Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

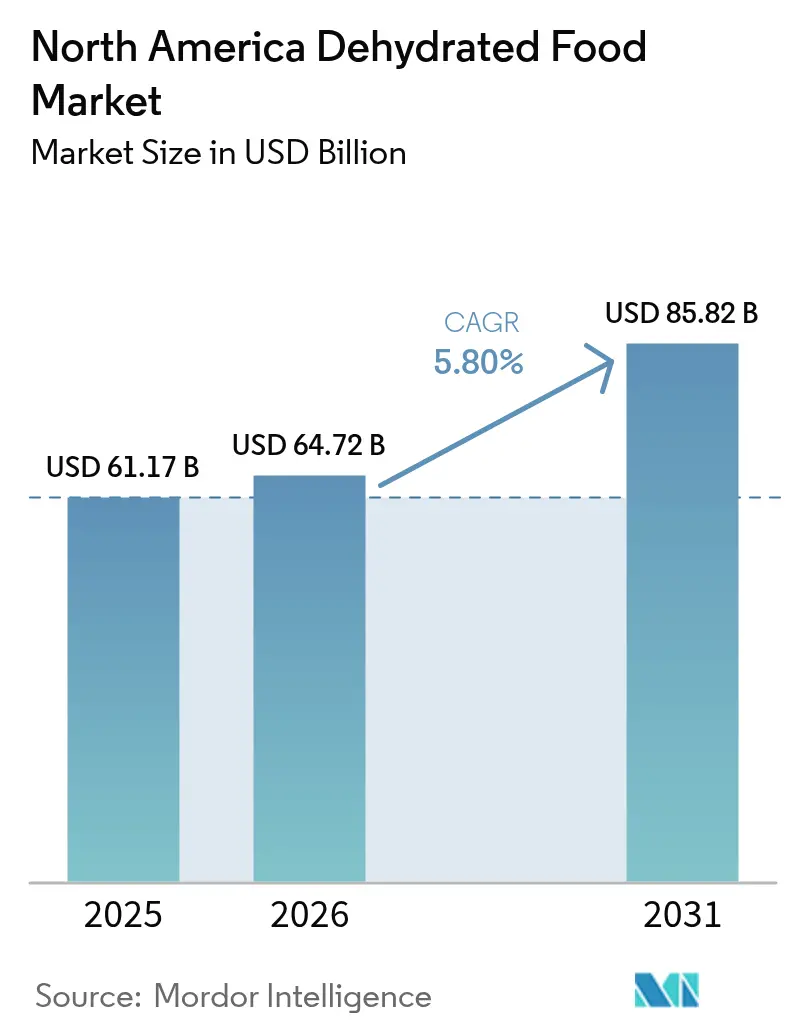

| Base Year Market Size (2025) | USD 61.17 Billion |

| Market Size (2026) | USD 64.72 Billion |

| Market Size (2031) | USD 85.82 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Dehydrated Food Market Analysis by Mordor Intelligence

The North America dehydrated food market size was valued at USD 61.17 billion in 2025 and estimated to grow from USD 64.72 billion in 2026 to reach USD 85.82 billion by 2031, at a CAGR of 5.80% during the forecast period (2026-2031). This growth is primarily driven by consumers in the United States, Canada, and Mexico, who increasingly prioritize convenience, nutritional value, and extended shelf life in their food choices. Urban households are increasingly adopting shelf-stable meal solutions as a precautionary measure against potential supply chain disruptions, ensuring food availability during uncertain times. Simultaneously, outdoor enthusiasts, such as hikers and campers, are favoring lightweight, nutrient-dense food options that cater to their needs during back-country travel and other outdoor activities. The trend of premiumization within the market has gained significant momentum, supported by advancements in freeze-drying technologies and the growing demand for clean-label formulations. These developments align with the rising disposable incomes of consumers, enabling them to opt for higher-quality products. Producers are increasingly leveraging direct-to-consumer sales channels, subscription-based programs, and e-commerce logistics to expand their market reach. These strategies not only enhance accessibility but also provide valuable data-driven insights that inform and refine product development processes. Furthermore, investments in energy-efficient dehydration equipment and vertically integrated organic supply chains are playing a pivotal role in reducing operational costs. These advancements are creating sustainable and profitable opportunities for both established market players and new entrants, ensuring long-term growth and competitiveness within the industry.

Key Report Takeaways

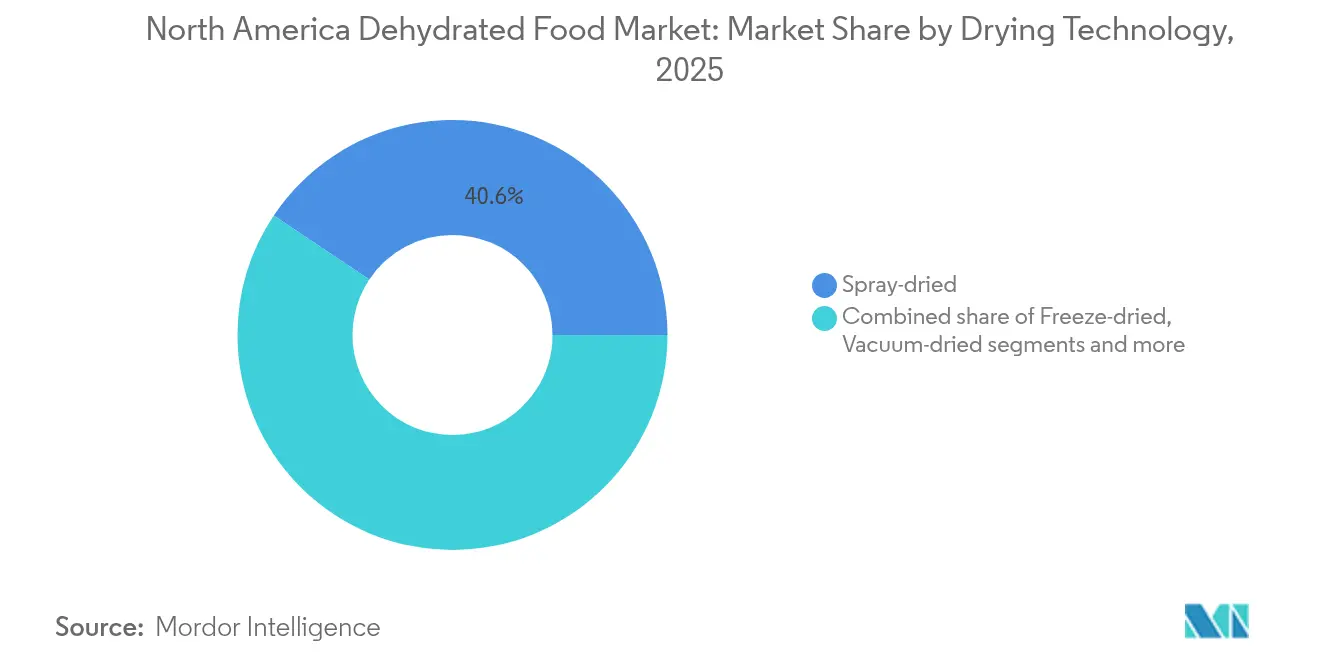

- By drying technology, spray-dried products led with 40.62% of North America dehydrated food market share in 2025, while freeze-dried formats are projected to expand at a 6.37% CAGR through 2031.

- By product category, fruits and vegetables held 34.92% share of the North America dehydrated food market size in 2025; nutraceutical and functional powders are advancing at a 6.41% CAGR to 2031.

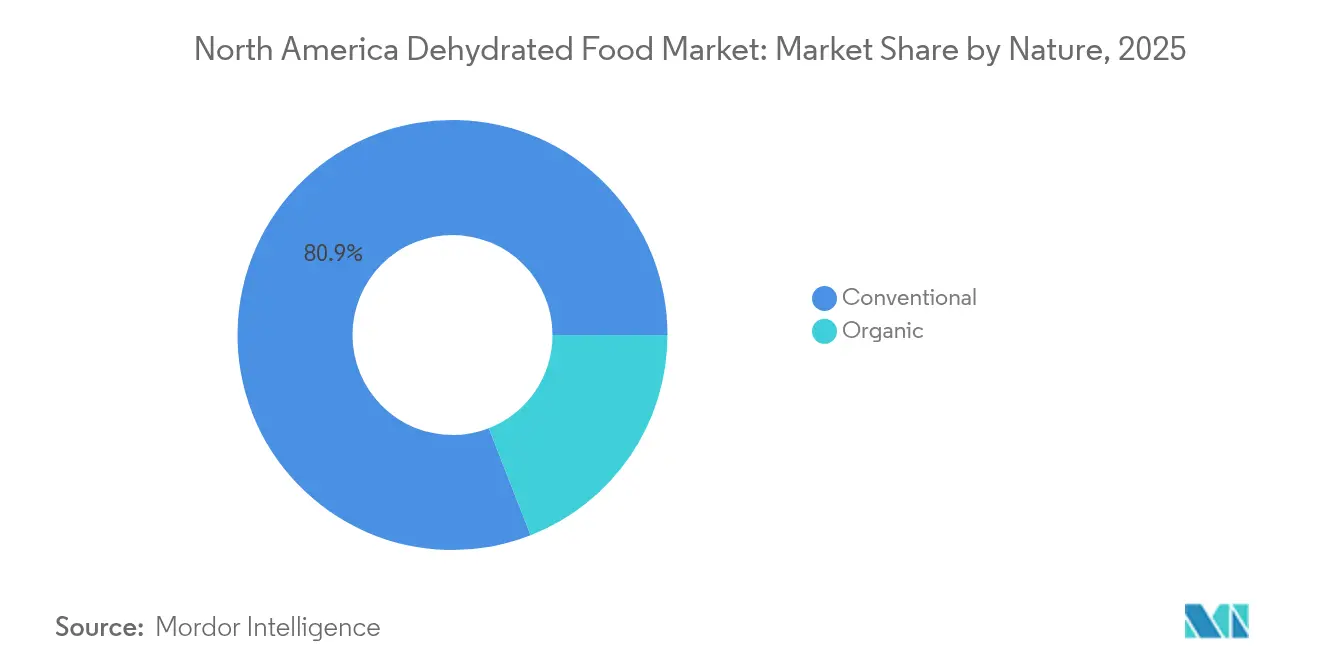

- By nature, conventional offerings accounted for 80.92% share of the North America dehydrated food market size in 2025, whereas organic variants are forecast to climb at a 6.52% CAGR.

- By end user, industrial packaged food captured 48.12% revenue in 2025, yet retail is expanding at a 6.66% CAGR on the strength of e-commerce and subscription models.

- By geography, the United States contributed 77.61% of 2025 regional sales, but Mexico is expected to register the fastest 6.29% CAGR through 2031 as its middle class expands.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Dehydrated Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient, shelf-stable foods among busy urban households | +1.2% | United States, Canada (urban cores), Mexico (emerging middle class) | Short term (≤ 2 years) |

| Growth in outdoor and adventure activities | +0.8% | United States (national parks, trail networks), Canada (wilderness tourism) | Medium term (2-4 years) |

| Advancements in dehydration technologies | +1.1% | United States and Canada | Medium term (2-4 years) |

| Shift toward clean-label, organic, and natural dehydrated foods | +1.0% | United States, Canada (coastal markets), Mexico (urban centers) | Long term (≥ 4 years) |

| Expansion of plant-based and vegan diets | +0.9% | United States, Canada (metropolitan areas) | Long term (≥ 4 years) |

| Growing consumer awareness of nutritional retention in dehydrated products | +0.7% | United States, Canada, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient, Shelf-Stable Foods Among Busy Urban Households

Time-starved professionals and dual-income families are increasingly adapting their meal-planning strategies to prioritize products that eliminate the need for refrigeration and help minimize food waste. Dehydrated soups, instant meals, and vegetable powders are particularly well-suited for urban micro-kitchens, where limited freezer space poses a challenge. According to the US Census Bureau, single-person households represented 38.1% of all American homes in 2023[1]Source: US Census Bureau, "Number of single-person households U.S.", census.gov. This demographic group demonstrates a strong preference for food options that are portion-controlled and have extended shelf lives. However, this shift is not solely driven by convenience. It also reflects a broader risk-averse mindset that emerged during the pandemic, when stockpiling behaviors became commonplace, normalizing the practice of maintaining a 30-day pantry reserve. In response to these evolving consumer preferences, retailers have expanded the shelf space allocated to dehydrated meal kits. These products are often strategically placed alongside ambient pasta and canned goods to encourage basket-building and maximize sales opportunities.

Growth in Outdoor and Adventure Activities

With the outdoor recreation industry on the rise, hiking, camping, and adventure sports enthusiasts are increasingly demanding lightweight, nutrient-dense food solutions. According to the Outdoor Foundation, over 56 million Americans aged six and older went camping in 2024, marking a significant increase compared to previous decades[2]Source: Outdoor Foundation, "2025 Sports, Fitness, and Leisure Activities Topline Participation Report", sfia.users.membersuite.com. Freeze-dried entrees deliver a critical 4:1 weight-to-nutrition advantage over canned alternatives, an essential factor for multi-day treks where carrying all provisions is necessary. Similarly, Canada's outdoor recreation economy has grown, with Parks Canada reporting a rise in backcountry camping permits in 2024, particularly in British Columbia and Alberta. This trend also benefits from crossover appeal, as emergency-preparedness enthusiasts stockpile the same freeze-dried products used by backpackers, creating dual revenue streams that mitigate the seasonal demand fluctuations typical in outdoor recreation. Additionally, the growing popularity of van life and overlanding has expanded the target audience. Beyond traditional backpackers, car campers and RV travelers now value the storage efficiency and convenience of dehydrated foods.

Advancements in Dehydration Technologies

Since 2024, manufacturers of freeze-drying equipment have successfully reduced cycle times by 15-20%. This achievement stems from advancements in vacuum-pump efficiency and heat-transfer optimization, which have significantly lowered production costs per unit. These cost reductions have enabled processors to target mid-tier price points, a segment previously dominated by spray-dried products. The introduction of next-generation freeze-dryers has further revolutionized the industry by preserving the cellular structure of fruits and vegetables more effectively than older systems. This improvement ensures better texture and color retention during rehydration, enhancing the overall quality of freeze-dried products. Simultaneously, spray-drying technology has also seen notable progress with the development of multi-stage drying towers. These towers are specifically designed to retain volatile flavor compounds, particularly in products like coffee and dairy powders, which are highly sensitive to flavor loss. These technological advancements hold strategic importance as they significantly reduce the quality gap between premium freeze-dried products and commodity spray-dried alternatives. Consequently, industry players are now compelled to shift their focus toward differentiation through innovative formulations and branding strategies, rather than relying solely on the drying process to maintain a competitive edge.

Shift Toward Clean-Label, Organic, and Natural Dehydrated Foods

As consumers pay closer attention to ingredient panels, manufacturers are under growing pressure to reformulate their legacy products. The scrutiny primarily targets artificial preservatives, anti-caking agents, and synthetic colors, as failing to address these concerns could result in losing shelf space to clean-label competitors. In 2024, U.S. sales of certified organic products experienced significant growth, achieving an annual growth rate of 5.2%, which is more than double the growth rate of the overall market, according to the Organic Trade Association [3]Source: Organic Trade Association, "Growth of U.S. Organic Marketplace Accelerated in 2024", ota.com. Retailers have observed that organic dehydrated vegetables and fruits command a price premium of 20-30%, yet their sell-through rates remain comparable to non-organic alternatives. This trend highlights that consumers perceive organic certification as an indicator of superior quality and safety. Additionally, this shift aligns with the growing adoption of plant-based diets, as vegan consumers increasingly prefer dehydrated products that exclude dairy-derived flow agents and other additives sourced from animals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy consumption in advanced dehydration processes | -0.6% | United States, Canada (regions with high electricity costs) | Short term (≤ 2 years) |

| Intense competition from fresh produce and frozen foods | -0.5% | United States, Canada (urban areas with robust cold-chain infrastructure) | Medium term (2-4 years) |

| Stringent food safety and labeling regulations | -0.3% | United States (FDA oversight), Canada (CFIA), Mexico (COFEPRIS) | Long term (≥ 4 years) |

| Dependence on seasonal raw material availability | -0.4% | United States (agricultural regions), Mexico (fruit-growing zones) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption in Advanced Dehydration Processes

Freeze-drying and vacuum-drying processes require a controlled environment with consistently low pressure and precise temperature management. These operations are significantly energy-intensive, consuming 3-5 times more electricity per kilogram of the finished product compared to spray-drying. The energy costs associated with these processes are largely fixed, leaving processors with limited opportunities to reduce expenses through operational efficiencies. As utility providers transition away from coal-fired power generation and adopt intermittent renewable energy sources, challenges related to grid reliability and demand-charge structures further complicate cost management. Smaller freeze-dry operators, who lack access to captive solar or wind energy installations, are at a structural disadvantage when compared to multinational corporations. These larger competitors benefit from economies of scale, enabling them to distribute energy procurement across multiple facilities and negotiate favorable long-term power-purchase agreements, thereby reducing their overall energy costs.

Intense Competition from Fresh Produce and Frozen Foods

Supermarket chains have made substantial investments in expanding their refrigerated and frozen-food sections. This strategic move provides consumers with year-round access to a variety of products, including berries, vegetables, and prepared meals, which closely replicate the sensory qualities of fresh food. Frozen vegetables, in particular, benefit from advanced flash-freezing technologies that preserve nutrients at their peak ripeness. This feature appeals strongly to health-conscious consumers, who often perceive frozen foods as "less processed" compared to dehydrated alternatives. The competitive intensity is especially pronounced in urban markets, where well-developed cold-chain infrastructure supports the availability of frozen products. In these markets, consumers tend to prioritize taste and texture over extended shelf life. Consequently, dehydrated-food manufacturers are focusing on highlighting specific use cases, such as outdoor activities like camping, emergency preparedness kits, and international shipping, where frozen products are less practical or viable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drying Technology: Freeze-Drying Gains Despite Spray-Dried Dominance

Spray-dried products accounted for 40.62% of market share in 2025, supported by significant investments in atomization towers and strong partnerships with instant-coffee roasters and dairy cooperatives. Although freeze-dried products represent a smaller volume, they are growing at a robust 6.37% CAGR through 2031, driven by rising demand from outdoor recreation and premium retail positioning. Vacuum-dried products cater to niche markets, such as pharmaceutical-grade nutraceuticals and specialty tea blends, where gentle moisture removal preserves delicate bioactive compounds. In Mexico and rural US regions, sun and solar-drying methods remain prominent in artisanal fruit and herb segments, benefiting from low labor costs and favorable climate conditions. Meanwhile, innovative drying technologies, such as microwave-assisted and infrared methods, are still in pilot phases but show potential for reducing energy consumption.

The gap between the dominant market share of spray-drying and the rapid growth of freeze-drying highlights a divergence in the value chain. Industrial bakeries and snack manufacturers favor the cost efficiency of spray-drying for commodity ingredients. Conversely, consumer brands are increasingly adopting freeze-drying to achieve premium pricing and stand out with unique textures. This dynamic presents a strategic challenge for processors: whether to sustain the high-volume, low-margin spray-dried business or transition to the capital-intensive, smaller-batch freeze-dried production. Hybrid facilities that can switch between technologies based on seasonal demand and contract requirements are emerging as a competitive advantage, particularly for mid-sized processors serving both industrial and retail markets.

By Product Category: Nutraceuticals Surge as Fruits Dominate

In 2025, fruits and vegetables contributed 34.92% of product-category revenue, highlighting their versatility in retail snacking, foodservice applications, and industrial soup and sauce production. Although nutraceutical and functional powders represent a smaller segment, they are experiencing growth, expanding at a 6.41% CAGR through 2031. This growth is primarily driven by sports-nutrition brands and meal-replacement formulators focusing on clean-label protein and fiber sources. While food-safety concerns and consumer skepticism about rehydrated animal proteins pose challenges, niche players have successfully positioned themselves in jerky-adjacent snacks and survival-food kits. Dairy and egg powders primarily serve institutional bakeries and food-aid programs, with demand closely linked to commodity milk prices and government procurement cycles. In North America, instant coffee and beverage powders face mature growth trends, but innovations like single-serve pod systems and cold-brew concentrates are reshaping coffee consumption habits.

Prepared meals and soups are a competitive category where dehydrated formats directly compete with frozen and refrigerated alternatives. Success in this segment requires expertise in formulation, balancing sodium content, ensuring quick rehydration, and enhancing flavor complexity, along with strategic distribution partnerships, particularly with outdoor retailers and emergency-preparedness channels. Spices, herbs, and seasonings maintain steady demand from foodservice operators and home cooks, with differentiation largely limited to organic certifications and country-of-origin labeling. The growing prominence of nutraceuticals is significant, reflecting a shift in consumer perception of dehydrated products. These products are increasingly seen not just as shelf-stable alternatives to fresh foods but as concentrated nutrient-delivery solutions that align with modern wellness and performance goals.

By Nature: Organic Accelerates Amid Conventional Scale

Conventional dehydrated products accounted for 80.92% of the market share in 2025, driven by established agricultural supply chains and pricing strategies designed for the mass market. At the same time, organic variants are experiencing significant growth, with a 6.52% CAGR projected through 2031. This growth is particularly evident in coastal urban markets, where higher disposable incomes support premium pricing. Retailers are increasingly prioritizing USDA-certified products to align with corporate sustainability objectives. The organic growth rate surpasses the overall market CAGR by nearly one percentage point, highlighting strong consumer demand for organic certification despite broader economic challenges. On the supply side, organic fruit and vegetable acreage in the U.S. expanded in 2024, easing procurement challenges that previously hindered organic dehydrated food production.

Processors are carefully evaluating the decision to pursue organic certification. The USDA National Organic Program enforces strict record-keeping and facility-segregation requirements, which increase compliance costs and pose challenges for smaller operators. However, organic certification provides access to natural-foods retailers and e-commerce platforms that typically exclude conventional products, creating a segmented distribution landscape. To address this, many forward-thinking manufacturers are investing in dual production lines, one for organic and one for conventional products, ensuring they can serve both markets without cross-contamination risks. Although this approach requires significant upfront investment, it positions companies to capture market share as organic products gain traction beyond early adopters and into mainstream grocery channels.

By End User: Retail Surges as Industrial Holds

In 2025, industrial packaged food constituted 48.12% of end-user demand, supported by long-term supply agreements with snack producers, ready-meal assemblers, and institutional foodservice distributors. Retail channels, expanding at a 6.66% CAGR through 2031, are surpassing industrial segments. This growth is fueled by direct-to-consumer brands bypassing traditional wholesalers and capitalizing on subscription models and branded e-commerce platforms. Foodservice operators, including restaurants and catering companies, consistently utilize dehydrated ingredients for soups, sauces, and seasoning blends. However, growth in this segment is limited by labor shortages and the cyclical nature of menu innovations. In the retail sector, supermarkets and hypermarkets continue to dominate transaction volumes, but online stores are rapidly expanding. This trend is particularly evident for bulkier freeze-dried meal kits, which consumers increasingly prefer to have delivered rather than carrying home from physical stores.

Specialty and convenience stores occupy distinct niches. Specialty retailers focus on organic and artisanal dehydrated products, appealing to health-conscious consumers. Conversely, convenience stores stock single-serve dehydrated soups and instant noodles, catering to on-the-go customers. The retail growth trajectory reflects a shift in consumer behavior: younger demographics are more inclined to research products online, read reviews, and subscribe to auto-replenishment programs that reduce per-unit costs. In contrast, industrial buyers prioritize consistent supply and price stability, often placing less emphasis on brand narratives. This divergence necessitates tailored sales and marketing strategies. Manufacturers excelling in both areas typically establish separate business units with distinct market approaches, recognizing that a unified sales force cannot effectively address the needs of both industrial procurement managers and retail consumers.

Geography Analysis

In 2025, the United States. led North America's dehydrated food market, capturing a significant 77.61% share. This dominance stems from its well-established distribution networks, high per-capita consumption of prepared meals, and a strong outdoor recreation infrastructure. Freeze-dried backpacking meals, instant soups, and dehydrated vegetable powders are widely available across grocery chains, outdoor specialty stores, and e-commerce platforms. However, the U.S. market's maturity results in slower growth compared to Mexico's emerging segments, where urbanization and increasing disposable incomes are expanding the consumer base. The U.S. Food and Drug Administration's 2024 updates to food-labeling regulations, focusing on allergen declarations and nutrient-content claims, have raised compliance costs for dehydrated-food manufacturers while creating higher entry barriers for smaller players lacking regulatory expertise.

Mexico is projected to grow at a 6.29% CAGR through 2031, the fastest rate among North American regions. This growth is driven by the expanding middle class in cities like Mexico City, Guadalajara, and Monterrey, who are increasingly adopting convenience-focused meal solutions. Government initiatives, such as subsidized loans for small and medium-sized enterprises, are modernizing food processing infrastructure and reducing capital barriers for domestic dehydrated-food producers. Mexican consumers' strong cultural preference for dried chiles, herbs, and spices provides a natural entry point for broader adoption of dehydrated products. However, cold-chain limitations in rural areas and a fragmented retail landscape give shelf-stable dehydrated formats a structural advantage over frozen alternatives, supporting sustained market penetration.

Canada's dehydrated food market is growing steadily but faces limitations due to its smaller population and demand concentration in Ontario, Quebec, and British Columbia. The Canadian Food Inspection Agency's regulations closely align with U.S. FDA standards, facilitating cross-border trade but limiting differentiation opportunities for Canadian processors. Outdoor recreation, particularly backcountry camping and wilderness tourism, remains a key driver of demand, sustaining freeze-dried meal sales in Alberta and British Columbia. Meanwhile, the "Rest of North America," which includes Caribbean and Central American regions with economic ties to the U.S. and Canada, accounts for a minor market share. However, it offers niche opportunities for exporters targeting the tourism and hospitality sectors in resort destinations.

Competitive Landscape

The North American dehydrated food market is moderately fragmented. Multinational conglomerates control the spray-drying capacity for commodity ingredients, while specialized freeze-dry operators dominate premium niches such as outdoor and emergency-preparedness markets. Incumbents leverage scale advantages in procurement, energy contracting, and distribution. However, technology-driven disruptors are utilizing direct-to-consumer channels and subscription models to bypass traditional retail gatekeepers. Key strategies in the market include vertical integration into organic farming, co-packing partnerships to distribute fixed costs across multiple brands, and geographic expansion into Mexico to capture faster-growing demand.

Opportunities remain untapped in hybrid retail-foodservice formats, such as dehydrated meal kits designed for restaurant chains aiming to reduce kitchen labor. Additionally, functional-food formulations that integrate adaptogens or probiotics into dehydrated bases present growth potential. Manufacturers are focusing on product innovation to align with shifting consumer preferences. Expansion is a critical strategy for players seeking to enhance competitiveness. Production innovation is particularly favored, as key players strive to meet demand and stay competitive in the market. Leading players include Thrive Foods, LLC, Van Drunen Farms, Harmony House Foods Inc., Mother Earth Products, andThe Kraft Heinz Company.

Patent filings in 2024 indicate growing interest in energy-efficient drying methods and texture-optimization techniques, with many applicants focusing on microwave-assisted freeze-drying systems. Emerging disruptors include plant-based meal-kit startups promoting dehydrated ingredients as zero-waste solutions and e-commerce-native brands leveraging customer data to customize flavor profiles and portion sizes. Compliance with ISO 22000 food-safety management standards and FSSC 22000 certification has become a standard requirement for suppliers serving major retail chains. While these certifications increase quality-assurance costs, they also consolidate market share among well-capitalized players capable of managing third-party audits and traceability systems.

North America Dehydrated Food Industry Leaders

-

Van Drunen Farms

-

Harmony House Foods Inc.

-

Mother Earth Products

-

Thrive Foods, LLC

-

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Open Farm has launched its new Freeze-Dried Raw Regeneratively Sourced Lamb Lung Treats. This product represents Open Farm's first-ever offering verified by the Land to Market initiative.

- May 2025: The Kraft Heinz Company has invested USD 3 billion to upgrade its U.S. factories, marking its largest plant investment in a decade. These upgrades are designed to enhance plant efficiency, reduce costs, and mitigate the impact of tariffs, which played a significant role in the company's decision to proceed with this investment.

- March 2024: Brothers All Natural has introduced its newest product, Infused Fruit Crisps. These crisps feature the sweetness of Fuji apples combined with the vibrant juices of three popular berries. The product was first showcased at the Natural Products Expo West in Anaheim, California. Infused Fruit Crisps are available in three enticing flavor combinations: Fuji Apples infused with Raspberry, Blueberry, and Strawberry.

North America Dehydrated Food Market Report Scope

By Drying Technology

| Spray-dried |

| Freeze-dried |

| Vacuum-dried |

| Sun / Solar-dried |

| Other Drying Technologies |

By Product Category

| Fruits and Vegetables |

| Meat and Seafood |

| Dairy and Eggs |

| Instant Coffee and Other Beverages |

| Prepared Meals and Soups |

| Spices, Herbs, and Seasonings |

| Nutraceutical and Functional Powders |

By Nature

| Conventional |

| Organic |

By End User

| Industrial Packaged Food | |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Drying Technology | Spray-dried | |

| Freeze-dried | ||

| Vacuum-dried | ||

| Sun / Solar-dried | ||

| Other Drying Technologies | ||

| By Product Category | Fruits and Vegetables | |

| Meat and Seafood | ||

| Dairy and Eggs | ||

| Instant Coffee and Other Beverages | ||

| Prepared Meals and Soups | ||

| Spices, Herbs, and Seasonings | ||

| Nutraceutical and Functional Powders | ||

| By Nature | Conventional | |

| Organic | ||

| By End User | Industrial Packaged Food | |

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the forecast value of the North America dehydrated food market in 2031?

The market is projected to reach USD 85.82 billion by 2031, reflecting a 5.80% CAGR.

Which drying technology is expanding fastest in North America?

Freeze-drying is growing at a 6.37% CAGR, driven by premium positioning and outdoor recreation demand.

Why is Mexico expected to outpace the United States in growth?

Rising middle-class incomes and government loans for food-processing modernization support a 6.29% CAGR in Mexico.

How large is the organic segment compared with conventional products?

Organic products hold a smaller base but are advancing at 6.52% CAGR, outpacing conventional growth.

Page last updated on: