Asia-Pacific Stone Plastic Composite (SPC) Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

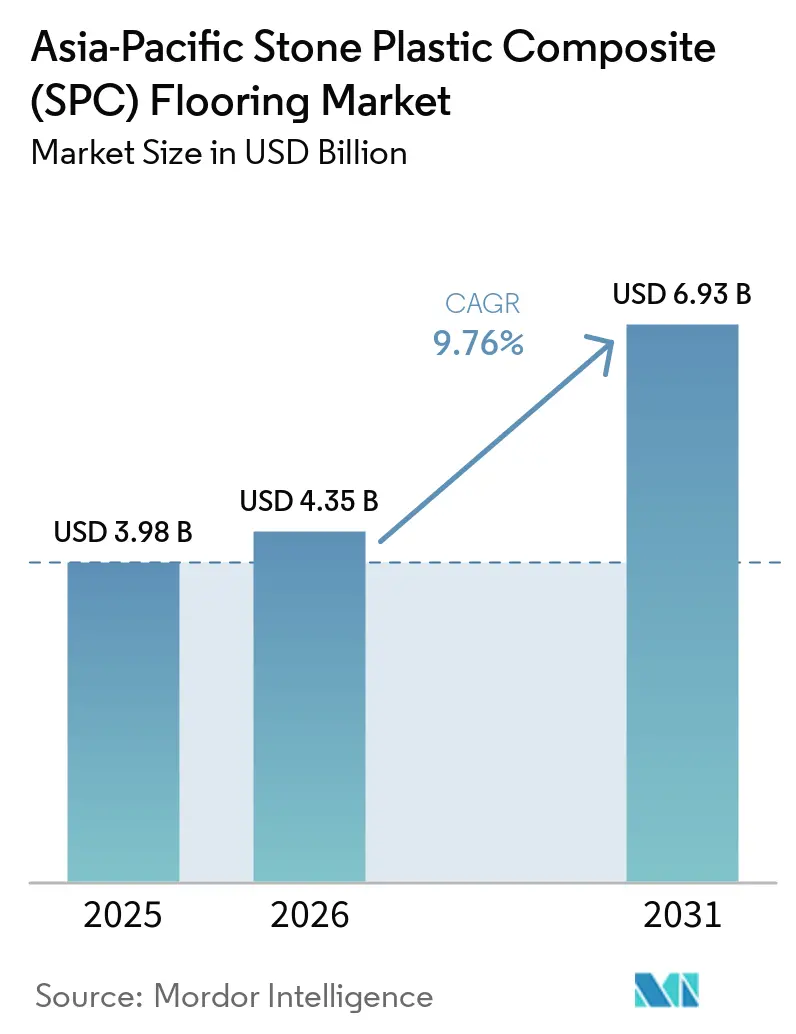

| Base Year Market Size (2025) | USD 3.98 Billion |

| Market Size (2026) | USD 4.35 Billion |

| Market Size (2031) | USD 6.93 Billion |

| Growth Rate (2026 - 2031) | 9.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Stone Plastic Composite (SPC) Flooring Market Analysis by Mordor Intelligence

The Asia-Pacific stone plastic composite flooring market size was valued at USD 3.98 billion in 2025 and is estimated to grow from USD 4.35 billion in 2026 to reach USD 6.93 billion by 2031, at a CAGR of 9.76% during the forecast period (2026-2031). Demand is strengthening across renovations, commercial upgrades, and new housing in China, India, and Southeast Asia, as waterproof rigid-core products continue to displace moisture-sensitive finishes in humid and monsoonal climates. The Asia-Pacific SPC flooring market is also benefiting from improved installation systems that reduce downtime and from capacity expansions in Vietnam and China, which are shortening lead times for large buyers. In Japan and South Korea, apartment sound insulation rules are accelerating the shift toward thicker formats with integrated acoustic pads, raising average selling prices and steering buyers toward premium specifications. The Asia-Pacific SPC flooring market is poised for steady growth through 2031, as low lifecycle costs in healthcare, hospitality, and retail projects align with measurable installation and maintenance advantages relative to traditional tile and engineered wood[1]VIVIDCOZYTILE.COM https://vividcozytile.com/blog/spc-flooring-benefits-installation-cons.

Key Report Takeaways

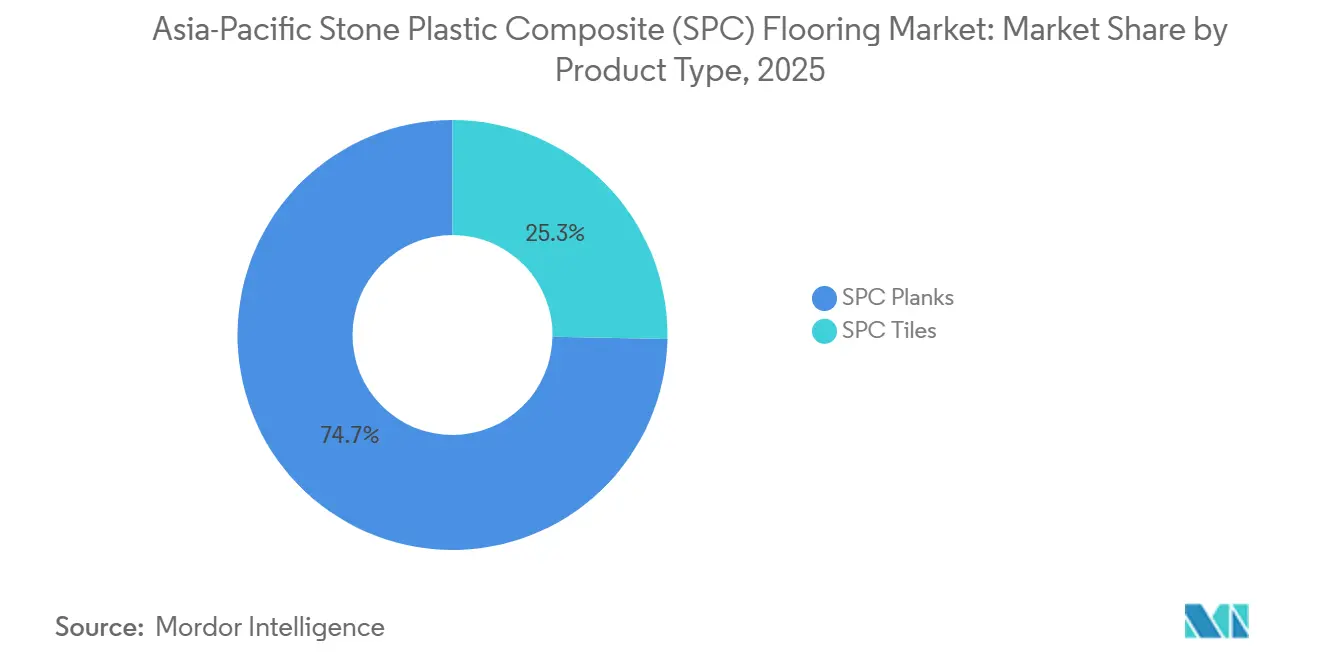

- By product type, SPC planks led with 74.71% of the Asia-Pacific SPC flooring market share in 2025, while SPC tiles are projected to record the fastest growth at 8.20% CAGR through 2031.

- By product thickness, the 5.1–6.0 mm category accounted for a 35.40% of the Asia-Pacific SPC flooring market share in 2025, and formats above 6.5 mm are forecast to grow at 8.57% CAGR through 2031.

- By installation method, interlocking or click-lock captured 84.55% of the market share in 2025. By installation method, interlocking or click-lock is projected to expand at an 8.72% CAGR through 2031.

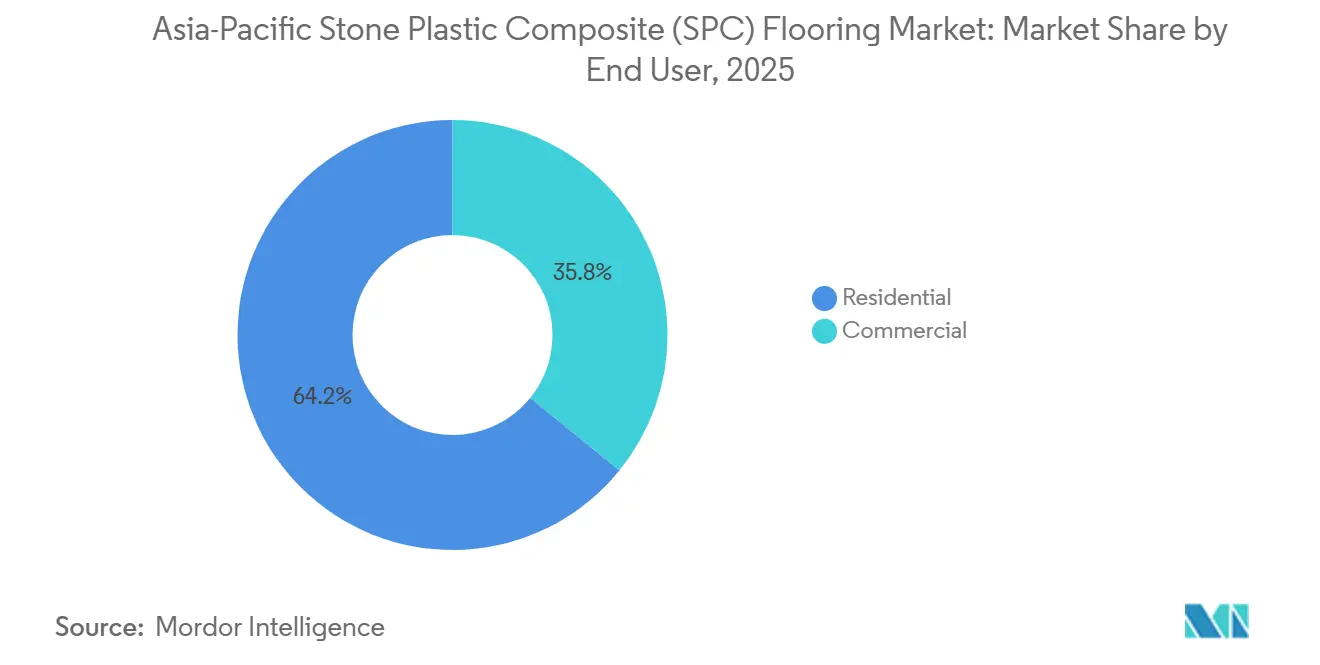

- By end user, residential commanded 64.17% of the Asia-Pacific SPC flooring market share in 2025, and commercial applications are on track to expand at a 9.24% CAGR through 2031.

- By distribution channel, B2C retail captured 33.24% of the Asia-Pacific SPC flooring market share in 2025, and online distribution is expected to post the highest growth at 11.53% CAGR through 2031.

- By geography, China retained 41.30% of the market share in 2025, while India is projected to grow at a 10.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Stone Plastic Composite (SPC) Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China's urban renewal-fueled renovation demand | 1.8% | China tier-2/tier-3 cities, spill-over to ASEAN renovation corridors | Medium term (2-4 years) |

| Waterproof rigid-core and click-lock, enabling fast refurb | 1.5% | Global, particularly coastal SEA (Vietnam, Thailand, Indonesia) and monsoonal India | Short term (≤ 2 years) |

| Adoption in healthcare, hospitality, and retail upgrades | 1.2% | APAC commercial hubs (Singapore, Bangkok, Mumbai, Seoul) | Medium term (2-4 years) |

| APAC SPC capacity expansions are improving availability | 1.1% | Vietnam, Thailand, China (Hebei, Jiangsu production zones) | Short term (≤ 2 years) |

| Apartment sound insulation standards (LL45/LL40) push thicker SPC | 0.9% | Japan and South Korea, with early adoption in tier-1 China condominiums | Long term (≥ 4 years) |

| Pre-grouted SPC tile innovations speeding tile-look installs | 0.7% | Global, with concentration in China, Vietnam, manufacturing hubs exporting to the US, EU. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

China Urban Renewal Amplifies Tier-2 Replacement Cycles

China’s policy direction for greener materials and lower-VOC construction products is encouraging wider use of rigid-core flooring in both newbuilds and renovations, which supports replacement cycles in large tier-2 and tier-3 city clusters[2]SUNLYSPC.COM https://www.sunlyspc.com/news/2026-market-outlook-oak-spc-floors-lead-with-aesthetics-performance-as-chinese-manufacturers-upgrade-technology-to-solve-industry-pain-points/. According to the National Bureau of Statistics of China, the country’s urbanization rate has exceeded 65%, reinforcing sustained residential turnover in secondary cities. In many of these markets, apartment flooring replacement is closely linked to property resale cycles. Waterproof click-lock SPC systems (typically 4–6 mm thick with 0.3–0.7 mm wear layers, as defined in resilient flooring specifications such as ASTM F3261) reduce installation downtime compared with ceramic tile systems, which require adhesive curing periods of 24–72 hours. Leading Chinese manufacturers have invested in denser core profiles and higher-wear layers. At the same time, some groups have added parallel bases in Vietnam or Thailand to serve tariff-sensitive export lanes more predictably. Production footprints in Hebei and Jiangsu now complement Southeast Asian capacity, helping balance lead times and improving resilience to trade policy swings. As these supply-side improvements align with China’s steady renovation cadence, the Asia-Pacific SPC flooring market is seeing broader geographic participation from both inland and coastal buyers.

Waterproof Rigid-Core Click Systems Collapse Refurbishment Lead Times

SPC’s waterproof limestone-PVC core and tool-free click systems significantly shorten renovation projects, reducing installation times by 30–50% compared with glue-down vinyl systems, as indicated in resilient flooring installation guidelines and ASTM F3261-based application practices. This makes it important for occupied apartments and fast-turnover commercial spaces where downtime directly affects revenue. Residential buyers place a high value on waterproofing for kitchens, bathrooms, and entries, and click-lock installation lowers disruption for families in small urban flats during refurbishments. Rigid-core formats installed over existing substrates limit demolition and reduce the need for leveling compounds, cutting labor hours, and making overnight or weekend retrofits feasible. As a result, the Asia-Pacific SPC flooring market continues to win specifications in both residential and commercial refresh programs where predictable schedules and clean turnarounds are essential.

Healthcare, Hospitality, and Retail Prioritize Low-Lifecycle-Cost Surfaces

Commercial-grade SPC with 0.5 mm wear layers and durable topcoats withstands high abrasion, making it suitable for facilities that manage heavy foot traffic and frequent cleaning cycles. Healthcare operators favor grout-free, easily sanitized surfaces that support quick disinfection routines, a requirement that has increased interest in rigid-core floors with consistent performance under aggressive cleaning chemicals. In hospitality projects, design fidelity to wood or stone at lower installed and maintenance costs strengthens the business case, as owners replace surfaces during soft renovations at four-to-seven-year intervals. Retail landlords and mall operators value impact resistance around entries and point-of-sale areas, and many specifications now call for rigid-core products in these zones to minimize chipping and grout staining risks common with tile under rolling cart traffic. Over the long term, SPC’s maintenance outlays compare favorably with those of ceramic and solid wood, which is one reason the Asia-Pacific SPC flooring market continues to penetrate cost-conscious commercial programs.

APAC Capacity Build-Out Tightens Lead Times and Localizes Supply Chains

Vietnam’s SPC capacity has scaled rapidly, with factory investments and advanced click-lock licenses enabling larger volumes for export markets under favorable tariff conditions. CFL Flooring’s new 750,000-square-foot plant near Haiphong began shipping in late 2024, which strengthens Vietnam’s role as a complementary base to China for diversified sourcing programs. In northern China, DECNO’s expanded base integrates production, storage, and exhibition functions, built to serve mid- to high-end SPC demand domestically and abroad[3]DECNOFLOORINGS.COM https://www.decnofloorings.com/news-events/SPC-production-base.html. Capital equipment providers such as StarsPlas are enabling turnkey SPC lines across Thailand and Vietnam, often with flexible financing that helps distributors localize manufacturing and reduce working capital risk. As these facilities ramp up, the Asia-Pacific SPC flooring market is experiencing shorter order-to-delivery cycles for ASEAN buyers, which supports just-in-time inventory strategies and reduces warehousing overhead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC sustainability/EPR raising compliance costs | -0.9% | Vietnam, Singapore, Philippines (mandatory schemes); Thailand, Malaysia (emerging frameworks) | Medium term (2-4 years) |

| PVC/plasticizer feedstock price volatility | -1.3% | Pan-APAC, acute in India, South Korea, and import-dependent SEA markets | Short term (≤ 2 years) |

| Competition from ceramic tile and engineered wood | -0.6% | Price-sensitive residential segments across India, China, tier-3 cities, and SEA markets | Long term (≥ 4 years) |

| Condo acoustic rules are increasing the installed system cost | -0.4% | Japan, South Korea, and premium China developments requiring LL40 compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EPR Mandates and Circularity Specifications Inflate Per-Unit Compliance Burdens

Extended Producer Responsibility (EPR) frameworks are tightening across ASEAN, pushing producers to fund collection, recycling, or stewardship schemes and increasing compliance obligations for plastics value chains. In Vietnam, the EPR policy includes mandated recycling or financial contributions to a national environmental protection fund, and similar approaches are influencing business planning in neighboring markets. In the Philippines, the EPR Act (Republic Act No. 11898) sets escalating recovery obligations for large enterprises, with mandated recovery rates increasing progressively up to 80% by 2028, directly influencing packaging, labeling, and product stewardship design for imported resilient flooring materials. Australia’s competition regulator authorized the ResiLoop stewardship program for resilient flooring, which supports a collection and recycling pathway and sets a precedent that many specifiers now look for in supplier credentials. These changes create new cost items and process requirements for supply chains that rely on PVC, and the Asia-Pacific SPC flooring market is adjusting product designs and documentation to align with public procurement and large-firm sustainability criteria.

Feedstock Price Surges Triggered by Supply Disruptions and Refinery Constraints

PVC resin pricing and upstream feedstock costs remain highly sensitive to global petrochemical cycles, with ethylene (a key PVC input derived largely from naphtha cracking) representing a major share of production economics, making flooring costs vulnerable to oil-linked volatility. In 2024, disruptions in Red Sea shipping routes extended container transit times on Asia–Europe corridors by an estimated 10–15 days, increasing freight and insurance costs for polymer exports from China and Southeast Asia into import-dependent markets such as India and the Middle East. These logistics pressures have compounded existing refinery constraints and periodic maintenance shutdowns in Asia-Pacific petrochemical hubs, tightening spot availability of PVC resin and plasticizers. For large infrastructure and institutional tenders, this volatility reduces the feasibility of long fixed-price contracts, as input costs can shift within a single procurement cycle, leading to delayed bidding decisions or shorter validity periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tiles Gain Traction Through Pre-Grouted Innovations

SPC planks dominated the Asia-Pacific SPC flooring market with a 74.71% share in 2025, supported by familiar wood-look aesthetics and straightforward click installations for residential refresh projects. SPC tiles are projected to expand at a 8.20% CAGR through 2031, aided by pre-grouted surface technologies that deliver the look of ceramic without grout maintenance, accelerating adoption in wet-room retrofits and commercial bathrooms[4]I4F.COM https://i4f.com/article/gimig-signs-i4f-ceragrout-license-agreement. Manufacturers are licensing integrated grout-line surface treatments that simulate two tiles on one panel, reducing layout complexity and potentially reducing installation steps for staggered patterns. In markets sensitive to downtime, tiles that click into place without wet trades are a practical alternative to mortar-set ceramic, which is a key reason the Asia-Pacific SPC flooring market continues to expand in bathrooms, entryways, and other wet zones. As product lines broaden into new sizes and finishes, tile-format SPC is improving design continuity alongside plank installations across open-plan spaces and adjacent rooms.

Acoustic compliance in Japan and South Korea is central to product selection, and wet-area tile formats that meet LL40 or LL45 standards are becoming a staple of multi-family retrofits. Developers lean toward heavier, denser cores with integrated foam pads to manage impact sound in vertical living arrangements where noise transmission is regulated by building associations. For project managers, the ability to install SPC tiles as a floating system over existing surfaces without demolition reduces labor and time, which can matter more than small differences in material costs. As these technical and practical features stack up, tiles are capturing more wet-room specifications. At the same time, planks continue to dominate living areas, corridors, and bedrooms across the Asia-Pacific SPC flooring market. The net effect is a clear two-format strategy where tiles complement planks to deliver a uniform aesthetic with lower maintenance and faster project turnover.

By Product Thickness: Premium Acoustics Drive Ultra-Thick Adoption

The 5.1–6.0 mm thickness category accounted for 35.40% of 2025 revenues, serving as a cost-and-handling sweet spot for homeowners and builders who need standard rigidity without premium acoustic layers. In overlay retrofits, thinner 4.0–4.5 mm products are preferred where door and threshold heights limit build-up, especially in apartments with tight tolerances between rooms. Many suppliers are optimizing mid-thickness SKUs with stable cores and protective wear layers that meet everyday residential performance needs, which sustains volume in this segment across the Asia-Pacific SPC flooring market. Residential installers cite predictable click performance and low call-back rates as reasons to keep 5.0–5.5 mm on standard spec lists where acoustic constraints are moderate. As supply chains scale in China and Vietnam, most distributors carry deep assortments in this thickness range to balance price points and design variety for regional markets.

Ultra-thick formats above 6.5 mm are forecast to grow at 8.57% CAGR through 2031, lifted by strict floor impact sound requirements in Japan and South Korea that favor pre-attached IXPE or EVA pads. Many condo associations and property managers enforce LL40 or LL45 equivalents for replacements, which point specifiers to higher-density cores and thicker underlayment layers to control impact transmission. Premium 6.5–7.0 mm planks with integrated pads often advertise IIC and STC ratings that meet common condominium rules, which shifts buyers toward higher-value SKUs within the Asia-Pacific SPC flooring market. The 6.0–6.5 mm tier remains a viable middle ground for budgets that are tighter and acoustic standards that are less prescriptive. Still, regulatory momentum is tilting replacements toward higher thicknesses in high-rise applications. As a result, manufacturers continue to invest in pad-attachment lines and denser core formulations to serve this premium demand profile.

By End User: Commercial Demand Fueled by Rapid Refurbishment Imperatives

Residential accounted for 64.17% of revenues in 2025, reflecting steady adoption in single-family homes, condominiums, and rental-apartment upgrades across large urban centers in India, China, and Southeast Asia. Buyers often prioritize waterproofing and cleanability in kitchens and baths, while plank designs replicate hardwood visuals at lower installed and lifecycle costs than solid wood or ceramic. The Asia-Pacific SPC flooring market benefits from owners’ desire to finish renovations in occupied units quickly, which aligns with floating, click-lock systems and familiar DIY techniques. As supply expands and lead times compress, residential channels are carrying broader assortments with varied decors and wear layers that meet both budget and premium needs. These consumer-facing shifts are reinforcing residential dominance across major APAC cities where apartment turnover and kitchen-bath renovations remain active.

Commercial is projected to grow at a 9.24% CAGR through 2031 as healthcare, hospitality, and retail upgrade to low-maintenance, durable finishes that withstand heavy daily use. Healthcare operators value grout-free, seamless surfaces for infection-control workflows, while hotels rely on resilient finishes to support quick refresh cycles between guest stays. Retail and office common areas increasingly specify rigid-core floors to avoid chipping and grout discoloration, and to simplify cleaning in high-visibility traffic zones. Quick-service restaurants and franchise retail programs can be installed during overnight windows and reopened the next day, which reduces revenue loss relative to wet trades that require curing time. Over time, these practical project economics help the Asia-Pacific SPC flooring market capture a larger share of commercial renovation budgets across the region.

By Installation Method: Click-Lock Systems Hold the Leading Position

Interlocking or click-lock SPC flooring accounted for 84.55% of the Asia-Pacific market in 2025. Its strong position comes from a simple installation process that reduces project time and makes it suitable for both professional installers and homeowners. The system can be laid over many existing subfloors without adhesives or long curing times, helping speed up renovation work in urban housing markets across China, India, and Southeast Asia. In Japan, floating systems with integrated acoustic underlayment also align well with condominium sound-control requirements, which supports their use in high-rise residential projects. The segment’s large share also reflects contractor familiarity, as many flooring teams across major Asian cities already use tools, labor plans, and installation methods built around click-lock products.

Glue-down SPC and loose-lay formats still serve specific commercial needs, but they hold a smaller share because installation typically takes longer and involves higher labor and material costs. These formats remain relevant in airports, hospitals, convention centers, and other heavy-use spaces where stronger joint stability is important under rolling loads and constant traffic. Some suppliers continue to position glue-down SPC for offices, malls, and hotel lobbies where durability at stress points matters more than installation speed. At the same time, pre-attached acoustic underlayment is strengthening the appeal of click-lock systems, especially in projects that need both easy installation and better sound control. This added convenience is helping click-lock products stay ahead as buyers look for flooring solutions that are faster to install and easier to specify.

By Distribution Channel: Digital Platforms Disrupt Traditional Retail Markup Layers

B2C retail captured 33.24% of 2025 sales, anchored by home centers and specialty stores that provide in-person product discovery, design consultations, and immediate availability for homeowners and small contractors. Local dealers also serve as trusted hubs for credit terms, delivery coordination, and jobsite troubleshooting, reinforcing their role in small- and mid-size projects across the Asia-Pacific SPC flooring market. As brands expand assortments and refresh display walls with better EIR textures and durable topcoats, shoppers can compare options side by side and get guided installation advice. This store-based model remains essential in many cities where same-day pickup and face-to-face support drive conversion for residential refurbishments. The Asia-Pacific SPC flooring market continues to rely on strong retail footprints even as digital channels rise.

Online distribution is the fastest-growing channel, with a 11.53% CAGR through 2031, as e-commerce platforms scale rich media tools and improve delivery networks for bulky items. Direct-to-consumer sellers demonstrate how visualization, clear specification sheets, and door-to-door logistics reduce complexity for first-time buyers and support price transparency across brands. Some manufacturers ship from Vietnam or China directly to residential job sites, which tightens landed costs relative to multi-tier distribution in legacy channels. As younger homeowners across India, Thailand, and Indonesia embrace mobile-first buying and simple payment plans, the Asia-Pacific SPC flooring market is seeing deeper digital engagement throughout the buyer’s journey. The long-run effect is a more balanced channel mix, with store-based strengths in consultation and sampling complementing online reach and delivery efficiency.

Geography Analysis

China was the largest country market in 2025, supported by a broad manufacturing footprint and resilient domestic renovation activity that favors waterproof, click-lock installations in many housing scenarios. Evolving product portfolios from established producers in Hebei and Jiangsu have expanded choices for local buyers while strengthening export capabilities for nearby regions. Chinese consumers show rising preference for oak and other textured decors combined with higher-wear layers and denser cores, a trend consistent with the shift to more durable, low-VOC materials. To diversify trade exposure and improve logistics options, several producers operate dual bases in China and Vietnam, which keeps the Asia-Pacific SPC flooring market better positioned against policy shifts and port congestion. These combined advantages reinforce China’s role as a demand and supply hub for the region’s rigid-core segment.

India is projected to be the fastest-growing country through 2031, propelled by urbanization, housing programs, and a consumer pivot away from high-maintenance marble and tile toward waterproof floating floors in apartments and villas. During 2026, supply disruptions and geopolitical tensions elevated PVC raw material costs, which placed added attention on sourcing and price stability in India’s resilient flooring value chain. The Asia-Pacific SPC flooring market is capturing demand from Indian homeowners who favor quick, dust-free retrofits and a warm underfoot feel compared to ceramic in living zones. As apartment renovations accelerate in major metros, specifiers and dealers continue to add SPC ranges that address bathrooms, kitchens, and entries without the complexity of wet trades. These shifts sustain India’s role as a core growth engine for the Asia-Pacific SPC flooring market through the forecast period.

Japan and South Korea demonstrate a premium mix and stricter acoustic compliance, which is lifting the adoption of 6.5–7.0 mm products with pre-attached pads for high-rise condominium retrofits. Building association rules often require LL40 or LL45 performance for replacements, which narrows the field to rigid-core options that can meet impact and airborne sound benchmarks without overbuilding floor height. Southeast Asia continues to gain as a production and export platform, with Vietnam benefiting from investments in advanced click technologies and increased monthly output geared to North American and European orders. In Australia and New Zealand, interest in circularity is supported by the ResiLoop stewardship program authorized by the national competition regulator, which informs commercial specifications that value end-of-life solutions. These geography-specific factors together shape the Asia-Pacific SPC flooring market’s growth profile and product mix choices through 2031.

Competitive Landscape

The Asia-Pacific SPC flooring market remains moderate, with many China and Vietnam-based OEMs supplying private-label and export accounts while regional brands compete on design, wear layers, and acoustic pads rather than on locking patents alone. Scaled producers gain procurement and automation advantages that trim per-unit costs, and recent plant investments in Hebei and Haiphong demonstrate a continued commitment to capacity-led competitiveness. Buyers place a growing premium on predictable delivery schedules, which benefits suppliers with dual-country footprints and stronger logistics networks across ASEAN trade corridors. As these operational capabilities spread, the Asia-Pacific SPC flooring market is seeing tighter service levels and faster product refresh cycles, keeping assortments aligned with end-market preferences.

Technology licensing has broadly democratized click systems, and suppliers now differentiate through surface innovation, scratch resistance, and integrated grout aesthetics in tile-format panels. Product managers are also responding to acoustic and circularity expectations in Japan, South Korea, and Australia by expanding pad-attached lines and by engaging emerging stewardship frameworks where they exist. In parallel, direct-to-consumer e-commerce is a notable commercial strategy that compresses landed costs and supports transparent pricing, especially for homeowners comfortable with DIY installation. These shifts continue to define how companies compete in the Asia-Pacific SPC flooring market, with design breadth, logistics reliability, and compliance readiness emerging as core differentiators.

Recent strategic moves reinforce this trajectory. DECNO expanded a multi-function production base in Hebei to increase output and support higher-end SPC formats. CFL commissioned a new Vietnam facility to diversify sourcing and shorten shipping lines to key overseas markets. i4F licensed CeraGrout surface technology to leading manufacturers, enabling pre-grouted SPC tiles that reduce wet trades and speed installations. StarsPlas continues to provide turnkey extrusion solutions, including financing options that allow regional distributors to localize SPC production. Together, these moves shape a competitive field where the Asia-Pacific SPC flooring market rewards speed, reliability, and differentiated product performance.

Asia-Pacific Stone Plastic Composite (SPC) Flooring Industry Leaders

CFL Flooring (Creative Flooring Solutions)

Power Dekor Group

Novalis Innovative Flooring

DECNO GROUP Ltd.

LX Hausys (HFLOR)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Biancogres, a Brazilian ceramic tile producer, adopted Välinge Innovation's 2G PRO mechanical locking system for its new SPC production line and launched the Clicados collection at Expo Revestir 2026 in São Paulo (March 9-13). While the development occurred outside APAC, Välinge's technology licensing model influences global SPC manufacturing standards, and the 2G PRO system's efficiency and durability features may eventually be adopted by APAC manufacturers seeking to differentiate click-lock performance.

- May 2025: Melbourne-based ResiLoop initiative, supported by 17 leading product suppliers, launched a flooring-waste recycling program targeting approximately 12.5 million square meters of resilient flooring waste generated annually in greater metropolitan Melbourne. The scheme collects unused off-cuts from commercial and residential installations through a registered contractor network, with Victorian manufacturer Think Manufacturing processing waste into durable garden edging products.

Asia-Pacific Stone Plastic Composite (SPC) Flooring Market Report Scope

| SPC Tiles |

| SPC Planks |

| 4.0–5.0 mm |

| 5.1–6.0 mm |

| 6.1–6.5 mm |

| Above 6.5 mm |

| Self-Adhesive |

| Glue-Down |

| Interlocking/Click-lock |

| Others |

| Residential |

| Commercial |

| B2C/Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B/Contractors |

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) |

| Rest of Asia-Pacific |

| By Product Type | SPC Tiles | |

| SPC Planks | ||

| By Product Thickness | 4.0–5.0 mm | |

| 5.1–6.0 mm | ||

| 6.1–6.5 mm | ||

| Above 6.5 mm | ||

| By Installation Method | Self-Adhesive | |

| Glue-Down | ||

| Interlocking/Click-lock | ||

| Others | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B/Contractors | ||

| By Geography | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the growth outlook for the Asia-Pacific SPC flooring market through 2031?

The Asia-Pacific SPC flooring market size is set to increase from USD 3.98 billion in 2025 to USD 6.93 billion by 2031 at a 9.76% CAGR, supported by waterproof performance, faster installs, and broader capacity across China and Vietnam.

Which product type leads and which is growing fastest across APAC?

SPC planks lead with the largest 2025 share, while SPC tiles are growing fastest through 2031 due to pre-grouted, click-in tile systems that simplify wet-area upgrades.

How do acoustic rules in Japan and South Korea influence SPC thickness choices?

Condominium sound requirements, such as LL40 and LL45, push specifiers toward 6.5–7.0 mm products with pre-attached pads, which raises premium adoption in high-rise retrofits.

Where are manufacturers localizing SPC capacity to improve lead times?

Vietnam and northern China are key hubs, with new facilities in Haiphong and Hebei that diversify sourcing, compress shipping times, and support tariff-sensitive routes.

What is driving commercial adoption of rigid-core floors across APAC?

Healthcare, hospitality, and retail upgrades rely on scratch-resistant, grout-free surfaces with predictable cleaning, and many projects value SPC’s faster turnaround for occupied spaces.

How are EPR and stewardship programs shaping resilient flooring procurement?

Policies across ASEAN and Australia require or encourage collection and recycling solutions, which push suppliers to document circularity pathways and adjust product design and labeling.

Page last updated on: