Self-injection Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

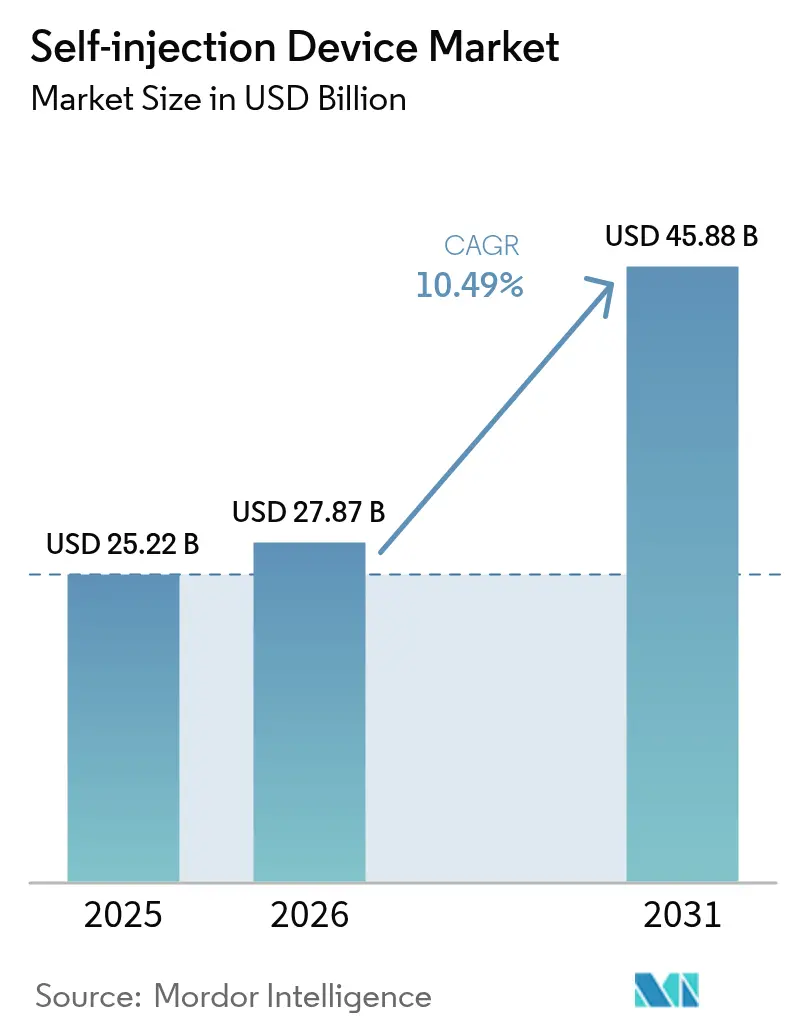

| Market Size (2026) | USD 27.87 Billion |

| Market Size (2031) | USD 45.88 Billion |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

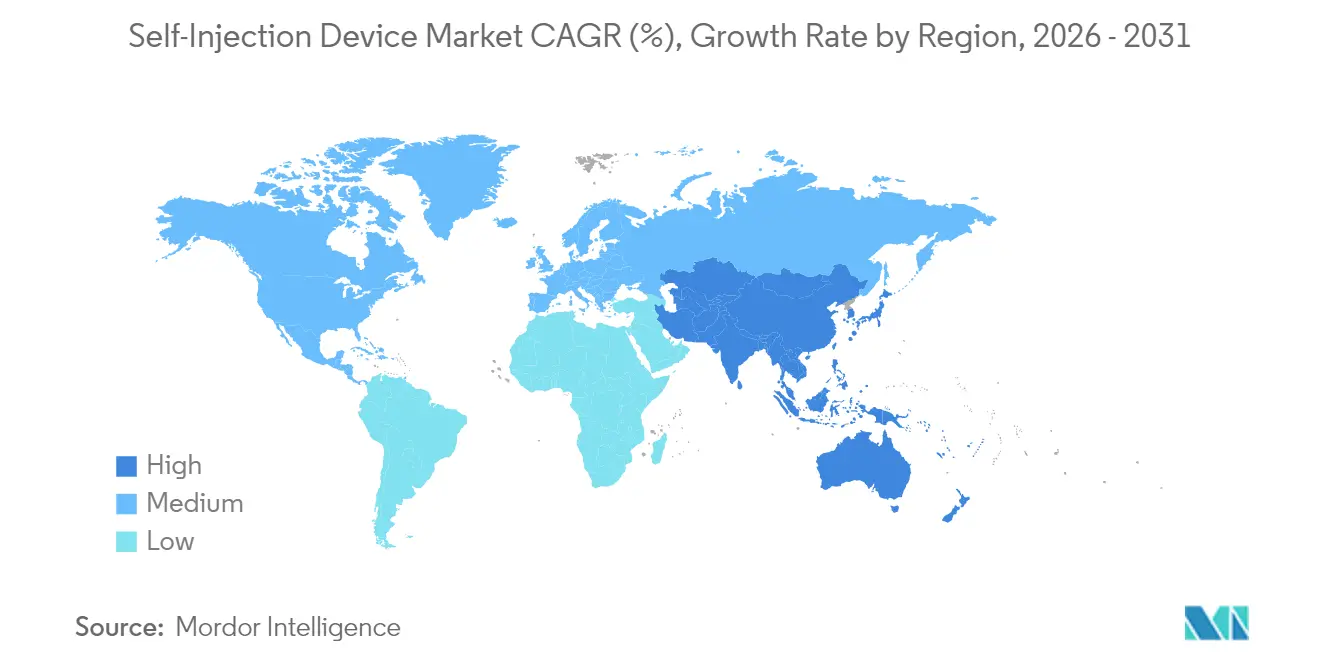

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

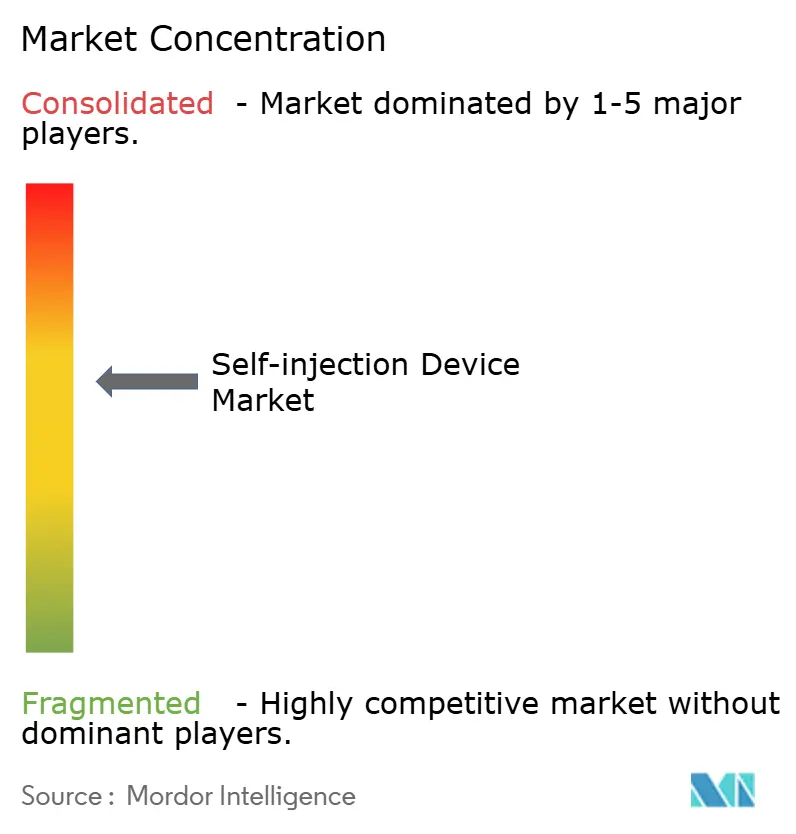

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-injection Device Market Analysis by Mordor Intelligence

The self-injection devices market size was valued at USD 25.22 billion in 2025 and estimated to grow from USD 27.87 billion in 2026 to reach USD 45.88 billion by 2031, at a CAGR of 10.49% during the forecast period (2026-2031). Growth rests on three pillars: population aging that drives chronic disease prevalence, the biopharmaceutical shift toward patient-centric delivery formats, and payer pressure to keep treatment in lower-cost settings. Pharmaceutical producers, device specialists, and contract manufacturers are expanding capacity for glucagon-like peptide-1 (GLP-1) therapies, oncology drugs, and other biologics formulated for at-home administration, signalling durable demand for advanced injection platforms. Regulatory harmonisation—in particular the United States Food and Drug Administration’s streamlined pathways for combination products and the European Union’s evolving Medical Device Regulation (MDR)—shortens approval cycles and spurs device iteration. Meanwhile, biosimilar launches are widening access to molecules once confined to infusion centres, further shifting the point of care to the patient’s home. Novo Nordisk’s USD 4.1 billion factory programme in North Carolina and the FDA clearance of Hikma’s liraglutide biosimilar in December 2024 encapsulate the dual forces of large-scale capacity build-out and affordable alternatives that underpin the current expansion[1]CNBC News Desk, “Novo Nordisk to Invest $4.1 Billion in North Carolina Manufacturing Hub,” cnbc.com.

Key Report Takeaways

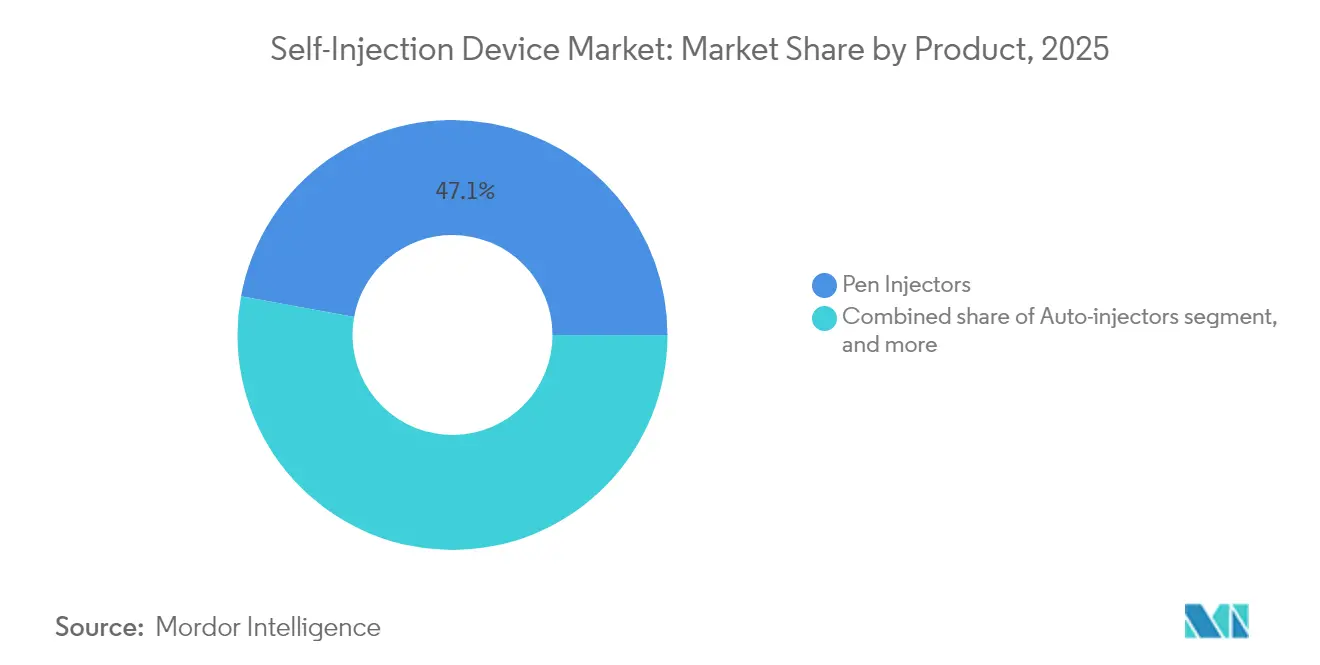

- By product category, pen injectors retained 47.12% of self-injection devices market share in 2025; wearable injectors are projected to expand at a 12.21% CAGR to 2031.

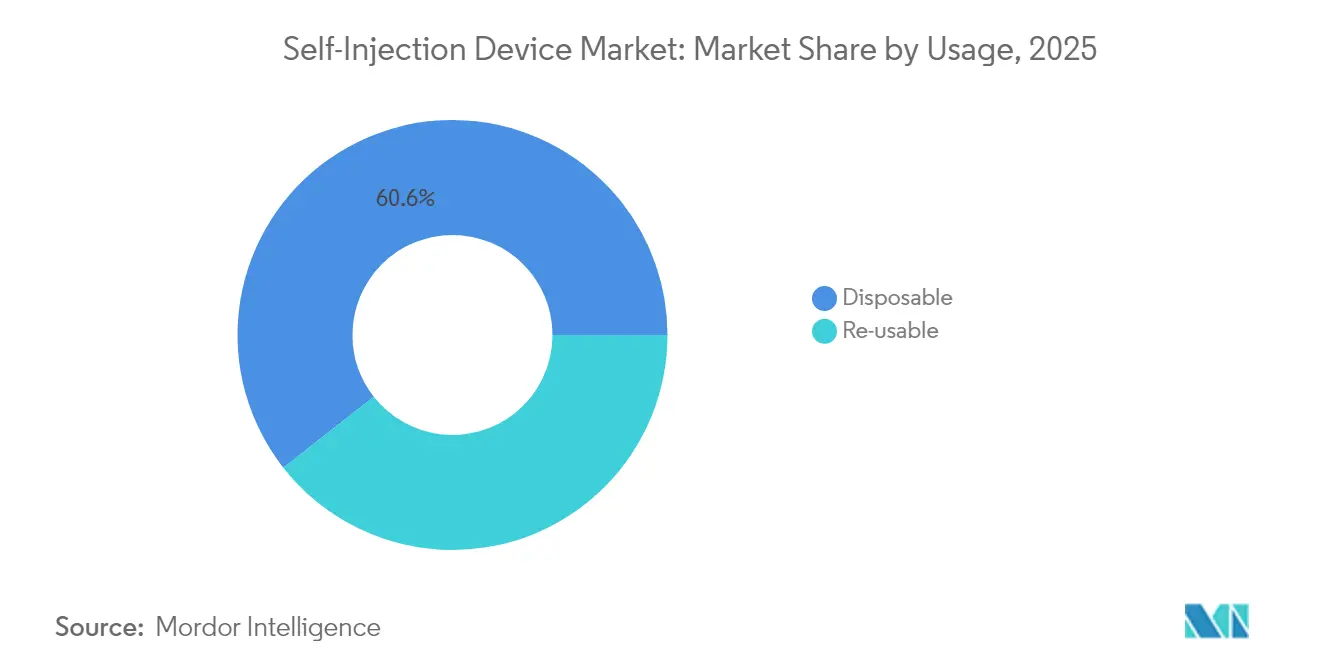

- By usage, disposable formats held 60.58% of the self-injection devices market size in 2025, while re-usable systems record the highest projected CAGR at 12.01% through 2031.

- By application, diabetes and hormonal disorders led with 46.02% of self-injection devices market size in 2025, whereas oncology registers the fastest 13.09% CAGR to 2031.

- By geography, North America commanded 38.12% revenue share in 2025; Asia-Pacific is the fastest-growing region, advancing at an 11.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self-injection Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +2.1% | Global with North America & Europe concentration | Long term (≥ 4 years) |

| Increasing patient preference for home healthcare | +1.8% | Global, led by North America & Asia-Pacific cities | Medium term (2–4 years) |

| Expansion of biologic & biosimilar therapeutics | +2.3% | North America & EU; emerging in Asia-Pacific | Medium term (2–4 years) |

| Advancements in drug-device combination technologies | +1.6% | Global, R&D centred in North America & EU | Long term (≥ 4 years) |

| Supportive reimbursement & cost-containment policies | +1.4% | North America & EU; developing in Asia-Pacific | Short term (≤ 2 years) |

| Growing pharma–medtech partnerships | +1.2% | Global, investment hubs in North America & EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

More than 537 million adults live with diabetes and cancer incidence has climbed 47% since 2000; these figures create a sustained pull for at-home injection therapies. Insulet’s SmartAdjust clearance in August 2024 illustrates regulators’ support for automated insulin delivery platforms that lower facility pressure while enabling multidisease care. Pharmaceutical pipelines now bundle agents addressing comorbidities into single high-viscosity formulations deliverable via connected autoinjectors, improving adherence and containing costs borne by payers. Ageing demographics in Europe, North America, and parts of Asia amplify the long-run influence of this driver.

Increasing Patient Preference For Home Healthcare

Pandemic-era exposure to telehealth strengthened demand for self-administration tools that offer privacy and flexibility. Coherus BioSciences’ UDENYCA ONBODY came to market in February 2024, letting neutropenia patients avoid a second clinic visit for pegfilgrastim. Real-time adherence monitoring and dosing feedback delivered through Bluetooth-enabled pen injectors lessen safety concerns and align with payers’ desire to shift care outside hospitals. Younger cohorts comfortable with digital interfaces now expect connected devices as standard rather than premium features, supporting mid-term growth.

Expansion of Biologic & Biosimilar Therapeutics

A recent screen identified 182 large-volume subcutaneous biologics—15% of all injectable biologics—highlighting the demand for platforms accommodating 2–10 mL doses while maintaining viscosity tolerances beyond 15 cP. BD’s collaboration with Ypsomed on the Neopak XtraFlow syringe for YpsoMate 2.25 underscores the tooling and glass-barrel innovations necessary to capture this opportunity. Patent cliffs for adalimumab, trastuzumab, and other blockbusters hasten biosimilar entry, expanding patient pools and pushing device volumes up across mature and emerging markets alike.

Advancements in drug-device combination technologies

R&D teams are embedding micro-controllers, pressure sensors, and cellular chips into autoinjectors to transform them into data-rich therapeutic managers. SHL Medical holds 227 active patent families covering disposable autoinjector layouts, drive mechanisms, and connectivity stacks, illustrating the intellectual property intensity of the segment. The FDA’s interoperability designation for diabetes ecosystems accelerates acceptance of modular, app-integrated devices that personalise dosing on the fly. Over the long term, these developments position self-injection devices as nodes within broader digital-health networks.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory & quality compliance requirements | -1.7% | Global, highest in North America & EU | Long term (≥ 4 years) |

| Availability of alternative drug-delivery modalities | -1.2% | Global, concentration in developed markets | Medium term (2–4 years) |

| High upfront device development & manufacturing costs | -1.5% | Global, most acute for small and mid-size manufacturers in the EU & US | Medium term (2–4 years) |

| Concerns over safety, needle anxiety & user errors | -1.3% | Global, with heightened sensitivity in pediatric and geriatric cohorts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory & Quality Compliance Requirements

The European Parliament’s October 2024 vote to revise MDR deadlines showed how certification backlogs can stall product introductions and inflate compliance costs, which can top USD 50 million for a globally launched combination product[2]European Parliament, “Resolution on Proposed MDR Transition Timelines,” europarl.europa.eu. The FDA treats on-body injectors as Class II devices subject to special performance controls, adding design-verification layers that can lengthen timelines by 18 months. Smaller innovators often lack the capital for parallel submissions across regions, consolidating power among larger companies with dedicated regulatory teams.

Availability of Alternative Drug-Delivery Modalities

Rani Therapeutics’ capsule-based delivery platform attracted obesity-drug collaborators in 2024, spotlighting oral biologic options that bypass injections entirely. Transdermal microneedle patches, a USD 768.9 million segment in 2024, are on a path to double within a decade, creating substitution risk in dermatology and vaccine indications[3]Frontiers in Bioengineering and Biotechnology, “Global Microneedle Market Forecast,” frontiersin.org. Long-acting depot injections lower dosing frequency and therefore device utilisation, while needle-free jet injectors challenge the conventional needle-and-syringe paradigm, forcing incumbents to invest in alternative formats or risk share erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wearable Injectors Accelerate Innovation Despite Pen Dominance

Pen injectors generated the highest revenue, holding 47.12% self-injection devices market share in 2025, supported by mature manufacturing infrastructure and clinician familiarity. The self-injection devices market size for pens is projected to reach USD 19.13 billion by 2031 at a steady 8.27% CAGR. Wearable injectors, however, outpace every other product class at a 12.21% rate as biologic concentrations and volumes rise. Stevanato Group’s Vertiva on-body system dispenses up to 10 mL over several minutes, lending itself to oncology and rare-disease regimens once limited to intravenous infusion. Auto-injectors remain a resilient sub-segment, buoyed by biosimilar filtration of adalimumab and etanercept into primary care. Needle-free devices, although technologically compelling, still confront price and regulatory hurdles that curb immediate impact.

A second wave of innovation focuses on device connectivity. Bluetooth modules in wearable pumps transmit dosing logs to cloud dashboards, giving physicians granular adherence visibility. Pharmaceutical firms now bundle apps with devices to differentiate therapy packages and gather real-world evidence for health-technology assessments. As data architecture becomes integral, device makers are forced to build cybersecurity competencies alongside mechanical engineering capabilities, raising entry barriers for new entrants and intensifying collaboration needs between software and hardware teams.

By Usage: Sustainability Concerns Lift Re-Usable Formats

Disposable units retained 60.58% revenue in 2025 because infection-control guidelines and patient convenience favour single-use simplicity. Yet pressure from European regulators and hospital sustainability mandates is nudging buyers toward re-usables, which are expanding at 12.01% annually through 2031. The self-injection devices market size for re-usable formats is forecast to climb from USD 9.94 billion in 2025 to USD 19.59 billion by 2031. SHL Medical’s electromechanical Elexy platform, compatible with cartridges and prefilled syringes from 1–5 mL, addresses both environmental and cost objectives by spreading electronics across hundreds of injections.

Healthcare providers in France and Sweden have begun pilot tenders requiring carbon-footprint disclosures, accelerating adoption curves for re-usable hardware. Meanwhile, the economics of embedding radios, batteries, and displays favour re-usables because fixed electronics costs are amortised over greater dose counts. Manufacturers respond with modular designs where drug-contact components remain disposable while drive units are retained, balancing sterility with sustainability.

By Application: Oncology Leads Growth While Diabetes Maintains Scale

Diabetes and hormonal disorders accounted for 46.02% revenue in 2025, underpinned by the entrenched insulin-pen ecosystem and growing prevalence of GLP-1 obesity treatments. However, oncology indications register the fastest 13.09% CAGR through 2031 because immuno-oncology agents migrate from infusion chairs to subcutaneous auto-injectors. The FDA’s July 2024 approval of Tecentriq Hybreza, cutting administration time to 7 minutes, accelerates oncologist embrace of in-home dosing protocols. Together, oncology and supportive-care injectors are set to represent USD 7.65 billion self-injection devices market size by 2031.

Autoimmune-disease treatments continue to benefit from 1 mL autoinjectors, but pipeline analysis shows upcoming agents trending toward higher concentrations, which may shift volume to wearable devices. Pain management lags because opioid stewardship dampens injections, although neurology biologics for migraine and multiple sclerosis add incrementally. Niche growth appears in rare diseases where high-cost therapies demand precision delivery to justify payer reimbursement.

Geography Analysis

North America contributed 38.12% of global revenue in 2025 thanks to robust reimbursement, high biologic penetration, and early connected-device adoption. The region’s self-injection devices market size is on track to grow 9.05% per year through 2031, supported by BD’s expanded syringe-barrel capacity and the FDA’s clear guidance on digital-health add-ons. Canada’s health-technology assessments increasingly endorse connected autoinjectors for adherence improvement, while Mexico’s maquiladora site expansions create a cost-efficient production corridor for export into the United States.

Asia-Pacific, expanding at an 11.21% CAGR, is propelled by China’s National Medical Products Administration, which approved 12,213 devices in 2024, a gateway for local manufacturers scaling into global supply chains. India’s contract-development organisations are pairing with European pharma to build fill-finish lines dedicated to GLP-1 pens, compressing lead times and costs. Japan, South Korea, and Australia combine mature reimbursement systems with ageing populations, creating immediate demand for high-end connected devices.

Europe sustains mid-single-digit growth as MDR compliance costs restrain smaller players even while harmonised rules simplify multi-country launches. Germany’s sickness funds reimburse electromechanical pens when paired with outcomes-based contracts that cap payer risk. The UK’s National Institute for Health and Care Excellence (NICE) has invited real-world evidence generated by connected autoinjectors into cost-effectiveness files, a move expected to encourage broader digital uptake across the bloc. Eastern European markets remain cost-sensitive but are adopting disposable pens for biosimilar adalimumab at faster clips than Western peers.

South America and the Middle East & Africa are at earlier stages, yet rising chronic-disease incidence and public-sector procurement reforms point to higher volumes over the decade. Brazil’s national immunisation plan has already earmarked budget for 3 mL prefilled devices to support oncology biosimilars, while Saudi Arabia’s Vision 2030 healthcare push fast-tracks registration of patient-centric devices.

Competitive Landscape

BD, SHL Medical, and Insulet anchor a market that remains moderately consolidated; the top five firms jointly hold roughly 60% share. BD surpassed USD 1 billion in biologics-delivery sales and deepened its moat with a French plant that will lift prefillable syringe output sevenfold by 2030. SHL Medical safeguards its lead through a patent wall and, in March 2025, inaugurated a United States facility to shorten customer supply chains and capture rising biologic volumes. Insulet exemplifies therapeutic-area specialisation: with more than 500,000 active global users of the Omnipod system, it booked 22% revenue growth in 2024 and plans a product family extension into multi-hormone delivery.

Competitive strategy now centres on three vectors. First, capacity scalability—Gerresheimer’s USD 180 million Georgia expansion and Gerresheimer–Eli Lilly supply deals underscore the premium on secure, high-volume output. Second, technology platforms—BD–Ypsomed’s collaboration illustrates demand for flexible systems that can accept highly viscous formulations without altering patient technique. Third, therapeutic alignment—Aktiv Medical Systems’ partnership with a global pharma company on 4 mL autoinjectors positions it as a go-to platform for obesity agents with higher dose volumes.

Mergers and acquisitions remain an expedient route to pipeline access; Teleflex’s EUR 760 million acquisition of BIOTRONIK’s vascular-intervention unit broadens its drug-coated device portfolio, hinting at further convergence between interventional and subcutaneous delivery technologies. At the fringes, needle-free specialists and oral-delivery startups present disruption risks, although regulatory and clinical validation hurdles remain high. Overall, capital intensity, regulatory expertise, and integrated digital capabilities act as key competitive buffers.

Self-injection Device Industry Leaders

Becton, Dickinson and Company

Insulet Corporation

Ypsomed AG

Gerresheimer AG

Halozyme (Antares Pharma Inc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SHL Medical opened a new autoinjector manufacturing site in the United States, adding regional capacity for high-volume biologics delivery.

- February 2025: Teleflex acquired BIOTRONIK’s Vascular Intervention business for EUR 760 million (USD 820 million) to enhance its drug-coated delivery portfolio.

- February 2025: The FDA approved Merilog (insulin-aspart-szjj), the first rapid-acting insulin biosimilar in a 3 mL prefilled pen, broadening access for 8.4 million Americans with insulin needs.

- January 2025: Aktiv Medical Systems partnered with a global pharmaceutical company to co-develop high-concentration autoinjectors up to 4 mL.

- December 2024: The FDA cleared Hikma’s generic liraglutide, the first GLP-1 biosimilar, reducing diabetes-therapy cost barriers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the self-injection device market as all prescription-grade, patient-handled injectors, including disposable or reusable pen injectors, pre-filled or on-body auto-injectors, patch-pump wearable injectors, and spring or gas-powered needle-free jet systems, sold for at-home medication delivery. Devices supplied empty for compounding or strictly confined to clinical settings sit outside this boundary, giving buyers a clear like-for-like baseline.

Scope Exclusion: Single-use safety syringes, smartphone apps without a hardware injector, and hospital-only infusion pumps are not part of the market universe.

Segmentation Overview

- By Product

- Pen Injectors

- Disposable Pens

- Re-usable Pens

- Auto-injectors

- Prefilled Disposable

- Prefilled Re-usable

- Wearable Injectors

- Large-volume Patch Pumps

- Bolus-on-demand Devices

- Needle-Free Injectors

- Spring-powered Jet

- Gas-powered Jet

- Pen Injectors

- By Usage

- Disposable

- Re-usable

- By Application

- Diabetes & Other Hormonal Disorders

- Auto-immune Diseases

- Oncology

- Pain Management

- Other Applications

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Desk Research

Our analysts started with open datasets from regulatory agencies such as the US FDA 510(k) database, EMA EUDAMED, and Health Canada to map approved SKUs. They then matched shipment volumes through UN Comtrade customs codes and national export statistics. Epidemiological and therapy uptake numbers came from sources such as the International Diabetes Federation, WHO Global Health Observatory, and peer-reviewed journals in BMJ and Diabetes Care. To benchmark company revenue splits, we accessed D&B Hoovers, while patent momentum checks were run in Questel. Securities filings, investor presentations, and trade-show proceedings filled remaining data gaps. The sources mentioned illustrate the mix; many additional public records were consulted during validation.

Primary Research

Interviews and structured surveys with device engineers, endocrinologists, procurement managers, and regional distributors across North America, Europe, and Asia-Pacific helped verify addressable patient pools, price corridors, and refill frequencies. Their insights allowed us to adjust model assumptions uncovered during desk work.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build was constructed for insulin, GLP-1, and biologic therapies, and then cross-checked with selective bottom-up supplier roll-ups of sampled ASP × volume. Key variables include diagnosed diabetes prevalence, biologic pipeline approvals, at-home care spending, injector ASP trends, device reuse ratios, and regional reimbursement policy shifts. Multivariate regression on these drivers underpins the 2025-2030 forecast, while scenario analysis stress-tests high and low adoption cases. Where distributor surveys lacked full country depth, we prorated volumes using chronic-disease incidence and GDP-weighted purchasing-power indices.

Data Validation & Update Cycle

Outputs are run through variance checks against external trade, revenue, and epidemiology markers, reviewed by a second analyst, and escalated for senior sign-off. Reports refresh annually, with interim updates triggered by material regulatory or competitive events. Every delivery includes a last-minute fact pass so clients receive the freshest view.

Why Mordor's Self-injection Device Baseline Earns Trust

Published estimates often diverge because firms choose different product mixes, currency bases, and forecast cadences. Recognizing this, we align scope to actual patient-usable hardware and refresh inputs each year, letting decision-makers compare like for like.

Key gap drivers include whether refill cartridges are bundled, how aggressively biologic pipeline launches are projected, and the cadence at which ASP deflation is applied. Our study reports the base year in today's dollars and rolls regional data upward only after bottom-up cross-checks, while some publishers rely on undisclosed mark-ups or exclude whole injector families.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.22 B | Mordor Intelligence | - |

| USD 24.80 B | Global Consultancy A | Broader therapy bundling, limited cross-check with device shipments |

| USD 4.88 B | Business Publisher B | Excludes pen and wearable injectors, uses conservative ASP index and regional weighting |

This comparison shows that when scope, variables, and refresh cadence are harmonized, our 2025 baseline offers a balanced, transparent reference that can be traced back to publicly verifiable data points and repeatable steps.

Key Questions Answered in the Report

What is the current size of the self-injection devices market?

The self-injection devices market is valued at USD 27.87 billion in 2026 and is projected to reach USD 45.88 billion by 2031.

Which product type is growing fastest within self-injection devices?

Wearable injectors are advancing at a 12.21% CAGR, outpacing pen and auto-injectors thanks to their ability to deliver large-volume biologics.

Why is Asia-Pacific the fastest-growing region for self-injection devices?

Regulatory streamlining, domestic manufacturing build-out, and rising chronic-disease prevalence are pushing Asia-Pacific market revenue at an 11.21% CAGR through 2031.

How are sustainability goals shaping device design?

Regulators and hospital systems, especially in Europe, favour re-usable or hybrid platforms that cut single-use plastics, driving 12.01% annual growth in re-usable formats.

Which therapeutic area will contribute most to future market acceleration?

Oncology is forecast to expand at 13.09% through 2031 as immuno-oncology agents transition from infusion to subcutaneous autoinjector delivery.

What major hurdle could slow market growth?

Stringent regulatory and quality-system requirements, particularly under the EU MDR and FDA combination-product rules, can extend development timelines and inflate compliance costs.

Page last updated on: