United States Diabetes Care Drugs And Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

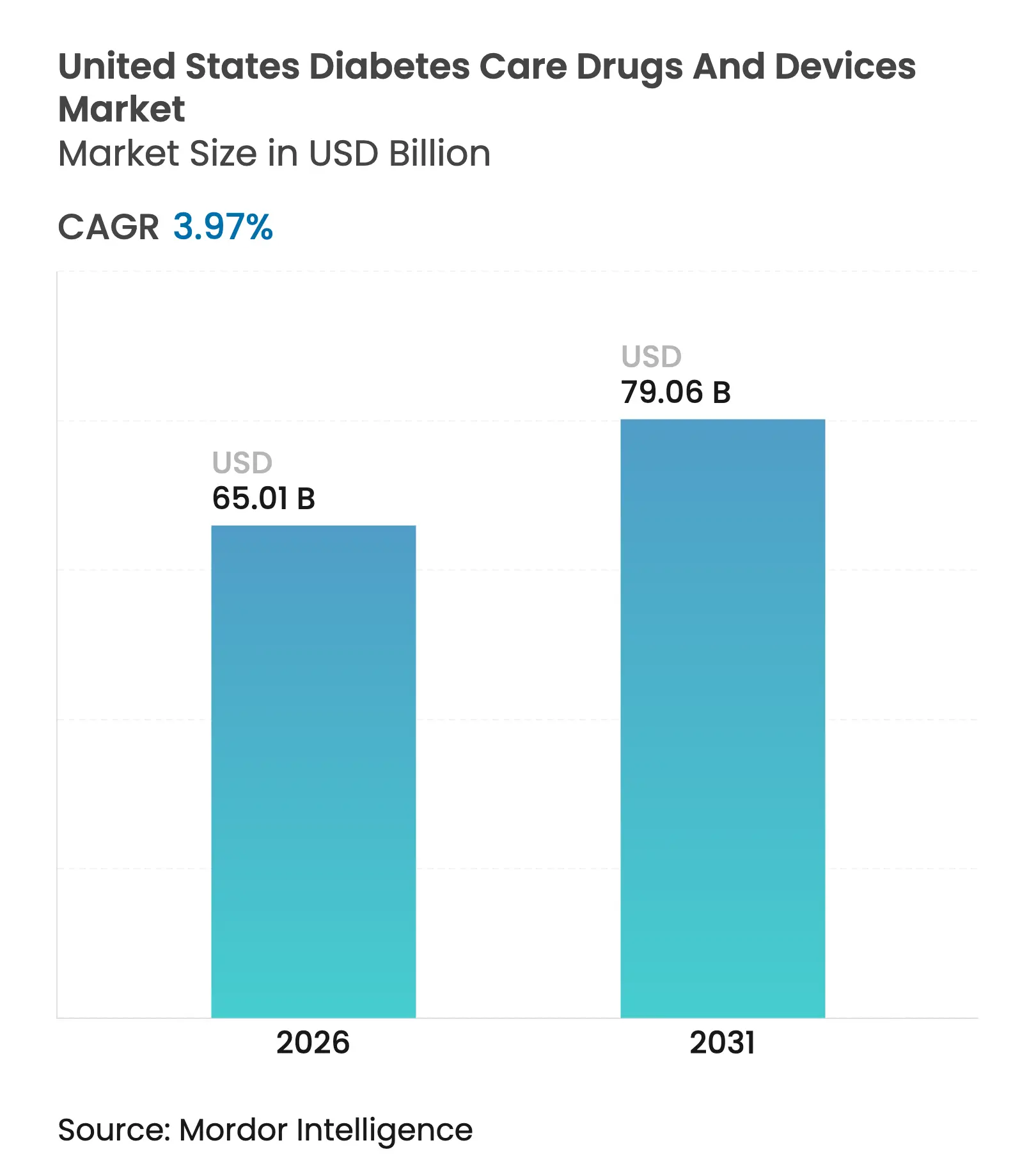

| Market Size (2026) | USD 65.01 Billion |

| Market Size (2031) | USD 79.06 Billion |

| Growth Rate (2026 - 2031) | 3.97 % CAGR |

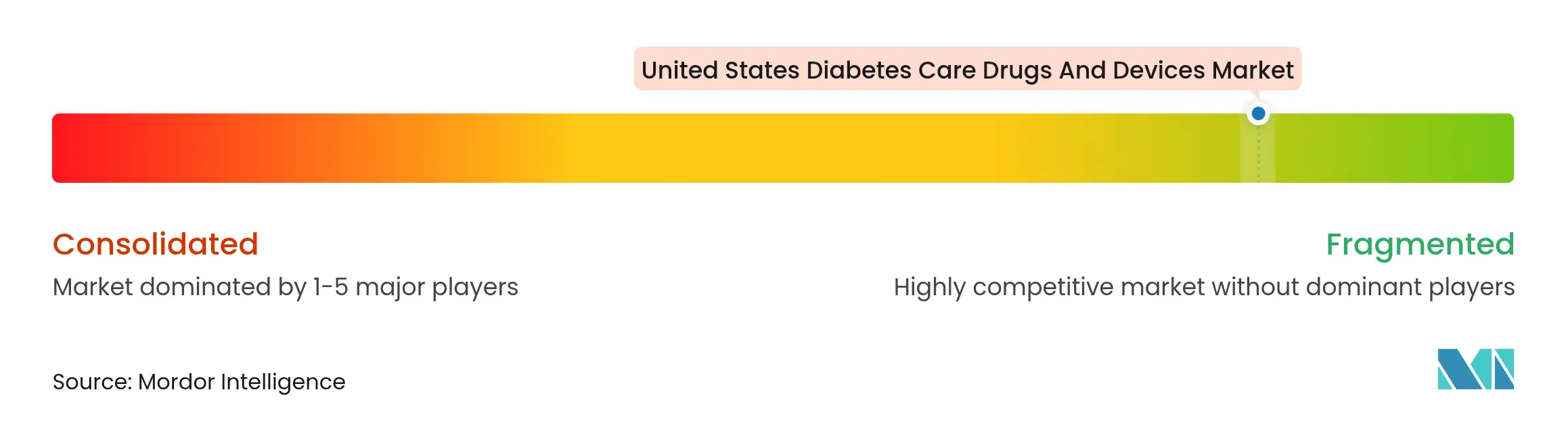

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United States Diabetes Care Drugs And Devices Market Analysis by Mordor Intelligence

The United States diabetes care drugs and devices market size was valued at USD 62.52 billion in 2025 and estimated to grow from USD 65.01 billion in 2026 to reach USD 79.06 billion by 2031, at a CAGR of 3.97% during the forecast period (2026-2031). Growth is steady rather than spectacular because headline figures mask deep structural change. Blockbuster GLP-1 receptor agonists are up-ending therapy mix, while consumer-grade continuous glucose monitors (CGMs) redraw device adoption curves. Medicare’s USD 35 insulin cap, wider CGM reimbursement, and the Food and Drug Administration’s (FDA) approval of over-the-counter (OTC) CGMs collectively lower access barriers, accelerating penetration among Type 2 diabetes patients who previously relied on finger-stick testing. At the same time, vertical integration among retail pharmacy benefit managers (PBMs) steers formularies toward preferred biosimilar insulins, compressing incumbent gross margins but freeing household budgets for advanced devices. Competitive intensity is rising as patent cliffs trigger pricing wars and supply constraints for GLP-1s open share opportunities. Privacy concerns over real-time glucose data monetization and stricter FDA oversight of closed-loop algorithms temper the outlook but do not derail the pivot toward predictive, automated management tools that blend sensors, dosing hardware, and software analytics.

Key Report Takeaways

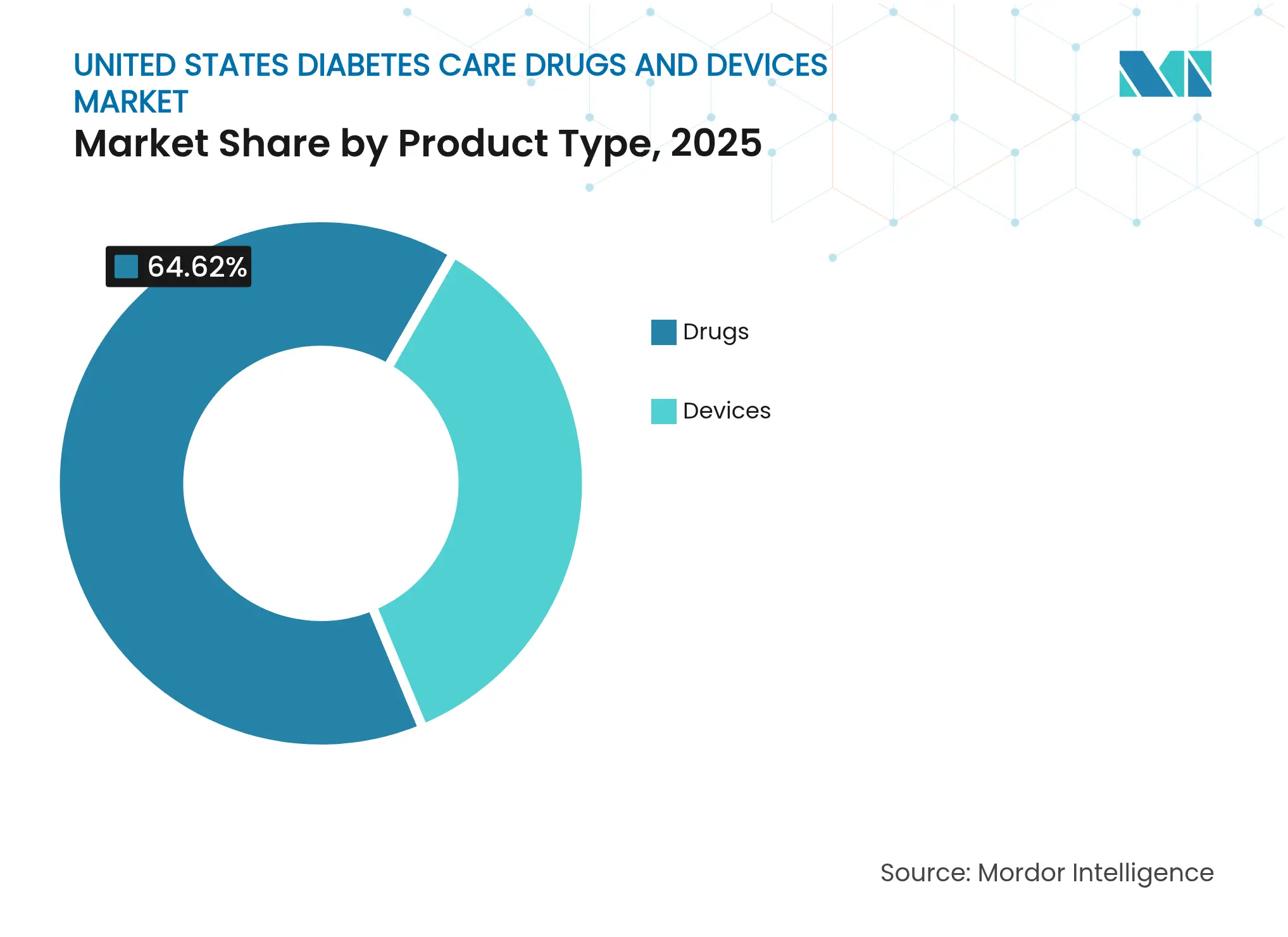

- By product type, devices captured 35.38% revenue in 2025 while drugs dominated with 64.62%; devices are projected to expand at a 4.72% CAGR through 2031, the fastest among all categories.

- By diabetes type, Type 1 diabetes accounted for 9.69% of patients yet led innovation with a 4.53% CAGR, whereas Type 2 retained 90.31% volume but expanded more modestly.

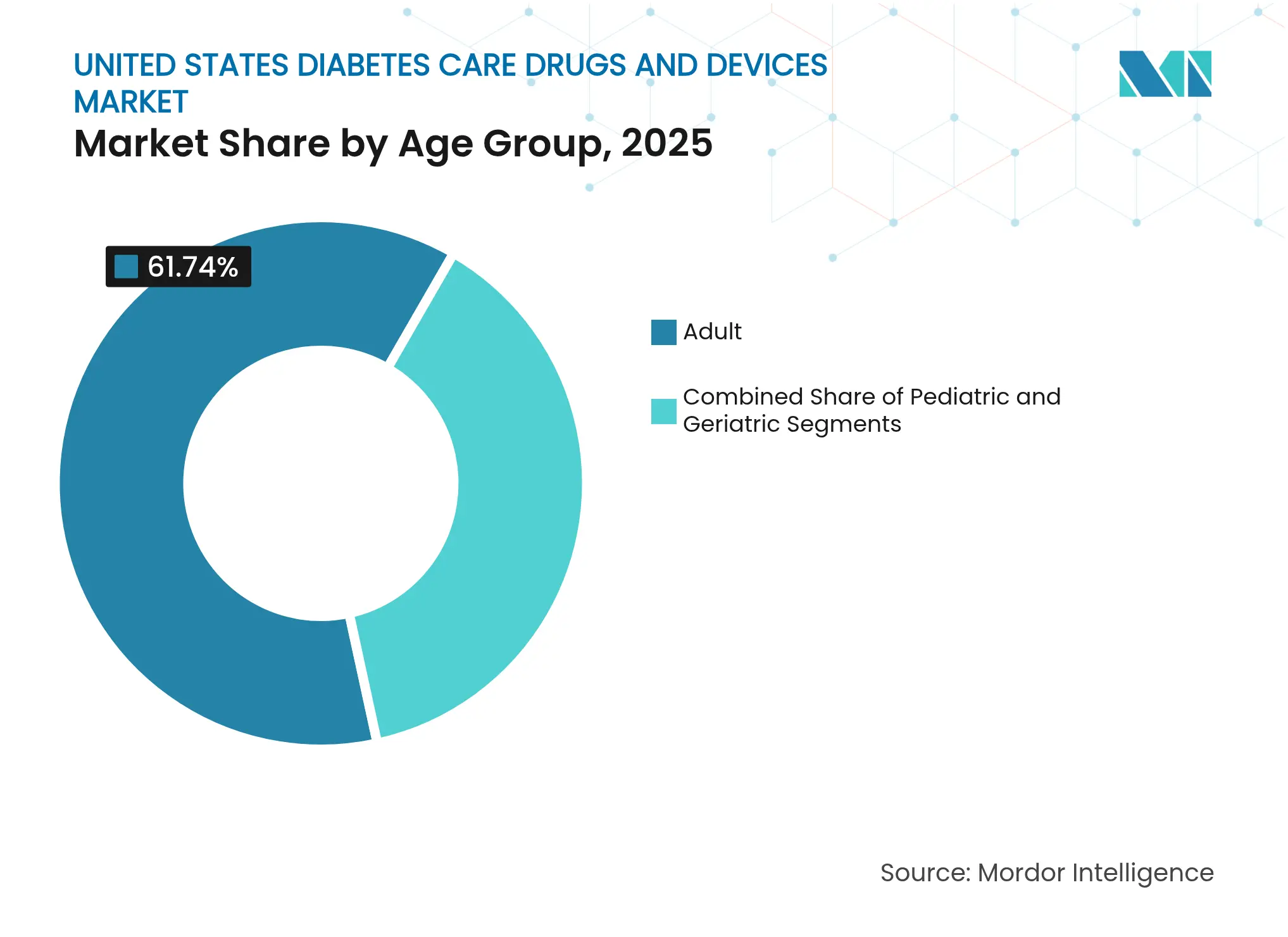

- By age group, the geriatric cohort drove 4.66% growth owing to Medicare coverage, while adults maintained 61.74% revenue share in 2025.

- By distribution channel, online platforms held 25.34% revenue in 2025 and are advancing at 4.86% CAGR as direct-to-consumer models take hold.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Diabetes Care Drugs And Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Blockbuster GLP-1 approvals & formulary uptake

Blockbuster GLP-1 approvals & formulary uptake

| +1.2% | National, strongest in Medicare Advantage plans | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

National, strongest in Medicare Advantage plans

|

Impact Timeline

:

Medium term (2-4 years)

|

Shift to consumer-grade CGMs

Shift to consumer-grade CGMs

| +0.8% | National, early adoption in urban markets | Short term (≤ 2 years) | |||

Medicare expansion for insulin cap & CGM reimbursement

Medicare expansion for insulin cap & CGM reimbursement

| +0.6% | National, marked benefit in rural areas | Medium term (2-4 years) | |||

Retail pharmacy PBM vertical integration &

preferred-drug steering

Retail pharmacy PBM vertical integration &

preferred-drug steering

| +0.4% | National, varies by PBM dominance | Long term (≥ 4 years) | |||

Patent cliff for basal insulins

Patent cliff for basal insulins

| +0.3% | National, rapid uptake in cost-focused systems | Short term (≤ 2 years) | |||

AI-driven closed-loop smart pens & phone ecosystems

AI-driven closed-loop smart pens & phone ecosystems

| +0.5% | National, early wins in tech hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Blockbuster GLP-1 Approvals & Formulary Uptake

GLP-1 receptor agonists such as tirzepatide are reshaping metabolic disease treatment by curbing progression from pre-diabetes and driving durable weight loss. Medicare Part D and major PBM formularies now prioritize these agents despite higher list prices because real-world studies show lower total cost of care via reduced complications. Integration with CGM data is improving adherence, while oral and once-weekly formulations in late-stage trials promise further convenience. The ripple effect is declining reliance on multiple daily injections and oral anti-diabetic agents, redirecting manufacturer R&D budgets toward combination therapies and precision dosing platforms.

Shift to Consumer-Grade CGMs

FDA authorization for OTC CGMs from Abbott and Dexcom eliminates prescription hurdles, expanding the addressable pool from 6 million insulin users to more than 25 million Type 2 diabetes patients who do not require insulin [1]FDA, "FDA Clears First Over-the-Counter Continuous Glucose Monitor," fda.gov. Simpler insertion, smartphone interfaces, and wellness positioning are catalyzing uptake among health-conscious consumers tracking metabolic health. Medicaid evidence reviews supporting cost-effectiveness strengthen payer confidence, and longer-wear sensors reduce per-patient supply costs [2]Washington State Health Care Authority, “Continuous Glucose Monitoring Cost-Effectiveness Review,” hca.wa.gov . Device makers are leveraging subscription models and lifestyle apps to sustain engagement.

Medicare Expansion for Insulin Cap & CGM Reimbursement

The USD 35 monthly cap on insulin under Medicare Parts B and D yields immediate savings for 3.3 million beneficiaries and sets a de facto benchmark for commercial insurers. Reclassifying CGMs as durable medical equipment simplifies coverage and removes prior authorization delays. Together, these policies elevate uptake among older adults and rural populations historically constrained by out-of-pocket costs. Commercial plans often mirror Medicare policy, amplifying nationwide impact.

Retail Pharmacy PBM Vertical Integration & Preferred-Drug Steering

Four integrated PBMs control 70% of national prescription volume, allowing them to favor high-rebate products and biosimilars that maximize spread pricing. Biosimilar insulin adoption is accelerating in cost-sensitive health systems, but formulary exclusions of certain branded GLP-1s and older DPP-4 inhibitors shift market share overnight. Legislative scrutiny and an ongoing Federal Trade Commission investigation could modify rebate contracting rules, potentially altering near-term pricing power.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

GLP-1–driven fall-off in daily glucose testing

GLP-1–driven fall-off in daily glucose testing

| -0.7% | National, largest in Type 2 cohort | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

National, largest in Type 2 cohort

|

Impact Timeline

:

Medium term (2-4 years)

|

FDA safety overhang on once-weekly insulin icodec

FDA safety overhang on once-weekly insulin icodec

| -0.3% | National, affects innovation funding | Short term (≤ 2 years) | |||

Persistent OOP costs for next-gen pumps

Persistent OOP costs for next-gen pumps

| -0.4% | National, varies by employer plans | Long term (≥ 4 years) | |||

Privacy push-back on real-time glucose data

Privacy push-back on real-time glucose data

| -0.2% | National, stronger in privacy-aware groups | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

GLP-1–Driven Fall-off in Daily Glucose Testing Frequency

As GLP-1 therapies stabilize glycemia, many Type 2 diabetes patients reduce finger-stick testing, eroding sales of test strips and lancets. Insulin pump initiation can also be deferred when HbA1c targets are met through weight loss and improved insulin sensitivity. Manufacturers are pivoting toward multi-parameter sensors and coaching platforms to offset shrinking single-use supply volumes.

FDA Safety Overhang on Once-Weekly Insulin Icodec for T1D

The FDA rejected Novo Nordisk’s once-weekly insulin icodec for Type 1 diabetes over hypoglycemia and manufacturing issues. Advisory committee caution extends to rival programs, raising bar for long-acting formulations. Developers may need additional trials and manufacturing validation, delaying potential market entry and sustaining dependence on daily basal analogues.

Segment Analysis

By Product Type: Devices Drive Innovation Despite Drug Dominance

Drugs held a market share of 64.62% in the United States diabetes care drugs and devices market. Devices contributed USD 22.12 billion in 2025 and are forecast to grow at 4.72% annually, well above the broader United States diabetes care drugs and devices market. Continuous monitoring platforms account for most incremental revenue as OTC CGMs permeate the Type 2 population and sensor wear time extends to 15 days. Automated delivery systems such as Tandem’s t:slim X2 and Insulet’s Omnipod 5 gain regulatory clearance for Type 2 diabetes, doubling their eligible pool. In contrast, the drug category expands slowly because biosimilar basal insulins compress prices even as GLP-1s climb the formulary.

Sensor-linked pumps enable algorithmic micro-bolusing and attract premium reimbursement. Abbott’s Libre Rio addresses clinical users while its Lingo targets wellness, illustrating a bifurcated go-to-market strategy that maximizes both prescription and retail channels. CGM makers increasingly bundle data analytics, subscription coaching, and lifestyle content to mitigate margin pressure on hardware. Across therapy classes, ecosystem lock-in—rather than standalone hardware—drives competitive advantage in the United States diabetes care drugs and devices market .

Note: Segment shares of all individual segments available upon report purchase

By Diabetes Type: Type 1 Innovation Leads Market Evolution

Type 1 diabetes generated USD 6.06 billion in 2025 and is advancing at 4.53% CAGR through 2031, outpacing the overall United States diabetes care drugs and devices market. High technology acceptance, willingness to pay, and the clinical necessity of tight glucose control underpin device penetration exceeding 75%. Tandem’s Control-IQ+ algorithm and Medtronic’s MiniMed 780G now extend closed-loop automation to younger age groups, further elevating Type 1 adoption curves.

Type 2 diabetes held 90.31% market share in 2025 and commands the bulk of revenue but faces decelerating volume growth due to aggressive prevention campaigns and evidence that tirzepatide cuts diabetes onset by 94%. Nonetheless, opportunity remains in early-stage Type 2 patients seeking metabolic insight; OTC CGMs and weight-management GLP-1s meet that demand. Device firms pilot lower-cost pump subscription models for insulin-requiring Type 2 patients, potentially lifting future United States diabetes care drugs and devices market size for this segment.

By Age Group: Geriatric Surge Drives Technology Adoption

The geriatric segment will expand at 4.66% CAGR. Medicare’s insulin cap, durable medical equipment designation for CGMs, and the FDA’s Health Care at Home initiative remove historic barriers to tech adoption. Simplified user interfaces, voice prompts, and auto-insert sensors suit cognitive and dexterity limitations common in older adults.

The adult cohort (18–64 years) remains the largest contributor to the United States diabetes care drugs and devices market size, holding 61.74% market share in 2025, sustained by employer insurance coverage and early uptake of wellness-focused CGMs. Pediatric growth is smaller numerically but strategically important; devices engineered for family oversight often inform broader platform design, enhancing overall ecosystem competitiveness.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates

Offline pharmacy and hospital channels still controlled 74.66% of 2025 revenue, yet online sales grew 4.86% annually and will surpass USD 21.04 billion by 2031. Direct-to-consumer storefronts for CGMs and smart pens reduce reliance on PBMs, while tele-prescribing services improve regional access. Manufacturers bundle sensors with virtual coaching subscriptions that ship supplies automatically, raising retention.

PBM formulary steering motivates device makers to court self-pay consumers through e-commerce, a tactic evident in Dexcom’s Stelo launch. Hybrid fulfillment models—online ordering with in-store pickup—help pharmacies retain foot traffic. Channel diversification decreases rebate leakage and expands margin capture across the United States diabetes care drugs and devices market.

Geography Analysis

Regional adoption patterns reflect income, payer mix, and infrastructure gaps. Medicare-led insulin and CGM reforms most profoundly affect the South and Midwest, where diabetes prevalence and lower incomes magnify out-of-pocket sensitivity. Rural clinics leverage remote monitoring to overcome specialist shortages, aligning with the FDA’s home-based care pilots.

Urban centers on the coasts adopt OTC CGMs fastest due to tech literacy and wellness trends. Employer self-insured plans in these regions frequently reimburse GLP-1s for obesity management, boosting early volume. Conversely, PBM concentration in certain states dictates formulary variation; single-PBM dominance can limit GLP-1 access yet encourage biosimilar insulin use.

State policy activism also shapes geography. California’s plan to manufacture low-cost insulin could upend pricing once capacity comes online. Meanwhile, Medicaid expansions in Washington and Colorado widen CGM eligibility, fostering device penetration beyond Medicare. Health-system consolidation in the Northeast supports bulk procurement of integrated device-drug ecosystems, advancing closed-loop adoption. Together, these regional vectors drive a patchwork growth profile inside the United States diabetes care drugs and devices market.

Competitive Landscape

Market Concentration

Abbott and Dexcom dominate sensing; Medtronic, Tandem, and Insulet lead pumps; Novo Nordisk and Eli Lilly command injectable therapies. Co-development deals such as Abbott’s integration with Tandem pumps illustrate convergence, as firms seek end-to-end solutions.

Patent cliffs for Lantus and other basal insulins unleash biosimilar entrants like Viatris, intensifying price wars. GLP-1 demand outstrips supply, prompting manufacturers to invest in capacity while competitors aim for next-generation dual-agonists. Device companies face FDA scrutiny of manufacturing controls, evidenced by Dexcom’s 2025 warning letter that forced corrective actions.

Non-traditional players—digital health start-ups and big-tech partners—deploy AI algorithms predicting glucose excursions an hour in advance, offering subscription dashboards. Interoperability guidelines allow smaller sensor or algorithm firms to plug into established pump ecosystems, lowering barriers. Privacy regulation remains a wild card; strict consent rules could crimp data-monetization strategies that subsidize hardware costs across the United States diabetes care drugs and devices market.

United States Diabetes Care Drugs And Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tandem Diabetes Care announced t:slim X2 pump compatibility with Abbott FreeStyle Libre 3 Plus 15-day sensor, targeting commercial release in H2 2025.

- April 2025: Medtronic gained FDA clearance for Simplera Sync sensor integration with MiniMed 780G, eliminating finger-stick calibration.

- March 2025: FDA issued warning letter to Dexcom citing G6 and G7 process-control deficiencies, requiring remediation to avoid sanctions.

- February 2025: Tandem secured FDA clearance for Control-IQ+ algorithm in Type 2 diabetes, expanding its addressable base by more than 2 million users.

Table of Contents for United States Diabetes Care Drugs And Devices Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Blockbuster GLP-1 approvals & formulary uptake

- 4.2.2Shift to consumer-grade CGMs

- 4.2.3Medicare expansion for insulin cap & CGM reimbursement

- 4.2.4Retail pharmacy PBM vertical integration & preferred?drug steering

- 4.2.5Patent cliff for basal insulins opening biosimilar pricing wars

- 4.2.6AI-driven closed-loop for smart pens and phone ecosystems

- 4.3Market Restraints

- 4.3.1GLP-1 driven fall-off in daily glucose testing frequency

- 4.3.2FDA safety overhang on once-weekly insulin icodec for T1D

- 4.3.3Persistent out-of-pocket costs for next-gen pumps in commercial plans

- 4.3.4Privacy push-back on real-time glucose data monetisation

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porters Five Forces Analysis

- 4.6.1Bargaining Power of Suppliers

- 4.6.2Bargaining Power of Consumers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Devices

- 5.1.1.1Monitoring Devices

- 5.1.1.1.1Self-Monitoring Blood Glucose Meters

- 5.1.1.1.2Continuous Glucose Monitoring Systems

- 5.1.1.2Management Devices

- 5.1.2Drugs

- 5.1.2.1Oral Anti-Diabetic Drugs

- 5.1.2.2Insulin Drugs

- 5.1.2.3Non-Insulin Injectables

- 5.1.2.4Combination Drugs

- 5.2By Diabetes Type

- 5.2.1Type 1 Diabetes

- 5.2.2Type 2 Diabetes

- 5.3By Age Group

- 5.3.1Adult

- 5.3.2Geriatric

- 5.3.3Pediatric

- 5.4By Distribution Channel

- 5.4.1Offline

- 5.4.2Online

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Abbott Laboratories

- 6.3.2Medtronic plc

- 6.3.3Dexcom Inc.

- 6.3.4F. Hoffmann-La Roche AG

- 6.3.5Tandem Diabetes Care

- 6.3.6Insulet Corporation

- 6.3.7Novo Nordisk A/S

- 6.3.8Eli Lilly and Company

- 6.3.9Sanofi

- 6.3.10AstraZeneca plc

- 6.3.11Pfizer Inc.

- 6.3.12Ypsomed AG

- 6.3.13Ascensia Diabetes Care

- 6.3.14Becton Dickinson & Co.

- 6.3.15Glooko Inc.

- 6.3.16Senseonics Holdings

- 6.3.17Beta Bionics

- 6.3.18Bigfoot Biomedical

- 6.3.19Valeritas Inc.

- 6.3.20MannKind Corporation

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product Type

- Devices

- Monitoring Devices

- Self-Monitoring Blood Glucose Meters

- Continuous Glucose Monitoring Systems

- Self-Monitoring Blood Glucose Meters

- Management Devices

- Monitoring Devices

- Drugs

- Oral Anti-Diabetic Drugs

- Insulin Drugs

- Non-Insulin Injectables

- Combination Drugs

- Oral Anti-Diabetic Drugs

- Devices

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- Type 1 Diabetes

- By Age Group

- Adult

- Geriatric

- Pediatric

- Adult

- By Distribution Channel

- Offline

- Online

- Offline

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's US Diabetes Drugs and Devices Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 62.52 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 54.84 B (2024) | Global Consultancy A | Excludes consumer CGM sensors and uses list prices only | ||

USD 48.00 B (2024) | Industry Association B | Focuses on retail channels, omits hospital pump sales and limited primary checks |