Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

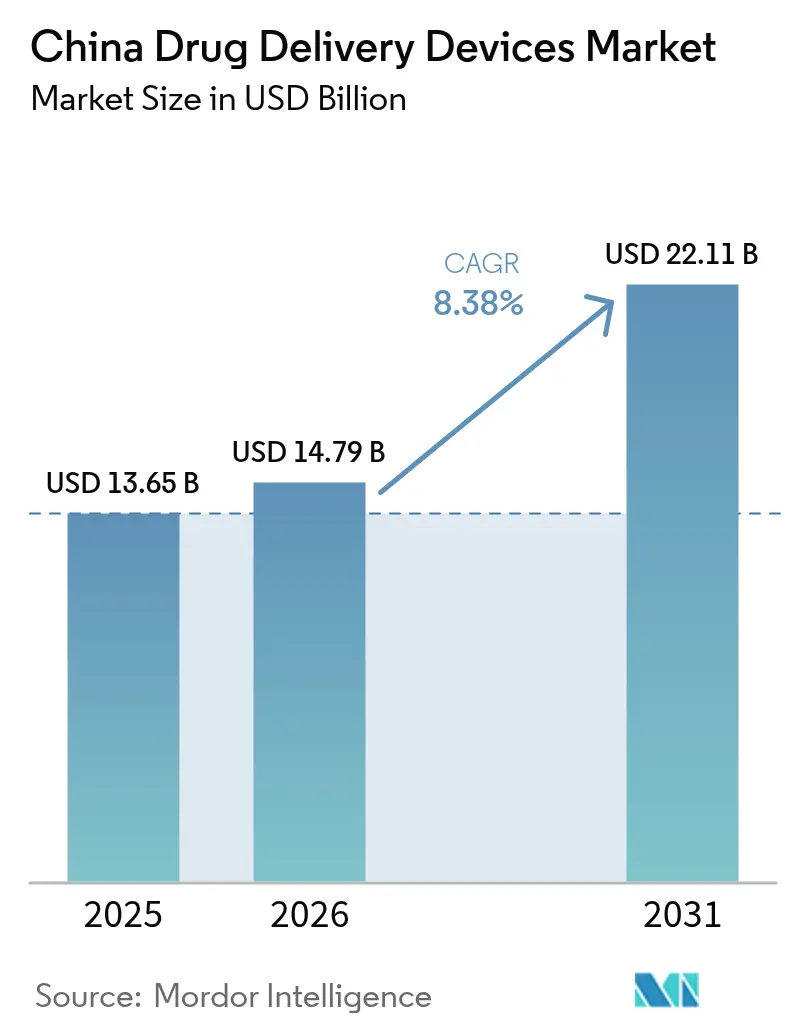

| Base Year Market Size (2025) | USD 13.65 Billion |

| Market Size (2026) | USD 14.79 Billion |

| Market Size (2031) | USD 22.11 Billion |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Drug Delivery Devices Market Analysis by Mordor Intelligence

The China drug delivery devices market size is expected to grow from USD 13.65 billion in 2025 to USD 14.79 billion in 2026 and is forecast to reach USD 22.11 billion by 2031 at 8.38% CAGR over 2026-2031. Growth is powered by a rapidly aging population, 28% of citizens will be over 60 by 2040, along with rising chronic-disease prevalence, sweeping reimbursement reforms, and a wave of biologics that demand precision delivery.[1]World Health Organization, “Ageing and health – China,” who.int Volume-Based Procurement (VBP) has lowered average drug prices by 53%, which is steering hospitals toward locally made devices while encouraging global suppliers to localize production. Persistent air-quality challenges in tier-1 cities are sustaining demand for inhalation platforms even as respiratory conditions remain a public-health priority. At the same time, 5G connectivity and AI-enabled adherence tools are opening fresh opportunities for smart, home-use systems in rural regions.[2]National Healthcare Security Administration, “China Focus: National medical insurance delivers more,” english.news.cn Competitive pressure is intensifying as domestic contract development and manufacturing organizations (CDMOs) scale up, compressing costs for both injectables and emerging implantables.

Key Report Takeaways

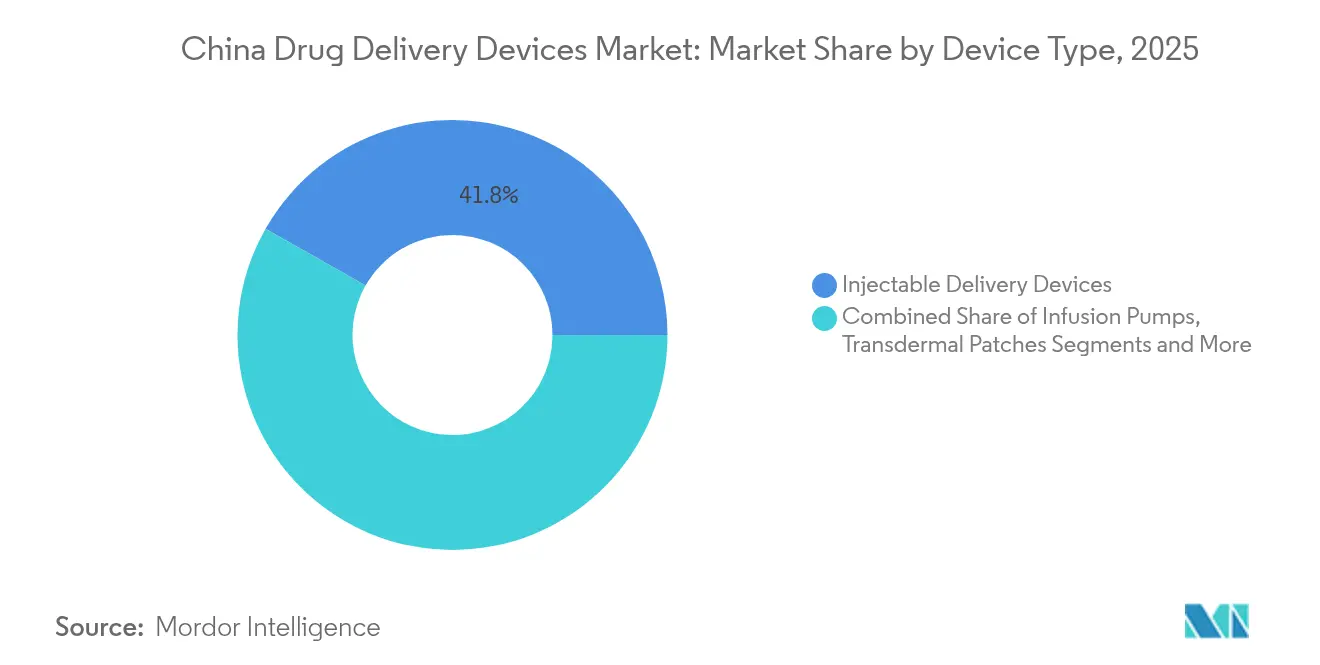

- By device type, injectable platforms led with a 41.78% revenue share in 2025, while implantable systems are projected to expand at an 10.74% CAGR to 2031.

- By route of administration, injectable routes accounted for 48.02% of the China drug delivery devices market share in 2025, whereas ocular delivery is forecast to post a 10.21% CAGR through 2031.

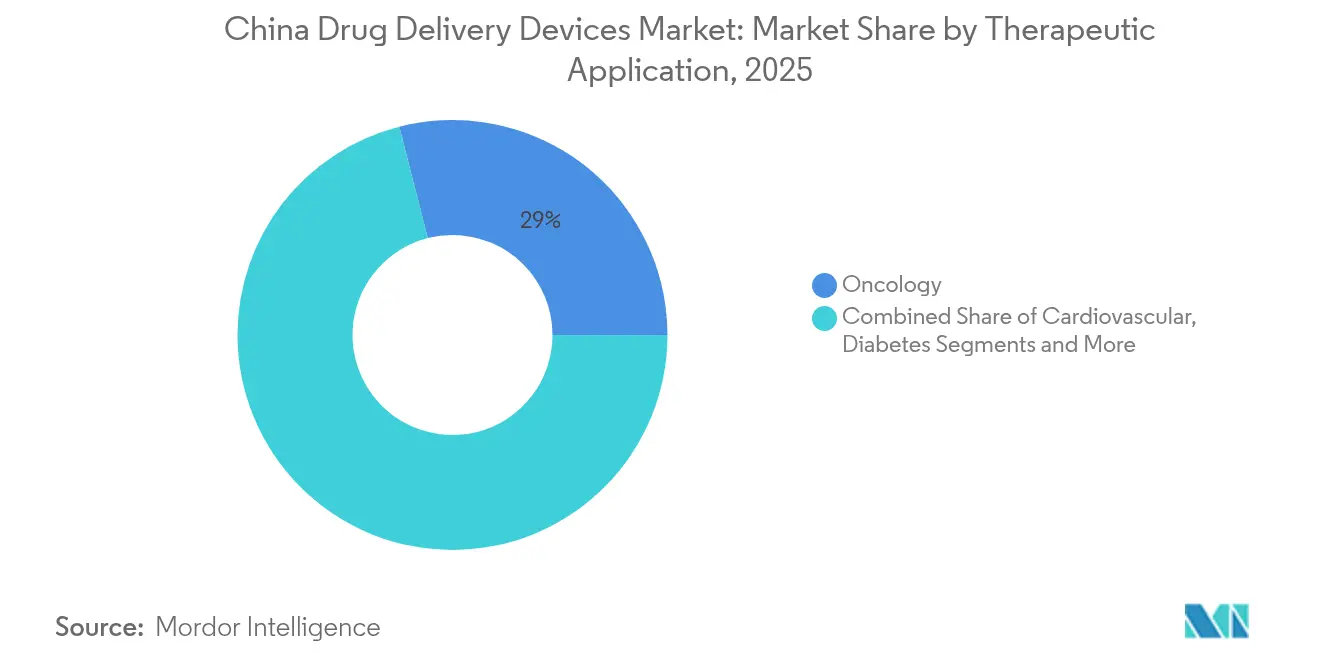

- By therapeutic application, oncology captured 28.98% of the China drug delivery devices market size in 2025, while diabetes devices are set to grow at a 9.18% CAGR to 2031.

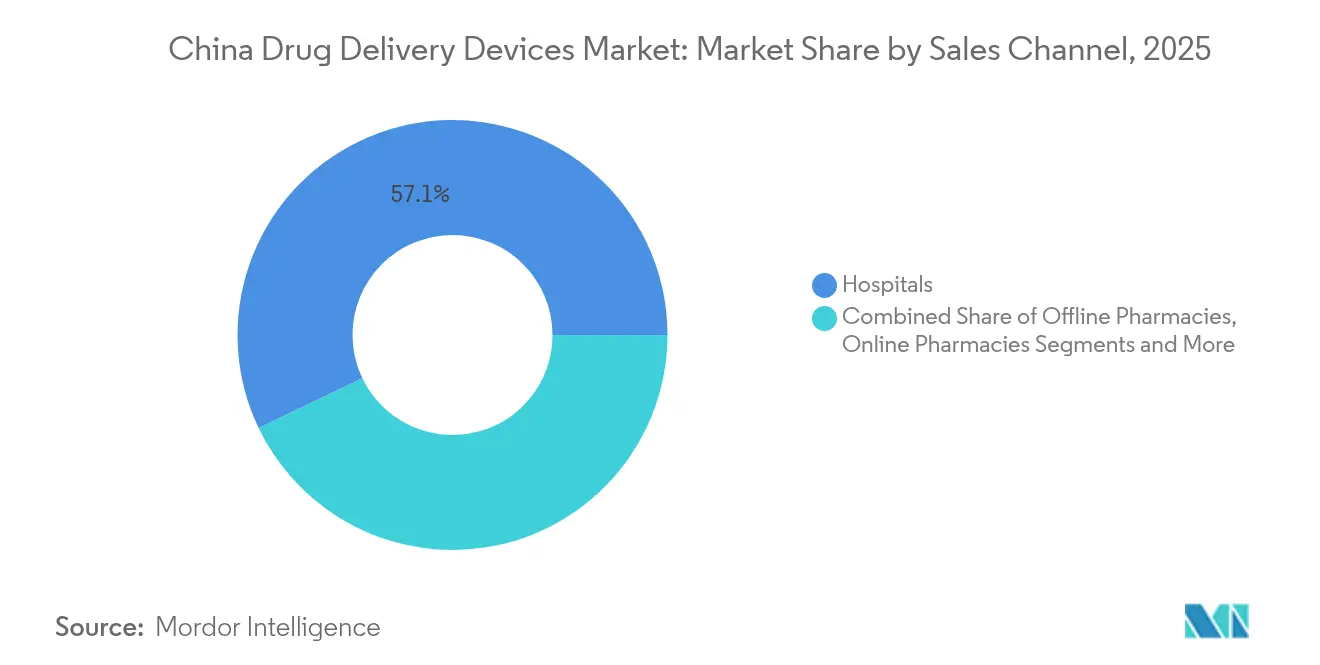

- By sales channel, hospitals held 57.12% revenue share in 2025; online pharmacies record the highest projected CAGR at 11.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases | +1.5% | National, concentrated in tier-1 and tier-2 cities | Long term (≥ 4 years) |

| Advances in biologics necessitating sophisticated devices | +1.2% | National, R&D hubs in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| Government health-insurance expansion | +0.8% | National, rural areas benefiting most | Short term (≤ 2 years) |

| Urban air-quality decline boosting inhalation demand | +0.6% | Beijing, Shanghai, Guangzhou, Shenzhen | Medium term (2-4 years) |

| Domestic CDMO scale-up lowering device costs | +0.9% | National, clusters in Jiangsu, Guangdong | Medium term (2-4 years) |

| 5G-enabled smart connectivity for adherence monitoring | +1.1% | Urban 5G zones, expanding to rural | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases

China now houses 22% of the global diabetes population, and cardiovascular illness affects around 330 million citizens, driving hospitals and payers toward precise, home-use devices that can curb readmissions while enabling self-management. The “Healthy China 2030” blueprint backs this shift, prioritizing chronic-disease control and broadening access to community-level services. Aging-related disability also lifts demand for long-acting implantables that reduce caregiver workload without compromising therapeutic outcomes. Devices that automate dosing or use remote monitoring are therefore gaining traction among provincial health authorities looking to shrink long-term care costs. Hospital groups in Shanghai and Guangzhou have already introduced bundled packages that pair insulin analogues with connected pens, demonstrating early commercial success.

Advances in Biologics Necessitating Sophisticated Devices

Chinese biotech funding remains buoyant—47 cell- and gene-therapy firms raised new capital in 1H 2024—pushing developers to seek materials and formats that protect fragile payloads. AI-driven start-ups such as METiS Pharmaceuticals are refining lipid nanoparticles for mRNA, which in turn boosts orders for temperature-controlled syringes and autoinjectors. Regulators have responded with guidelines that mandate post-marketing stability data, adding urgency for delivery innovations that maintain bioavailability from plant to patient.[3]Center for Drug Evaluation, NMPA, “Technical Guidelines for Studies on Pharmaceutical Changes of Marketed Vaccines,” ccfdie.orgOncology remains a focal point: personalized dosing regimens require variable-volume cartridges compatible with in-clinic compounding workflows. As a result, domestic syringe makers in Jiangsu have expanded clean-room capacity by double digits to serve local biopharma clients.

Government Health-Insurance Expansion

In 2025, the National Healthcare Security Administration (NHSA) added 91 formulations to the reimbursement list and secured average discounts of 63%, saving patients USD 7.6 billion. Because devices that demonstrate lower total cost of care receive faster catalog entry, innovators able to link adherence gains or reduced hospital stays to their platforms enjoy a clearer path to scale. Recent tenders for cochlear implants show how price negotiations can slash unit costs by 75%, setting a template for insulin pumps and wearable injectors. Rural pilots funded under the same program supply home-based lymphedema pumps bundled with tele-rehab, highlighting the policy’s reach beyond tertiary centers.

Domestic CDMO Scale-Up Lowering Device Costs

Local CDMOs have reached RMB 3.6 trillion in combined R&D spend, helping home-grown suppliers rival multinationals on quality while undercutting their cost base. Weigao Group’s revenue passed RMB 10.36 billion after it pioneered domestic prefilled syringes, demonstrating how economies of scale can unlock rapid share gain. Integrated “design-to-delivery” campuses in Guangdong shorten lead times by bypassing customs bottlenecks, which is critical for temperature-sensitive biologics. These efficiencies are feeding through to provincial tenders, where domestic implantables enter bids at discounts of 15-20% versus imported peers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and approval costs | -1.8% | National, smaller manufacturers | Medium term (2-4 years) |

| Centralized VBP price pressure | -0.7% | National, tier-2/3 cities | Short term (≤ 2 years) |

| Cold-chain gaps in lower-tier cities | -0.5% | Tier-3/4 cities, rural | Medium term (2-4 years) |

| Fragmented IP landscape delaying innovation | -0.4% | National, domestic start-ups | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High R&D and Approval Costs

Maider Medical’s revenue slid 42.77% in 2024 even as it kept R&D at 14.70% of sales, underscoring cost pressures on smaller firms. Contec Medical Systems faced a similar squeeze after a 35.76% top-line drop while sustaining RMB 10.52 million in research outlays. Enhanced NMPA testing requirements heighten compliance spend, creating a hurdles-to-entry effect that favors capital-rich incumbents. BeiGene’s cumulative loss of RMB 62.67 billion illustrates how even leading innovators absorb steep investment to meet global standards.

Centralized VBP Price Pressure

Artificial-joint tenders saved RMB 32.89 billion in 2024, proving the government’s ability to compress margins via bulk buys. With DRG reimbursement now rolling nationwide, device pricing is tied to episode-of-care ceilings rather than physician preference, curbing upsell potential in mid-tier cities. Multinationals that rely on imported bill-of-materials face tougher economics, spurring joint ventures and site transfers to Suzhou and Tianjin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Injectable Devices Lead Market Transformation

Injectable platforms retained a 41.78% share in 2025, anchoring the China drug delivery devices market as hospitals prefer proven parenteral formats for biologics and vaccines. Implantables post the fastest 10.74% CAGR, benefiting from materials science advances that support weeks-long release profiles. Inhalers continue to thrive in polluted metropolitan zones, while infusion pumps rise steadily on the back of ICU modernization projects. Transdermal patches win favor among seniors seeking pain relief without oral side effects, and ocular inserts gain momentum as diabetic retinopathy rates climb. Nasal and buccal formats, though niche, attract pediatric demand where needle avoidance is critical.

Injectables are also the first choice for home-based biologic regimens, which tightens linkages between prefilled syringe makers and tele-pharma platforms. Meanwhile, implantables ride on gene-therapy momentum: start-ups in Shanghai are prototyping refillable micro-reservoirs to pair with autologous cell payloads. These trends reinforce the China drug delivery devices market size leadership of injectable formats, yet implantables are closing the gap as payers recognize reduced dosing frequency benefits.

By Route of Administration: Injectable Routes Dominate Therapeutic Delivery

With 48.02% of 2025 revenue, injectables remain the backbone of therapeutic delivery owing to unmatched bioavailability and multi-therapeutic flexibility. Ocular routes, however, show a 10.21% CAGR through 2031 as sustained-release implants cut injection frequency for macular degeneration. Inhalation stands firm because pollution-driven chronic obstructive pulmonary disease (COPD) cases remain high in urban clusters. Transdermal lines grow in cardiovascular care, aided by skin-friendly adhesives that enable week-long nitroglycerin delivery. Oral mucosal and nasal routes gain share for emergency and pediatric uses where rapid onset is pivotal.

Regulators now encourage patient-reported outcomes in ocular trials, fast-tracking approvals for micro-dose injectors that limit systemic exposure. Local inhaler makers add smartphone pairing to monitor technique, meeting NHSA evidence thresholds for reimbursement. As a result, the China drug delivery devices market share of non-injectable routes is set to widen, although injectables keep pole position for biologics and vaccines.

By Therapeutic Application: Oncology Leadership Amid Diabetes Surge

Oncology captured 28.98% revenue in 2025, reflecting heavy R&D spending by firms like BeiGene on targeted antibodies requiring specialized delivery. Diabetes devices are projected to clock a 9.18% CAGR as the country grapples with its vast diabetic population. Cardiovascular applications stay prominent given 330 million affected patients, while autoimmune therapies benefit from biologics entering NHSA coverage. Pulmonary indications tap pollution-linked disease burden, and neurology sees steady growth as Alzheimer’s detection rises. Gene-therapy deliveries remain small but climb quickly due to landmark financings in 2024.

Oncology players innovate with subcutaneous on-body injectors that deliver multi-hour infusions at home, easing hospital load. Diabetes interprets smart-pen and patch-pump ecosystems to bolster adherence, aligning with Healthy China guidelines. Consequently, diabetes stands ready to challenge oncology’s dominance as connected dosage tracking proves cost-effective for payers.

By Sales Channel: Hospital Dominance Challenged by Digital Transformation

Hospitals controlled 57.12% of 2025 sales, mirroring China’s institutional care model and complex device calibration needs. Online pharmacies, though smaller, will log a 11.32% CAGR on the back of e-prescription policy liberalization and telehealth uptake. Brick-and-mortar pharmacies fill gaps in tier-2 cities and handle immediate pickup for chronic prescriptions, while specialty clinics and home-health services join distribution chains as payers push care closer to patients.

VBP policies now apply across channels, so online retailers compete on logistics and adherence services instead of price. Hospitals, meanwhile, integrate 5G pumps into electronic medical records, giving them an edge in bundled outcome contracts. Over time, device makers will refine packaging and user interfaces for direct-to-patient supply, nurturing a multi-channel China drug delivery devices market size dynamic.

Geography Analysis

Tier-1 cities—Beijing, Shanghai, Guangzhou, and Shenzhen—set adoption benchmarks owing to higher incomes, dense hospital networks, and early access to NMPA-approved innovations. Pollution remains acute, sustaining premium inhaler uptake, while provincial tenders in these hubs often become bellwethers for national reimbursement. Tier-2/3 cities such as Chengdu and Wuhan post faster growth as infrastructure builds out and NHSA reimbursement boosts affordability. Cold-chain gaps remain a hurdle but also spur investment in passive cooling and temperature-stable formulations.

Rural regions, despite thin provider density, offer long-term volume upside thanks to Healthy China mandates focused on equity. Portable injectors and connected patches are attractive here because they minimize clinic visits. County-wide 5G pilots in Shanxi cut adherence lapses, illustrating how connectivity can offset staff shortages. Domestic manufacturers in Jiangsu and Guangdong leverage proximity to export ports and skilled labour to scale production that feeds both coastal and inland demand.

Regional supply chains now feature vertically integrated parks that cluster molding, sterilization, and packaging within a single free-trade zone, trimming lead times to western provinces by up to 30%. As such ecosystems mature, the China drug delivery devices market is expected to show narrowing regional price differentials while premium adoption still skews east.

Competitive Landscape

Global suppliers such as Becton Dickinson, Gerresheimer and Pfizer still anchor high-value tiers, yet their pricing leverage is shrinking as Volume-Based Procurement forces local manufacturing and leaner cost structures. Becton Dickinson has expanded syringe capacity in Suzhou to secure future bulk tenders for prefilled systems npe.org. Gerresheimer entered a Shandong joint venture that shortens lead times on moulded glass vials for provincial reimbursement cycles. Pfizer now packages oncology kits in Zhejiang to keep cold-chain logistics entirely within China. Together, these moves underline how multinationals are recalibrating footprints to stay price-competitive.

Domestic champions are scaling quickly on the back of integrated campuses and targeted R&D. Weigao Group lifted revenue to RMB 10.36 billion after opening a Weihai complex that cuts syringe unit cost by nearly 20%. MicroPort leveraged its cardiology franchise to launch the Firelimus drug-eluting balloon in 2025, positioning the product as a home-grown alternative to imported stents. Keymed Biosciences gained supplemental approval for Stapokibart and paired the antibody with a proprietary prefilled pen to reduce clinic visits for chronic rhinosinusitis. These successes show how local innovators marry rapid regulatory navigation with cost advantages.

Investment remains brisk even as compliance costs climb. METiS Pharmaceuticals raised USD 100 million for AI-guided lipid nanoparticle platforms aimed at mRNA and cell therapies, signalling strong appetite for next-generation delivery science. Contract development and manufacturing hubs in Jiangsu and Guangdong provide turnkey scale for start-ups that lack capex headroom. Rising capital intensity is nudging smaller firms toward mergers, pointing to gradual consolidation around players that combine local cost bases with clinically verified performance.

China Drug Delivery Devices Industry Leaders

Becton, Dickinson and Company

Gerresheimer AG

Pfizer Inc.

Kindly Medical Instruments Co., Ltd

Ypsomed Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: MicroPort’s Firelimus Rapamycin Drug-Eluting Balloon Catheter gained NMPA approval for coronary bifurcation lesions, offering an excipient-free alternative to permanent stents.

- January 2025: NHSA added 91 drugs to reimbursement with 63% price cuts, saving USD 7.6 billion and widening access to advanced delivery systems.

- December 2024: Keymed Biosciences received sNDA approval for Stapokibart to treat chronic rhinosinusitis with nasal polyposis.

- September 2024: Regeneron and Sanofi secured NMPA clearance for Dupixent as add-on COPD therapy, marketed in 300 mg pre-filled devices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China drug-delivery-devices market as revenue generated within China from purpose-built medical devices, including injectors, inhalers, infusion pumps, patches, implants, and ocular and nasal platforms that meter, time, or otherwise control therapeutic administration. We size the market at the manufacturer "factory-gate" level in U.S. dollars, net of the drug payload itself.

Scope Exclusions: Single-use syringes, intravenous sets, and pharmaceutical sales lacking an integrated delivery mechanism lie outside this scope.

Segmentation Overview

- By Device Type

- Injectable Delivery Devices

- Inhalation Delivery Devices

- Infusion Pumps

- Transdermal Patches

- Implantable Drug Delivery Systems

- Ocular Inserts & Delivery Implants

- Nasal & Buccal Delivery Devices

- By Route of Administration

- Injectable

- Inhalation

- Transdermal

- Oral Mucosal (Buccal & Sublingual)

- Ocular

- Nasal

- By Therapeutic Application

- Cardiovascular

- Oncology

- Autoimmune Disorders

- Pulmonary Diseases

- Diabetes

- Neurological Disorders

- Other Applications

- By Sales Channel

- Hospitals

- Offline Pharmacies

- Online Pharmacies

- Other Channels

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed biomedical engineers at three domestic pump makers, purchasing managers from top-tier hospitals in Beijing and Chongqing, and provincial drug-device distributors. These discussions verified average selling prices, usage mix shifts toward smart pens, and regional tender volumes, enabling us to refine model assumptions.

Desk Research

We gathered baseline figures from public sources such as National Medical Products Administration (NMPA) device approvals, General Administration of Customs HS codes 9018/9021 shipment data, National Health Commission hospital procurement bulletins, and Chinese Medical Device Industry Association yearbooks. Company 10-Ks, investor decks, and peer-reviewed articles in the Chinese Journal of Medical Instruments helped us map competitive footprints. Paid databases, including D&B Hoovers for manufacturer financials, Dow Jones Factiva for deal news, and Questel for recent patent filings, supplemented gaps. The sources listed are illustrative; many additional references were consulted for corroboration.

Market-Sizing & Forecasting

A top-down construct begins with NMPA Class III registered device stocks and annual import volumes, which are then multiplied by blended ex-factory ASPs derived from tender databases. Bottom-up roll-ups of leading supplier revenues provide reasonableness checks. Key variables, like insulin-dependent diabetic population, COPD prevalence, hospital bed additions, average tender frequency, and RMB-USD exchange trends, feed a multivariate regression that projects demand to 2030. Scenario analysis adjusts for reimbursement policy swings and domestic substitution rates where data gaps persist.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst self-audit, senior peer check, and domain lead sign-off. Variances beyond +/-5 percent versus independent indicators trigger re-work. We refresh the model annually and issue interim updates after material regulatory or recall events.

Why Mordor's China Drug Delivery Devices Baseline Commands Reliability

Published estimates often diverge because firms select different device lists, price points, and refresh cadences. By anchoring our starting pool to legally registered devices and verified tender prices, we limit scope creep and currency noise.

Key gap drivers include whether pumps and smart wearables are counted, how imported ASP inflation is handled, and the year used as the base for CAGR math.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.65 B (2025) | Mordor Intelligence | |

| USD 16.93 B (2024) | Regional Consultancy A | Adds pre-filled syringe contract manufacturing and keeps FX fixed |

| USD 7.84 B (2023) | Global Consultancy B | Omits inhalers and electronic pumps, focusing on conventional devices only |

| USD 4.80 B (2024) | Sector Newsletter C | Extrapolates from limited hospital sample and oncology-only spend |

Taken together, the comparison shows that Mordor's disciplined scope, variable selection, and annual refresh yield a balanced, transparent baseline that decision-makers can trace back to concrete volumes and repeatable steps.

Key Questions Answered in the Report

What is the current size of the China drug delivery devices market and how fast is it growing?

The market stands at USD 14.79 billion in 2026 and is projected to expand to USD 22.11 billion by 2031, reflecting an 8.38% CAGR.

Which device segment is expanding the quickest?

Implantable drug delivery systems show the fastest momentum, advancing at an 10.74% CAGR through 2031 on the back of long-acting therapies and aging-related demand.

How is Volume-Based Procurement (VBP) influencing device pricing?

VBP rounds have driven average drug-price cuts of 53%, compelling manufacturers to lower device costs and favoring suppliers with local production footprints.

Why are inhalation devices in strong demand despite pollution improvements?

Tier-1 city air-quality levels remain 5.6 times above WHO guidelines, sustaining a large respiratory patient pool that requires advanced inhaler platforms.

What role does 5G connectivity play in China’s drug delivery devices landscape?

More than 94,000 commercial 5G cases enable real-time adherence monitoring, particularly boosting uptake of smart infusion pumps and connected insulin pens in underserved areas.

Which restraint poses the greatest challenge for new entrants?

High R&D and regulatory-approval costs, intensified by stricter NMPA testing requirements, represent the steepest barrier, cutting most sharply into smaller manufacturers’ margins.

Page last updated on: