Denmark Bulky Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

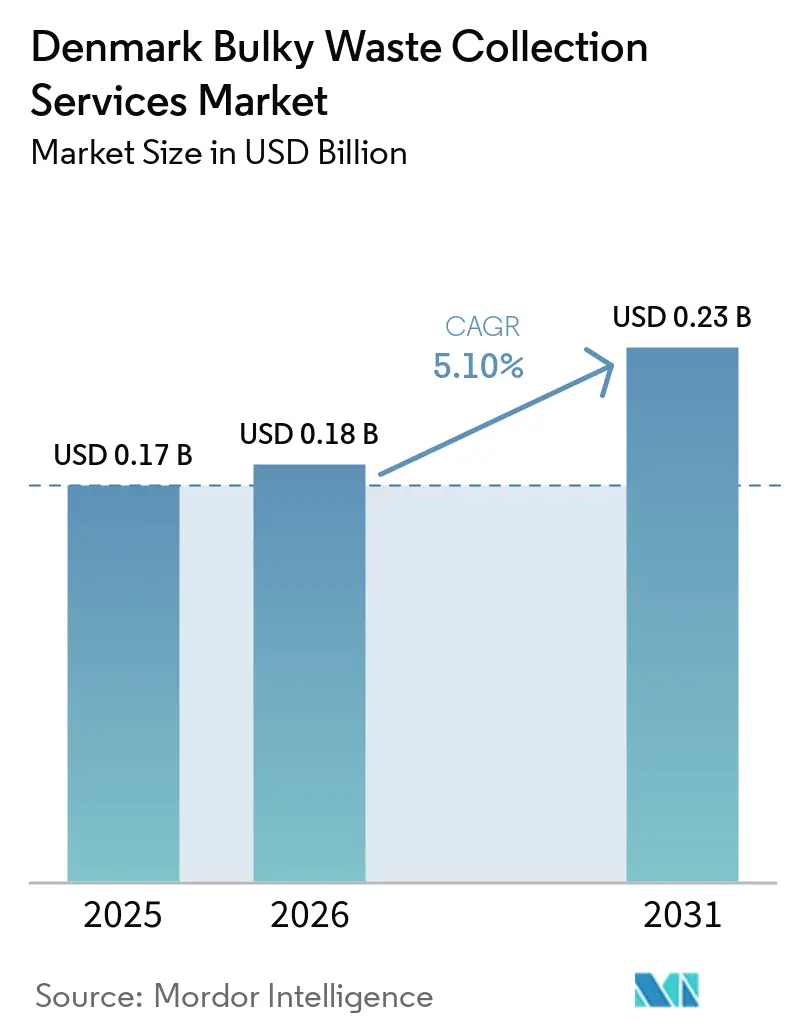

| Base Year Market Size (2025) | USD 0.17 Billion |

| Market Size (2026) | USD 0.18 Billion |

| Market Size (2031) | USD 0.23 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

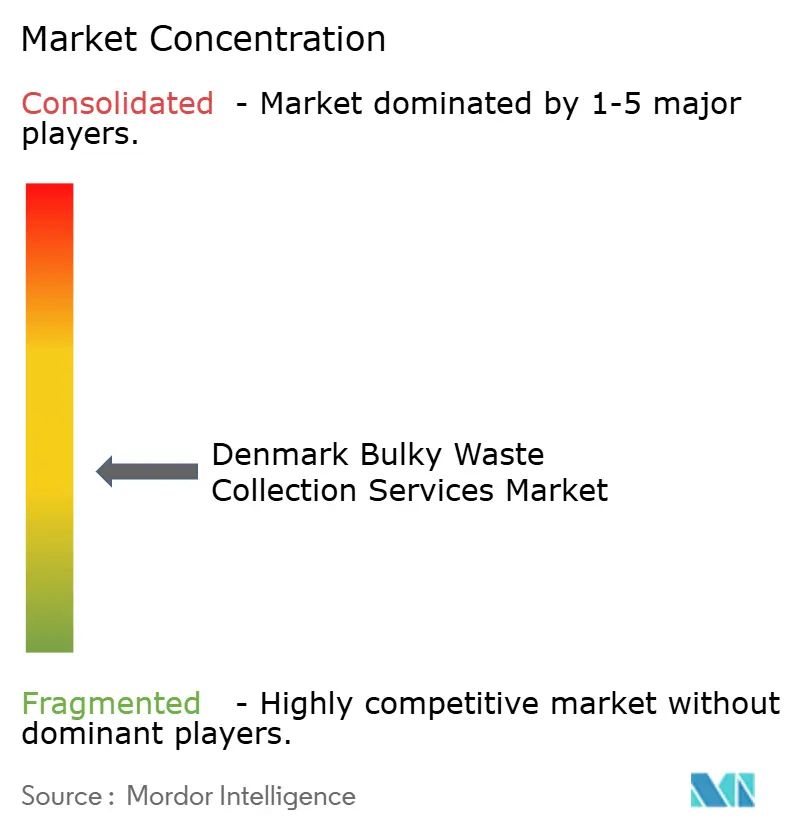

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Denmark Bulky Waste Collection Services Market Analysis by Mordor Intelligence

The Denmark Bulky Waste Collection Services Market size is expected to grow from USD 0.17 billion in 2025 to USD 0.18 billion in 2026 and is forecast to reach USD 0.23 billion by 2031 at 5.10% CAGR over 2026-2031.

Denmark’s shift toward mandatory tendering of incineration-suitable waste treatment under the 2022 climate plan has sharpened competition, nudged operational transparency, and reinforced consolidation among qualified operators. Digital booking platforms continue to reduce acquisition and servicing frictions for municipal and on-demand providers, compressing response times and improving route compliance, which supports steady adoption in dense urban cores. High household waste generation per person, one of Europe’s highest, sustains demand for convenient bulky-waste solutions even as Denmark works to raise real recycling rates. Producer responsibility for packaging, introduced in late 2025, begins to shift municipal cost burdens and may encourage upstream design choices that incrementally reduce downstream bulk flows over time. Municipal capacity for energy-from-waste remains significant, keeping disposal a viable backstop while source separation and digitalization scale, affecting the pace and profile of growth across the Denmark bulky waste collection services market.

Key Report Takeaways

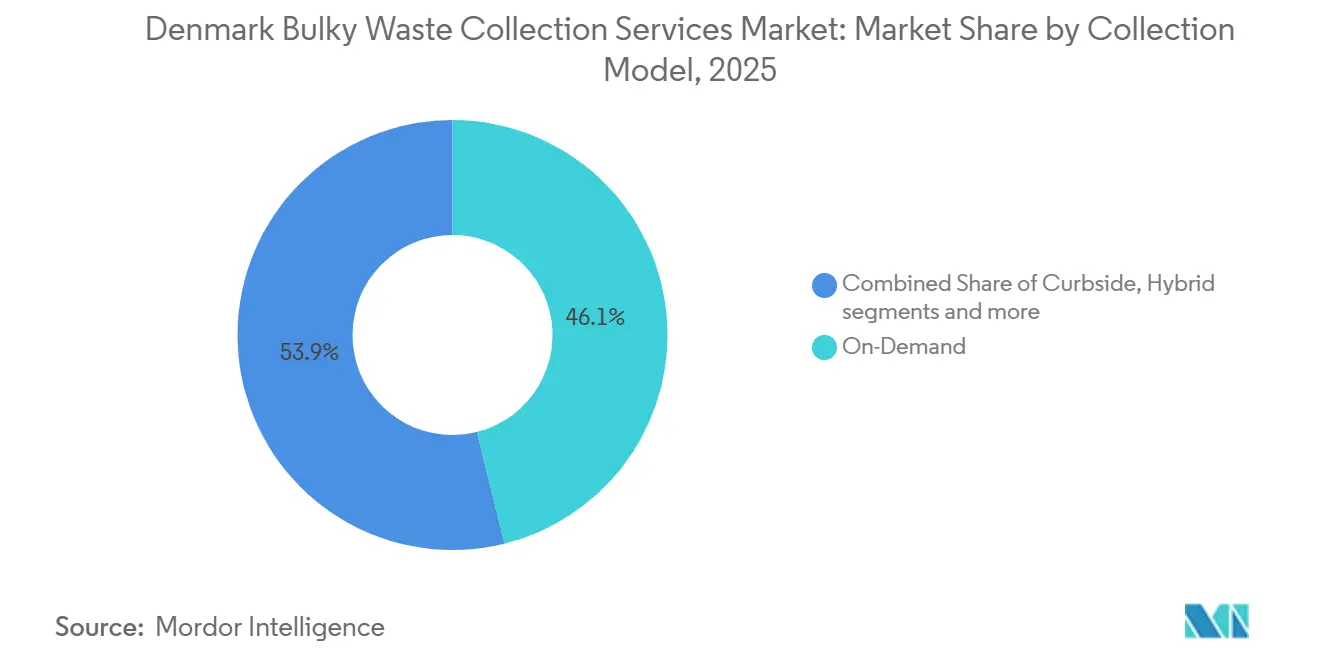

- By collection model, On-Demand held 46.21% of the Denmark bulky waste collection services market share in 2025 and is projected to grow at 5.78% CAGR through 2031.

- By source, the Residential segment accounted for 72.31% of the Denmark bulky waste collection services market size in 2025 and is slated to grow at a 6.21% CAGR through 2031.

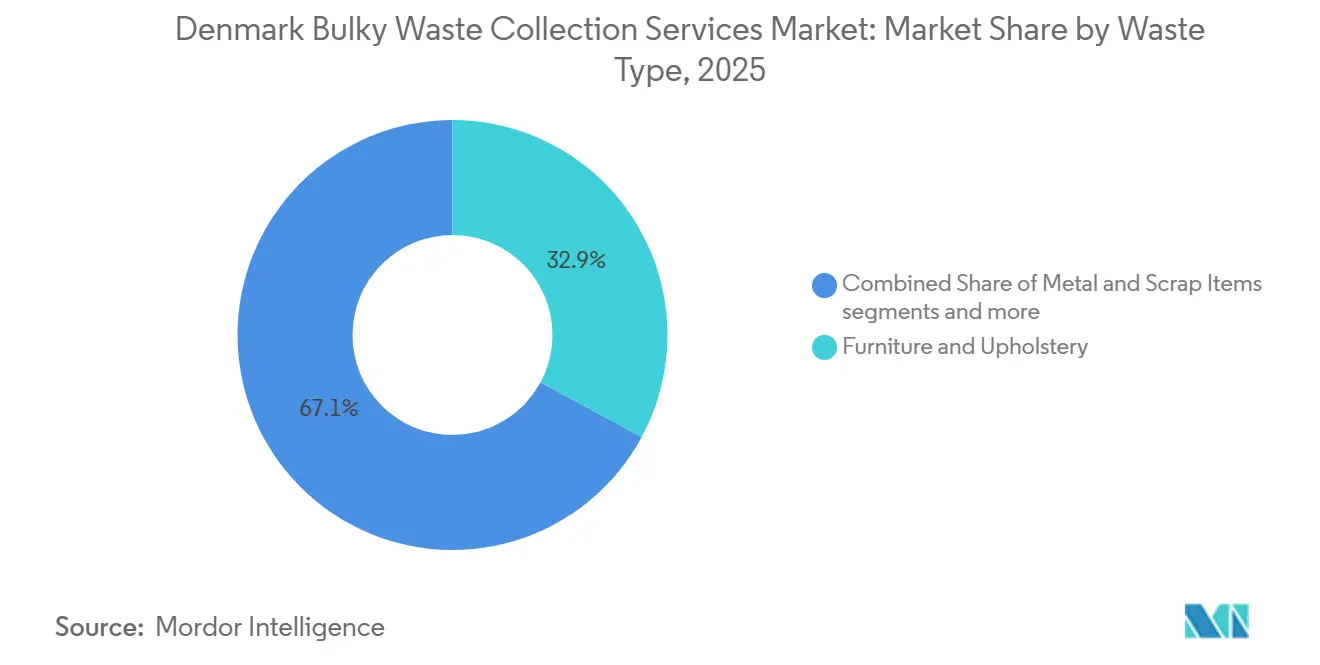

- By waste type, Furniture & Upholstery led with a 32.87% share in 2025 and is expected to expand at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Denmark Bulky Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Source Separation for Bulky Waste | +1.2% | National, with enforcement concentrated in municipalities exceeding 20,000 inhabitants | Medium term (2-4 years) |

| Digital Booking Platform Adoption in Municipalities | +0.8% | Urban cores (Copenhagen, Aarhus, Odense), gradual diffusion to Zealandic suburbs | Short term (≤ 2 years) |

| 70% Residual Waste Reduction Target by 2030 | +1.5% | National, with highest impact in incineration-dependent regions (Capital, Central Jutland) | Long term (≥ 4 years) |

| Rising White Goods and Mattress Replacement Rates | +0.9% | National, with pronounced effect in single-family residential zones | Medium term (2-4 years) |

| Avfall Danmark Industry Standardization | +0.3% | National, sector-wide harmonization | Long term (≥ 4 years) |

| Recycling Centres Integration with Collection Routes | +0.7% | Regional, particularly North Zealand and Funen | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Source Separation for Bulky Waste

Denmark’s July 2025 update requires clearer source separation of bulky and combustible fractions, including the use of transparent bags and stricter on-site sorting obligations, which shifts sorting labor to the generator and heightens quality control at the collection stage[1]Bramidan, “Nye krav til affaldssortering fra 1. juli 2025 – undgå bøder,” Bramidan, bramidan.dk. For construction activities exceeding defined thresholds, selective demolition and resource mapping have become standard, increasing pre-segregation of materials like metals, timber, and gypsum before pickup and lowering contamination loads downstream. Municipal guidance to households reinforces transparent sorting and discourages the use of mixed combustible bags, signaling rising compliance expectations for both residential and commercial generators. Collection operators are responding by configuring multi-compartment vehicles and levying fees for non-conforming loads, an approach already publicized by large national players. Centralized reclassification authority at the Danish EPA streamlines national consistency but can extend approval timelines for novel streams, thereby delaying pilots for niche bulky fractions despite standardized rules. These shifts elevate operational readiness as a differentiator in the Denmark bulky waste collection services market, since compliance-centered investments increasingly shape tender outcomes.

Digital Booking Platform Adoption in Municipalities

Platform deployments like Sweco’s RenoWeb automate service tickets based on sensor thresholds, enabling real-time routing that displaces manual planning and shortens the cycle between reported demand and collection. Case implementations show fewer overflowing bins and measurable reductions in asset counts when capacity data informs bin placement and frequency decisions, which cuts capital and diesel hours in parallel. Despite growing coverage, municipalities run heterogeneous systems that complicate cross-boundary route consolidation, creating openings for vendor-agnostic aggregators that interface with multiple back ends. Feature improvements, such as RFID- or GPS-backed verification, have boosted response times and increased service accuracy, with providers reporting strong gains in areas where fleets operate at high utilization. Municipal transitions to next-generation apps now test adoption dynamics across demographics, as recent rollouts in Greater Copenhagen shift communication and reminders from legacy portals to consumer-grade interfaces. These digital shifts further entrench convenience as a growth lever in the Denmark bulky waste collection services market, especially where density and broadband coverage support rapid scaling.

70% Residual Waste Reduction Target by 2030

Denmark’s residual-waste reduction goal by 2030 depends on scaling separate collection for challenging streams and closing infrastructure gaps for pre-treatment and downstream recovery. Early procurement signals for diaper and textile programs indicate targeted tonnage that can be captured through dedicated collection and processing pathways once sufficient scale is secured through public tenders. Packaging producer responsibility, which began in October 2025, shifts costs and incentives upstream, including eco-modulation that can steer design away from persistent composites and toward higher-recyclability configurations. Private investment in pre-treatment capacity for organics also signals confidence that higher-quality feedstock will find a stable offtake in biogas, even under strict purity specifications. Municipal resource plans underscore the need for higher capture and reuse at stations, which complement curbside reforms and create multiple lanes to reduce residuals. Taken together, these measures keep the Denmark bulky waste collection services market oriented toward quality-controlled inputs and measurable diversion outcomes.

Rising White Goods and Mattress Replacement Rates

Average lifespans for large household appliances have shortened relative to the 1990s, reflecting a mix of repair economics, reliability expectations, and retail promotion cycles. Denmark introduced a repair-refund scheme in late 2025 to tilt decisions toward repair for large appliances. While early usage has been limited, the policy direction supports longer asset lives over time. The regulatory landscape for e-waste reporting has also tightened, creating more systematic capture of flows in large equipment and temperature-exchange categories. Official waste accounts show small shares for electronics in household waste by mass, which contrasts with higher e-waste generation per capita and indicates a significant share moves through specialized channels rather than mixed bulky streams. Collection operators must therefore plan for episodic surges around household events while navigating policy signals that increasingly reward repair and channel compliance. These factors continue to influence composition, timing, and handling requirements across the Denmark bulky waste collection services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages in Rural Municipalities | -0.6% | Southern Denmark (Triangle Region), North Jutland periphery | Short term (≤ 2 years) |

| High Costs from Strict Vehicle Emission Standards | -0.4% | National, disproportionate burden on SME collectors (<50 employees) | Medium term (2-4 years) |

| Limited Operator Differentiation Under Tender Rules | -0.3% | National, affecting all tender-dependent revenue streams | Medium term (2-4 years) |

| Household Confusion on Collection vs. Drop-off | -0.2% | Suburban/semi-rural municipalities implementing 10-fraction sorting | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor Shortages in Rural Municipalities

Recruiting and retaining heavy-vehicle drivers in peripheral regions remains challenging, leading to extended time-to-fill for waste-route roles and service frequency tradeoffs in sparsely populated areas. While route optimization and sensor-driven dispatch reduce non-productive driving time, they cannot replace the manual tasks required to collect and handle bulky items at the curb or in constrained residential settings. Operators continue to balance pay, training, and scheduling flexibility to stabilize crews, yet demographic headwinds and competing logistics employers keep vacancy levels elevated in rural municipalities. Municipalities sometimes respond by extending collection intervals or encouraging self-haul to staffed stations where it is feasible to maintain service coverage with limited driver availability[2]BOFA, “Self-service Private,” BOFA, bofa.dk . The net effect is persistent operating pressure for smaller haulers, which sustains the case for integrated platforms that can match intermittent rural demand to available capacity in the Denmark bulky waste collection services market.

High Costs of Strict Vehicle Emission Standards

Euro 7 compliance from late 2026 increases technical and cost requirements for new vehicles and extends durability obligations, thereby elevating the capital planning burden for fleets serving bulky-waste routes. Brake particulate rules also apply to electric vehicles, shaping component specifications and maintenance strategies for early adopters who commit to zero-emission fleets under public contracts. Fleet managers face multi-year uncertainty around residual values and retrofit needs, which affects financing costs and procurement timing across tenders. At the same time, municipal awards are beginning to favor fully electric operations for household waste streams, signaling a direction of travel that will likely cascade to bulky-waste fleets in the next tender cycles. EU-level targets to lower the CO2 intensity of heavy-duty vehicle fleets further compress the decision window, adding urgency to planning for zero-emission readiness across the Denmark bulky waste collection services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Collection Model: Digital Platforms Rewire Convenience Economics

On-Demand models captured 46.21% of the Denmark bulky waste collection services market share in 2025 and are projected to grow at a 5.78% CAGR through 2031, reflecting strong adoption in dense urban zones that benefit from rapid confirmations and shorter booking cycles. Digital portals and apps from municipal and private providers compress the time between request and collection, while GPS and RFID verification lift service accuracy and reduce manual routing tasks. In practice, platforms that combine request intake, routing, and proof of service help operators better match supply with episodic household disposal events, which strengthens utilization in cities. Private aggregators that market directly to households and then coordinate with contractors illustrate a nimble approach that targets convenience-first users who prefer app-based scheduling. Over time, this pattern will keep the Denmark bulky waste collection services industry oriented toward hybrid models that mix scheduled neighborhood sweeps with on-demand pickups to balance utilization and responsiveness.

Operators also use white-label municipal platforms to diversify revenue between public contracts and direct-to-consumer bookings, thereby reducing exposure to tender cycles and seasonal dips. These models work best in the Capital Region and larger cities where population density supports tighter routing and enables same-day or next-day slots. In rural and semi-rural areas, adoption is steady but slower, given fewer stops per hour and higher reliance on phone-based or self-haul alternatives. As user familiarity grows and platform interoperability improves, the Denmark bulky waste collection services market size associated with on-demand flows is likely to rise further in urban cores relative to fixed-schedule services.

By Source: Residential Sorting Chaos Drives Collection Demand

The Residential segment accounted for 72.31% of the Denmark bulky waste collection services market in 2025 and is projected to grow at a 6.21% CAGR through 2031, reflecting sustained household disposal events and the convenience pull of flexible curbside pickups. Ten-fraction sorting has improved awareness but also increases the share of bulky items routed to curbside when users are uncertain about composite materials versus recyclable components, which lifts residential pickup volumes. Municipal resource and waste plans call for enhanced reuse and higher real recycling from station operations. Yet, recurring disposal peaks around moves or renovations continue to channel significant bulky flows to curbside. Over time, consistent communications, clear sorting visuals, and app reminders could shift a portion of bulky residential items toward reused or station drop-off, where quality control is higher. For now, density-driven urban neighborhoods remain the core of residential bulky collections in the Denmark bulky waste collection services market.

Commercial and institutional streams show steadier trajectories as compliance regimes and supervision tighten for business waste, encouraging pre-sorting and reducing mixed bulky dispatches. Industrial sources are increasingly partnering with circular feedstock providers for organic and processable materials, expanding options beyond standard collection contracts. In the near term, residential remains the most dynamic contributor to the Denmark bulky waste collection services industry, while commercial and industrial sources are moving toward more specialized, contract-stabilized flows. That balance allows operators to smooth cash flows by combining recurring B2B pickups with demand-responsive household routes aligned to home improvements and moving cycles.

By Waste Type: Furniture Dominance Masks Substitution Threats

Furniture & Upholstery led the Denmark bulky waste collection services market with a 32.87% share in 2025, supported by frequent household refresh cycles and the absence of dedicated take-back obligations. Marketing and consumer expectations around hygiene and aesthetics continue to produce steady disposal events for sofas, mattresses, and case goods that do not fit residual bins or small-item recycling. Municipal reuse initiatives at stations are expanding the capture of intact furniture and subassemblies, which could moderate curbside flows as programs scale and communications improve. The segment is projected to post a 6.72% CAGR through 2031, contingent on continued household replacement behavior and steady service availability through digital channels.

Other relevant fractions include white goods, which are increasingly influenced by repair economics and WEEE compliance channels, and metals, which often receive favorable pricing at recycling facilities that can incentivize self-haul. Construction and demolition-related bulky flows are evolving under selective demolition rules and resource mapping, which improves purity and reduces mixed loads that would otherwise move through bulky pickup channels. Expanded EPS compaction at station points to scalable handling for lightweight, bulky foam materials once contamination controls are dependable. As program design and pricing align across these categories, operators will continue to balance curbside convenience with station-centric capture in the Denmark bulky waste collection services market.

Geography Analysis

Urban density remains the dominant operating advantage, with the Capital Region supporting high stop rates per hour that enable same-day or next-day on-demand bookings and frequent scheduled services. Surrounding municipalities in North Zealand coordinate tenders and operational standards to pool volume and sustain stable service levels. At the same time, suburban patterns continue to evolve with platform rollouts and improved station reuse programs. The Denmark bulky waste collection services market benefits from platform consolidation in and around Copenhagen, where communications and reminders reinforce participation and reduce missed pickups.

Central Jutland’s organic pre-treatment capacity supports bundling opportunities, enabling trucks to backhaul compatible fractions to regional plants after deliveries or pickups, which improves utilization for mixed-route operators. Funen’s logistics corridor and proximity to cross-border flows support larger integrators that blend bulky-waste services with packaging and commercial materials handling, leveraging transfer and baling stations to aggregate loads. The Denmark bulky waste collection services market also sees island and remote geographies adapt by combining self-service stations with targeted curbside services for residents unable to self-haul, which holds costs in check while maintaining access.[3]Sweco, “RenoWeb - Digital solutions,” Sweco, sweco.dk

North and West Jutland exhibit strong seasonality in summer-house areas, which benefit from sensor-driven collection triggers to match volumes during peak months without over-servicing off-peak periods. Across these regions, continued investment in container-level sensors, platform standardization, and clear resident communications will help close remaining gaps in route density and material quality. These moves keep the Denmark bulky waste collection services market positioned for stable growth while channeling more bulky flows toward reuse and material recovery.

Competitive Landscape

Market structure in Denmark remains moderately concentrated by capability and region, with large European integrators and established Danish operators competing across municipal tenders, specialized streams, and platform-enabled consumer services. Recent investments in baling, transfer, and pre-treatment increase opportunities to internalize downstream margins that pure collection players cannot access, while platform deployments raise the bar for responsiveness and service verification. Given procurement’s emphasis on demonstrable environmental management and service quality, certifications and data transparency are becoming de facto entry tickets for tender participation.

Strategic moves highlight three vectors. First, vertical integration is advancing through new capacity for packaging and organics, helping reduce exposure to price volatility at third-party processors and aligning with circular-economy goals. Second, electrification has moved from pilots to contract-level commitments, with recent municipal awards requiring fully electric fleets over multi-year terms, setting a template other municipalities can follow. Third, software providers continue to offer modular solutions to municipalities and haulers that improve operational efficiency without necessarily disintermediating the collector, leaving room for partnership models.

At the edge of the market, nimble aggregators and regional specialists exploit gaps in service where density or scheduling constraints limit traditional routes. At the same time, municipal platforms increase baseline digital engagement for residents. Integrators with standardized data and reporting tools for customers gain an advantage as EU sustainability disclosure rules shape what enterprise clients expect from service providers. Overall, the Denmark bulky waste collection services market favors operators that pair asset scale with credible digital capabilities, compliance assurance, and measurable climate performance.

Denmark Bulky Waste Collection Services Industry Leaders

-

Vestforbrænding I/S

-

Amager Ressourcecenter (ARC)

-

ARGO I/S

-

Kredsløb A/S

-

AffaldPlus I/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Verdis A/S won an 8-year tender from Vejen Kommune to provide household waste collection using 100% electric refuse vehicles starting November 1, 2027.

- December 2025: REMONDIS Danmark inaugurated a new baling station in Ishøj to process cardboard, paper, and plastics from household packaging waste and serve as a transfer node for hazardous fractions.

- November 2025: Copenhagen adopted its 2025-2030 Resource and Waste Plan, targeting higher reuse and real recycling, along with expanded supervision to move commercial flows into recovery pathways.

Denmark Bulky Waste Collection Services Market Report Scope

| Curbside |

| On-Demand |

| Hybrid |

| Contracted B2B |

| Others |

| Residential |

| Commercial |

| Industrial |

| Municipal/Government |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) |

| Furniture & Upholstery |

| Metal & Scrap Items |

| White Goods/Appliances |

| Construction & Demolition |

| Others (Event-specific Waste, Biomedical/Institutional) |

| By Collection Model | Curbside |

| On-Demand | |

| Hybrid | |

| Contracted B2B | |

| Others | |

| By Source | Residential |

| Commercial | |

| Industrial | |

| Municipal/Government | |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) | |

| By Waste Type | Furniture & Upholstery |

| Metal & Scrap Items | |

| White Goods/Appliances | |

| Construction & Demolition | |

| Others (Event-specific Waste, Biomedical/Institutional) |

Key Questions Answered in the Report

What is the Denmark bulky waste collection services market size and projected growth to 2031?

The Denmark bulky waste collection services market size was USD 0.17 billion in 2025 and is projected to reach USD 0.23 billion by 2031 at a 5.1% CAGR over 2026-2031.

Which segment leads in the collection model in Denmark, and how fast is it growing?

On-Demand leads by collection model, with a 46.21% share in 2025, is projected to grow at a 5.78% CAGR through 2031.

Which source dominates bulky waste collection in Denmark?

Residential is the largest source with a 72.31% share in 2025, supported by flexible curbside pickups and digital booking, and is set to grow at a 6.21% CAGR through 2031.

What is the largest waste type category handled, and what is its outlook?

Furniture & Upholstery is the largest waste type category, with a 32.87% share in 2025 and a projected 6.72% CAGR to 2031, driven by frequent household refresh cycles.

How are regulations shaping Denmark’s collection landscape through 2030?

Tighter source separation, packaging EPR, and EU fleet targets are driving higher-quality inputs, more pre-treatment capacity, and electrified fleets, which in turn influence procurement and operator strategies.

How are digital platforms changing bulky-waste operations in Denmark?

Municipal and private platforms automate requests, route optimization, and proof of service, enabling shorter response times and better utilization in dense urban areas.

Page last updated on: