Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

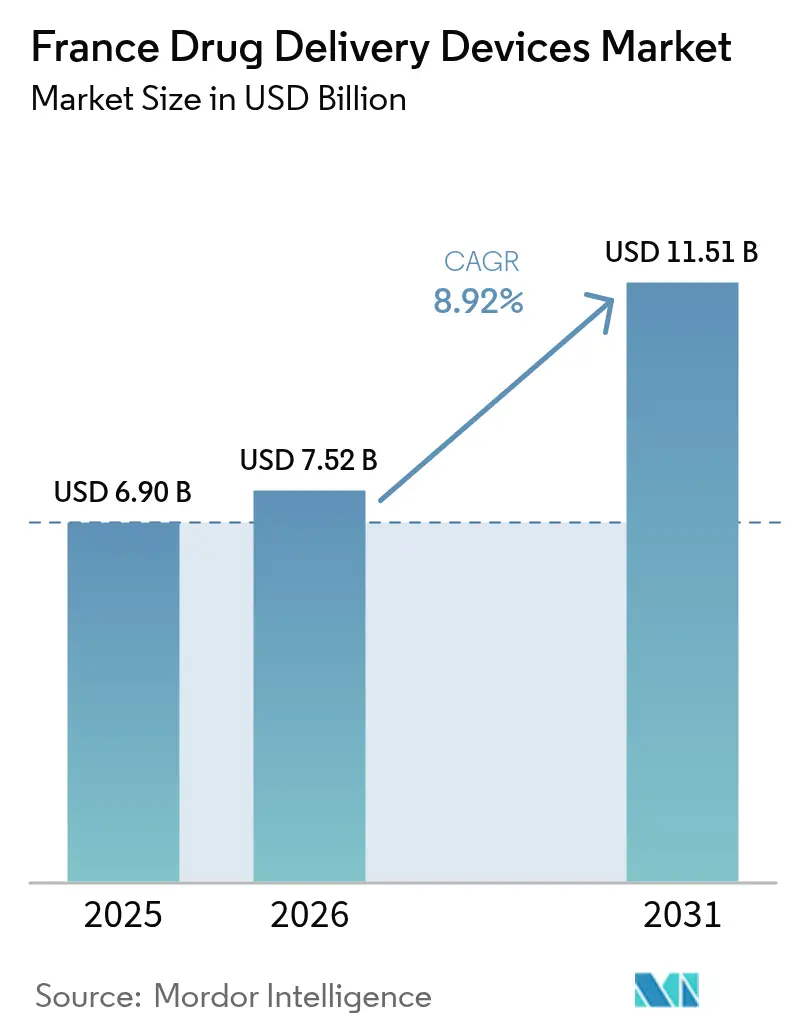

| Base Year Market Size (2025) | USD 6.90 Billion |

| Market Size (2026) | USD 7.52 Billion |

| Market Size (2031) | USD 11.51 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Drug Delivery Devices Market Analysis by Mordor Intelligence

The France drug delivery devices market size was valued at USD 6.90 billion in 2025 and estimated to grow from USD 7.52 billion in 2026 to reach USD 11.51 billion by 2031, at a CAGR of 8.92% during the forecast period (2026-2031). Rapid expansion is fueled by connected-device innovation, growth in biologic and biosimilar therapies, and national e-health programs that encourage self-administration. Manufacturers gain momentum from France’s robust contract development and manufacturing organization (CDMO) ecosystem, while high chronic-disease prevalence sustains steady demand. Regulatory initiatives such as early reimbursement pathways for digital devices shorten time to market, although complex pricing caps and EU Medical Device Regulation (MDR) compliance remain notable obstacles. Together, these factors position the France drug delivery devices market as a key growth engine within Europe.

Key Report Takeaways

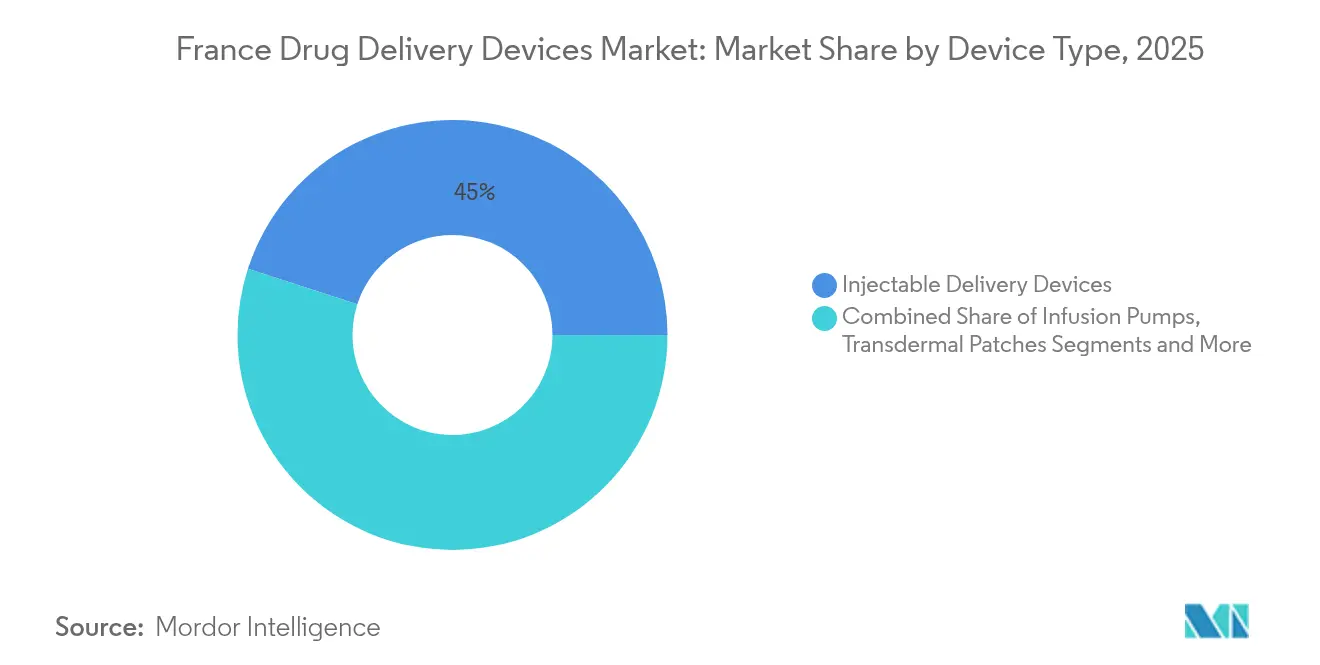

- By device type, injectable delivery devices led with 45.02% of France drug delivery devices market share in 2025, while implantable systems are forecast to expand at a 11.32% CAGR through 2031.

- By route of administration, injectables commanded 57.55% share of the France drug delivery devices market size in 2025; inhalation delivery is set to grow at a 9.24% CAGR to 2031.

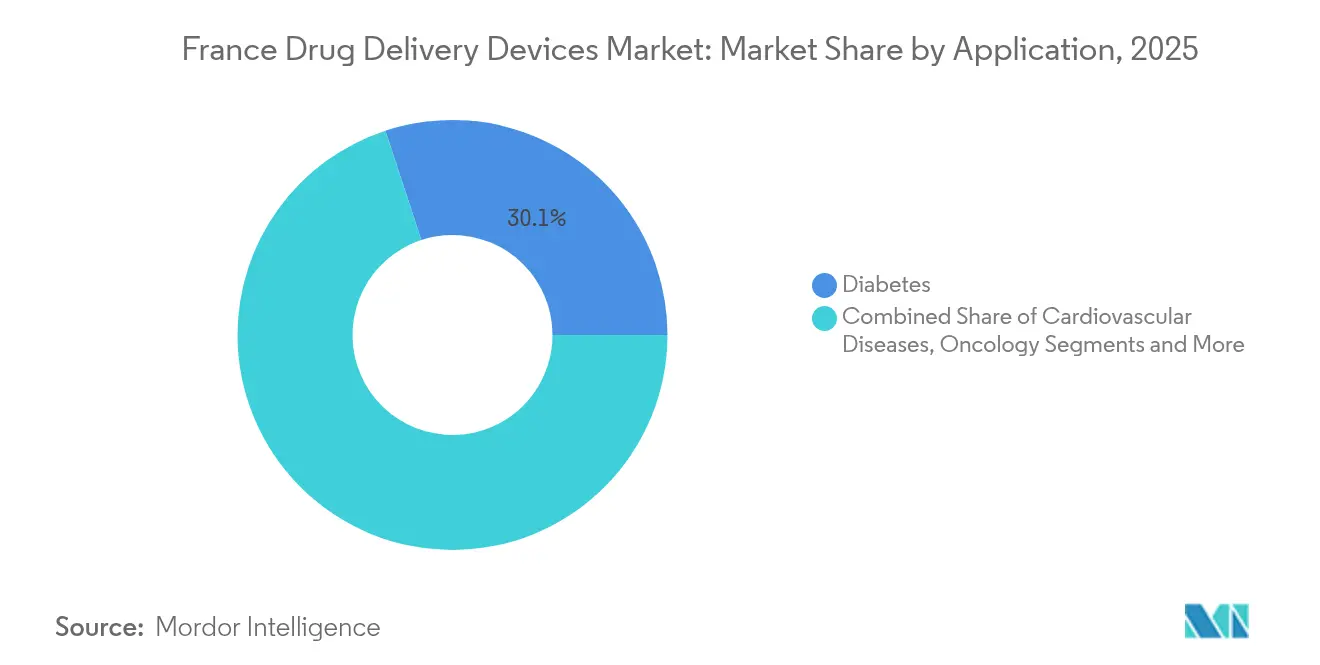

- By application, diabetes represented 30.05% of France drug delivery devices market share in 2025, whereas oncology applications are advancing at a 10.85% CAGR between 2026-2031.

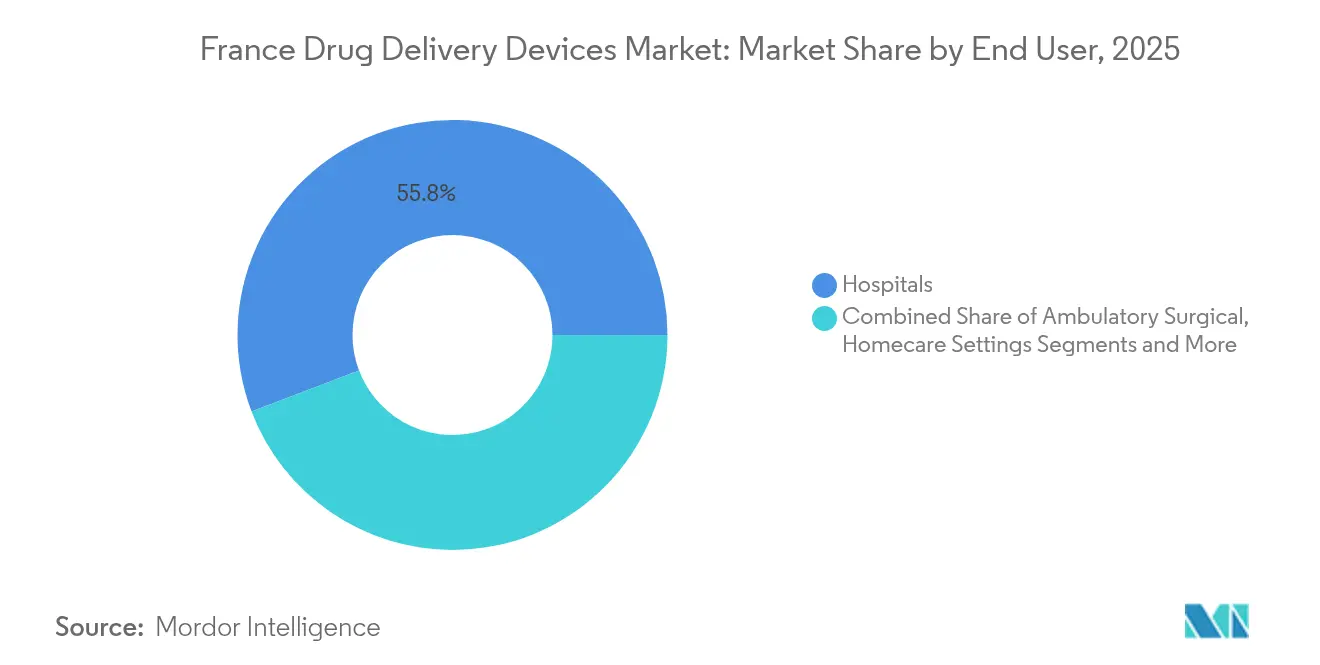

- By end user, hospitals accounted for 55.78% of the France drug delivery devices market size in 2025; homecare settings are progressing at a 12.37% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to home-based care & self-administration | +2.1% | National, early adoption in urban centers | Medium term (2-4 years) |

| Expansion of biologic & biosimilar injectables | +1.8% | National | Long term (≥ 4 years) |

| Technological advancements & e-health strategy accelerating connected devices | +1.5% | National, concentration in innovation hubs | Medium term (2-4 years) |

| Robust CDMO & device manufacturing ecosystem | +1.2% | Paris, Lyon, Strasbourg clusters | Medium term (2-4 years) |

| High burden of chronic diseases | +0.9% | National, stronger impact in aging regions | Long term (≥ 4 years) |

| Supporting reforms and regulations fueling demand for drug-delivery devices | +0.7% | National, aligned with EU frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Home-Based Care & Self-Administration

France is prioritizing homecare, and the end-user segment already shows a 13.03% CAGR, the highest across settings. The National eHealth Roadmap (2023-2027) backs connected devices that transmit real-time dosing data and support remote consultations.[1]Ministère des Solidarités et de la Santé, “France Digital Health Roadmap 2023-2027,” gnius.esante.gouv.frSanofi’s Solosmart sensor, available in 21,000 pharmacies, captures insulin injection records and integrates seamlessly with patient apps. Such devices redefine competition by elevating usability and data connectivity to the same level as pharmacological performance, driving France drug delivery devices market adoption.

Expansion of Biologic & Biosimilar Injectables

High-viscosity biologics need specialized delivery formats. Novo Nordisk invested €2.1 billion in its Chartres site to double insulin capacity. BD’s Neopak XtraFlow syringe targets these formulations, highlighting collaborative innovation between pharma and device makers. Growing biologic pipelines ensure sustained demand in the France drug delivery devices market, particularly for self-injectors and wearable pumps.

Technological Advancements and e-Health Strategy

The ‘Mon espace santé’ digital record positions France as an early adopter of connected drug delivery. Integration with the European Health Data Space promises smoother secondary-data use for research. Manufacturers gain a platform to demonstrate adherence gains, strengthening value-based reimbursement arguments and lifting the France drug delivery devices market outlook.

Robust CDMO & Device Manufacturing Ecosystem

France’s network of specialized CDMOs accelerates scale-up for complex systems. Meribel Pharma Solutions’ April 2025 launch added ten manufacturing sites, widening capacity for advanced injectables and implants. Concentrated know-how in Île-de-France, Lyon, and Strasbourg cuts development timelines, giving the France drug delivery devices market a competitive edge in Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex reimbursement price caps | -1.3% | National | Medium term (2-4 years) |

| Stringent regulatory framework | -0.8% | National, EU-wide implications | Short term (≤ 2 years) |

| Issues related to fragmented hospital tendering & generics affecting price of drug-device combinations | -0.6% | National, regional variations | Medium term (2-4 years) |

| Limitations associated with different devices and risks | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Reimbursement Price Caps

France differentiates device and service payments and caps distributor margins, extending the average approval-to-reimbursement period to 12.9 months, compared with 6 months in Switzerland and 7.4 months in Germany. The SMR/ASMR scoring method can exclude low-benefit products from coverage, slowing revenue for combination devices and tempering growth within the France drug delivery devices market.

Stringent Regulatory Framework

Adapting to EU MDR raises compliance costs, particularly for combination and connected devices. Temporary measures by ANSM to prevent shortages of critical delivery cannulas illustrate transitional pressure.[2]ANSM, “French National Agency for the Safety of Medicines and Health Products,” gnius.esante.gouv.fr Additional substance-use guidelines (e.g., phthalates) elevate documentation workloads, challenging smaller innovators and moderating the France drug delivery devices industry expansion pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Implantables Gain Ground

Injectables retained 45.02% share in 2025, supported by steady biologic usage and continuous upgrades in prefilled syringes and autoinjectors. BD’s RFID-enabled iDFill syringe shown at Pharmapack 2025 underscores a focus on traceability and patient safety. Despite this lead, implantables are forecast to rise at 11.32% CAGR to 2031, reflecting patient preference for longer dosing intervals and emerging hydrogel reservoirs that stretch semaglutide dosing to monthly schedules. This momentum positions implantables as a disruptive force inside the France drug delivery devices market.

Transdermal patches, ocular inserts, and intranasal systems broaden therapeutic choices. The nasal route, highlighted by Pfizer’s approved Zavzpret spray for migraine, demonstrates expanding utility beyond respiratory therapy. These additive modalities bolster device diversity and reinforce overall resilience of the France drug delivery devices market.

By Route of Administration: Inhalation Pathways Rise

Injectables accounted for 57.55% of France drug delivery devices market size in 2025, favored for precision dosing across chronic illnesses. Continuous needle-design refinements improve user comfort, strengthening retention in both hospital and home settings.

Inhalation is slated for 9.24% CAGR between 2026-2031. Partnerships such as Chiesi-Affibody on inhaled biologics widen respiratory portfolios. Nasal delivery gains traction for central nervous system targets; French start-up Lovaltech advances an intranasal vaccine platform under France 2030 funding. These advances expand treatment horizons and feed sustained growth within the France drug delivery devices market.

By Application: Oncology Accelerates

Diabetes held 30.05% of France drug delivery devices market share in 2025, underpinned by Novo Nordisk’s Chartres capacity expansion. Cardiovascular care remains sizable, aided by France’s ongoing push to lower morbidity.

Oncology is forecast to climb at a 10.85% CAGR through 2031 as precise, often implantable, delivery technologies support targeted therapeutics. Nanoparticle carriers that breach the blood-brain barrier exemplify device innovation aimed at difficult cancers. This surge solidifies oncology as a pivotal growth pillar in the France drug delivery devices market.

By End User: Homecare Surges

Hospitals dominated usage with 55.78% of France drug delivery devices market size in 2025, reflecting their central role in initiating complex therapies. Ambulatory clinics also show strength as day-surgery volumes rise.

Homecare/self-use is growing at 12.37% CAGR, buoyed by connected wearables such as the BD Libertas on-body injector that administers large-volume biologics outside clinical walls. National digital-health infrastructure ensures data integration, reinforcing adherence monitoring. Collectively, these shifts advance decentralization across the France drug delivery devices market.

Geography Analysis

France benefits from a dense life-sciences corridor. Paris ranks as Europe’s second-strongest site for drug manufacturing and packaging, concentrating design, testing, and logistics talent. The France drug delivery devices market thus enjoys proximity between research institutes, hospitals, and CDMOs that shorten innovation cycles. Pharmaceutical output reached €32,773 million (USD 35,722.6 million) in 2023, and R&D spend totaled €4,451 million (USD 4,851.6 million).

Regional disease burdens shape uptake. Higher heart-failure incidence in deprived areas mandates accessible self-administration tools. The National eHealth Roadmap aims to equalize access nationwide through digital prescriptions and remote monitoring gnius.esante.gouv.fr. Lyon’s new microbiome therapy facility signals geographic diversification and supports high-value manufacturing outside Île-de-France.

Integration with EU frameworks further influences trajectories. The European Health Data Space harmonizes governance, facilitating cross-border evidence from connected devices. Nevertheless, France’s longer reimbursement timelines versus neighboring states temper immediate returns. Sustained EU digital-health funding of EUR 13.6 billion for 2021-2027 provides ongoing support for technology adoption, reinforcing the long-term outlook for the France drug delivery devices market.

Competitive Landscape

Competition is moderate. Global leaders such as Sanofi, BD, and Novo Nordisk secure share through continual device upgrades and sizable capital commitments. Sanofi’s Solosmart sensor exemplifies convergence of drug and data. Novo Nordisk’s expansion cements domestic insulin leadership.

Specialists like Nemera and Aptar focus on niche technologies. Aptar’s metal-free multidose nasal pump, showcased at Pharmapack, addresses sustainability goals. Emerging firms leverage France’s CDMO base; Meribel Pharma Solutions supplies end-to-end services for complex formulations, enhancing agility for mid-sized projects.

Strategy shifts from hardware alone to integrated platforms pairing devices with analytics dashboards and adherence support. This evolution differentiates suppliers and fuels service-based revenue streams, maintaining competitive dynamism in the France drug delivery devices industry.

France Drug Delivery Devices Industry Leaders

Becton, Dickinson and Company

Sanofi

F. Hoffmann-La Roche AG

Novo Nordisk A/S

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Meribel Pharma Solutions launched with ten manufacturing and three development sites across France, Spain, and Sweden, targeting mid-sized, complex drug-delivery projects

- January 2025: BD displayed RFID-enabled prefilled syringes, high-viscosity solutions, and wearable injectors at Pharmapack 2025 in Paris

- March 2024: AdhexPharma opened a state-of-the-art patch and oral-film facility in Chenôve, France

- January 2024: Lemer Pax partnered with ICU Medical to distribute Plum 360™ infusion pumps in France’s nuclear-medicine segment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines France's drug delivery devices market as the annual revenue, expressed in constant 2024 USD, generated by finished devices that actively meter or facilitate the administration of therapeutic agents through injectable, inhalation, transdermal, oral-mucosal, ocular, nasal, or implantable routes within French borders.

Scope Exclusions: We do not count bulk drug substances, passive packaging, contract manufacturing services, or purely diagnostic equipment.

Segmentation Overview

- By Device Type

- Injectable Delivery Devices

- Inhalation Delivery Devices

- Infusion Pumps

- Transdermal Patches

- Implantable Drug Delivery Systems

- Ocular Inserts & Delivery Implants

- Nasal & Buccal Delivery Devices

- By Route of Administration

- Injectable

- Inhalation

- Transdermal

- Oral Mucosal (Buccal & Sublingual)

- Ocular

- Nasal

- By Application

- Diabetes

- Oncology

- Cardiovascular Diseases

- Respiratory Diseases

- Infectious Diseases

- Auto-Immune & Inflammatory Disorders

- CNS Disorders

- By End User

- Hospitals

- Ambulatory Surgical & Specialty Clinics

- Homecare Settings / Self-Use

- Retail & Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Interviews with respiratory therapists, endocrinologists, biomedical engineers, procurement managers, and home-care nurses across Île-de-France, Auvergne-Rhône-Alpes, and Nouvelle-Aquitaine clarified therapy shifts, device lifecycles, and price corridors before findings were folded back into the model.

Desk Research

We reviewed open datasets from the French Ministry of Health, Eurostat medical-technology trade files, and ANSM device registration logs to establish production, import, and installed-base trends. Clinical society registries that track insulin-dependent diabetes, COPD, and oncology prevalence offered patient pools, while Questel patent alerts signaled forthcoming launches. Company filings, hospital tender bulletins, and Dow Jones Factiva news helped fine-tune average selling prices and competitive shifts. These sources are illustrative; many additional references informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction that sums domestic production and net imports set the baseline. Then, sampled supplier roll-ups and channel checks tested the totals. Key variables like diabetic population growth, biologic prescription share, median pen-injector ASP drift, hospital tender frequency, and home-use penetration drive a multivariate regression that projects demand to 2030. Scenario analysis adjusts for regulatory delays or accelerated uptake of connected injectors. When unit data were sparse, ratios derived from expert insight bridged gaps.

Data Validation & Update Cycle

We run variance scans against independent indicators, escalate anomalies for analyst review, and update every twelve months, with interim refreshes triggered by major reimbursement, recall, or merger events.

Why Mordor's France Drug Delivery Devices Baseline Commands Reliability

Published estimates often differ because firms vary device lists, currency assumptions, and update cadence. Mordor analysts confine scope to therapeutic delivery hardware sold in France, apply one constant currency base, and refresh models annually, yielding a balanced baseline that decision-makers can trace to transparent drivers.

Key Gap Drivers: Other publishers may fold in passive disposables, rely solely on hospital prices, or freeze exchange rates at report release, whereas we validate prices across channels, layer in prevalence-based demand signals, and reconfirm inputs before publication.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.90 B (2025) | Mordor Intelligence | |

| USD 18.52 B (2024) | Global Consultancy A | Includes passive disposables and rolls retail prices into totals |

| USD 2.20 B (2024) | Industry Association B | Excludes implantables and counts hospital channel only |

These contrasts show that by selecting the right scope, validating multichannel prices, and refreshing data on a disciplined cycle, Mordor Intelligence delivers the dependable midpoint clients need for confident planning.

Key Questions Answered in the Report

What is the current value of the France drug delivery devices market?

The France drug delivery devices market size is USD 7.52 billion in 2026.

Which device type is growing fastest in France?

Implantable drug delivery systems show the highest growth, with a 11.32% CAGR forecast to 2031.

Why are homecare settings important for drug delivery in France?

Homecare is expanding at 12.37% CAGR as connected devices enable self-administration and align with national e-health goals

How do reimbursement timelines in France compare with other European countries?

France averages 12.9 months from approval to reimbursement, longer than Switzerland’s 6 months and Germany’s 7.4 months.

What role do CDMOs play in the French market?

An extensive CDMO network, exemplified by Meribel Pharma Solutions, accelerates development and manufacturing of complex delivery systems.

Which therapeutic area is expected to drive future growth?

Oncology applications are projected to advance at a 10.85% CAGR due to demand for targeted drug delivery.

Page last updated on: