Implantable Drug Delivery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

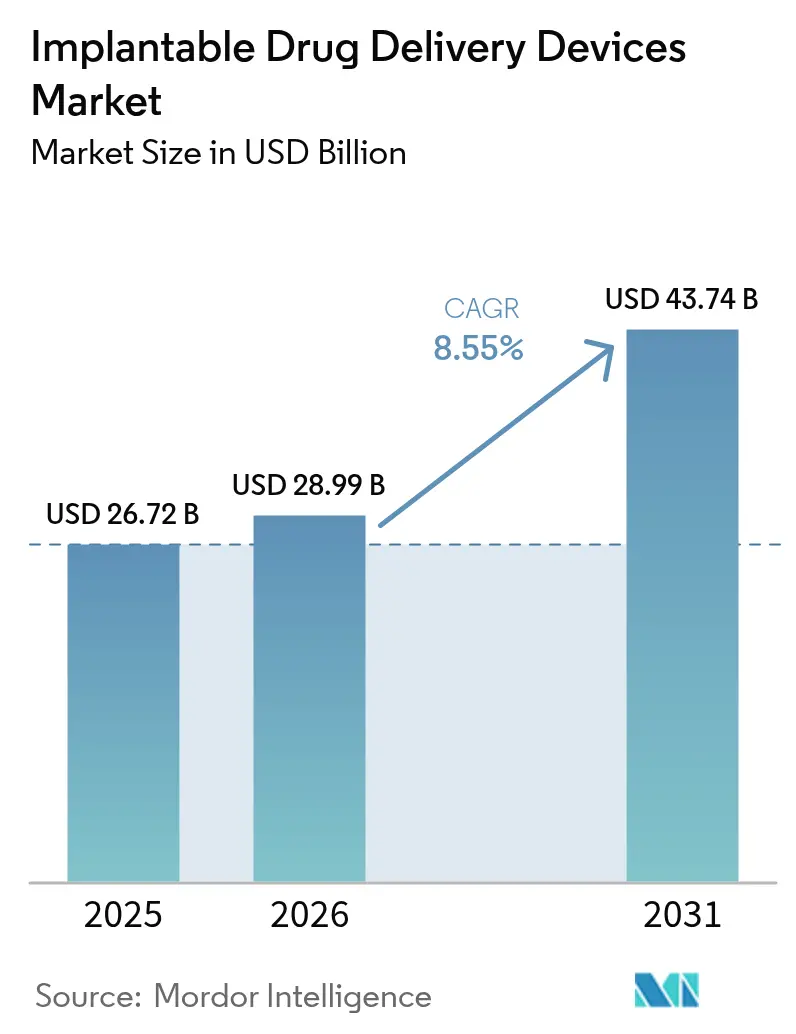

| Market Size (2026) | USD 28.99 Billion |

| Market Size (2031) | USD 43.74 Billion |

| Growth Rate (2026 - 2031) | 8.55% CAGR |

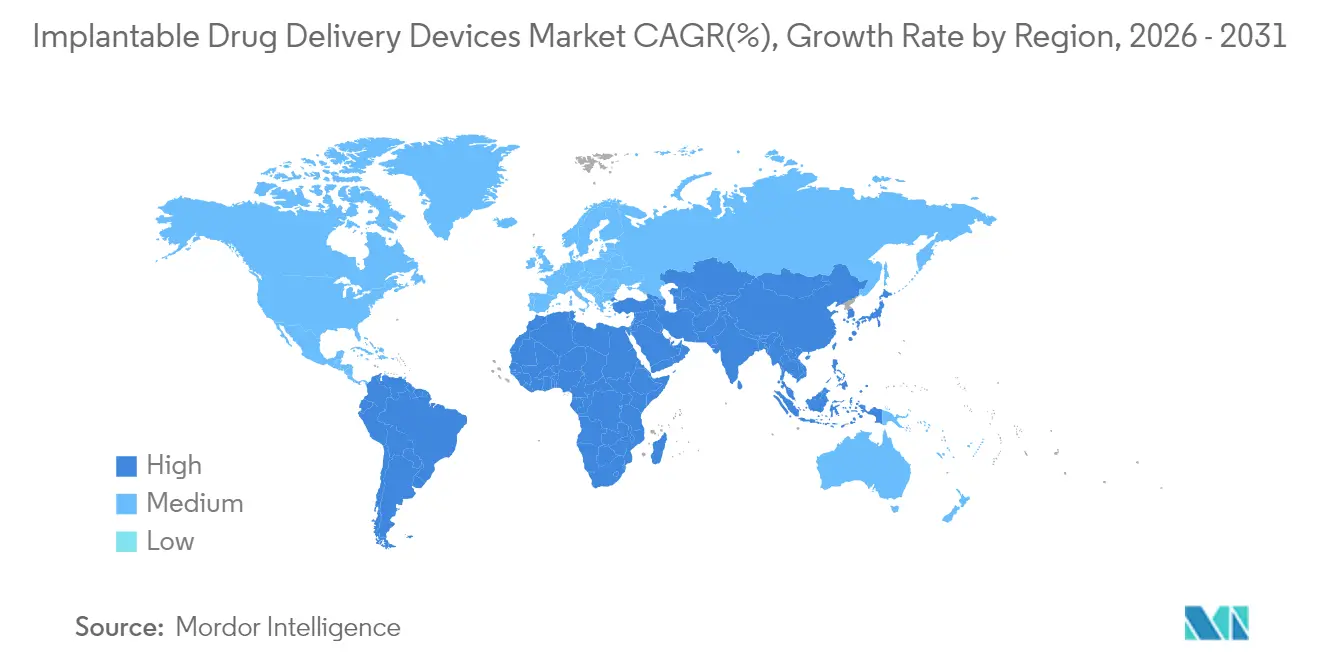

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Implantable Drug Delivery Devices Market Analysis by Mordor Intelligence

Implantable drug delivery devices market size in 2026 is estimated at USD 28.99 billion, growing from 2025 value of USD 26.72 billion with 2031 projections showing USD 43.74 billion, growing at 8.55% CAGR over 2026-2031. Growth reflects the steady transition from broad therapeutic regimens toward precision medicine that minimizes systemic exposure, improves adherence, and curbs repeat procedures. Rising chronic disease prevalence, wider adoption of minimally invasive techniques, and breakthroughs in bioresorbable materials jointly widen clinical indications while lowering lifetime complication risks. Rapid innovation across oncology, ophthalmology, and metabolic care supports new revenue streams that complement the established cardiovascular base. Competition is intensifying as pharmaceutical firms and biotech start-ups introduce drug–device hybrids, compelling incumbent device manufacturers to accelerate R&D alliances and portfolio refurbishments. Regulators are responding with combination-product guidance that balances safety with expedited access, thereby sustaining investor appetite for disruptive platforms.

Key Take Aways

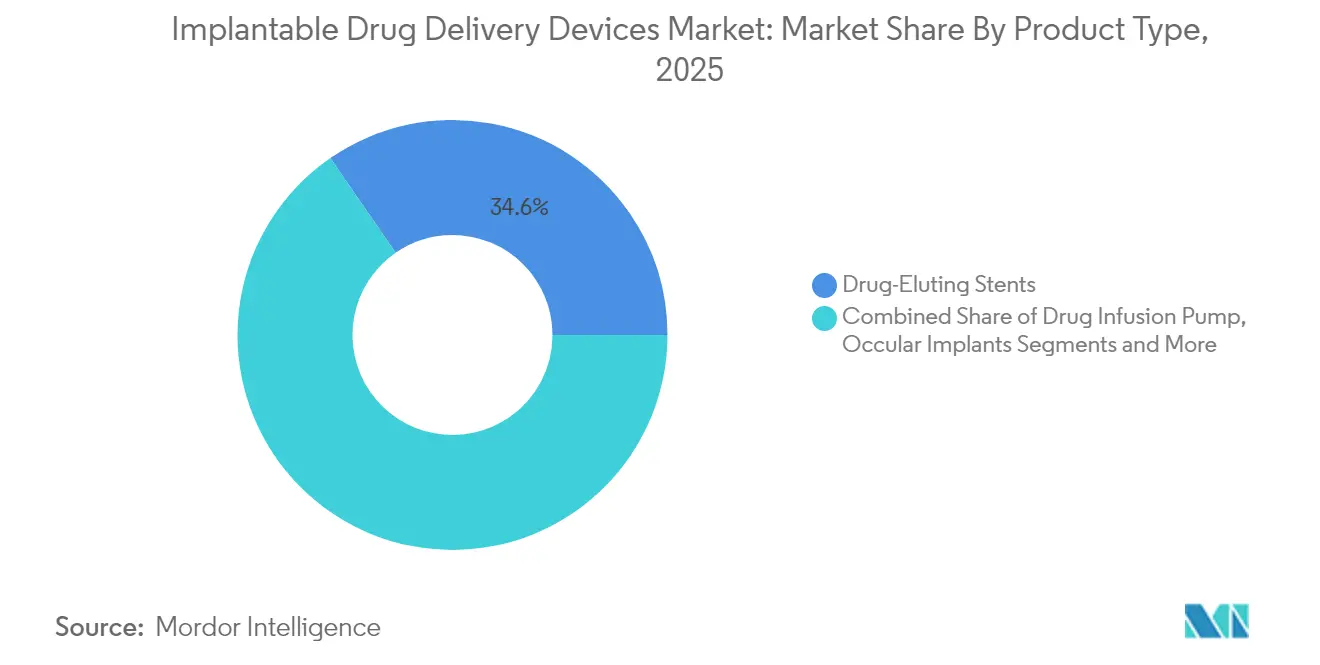

- By product type, drug-eluting stents led with 34.62% revenue share in 2025; bioresorbable stents are projected to advance at a 9.95% CAGR through 2031.

- By technology, non-bioresorbable implants held 57.41% of the implantable drug delivery devices market share in 2025, while bioresorbable formats are forecast to post a 10.23% CAGR to 2031.

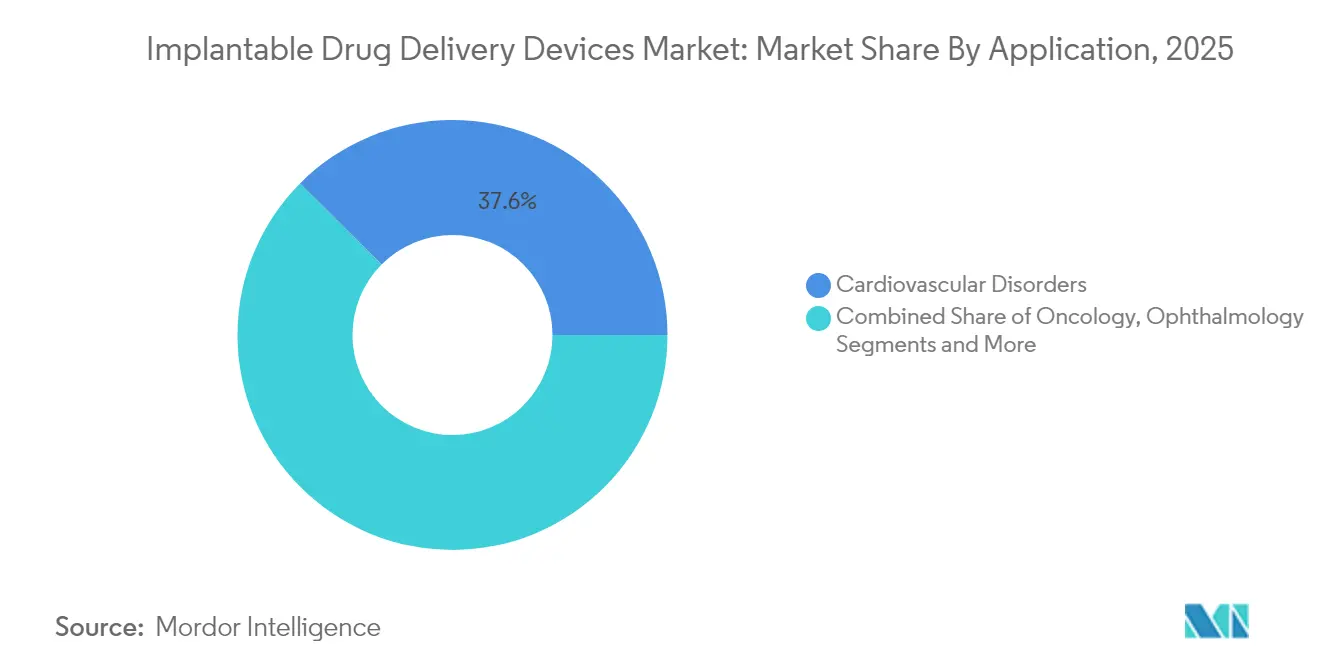

- By application, cardiovascular therapies accounted for 37.55% of the implantable drug delivery devices market size in 2025; oncology applications are expected to expand at a 9.56% CAGR between 2026-2031.

- By end-user, hospitals and surgical centers captured 48.55% share in 2025, whereas ambulatory settings are set to grow quickest at a 8.93% CAGR through 2031.

- By geography, North America maintained 40.62% share in 2025; Asia-Pacific is the fastest-growing region at 9.34% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Implantable Drug Delivery Devices Market Trends and Insights

Driver Impact Analysi*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Burden of Chronic Diseases | 2.4% | Global, with higher impact in North America and Europe | Long term (≥ 4 years) |

| Growing Preference for Targeted and Sustained Drug Delivery | 1.8% | North America, Europe, and developed APAC (Japan, South Korea) | Medium term (2-4 years) |

| Advancements in Biocompatible Materials and Microtechnology | 1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing Demand for Minimally Invasive Procedures | 1.2% | Global, with higher adoption in developed regions | Medium term (2-4 years) |

| Benefits Associated with the Use of Implantable Drug Delivery Systems and Patient Awareness | 0.9% | North America, Europe, and urban centers in APAC | Medium term (2-4 years) |

| Integration of smart sensors and wireless telemetry enabling real-time, personalized dose modulation | 0.7% | North America, Europe, and developed APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Burden of Chronic Diseases

Soaring chronic disease prevalence underpins sustained demand for implantable solutions. In 2024, 60% of US adults lived with at least one chronic condition, with cardiovascular disease alone projected to affect 45.1% of the national population by 2035.[1],Centers for Disease Control and Prevention, “Living With a Chronic Condition,” cdc.gov [2]Journal of the American Heart Association, “Cardiovascular Disease Prevalence and Mortality,” ahajournals.org Hospitals and payers, therefore, prioritize targeted, long-acting therapies that curb hospital readmissions and long-term pharmacotherapy costs. Drug-eluting stents and emerging bioresorbable scaffolds address restenosis while minimizing systemic drug exposure, reinforcing clinician confidence and fuelling procurement budgets. Similar patterns appear across Europe and high-income Asia, where aging demographics magnify chronic disease treatment gaps.

Growing Preference for Targeted and Sustained Drug Delivery

Healthcare providers increasingly favor controlled, site-specific delivery that reduces dosing frequency, toxicity, and adherence lapses. Implantable reservoirs release APIs over months rather than hours, improving performance in glaucoma, chronic pain, and endocrine disorders. Payers welcome the reduction in repeat pharmacy visits and emergency care, while patients gain from fewer side effects and lower lifestyle disruption. Collectively, these benefits catalyze multi-year purchasing plans across accountable-care organizations in the United States and value-based systems in Western Europe.

Advancements in Biocompatible Materials and Microtechnology

Breakthroughs in polymer chemistry and micro-machining elevate device capabilities and safety. Next-generation poly-L-lactic acid scaffolds sustain mechanical integrity and drug elution for up to 150 days while dissolving within 24 months, as documented in a 2025 Journal of Biomaterials Science study.[3]Journal of Biomaterials Science, “Advancements in Drug Delivery Systems Using Biodegradable Polymers,” tandfonline.com Magnesium alloys and tyrocore blends further widen the therapeutic toolkit by shortening degradation times and enhancing radiopacity. Complementary surface-modification techniques improve titanium implant hemocompatibility, trimming rejection rates. These material advances directly expand the implantable drug delivery devices market by overcoming prior durability and inflammation constraints.

Increasing Demand for Minimally Invasive Procedures

Clinicians and patients alike gravitate toward catheter-based or keyhole implantation that lowers infection risk, cuts hospital stays, and facilitates same-day discharge. The SpyGlass intraocular platform, implanted during routine cataract surgery, cut intraocular pressure by 43.7% at 18 months in glaucoma subjects, eliminating topical drops for all participants. Parallel progress in cardiovascular catheter delivery has broadened eligibility for fragile seniors once excluded from open procedures, bolstering procedural volumes in ambulatory surgical centers.

Safety Concerns and Product Recalls

Regulatory vigilance remains high following high-profile recalls such as the 2024 BioZorb incident, which prompted an FDA warning letter highlighting the need for robust post-market surveillance.[4]U.S. Food and Drug Administration, “Medical Device Recalls,” U.S. Food and Drug Administration, fda.gov Even isolated events can dampen surgeon confidence and delay procurement cycles, especially in reimbursement-sensitive markets such as Germany or Japan. Companies must therefore demonstrate comprehensive risk-management frameworks and transparent field-action communication to preserve clinician trust and protect growth trajectories.

Limited Drug Compatibility with Novel Biodegradable Matrices

Roughly 30% of oncology candidates tested in 2025 displayed inadequate stability or altered pharmacokinetics when loaded into biodegradable polymers. Large-molecule biologics remain particularly challenging because conformational integrity can suffer during polymer curing or degradation. Formulation innovations and novel excipients are under development but lengthen R&D timelines and elevate unit costs, temporarily restraining penetration in complex therapeutic categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bioresorbable stents reshape competitive priorities

The product landscape reached an estimated implantable drug delivery devices market size of USD 26.72 billion in 2025, with drug-eluting stents capturing 34.62% share owing to proven restenosis mitigation. Bioresorbable stents, however, command the fastest 9.95% CAGR on the promise of dissolving post-healing and thus averting late-stage thrombosis. The 2024 FDA clearance for Abbott’s Esprit scaffold spurred hospital formulary updates across the United States and the United Kingdom. In ophthalmology, three-year intracameral implants such as SpyGlass' bimatoprost platform advance patient adherence and heighten specialty-clinic demand. Drug infusion pumps remain a workhorse across pain and diabetes indications, and programmable osmotic pumps are moving into neurology, offering micro-dosing that matches circadian rhythms.

Growing clinical evidence accelerates physician uptake. Randomized data show that bioresorbable scaffolds achieve comparable revascularization rates to permanent metal stents at one year, yet avoid the need for lifelong dual-antiplatelet therapy. Such benefits resonate in emerging markets where medication adherence is variable. Meanwhile, contraceptive implants preserve a stable niche, supported by recognized effectiveness and favorable reimbursement. Collectively, these developments keep the implantable drug delivery devices market on an upward trajectory as hospitals diversify inventories to align with specialty-driven care pathways.

By Technology: Bioresorbable platforms headline the innovation wave

Non-bioresorbable formats dominated 2025 revenue at 57.41%, reflecting decades of clinical familiarity. Yet the superior risk profile of degradable systems will lift bioresorbable market value at a 10.23% CAGR. Recent advances in biopolymer gels presented by the Royal Society of Chemistry enable synchronized strength retention and drug-release modulation. Diffusion-controlled implants continue to hold the largest installed base thanks to simple engineering and limited maintenance. Osmotic pressure-driven devices satisfy disease states requiring nanoliter-scale accuracy, while magnetically triggered implants—validated in 2025 Nanoscale research—offer on-demand release with centimeter-level precision.

Electronic pump miniaturization benefits from Moore’s law and wireless charging refinements, opening avenues for home-care deployment. Polymer degradation-driven matrices appeal to oncologists seeking predictable kinetics for local chemotherapy. Together, these trends diversify revenue sources and reinforce long-term confidence in the implantable drug delivery devices market.

By Application: Oncology demonstrates the fastest clinical uptake

Cardiovascular applications retained 37.55% revenue in 2025, but oncology illustrates the steepest 9.56% CAGR as localized chemotherapy and immunotherapy implants ease systemic toxicity. Biodegradable wafers delivering chemotherapeutics into resected tumor beds now extend progression-free intervals in glioblastoma and pancreatic cancer models. Ophthalmology also moves quickly: PolyActiva’s latanoprost implant maintained efficacy for six months in phase II trials, signaling broader potential for chronic ocular diseases. Chronic pain and neurology exploit electronic pumps that titrate dosing via remote algorithms, whereas metabolic disorders rely on implantable insulin pumps that mimic physiologic secretion.

Growing cancer incidence in Asia-Pacific, coupled with under-penetrated radiation capacity, positions localized drug implants as cost-effective adjuncts. In cardiovascular care, the availability of below-the-knee scaffold solutions propels peripheral arterial disease treatment volumes. These dynamics keep the implantable drug delivery devices market diversified across clinical specialties.

By End-user: Ambulatory settings capture expansion momentum

Hospitals and surgical centers represented 48.55% of 2025 revenues, reflecting complexity and acute-care financing. Nevertheless, outpatient migration will lift ambulatory settings at a 8.93% CAGR as device miniaturization and catheter techniques cut procedure times. Medicare data show ASC payment rates below those of hospital outpatient departments, incentivizing payers to redirect elective interventions. Specialty ophthalmology clinics integrate drug-delivery implants into standard cataract workflows, while home-care models extend reach via remote monitoring dashboards that adjust dosing without clinic visits.

Urbanizing populations in Asia and Latin America prefer ambulatory centers for convenience and lower copayments, accelerating device procurement. Hospitals respond by launching dedicated same-day implant suites, ensuring the implantable drug delivery devices industry remains adaptable to care-delivery reforms.

Geography Analysis

North America defended a 40.62% revenue slice in 2025, guided by robust reimbursement, concentrated R&D, and rapid policy adaptation. The FDA’s 2024 communications pilot heightened recall transparency while pledging priority reviews for breakthrough combination products. This environment supports continuous product cycles and early adoption of AI-enabled pumps. The United States contributes roughly 85% of regional sales as ambulatory centers add device procedures to offset elective surgery backlog.

Europe ranks second; Germany and the United Kingdom anchor demand through cardiology and oncology investment. Implementation of the Medical Device Regulation entails additional EMA consultation for drug-device combinations, prolonging dossier compilation yet reinforcing clinical credibility. Notwithstanding these hurdles, local innovators benefit from public grants targeting biodegradable scaffold research, bolstering long-term competitiveness.

Asia-Pacific delivers the swiftest 9.34% CAGR, propelled by chronic-disease epidemiology, insurance expansion, and domestic manufacturing. China’s medical device segment grew above 15% annually, with implantables spotlighted as strategic during the 14th Five-Year Plan. Japan’s super-aging demographics translate into outsized ophthalmology and cardiovascular case volumes, while India leverages public-private hospital partnerships to upgrade catheter-lab capacity. Collaborative trials with Western partners shorten learning curves, injecting credibility into local implants and magnifying export prospects.

Latin America and the Middle East/Africa advance more gradually, constrained by import tariffs and specialist shortages. Still, GCC nations widen adoption through government-funded mega hospitals, whereas Brazil’s private insurers support bioresorbable stent rollouts in tier-one urban centers. Cross-border tele-mentoring mitigates training deficits and opens incremental unit sales.

Competitive Landscape

The implantable drug delivery devices market features moderate fragmentation characterized by overlapping portfolios across medical-device majors, pharmaceutical companies, and agile start-ups. Medtronic, Boston Scientific, and Abbott hold notable shares in cardiovascular stents, benefiting from entrenched surgeon trust and scale-driven procurement discounts. Yet innovation leadership increasingly emerges from ophthalmology and oncology specialists such as SpyGlass Pharma and PolyActiva, whose focused R&D cycles outpace conglomerate processes.

Strategic alliances bridge material science, drug formulation, and sensor analytics. In 2025, Abbott disclosed an AI-enhanced pump prototype that adjusts real-time dosing via physiological feedback, signaling convergence between digital health and implantable therapeutics. Boston Scientific broadened pipeline scope through minority stakes in magnetically triggered implant start-ups, hedging against diffusion-only obsolescence. Simultaneously, pharmaceutical firms leverage drug portfolios to launch combination implants that extend IP protection beyond molecule expiration.

Regulatory sophistication acts as both moat and catalyst. Companies mastering combination-product submissions secure multi-year lead times. Conversely, missteps—as evidenced by BioZorb’s recall—expose reputational risk and invite challenger share gains. Across regions, distributor consolidation yields pricing leverage, motivating manufacturers to adopt direct sales channels or co-marketing with hospital networks. Overall, the sector rewards differentiated technology, robust evidence packages, and agile market-access strategies

Implantable Drug Delivery Devices Industry Leaders

Medtronic PLC

Boston Scientific Corporation

Abbott Laboratories

Bayer AG

Bausch + Lomb Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Vivani Medical expanded its collaboration with Okava Pharmaceuticals to develop OKV-119, a GLP-1 implant for canine weight and diabetes management

- April 2025: Orchestra BioMed received FDA IDE amendment approval for its Virtue SAB sirolimus-angioinfusion balloon pivotal trial

- April 2025: Continuity Biosciences invested in PinPrint’s high-resolution 3D-printed microneedle technology to reach therapeutic and cosmetic segments.

- March 2025: ANI Pharmaceuticals secured an FDA label expansion for ILUVIEN to treat chronic non-infectious uveitis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the implantable drug-delivery devices market as all permanently or temporarily placed systems, such as drug-eluting stents, contraceptive rods, programmable osmotic pumps, and intra-/trans-ocular implants, that release an active pharmaceutical ingredient inside the body in a controlled manner for at least seven days.

Scope Exclusion: External infusion pumps and wearables that can be removed without a minor procedure are out of scope.

Segmentation Overview

- By Product Type

- Drug-Eluting Stents

- Bioresorbable Stents

- Drug Infusion Pumps (incl. Intrathecal)

- Intra-/Trans-Ocular Implants

- Contraceptive Implants

- Programmable Osmotic Pumps

- Other Product Types

- By Technology

- Diffusion-Controlled Implants

- Osmotic Pressure–Driven Implants

- Magnetically-Triggered Implants

- Pump-Based (Electronic / Mechanical)

- Polymer Matrix Degradation–Driven

- By Application

- Cardiovascular Disorders

- Oncology

- Autoimmune / Inflammatory Diseases

- Obstetrics and Gynecology

- Ophthalmology

- Chronic Pain and Neurology

- Metabolic Disorders (e.g., Diabetes)

- Other Applications

- By End-user

- Hospitals and Surgical Centres

- Ambulatory Care and Pain Clinics

- Specialty Ophthalmology Centres

- Home-Care Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We then interview interventional cardiologists, ophthalmologists, pain-clinic heads, and device supply-chain managers across North America, Europe, and Asia Pacific. These discussions clarify off-label adoption rates, typical selling prices, and near-term regulatory expectations, letting us challenge or affirm secondary totals before numbers reach the model.

Desk Research

Our analysts first canvass freely available tier-1 sources, such as the US FDA device approvals database, WHO Chronic Disease Dashboard, Eurostat procedure counts, and trade association briefs from AdvaMed and the European Society of Cardiology, to ground the patient pool, procedure volume, and regulatory context. Company 10-Ks, investor presentations, and peer-reviewed journals in Biomaterials supplement insight on material science shifts toward bioresorbables. Subscription files from D&B Hoovers, Dow Jones Factiva, and Questel help us validate revenue splits, news flow, and patent density. This list is illustrative; many more references underpin the desk review.

Market-Sizing & Forecasting

A top-down build, starting with coronary stent implant counts, contraceptive implant penetration, and programmable pump placements captured from hospital discharge and customs data, is cross-checked with sampled ASP × unit estimates from supplier roll-ups to avoid blind spots. Key variables include chronic disease prevalence, elective procedure rebound, FDA and CE approvals per year, polymer adoption rates, and average stent ASP shifts. Multivariate regression links those drivers to value growth, after which scenario analysis adjusts for price erosion and country spend trajectories. Gaps in bottom-up granularity are bridged through ratio benchmarks agreed on during expert calls.

Data Validation & Update Cycle

Before release, every worksheet passes a three-layer analyst review where variance beyond ±5 % versus historical series or peer signals triggers re-checks. We refresh the full dataset annually and issue interim updates when recalls, major approvals, or reimbursement changes materially alter demand; clients therefore receive the latest vetted view.

Why Mordor's Implantable Drug Delivery Devices Baseline Commands Reliability

Published estimates often diverge because firms pick different product baskets, base years, and refresh cadences.

Key gap drivers include some studies that fold external pumps or broader drug-delivery devices into totals, a few that assume uniform ASP declines across geographies, and others that project aggressive bioresorbable uptake without matching regulatory milestones. Mordor's scope, our mixed driver set, and an annual refresh anchored in primary validation temper such extremes, giving decision-makers a balanced starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.72 B (2025) | Mordor Intelligence | - |

| USD 29.32 B (2024) | Global Consultancy A | Includes external infusion pumps and broader drug-delivery devices |

| USD 13.29 B (2025) | Trade Journal B | Omits ocular and contraceptive implants, uses hospital revenue sampling only |

| USD 11.09 B (2025) | Regional Consultancy C | Conservative price assumptions and limited Asia-Pacific coverage |

These comparisons show that, by selecting the right device list, blending top-down incidence math with targeted bottom-up checks, and revisiting inputs yearly, Mordor Intelligence delivers a dependable, transparent baseline clients can trace and replicate.

Key Questions Answered in the Report

How large is the implantable drug delivery devices market in 2026?

The implantable drug delivery devices market size stands at USD 28.99 billion in 2026 and is forecast to grow to USD 43.74 billion by 2031.

Which product segment holds the largest market share?

Drug-eluting stents led the market with 34.62% share in 2025, thanks to wide adoption in cardiovascular interventions.

Which is the fastest growing region in Implantable Drug Delivery Devices Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What is the fastest-growing regional market?

Asia-Pacific is expanding at a 9.34% CAGR through 2031, driven by rising chronic disease incidence and accelerating healthcare investment.

Which application area shows the highest growth rate?

Oncology applications are projected to advance at a 9.56% CAGR as localized implants reduce systemic chemotherapy toxicity.

How are regulatory changes affecting market growth?

New FDA combination-product guidelines and Europe’s Medical Device Regulation lengthen approval timelines but offer clearer pathways, rewarding firms that align early with enhanced evidence requirements .

What technological trend will shape future competition?

Bioresorbable materials integrating AI-enabled dosing sensors are poised to redefine therapy personalization and could unlock new indications across neurodegenerative and metabolic disorders.

Page last updated on: