Drug Device Combination Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

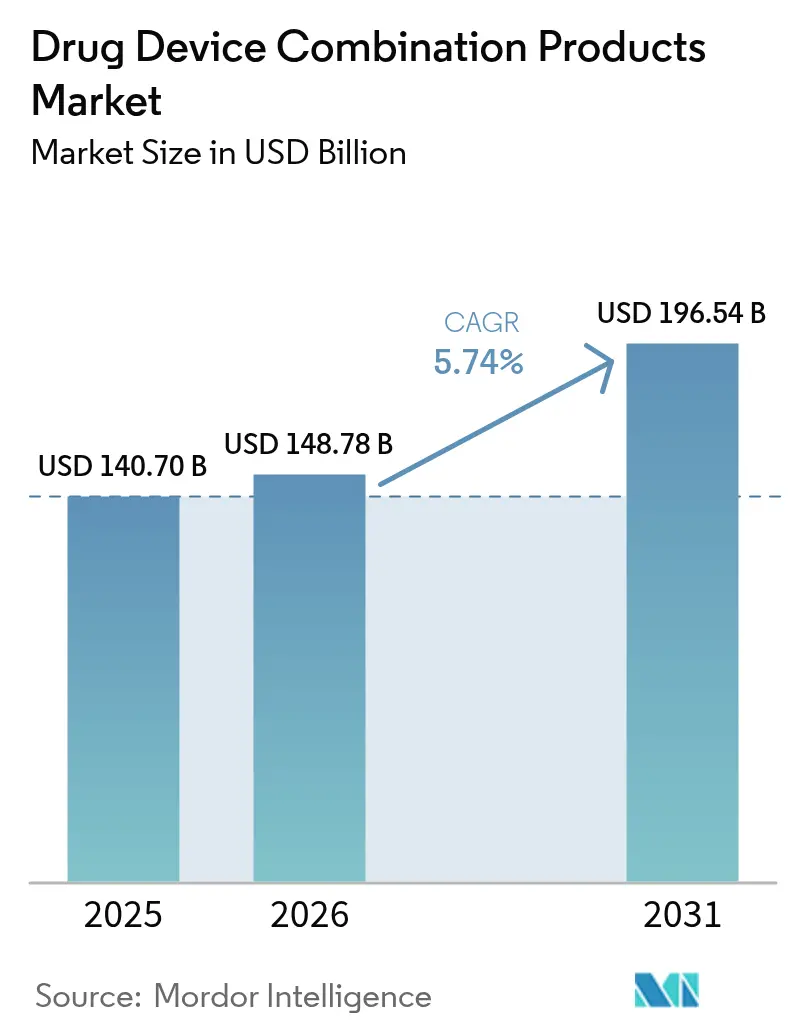

| Market Size (2026) | USD 148.78 Billion |

| Market Size (2031) | USD 196.54 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Drug Device Combination Products Market Analysis by Mordor Intelligence

The drug device combination products market size was valued at USD 140.7 billion in 2025 and estimated to grow from USD 148.78 billion in 2026 to reach USD 196.54 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031). Growth stems from rising chronic-disease prevalence, faster U.S. regulatory pathways that trim approval timelines [1]U.S. Food and Drug Administration, “Combination Products: Fast Facts,” fda.gov , and patient demand for integrated therapies that improve adherence while lowering overall care costs. Convergence of real-time monitoring with targeted drug delivery is turning once-passive devices into active disease-management platforms, creating fresh value propositions for payers and providers. North America keeps its lead through robust innovation funding, whereas Asia-Pacific gains momentum on cost-competitive sterile manufacturing and supportive policy harmonization. Competitive activity intensifies as incumbents buy niche innovators to secure drug-device know-how and digital capabilities.

Key Report Takeaways

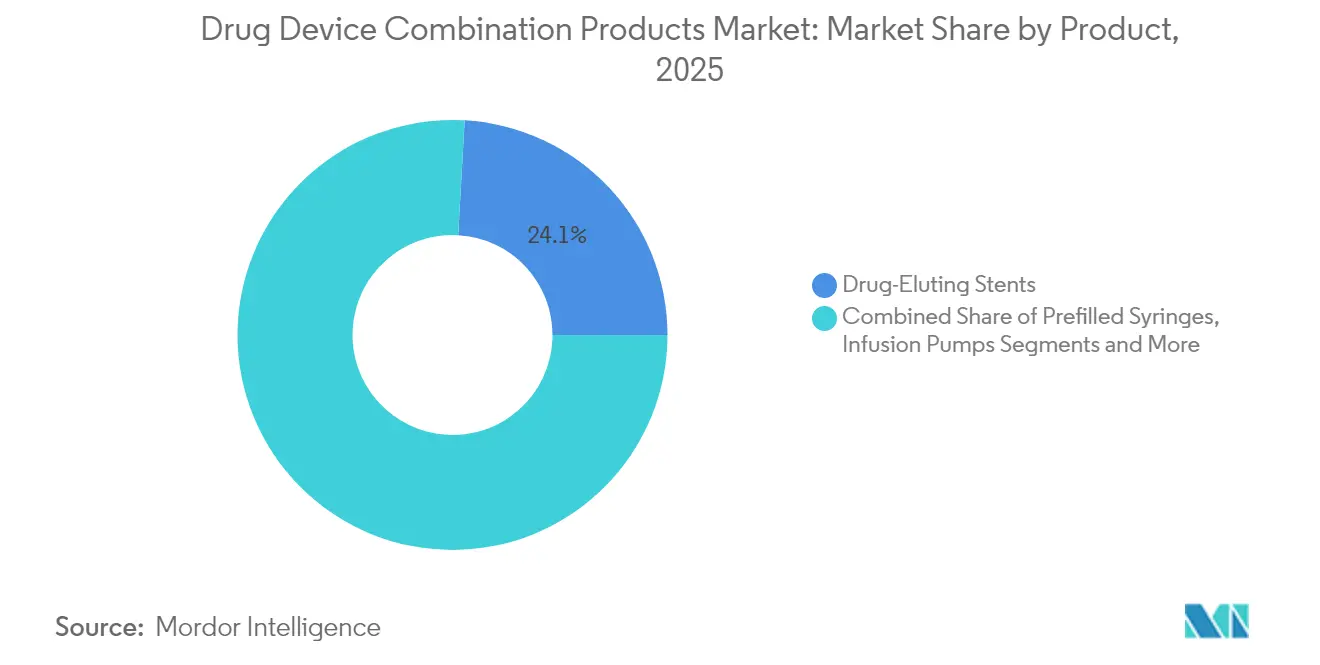

- By product category, drug-eluting stents held 24.10% of drug device combination products market share in 2025; prefilled syringes are projected to expand at a 6.21% CAGR through 2031.

- By application, cardiovascular diseases commanded 35.02% share of the drug device combination products market size in 2025, while pain management is advancing at a 6.31% CAGR to 2031.

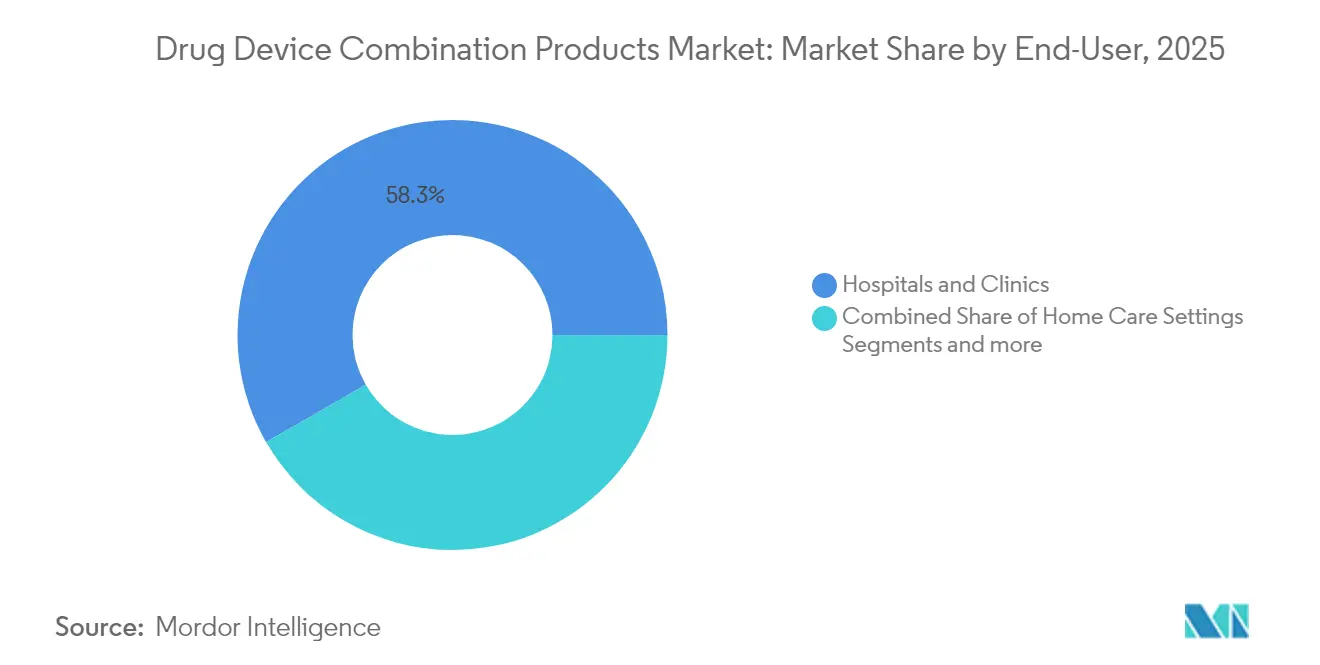

- By end-user, hospitals and clinics accounted for 58.30% share of the drug device combination products market size in 2025; home-care settings record the highest projected CAGR at 6.41% over 2026-2031.

- By route of administration, parenteral delivery led with 31.05% of drug device combination products market share in 2025; implantable delivery routes are growing fastest at 6.60% CAGR.

- By geography, North America contributed 40.12% revenue in 2025; Asia-Pacific is set to post the strongest regional CAGR at 6.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Drug Device Combination Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Chronic Illnesses Driving Demand for Targeted Combination Therapies | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Rapidly Ageing Population Boosting Uptake of Self-Administered Delivery Formats | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Breakthroughs In Minimally-Invasive & Smart Delivery Platforms | +0.8% | North America & EU leading, APAC adoption accelerating | Short term (≤ 2 years) |

| US FDA's Expedited Combo-Product Pathways Shortening Time-To-Market | +0.6% | North America primary, spillover to global markets | Medium term (2-4 years) |

| Connected Inhalers & Patches Enabling Payer-Mandated Adherence Analytics | +0.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Low-Cost Sterile Assembly Capacity Scaling Up Across Asia Lowers ASPs | +0.4% | APAC core, global cost benefits | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Illnesses Driving Demand for Targeted Combination Therapies

Cardiovascular disease affects 655 million people worldwide, sustaining demand for drug-eluting stents and drug-coated balloons that unite mechanical support with localized pharmacotherapy. The FDA-cleared AGENT paclitaxel-coated balloon cut major adverse cardiac events by 11.1% versus uncoated devices, reinforcing the clinical edge of integrated platforms [2]U.S. Food and Drug Administration, “AGENT Paclitaxel,” fda.gov . Diabetes solutions that couple continuous glucose monitoring with automated insulin dosing now achieve 70% glycemic-control rates, far higher than traditional regimens. Oncology is moving toward intra-operative imaging-drug hybrids such as Lumisight, which delivers 84% diagnostic accuracy and limits repeat surgeries. These examples show how drug device combination products market innovators lower long-term costs by pairing precision diagnostics with therapy [3]Anton Camaj, "Drug-Coated Balloons for the Treatment of Coronary Artery Disease," JAMA Cardiology, jamanetwork.com.

Rapidly Ageing Population Boosting Uptake of Self-Administered Delivery Formats

The global population aged 65+ will reach 771 million by 2030, amplifying need for easy-to-use devices that offset declining dexterity. Autoinjectors like Ypsomed’s YpsoDose use audio-visual cues to aid seniors. Home care settings—already the fastest-growing end-user at a 6.56% CAGR—benefit from patch pumps such as Embecta’s smartphone-enabled insulin system that lets patients treat themselves safely. Real-time adherence data address non-compliance, which affects half of chronic-disease patients. The FDA’s human-factors guidance steers manufacturers toward designs that older adults can use correctly on first attempt.

Breakthroughs in Minimally-Invasive & Smart Delivery Platforms

Pulsed-field ablation systems from Boston Scientific and Medtronic recently secured FDA approval for atrial fibrillation, offering lower collateral damage than thermal methods. Smartphone-controlled microneedle patches enable on-demand therapy for neurodegenerative disorders. Long-acting GLP-1 implants deliver weight-loss therapy up to 12 months, tackling obesity adherence challenges. Medtronic’s closed-loop spinal cord stimulator cut overstimulation incidents by 93% through real-time feedback. Such breakthroughs highlight why the drug device combination products market continues to expand into precision medicine.

US FDA’s Expedited Combo-Product Pathways Shortening Time-to-Market

The agency’s Essential Drug Delivery Outputs guidance released in 2024 clarified performance metrics and removed ambiguity that once delayed launches. Abbott’s AVEIR leadless pacemaker gained Breakthrough Device status, trimming review time by a year. The Platform Technology Designation now allows reuse of core data across indications, slashing duplicative trials. As a result, pipeline developers report 40% faster development when standardized imaging endpoints are adopted. The broadened Total Product Life-Cycle Advisory Program offers early dialogue that boosts predictability, a critical plus for this tightly regulated space.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multicentre Regulatory Compliance Adds Cost & Delays | -0.8% | Global, particularly complex in EU post-MDR | Medium term (2-4 years) |

| High Recall Rates Linked to Sterility / Dose Accuracy | -0.6% | Global, with highest impact in North America | Short term (≤ 2 years) |

| Tight Supply of Specialty Polymers Compatible with APIs | -0.4% | Global supply chain, concentrated manufacturing in Asia | Long term (≥ 4 years) |

| Absence Of Unified Reimbursement Codes for Digital Combo Devices | -0.3% | North America & EU primary impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multicentre Regulatory Compliance Adds Cost & Delays

Europe’s MDR and IVDR expansions raise documentation burdens, adding 8-12 months to approvals versus earlier rules. Notified-body reviews elevate compliance costs 25-40% for combination developers. Divergent FDA-EMA classifications force duplicate studies, while Asia-Pacific remains fragmented despite ASEAN harmonization efforts. Without mutual recognition, firms must maintain separate quality systems, inflating overhead and slowing global roll-out of novel therapies within the drug device combination products market.

High Recall Rates Linked to Sterility / Dose Accuracy

Combination products exhibit 2.3-times more sterility-related recalls than standalone drugs or devices because dual manufacturing lines introduce contamination risks. Mechanical variance in prefilled syringes triggers FDA warning letters when dose deviation tops 5%. Genentech’s 2022 recall of the Susvimo ocular implant after septum failures illustrated USD 200 million in replacement and monitoring costs. Software flaws add cyber vulnerabilities to digital devices, emphasizing the need for tighter cross-disciplinary quality protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Technologies Drive Prefilled Syringe Innovation

Drug-eluting stents retained leadership with a 24.10% share in 2025, reflecting decades of evidence for reduced restenosis. Continued polymer advances extend drug elution beyond 180 days, preserving the segment’s dominance in the drug device combination products market. Prefilled syringes, however, are charting a 6.21% CAGR through 2031 as biologics volumes climb and smart sensors log injection events for payers. The drug device combination products market size for prefilled systems is projected to climb markedly as connectivity standards mature and value-based care rewards adherence tracking.

Transdermal patches now use microneedles for macromolecules, expanding into weight-loss therapies. Autoinjectors grow on ergonomic refinements, while wearable injectors turn basal-insulin delivery into a discreet patch experience. Connected inhalers that pair with mobile apps improved asthma-control scores 43% versus conventional devices. Infusion pumps miniaturize for hepatic-artery cancer infusions following Boston Scientific’s Intera Oncology buy, strengthening its presence inside the drug device combination products market.

By Application: Pain Management Emerges as High-Growth Therapeutic Area

Cardiovascular therapies claimed 35.02% of 2025 revenue, anchored by drug-eluting stents, coated balloons, and rhythm-management implants. Pulsed-field ablation represents the next cardiac frontier and keeps the segment a mainstay in the drug device combination products market. Pain management, however, is on a 6.31% CAGR path as implantable neuromodulation offers a non-opioid alternative and garners insurance coverage. The drug device combination products market size for neuromodulation systems is projected to rise quickly as chronic-pain prevalence climbs.

Diabetes maintains robust momentum through sensor-pump ecosystems. Respiratory disorders benefit from digital inhalers and novel formulations for pulmonary hypertension. Oncology is shifting toward imaging-guided drug delivery that provides immediate feedback on therapeutic placement. Obesity implants and mental-health patches represent emerging categories that could further diversify the drug device combination products industry.

By End-User: Home Care Settings Drive Market Expansion

Hospitals and clinics delivered 58.30% of 2025 revenue, leveraging trained staff and advanced imaging to deploy complex implants. Yet home-care settings post the highest 6.41% CAGR as payers push therapy decentralization. Connected patch pumps and autoinjectors send dosing logs to clinicians, allowing tele-supervision that supports reimbursement. The drug device combination products market size dedicated to home use is expected to rise as digital therapeutics integrate seamlessly with consumer electronics.

Ambulatory surgical centers show steady adoption of minimally invasive procedures that rely on fast-acting combination devices for day-case turnover. Integrated care models now span hospital initiation, clinic follow-up, and home maintenance, relying on cloud data continuity.

By Route of Administration: Implantable Delivery Shows Highest Growth Potential

Parenteral delivery remained dominant at 31.05% share in 2025 on the strength of biologic injections. The drug device combination products market share for parenteral routes stays high because injectable GLP-1 drugs and mRNA therapies use advanced syringes. Implantable systems, though, are gaining fastest at 6.60% CAGR thanks to once-yearly GLP-1 rods and long-acting hormonal implants. These low-maintenance options address adherence and reshape chronic-care economics.

Transdermal pathways leverage iontophoresis for larger molecules, widening therapeutic scope. Oral capsules with micro-needles target GI walls to deliver insulin, led by Rani Therapeutics’ platform. Route selection now factors patient lifestyle alongside pharmacokinetics, making implantables central to future drug device combination products market innovation.

Geography Analysis

North America contributed 40.12% of global revenue in 2025, supported by the FDA’s clear regulatory architecture and high healthcare spending. Large acquisitions, such as Johnson & Johnson’s USD 12.5 billion Shockwave Medical buy, augment cardiac-intervention portfolios and reinforce regional dominance. Digital-health partnerships flourish, enabling connected glucose-monitoring ecosystems that further entrench the drug device combination products market.

Asia-Pacific delivers the fastest 6.66% CAGR through 2031. Manufacturing clusters in China, India, and Vietnam slash sterile-assembly costs, while initiatives like the ASEAN Medical Device Directive streamline cross-border registration. Governments fund R&D tax incentives, and regional CDMOs win global outsourcing contracts, broadening market reach. Singapore and South Korea attract clinical-trial activity through efficient ethics-approval cycles.

Europe continues moderate progress despite MDR-related paperwork. Innovation hubs in Germany, Switzerland, and Ireland lead in connected inhalers and digital neuromodulation. Public-private alliances support pilot programs that integrate reimbursement for data-enabled devices, keeping the region integral to the drug device combination products industry.

Competitive Landscape

The marketplace shows moderate fragmentation as diversified conglomerates integrate upstream drug know-how with downstream device expertise. The Kindeva-Meridian merger established a CDMO powerhouse spanning inhalation, injectable, and transdermal platforms. Vertical integration lets majors bundle drug, device, and digital services, raising switching costs for hospital groups inside the drug device combination products market.

Emerging disruptors pursue white-space niches. Vivani Medical’s ultra-long-acting implants aim at weight management, while smartphone-controlled microneedle patches target neurodegeneration. Artificial-intelligence dosing algorithms evolve into key differentiators as payers link reimbursement to outcome metrics. Patent estates around autoinjector mechanics and battery-free sensors remain vital barriers; Meridian alone holds over 300 such patents.

Strategic partnerships bridge pharma molecules with device shells. Sanofi’s EUR 300 million radioligand investment with Orano Med underscores cross-sector synergy. Regulatory mastery also sets leaders apart; companies that navigate FDA, EMA, and NMPA classifications efficiently enjoy first-mover pricing power in the drug device combination products market.

Drug Device Combination Products Industry Leaders

-

Abbott Laboratories

-

Medtronic Plc

-

Boston Scientific Corp

-

Becton, Dickinson and Company

-

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Medtronic received CE-mark expansion for Prevail paclitaxel drug-coated balloon indications.

- May 2025: iVascular and Medico’s Hirata won Japanese approval for the rapid-exchange Luminor 18 RX DCB.

- April 2025: Luye Pharma launched Rotigotine Luye transdermal patch in the UK for Parkinson’s disease and restless-legs syndrome.

- March 2025: Corsair Pharma announced plans for a Phase 1 trial of a treprostinil skin patch targeting pulmonary arterial hypertension.

Global Drug Device Combination Products Market Report Scope

As per the scope of this report, drug-device combination products comprise at least two products, one of the medical devices and the other of drugs that work in coordination with treatment. The Drug-Device Combination Products Market is segmented by Products (Drug-Eluting Stents, Transdermal Patches, Drug-Eluting Balloons, Infusion Pumps, Inhalers, Others), Applications (Cardiovascular, Diabetes, Cancer Treatment, Respiratory Diseases, Others), End-User (Hospitals, Ambulatory Surgical Centers, Others) and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Drug-Eluting Stents |

| Transdermal Patches |

| Infusion Pumps |

| Drug-Coated Balloons |

| Inhalers |

| Prefilled Syringes |

| Wearable Injectors |

| Autoinjectors |

| Others |

| Cardiovascular Diseases |

| Diabetes |

| Cancer Therapy |

| Respiratory Disorders |

| Pain Management |

| Others |

| Hospitals and Clinics |

| Ambulatory Surgical Centers |

| Home Care Settings |

| Others |

| Oral |

| Parenteral |

| Transdermal |

| Implantable |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Drug-Eluting Stents | |

| Transdermal Patches | ||

| Infusion Pumps | ||

| Drug-Coated Balloons | ||

| Inhalers | ||

| Prefilled Syringes | ||

| Wearable Injectors | ||

| Autoinjectors | ||

| Others | ||

| By Application | Cardiovascular Diseases | |

| Diabetes | ||

| Cancer Therapy | ||

| Respiratory Disorders | ||

| Pain Management | ||

| Others | ||

| By End-User | Hospitals and Clinics | |

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| Others | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Transdermal | ||

| Implantable | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the drug device combination products market?

The market reached USD 148.78 billion in 2026 and is projected to hit USD 196.54 billion by 2031 at a 5.74% CAGR.

Which product segment leads the market today?

Drug-eluting stents held the largest 24.10% share in 2025 thanks to proven efficacy in reducing restenosis.

Why is Asia-Pacific experiencing the fastest growth?

Low-cost sterile manufacturing, harmonized regulations, and rising healthcare investment drive a regional CAGR of 6.66% through 2031.

How are regulatory pathways affecting market timelines?

FDA expedited programs shorten U.S. approval cycles by roughly 18 months, speeding global roll-out for qualifying innovations.

Which application area is growing quickest?

Pain management is advancing at 6.31% CAGR due to adoption of implantable neuromodulation devices that offer non-opioid relief.

What factor most influences home-care adoption?

Connected patch pumps and autoinjectors with real-time adherence monitoring underpin the 6.41% CAGR posted by home-care settings.

Page last updated on: