Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

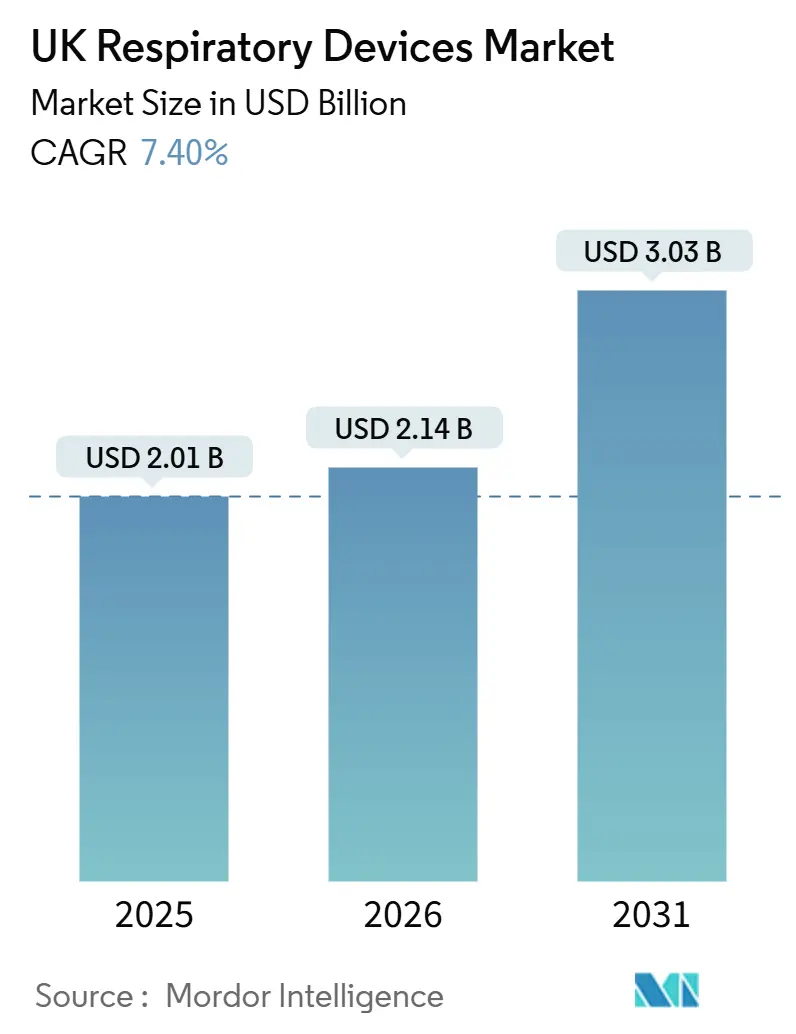

| Base Year Market Size (2025) | USD 2.01 Billion |

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

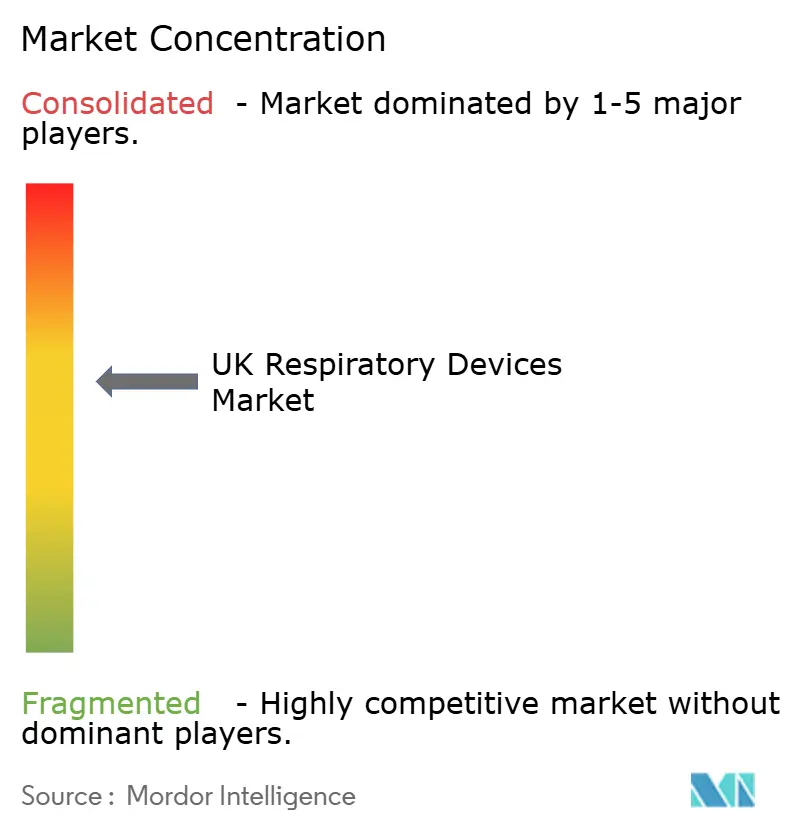

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Respiratory Devices Market Analysis by Mordor Intelligence

The UK Respiratory Devices Market size is projected to be USD 2.01 billion in 2025, USD 2.14 billion in 2026, and reach USD 3.03 billion by 2031, growing at a CAGR of 7.40% from 2026 to 2031.

Pent-up post-pandemic demand, broader telehealth coverage, and the National Health Service’s (NHS) push to cut avoidable admissions underpin this growth trajectory. Uptake of cloud-connected diagnostic tools rose sharply after 2024 when integrated care systems began sharing spirometry and oximetry data with general-practice records, accelerating time-to-treatment in chronic obstructive pulmonary disease (COPD) and sleep apnea. Segment momentum is strongest in single-use disposables because hospital infection-control committees now favor masks and breathing circuits designed for one-time application. At the same time, sustainability rules that phase out high-propellant metered-dose inhalers (MDIs) channel capital toward dry-powder and next-generation propellant platforms, fortifying long-term demand for device–drug combinations.

Key Report Takeaways

- By device type, therapeutic devices led with 58.10% of the UK respiratory devices market share in 2025, and disposables are advancing at an 8.80% CAGR, the fastest pace within the device type category.

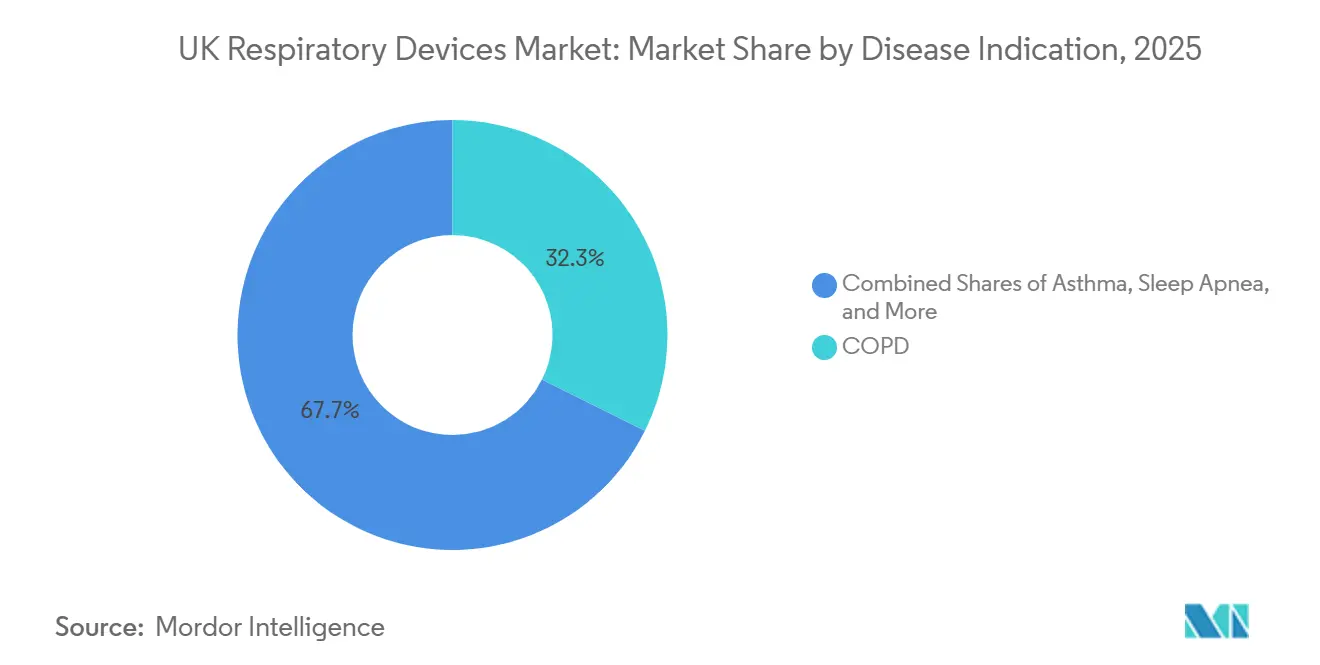

- By disease, COPD accounted for 32.34% of demand in 2025, while sleep-apnea solutions are expanding 10.11% through 2031.

- By age, the pediatric segment is forecast to grow 10.90% through 2031, and adults accounted for 69.80% of demand in 2025.

- By end user, hospitals and clinics accounted for 60.04% of revenue in 2025; however, home health settings are growing at 10.40% per year as virtual ward strategies gain traction.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UK Respiratory Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of COPD, asthma & sleep apnea | +1.8% | National, concentrated in urban centers and post-industrial regions | Long term (≥ 4 years) |

| Ageing population & co-morbidities | +1.5% | National, acute in Scotland and Wales | Long term (≥ 4 years) |

| Technological advances & home-care shift | +2.2% | National, early gains in Greater London, Manchester, Birmingham | Medium term (2-4 years) |

| NHS low-carbon-inhaler initiative | +0.9% | National, Wales leading adoption | Short term (≤ 2 years) |

| AI-enabled diagnostics in UK primary care | +0.7% | National, pilot rollouts in integrated care systems | Medium term (2-4 years) |

| Decentralised clinical-trial adoption of connected spirometry | +0.3% | National, concentrated in academic medical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of COPD, Asthma & Sleep Apnea

Chronic respiratory conditions now affect about 12 million UK residents, raising emergency admissions for asthma by 17% in the financial year ending 2024.[1]Asthma + Lung UK, “Asthma and Lung Statistics,” asthmaandlung.org.uk The prevalence of sleep apnea is around 8% among adults. Yet, underdiagnosis keeps a wide care gap, which home sleep-testing devices approved by the National Institute for Health and Care Excellence (NICE) in 2024 are beginning to close. Obesity reached 29% of adults in 2025, further boosting demand for continuous positive airway pressure (CPAP) and bilevel positive airway pressure (BiPAP).[2]National Institute for Health and Care Excellence, “Medical Technology Guidance,” nice.org.uk New biologics such as GSK’s Nucala reduce severe-asthma flare-ups but still require rescue inhalers and nebulizers, sustaining equipment volumes. Together, these epidemiological trends lift the UK respiratory devices market by expanding both therapeutic and monitoring use cases.

Ageing Population & Co-Morbidities

Citizens aged 65 and older climbed to 12.9 million in 2025, and COPD prevalence in this group is four times that of younger adults.[3]Office for National Statistics, “Population Estimates,” ons.gov.uk Two-thirds of individuals over 75 live with multiple chronic illnesses, which pushes clinicians to favor platforms that monitor oxygen saturation, heart rate, and respiration in one unit. Frailty screenings now routinely include spirometry, broadening the diagnostic installed base beyond pulmonology departments. Higher co-morbidity also lengthens therapy duration, lifting recurring sales of disposables. These demographic realities reinforce long-run demand in the UK respiratory devices market.

Technological Advances & Home-Care Shift

Home healthcare volume is rising 10.40% annually as the NHS steers COPD and sleep apnea follow-up into virtual wards. The N-Tidal Diagnose test, cleared in 2025, offers an artificial-intelligence alternative to traditional spirometry and will debut in April across select trusts. Interoperability mandates force vendors to adopt HL7 FHIR data standards, ensuring that results flow seamlessly into general-practice records. Portable oxygen concentrators with eight-hour batteries, including Invacare’s Platinum Mobile, address mobility barriers for working-age COPD patients. As a result, the UK respiratory devices market gains from faster adoption cycles and higher replacement rates for legacy equipment.

NHS Low-Carbon-Inhaler Initiative

The health service is committed to achieving net-zero emissions by 2045, with inhalers accounting for 3.1% of its 2024 carbon footprint. Guidance issued in 2024 urges prescribers to switch to dry-powder products or propellants such as HFA-152a. The European Medicines Agency (EMA) endorsed the safety of HFA-152a in 2024, removing a key regulatory obstacle. GSK’s Trelegy Ellipta, a dry-powder triple therapy, has seen rapid formulary uptake because of its negligible climate impact. These policies encourage long-term product redesign and expand the UK respiratory devices market toward greener alternatives.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High device cost & NHS budget limits | -1.2% | National, acute in devolved administrations | Short term (≤ 2 years) |

| MHRA post-brexit regulatory hurdles | -0.8% | National, affecting importers and EU-based manufacturers | Medium term (2-4 years) |

| Sustainability phase-out of high-propellant MDIs | -0.5% | National, Wales and Scotland leading | Short term (≤ 2 years) |

| Semiconductor-sensor supply fragility | -0.4% | National, impacting diagnostic device availability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Cost & NHS Budget Limits

The 2025-2026 NHS allocation of GBP 165 billion held capital budgets flat amid inflation, curbing new-equipment outlays.[4]European Medicines Agency, “Reflection Paper on Environmentally Sustainable Inhalers,” ema.europa.eu BiPAP units range from GBP 1,200–2,500 (USD 1,639 -3,414), while portable concentrators cost up to GBP 3,500 (USD 4,780), stretching trust finances. Home oxygen reimbursement has not changed since 2018, dimming suppliers’ incentive to refresh fleets. Scotland’s 2025 tender rewarded the lowest total cost of ownership, favoring makers that bundle maintenance. Private CPAP purchases average GBP 800 and remain out of reach for many undiagnosed apnea patients.

MHRA Post-Brexit Regulatory Hurdles

CE-marked devices were grandfathered only until June 2024, forcing firms to secure UKCA labels through one of four notified bodies, thereby lengthening the approval process from 4 to 10 months. Duplicate biocompatibility testing raised costs for small disposable-kit suppliers. Divergent software rules add uncertainty for AI-enabled spirometry players eyeing both UK and EU sales. The Windsor Framework keeps Northern Ireland under EU law, splitting launch strategies inside the kingdom.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Dominance Anchors Revenue Base

Therapeutic models captured 58.10% of the UK respiratory devices market share in 2025 as CPAP, BiPAP, and concentrators remain integral to chronic-care pathways. Continuous-positive-airway-pressure equipment benefited from NICE-endorsed home testing, which cut wait times from 22 to 8 weeks, creating a brisk referral flow. BiPAP devices saw higher uptake in virtual wards where clinicians remotely adjust settings via cloud dashboards, improving adherence and reducing readmissions. Nebulizers remain relevant for acute flares and pediatric asthma, with PARI’s eFlow delivering treatments in under 3 minutes. Oxygen concentrators serve roughly 150,000 long-term patients, yet stagnant reimbursement hampers fleet modernization.

Disposable masks, circuits, and filters posted an 8.80% annual growth rate, the fastest within this segmentation, encouraged by strict infection-prevention guidelines. Pulse oximeters, widely distributed during the pandemic, now face a replacement cycle that favors Bluetooth-enabled models with trend analytics. Fisher & Paykel’s Evora nasal mask shows how incremental ergonomic tweaks sustain premium positioning. High-priced ventilators from Dräger and Hamilton remain essential in intensive care, although volumes are smaller than for sleep-apnea and COPD hardware.

By End User: Home Healthcare Outpaces Institutional Channels

Hospitals and clinics accounted for 60.04% of revenue in 2025, yet home-health sites are expanding by 10.40% annually as the NHS diverts chronic follow-up to community settings. Virtual wards enrolled 50,000 respiratory patients in 2025, using pulse oximeters and capnographs to monitor daily vitals. ResMed’s myAir platform reduced the average length of stay by 3 days in pilot trusts, freeing acute beds for surgical cases. Ambulatory surgery centers increasingly rely on portable spirometers for pre-op risk stratification in patients aged 60 and older, as advised by NICE.

Home-health momentum in the UK respiratory devices market reflects gains in portability: concentrators with eight-hour batteries enable work and travel, while smart-inhaler data integrate with electronic records to auto-alert clinicians. Hospitals still dominate invasive ventilation and complex diagnostics, such as bronchoscopy. Ambulatory centers, which performed 1.2 million procedures in 2024, adopted end-tidal CO₂ monitoring following an MHRA safety alert. Long-term care facilities are now adopting handheld spirometers so staff can conduct on-site lung function screening.

By Disease Indication: Sleep Apnea Gains on COPD

COPD commanded 32.34% of demand in 2025, mirroring its status as the nation’s fifth-leading cause of death. Even so, sleep-apnea solutions are forecast to grow 10.11% through 2031, the highest among indications, as home polygraphy slashes diagnostic costs to GBP 150 and clears wait-list bottlenecks. ResMed’s AirSense 11 and Philips’ DreamStation 2 dominate CPAP, while Fisher & Paykel masks gain share with modular seals that cut in-person fitting needs. Asthma affects 5.4 million citizens and drives steady turnover of inhalers and nebulizers; smart-inhaler trials show 19% fewer pediatric emergency visits when adherence data is shared with caregivers.

Pneumonia spikes in winter sustain nebulizer and oxygen-concentrator sales for remote monitoring. The “others” category includes interstitial lung disease, pulmonary hypertension, and cystic fibrosis, which require specialized kits such as oscillating positive-expiratory-pressure devices, a niche served by Vitalograph and Intersurgical. Collectively, these niches keep the UK respiratory devices market diversified across acute and chronic applications.

By Age: Pediatric Segment Surges on Smart-Device Adoption

Adults represented 69.80% of 2025 volumes, driven by COPD and sleep-apnea prevalence in middle age. Yet pediatric equipment is on track for 10.90% annual growth, the fastest across age cohorts, propelled by Small Business Research Initiative funding for connected nebulizers and adherence-tracking inhalers. TEAMCare trials showed a 19% drop in emergency-department visits when children used smart inhalers that transmit real-time data to clinicians.

Portable concentrators with simplified controls help mitigate dexterity limitations. Meanwhile, MHRA consultation papers propose tougher algorithm-validation rules for pediatric software, reflecting physiological variability in lung development. Both pediatric and geriatric ends of the spectrum increasingly benefit from remote-monitoring alerts embedded into electronic health records.

Geography Analysis

England, home to 84% of the population, drives the bulk of the UK respiratory devices market; however, Scotland and Wales act as innovation test beds. Greater London, Manchester, and Birmingham piloted AI-enabled spirometry and virtual-ward platforms sooner than rural regions, creating a phased adoption curve. Northern Ireland’s alignment with EU medical device rules requires dual certification, which discourages particular launches.

Scotland’s 2024 rural-oxygen program subsidized portable concentrators for residents more than 30 minutes from hospital care, recognizing that stationary units weighing 15–20 kg are impractical in remote terrain. Post-industrial areas in the North of England and South Wales, where COPD rates exceed national averages by 30%, lean heavily on nebulizers and long-term oxygen therapy. Still, constrained budgets steer procurement toward value models.

Wales hit 41% low-GWP inhaler prescribing by late 2024, setting a sustainability benchmark. England aims to reach comparable levels by 2027, while Scotland trails marginally behind due to differing formulary policies. Such devolved priorities influence vendor rollout strategies and shape pockets of above-trend growth across the UK respiratory devices market.

Competitive Landscape

The vendor field is moderately fragmented; the NHS 2024 non-invasive ventilation framework named 28 suppliers under a GBP 160 million ceiling. Philips, ResMed, and Fisher & Paykel together hold roughly 35% in value terms, supported by cloud platforms such as DreamMapper and myAir that differentiate otherwise commoditizing CPAP devices. Cost-effectiveness remains pivotal because NHS contracts cap unit prices and reward bundled maintenance offerings.

Start-ups exploit white spaces: Hailie’s adherence sensors and N-WATCH’s pediatric capnography fill gaps in monitoring that incumbents don't address. Regulatory agility also shapes competition; firms with established UK-based notified-body links gain approval faster under UKCA rules, while EU-focused manufacturers face longer lead times. Technology adoption often starts in integrated care systems across London and Manchester before national scaling, rewarding suppliers that provide phased implementation support.

UK Respiratory Devices Industry Leaders

Fisher & Paykel Healthcare Ltd

DeVilbiss Healthcare LLC

GSK plc

GE Healthcare

Drägerwerk AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Chiesi UK and Ireland has announced the submission of beclometasone (available in 100mcg and 200mcg doses), reformulated with the next-generation propellant HFA-152a, to the MHRA. This development positions beclometasone as the first product in Chiesi’s global pMDI portfolio to integrate the next-generation propellant, reflecting the company’s strategic commitment to achieving Net Zero emissions by 2035.

- March 2025: N-Tidal Diagnose became the first non-spirometry AI COPD test to be cleared under the EU MDR and launched across the NHS in April 2025.

- March 2025: Smart Respiratory launched a London pharmacy pilot using Smart Peak Flow and Smart Asthma digital tools to monitor and control lung function.

UK Respiratory Devices Market Report Scope

As per the scope of the report, respiratory devices include respiratory diagnostic devices, therapeutic devices, and breathing devices for administering long-term artificial respiration. It may also include a breathing apparatus used for resuscitation, by forcing oxygen into the lungs of a person who has undergone asphyxia.

The UK respiratory devices market is segmented by device type, end-user, disease indication, and age. By device type, the market is segmented into diagnostic and monitoring devices, therapeutic devices, and disposables. By end-user, the market is segmented into hospitals & clinics, home healthcare settings, ambulatory surgical centers, and others. By disease indication, the market is segmented into COPD, asthma, sleep apnea, pneumonia & acute respiratory infections, and others. By age, the market is segmented into adult, geriatric, and pediatric. The report offers the value (in USD) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | |

| Peak Flow Meters | |

| Pulse Oximeters | |

| Capnographs | |

| Other Diagnostic & Monitoring | |

| Therapeutic Devices | CPAP Devices |

| BiPAP Devices | |

| Humidifiers | |

| Nebulizers | |

| Oxygen Concentrators | |

| Ventilators | |

| Inhalers | |

| Other Therapeutic Devices | |

| Disposables | Masks |

| Breathing Circuits | |

| Other Disposables |

By End-User

| Hospitals & Clinics |

| Home Healthcare Settings |

| Ambulatory Surgical Centers |

| Others |

By Disease Indication

| COPD |

| Asthma |

| Sleep Apnea |

| Pneumonia & Acute Respiratory Infections |

| Others |

By Age

| Adult |

| Geriatric |

| Pediatric |

| By Device Type | Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | ||

| Peak Flow Meters | ||

| Pulse Oximeters | ||

| Capnographs | ||

| Other Diagnostic & Monitoring | ||

| Therapeutic Devices | CPAP Devices | |

| BiPAP Devices | ||

| Humidifiers | ||

| Nebulizers | ||

| Oxygen Concentrators | ||

| Ventilators | ||

| Inhalers | ||

| Other Therapeutic Devices | ||

| Disposables | Masks | |

| Breathing Circuits | ||

| Other Disposables | ||

| By End-User | Hospitals & Clinics | |

| Home Healthcare Settings | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Disease Indication | COPD | |

| Asthma | ||

| Sleep Apnea | ||

| Pneumonia & Acute Respiratory Infections | ||

| Others | ||

| By Age | Adult | |

| Geriatric | ||

| Pediatric | ||

Key Questions Answered in the Report

How large is the UK respiratory devices market in 2026?

It reached USD 2.0 billion in 2026 and is on track to reach USD 3.03 billion by 2031.

Which device category earns the most revenue?

Therapeutic equipment such as CPAP, BiPAP, and oxygen concentrators held 58.10% of 2025 revenue.

What is driving growth in home respiratory care?

NHS virtual-ward programs, eight-hour-battery concentrators, and telehealth data integration are pushing a 10.40% CAGR in home settings.

Why are disposables growing faster than capital equipment?

Infection-control policies now favor single-use masks and circuits, driving an 8.80% annual rise in consumables demand.

How are sustainability goals reshaping inhaler demand?

The NHS aims to halve high-propellant MDI use by 2027, shifting prescribing toward dry-powder and low-GWP alternatives.

What regulatory change affects market entry timelines?

Post-Brexit UKCA certification, managed by only four notified bodies, extends average device approval to about ten months.

Page last updated on: