United Kingdom Drug Delivery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

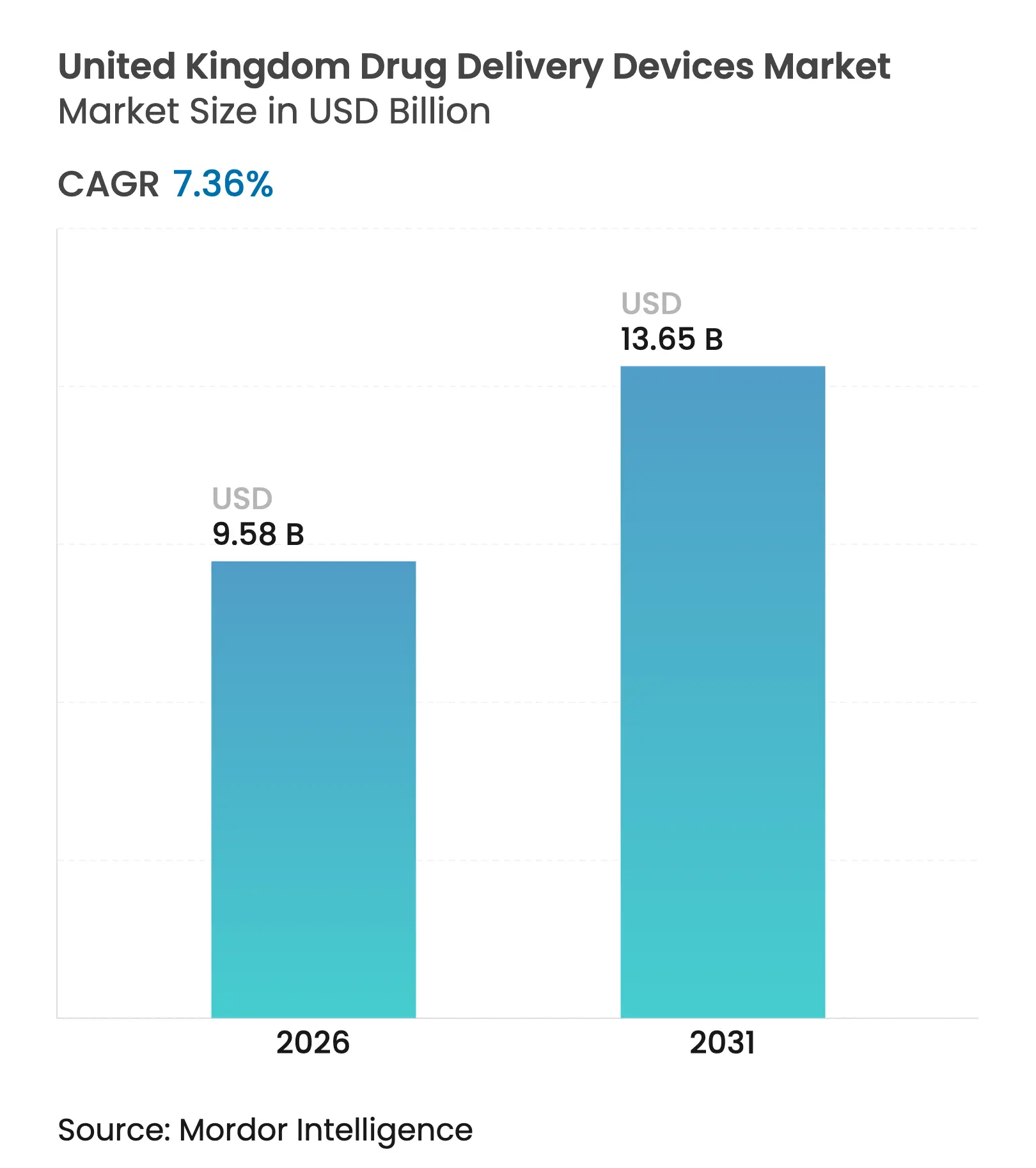

| Market Size (2026) | USD 9.58 Billion |

| Market Size (2031) | USD 13.65 Billion |

| Growth Rate (2026 - 2031) | 7.36 % CAGR |

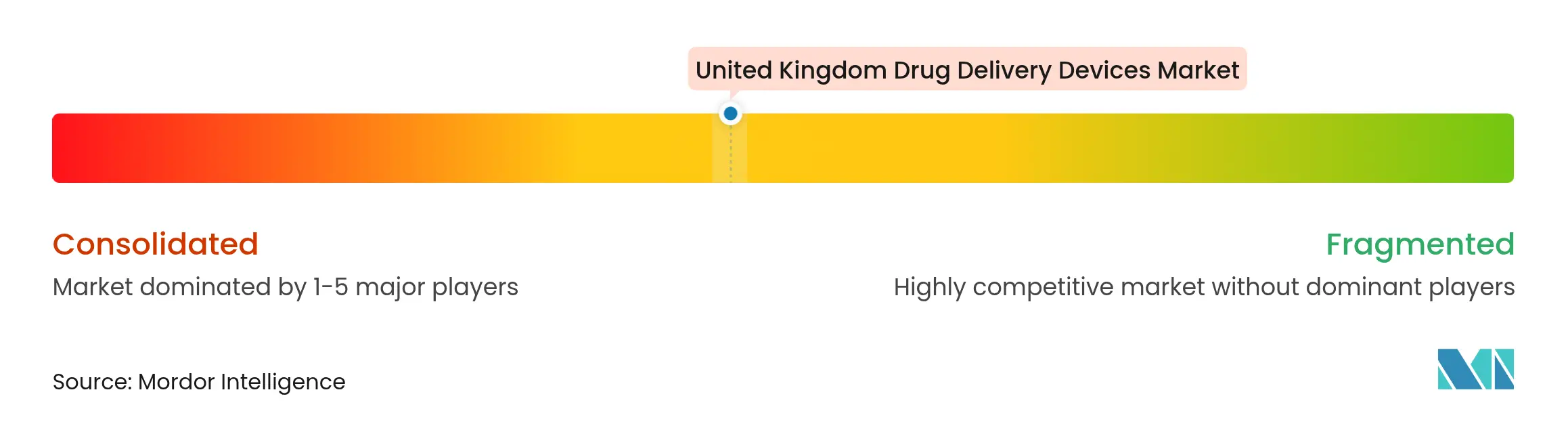

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United Kingdom Drug Delivery Devices Market Analysis by Mordor Intelligence

The United Kingdom drug delivery devices market size is expected to grow from USD 8.92 billion in 2025 to USD 9.58 billion in 2026 and is forecast to reach USD 13.65 billion by 2031 at 7.36% CAGR over 2026-2031. Growth is propelled by the National Health Service (NHS) drive for precision medicine, rising adoption of home-based care, and accelerated approval pathways that shorten time-to-market for innovative devices. Every 1% gain in adherence is estimated to save the NHS about GBP 500 million in avoided hospital admissions, keeping cost reduction at the center of procurement strategies.[1]NHS England, “Medicines Value Programme,” england.nhs.uk Post-Brexit regulation has shifted to UKCA marking, yet the new International Reliance procedure allows devices cleared in Australia, Canada, the European Union, or the United States to enter the United Kingdom drug delivery devices market more rapidly, sustaining the country’s attractiveness for foreign innovators. Sustainability also matters: near-zero global-warming-potential (GWP) propellants in next-generation pressurised metered-dose inhalers (pMDIs) are helping manufacturers win NHS tenders while meeting carbon-reduction targets. A parallel surge in connected devices responds to medication non-adherence that costs the NHS roughly GBP 637 million each year.[2]National Institute for Health and Care Research, “Impact of Non-Adherence on Healthcare Outcomes,” nihr.ac.uk

Key Report Takeaways

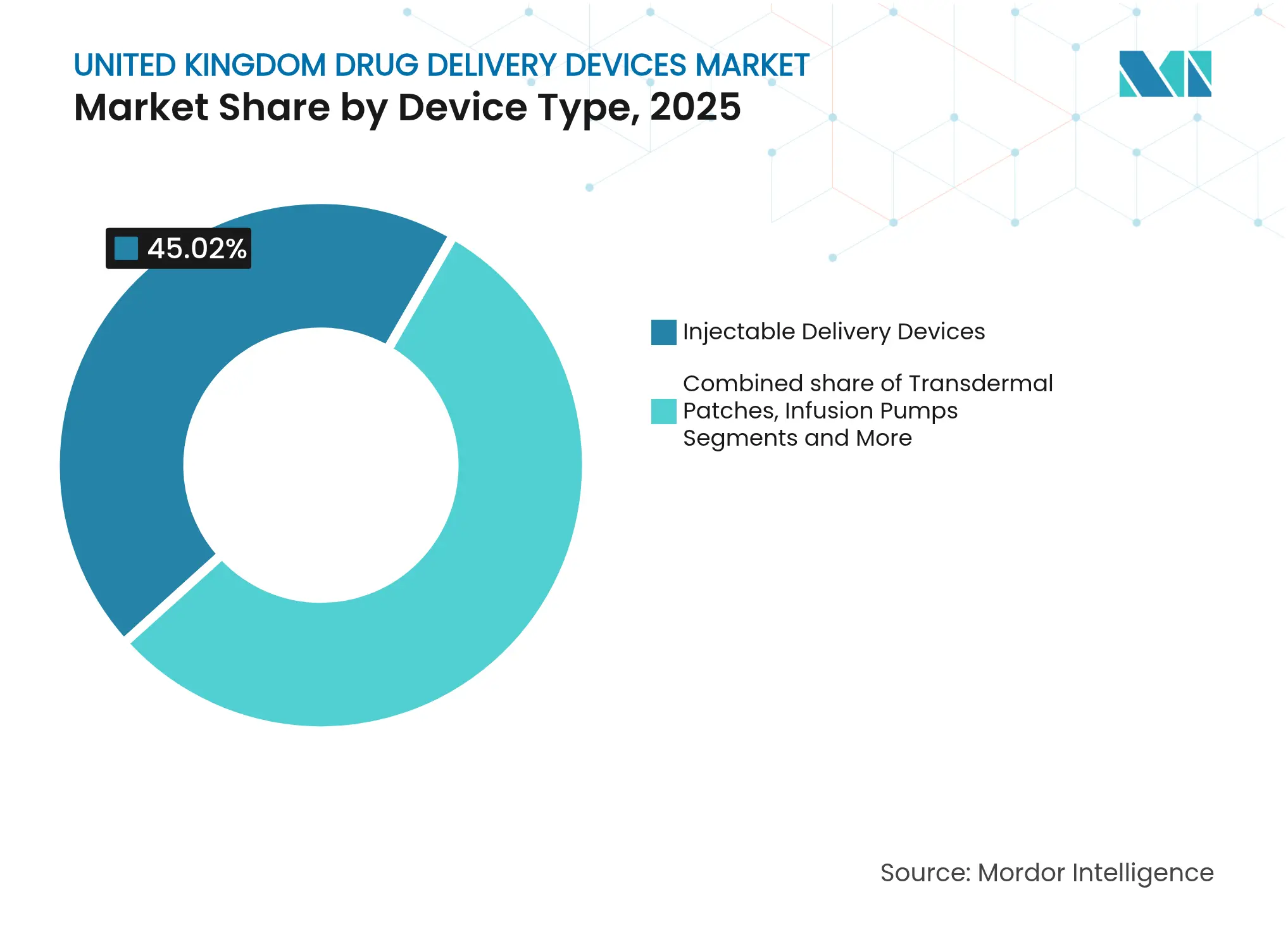

- By device type, injectable devices led with 45.02% of the United Kingdom drug delivery devices market share in 2025; implantable systems are projected to expand at an 10.65% CAGR to 2031.

- By route of administration, injectable formats accounted for 51.86% share of the United Kingdom drug delivery devices market size in 2025, while oral mucosal delivery is advancing at a 9.29% CAGR through 2031.

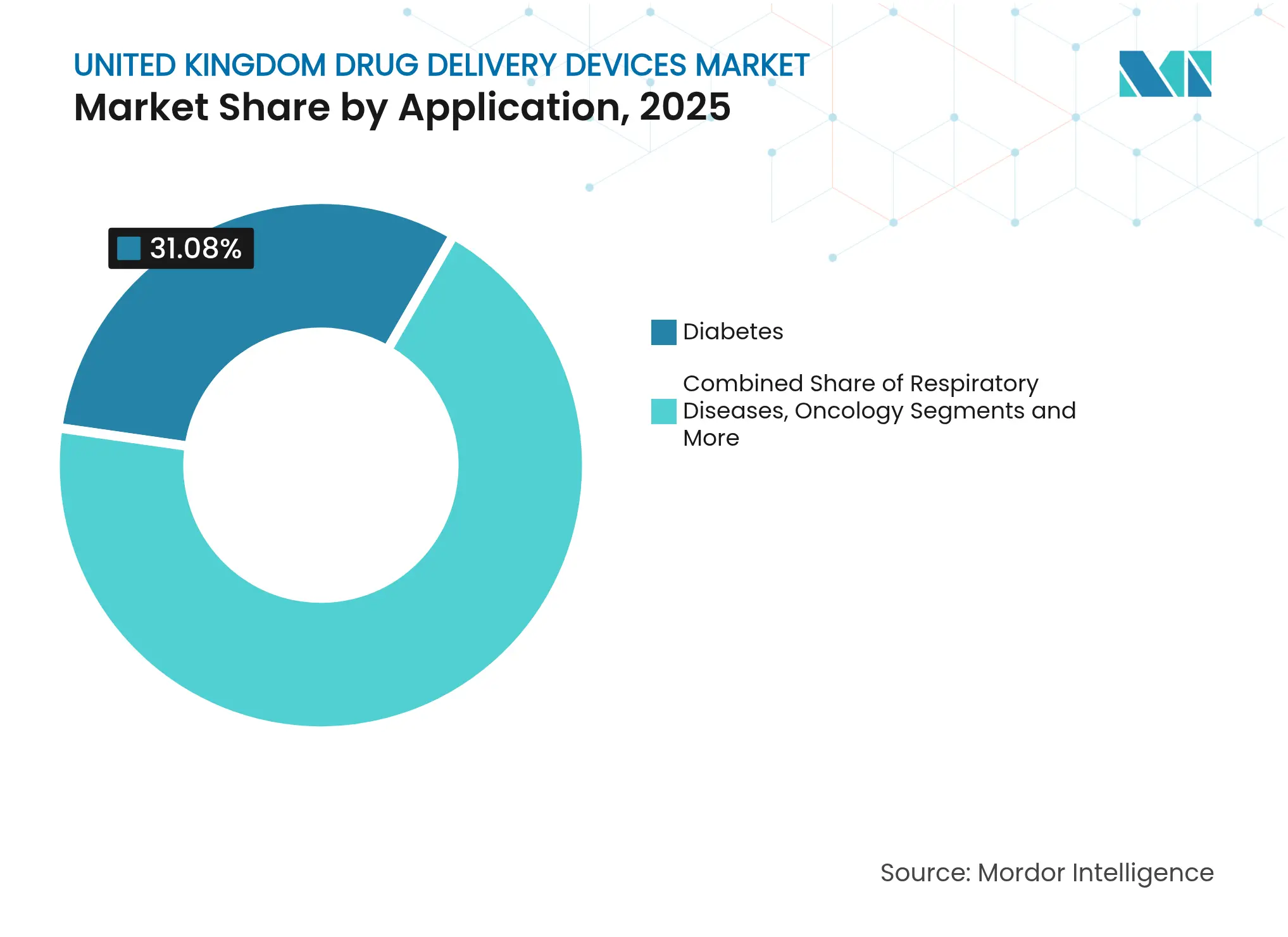

- By application, diabetes management held 31.08% of the United Kingdom drug delivery devices market size in 2025; oncology applications are forecast to grow at a 9.78% CAGR between 2026-2031.

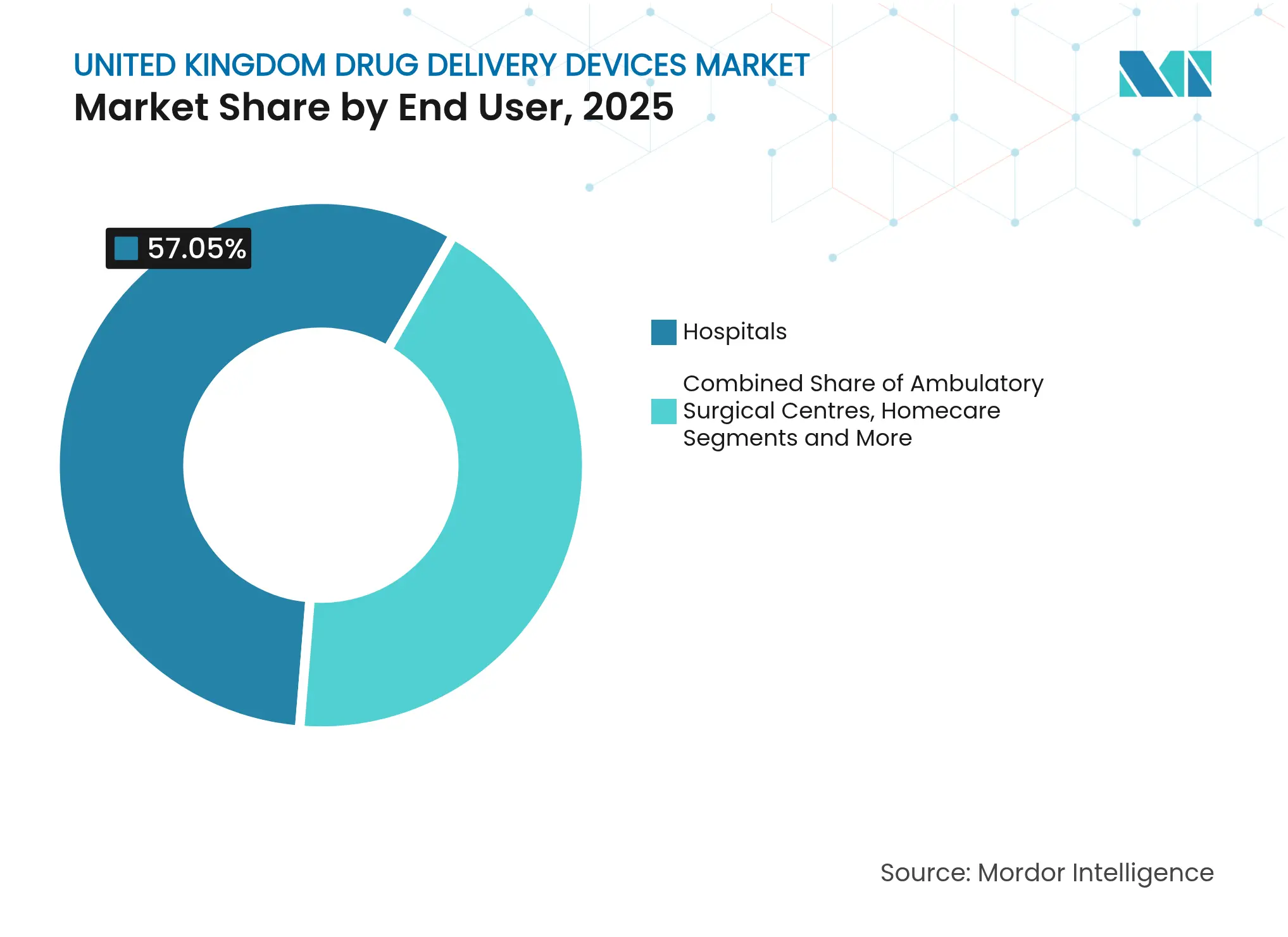

- By end-user, hospitals commanded 57.05% share of the United Kingdom drug delivery devices market size in 2025, whereas homecare settings record the fastest CAGR at 10.07% over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government initiatives for

self-administration & homecare

Government initiatives for

self-administration & homecare

| +2.1% | National, early gains in urban centres | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic Relevance

:

National, early gains in urban

centres

|

Impact Timeline

:

Medium term (2-4 years)

|

Smart connected drug delivery

devices

Smart connected drug delivery

devices

| +1.8% | National, tech hubs | Medium term (2-4 years) | |||

Biologics pipeline growth boosting

advanced injectors

Biologics pipeline growth boosting

advanced injectors

| +1.6% | National | Medium term (2-4 years) | |||

Expanded R&D funding and

academic–industry clusters

Expanded R&D funding and

academic–industry clusters

| +1.3% | National | Long term (≥ 4 years) | |||

Higher chronic disease prevalence

Higher chronic disease prevalence

| +0.9% | National, ageing regions | Long term (≥ 4 years) | |||

Fast-track approvals for combination

products

Fast-track approvals for combination

products

| +0.8% | National | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Government initiatives for self-administration & homecare

An extra GBP 86 million added to the Disabled Facilities Grant in 2025 enables more patients to manage conditions at home, complementing the Pharmacy First scheme that now covers seven minor conditions at almost every community pharmacy.[3]Department of Health and Social Care, “NHS Long Term Plan 2024-2034,” gov.uk The NHS plan to distribute artificial-pancreas technology over five years exemplifies policy-driven demand for intuitive self-use systems. Such measures channel volume into the United Kingdom drug delivery devices market for pen injectors, wearable pumps, and inhalers designed for layperson operation.

Development and adoption of smart connected drug delivery devices

Connected devices are expected to post a doubt digit CAGR in United Kingdom healthcare through 2030 as electronic health-record coverage climbs toward 95% of NHS trusts. Smart inhalers reimbursed under the MedTech Funding Mandate and Bluetooth add-ons like DOSE for insulin pens show how IoT integration addresses non-adherence that leads to 22,000 premature deaths a year. The broad data backbone being built by the Digital Health and Care Plan lets these devices feed real-time dosing data directly into clinical workflows.

Biologics pipeline growth driving advanced injectors demand

Conference agendas and product pipelines confirm high-volume injectable formats as a priority for biologic and biosimilar launches. GSK’s specialty-medicine sales rose 22% in Q2 2024, much of it tied to oncology and HIV therapies that require sophisticated delivery systems. With 85 biologic patents due to expire by 2028, biosimilar competition is intensifying the need for cost-efficient yet user-friendly autoinjectors within the United Kingdom drug delivery devices market.

Increasing R&D investment

A GBP 400 million package for clinical-trial acceleration and a dedicated Intracellular Drug Delivery Centre focused on lipid nanoparticle research highlight the government’s long-term commitment to platform breakthroughs.[4]Association of the British Pharmaceutical Industry, “UK Secures £400 Million Investment,” abpi.org.uk Grants for technologies such as DriDose nasal powders illustrate targeted support for innovators outside big-pharma circles, broadening the innovation base.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Post-Brexit delays and extra cost

Post-Brexit delays and extra cost

| -0.9% | National, international firms | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.9%

|

Geographic Relevance

:

National, international firms

|

Impact Timeline

:

Short term (≤ 2 years)

|

High development cost & limited

clean-room capacity

High development cost & limited

clean-room capacity

| -0.7% | National | Medium term (2-4 years) | |||

NHS pricing and rebate pressure

NHS pricing and rebate pressure

| -0.5% | National, therapy-specific | Medium term (2-4 years) | |||

Device-specific safety concerns

Device-specific safety concerns

| -0.3% | National | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent fragmented regulatory landscape coupled with post-Brexit challenges

Manufacturers must maintain both CE and UKCA certification until 2030, and the post-market-surveillance rules effective June 2025 widen the definition of a serious incident. Non-UK suppliers must appoint a Responsible Person, adding cost and complexity, although expansion of approved bodies and an International Reliance route offer partial relief.

High development and manufacturing cost

Software-heavy connected devices raise spending beyond traditional hardware budgets, and the United Kingdom lacks abundant GMP-grade clean-room capacity. The NHS spends GBP 3.8 billion a year on aseptically produced injectables, prompting proposals for regional hub facilities to ease bottlenecks. Targeted grants, such as GBP 33 million for greener inhaler production, help but do not fully offset the capital burden for smaller firms.

Segment Analysis

By Device Type: Injectable dominance with implantable acceleration

Injectable formats held 45.02% of the United Kingdom drug delivery devices market share in 2025. The prevalence of biologics and patient preference for self-injection explain this lead. Integration of sensors and wireless modules is turning prefilled pens into data-rich adherence tools. Over 2026-2031, implantable systems will post the fastest 10.65% CAGR as research centers such as OxCD3 advance ultrasound-triggered depots that release drugs over months.

The inhalation segment benefits from NHS decarbonisation targets, steering procurement toward pMDIs with near-zero GWP propellants. Transdermal patches are expanding as microneedle arrays improve permeability without needles. Nasal and ocular devices remain niche but attract specialised R&D funding, reflecting an overall diversification of the United Kingdom drug delivery devices market.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Parenteral scale meets oral-mucosal speed

Injectables delivered 51.86% of revenue in 2025 and leverage NHS investment of GBP 204 million into modern aseptic hubs that raise throughput for large-volume syringes. Oral mucosal systems, however, are gaining ground with a 9.29% forecast CAGR thanks to muco-adhesive films that avoid first-pass metabolism and reach peak plasma levels within minutes.

The inhalation route benefits from sustainability mandates, while transdermal patches ride patient demand for painless options. Nasal administration promises direct brain delivery for neurological disorders, a white-space opportunity within the United Kingdom drug delivery devices market that could reshape therapy for Alzheimer’s and Parkinson’s. Ocular implants are moving from monthly injections to semestral inserts, easing clinic workload and improving adherence.

By Application: Diabetes Holds Sway while Oncology Accelerates

Diabetes accounted for 31.08% of sales in 2025, helped by nationwide rollout of hybrid closed-loop insulin systems that cut HbA1c within months and now qualify for NHS reimbursement under NICE TA943. Oncology shows the quickest climb, tracking a 9.78% CAGR to 2031 as stimulus-responsive nanocarriers move from Oxford laboratories to phase-I trials gtr.ukri.org. Respiratory care keeps volume high; greener pMDIs answer NHS carbon rules while protecting asthma control. Cardiovascular, infectious-disease and neurology niches gain from wearable pumps, thermostable nasal vaccines and nose-to-brain sprays that ease hospital load yet broaden treatment reach.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Hospitals Rule, Homecare Rises Fast

Hospitals still handle 57.05% of device spend thanks to sterile facilities and near-universal electronic health records that now pull dosing data straight from smart injectors, trimming prescription turnaround from days to hours in early pilots. Homecare is the fastest mover at 10.07% CAGR, powered by an extra GBP 86 million for Disabled Facilities Grants and pharmacy-led schemes that shift routine care into living rooms. Ambulatory centres and virtual wards add momentum by sending patients home with on-body infusors and Bluetooth patches, freeing beds without compromising clinical oversight.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

London and the Southeast anchor the United Kingdom drug delivery devices market with their cluster of teaching hospitals, contract manufacturers, and venture capital. Implementation of e-signature platforms at University Hospitals of Leicester cut prescription processing time from two days to two hours and saved GBP 95,324 annually, underscoring the operational gains from digital adoption.

Scotland’s homecare population has risen nearly 50% since 2018 to exceed 41,000 patients, leading regulators to propose clearer governance for medicines delivered outside hospital walls. Wales follows NHS England’s artificial-pancreas rollout, ensuring nationwide consistency in advanced diabetes care.

Northern Ireland operates under the Windsor Framework, easing cross-border supply with Ireland but adding compliance layers for goods shipped from Great Britain. About 28% of device makers report additional paperwork, which marginally slows their participation in the United Kingdom drug delivery devices market. Region-specific digital maturity levels will determine how evenly connected devices are deployed by 2030.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Large pharmaceutical companies, mid-tier device specialists, and start-ups coexist in a moderately fragmented setting. AstraZeneca, CamDiab, and Ypsomed are collaborating on an automated insulin delivery ecosystem that couples continuous glucose monitoring, algorithm-driven dosing, and a tubeless pump to serve United Kingdom users. Such partnerships combine drug, device, and data expertise that single firms seldom hold internally.

Sustainability distinguishes market leaders. AstraZeneca’s shift to near-zero GWP propellants aims to cut pMDI carbon impact by 90% while safeguarding asthma control, aligning environmental and clinical goals. The Sustainable Markets Initiative’s Health Systems Task Force extends this focus across the supply chain.

White-space opportunities lie in CNS disorders where nasal and intrathecal routes remain under-served. Artificial-intelligence-guided dosing and predictive maintenance of connected pumps also open service-revenue streams. Firms that can clear evolving UKCA documentation while proving patient-centric value are best placed to secure long-term contracts within the United Kingdom drug delivery devices market.

United Kingdom Drug Delivery Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Department of Health and Social Care issued a medicines supply notification for Reletrans buprenorphine patches, with stock expected back in July 2025.

- March 2025: Scottish Government published the Independent Review of Medicines Homecare, calling for clearer governance of a service now serving over 41,000 patients

- March 2025: MHRA outlined a new framework for decentralised manufacture, effective July 23 2025, which will benefit advanced-therapy delivery.

- September 2024: NHS England confirmed nationwide rollout of artificial-pancreas systems for type 1 diabetes over five years, backed by GBP 2.5 million.

Table of Contents for United Kingdom Drug Delivery Devices Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Government Initiatives and Trends for Self-Administration & Homecare

- 4.2.2Development and Adoption Smart Connected Drug Delivery Devices

- 4.2.3Increasing Research and Development Initiatives and Support from Government

- 4.2.4Biologics Pipeline Growth Driving Advanced Injectors Demand

- 4.2.5Rising Prevalence and Incidence of Chronic and Infectious Diseases

- 4.2.6Fast-Track Approvals for Combination Products Post-Brexit

- 4.3Market Restraints

- 4.3.1Post Brexit Challenges Related to Delays and Cost

- 4.3.2High Development and Manufacturing Cost Coupled with Limited Domestic Clean-Room Manufacturing Capacity

- 4.3.3Risk and Concerns Associatied with Different Devices

- 4.3.4NHS Pricing and Rebate Pressure

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory and Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Bargaining Power of Suppliers

- 4.6.2Bargaining Power of Buyers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Device Type

- 5.1.1Injectable Delivery Devices

- 5.1.2Inhalation Delivery Devices

- 5.1.3Infusion Pumps

- 5.1.4Transdermal Patches

- 5.1.5Implantable Drug Delivery Systems

- 5.1.6Ocular Inserts & Delivery Implants

- 5.1.7Nasal & Buccal Delivery Devices

- 5.2By Route of Administration

- 5.2.1Injectable

- 5.2.2Inhalation

- 5.2.3Transdermal

- 5.2.4Oral Mucosal (Buccal & Sublingual)

- 5.2.5Ocular

- 5.2.6Nasal

- 5.3By Application

- 5.3.1Diabetes

- 5.3.2Respiratory Diseases

- 5.3.3Oncology

- 5.3.4Cardiovascular Diseases

- 5.3.5Infectious Diseases

- 5.3.6Neurological Disorders

- 5.3.7Others

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.2Ambulatory Surgical Centres

- 5.4.3Homecare Settings

- 5.4.4Speciality Clinics

- 5.4.5Others

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Pfizer Inc.

- 6.4.2AstraZeneca plc

- 6.4.3GlaxoSmithKline plc

- 6.4.4Novartis AG

- 6.4.5F. Hoffmann-La Roche Ltd

- 6.4.6Solventum

- 6.4.7Becton, Dickinson and Company

- 6.4.8Baxter International Inc.

- 6.4.9Ypsomed AG

- 6.4.10Nemera

- 6.4.11Gerresheimer AG

- 6.4.12AptarGroup Inc.

- 6.4.13Owen Mumford Ltd.

- 6.4.14Teva Pharmaceutical Industries Ltd.

- 6.4.15West Pharmaceutical Services Inc.

- 6.4.16SHL Medical

- 6.4.17ICU Medical

- 6.4.18Terumo Corporation

- 6.4.19Insulet Corporation

- 6.4.20Tandem Diabetes Care, Inc.

7. Market Opportunities and Future Outlook

- 7.1White-Space and Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis defines the United Kingdom drug-delivery devices market as the aggregated value of finished, patient-facing devices that actively meter or release a human pharmaceutical, whether single-use or reusable, across parenteral, pulmonary, transdermal, implantable, ocular, nasal, buccal, and oral-mucosal routes. Devices that are software-enabled or paired with adherence sensors are counted only where a physical delivery mechanism is present.

Scope Exclusion: Animal-health delivery devices and pure contract manufacturing services are kept outside the study.

Segmentation Overview

- By Device Type

- Injectable Delivery Devices

- Inhalation Delivery Devices

- Infusion Pumps

- Transdermal Patches

- Implantable Drug Delivery Systems

- Ocular Inserts & Delivery Implants

- Nasal & Buccal Delivery Devices

- Injectable Delivery Devices

- By Route of Administration

- Injectable

- Inhalation

- Transdermal

- Oral Mucosal (Buccal & Sublingual)

- Ocular

- Nasal

- Injectable

- By Application

- Diabetes

- Respiratory Diseases

- Oncology

- Cardiovascular Diseases

- Infectious Diseases

- Neurological Disorders

- Others

- Diabetes

- By End-User

- Hospitals

- Ambulatory Surgical Centres

- Homecare Settings

- Speciality Clinics

- Others

- Hospitals

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview respiratory physicians, diabetes educators, home-care nurses, and device R&D engineers across England, Scotland, and Wales. These discussions surface in-field penetration rates, emerging price points, and real-world adherence hurdles, allowing us to challenge desktop assumptions and fine-tune growth levers.

Desk Research

We capture foundational signals from open-access authorities such as NHS Digital hospital episode statistics, Medicines and Healthcare Products Regulatory Agency device registries, Office for National Statistics trade data, and scientific literature on device adoption trends in chronic diseases. Company 10-Ks, investor decks, and procurement frameworks released by NHS Supply Chain complement these inputs, while D&B Hoovers and Dow Jones Factiva provide paywalled financial snapshots that sharpen revenue splits. Other public and subscription sources were consulted; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down build begins with import-export data and domestic production disclosures, which are then adjusted for hospital procurement share and home-care uptake. Select bottom-up checks, sampled average selling price multiplied by unit flow for auto-injectors, smart inhalers, and infusion pumps, help calibrate totals. Key variables include diagnosed diabetes prevalence, asthma and COPD prescription volumes, innovation-driven device ASP shifts, MHRA approval counts, and the share of self-administration within primary-care pathways. Multivariate regression, allied to scenario analysis around reimbursement reform, produces the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs face variance screening versus historical spending, clinician utilization surveys, and currency-converted trade values. Senior analysts review anomalies before sign-off. The dataset refreshes annually, with expedited updates if major regulatory or pricing events emerge.

Why Mordor's United Kingdom Drug Delivery Devices Baseline Earns UK Stakeholder Trust

Benchmark comparison

Published figures often diverge because firms choose different device lists, pricing anchors, and refresh speeds.

Key gap drivers include broader scopes that bundle consumables, global-to-country scaling without local clinical inputs, or reliance on headline company revenues. Mordor's disciplined device taxonomy, primary-validated unit counts, and yearly model rebuild narrow such gaps and provide a defensible baseline for planners.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 8.92 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 30.20 B (2024) | Regional Consultancy A | Includes packaging and connected add-ons, minimal bottom-up validation | ||

USD 15.20 B (2024) | Global Consultancy B | Applies global per-capita ratios, lacks UK-specific primary checks | ||

USD 3.80 B (2024) | Trade Journal C | Draws from listed company revenue only, omits hospital infusion devices |