established household reach and installed base.

Which revenue model is growing the fastest in satellite TV?

Transactional and pay-per-view is projected to expand at a 4.62% CAGR through 2031 as operators capture more value from sports and other event-led viewing.

Why do residential households still dominate demand?

Residential households accounted for 75.72% of revenue in 2025 because home entertainment remains the core use case for satellite television, even as streaming competition grows.

Which region offers the strongest growth outlook for satellite TV?

Asia-Pacific is projected to grow at a 3.42% CAGR through 2031, supported by uneven broadband availability, rural demand, and broad television distribution needs.

What are the main strategies used by leading satellite TV operators?

Leading operators are focusing on scale-building acquisitions, sports-led packaging, hybrid satellite and streaming bundles, and expansion into commercial settings such as aviation.

Page last updated on: