Dehydrated Vegetables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

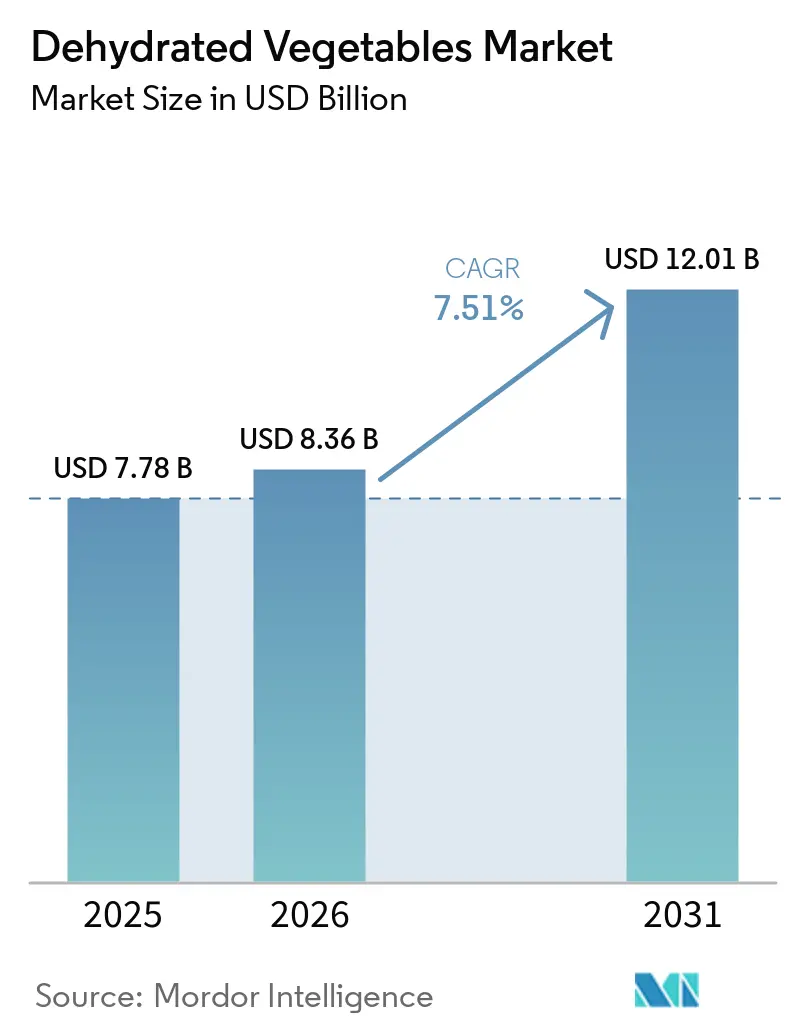

| Market Size (2026) | USD 8.36 Billion |

| Market Size (2031) | USD 12.01 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dehydrated Vegetables Market Analysis by Mordor Intelligence

The dehydrated vegetables market was valued at USD 7.78 billion in 2025, reached USD 8.36 billion in 2026, and is projected to grow to USD 12.01 billion by 2031, registering a compound annual growth rate (CAGR) of 7.51% during 2026–2031. This growth is driven by the increasing preference for convenience-oriented food consumption and the rising demand for shelf-stable, easy-to-use ingredients in modern food systems. The market is supported by the growing popularity of ready-to-eat and ready-to-cook meals, where dehydrated vegetables help reduce preparation time while preserving flavor and nutritional content. Additionally, the trend toward clean-label and natural ingredients is boosting adoption, as these products typically require minimal additives and align with consumer preferences for transparency and simplicity in food products.

Key Report Takeaways

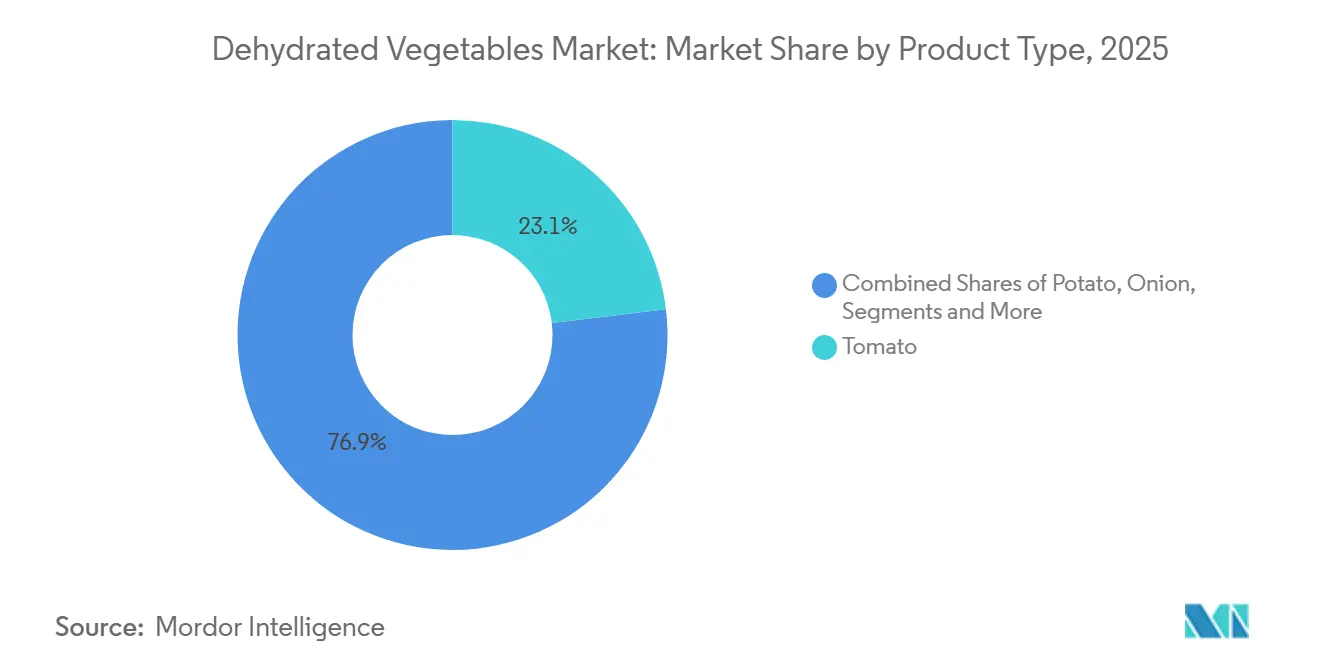

- By product type, tomato led with 23.09% of dehydrated vegetables market share in 2025, whereas onion is forecast to post the highest 8.56% CAGR through 2031.

- By form, powder and flakes captured 42.89% revenue in 2025; whole pieces are projected to expand at a 7.91% CAGR to 2031.

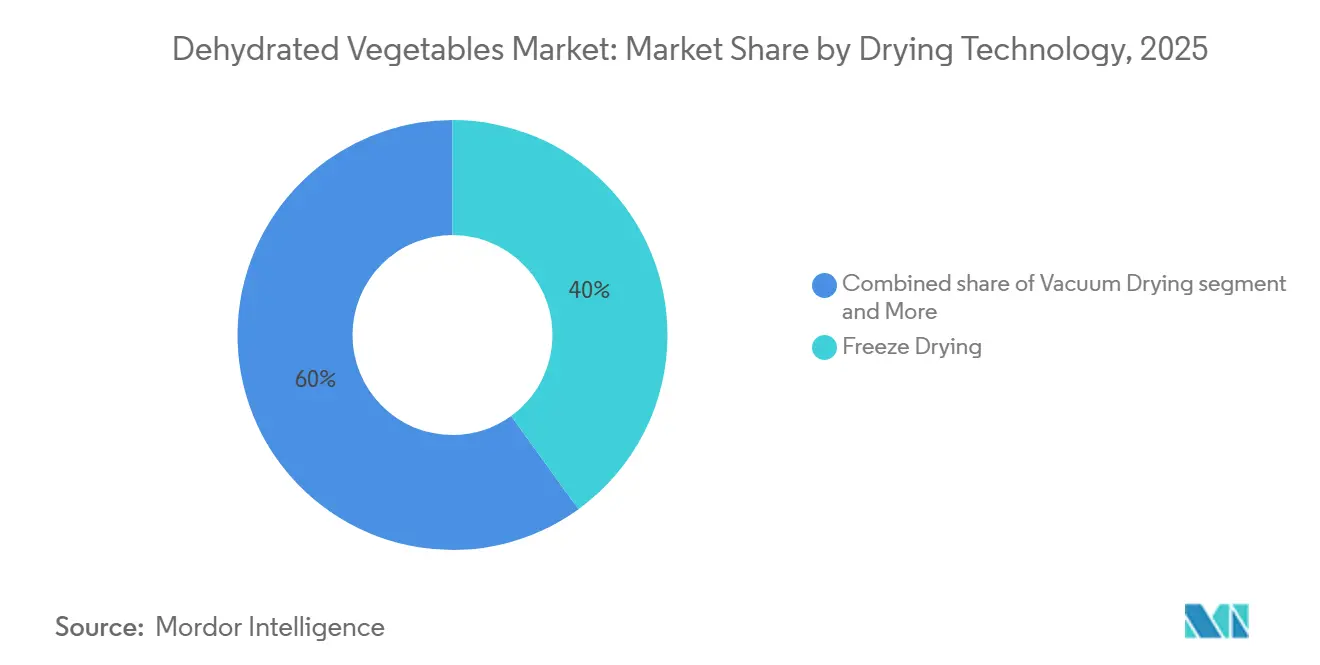

- By drying technology, freeze drying held 40.03% share in 2025, while drum and spray platforms are set to grow at 8.61% annually.

- By distribution channel, retail accounted for 70.03% of 2025 sales, yet foodservice is expected to register an 8.76% CAGR to 2031.

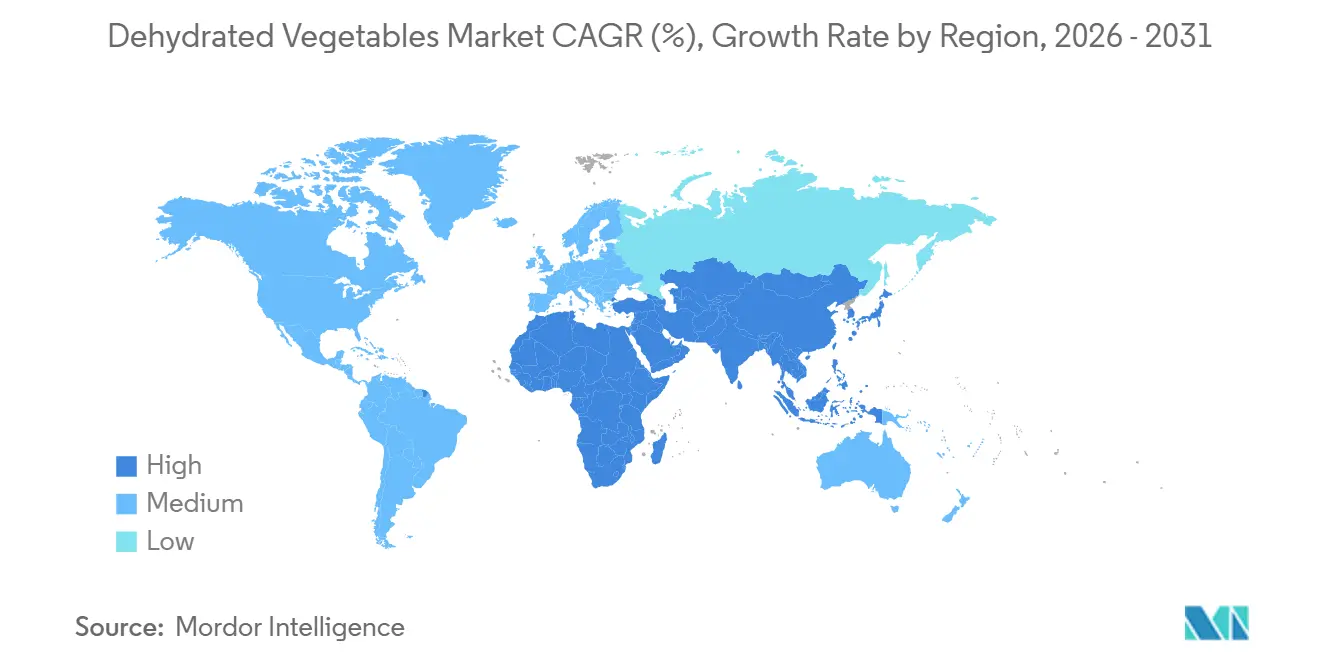

- By geography, North America contributed 34.09% of 2025 value, whereas Asia-Pacific is on track to record the fastest 9.03% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dehydrated Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience foods | +1.8% | Global, with pronounced uptake in North America and urban Asia-Pacific | Medium term (2-4 years) |

| Clean label and natural ingredient trends | +1.5% | North America and Europe, spillover to premium segments in Asia-Pacific | Short term (≤ 2 years) |

| Growth in plant-based and vegan food products | +1.3% | North America and Europe core, expanding in urban India and China | Medium term (2-4 years) |

| Growing awareness of food waste reduction | +0.9% | Global, particularly Europe and North America with regulatory backing | Long term (≥ 4 years) |

| Product versatility in culinary applications | +0.7% | Global, strongest in foodservice and industrial segments | Medium term (2-4 years) |

| Advancements in dehydration technologies | +1.2% | Asia-Pacific manufacturing hubs, technology transfer to South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenience foods

The increasing demand for convenience foods is a significant driver of the global dehydrated vegetables market. Consumers are seeking quick and easy meal solutions that accommodate busy lifestyles. Dehydrated vegetables meet this demand by offering ready-to-use formats that reduce preparation time, eliminating tasks such as washing, peeling, and chopping. Their extended shelf life and ease of storage make them appealing to both households and foodservice operators, facilitating efficient meal planning and reducing food waste. Furthermore, the rising popularity of ready-to-eat and ready-to-cook products, including instant soups, noodles, meal kits, and snack mixes, is boosting the use of dehydrated vegetables as key ingredients. These vegetables provide consistent flavor, texture, and nutritional value, supporting their integration into modern food processing and meal solutions. This trend toward convenience-focused consumption continues to drive market growth, establishing dehydrated vegetables as an essential component in the food industry.

Clean label and natural ingredient trends

Trends toward clean labels and natural ingredients are a key driver of the global dehydrated vegetables market, as consumers increasingly value transparency, minimal processing, and recognizable ingredients in their food. Dehydrated vegetables align well with these preferences, as they generally require few additives or preservatives while maintaining their nutritional value and flavor. This makes them a popular choice for clean-label formulations in products such as soups, snacks, ready meals, and seasoning blends. The focus on natural and organic products is further supported by consumer behavior data. According to the International Food Information Council, in 2024, 36% of consumers in the United States preferred foods labeled as natural, organic, or healthy [1]Source: International Food Information Council (IFIC), "2024 IFIC Food & Health SURVEY", ific.org. This growing trend is prompting food manufacturers to replace artificial ingredients with minimally processed options like dehydrated vegetables, thereby driving their demand.

Growth in plant-based and vegan food products

Growth in plant-based and vegan food products is a significant driver of the global dehydrated vegetables market, as consumers increasingly adopt plant-forward diets for health, sustainability, and ethical considerations. Dehydrated vegetables are essential in this transition, serving as key ingredients in plant-based meals such as soups, ready-to-eat dishes, snack products, and meat alternatives. They contribute to flavor, texture, and nutritional value while offering benefits like long shelf life, ease of storage, and versatility, making them ideal for large-scale production of vegan and vegetarian food products. This trend is further reinforced by growing consumer adoption. According to the Good Food Institute, 59% of households in the United States purchased plant-based foods in 2024 [2]Source: Good Food Institute (GFI), "U.S. retail market insights for the Plant-Based Industry", gfi.org. As demand for plant-based products continues to grow, food manufacturers are increasingly utilizing dehydrated vegetables to enhance product appeal while maintaining clean-label and natural positioning, thereby driving market growth.

Growing awareness of food waste reduction

Increasing awareness of food waste reduction is a key factor driving the global dehydrated vegetables market. Both consumers and food manufacturers are actively seeking solutions to minimize spoilage and enhance resource efficiency. Dehydrated vegetables provide a practical solution by significantly extending shelf life compared to fresh produce, thereby reducing waste during storage, transportation, and usage. This is particularly critical in supply chains where the perishability of fresh vegetables often results in substantial post-harvest losses. By converting fresh vegetables into stable, long-lasting formats, manufacturers can better utilize surplus production and lower disposal rates. Furthermore, dehydrated products enable portion control and on-demand usage, allowing households and foodservice operators to use only the required quantity, minimizing excess waste. The reduced need for refrigeration and decreased risk of spoilage also contribute to more efficient inventory management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quality degradation compared to fresh produce | -0.8% | Global, particularly in premium retail segments | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations | -0.6% | North America and Europe, with spillover to export-oriented Asia-Pacific | Medium term (2-4 years) |

| Seasonal fluctuations and supply chain disruptions | -0.7% | Global, acute in regions dependent on rain-fed agriculture | Short term (≤ 2 years) |

| Allergen and contamination risks during processing | -0.4% | Global, heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Quality degradation compared to fresh produce

Quality degradation compared to fresh produce remains a significant restraint in the global dehydrated vegetables market. The drying process can impact key sensory attributes, including texture, color, and flavor. Although dehydration extends shelf life, it often results in a softer or less crisp texture after rehydration, which may not replicate the mouthfeel of fresh vegetables. Additionally, some dehydration methods can cause color dulling or flavor loss due to the breakdown of volatile compounds during processing. These changes can reduce the acceptance of dehydrated vegetables in applications where freshness and sensory quality are essential, particularly in premium or minimally processed food segments. Consequently, some consumers and foodservice operators continue to favor fresh alternatives, creating challenges for the broader adoption of dehydrated formats despite their functional advantages.

Stringent food safety and labeling regulations

Stringent food safety and labeling regulations present a significant restraint in the global dehydrated vegetables market. Manufacturers are required to adhere to complex and evolving standards concerning product safety, traceability, and ingredient transparency. These regulations often impose strict limits on microbial contamination, pesticide residues, and additives, alongside detailed labeling requirements that include information on origin, processing methods, and nutritional content. Compliance necessitates substantial investment in quality control systems, testing procedures, and certification processes, adding to operational complexity. Furthermore, variations in regulatory frameworks across countries pose additional challenges for exporters, as companies must meet diverse compliance standards to access international markets. These regulatory demands can extend product approval timelines and increase the costs and efforts associated with market entry, particularly impacting smaller manufacturers and constraining market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tomato Leadership Faces Onion Acceleration

The tomato segment accounted for 23.09% of the overall product-type revenue in 2025, maintaining its dominance in the global dehydrated vegetables market. This is attributed to its versatility, high consumption frequency, and widespread use across various food applications. Dehydrated tomatoes are a key ingredient in numerous products, including soups, sauces, instant meals, seasonings, snack mixes, and bakery fillings. Their role is critical for food manufacturers aiming to ensure consistent flavor and production efficiency. The dehydration process enhances the naturally rich umami taste of tomatoes, allowing for improved flavor profiles without significant reliance on artificial additives. This aligns with the growing consumer preference for clean-label and natural ingredients.

The onion segment is projected to grow at a CAGR of 8.56% through 2031, making it the fastest-growing category within the product-type segment. This growth is driven by onions' essential role as a base ingredient in global cuisines and their extensive use in processed food formulations. Dehydrated onions are widely utilized in products such as soups, sauces, ready meals, spice blends, and snack seasonings due to their robust flavor, ease of handling, and extended shelf life. These attributes make them highly valuable for food manufacturers seeking consistency and operational efficiency. Additionally, strong export momentum, particularly from major producing regions like India, supports this segment's growth. For example, according to the Agricultural and Processed Food Products Export Development Authority (APEDA), Gujarat's dehydrated white onion exports increased by 67% in the financial year 2023–24, reflecting rising global demand and enhanced supply capabilities.

By Form: Powder and Flakes Reign, Whole Pieces Niche

The powder and flakes segment accounted for 42.89% of form-based revenue in 2025 and is projected to grow at a CAGR of 7.91% through 2031. This growth is attributed to their superior functionality, processing efficiency, and broad applicability within the food industry. These forms are particularly favored for their excellent solubility and dispersion properties, making them ideal for use in liquid and semi-solid food systems such as soups, sauces, dressings, and ready-to-eat meals. Their fine and uniform texture ensures consistent flavor distribution, a critical factor in large-scale food manufacturing. Furthermore, powders and flakes are easier to handle, measure, and store compared to bulkier or irregular forms, enhancing their compatibility with automated production lines and modern food processing technologies.

The slices and cuts segment is essential for rehydration-intensive applications, including camping meals, military rations, and emergency food supplies, where preserving the original shape, texture, and identity of vegetables after rehydration is crucial. These formats are particularly preferred in applications requiring visual appeal and a closer resemblance to fresh vegetables once prepared, thereby improving the overall eating experience in dehydrated meal solutions. Their effective rehydration capabilities, combined with the ability to retain structural integrity, make them well-suited for ready-to-cook meal kits, outdoor food products, and institutional catering, where both functionality and presentation are important. Whole pieces occupy a niche yet premium position in the market, often associated with high-quality, minimally processed offerings. These products cater to consumers seeking premium options that emphasize natural and less processed food attributes.

By Drying Technology: Freeze Drying Leads, Drum and Spray Surge

The freeze drying segment accounted for 40.03% of technology-based revenue in 2025 and continues to lead the global dehydrated vegetables market. This dominance is attributed to its superior ability to preserve product quality, nutritional value, and sensory characteristics. Operating at low temperatures, freeze drying retains heat-sensitive nutrients, natural color, aroma, and structural integrity, making freeze-dried vegetables closely comparable to fresh ones upon rehydration. Consequently, they are widely used in premium food applications where quality and authenticity are essential, such as ready-to-eat meals, functional foods, and high-end culinary products. Furthermore, freeze-dried vegetables exhibit excellent rehydration properties, quickly regaining their original texture and appearance, which enhances consumer acceptance and expands their application across various food formats.

The drum and spray drying segment is projected to grow at a CAGR of 8.61% through 2031, representing the fastest growth among drying technologies. This growth is driven by its cost-effectiveness, scalability, and suitability for high-volume food processing applications. These technologies are particularly efficient in producing fine powders and uniform dehydrated ingredients, making them ideal for manufacturing soups, sauces, seasonings, instant mixes, and snack flavorings. Their ability to convert large quantities of vegetable purees and extracts into stable, easy-to-handle powdered forms ensures consistent quality and rapid production cycles, meeting the rising demand for convenience and processed foods. Additionally, drum and spray drying offer shorter processing times and compatibility with continuous production systems, improving operational efficiency and throughput for manufacturers.

By Distribution Channel: Retail Dominates, Foodservice Accelerates

Retail channels accounted for 70.03% of distribution revenue in 2025, dominating the global dehydrated vegetables market due to their extensive consumer reach, product accessibility, and alignment with evolving household consumption patterns. Retail formats such as supermarkets, hypermarkets, convenience stores, and online platforms offer consumers easy access to a wide variety of dehydrated vegetable products in different forms and packaging sizes. These formats cater to both daily cooking needs and long-term storage preferences. The dominance of this channel is further supported by the growing preference for convenience-driven meal preparation, where consumers seek ready-to-use ingredients that save preparation time without compromising flavor or nutrition. Additionally, retail environments enhance product visibility, branding, and variety, enabling consumers to compare options and select products based on quality, format, and usage requirements.

The foodservice segment is projected to grow at a CAGR of 8.76% through 2031, driven by the increasing reliance of commercial kitchens on efficient, consistent, and time-saving ingredient solutions. Dehydrated vegetables are highly valued in foodservice operations, including restaurants, hotels, catering services, and institutional kitchens, due to their extended shelf life, reduced storage needs, and ease of handling. These attributes streamline back-end operations and help minimize food waste. Their ready-to-use nature eliminates labor-intensive tasks such as washing, peeling, and chopping, enabling faster preparation and consistent quality across dishes. Additionally, dehydrated vegetables ensure year-round availability of ingredients that may otherwise be seasonal, supporting menu standardization and operational stability.

Geography Analysis

North America accounted for 34.09% of the global dehydrated vegetables market value in 2025, maintaining its leading position due to its highly developed food processing ecosystem and strong demand for convenience-oriented food products. The widespread consumption of ready-to-eat and ready-to-cook meals, along with the high penetration of packaged and processed foods, continues to drive the adoption of dehydrated vegetables across various applications. Additionally, well-established supply chains, advanced dehydration technologies, and a focus on product standardization and quality consistency further support the region's market dominance. The mature retail and foodservice landscape in North America also benefits the market, as the long shelf life, ease of storage, and operational efficiency of dehydrated vegetables make them a preferred ingredient choice.

Asia-Pacific is projected to grow at the fastest CAGR of 9.03% through 2031, driven by rapid infrastructure development, increasing urbanization, and rising demand for convenience foods among the expanding middle-class population. Countries such as India are experiencing significant momentum, supported by strong government initiatives and investments in food processing capabilities. According to the India Brand Equity Foundation, India’s food processing sector reached USD 354.5 billion in 2024, with policy incentives actively channeling investments into cold storage infrastructure and dehydration facilities [3]Source: India Brand Equity Foundation, "Food Processing", ibef.org. This growth is enhancing production capacity, reducing post-harvest losses, and strengthening the supply chain for dehydrated vegetables. Additionally, increasing awareness of convenience foods and the growing adoption of packaged meal solutions in urban centers are accelerating regional demand.

Europe, South America, and the Middle East and Africa collectively account for the remaining share of global demand, each exhibiting unique growth dynamics influenced by regional consumption patterns and industry structures. Europe demonstrates a strong preference for clean-label, natural, and minimally processed food ingredients, supporting the use of dehydrated vegetables in premium and health-focused applications. South America is experiencing gradual growth, driven by expanding food processing activities and the increasing incorporation of dehydrated ingredients in local cuisines. In the Middle East and Africa, rising demand is attributed to improving food distribution networks, increasing urbanization, and the need for shelf-stable food products in regions with challenging climatic conditions.

Competitive Landscape

The dehydrated vegetables market is moderately fragmented, with multinational ingredient and flavor companies competing alongside regional specialists. Competition is based on factors such as scale, processing capabilities, and technological differentiation. Global players like Sensient Technologies Corp. utilize advanced processing technologies and robust Research and Development (R&D) capabilities to deliver high-quality, standardized products for diverse applications. Meanwhile, regionally focused companies such as Jain Farm Fresh Foods Ltd., BCFoods Inc., Harmony House Foods Inc., and Garon Dehydrates Pvt. Ltd. maintain strong market positions by leveraging localized sourcing, cost efficiencies, and specialized product offerings. This competitive environment highlights the importance of both global reach and regional expertise in market positioning.

Vertical integration strategies are increasingly shaping competition in the market. Companies are focusing on securing consistent raw material supplies, improving traceability, and enhancing cost control across the value chain. Many players are integrating backward into farming and primary processing while investing in advanced dehydration technologies such as freeze drying and spray drying. These efforts aim to improve product quality and expand the scope of applications. Vertical integration reduces reliance on external suppliers, ensures better quality control, and allows for greater customization to meet the needs of end-use industries. Additionally, technological advancements in preserving flavor, color, and nutritional value have become critical competitive factors, enabling companies to cater to premium and functional food segments.

Despite the presence of established players, significant opportunities remain in areas such as allergen-free production lines and blockchain-enabled traceability systems. These capabilities are becoming increasingly important for institutional buyers and large food manufacturers that must adhere to stringent food safety regulations and mitigate liability risks. Companies offering transparent sourcing, clean-label compliance, and enhanced traceability are gaining a competitive advantage. As regulatory scrutiny intensifies and demand for high-quality, safe, and traceable ingredients grows, innovations in supply chain transparency and specialized production capabilities are expected to further influence the competitive dynamics of the dehydrated vegetables market.

Dehydrated Vegetables Industry Leaders

-

Sensient Technologies Corp.

-

Jain Farm Fresh Foods Ltd.

-

BCFoods Inc.

-

Harmony House Foods Inc.

-

Garon Dehydrates Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: HyFun Foods has inaugurated India's largest potato flake production line at its manufacturing facility in Mehsana. This new production line has an annual capacity of 18,000 metric tons (MT), enhancing the company's potato processing capabilities within the country.

- December 2024: Qingdao Wanlin Food Co. enhanced its market position by establishing a new production facility in the Turkestan Region. The facility focuses on producing dehydrated vegetables, primarily onions and garlic, reflecting the company's efforts to expand processing capabilities and address the increasing market demand for processed vegetable products.

Global Dehydrated Vegetables Market Report Scope

Dehydrated vegetables are fresh vegetables that undergo carefully controlled drying methods, including freeze drying, vacuum drying, or spray drying. The dehydrated vegetables market is segmented by product type, form, drying technology, distribution channel, and geography. Based on product type, the market is segmented intotomato, potato, onion, carrot, peas and other vegetables. Based on form, the market is segmented slices/cuts, minced/granules, whole pieces, and Powder/Flakes. Based on Drying Technology, the market is segmented into freeze drying, vacuum drying, drum and spray drying, and others. Based on distribution channel, the market is segmented into foodservice and off-trade. Off-trade segment is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Tomato |

| Potato |

| Onion |

| Carrot |

| Peas |

| Other Vegetables |

| Slices/Cuts |

| Minced/Granules |

| Whole Pieces |

| Powder/Flakes |

| Freeze Drying |

| Vacuum Drying |

| Drum and Spray Drying |

| Others |

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Tomato | |

| Potato | ||

| Onion | ||

| Carrot | ||

| Peas | ||

| Other Vegetables | ||

| By Form | Slices/Cuts | |

| Minced/Granules | ||

| Whole Pieces | ||

| Powder/Flakes | ||

| By Drying Technology | Freeze Drying | |

| Vacuum Drying | ||

| Drum and Spray Drying | ||

| Others | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand be by 2031?

The dehydrated vegetables market is forecast to reach USD 12.01 billion by 2031, expanding at a 7.51% CAGR from 2026.

Which product type leads current sales?

Tomato powder leads with 23.09% of 2025 revenue, reflecting its use across sauces, soups, and seasonings.

Which region is growing the fastest to 2031?

Asia-Pacific is projected to grow at 9.03% annually, driven by infrastructure investment and rising convenience-food demand.

What technology is gaining cost traction?

Drum and spray drying, boosted by energy-saving platforms such as ZeoDry, is expected to post an 8.61% CAGR through 2031.

Page last updated on: