Europe Stone Plastic Composite (SPC) Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

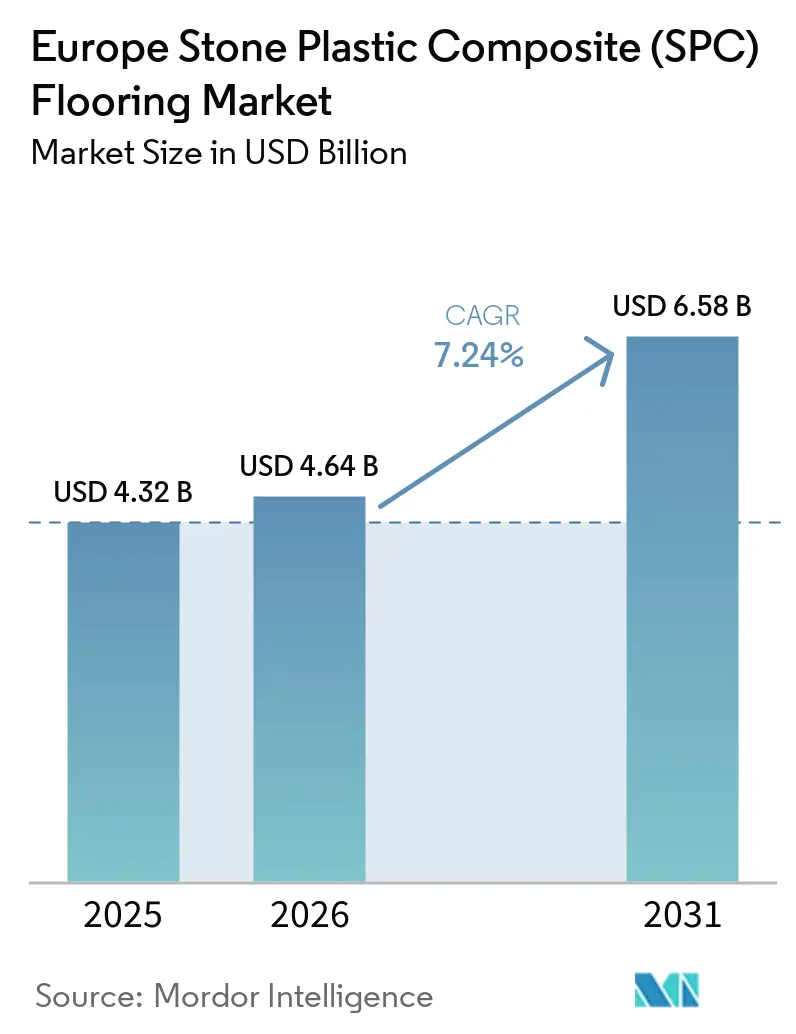

| Base Year Market Size (2025) | USD 4.32 Billion |

| Market Size (2026) | USD 4.64 Billion |

| Market Size (2031) | USD 6.58 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

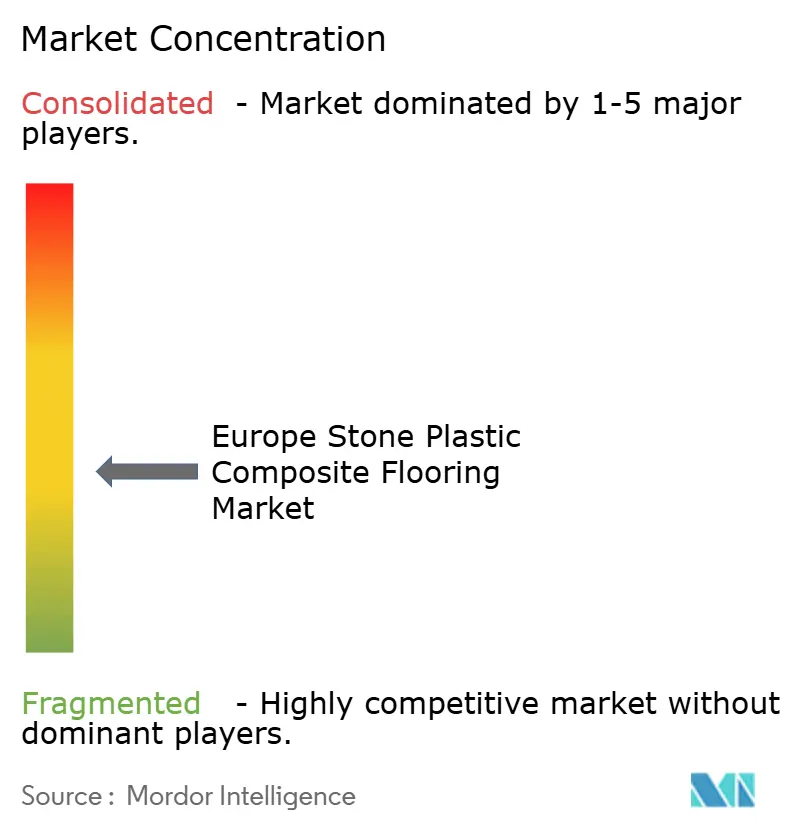

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Stone Plastic Composite (SPC) Flooring Market Analysis by Mordor Intelligence

The Europe stone plastic composite flooring market size is expected to increase from USD 4.32 billion in 2025 to USD 4.64 billion in 2026 and reach USD 6.58 billion by 2031, growing at a CAGR of 7.24% over 2026-2031. The policy environment supports this trajectory, as the EPBD recast embeds whole-life-cycle carbon considerations for buildings and sets stepped renovation requirements that raise demand for fast, low-disruption flooring systems[1]ENERGY.EC.EUROPA EUhttps://energy.ec.europa.eu/topics/energy-efficiency/energy-performance-buildings/energy-performance-buildings-directive_en. Adoption also benefits from REACH diisocyanate training mandates that steer installers toward click install solutions, which reduce exposure to adhesives and speed up projects. France’s Extended Producer Responsibility (EPR) eco-modulation under the PMCB scheme incentivizes recycled content and design for reuse, favoring stone plastic composite (SPC) formulations that enable circularity and demountability. Competitive dynamics remain active as the European SPC flooring market faces price pressure from imports, while European brands lean on patented locking systems, EPD transparency, and local service to defend market share.

Key Report Takeaways

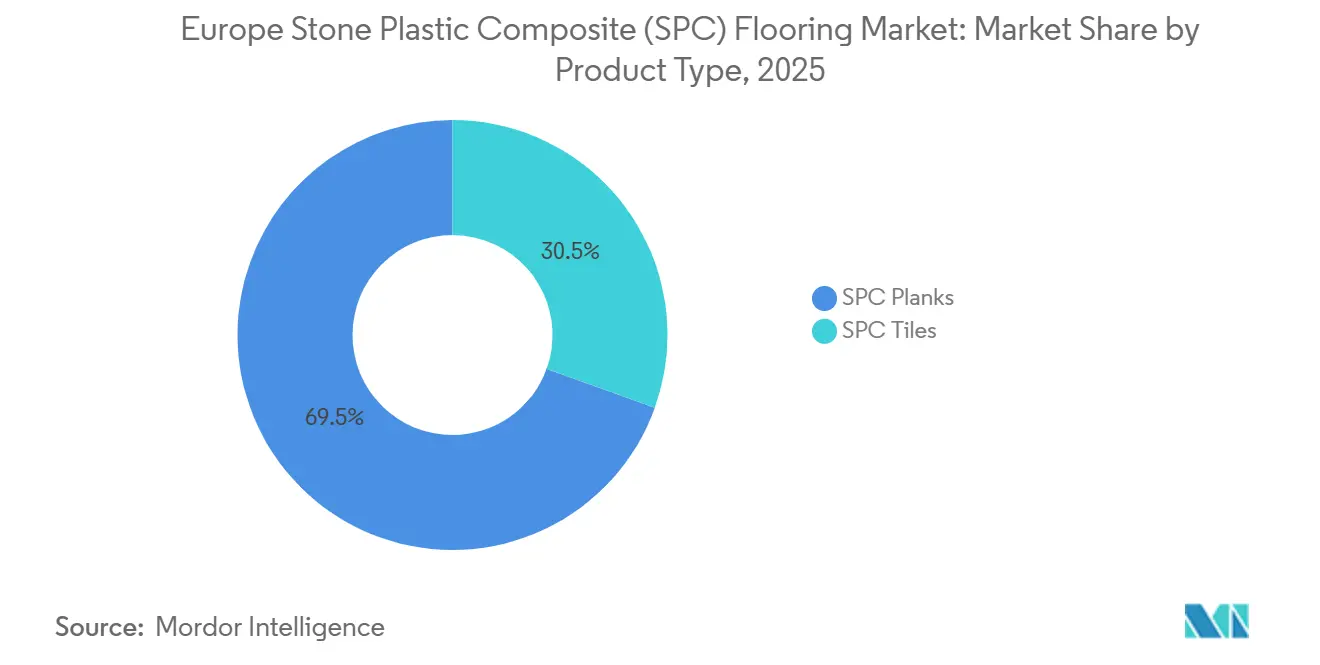

- By product type, SPC planks led with 69.50% of the Europe SPC flooring market share in 2025, while SPC tiles are projected to grow at a 7.40% CAGR to 2031.

- By product thickness, 5.1–6.0 mm captured 33.60% of the European SPC flooring market share in 2025, while formats above 6.5 mm are projected to expand at a 7.85% CAGR through 2031.

- By installation method, interlocking or click-lock captured 81.15% of the market share in 2025. By installation method, interlocking or click-lock is projected to expand at an 7.23% CAGR through 2031.

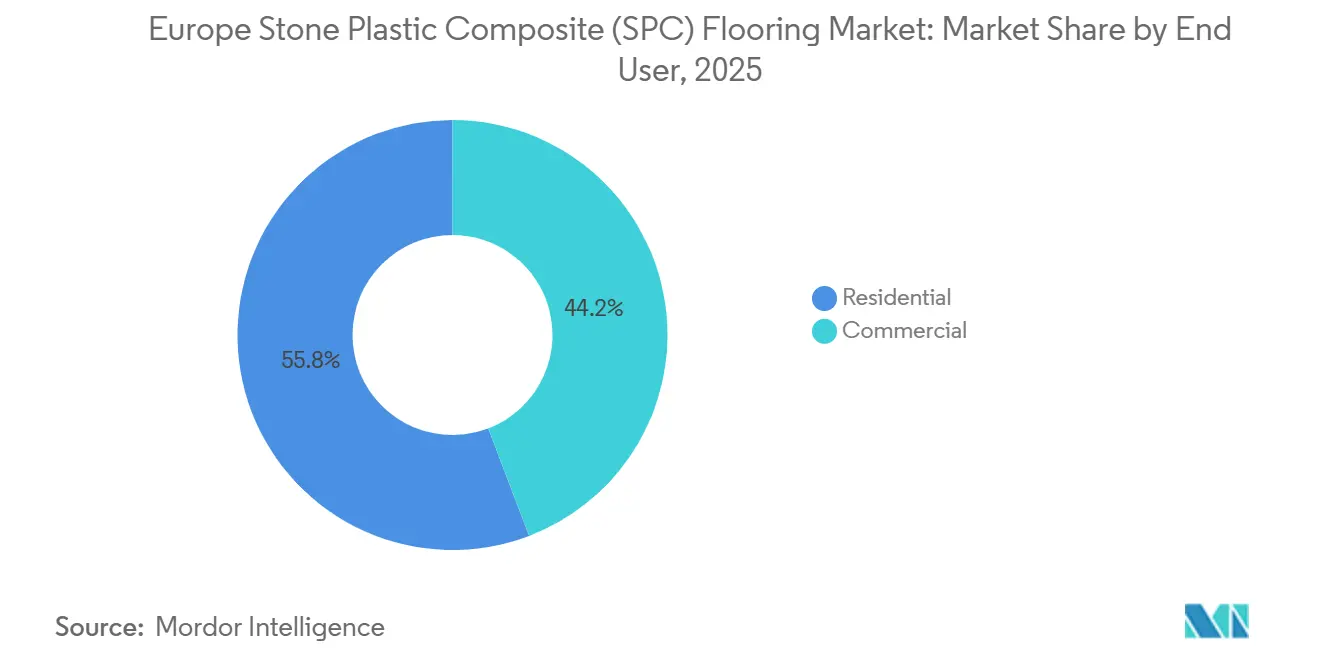

- By end user, residential accounted for 55.80% of the Europe SPC flooring market share in 2025, while commercial is expected to record a 7.35% CAGR to 2031.

- By distribution channel, specialty flooring retailers within B2C/retail held 36.73% of the European SPC flooring market share in 2025, while online is projected to grow at an 8.65% CAGR through 2031.

- By geography, Germany retained 19.80% of the Europe SPC flooring market share in 2025, while Spain is projected to grow at a 7.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Stone Plastic Composite (SPC) Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPBD recast and renovation wave accelerate residential and public building retrofits (demand pull for fast, low-disruption flooring) | +1.2% | Global EU-27, Norway, Switzerland, UK; strongest in Germany, France, Netherlands (large public building stock) | Medium term (2-4 years) |

| SPC's rising share within multilayer modular flooring (MMF) channels shifts specifications toward rigid core designs | +1.1% | Western Europe (Germany, France, BENELUX); spillover to Spain, Italy, and Poland | Medium term (2-4 years) |

| Low-VOC and phthalate restrictions drive phthalate-free rigid LVT/SPC adoption | +0.7% | EU-27, aligned with CPR and national VOC limits; France A+ labeling | Short term (≤ 2 years) |

| Brand and EU circularity programs (VinylPlus, EU Ecolabel/CPR/ESPR) reward recycled content and traceability | +0.9% | EU-27, Norway, Switzerland, UK; early gains in France (EPR eco-modulation), Germany (VinylPlus Deutschland programs) | Long term (≥ 4 years) |

| REACH diisocyanates training nudges installers from glue-down to click rigid-core systems | +1.0% | EU-27, UK; highest impact in Germany, Austria, Netherlands (large installer base with mandatory training compliance) | Short term (≤ 2 years) |

| France PMCB EPR eco-modulation (bonuses/penalties) favors recyclable, detachable, take-back-ready SPC | +0.8% | France initially, with potential spillover to Belgium and Spain, as EPR schemes expand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy Performance of Buildings Directive (EPDB) Recast and Renovation Wave, Fast Low‑Disruption Flooring Demand

The EPBD recast requires member states to transpose updated energy performance rules and to adopt whole-life-cycle assessments for new buildings, which underscores the importance of materials that combine speed, carbon efficiency, and low operational disruption in retrofit work. SPC’s rigid mineral core enables direct installation over many existing substrates, helping contractors compress schedules in occupied buildings and public facilities that must remain open. SPC volumes in France reached 13.9 million m² in 2024, surpassing Germany for a second year as public programs and consumer preferences aligned with quick install solutions[2]MMFA.EU https://mmfa.eu/en/2025/03/19/2024-sales-figures-steady-growth-for-mmfa-members-as-spc-continues-its-upward-trajectory. Capital deployment within European manufacturing reinforces this direction, including Unilin’s 2025 investment to accelerate production and surface customization for rigid formats that target renovation use cases. Nordic markets reinforce the connection between policy and product choice, with Denmark and Norway each exceeding 1 million m² of SPC in 2024 alongside strong growth from a base of demanding public procurement standards. These conditions collectively channel budget and specifications toward the European SPC flooring market as agencies and building owners prioritize certified products that can be installed with minimal disruption.

SPC Share Gains Within MMF, Rigid Core Specification Shift

Within Europe's multilayer modular flooring (MMF) ecosystem, SPC expanded its share to 75% of the MMF category in 2024, up from 65% in 2023, as specifiers favored dimensional stability alongside wood- and stone-look versatility. The category shift correlated with declines in LVT click-through rate (CTR) and EPC as buyers converged on rigid cores that better withstand moisture variation and heavy traffic. Markets such as Italy and Poland posted strong 2024 increases in polymer products, reflecting consumer and institutional projects that prefer waterproof, scratch-resistant surfaces in refurbishments. The publication of an SPC EPD by MMFA in March 2025 provides members with a standardized way to communicate environmental performance to public buyers, supporting bid compliance and documentation in tenders that require verified life-cycle data. Spain’s 2024 rebound highlighted hospitality and mixed-use projects that favor rigid-core tile looks for faster room turns and coordinated maintenance in high-traffic spaces. This set of choices continues to move specifications toward SPC, supporting volume growth in the European SPC flooring market even as new-build cycles soften.

Phthalate Free Rigid LVT/SPC, VOC Rules Speed Substitution

Indoor air quality criteria across Europe shape materials selection, and brand launches have highlighted third-party emission certifications to reassure specifiers and consumers. PROJECT FLOORS SPC Collection introduced in 2025 includes an Indoor Air Comfort Gold certificate and a product pass for transparency, which signal alignment with low-emission expectations in both residential and commercial buildings. On the recycling side, VinylPlus reported sorting and processing advances that allow removal of legacy plasticizers from post-consumer streams, enabling higher recycled content without triggering hazardous substance penalties in markets like France. These steps make it easier for manufacturers to pursue eco-modulation bonuses under EPR schemes when their products demonstrate recyclability and reduced hazardous content. Region-specific product lines, including Tarkett Elegance Rigid 55, introduced for Greece with a 5.5 mm total thickness and TEKTANIUM surface treatment, illustrate how brands adapt rigid core features to local preferences while maintaining click install benefits[3]TAPEN.GR https://tapen.gr/portfolio/lvt-tarkett-elegance-rigid-55. The interplay of emissions labeling, recycled content validation, and resilient design lines supports steady adoption across the European SPC flooring market as buyers balance compliance and performance.

EU Circularity Programs, EPR, and Ecolabels Accelerate Recycled Content Use

France's PMCB (Produits et Matériaux de Construction du Bâtiment) EPR program applies eco-modulation to building products, rewarding recycled content and design for reusability, which directly affects SPC material choices and construction logistics. Company actions align with this direction, such as Mohawk’s SolidTech R initiatives and broader 2026 investment plans that emphasize material efficiency and circular design across European operations. VinylPlus reported 724,638 tonnes of PVC recycled in 2024, along with rising converter uptake of rPVC, indicating stable post-industrial flows and a gradual increase in post-consumer participation[4]VINYLPLUS.EU https://www.vinylplus.eu/our-achievements/progress-report-2025. Post-consumer flooring recycling is still emerging, with 2023 figures below total potential as systems build capacity, but pilots such as Revinylfloor have demonstrated detection technologies that improve sorting fidelity. Complementary programs like the UK’s Recofloor expand return logistics and improve material quality through contractor and distributor participation, helping to raise circularity credentials in public tenders. With EPR incentives maturing and recycling infrastructure expanding, these pathways reinforce demand for SPC products designed for reuse, recovery, and verified traceability across the European SPC flooring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Broad PFAS restriction proposals could affect topcoats/auxiliaries, raising reformulation risk | -0.6% | EU-27, Norway; highest uncertainty in Germany, Netherlands, Denmark (PFAS-proposal submitters) | Medium term (2-4 years) |

| Construction slowdown and logistics/raw-material cost swings pressure demand and margins | -0.9% | EU-27, UK; acute in Germany (residential -11.8% wood 2024), France (LVT click -21.9% 2024) | Short term (≤ 2 years) |

| France PMCB EPR eco-contributions increase producer/importer compliance costs | -0.4% | France; potential expansion to other EU markets adopting building-product EPR schemes | Short term (≤ 2 years) |

| EU fire classification (Bfl-s1/s1 smoke) plus acoustic layers add testing/CE-mark costs | -0.5% | EU-27, Norway, Switzerland, UK; strongest in commercial/public procurement (Germany, NORDICS, France) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PFAS‑Related Topcoat Reformulation Risks

The EU REACH PFAS restriction creates uncertainty for coatings and auxiliaries used in high-performance surface treatments, prompting suppliers to validate alternative chemistries early. Many brands have highlighted low-emission, durable finishes that meet intensive-use standards without relying on problematic additives, and this trend continues as the ECHA PFAS proposal evolves. Procurement criteria in public projects typically reward documentation and third-party testing, incentivizing companies to align coating systems with anticipated restrictions. This can add time and cost to product development as suppliers test EN 13329 wear testing alongside emissions outcomes to maintain specifications. As brands move their ranges toward PFAS-free products, the transition period may shift launch calendars and assortment decisions for premium lines in the European SPC flooring market.

Construction Slowdown and Raw Material Volatility

Category mix within flooring shifted in 2024 as wood and LVT click volumes fell in Eurostat-tracked indices, which indicates softer discretionary spending and project deferrals in parts of the residential segment. While SPC gained share in multilayer modular flooring, margin pressure intensified for producers facing higher logistics costs and uneven resin pricing due to the ECB cycle. Operational responses have included restructuring and EU capex discipline to improve productivity while preserving capacity in priority lines. In the near term, the demand backdrop remains sensitive to housing activity, the ECB's 4% rate, and public-sector budget timing across municipalities. This creates a planning environment in which volume risk and cost variability need to be balanced with the retrofit pull supported by the EU Renovation Wave in the European SPC flooring market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Planks Dominate as Tiles Gain in Hospitality and Healthcare

SPC planks held 69.50% of Europe's SPC flooring market share in 2025, reflecting consumer preference for wood look visuals and installers’ need for fast, floating systems in renovation projects. The European SPC flooring market benefits from this format’s ability to bridge the DIY and professional channels by using the same core sizes and wear layers, simplifying inventory and shortening installation time on occupied sites. Click profiles and integrated underlays help reduce noise transmission, which remains important in multi-family buildings and top-floor conversions. The European SPC flooring market also sees value in product lines that pair robust wear layers with embossed-in-register textures to improve realism in living spaces and retail zones. This combination of speed, aesthetics, and day-two maintenance advantages makes planks the default choice in residential upgrades and a mainstay in light commercial programs.

SPC tiles are projected to grow at a 7.40% CAGR to 2031 as hospitality, healthcare, and mixed-use refurbishments prioritize large-format stone looks and slip-resistant finishes that maintain uptime. The European SPC flooring market size for tile formats is expected to expand alongside region-specific launches that tailor formats, thicknesses, and finishes for public projects and hotel rooms. Tile layouts can reduce waste in square rooms and open areas, and glue-down installation in corridors or lobbies can enhance point load resilience where trolleys or gurneys are common. New assortments for Southern Europe, including Elegance Rigid 55, introduced for Greece, show how brands position mineral core tiles for heavy residential and moderate commercial applications with clear performance ratings. As public procurement emphasizes certified materials and predictable maintenance, tile designs will steadily capture a larger slice of the European SPC flooring market in projects that benefit from stone aesthetic continuity and robust cleanability.

By Product Thickness: 5.1–6.0 mm Leads, Ultra Thick Builds Momentum

The 5.1–6.0 mm band captured a 33.60% share in 2025, anchoring the volume center of the category by balancing cost, weight, and performance for everyday use. This range serves mid-tier residential and light commercial environments where floating installation and integrated underlay offer a straightforward path to comfort and sound control. Company assortments in this zone often highlight formaldehyde-free and low-emission claims, as well as Class 23 or 31 ratings that broaden placement options across rooms. Examples on the market include budget-oriented rigid core lines that promote click ease, durability, and compatibility with standard underfloor heating systems for modern apartments. The European SPC flooring market relies on this sweet spot to deliver consistent throughput across both specialty retail and trade accounts.

Formats above 6.5 mm are projected to grow at a 7.85% CAGR through 2031 as specifiers in luxury residential and premium commercial segments seek greater underfoot solidity and improved impact sound performance. The European SPC flooring market size for these thicker profiles will scale with projects that emphasize acoustic upgrades and dent resistance under rolling loads. Retail offerings demonstrate how added core density and integrated insulation help meet Class 23 and 34 use ratings while preserving click install convenience in intensive spaces. France’s EPR eco-modulation framework further favors designs that withstand disassembly and reinstallation without damage to locking profiles, thereby strengthening the case for robust cores in circular models. Over the forecast, thicker formats will continue to gain penetration in rooms where premium acoustics and durability carry more weight than cost per square meter.

By End User: Residential Drives Revenue, Commercial Advances on Lifecycle Value

Residential accounted for 55.80% of revenue share in 2025, supported by a large installed base and steady renovation cycles in kitchens, bathrooms, living rooms, and hallways. Buyer priorities include waterproof performance, dimensional stability, and straightforward floating installs that avoid adhesive certifications under REACH diisocyanate requirements. The European SPC flooring market earns trust in this channel through certified indoor air profiles, long domestic warranties, and a wide range of décor selections that align with current color and texture preferences. Brand portfolios also highlight options with recycled content to meet household sustainability goals alongside value and practicality. Company disclosures in 2026 underscore continued investment in European capacity and product development to serve these demand patterns.

Commercial is projected to grow at a 7.35% CAGR as hotels, offices, healthcare buildings, and education facilities focus on lifecycle cost, predictable maintenance, and compliance documentation. The European SPC flooring industry continues to adapt by offering products with higher wear layers, slip resistant finishes, and environmental product data that align with public tender requirements. Programs like VinylPlus and Recofloor expand the circular toolkit available to specifiers planning replacement cycles and material recovery over building lifetimes. In hospitality, rigid core tiles often displace ceramic in guestrooms to speed refurbishment and reduce downtime, while heavy use corridors may keep glue down products for point load performance. Company investments in European plants and R&D centers are designed to protect lead times and customize assortments for these varied commercial needs.

By Installation Method: Click-Lock Leads, While Adhesive Keeps a Specialized Commercial Role

Interlocking or click-lock systems held 81.15% share in 2025, making them the leading installation method across residential and commercial SPC flooring applications in Europe. Their lead reflects a broader move toward faster, simpler installation, especially in renovation work, where shorter project timelines and lower disruption matter. Since August 2023, REACH rules have required training for professional users of diisocyanate-containing polyurethane adhesives, adding compliance steps and extra costs for installers and making adhesive-free systems more appealing. Click-lock products also align well with France’s PMCB EPR eco-modulation framework, which rewards reusable and demountable building materials, as these floors can be removed and reinstalled with minimal damage. This combination of easier installation, lower handling complexity, and stronger circularity credentials continues to support click-lock demand across the European SPC flooring market.

Interlocking or click-lock is also projected to grow at a 7.23% CAGR through 2031, showing that floating systems are likely to keep expanding their role even as adhesive methods retain a clear niche in demanding commercial applications.

By Distribution Channel: Retail Holds Scale, Online Rises on Click Install Confidence

Specialty flooring retailers within B2C/retail held 36.73% of the European SPC flooring market share in 2025, while online is projected to grow at an 8.65% CAGR through 2031. The European SPC flooring market benefits from retail displays that present wear layers, surface textures, and acoustic options side by side, which helps households and small contractors align on performance and price. Showrooms also support higher ticket assortments that combine certified emissions, scratch resistance, and long warranties, which justify premium positioning. European production investments feed this channel by ensuring consistent lead times for décor breadth and surface realism, reducing substitution risk during busy renovation periods.

Online is projected to grow at an 8.65% CAGR as buyers gain confidence in standardized sizes, simple installation, and return policies that reduce purchase risk. The European SPC flooring market for e-commerce will expand as brands optimize content, sampling, and logistics for direct delivery to households and microcontractors. Product pages that clearly show performance ratings, emissions certificates, and installation guides can shorten the evaluation cycle and convert consideration to purchase. Retailers and brand sites also use curated décor sets to guide room-by-room choices, helping bridge the gap between the showroom experience and digital convenience. As regional warehouses and cross border delivery networks improve, online volumes will continue to complement store-based sales without displacing the consultative role of specialty retail in the Europe SPC flooring market.

Geography Analysis

Germany retained 19.80% of Europe's SPC flooring market share in 2025, supported by its broad distributor base and the embedded role of installers in residential refurbishment. Polymer product volumes in Germany rose in 2024, although the pace reflected broader housing softness that tempered category expansion. France led Europe in SPC by volume for a second year in 2024, and its EPR framework strengthens incentives for products that demonstrate recycled content and reusability. Documented EPDs for SPC now assist in public projects across DACH and France, where verified environmental data is a procurement requirement. These conditions sustain demand in both countries even as the mix of residential and public retrofit activity evolves through the forecast.

Spain is projected to be the fastest growing large market at a 7.60% CAGR to 2031 as tourism related renovations and coastal housing upgrades continue. Spain posted a strong 2024 rebound in polymer products, which balanced earlier construction lulls and positioned distributors for improved throughput in 2026. Italy and Poland also advanced sharply in 2024 as residential and social housing programs specified waterproof surfaces with straightforward maintenance. Nordic markets remained notable for high SPC penetration relative to population and for digital adoption that shortens the path from research to purchase. The UK also expanded in 2024, helped by established take back logistics that reinforce sustainability claims in commercial and public projects.

Across Europe, 2024 category results illustrated how renovation activity and public funding support can counterbalance softer new build indicators, especially when product documentation and circular pathways are in place. The European SPC flooring market will continue to align with policies that value speed, verified emissions, and recoverability, which suits rigid cores that click together over older surfaces. The combination of national subsidy programs, EPR incentives, and installer familiarity creates a path for steady adoption through the forecast window.

Competitive Landscape

The European SPC flooring market shows moderate fragmentation, with the top five players estimated to hold about 30-40% combined share, while many regional converters and importers compete on price and service. European brands lean on production investments and design differentiation to protect throughput and reduce substitution risk during peak renovation months. Unilin’s 2025 investment in Belgium increased maximum capacity and improved surface realism through AI-enabled processes, helping supply flagship assortments to showrooms across the region. VinylPlus participation and EPD documentation strengthen credibility in public tenders that require traceable environmental data and recovery options.

Competition intensifies around three themes that matter to specifiers and retailers: installation speed, documented environmental performance, and proven durability in high-use areas. Programs like Recofloor and company product passes for emissions transparency help support procurement requirements while guiding take-back and recycling in commercial rollouts. European portfolios also reflect regional preferences through tile-led lines in hospitality markets and thicker formats where acoustic comfort is a purchase driver. As these themes sharpen, the European SPC flooring market remains open to challenger brands that offer credible documentation, stable lead times, and localized support.

Disciplined capital plans in 2026 indicate continued focus on cost efficiency and product development to navigate margin pressure from imports and logistics variability. Restructuring actions in 2025 aimed to align capacity with demand while protecting innovation pipelines for rigid core and hybrid ranges in Europe. These steps, combined with association-led EPDs and expanded take-back logistics, position leading suppliers to compete effectively for renovation work that values certified materials and predictable installation.

Europe Stone Plastic Composite (SPC) Flooring Industry Leaders

Mohawk Industries

Tarkett

Gerflor

Beaulieu International Group (BerryAlloc)

James Halstead plc (Polyflor)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mohawk Industries reported Q4 2025 results, disclosing plans to invest approximately USD 480 million in 2026 for capacity expansion projects, cost-reduction initiatives, and operational improvements across its Flooring Rest of World segment, which includes Europe. The company anticipates improved sales and earnings in 2026 as European housing markets benefit from lower mortgage rates and greater availability of existing homes.

- March 2026: Karndean Designflooring launched three new "Design Aesthetics" (Senti, Luma, Dopa•Mine) for 2026, building on a 2025 concept. These curated interior design styles are paired with resilient flooring recommendations and promoted directly to consumers via social media and the company website, supported by brochures and product knowledge sessions for retailers.

Europe Stone Plastic Composite (SPC) Flooring Market Report Scope

| SPC Tiles |

| SPC Planks |

| 4.0–5.0 mm |

| 5.1–6.0 mm |

| 6.1–6.5 mm |

| Above 6.5 mm |

| Self-Adhesive |

| Glue-Down |

| Interlocking/Click-lock |

| Others |

| Residential |

| Commercial |

| B2C/Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX |

| NORDICS |

| Rest of Europe |

| By Product Type | SPC Tiles | |

| SPC Planks | ||

| By Product Thickness | 4.0–5.0 mm | |

| 5.1–6.0 mm | ||

| 6.1–6.5 mm | ||

| Above 6.5 mm | ||

| By Installation Method | Self-Adhesive | |

| Glue-Down | ||

| Interlocking/Click-lock | ||

| Others | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the Europe stone plastic composite flooring market growth outlook to 2031?

The Europe stone plastic composite flooring market size is projected to reach USD 6.58 billion by 2031 at a 7.24% CAGR over 2026–2031, supported by policy‑driven renovations and product innovation.

Which formats lead demand across Europe in 2026?

SPC planks lead due to quick floating installs and broad décor choices, while tiles gain in hospitality and healthcare, where stone looks and slip resistance matter.

How do EU policies affect SPC flooring specifications?

The EPBD recast elevates whole‑life‑cycle performance in renovations, and France’s PMCB EPR rewards recycled content and reusability, which favor compliant SPC designs.

Which end-user segments show the strongest momentum?

Residential holds the largest share at 55.80%, while commercial shows faster growth at 7.35% CAGR as tenders value lifecycle cost, emissions documentation, and recoverability.

Which European geographies are most attractive through 2031?

Germany remains a large, structured market with 2025 leadership by share, while Spain shows the fastest projected growth at 7.60% CAGR in hospitality and coastal renovations.

What documentation supports public tender compliance for SPC?

EPDs from MMFA and program participation through VinylPlus or Recofloor help meet specification and circularity requirements in public and large private projects.

Page last updated on: