Commercial Stone Plastic Composite (SPC) Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

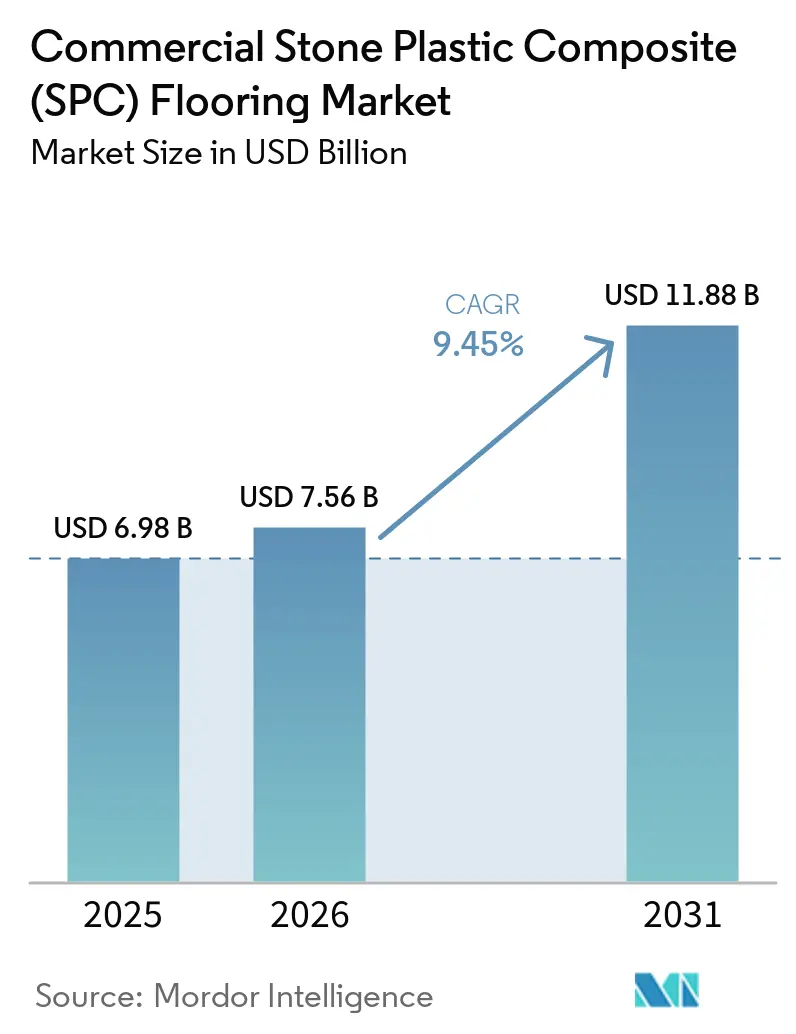

| Market Size (2026) | USD 7.56 Billion |

| Market Size (2031) | USD 11.88 Billion |

| Growth Rate (2026 - 2031) | 9.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Stone Plastic Composite (SPC) Flooring Market Analysis by Mordor Intelligence

The Commercial stone plastic composite flooring Market size was valued at USD 6.98 billion in 2025 and is estimated to grow from USD 7.56 billion in 2026 to reach USD 11.88 billion by 2031, at a CAGR of 9.45% during the forecast period (2026-2031). Demand in 2026 centers on fast installation, waterproof performance, and dimensional stability that support renovation programs across offices, hospitality, healthcare, and education. Buyers in these settings now treat indoor air quality credentials as baseline requirements for tenders, elevating the relevance of FloorScore and comparable certifications that link directly to green building frameworks. Industry associations have also expanded access to environmental disclosures for SPC through standardized Environmental Product Declarations (EPDs), which streamline documentation for rating systems and public procurement. Capacity moves and nearshoring programs continue to reshape supply footprints, supported by new facilities in Vietnam that integrate modern rigid-core designs and advanced acoustic builds into diversified, multi-country networks. Licensing activity around rigid core and locking technologies remains an important competitive lever because it supports legal import, coherent product roadmaps, and credible performance claims in specification-driven bids[1]I4F.COM https://i4f.com/article/lioncore-selects-i4f-as-exclusive-licensor-for-its-new-patented-l-spc-lightweight-rigid-core-product-build-up-and-composition/.

Key Report Takeaways

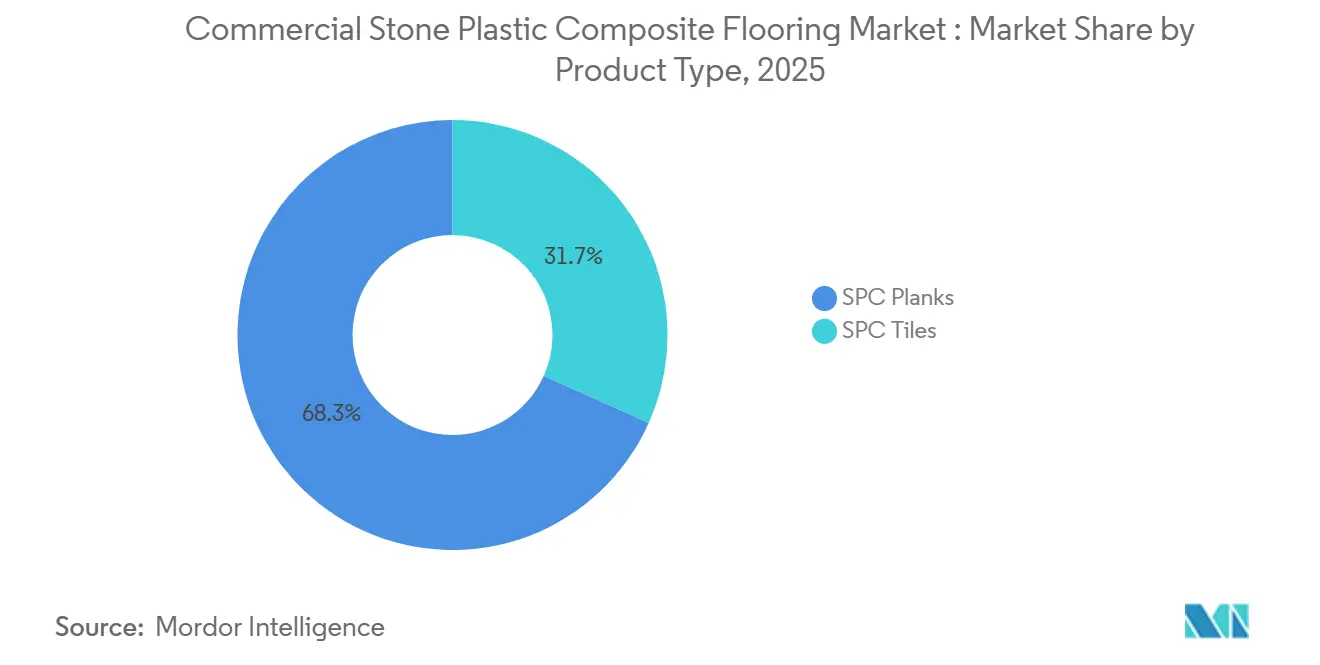

- By product type, planks led with 68.30% of the global commercial stone plastic composite flooring market share in 2025; tiles are forecast to post the fastest growth at an 9.82% CAGR through 2031.

- By product thickness, the 5.1–6.0 mm band accounted for 42.75% of the global commercial stone plastic composite flooring market share in 2025; thicknesses above 6.5 mm are projected to expand at a 9.65% CAGR through 2031.

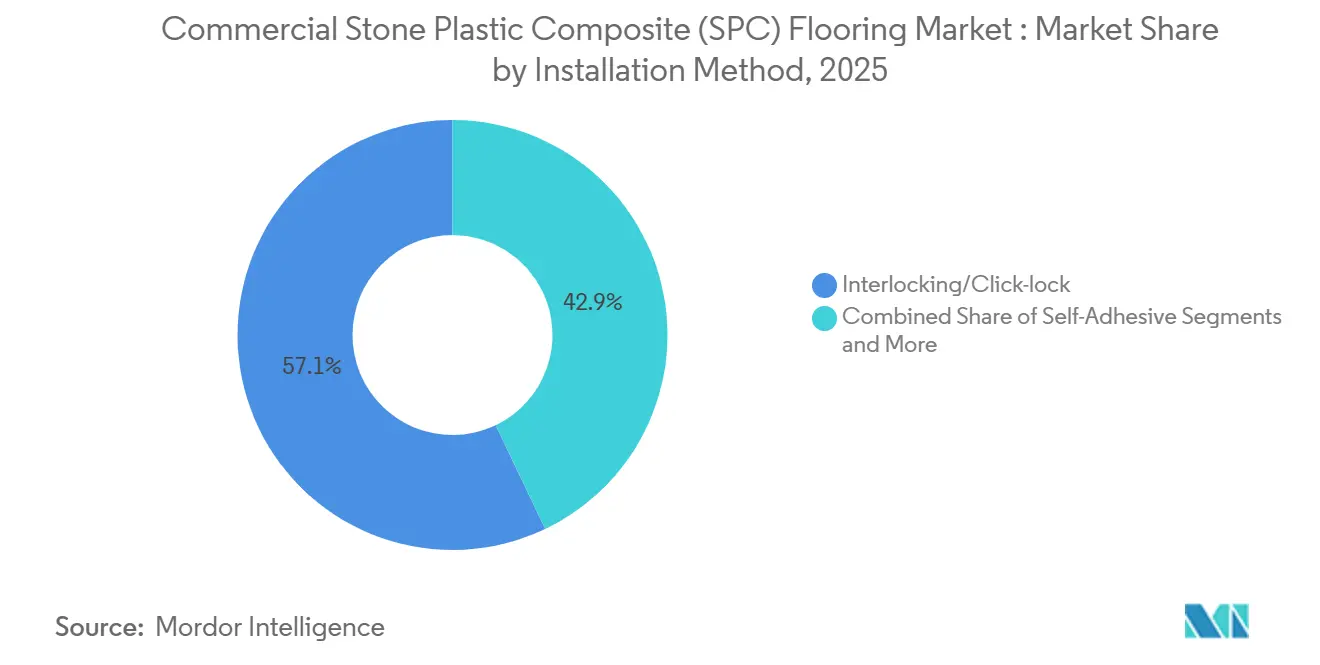

- By installation method, interlocking click lock held 57.10% of the global commercial stone plastic composite flooring market share in 2025; this method is advancing at an 8.54% CAGR through 2031.

- By commercial end user, offices & corporate workspaces held 25.00% of the global commercial stone plastic composite flooring market share in 2025; the retail segment is advancing at an 10.03% CAGR through 2031.

- By distribution channel, indirect/dealers held 61.85% of the global commercial stone plastic composite flooring market share in 2025; this segment is advancing at an 9.78% CAGR through 2031.

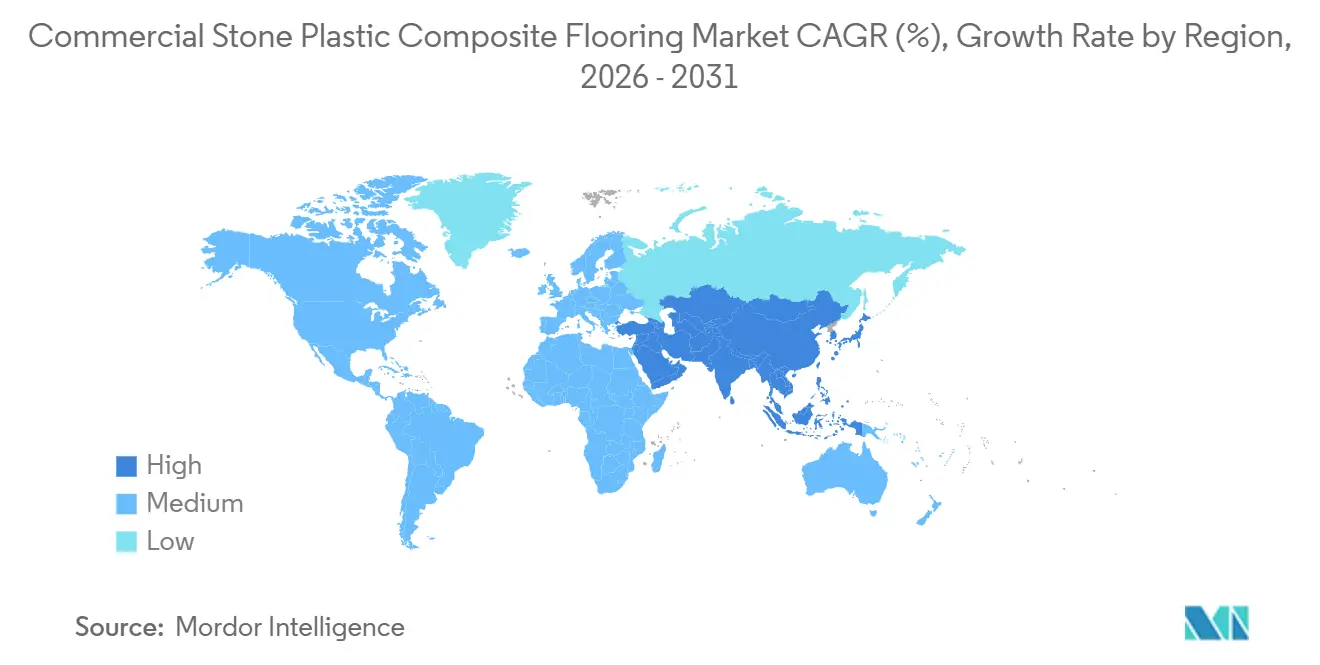

- By geography, North America captured 32.90% of the global commercial stone plastic composite flooring market share in 2025; Asia-Pacific is expected to grow at a 10.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Stone Plastic Composite (SPC) Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation‑driven demand for fast, low‑downtime rigid core in commercial interiors | +1.8% | Global, with acute pressure in North America hospitality, Europe office refits, and Asia‑Pacific mixed‑use | Short term (≤ 2 years) |

| Rigid core (SPC) is gaining share within LVT for durability and waterproofing | +1.5% | Global core, particularly APAC manufacturing hubs and North America end‑markets | Medium term (2-4 years) |

| IAQ‑certified low‑emitting SPC easing specs in healthcare and education | +1.2% | North America and the EU, emerging in the Middle East | Medium term (2-4 years) |

| Expanding commercial adoption across office, hospitality, healthcare, and education | +2.0% | Global, led by APAC urbanization and steady renovations in North America and Europe | Long term (≥ 4 years) |

| Acoustic and lightweight core innovations enabling code compliance and occupant comfort | +0.9% | North America multifamily, EU mixed‑use, APAC dense urban projects | Medium term (2-4 years) |

| Nearshoring and regional SPC plants are reducing tariff and lead‑time risk | +0.6% | USA, Canada, Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renovation Driven Demand for Fast, Low Downtime Rigid Core in Commercial Interiors

Project owners favor SPC rigid core for renovation schedules that keep facilities operational while construction moves zone by zone. According to supplier installation guides, click lock systems enable floating installation that is significantly faster than glue-down alternatives, with immediate walk-on access and no 24-48 hour adhesive curing time, resulting in reduced labor and minimal business downtime in occupied hospitality and office spaces. These floating assemblies bridge minor subfloor irregularities without extensive surface preparation, lowering callbacks compared with glue-down options that require longer adhesive curing and more intensive prep work. Institutional environments prioritize low-emission certifications to speed re-occupancy after renovation, which is why FloorScore, testing to California Section 01350 VOC limits, has become standard for procurement in healthcare and education facilities seeking LEED, WELL, or CHPS compliance. Suppliers’ renovation references highlight cleaner execution, waterproof cores that tolerate daily wet cleaning and spills, and lower risk of moisture-related delays in commercial interiors.

Rigid Core (SPC) Gaining Share Within LVT for Durability and Waterproofing

Rigid core SPC constructions address dimensional stability issues more effectively than traditional flexible LVT. Manufacturer specifications and product comparisons emphasize low expansion rates (typically ≤0.05%, with some reporting shrinkage ≤0.02%) and stable performance in temperature swings, with high-density cores and thicker commercial wear layers (0.5 mm / 20 mil or more) supporting castor chair tests (often passing 25,000 cycles under 90 kg load) for rolling loads and high footfall zones such as corridors and lobbies. SPC’s waterproof core eliminates swelling and surface deformation after daily wet cleaning and spills in healthcare sterile processing, kitchens, and public restrooms, unlike flexible LVT, which can be affected by prolonged moisture exposure around edges. The format is often delivered with click systems under formal license agreements for consistent locking integrity and repeatable quality across large footprints. These product attributes, together, are driving substitution from flexible vinyl toward rigid-core choices within the commercial segment in 2026[2]Adasea Content Team, “How to Hedge Against PVC Price Trends 2026,” Adasea Flooring, adaseaflooring.com .

IAQ Certified Low Emitting SPC Easing Specs in Healthcare and Education

Indoor air quality labels such as FloorScore now function as a de facto entry ticket in healthcare and education tenders because the certifications reference established emissions protocols and link to major building rating systems. According to program documents from SCS Global Services and the Resilient Floor Covering Institute (RFCI), FloorScore evaluates products for compliance with California Section 01350 (CDPH Standard Method v1.2), testing for 35 individual VOCs, including formaldehyde, and modeling emissions for office and classroom scenarios. Certificates and program documents issued by certifying bodies confirm the evaluation of VOC emissions, along with annual product retesting and periodic manufacturing facility surveillance audits that sustain listing status for SPC lines installed in school classrooms, patient rooms, and office settings. Several commercial brands present public documentation of FloorScore achievement to simplify submittals, and some factories post multi-year certification continuity as evidence of quality systems that extend beyond one-time tests. Healthcare-oriented LVT and rigid core product pages also feature multi-standard alignment covering IAQ, slip performance, and infection control parameters, helping specifiers consolidate compliance checks across categories. The net effect is that low-emission credentials lower procurement friction and shorten approval cycles where occupant health and regulatory scrutiny are most pronounced [3]FLOORDI.CA floordi.ca/floordi-achieves-floorscore-certification-laminate-spc-flooring.

Expanding Commercial Adoption Across Office, Hospitality, Healthcare, Education

The use of SPC in commercial interiors spans diverse applications because product engineering can be tuned to specific performance needs such as slip resistance, indentation resistance, and acoustic comfort. In hospitality, pre-attached acoustic underlayment and waterproof cores align with the rapid room turn cycles and moisture conditions that characterize guest floors, corridors, and public spaces. In office and education, chair castor resistance, stain performance, and maintainability stand out in specification guides, with thicker wear layers and dense cores often paired to support longevity. Suppliers publishing technical data also document how acoustic assemblies with integrated foam backings can reduce impact transmission and minimize the need for separate underlayment in many building types. This bundled performance set, delivered with stable locking systems and IAQ documentation, sustains wider SPC adoption across the main institutional segments in 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC resin and additive price volatility are impacting bid competitiveness | -0.5% | Global, acute in regions dependent on naphtha‑based ethylene | Short term (≤ 2 years) |

| End‑of‑life recycling limits and PVC scrutiny in specifications | -0.3% | EU regulatory zone, North America green‑building projects, and emerging in APAC | Long term (≥ 4 years) |

| Floating click joints under heavy rolling loads, prompting more glue‑down specs | -0.2% | Healthcare, hospitality service areas, institutional corridors | Medium term (2-4 years) |

| IP and trade enforcement on click systems, raising compliance and import risks | -0.1% | U.S. and EU import channels for non‑licensed products | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PVC Resin and Additive Price Volatility Impacting Bid Competitiveness

SPC relies on PVC resin alongside calcium carbonate, and several producers flag resin and additive volatility as pricing risks that compress margins on long-lead projects. According to manufacturer formulations and production references, PVC resin typically accounts for 25-30% of the core, while limestone (calcium carbonate) accounts for 60-75%, with prices closely linked to global oil and feedstock fluctuations, such as the documented 3-5¢/lb increases in PVC resin in early 2026. Petrochemical market reports explain how upstream cycles translate into resin price changes that flow through flooring price quotes with timing lags that complicate bidding and procurement. Regional differentials also shape sourcing choices in a given year, prompting buyers to weigh lower-resin-price zones against trade actions and logistics exposures. Many wholesalers and importers have shifted from just-in-time to more buffered inventories to sustain supply continuity during feedstock spikes. The partial mitigation of SPC versus flexible vinyl, due to its higher limestone content, does not eliminate volatility but can moderate exposure relative to fully PVC-dependent constructions.

End of Life Recycling Limits and PVC Scrutiny in Specifications

The multilayer SPC construction complicates mechanical separation and homogeneous reprocessing because diverse films, stabilizers, and core materials reduce the purity of recyclate streams. Company technical blogs acknowledge that SPC can be downcycled into lower-grade vinyl products, while chemical recycling remains capital- and energy-intensive and has limited facility availability. Green procurement frameworks are raising expectations for EPDs, recycled content, and documented end-of-life pathways, introducing non-trivial documentation burdens for smaller plants. Some producers have launched take-back and closed-loop programs to reclaim materials and reduce waste at all stages of production and at the end of life, including dedicated SPC recycling systems integrated into flooring manufacturing lines. Awareness and infrastructure gaps remain, which positions circular design choices and investments in collection networks as key to maintaining long-horizon acceptance in projects that prioritize sustainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Planks Dominate Yet Tiles Accelerate on Modular Design Appeal

SPC planks captured 68.30% share in 2025, as large-format visuals, realistic wood textures, and efficient installation supported scale across corridors, guest rooms, and open offices. Designers often select long boards to reduce seam frequency and to deliver continuous lines of sight across expansive spaces while maintaining commercial durability. SPC tiles are advancing as the fastest-growing format, with a 9.82% CAGR through 2031, driven by increased interest in modular and geometric patterns for lobbies, reception areas, and branded public spaces. Company design guides show herringbone, chevron, and large-format stone looks implemented via licensed locking systems that support reliable alignment across patterned installations. The functional performance of planks and tiles is comparable because both formats share waterproof rigid cores and commercial wear layers, so selection pivots on design language and installation workflows rather than core differences.

In projects with high aesthetic stakes, stone-look SPC tiles in larger dimensions are gaining traction where maintenance, slip performance, and weight reduction are priorities relative to ceramics. Vendors outline how click-lock assemblies reduce job-site complexity for patterned or large-format designs compared with traditional ceramic-setting materials. As procurement teams standardize on IAQ and Environmental Product Declaration (EPD) documentation for the commercial stone plastic composite flooring market, the adoption of tiles in signature zones complements the broad utility of planks in background and circulation spaces. Specifiers who rely on a single family across both tile and plank formats can consolidate colorways, textures, and trim details while preserving consistent maintenance protocols. This mix supports a balanced volume strategy across the commercial stone plastic composite flooring market as 2026 decisions blend design intent with predictable performance.

By Product Thickness: Premium Acoustic Specifications Drive >6.5 mm Surge

The 5.1–6.0 mm band accounted for 42.75% of 2025 demand as buyers balanced unit costs with commercial performance in light-to-mid-duty corridors and multipurpose rooms. Factory-attached acoustic foams in these mid-thickness builds help projects meet baseline impact-isolation targets in many codes, reducing procurement and coordination steps compared with separate underlayment. Above 6.5 mm, products are projected to grow at a 9.65% CAGR through 2031, reflecting tighter acoustic targets and occupant comfort expectations in multifamily and senior living spaces. Supplier documentation points to thicker cores with higher IIC and STC ratings that can avoid the cost and complexity of secondary sound mats in many assemblies, while maintaining waterproof performance and commercial wear layers. These dynamics support a tilt toward premium construction in the commercial stone plastic composite flooring market when long-term lifecycle costs and warranty risk outweigh initial material savings.

Buyers who continue to specify thinner formats usually do so for budget-constrained refreshes or lighter-duty retail and office applications where rolling loads and acoustic transmission are minimal. Where code or brand standards direct higher acoustic values, thicker constructions with integrated foam layers deliver measurable performance benefits without introducing different installation methods across a project. The commercial stone plastic composite flooring industry has also adopted thicker profiles to increase click-joint strength and ease fit-up on large, open floors, thereby shortening installation schedules and reducing rework risk. These advantages now appear in many standard spec templates that institutional procurement teams distribute for fit-outs and renovations. The appeal of thicker profiles, therefore, extends beyond acoustics and reflects a more general desire for stability in heavy wear environments served by the commercial stone plastic composite flooring industry.

By Installation Method: Click Lock Convenience Versus Glue Down Permanence in Heavy Duty Zones

Interlocking click lock accounted for a 57.10% share in 2025 and is projected to grow at an 8.54% CAGR, driven by floating assemblies that tolerate minor substrate variation and reduce labor time. Installers also value the ability to isolate small areas for repair without affecting adjacent zones, which is particularly useful in healthcare and hospitality operations that prioritize service continuity. Vendors and installation resources emphasize that licensed locking geometries improve joint integrity and reduce the risk of failure under dynamic loads compared with generic systems. The glue-down method, however, continues to anchor heavy-duty corridors and service areas because the permanent bond and strict indentation controls reduce seam movement under wheel traffic. The selection framework in 2026 is therefore straightforward: click lock is used to accelerate most commercial make-readies, and glue-down is reserved for service corridors and other locations with constant rolling loads.

Procurement teams often adopt a mixed approach within a single building, using floating SPC in guest rooms and offices while specifying glue-down for back-of-house or clinical corridors. Published B2B guides from flooring suppliers support this design logic, showing side-by-side assemblies that document sound performance, subfloor preparation, and warranty parameters. As e-procurement portals standardize data fields for emissions certificates and test reports, submittals for both methods have become more predictable in 2026. License compliance for click systems remains important because it simplifies customs clearance and lowers litigation risk for importers and brand owners. These operational considerations are well understood by installers and distributors serving the commercial stone plastic composite flooring market.

By Commercial End User: Offices Lead Share Yet Retail Surges on Experiential Build-Outs

Offices and corporate workspaces accounted for 25.00% of commercial SPC flooring demand in 2025, driven by post-pandemic workplace redesigns prioritizing hybrid-ready layouts, biophilic materials, and acoustic zoning, which SPC's click-lock speed and sound-dampening cores uniquely enable. Open-plan configurations mandate products meeting ISO 4918 castor-chair cycle thresholds (25,000+ rotations) and residual indentation limits ≤0.05 mm to eliminate chair mats while preserving aesthetic cohesion, specifications that SPC's high-density limestone core (1,950–2,050 kg/m³) satisfies without the maintenance burden of hardwood or the moisture vulnerability of carpet. Hospitality projects, hotels, resorts, restaurants, specify SPC for guest rooms and public areas requiring waterproof performance against spills, wheeled-luggage traffic, and daily wet-cleaning protocols, with a Southeast Asia boutique hotel deploying 8,200 sq m across renovations that maintained operations during phased installation.

Educational institutes demand lifecycle cost-efficiency and IAQ compliance (formaldehyde-free, heavy-metals-free per ASTM F 963-11) for Utilization Class 31/33 spaces subjected to unpredictable spills, abrasive dirt from playgrounds, and high-density foot traffic during class transitions. A California commercial retrofit achieved a 30% reduction in embodied carbon by specifying recycled-content SPC planks in place of traditional vinyl, illustrating how sustainability-focused institutional buyers align flooring procurement with green-building mandates. Healthcare facilities prioritize infection control through non-porous SPC surfaces that resist bacterial growth, chemical resistance per ISO 26987 for disinfectant compatibility, and acoustic performance (△IIC 21 with 1 mm IXPE underlay) that reduces noise transmission in patient-recovery zones.

By Distribution Channel: Indirect Dealers Consolidate Reach as Digital Platforms Accelerate Faster

Indirect dealer networks, comprising distributors, wholesalers, specialty retail, home improvement chains, and e-commerce/B2B marketplaces, commanded 61.85% market share in 2025 and are expanding at 9.78% CAGR through 2031, the fastest channel growth trajectory, reflecting a structural shift as manufacturers leverage third-party infrastructure to scale geographically without capital-intensive branch expansions. Distributors and wholesalers provide inventory buffers, credit terms, and regional logistics that independent flooring retailers and small contractors cannot access directly from manufacturers, while specialty retail chains (home improvement centers, flooring showrooms) offer display vignettes, sales-associate training, and consumer financing that bridge the specification gap for light-commercial buyers upgrading boutique retail spaces or small-office interiors. E-commerce and B2B marketplaces within the indirect segment are the primary drivers of CAGR, capitalizing on digital procurement trends that compress decision cycles through augmented-reality preview tools, algorithmic product matching, and real-time inventory visibility across distributed warehouse networks.

Direct sales channels, including offline direct-to-projects/contractors and online D2C, held 38.15% share in 2025, serving large-scale institutional buyers (universities, hospital systems, government agencies) that require specification-writing support, job-site delivery coordination, and post-installation training unavailable through retail intermediaries. Offline direct channels excel in projects exceeding 50,000 sq ft where manufacturers deploy dedicated account managers to navigate multi-stakeholder procurement (facilities directors, architects, general contractors, end-user representatives) and customize product mixes, blending click-lock for common areas with glue-down for heavy-traffic corridors, to optimize lifecycle value.

Geography Analysis

North America accounted for 32.90% of the global market share for commercial stone plastic composite flooring in 2025, driven by institutional renovations in hospitality, healthcare, and education. U.S. and Canadian buyers give weight to IAQ credentials and public documentation of environmental performance, which has reinforced the importance of formal certifications linked to LEED, WELL, and related frameworks. Manufacturers and certification bodies publicly list SPC products that meet emissions standards and maintain active certificates, providing procurement teams and designers with a common language for compliance. This region also benefits from diversified sourcing strategies that combine regional and overseas supply to address project schedules and inventory planning. As a result, specification flow in 2026 favors SPC lines with clear documentation, strong locking systems, and acoustic packages that meet or exceed baseline isolation targets.

Europe combines mature renovation activity with a high bar for environmental and health documentation, which shapes brand assortments and compliance investments. Industry associations have responded by producing verified EPDs that cover vinyl SPC floor coverings to simplify documentation for architects and general contractors. European portfolios also emphasize phthalate-free stabilizers and emission classifications validated under regional schemes, supported by corporate sustainability content that is readily auditable. Localized warehousing and faster service responses support tight construction timelines, and firms maintain European support teams to align with procurement norms and language expectations. These moves help commercial buyers in 2026 align design, performance, and compliance against the broader decarbonization and health priorities that drive large renovation budgets.

Asia-Pacific is the fastest-growing region, with a 10.47% CAGR through 2031, driven by urbanization dynamics and the continued buildout of diversified rigid-core capacity. Vietnam has become a pivotal node in global SPC supply with large factory investments near deepwater ports to serve both exports and domestic demand. Company disclosures indicate that these factories produce advanced acoustic SPC and scratch-resistant variants that complement capacity in the U.S. and China, forming resilient multi-site networks. Comparative guidance from regional suppliers outlines the practical considerations of sourcing SPC from China versus Vietnam, including trade agreements and shipping profiles into North America and Europe. These factors position Asia-Pacific as both a manufacturing anchor and an expanding demand center for the commercial stone plastic composite flooring market.

Competitive Landscape

The commercial stone plastic composite flooring market shows moderate concentration. Market leaders continue to emphasize certification velocity and complete documentation sets that meet institutional RFQs and public procurement requirements. IP licensing and technology partnerships remain a key instrument because they support robust click joint performance and protect global importability, which is central to distributors and brands working across regions. In 2026, licensing platforms have added lightweight rigid core formulations that reduce unit weight while maintaining durability, expanding design options for projects sensitive to freight profiles or installation ergonomics. This strategic focus supports higher-specification hit rates in design-forward commercial segments where acoustic, IAQ, and lifecycle requirements must be demonstrated with third-party materials.

Supply-side strategies are also visible in manufacturing footprint decisions and in partnership structures that extend commercial reach. Factory investments in Vietnam shorten lead times to U.S. and EU ports and hedge against tariff-related volatility, with features such as acoustic SPC and reinforced scratch resistance that strengthen the category. Distributors and contract sales alliances expand brand presence in healthcare, education, and institutional projects where national coverage and consistent service are decisive. These moves, taken together, improve load balancing across plants and create redundancy to sustain deliveries during seasonal demand spikes and transport disruptions. Leading brands use this resilience as a proof point in enterprise bids that prioritize execution certainty in the commercial stone plastic composite flooring market.

Product portfolios in 2026 reflect a steady cadence of enhancements across textures, acoustic builds, and low-emission materials, with supporting procurement documentation. Several firms publish or link to their certifications and EPDs directly on product pages or technical hubs, giving specifiers immediate access to compliance artifacts. IAQ certificates, healthcare-ready LVT and rigid core lines, and factory-level quality system attestations are integral to qualifying for sensitive spaces. Industry association EPDs further lower the barrier to evaluation because they are third-party reviewed and valid for multiple years, thereby reducing mid-project renewal burdens. This combination of credible disclosure and steady product innovation underwrites credible claims across a competitive field that remains fragmented below the top tier of brands in the commercial stone plastic composite flooring market.

Commercial Stone Plastic Composite (SPC) Flooring Industry Leaders

CFL Flooring

Huali Group

Shaw Industries

Tarkett

Mohawk Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lioncore Industries Vietnam granted i4F exclusive licensing rights for its new patented Lightweight Stone Polymer Composite (LSPC) technology, which reduces weight by 25% versus traditional SPC while maintaining superior dimensional stability, durability, and waterproof performance through a four-layer construction (wear, décor, light foamed SPC core, LVT bottom). The innovation immediately became available to manufacturers globally via i4F’s licensing platform.

- May 2025: HMTX Industries announced an expanded national partnership with Spartan Surfaces, granting Spartan national rights for Teknoflor and Aspecta-branded products throughout the United States. The collaboration aims to enhance service, expand HMTX’s reach, and provide customers with greater access to high-performance design flooring solutions. Nicolette Grieco and Kendra Mahen continue to lead Teknoflor-branded sales as Vice Presidents for the Midwest/Eastern U.S. and Southwest/Western states, respectively.

Global Commercial Stone Plastic Composite (SPC) Flooring Market Report Scope

| SPC Tiles |

| SPC Planks |

| 4.0–5.0 mm |

| 5.1–6.0 mm |

| 6.1–6.5 mm |

| Above 6.5 mm |

| Self-Adhesive |

| Glue-Down |

| Interlocking/Click-lock |

| Others |

| Hospitality |

| Healthcare Facilities |

| Educational Institutes |

| Retail (malls, showrooms, stores) |

| Offices & Corporate Workspaces |

| Other Commercial End Users |

| Direct Sales | Offline Direct to Projects/Contractors |

| Online D2C | |

| Indirect/Dealers | Distributors/Wholesalers |

| Specialty Retail & Home Improvement | |

| E-commerce/B2B Marketplaces |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | SPC Tiles | |

| SPC Planks | ||

| By Product Thickness | 4.0–5.0 mm | |

| 5.1–6.0 mm | ||

| 6.1–6.5 mm | ||

| Above 6.5 mm | ||

| By Installation Method | Self-Adhesive | |

| Glue-Down | ||

| Interlocking/Click-lock | ||

| Others | ||

| By Commercial End Users | Hospitality | |

| Healthcare Facilities | ||

| Educational Institutes | ||

| Retail (malls, showrooms, stores) | ||

| Offices & Corporate Workspaces | ||

| Other Commercial End Users | ||

| By Distribution Channel | Direct Sales | Offline Direct to Projects/Contractors |

| Online D2C | ||

| Indirect/Dealers | Distributors/Wholesalers | |

| Specialty Retail & Home Improvement | ||

| E-commerce/B2B Marketplaces | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the commercial stone plastic composite flooring market’s headline outlook to 2031?

The commercial stone plasticro composite flooring market size was USD 6.98 billion in 2025 and is pjected to reach USD 11.87 billion by 2031 at an 9.45% CAGR over 2026‑2031.

Which installation method will be most used in commercial settings through 2031?

Interlocking click‑lock leads with a 57.10% share in 2025 and is projected to grow at 8.54% as buyers prioritize speed, modular repairs, and fewer disruption risks during renovations.

Which formats and thicknesses gain the most traction in high‑traffic spaces?

Planks hold a 68.30% share for continuous visuals, while tiles post the fastest growth at 9.82%, and thickness above 6.5 mm is projected at 9.15% as acoustic and stability needs increase.

Which regions drive the fastest growth for commercial SPC?

Asia‑Pacific is expected to be the fastest with a 10.47% CAGR through 2031, supported by diversified supply footprints in Vietnam and rising regional demand.

What standards and certifications matter most in 2026 commercial specifications?

FloorScore IAQ credentials and industry EPDs are central in tenders, with public certificates and association‑verified reports enabling faster qualification and selection.

How do brands reduce supply risk for large projects?

Leading suppliers combine multi‑site manufacturing, licensing for click systems, and standardized EPD and IAQ documentation to de‑risk imports, shorten lead times, and ease submittals.

Page last updated on: