Denmark Organic Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

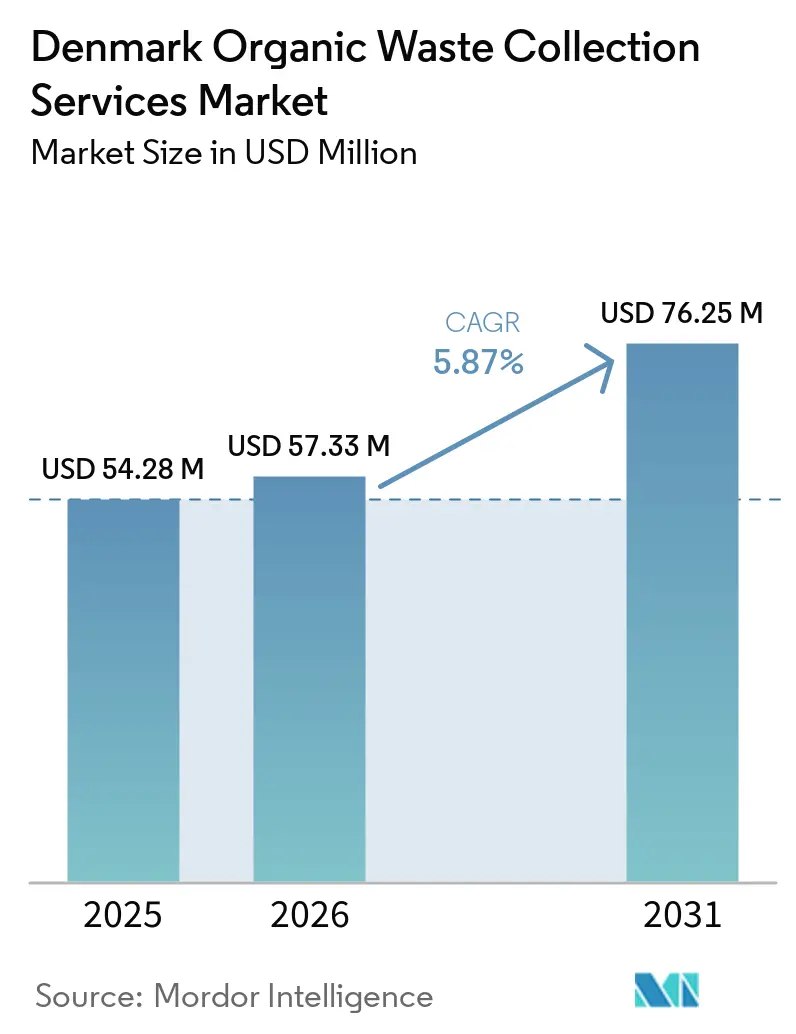

| Base Year Market Size (2025) | USD 54.28 Million |

| Market Size (2026) | USD 57.33 Million |

| Market Size (2031) | USD 76.25 Million |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

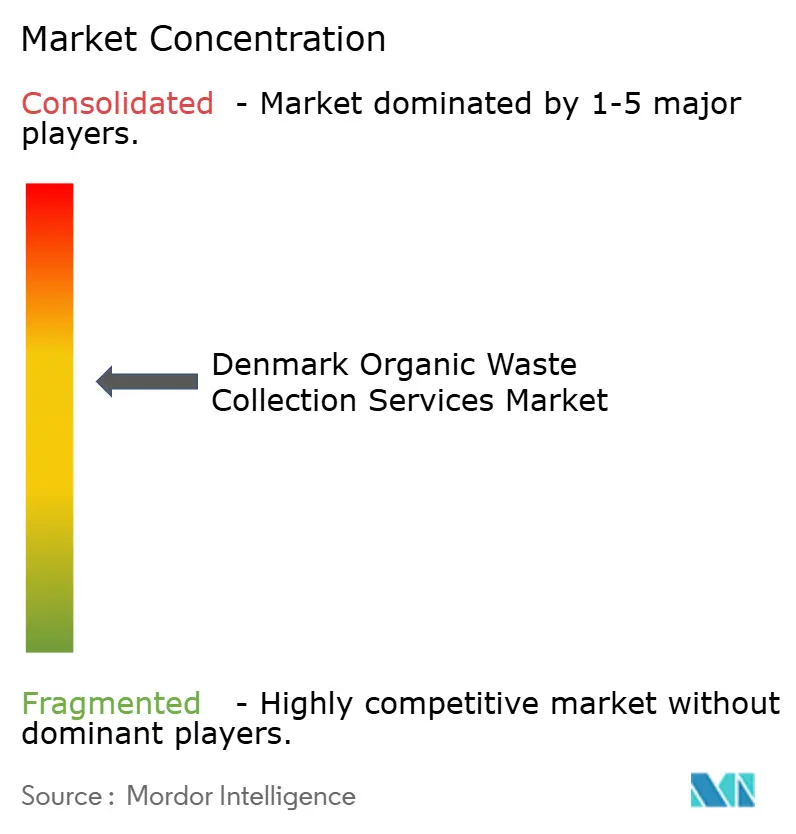

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Organic Waste Collection Services Market Analysis by Mordor Intelligence

The Denmark Organic Waste Collection Services Market size was valued at USD 54.28 million in 2025 and is estimated to grow from USD 57.33 million in 2026 to reach USD 76.25 million by 2031, at a CAGR of 5.87% during the forecast period (2026-2031).

Policy certainty anchors growth, as Denmark’s climate-neutrality target for 2045 and the nationwide ten-fraction separate collection mandate, fully implemented by 2025, reinforce stable, long-term demand for collection services. The Denmark organic waste collection services market benefits from energy transition tailwinds as biomethane supplied almost 40% of the national gas system in 2023, and the country targets 100% green gas by 2030, which improves feedstock economics for source-separated organics routed to anaerobic digestion. Operators modernize logistics with AI and IoT, as municipalities like Vejle report 30% driving reductions and 5.5 tonnes of annual CO2 savings from dynamic, sensor-driven routing, which reduces operating costs and fuel exposure for fleets serving distributed residential and commercial customers. Elevated municipal waste generation at 755 kg per capita in 2024 sustains collection volumes. Still, it increases contamination control costs, requiring stronger quality systems and resident engagement to protect digester performance and recycling outcomes. New environmental taxation, including the June 2024 Green Tripartite Agreement’s CO2e tax on agricultural emissions from 2030, strengthens the business case for routing organic material to biogas plants, thereby shifting feedstock competition in favor of collection operators that guarantee high-purity streams.

Key Report Takeaways

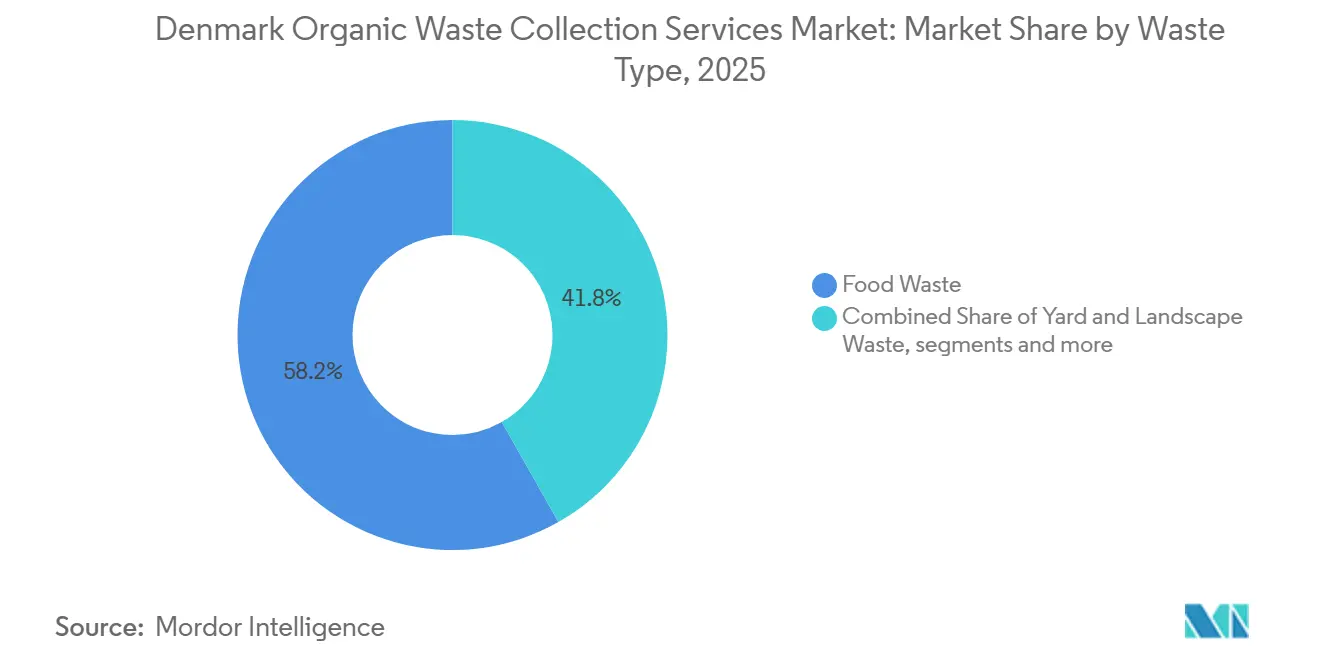

- By waste type, food waste accounted for 58.2% of the Denmark organic waste collection services market share in 2025 and is forecast to grow at a 6.78% CAGR through 2031.

- By end-user, residential accounted for 62.4% of the Denmark organic waste collection services market size in 2025, while commercial food service is projected to expand at a 7.46% CAGR to 2031.

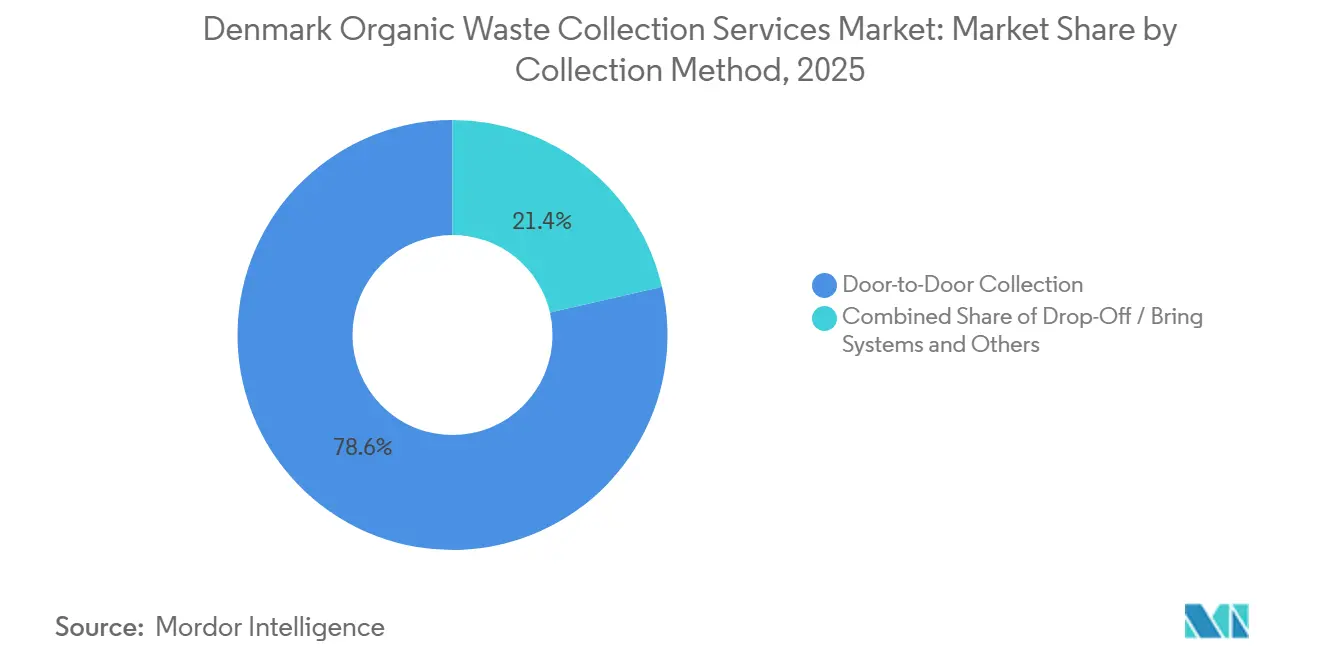

- By collection method, door-to-door commanded a 78.6% share in 2025 and is also advancing at a 7.81% CAGR through 2031.

- By technology and equipment, semi-automated systems held a 68.9% market share in 2025, while fully automated systems are projected to grow at an 8.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Denmark Organic Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Separate Collection Regulations | +2.1% | National, with accelerated compliance in Copenhagen, Roskilde, Aarhus urban cores | Medium term (2-4 years) |

| Circular Economy Action Plan and National Waste Strategy | +1.6% | National policy framework, strongest enforcement in Copenhagen metropolitan region | Medium term (2-4 years) |

| Advanced Biogas Infrastructure and Energy Security | +1.3% | National grid integration; concentrated capacity in Western Denmark (agricultural density zones) | Long term (≥ 4 years) |

| Economic Incentives and Environmental Taxes | +0.9% | National; agricultural CO2e tax most impactful in Jutland livestock regions | Medium term (2-4 years) |

| Nutrient Recovery and Circular Fertilizer Markets | +0.5% | National, with spillover to agricultural municipalities prioritizing nitrogen reduction compliance | Long term (≥ 4 years) |

| Climate Neutrality Targets and GHG Reduction | +0.4% | National Climate Act obligations; municipal-level differentiation in implementation rigor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Separate Collection Regulations

Denmark’s 2020 Statutory Order on Waste established a harmonized ten-fraction framework that includes food waste, driving a uniform door-to-door collection baseline across all 98 municipalities and ending regulatory fragmentation that had hindered consistent service standards[1]European Environment Agency, “Municipal and Packaging Waste Management Country Profiles 2025: Denmark,” European Environment Agency, eea.europa.eu.. By December 2023, 80 municipalities had reached full compliance, and the remaining municipalities completed implementation by 2025, enabling operators to scale standardized container formats, contamination controls, and service frequencies for the Denmark organic waste collection services market. Egedal Kommune’s 2024 household waste regulation codified two-chamber bins with a 60% residual and 40% food waste split for single-family homes, biweekly pickup, and mandatory green bags for food waste, which increased predictability for route planning and equipment specifications. From January 2026, Affaldsdatasystemet requires annual reporting of quantities, EAK codes, and treatment methods, with food waste digestion considered recycling only when digestate is land-applied, thereby supporting traceability and quality-driven tender criteria in the Denmark organic waste collection services market. Copenhagen’s draft Resource and Waste Plan 2025-2030 targets 60% real recycling from 2030 and reported collecting over 15,000 tonnes of food waste in 2023, underscoring the scale of capture potential in dense urban areas and signaling tightening enforcement against mis-sorting. IoT adoption and dynamic routing further align municipal obligations with operator efficiency, as seen in Vejle’s 30% reduction in collection driving and 5.5 tonnes of CO2 savings through sensor-triggered logistics, which supports cost and climate objectives in the Denmark organic waste collection services market.

Circular Economy Action Plan and National Waste Strategy

The Circular Economy Action Plan 2020-2032 set out 129 initiatives with 79 completed by April 2024, which included measures for biomass valorization and household food waste reduction that reinforce consistent feedstock flows to digestion and composting in the Denmark organic waste collection services market. Denmark’s National Strategy for Fighting Food Waste 2024-2027, led by the Danish Veterinary and Food Administration, allocated USD 3.3 million to 15 initiatives that support data collection, pilots, and consumer outreach, thereby improving upstream sorting and reducing contamination risk in municipal organics streams. Roskilde Kommune’s frontrunner performance with 60% household recycling in 2023 and 5,170 tonnes of food waste collected shows how local planning, service design, and processing partnerships can achieve high capture and real recycling rates for the Denmark organic waste collection services market. The national shift to competitive tendering for recyclable waste treatment from 2025 opens processing choices while Extended Producer Responsibility for packaging, effective in 2025, increases accountability for packaging design and end-of-life outcomes that intersect with organic waste collection schemes. Verdis’ selection in February 2025 as Denmark’s central sorting partner for plastics, metals, and cartons, at 8,500 tonnes per year from October 2025, illustrates how centralized sorting partnerships can improve quality and traceability, complementing municipal organics programs in the Denmark organic waste collection services market. Innovation projects that link organics to higher-value outputs, such as biogas-to-protein concepts with CO2 capture, signal a pathway to improve gross margins per tonne handled without deviating from collection mandates that guide service design in cities and towns.

Advanced Biogas Infrastructure and Energy Security

Denmark operates about 150 biogas plants and reached close to 40% biomethane in the gas system in 2023, while targeting 100% green gas consumption by 2030, linking organic waste collection to national energy security and decarbonization plans. Grid connectivity is mature, with 57 plants tied to the distribution network and one to transmission, which reduces haul distances and supports stable gate fee structures for food and yard waste delivered from municipal schemes in the Denmark organic waste collection services market. Tønder Biogas, inaugurated in May 2025, processes 930,000 tonnes of biomass annually into more than 41 million Nm³ of methane and captures 48,000 tonnes of liquid CO2 for synthetic fuel, which demonstrates industrial-scale integration that raises downstream demand for high-quality organic feedstock. Copenhagen’s 2025-2030 plan considers pathways for mechanically separated food waste to complement source-separated streams, increasing flexibility to achieve higher capture rates while maintaining quality targets for digestion outputs. Methane slip regulations introduced in 2023, with a 1% leakage target from 2024, require plant inspections and drive performance improvements that maintain the greenhouse gas advantage of biomethane relative to fossil gas, thereby sustaining premium pricing and supporting robust organics. Limits on energy crops from 2025, including a 4% cap and a ban on corn, prioritize waste-based feedstocks and favor food waste, yard waste, and agricultural residues sourced through compliant collection routes across the Denmark organic waste collection services market.

Economic Incentives and Environmental Taxes

A landfill tax of USD 74.8 per tonne, an incineration tax of USD 8.3 per GJ on residual municipal waste, and a CO2 tax of USD 28.2 per tonne on non-biodegradable incinerated waste design a price signal that favors organics collection for recycling and digestion pathways. Biogas production from food waste qualifies as recycling under the Affaldsdatasystemet regulation, effective from January 2026, which aligns fiscal incentives with circular outcomes in the Denmark organic waste collection services market. The June 2024 Green Tripartite Agreement introduces an agricultural CO2e tax of USD 47.3 per tonne in 2030, with a 60% allowance that reduces effective rates, nudging manure and co-digestion strategies that raise demand for clean organic waste inputs. Pay-as-you-throw schemes expand across large portions of the population, which penalize mis-sorting and increase household participation in organics separation over time in the Denmark organic waste collection services market. Extended Producer Responsibility for packaging from 2025 increases producer accountability and encourages design choices that reduce contamination in organics bins, which supports municipal quality targets and the viability of biogas routes. Together, these incentives strengthen the revenue model for high-purity collection services while raising the cost of disposal routes that erode circular outcomes, which benefits operators positioned for quality and traceability in the Denmark organic waste collection services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highest Per Capita Waste Generation in Europe | -1.4% | National; most pronounced in Greater Copenhagen and holiday home municipalities | Short term (≤ 2 years) |

| Incineration Overcapacity and Economic Lock-in | -1.1% | National; district heating-dependent municipalities face sunk-cost inertia | Medium term (2-4 years) |

| Regulatory Barriers for Mechanically Separated Organic Waste | -0.6% | National; EU classification rules constrain post-collection sorting credit | Medium term (2-4 years) |

| Contamination and Quality Control Challenges | -0.8% | National; variable mis-sorting rates reduce effective recycling | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Highest Per Capita Waste Generation in Europe

Denmark generated 755 kg of municipal waste per capita in 2024, compared with an EU average of 517 kg, which sustains demand for collection services and increases the cost of ensuring high-quality organic fractions during pickup and transfer operations in the Denmark organic waste collection services market[2]Eurostat, “517 kg Municipal Waste Per Capita in 2024,” European Commission, ec.europa.eu.. Despite meaningful progress since 2014, elevated absolute generation continues to flow significant organic content into residual streams, which depresses real recycling rates and complicates digester feedstock planning for operators. Municipal variation is wide, with Fredensborg at 1,203 kg per inhabitant in 2023 and a national household average of 531 kg, complicating the standardization of pricing and the planning of service frequency under competitive tenders in the Denmark organic waste collection services market. Total waste generation excluding soil reached 12.5 million tonnes in 2023, and household waste included a large mixed fraction, indicating persistent opportunities to improve organics capture through bin design, routing, and education. Municipal measures such as green-bag entitlements and overfill penalties seek to stabilize quality and pickup efficiency. Still, they also increase unit costs that operators must manage within price-capped tenders in the Denmark organic waste collection services market.

Incineration Overcapacity and Economic Lock-in

Denmark’s waste-to-energy fleet underpins district heating and electricity supply for hundreds of thousands of households, which creates fiscal and operational incentives to maintain throughput even as national policy aims to reduce incineration capacity by about 30% by 2030. Competitive tendering from 2025 and plant corporatization seek to realign capacity with domestic waste volumes and reduce imports. Still, municipalities with legacy debt tied to tipping fees face financial constraints that can slow organics diversion in the Denmark organic waste collection services market. The trajectory of carbon capture at selected incinerators, energy prices, and import demand introduces uncertainty that some municipalities cite when pacing down residual streams while balancing heat obligations, which sustains pressure on organics collection growth during 2026-2030. An analysis across Europe points to a structural capacity gap by 2035, which reinforces Danish operators’ view that waste-to-energy will remain part of the system even as recycling targets rise and organic diversion expands. In Greater Copenhagen, facilities such as ARC’s Amager Resource Center continue to anchor district heating and materials sorting, which shape local collection priorities and the competitive context for organic feedstock between digestion and incineration. The Denmark organic waste collection services market, therefore, advances within a transition period in which policy, tenders, and infrastructure must align to increase capture while managing energy reliability commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Food Waste Dominance Anchored by Biogas Economics

Food waste accounted for 58.2% of the Denmark organic waste collection services market in 2025 and leads the growth pace at a 6.78% CAGR through 2031, supported by policy, household coverage, and downstream biogas demand that values high-energy organic streams. Roskilde collected 5,170 tonnes of household food waste in 2023, with a high real recycling performance, and Copenhagen reported more than 15,000 tonnes that same year, with further capture potential pending stronger sorting discipline. Reporting obligations that took effect in 2026 classify biogas as recycling when digestate is land-applied, which strengthens the economics for operators channeling food waste to the roughly 150 digestion plants across Denmark. Yard and landscape waste add stable seasonal volumes, with Nordic comparisons noting strong garden waste collection that municipalities integrate through bins and scheduled pickups, which requires flexible fleet utilization for the Denmark organic waste collection services market. Agricultural residues hold a smaller share but gain relevance through limits on energy crops and incentives for manure co-digestion, which increase the value of clean organics, lift methane yield, and support gate fees favorable to collection contracts[3]Københavns Kommune, “Resource and Waste Plan 2025-2030,” City of Copenhagen, kk.dk..

Yard waste collection remains sensitive to seasonality and requires container options, as well as pickup events that account for branches and bulk. In contrast, food waste is collected biweekly with strict contamination rules to protect digester performance and recycling credits. Municipalities explore mechanically separated organic fractions to supplement source-separated inputs where practical, and they rely on grid-connected plants that minimize haul distances and stabilize organics processing slots. Agricultural residues are growing within Denmark's organic waste collection services industry as farmers respond to the Green Tripartite Agreement’s tax signals that reward manure delivery and methane capture before field application. Digital routing and container-level monitoring improve bin rightsizing, reduce truck-kilometers, and support stronger curb contamination control, helping sustain leadership in the Denmark organic waste collection services market. Together, these elements keep food waste at the center of the segment mix while allowing municipal plans to adapt collection design to local density, garden waste volumes, and downstream plant availability across regions.

By End-User: Residential Base Secured; Commercial Food Service Accelerating

Residential accounted for 62.4% of the Denmark organic waste collection services market in 2025, reflecting universal municipal obligations under the 2020 Statutory Order that make door-to-door organics service a standard feature of household waste management. Household container standards, such as Egedal’s two-chamber bins and biweekly pickup frequency, enable predictable route design and fleet utilization in suburban and mixed-density zones. Municipalities pair bin standards with enforcement and green-bag systems that drive compliance and cleanliness, anchoring volume and protecting quality in the Denmark organic waste collection services market. Digital monitoring elevates service quality while reducing costs, as Vejle documents with a 30% reduction in driving and routine dynamic routing triggered by bin-level sensors. Municipal data suggests household capture remains below potential, which sets a clear growth path as Copenhagen and peers tighten mis-sorting penalties and consider pricing signals, such as pay-as-you-throw, to boost food waste separation.

Commercial food service is projected to grow at a 7.46% CAGR to 2031, supported by clarified regulatory obligations for businesses with household-like waste and stepped-up inspections that limit diversion of recyclables to residual streams. Dense HoReCa zones in Greater Copenhagen generate consistent, high-quality organics with a lower contamination risk when operators provide clear bin signage, training, and scheduling that align with service hours, thereby contributing to resilient growth in the Denmark organic waste collection services market. Municipal examples show strong commercial organics capture when supported by clear rules and reliable collection windows, which helps stabilize co-digestion blends and plant throughput. The agricultural CO2e tax amplifies demand for consistent organic products, reinforcing contract stability for specialized commercial routes in the Denmark organic waste collection services market. Industrial food processing streams often flow under direct contracts to plants. Yet, they inform local logistics and equipment needs that operators can adapt to lift overall system efficiency across residential and commercial pickup.

By Collection Method: Door-to-Door Primacy Driven by Regulatory Mandate and IoT Economics

Door-to-door captured 78.6% of the Denmark organic waste collection services market in 2025 and is also the fastest-growing method, with a 7.81% CAGR through 2031, reflecting the default service standard in the ten-fraction framework that binds all municipalities. Harmonized containers for single-family homes and shared systems for multi-unit buildings enable crews and equipment to serve mixed routes efficiently, supporting asset utilization and reliable frequencies in urban and suburban areas. IoT sensors embedded in public bins and route-optimization platforms enable dynamic pickup based on fill levels and location patterns, which reduces unnecessary trips and emissions across municipal operations in the Denmark organic waste collection services market. Data-sharing between sensors and task systems further cuts complaints and missed pickups, as Rudersdal’s integration with workflows shows through automatic service orders at threshold levels. These efficiencies free up resources for quality control, resident education, and targeted contamination reduction in organics bins, stabilizing digester feedstock quality in the Denmark organic waste collection services market.

Drop-off and bring systems serve rural and seasonal contexts where door-to-door economics are less favorable, as underground containers and sensor-enabled pickups in dispersed geographies improve service levels while limiting transport intensity. Airport and transit hubs deploy compacting smart bins that reduce pickup frequency and supply data on waste composition, which complements municipal systems and informs commercial route design in the Denmark organic waste collection services market. Home composting allowances for garden waste exist in some municipalities. In contrast, prepared food waste remains ineligible due to hygiene and pest risk, which keeps organics collection central to food waste management. Together, these methods keep door-to-door as the backbone while integrating drop-off and smart public infrastructure in high-traffic and hard-to-reach settings across the Denmark organic waste collection services market.

Geography Analysis

National policy creates a cohesive framework for the Denmark organic waste collection services market, while regional differences in density, infrastructure, and municipal capacity shape operating models. Greater Copenhagen collects large absolute volumes due to population and HoReCa concentration, with over 15,000 tonnes of food waste captured in 2023 and a plan to lift real recycling to 60% from 2030, which drives investment in smart bins, pay-as-you-throw pilots, and clear enforcement to improve organics capture at the curb. Zealand municipalities such as Roskilde demonstrate frontrunner execution with a 60% household recycling rate and documented food waste capture supported by aligned processing partnerships, which shows how planning and tender design can accelerate outcomes in the Denmark organic waste collection services market. Suburban areas with high household consumption, such as Fredensborg, illustrate capacity and contamination pressures that operators address with green-bag systems, standardized bins, and route optimization to stabilize pickup quality.

Western Denmark concentrates biogas production and grid connections that support short-haul logistics from organic routes to plants, reducing transport intensity and supporting consistent gate fees for municipal and commercial feedstock in the Denmark organic waste collection services market. Tønder Biogas shows industrial-scale integration that elevates downstream capacity for organics and co-digestion blends, which anchors a regional pull for high-purity feedstock from both households and businesses. The agricultural CO2e tax’s regional impact is strongest in livestock-intensive Jutland, where it increases manure-to-biogas flows and keeps pressure on operators to secure complementary food waste to optimize methane yields in the Denmark organic waste collection services market. Islands and smaller municipalities adopt self-sufficient solutions for garden waste, while relying on standardized household organics service for food waste to maintain hygiene and prevent pests within the shared regulatory framework.

In northern and rural regions, underground containers and NB-IoT sensors are deployed to accommodate dispersed settlement patterns, making needs-based pickups and remote monitoring critical for cost control and service reliability in the Denmark organic waste collection services market. As IoT costs decline and case studies spread through municipal networks, rural adoption accelerates and narrows the efficiency gap with cities, which benefit from shorter routes and higher collection density, supporting a more even rollout of digital practices over 2026-2031. The shared objective of meeting EU recycling targets and national climate commitments keeps the regional strategy aligned while allowing local adaptation of container types, pickup frequencies, and equipment choices that fit the geography and fleet assets in the Denmark organic waste collection services market.

Competitive Landscape

The Denmark organic waste collection services market shows moderate consolidation, with consolidation momentum as competitive tendering expands for recyclable and residual waste, favoring operators with scale, electrified fleets, and data capabilities. VERDIS’s regional footprint across about 100 Nordic municipalities and its February 2025 central sorting partnership in Denmark demonstrate how integrated post-collection capabilities create procurement advantages that complement municipal organics programs. REMONDIS invested in a new baling site and launched a digital ordering module that enhances customer experience, signaling a focus on upstream control and transparency that supports higher-quality feedstock and operational predictability. Danish operators and municipal utilities maintain strong positions through local knowledge and contract incumbency, yet they face competitive benchmarks that reward electrification, IoT integration, and automated reporting under Affaldsdatasystemet.

Vertical integration aligns with energy transition strategies, as shown by Tønder Biogas’ scale and CO2 capture, which broaden revenue streams and tighten the linkage between organic waste collection economics and biomethane demand in the Denmark organic waste collection services market. Equipment suppliers and digital partners such as Liebherr, Volvo Trucks, Maacks, and Sweco enable differentiators across operations, including zero-emission loaders, purpose-built electric garbage trucks, and platform-based route and task management that deliver measurable efficiency gains. This technology stack supports tender criteria that now rely more on emissions, data, and service performance, and it encourages operators to plan multi-year investments to stay competitive as policy raises the baseline.

Mid-tier and niche players compete in specialized routes such as industrial food processing, organics, and HoReCa pickups, where volume predictability and lower contamination can support premium gate fees. At the same time, municipal utilities retain household services but increasingly partner on digital enablement and electrification pilots. As tenders evolve, contract structures that reward per-tonne outcomes and quality metrics may outcompete per-collection models that suffer under sensor-driven frequency reductions, which changes revenue profiles across the Denmark organic waste collection services market. The competitive picture, therefore, reflects a transition in which scale, technology, vertical ties to biomethane, and regulatory reporting competence shape advantage as municipal plans aim for higher real recycling rates and reliable service levels.

Denmark Organic Waste Collection Services Industry Leaders

Meldgaard Miljø A/S

Verdis A/S

City Container A/S (Reconor Group)

Marius Pedersen A/S

Daka ReFood (Daka Denmark A/S)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Danish IT firm Waste2x won a significant multi-year tender to deliver a fully integrated digital platform for municipal organic and general waste collection in Odense Municipality, in partnership with Odense Renovation. The platform covers end-to-end operations management, real-time data analytics, and customer service functions.

- January 2026: Greater Copenhagen's primary utility launched a pioneering project to repurpose ochre sludge (a by-product of drinking water treatment) as a substitute for synthetic chemicals in biogas production facilities that process organic food waste. Denmark's water companies collectively generate over 6,400 tons of ochre sludge annually, with two-thirds currently sent to landfill.

- May 2025: Copenhagen Infrastructure Partners inaugurated Tønder Biogas in West Denmark, financed by a USD 39.4 million Nordic Investment Bank loan, with 930,000 tonnes per year of biomass processed, more than 41 million Nm³ of methane produced, and 48,000 tonnes of liquid CO2 captured.

- February 2025: Verdis A/S was selected as Denmark’s central sorting partner for the national scheme, effective October 1, 2025, to handle 8,500 tonnes per year of plastics, metals, and cartons from household streams.

Denmark Organic Waste Collection Services Market Report Scope

The Denmark Organic Waste Collection Services Market Report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and more), by End-User (Residential, Commercial, Industrial, and Others), by Collection Method (Door-to-Door Collection, and more), and by Technology & Equipment (Manual Collection Systems, Semi-Automated Systems, and more). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste |

| Agricultural Residues |

| Others |

| Residential |

| Commercial (HoReCa, Retail) |

| Industrial (Food Processing & Manufacturing) |

| Others (Agri-waste) |

| Door-to-Door Collection |

| Drop-Off / Bring Systems |

| Others |

| Manual Collection Systems |

| Semi-Automated Systems |

| Fully Automated Systems |

| Others |

| By Waste Type | Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste | |

| Agricultural Residues | |

| Others | |

| By End-User | Residential |

| Commercial (HoReCa, Retail) | |

| Industrial (Food Processing & Manufacturing) | |

| Others (Agri-waste) | |

| By Collection Method | Door-to-Door Collection |

| Drop-Off / Bring Systems | |

| Others | |

| By Technology & Equipment | Manual Collection Systems |

| Semi-Automated Systems | |

| Fully Automated Systems | |

| Others |

Key Questions Answered in the Report

What is the outlook for the Denmark organic waste collection services market to 2031?

The Denmark organic waste collection services market size was USD 54.28 million in 2025 and is projected to reach USD 76.25 million by 2031 at a 5.87% CAGR over 2026-2031.

Which waste type leads to growth in Denmark?

Food waste accounted for 58.2% in 2025 and is also the fastest-growing segment, with a 6.78% CAGR to 2031, supported by biogas demand and full municipal coverage.

Which end-user segment is expanding the quickest?

Commercial food service records the highest growth at a 7.46% CAGR through 2031, driven by clarified obligations and inspections that move recyclable organics out of residual streams.

What collection method dominates in Denmark?

Door-to-door collection commanded a 78.6% share in 2025 and is advancing at a 7.81% CAGR through 2031, driven by regulatory mandates and IoT-enabled routing.

How do policies shape the Denmark organic waste collection services market?

National separate collection rules, landfill and incineration taxes, EPR for packaging, and a new agricultural CO2e tax align incentives toward high-purity organics streams and biogas routes.

Why is Denmark’s biogas capacity important for collection services?

Nearly 150 plants with strong grid connectivity and a 2030 target for 100% green gas create stable offtake and gate fees for organics collected under municipal and commercial schemes.

Page last updated on: