Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 268.26 Million |

| Market Size (2026) | USD 283.14 Million |

| Market Size (2031) | USD 370.94 Million |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Respiratory Devices Market Analysis by Mordor Intelligence

The Australia Respiratory Devices Market size is projected to be USD 268.26 million in 2025, USD 283.14 million in 2026, and reach USD 370.94 million by 2031, growing at a CAGR of 5.55% from 2026 to 2031.

Demand is reinforced by rising COPD burden among older Australians and persistent underdiagnosis that keeps diagnosis and monitoring equipment in use across primary and specialty care settings. Regulatory activity is shaping both time-to-market and compliance costs, rewarding players with strong quality systems and local regulatory teams that can navigate TGA pathways efficiently. Public funding for Medicare, connected care, and disability support is driving home-based therapy adoption, benefiting vendors that bundle hardware with remote monitoring and software services. Competitive dynamics remain balanced as ResMed and Fisher & Paykel Healthcare build on product depth and cloud ecosystems. At the same time, Philips addresses recall-driven remediation under active TGA oversight that is still reshaping channel choices among providers.

Key shifts in the Australian respiratory devices market include faster growth of disposables tied to infection control protocols, acceleration of home-based sleep apnea and COPD care supported by permanent telehealth devices, and deeper integration between connected devices and electronic medical records. State health systems and aged-care operators are also building preparedness for smoke and seasonal respiratory surges by expanding stocks of nebulizers, oxygen concentrators, and monitoring devices, which supports a steadier procurement cadence.

Key Report Takeaways

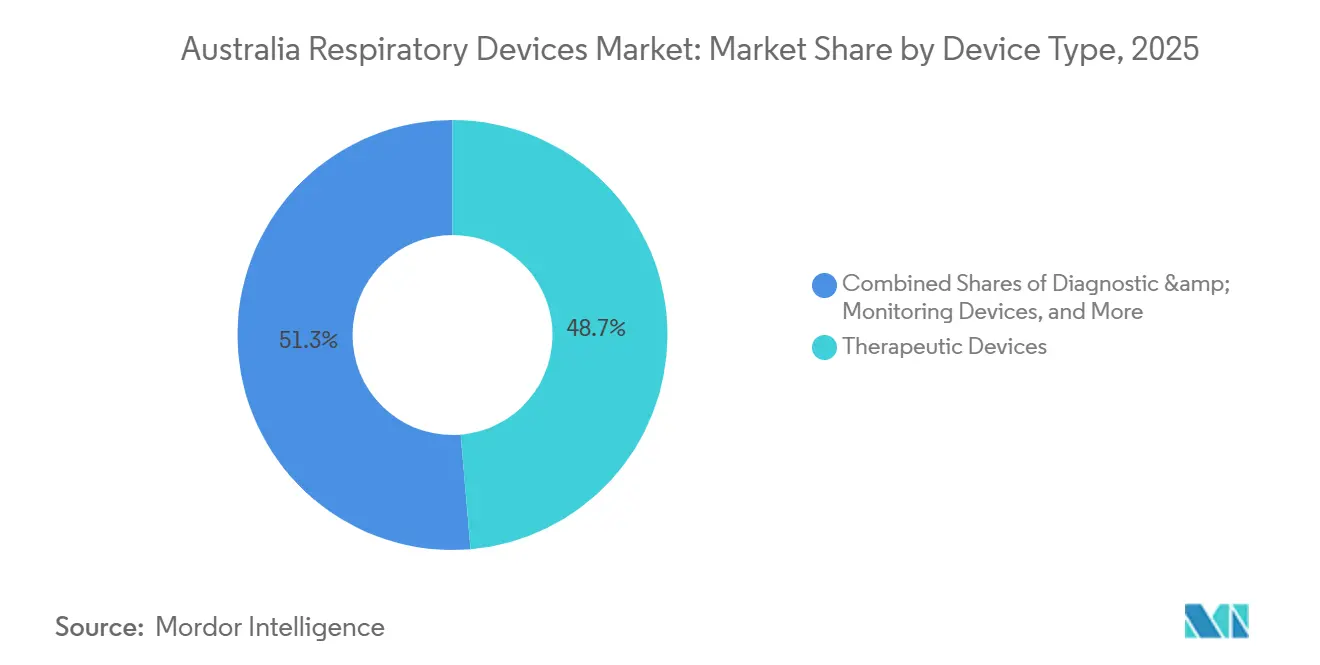

- By device type, therapeutic devices led with 48.67% revenue share in 2025, while disposables are forecast to expand at an 8.80% CAGR through 2031.

- By end user, hospitals and clinics held 61.05% of the Australia respiratory devices market share in 2025, while home healthcare recorded the highest projected CAGR at 10.40% through 2031.

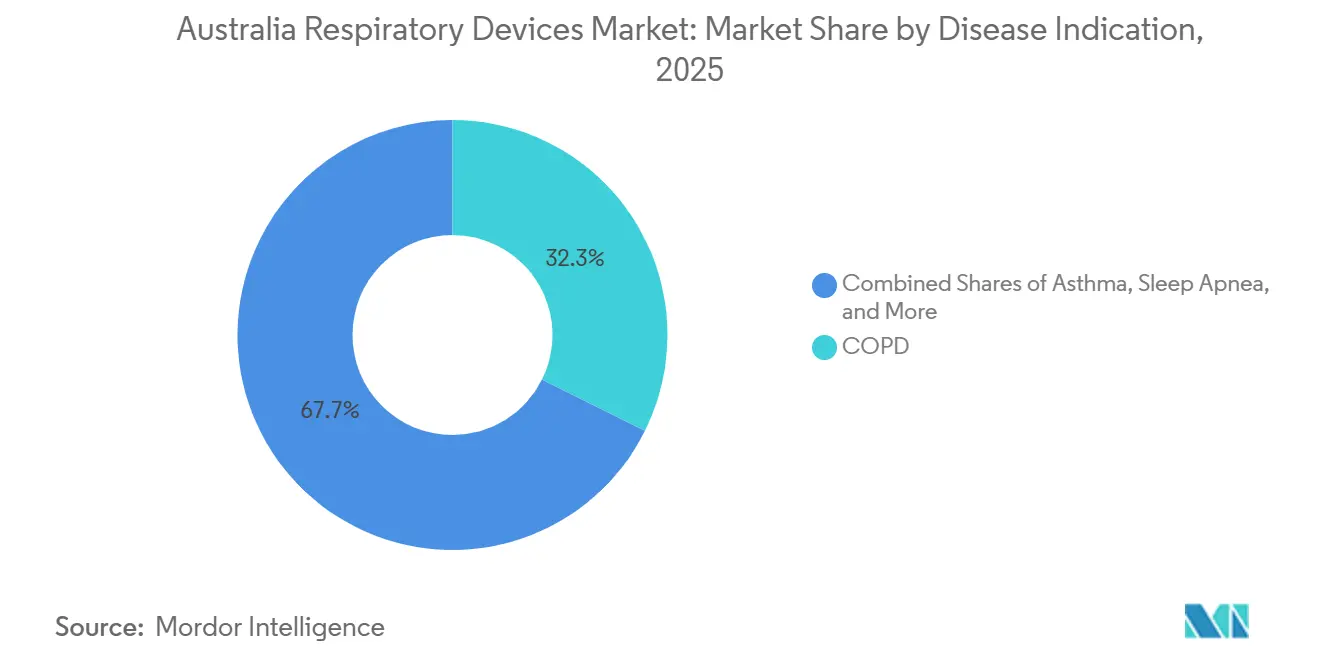

- By disease indication, COPD accounted for 32.34% of the Australian respiratory devices market in 2025, and sleep apnea is advancing at a 5.84% CAGR through 2031.

- By age group, the adult segment retained a 69.80% share in 2025, and the pediatric segment is projected to grow at a 10.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Respiratory Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing prevalence of chronic respiratory disorders | +1.2% | National, with higher concentration in New South Wales, Victoria, Queensland | Long term (≥ 4 years) |

| Government investment in respiratory clinics & home-care programs | +0.9% | National, with early gains in metropolitan areas and NDIS-eligible populations | Medium term (2-4 years) |

| Technological advances in connected respiratory devices | +0.8% | National, with early adoption in urban centers and private healthcare networks | Medium term (2-4 years) |

| Shift toward home-based sleep-apnea & COPD management | +1.1% | National, accelerated in Sydney, Melbourne, Brisbane metropolitan regions | Short term (≤ 2 years) |

| TGA fast-track pathways for digital/AI-enabled devices | +0.6% | National, benefiting manufacturers with Australian Regulatory Affairs teams | Medium term (2-4 years) |

| Bushfire-related air-quality deterioration boosting demand | +0.7% | Southeastern states, including NSW, Victoria, ACT, and Tasmania during fire seasons | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic Respiratory Disorders

Australia continues to face a heavy respiratory disease burden that keeps both diagnostic and therapeutic equipment in steady use across care settings. COPD prevalence rises sharply with age, reaching 7.0% among those 65 and older compared to 2.5% nationally, which concentrates utilization among older cohorts and supports sustained replacement cycles for spirometers, oxygen therapy, and ventilatory support.[1]Australian Institute of Health and Welfare, “Chronic Obstructive Pulmonary Disease (COPD),” Australian Institute of Health and Welfare, aihw.gov.au Underdiagnosis remains a recognized challenge, underscoring the role of primary care spirometry and remote monitoring in closing gaps in detection and long-term management. Disparities in COPD prevalence create a policy case for targeted access programs and procurement models that reduce up-front barriers to therapy in underserved communities. National clinical guidance updates introduced in late 2024 are intended to improve diagnosis quality and care consistency, which typically increases test volumes and drives a more standardized approach to device selection in hospitals and clinics. As Australia’s median age rises, these clinical and demographic dynamics support durable demand for connected devices that can alert care teams to deteriorations earlier and help prevent avoidable admissions.

Government Investment in Respiratory Clinics & Home-Care Programs

Federal funding is locking in the shift toward virtual and community-based respiratory care, reducing strain on tertiary hospitals. The 2025–26 Budget allocates AUD 8.5 billion (USD 5.7 billion) to strengthen Medicare, including sustained support for telehealth items that keep respiratory consultations and at-home follow-up viable at scale.[2]Australian Government Department of Health and Aged Care, “Budget 2025–26,” Australian Government Department of Health and Aged Care, health.gov.au The budget also funds a national lung cancer screening program over four years, which is expected to increase the use of spirometry and related diagnostic equipment across primary and specialist pathways. The National Disability Insurance Scheme received AUD 175.4 million (USD 117 million) in additional appropriations that improve access to assistive technology for eligible participants who require home ventilators and portable oxygen systems. State initiatives that embed remote monitoring into chronic care pathways have shown promise in reducing avoidable admissions for COPD, which encourages broader payor and provider adoption of connected respiratory devices. This public investment environment favors suppliers that can meet TGA requirements and align product roadmaps with care models designed around telehealth, home titration, and proactive disease management.

Technological Advances in Connected Respiratory Devices

Connected platforms are raising adherence and enabling earlier interventions that improve outcomes and reduce the total cost of care. ResMed’s AirSense 11 integrates cellular connectivity and the myAir app to transmit nightly therapy data to clinicians, which enables rapid adjustments and closer patient support across Australian sleep clinics. Integration of device data with primary-care electronic records via HL7 FHIR interfaces is maturing in urban networks, enabling general practitioners to act on meaningful trends, such as declining lung function, without waiting for in-person reviews. Vendors are moving from single-transaction sales to multi-year service bundles that include devices, connectivity, and clinical decision support, deepening switching costs and stabilizing revenue. These service-led models also align with how providers budget for digital health, since software-enabled monitoring can be tied to outcomes and quality metrics. As the Australian respiratory devices market standardizes on interoperable data flows, device selection is increasingly driven by the reliability of remote monitoring, alert specificity, and integration simplicity rather than by capital price alone.

Shift Toward Home-Based Sleep-Apnea & COPD Management

Permanent medicare telehealth items for respiratory consultations are underpinning a faster shift to home initiation, monitoring, and optimization, particularly for stable sleep apnea and COPD patients. Home healthcare is the fastest-growing end user as payors and providers use remote titration and digital adherence tools to improve therapy quality without requiring frequent clinic visits. Virtual pulmonary rehabilitation that pairs app-based programs with Bluetooth spirometers is now a recognized option in chronic care plans, which supports better continuity for patients who face travel or scheduling barriers. Direct-to-consumer channels are expanding access to sleep apnea for tech-savvy patients who prefer app guidance and remote follow-up. However, providers remain central to diagnosis and long-term prescription management. These care shifts, together with connected monitoring, continue to position the Australia respiratory devices market for sustained growth in devices and services purpose-built for home use and proactive clinical oversight.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront cost of advanced devices | -0.8% | National, with disproportionate impact on low-income and rural populations | Medium term (2-4 years) |

| Stringent post-market surveillance & UDI compliance | -0.5% | National, affecting all manufacturers in Australian Register of Therapeutic Goods | Short term (≤ 2 years) |

| Semiconductor supply constraints | -0.3% | National, with spillover effects from global supply chain disruptions | Short term (≤ 2 years) |

| Sparse remote-servicing infrastructure in rural areas | -0.6% | Rural and remote Australia, including Northern Territory and Western Australia regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Devices

High acquisition costs for advanced devices make access uneven across income bands and geographies, especially when home-use equipment lacks a consistent public subsidy. While hospital procurement can amortize capital over multi-year cycles, patients who require personal CPAP or portable oxygen for home use face meaningful out-of-pocket exposure and variable private insurance coverage. Regulatory fee schedules also flow into end-user pricing and distributor margins, since manufacturers pass through TGA cost-recovery charges that scale with application complexity. Tiered application fees create hurdles for smaller suppliers of low-volume specialty devices, which can limit competition in narrow subcategories where clinical needs are acute. As a result, procurement teams and providers weigh the total cost of ownership and service reliability when choosing between premium connected platforms and more basic alternatives. The Australia respiratory devices market continues to benefit from telehealth-driven efficiency, but affordability barriers temper the pace of penetration in segments that rely on self-funding.

Stringent Post-Market Surveillance & UDI Compliance

Mandatory UDI labeling from 1 July 2026 for Class III and IIb devices requires end-to-end traceability, with data captured in the national AusUDID and retention periods that extend several years, adding direct compliance tasks across engineering, operations, and IT.[3]Therapeutic Goods Administration, “Priority Review Pathway,” Therapeutic Goods Administration, tga.gov.au TGA’s active post-market stance has been visible in its enforcement related to PE-PUR foam issues in specific Philips devices, including infringement notices in 2024 for failures to provide timely information. Conditions of inclusion may require recurring safety reporting and patient communications, which diverts resources from new product development while remediation programs are underway. The Software as a Medical Device guidance has clarified expectations for clinical evaluation and change control, affecting connected platforms that update algorithms post-market. The regulatory framework rewards suppliers with strong quality systems and local regulatory teams, but near-term compliance steps can strain mid-market players that lack scale. Over time, stricter traceability improves recall efficiency and patient safety, which supports confidence in connected solutions across the Australia respiratory devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Devices Lead, Disposables Surge

Therapeutic devices commanded 48.67% of the Australia respiratory devices market size in 2025, reflecting the central role of CPAP and BiPAP platforms in sleep-disordered breathing and chronic respiratory care. This dominance is reinforced by the ongoing adoption of connected CPAP systems that enable remote titration, nightly adherence tracking, and rapid clinical interventions for therapy adjustment. Disposables are the fastest-growing category, with an 8.80% CAGR through 2031, as infection prevention teams codify single-use practices across ICUs and sleep labs, which increases pull-through for circuits, masks, bacterial filters, and humidification accessories. Nebulizers remain essential for acute management of asthma and COPD exacerbations, with mesh technology gaining share due to quieter operation, rapid aerosol delivery, and better acceptance among children and older adults. Oxygen concentrators benefit from overlapping demand drivers that include COPD progression among older Australians and seasonal smoke or infection surges that spike needs for ambulatory oxygen support. Smart inhalers that incorporate counters and connectivity are expanding in chronic use cases where adherence gaps and technique errors have historically driven preventable exacerbations. Together, these factors keep the therapeutic, disposable, and monitoring subcategories aligned with the connectivity trend that now defines leadership in the Australia respiratory devices market.

By End-User: Home Healthcare Gains as Hospitals Dominate

Hospitals and clinics held a 61.05% share of the Australia respiratory devices market in 2025, as high-acuity ventilators, anesthesia workstations, and polysomnography systems remain anchored in inpatient and specialist settings. These facilities also standardize on integrated monitoring that pulls vital signs and respiratory data into centralized platforms, which creates switching costs that favor established device ecosystems. At the same time, home healthcare is growing at a 10.40% CAGR through 2031 as permanent Medicare telehealth items support remote consultations, CPAP titration, and virtual follow-up for stable chronic conditions. This tilt toward the home opens opportunities for remote setup, digital adherence support, and proactive troubleshooting by vendors and providers. Ambulatory surgical centers increase the adoption of portable anesthesia and basic respiratory monitoring for day procedures, although clinical scope rules limit the complexity of cases managed outside hospitals. Aged-care operators are raising device density per bed, given the growth in residents with COPD and chronic heart failure, and they prefer options that integrate with electronic medication records to streamline workflows.

By Disease Indication: COPD Dominates, Pediatric Asthma Accelerates

COPD accounted for 32.34% of disease-indication share in 2025, which aligns with the condition’s high prevalence among older Australians and its contribution to hospitalizations and prescription volumes. Elevated COPD risk among lower-income cohorts also concentrates device use in public hospital pathways, reinforcing procurement of nebulizers, oxygen therapy systems, and non-invasive ventilation. Seasonal respiratory infections continue to drive episodic demand for high-flow nasal cannula systems and ventilators, which pressure ICU resources during winter surges. Sleep apnea remains an important therapeutic area, with connected CPAP platforms and masks seeing consistent renewals and upgrades, supported by digital adherence programs. These device needs span acute episodes and chronic management, which strengthens vendor relationships with hospital respiratory departments and primary care practices. Together, these patterns stabilize the Australia respiratory devices market through a mix of recurring disposables and periodic capital replacements.

By Age: Adult Prevalence Meets Pediatric Growth

The adult segment retained 69.80% share in 2025 due to the concentration of COPD, sleep apnea, and chronic asthma in working-age and older groups who typically engage more frequently with health services. COPD prevalence rises with age, which concentrates device needs among Australians 65 and older and reinforces demand for portable oxygen solutions that preserve mobility and social participation. Private insurance uptake among middle-aged cohorts supports access to premium connected CPAP and monitoring devices, though affordability still affects adoption outside major cities. As adults age into higher risk brackets, providers lean on remote monitoring and titration to maintain therapy quality, which favors vendors with robust adherence platforms. Adults also drive throughput in primary care spirometry that supports medication optimization and referral decisions.

Geography Analysis

New South Wales, Victoria, and Queensland together account for the majority of the national demand in 2025, reflecting their population density, hospital capacity, and private insurance penetration, which directs most installed base and service resources to Sydney, Melbourne, and Brisbane. These hubs host core manufacturing, distribution, and service infrastructure, including ResMed’s Sydney presence, which supports rapid fulfillment and inventory resilience amid component volatility. Concentrated specialist networks and home-care providers in these states also accelerate the adoption of connected CPAP platforms and remote monitoring, which reinforces ecosystem lock-in across clinics. Procurement teams in tertiary hospitals tend to prefer vendors with proven integration histories and local repair capability, which strengthens incumbent positions. As a result, the Australian respiratory devices market sees faster refresh cycles and greater adoption of connected features in these metropolitan areas than in the rest of the country.

Competitive Landscape

Market concentration is moderate, as three brands account for the majority of volumes in key categories, while smaller innovators capture niche growth through targeted devices and channel innovation. ResMed, Fisher & Paykel Healthcare, and Philips collectively hold substantial shares across CPAP, humidification, and ventilation. However, recall-related headwinds for specific Philips devices have created white space for challenger brands in sleep and portable oxygen. Local innovators like AirPhysio have carved out positions in mucus clearance, while global players like Inogen remain active in portable oxygen concentrators through differentiated designs and mobility-focused use cases. Across the Australia respiratory devices market, the ability to pair devices with adherence software and service pathways is becoming a key determinant of share gains.

Australia Respiratory Devices Industry Leaders

GSK PLC

GE Healthcare Inc.

Drive Medical (DeVilbiss Healthcare LLC)

Drägerwerk AG & Co. KGaA

Fisher & Paykel Healthcare Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Australia-based 4DMedical Limited announced that its advanced imaging technology, CT:VQ, had received CE Mark certification for commercial use in the European Union. The company promptly initiated the commercial deployment of CT:VQ in one of the world's largest respiratory imaging markets.

- December 2025: AeviceMD Monitoring System, a non-invasive wearable respiratory monitoring solution developed by Singapore-based Aevice Health, has been included in the Australian Register of Therapeutic Goods (ARTG) as a Class IIa medical device. This milestone marks an important step in Aevice Health’s expansion into the Australian market.

- July 2025: AusHealth partnered with Ventora Medical to advance an innovative device that promises to improve breathing support for newborns.

Australia Respiratory Devices Market Report Scope

Respiratory devices include respiratory diagnostic devices, therapeutic devices, and breathing devices for administering long-term artificial respiration. It may also include a breathing apparatus used for resuscitation by forcing oxygen into the lungs of a person who has undergone asphyxia.

The Australia respiratory devices market is segmented by device type, end-user, disease indication, and age. By device type, the market is segmented into diagnostic and monitoring devices, therapeutic devices, and disposables. By end-user, the market is segmented into hospitals & clinics, home healthcare settings, ambulatory surgical centers, and others. By disease indication, the market is segmented into COPD, asthma, sleep apnea, pneumonia & acute respiratory infections, and others. By age, the market is segmented into adult, geriatric, and pediatric. The report offers the value (in USD) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | |

| Peak Flow Meters | |

| Pulse Oximeters | |

| Capnographs | |

| Other Diagnostic & Monitoring | |

| Therapeutic Devices | CPAP Devices |

| BiPAP Devices | |

| Humidifiers | |

| Nebulizers | |

| Oxygen Concentrators | |

| Ventilators | |

| Inhalers | |

| Other Therapeutic Devices | |

| Disposables | Masks |

| Breathing Circuits | |

| Other Disposables |

By End-User

| Hospitals & Clinics |

| Home Healthcare Settings |

| Ambulatory Surgical Centers |

| Others |

By Disease Indication

| COPD |

| Asthma |

| Sleep Apnea |

| Pneumonia & Acute Respiratory Infections |

| Others |

By Age

| Adults |

| Geriatric |

| Pediatric |

| By Device Type | Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | ||

| Peak Flow Meters | ||

| Pulse Oximeters | ||

| Capnographs | ||

| Other Diagnostic & Monitoring | ||

| Therapeutic Devices | CPAP Devices | |

| BiPAP Devices | ||

| Humidifiers | ||

| Nebulizers | ||

| Oxygen Concentrators | ||

| Ventilators | ||

| Inhalers | ||

| Other Therapeutic Devices | ||

| Disposables | Masks | |

| Breathing Circuits | ||

| Other Disposables | ||

| By End-User | Hospitals & Clinics | |

| Home Healthcare Settings | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Disease Indication | COPD | |

| Asthma | ||

| Sleep Apnea | ||

| Pneumonia & Acute Respiratory Infections | ||

| Others | ||

| By Age | Adults | |

| Geriatric | ||

| Pediatric | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Australia respiratory devices market?

The Australia respiratory devices market size is USD 268.26 million in 2026 and is projected to reach USD 370.94 million by 2031 at a 5.55% CAGR.

Which device categories are growing fastest in Australia?

Disposables are the fastest growing category due to infection-control protocols, registering an 8.80% CAGR through 2031, while connected CPAP systems continue to expand adoption for home-based care.

How is government policy influencing demand for respiratory devices in Australia?

The 2025-26 Budget strengthens Medicare telehealth and funds screening programs that lift diagnostic and home-care device use, and NDIS allocations support assistive technologies for eligible participants.

What is driving the shift toward home-based care for sleep apnea and COPD in Australia?

Permanent telehealth items for respiratory consultations, broader virtual rehabilitation options, and connected devices that enable remote titration and adherence management are moving more stable care into homes.

How are TGA regulations affecting respiratory device suppliers in Australia?

Priority Review shortens time-to-approval for qualifying devices while UDI from July 2026 adds traceability requirements, which benefits suppliers with strong quality systems and local regulatory teams.

Which companies hold leading positions in the Australia respiratory devices market?

ResMed and Fisher & Paykel Healthcare are leaders in CPAP, humidification, and interfaces, while Philips is active under ongoing TGA post-market conditions, and challengers like Inogen and AirPhysio are growing in focused segments.

Page last updated on: