Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

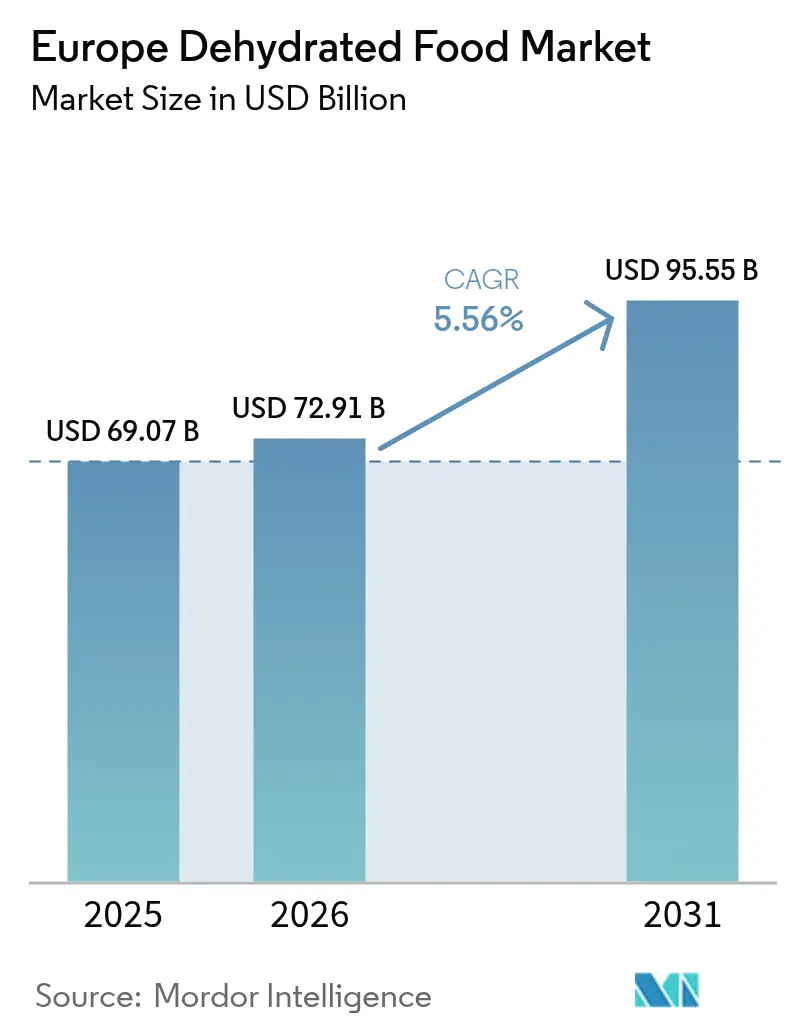

| Base Year Market Size (2025) | USD 69.07 Billion |

| Market Size (2026) | USD 72.91 Billion |

| Market Size (2031) | USD 95.55 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Dehydrated Food Market Analysis by Mordor Intelligence

The Europe Dehydrated Food Market size was valued at USD 69.07 billion in 2025 and estimated to grow from USD 72.91 billion in 2026 to reach USD 95.55 billion by 2031, at a CAGR of 5.56% during the forecast period (2026-2031). Key drivers include increasing demand for clean-label and organic products, on-the-go meal options, and functional powders, coupled with rising health consciousness and awareness of sustainability. Advances in spray-drying and freeze-drying technologies are facilitating the production of high-quality, long-shelf-life products, while innovations in protein-rich and specialty ingredients are broadening applications in industrial and foodservice sectors. The market is trending toward greater product diversification, premiumization, and alignment with consumer preferences for health, convenience, and environmentally friendly solutions.

Key Report Takeaways

- By drying technology, spray-dried products led with 39.15% of Europe Dehydrated Food market share in 2025, whereas freeze-drying is forecast to expand at a 5.58% CAGR through 2031.

- By product type, fruits and vegetables accounted for 37.62% of the Europe Dehydrated Food market size in 2025; nutraceutical and functional powders are projected to grow at a 6.44% CAGR to 2031.

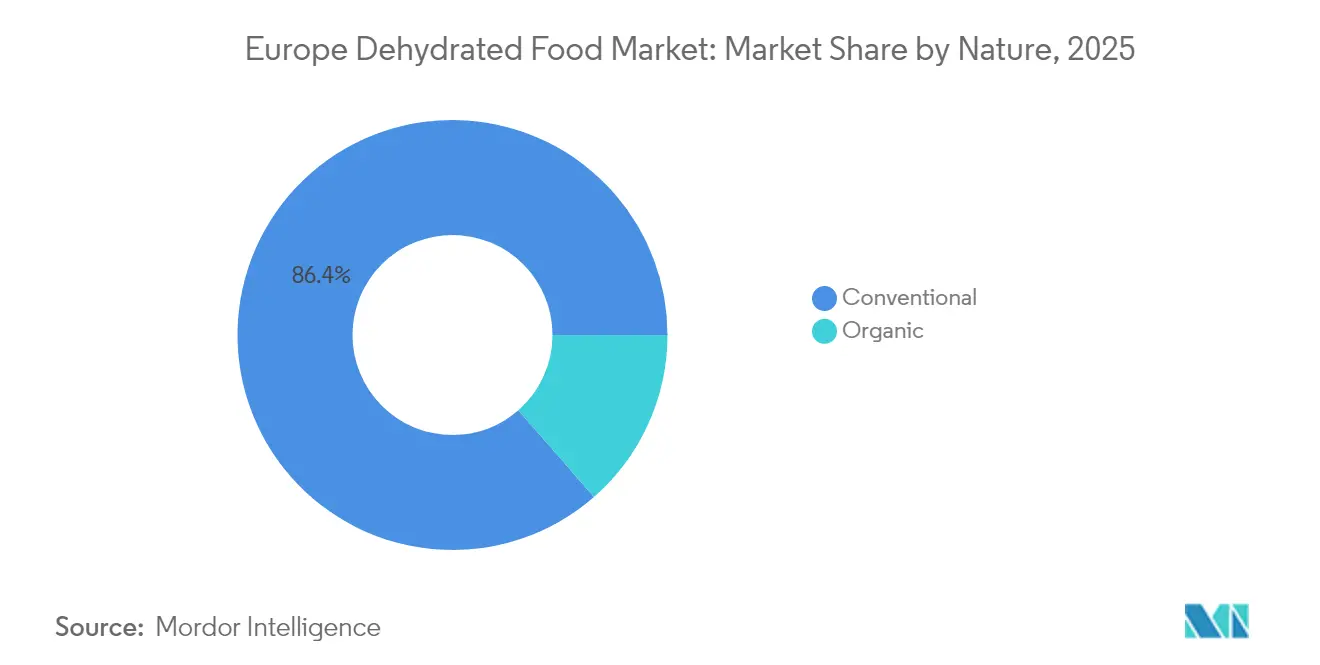

- By nature, conventional formats held 86.43% of Europe Dehydrated Food market volume in 2025, while organic products are set to rise at a 6.6% CAGR driven by stronger certification rules.

- By end user, industrial packaged food absorbed 48.75% of 2025 demand, yet retail channels are advancing at a 6.55% CAGR as supermarkets and e-commerce platforms widen single-serve camping meals and plant-based soup assortments.

- By geography, Germany captured 20.32% of 2025 revenue; Italy is poised for the fastest growth at a 6.02% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Dehydrated Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need for convenience and quick meal solutions | +1.2% | Pan-European, strongest in Germany, United Kingdom, Netherlands | Short term (≤ 2 years) |

| Clean-label/organic minimally processed food demand | +1.0% | Western Europe (Germany, France, Netherlands, Belgium), expanding to Italy, Spain | Medium term (2-4 years) |

| Increasing outdoor activities and travelling | +0.7% | Alpine regions (Germany, Italy), Scandinavia (Sweden), coastal Spain | Short term (≤ 2 years) |

| Sustainability awareness and eco-conscious consumer behavior | +0.9% | Nordic countries (Sweden), Germany, Netherlands, France | Medium term (2-4 years) |

| Improvements in dehydration technologies | +0.8% | Manufacturing hubs in Germany, Netherlands, Poland, United Kingdom | Long term (≥ 4 years) |

| Surge in plant-based and vegan diets | +1.1% | United Kingdom, Germany, Netherlands, Sweden, urban centers across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Need for convenience and quick meal solutions

The growing demand for convenience and quick meal solutions is a significant driver of the Europe dehydrated food market. Modern European consumers increasingly lead busy, urban lifestyles with limited time for cooking, which has heightened the need for foods that are easy to store, quick to prepare, and require minimal effort. Dehydrated foods address these requirements effectively, offering a long shelf life, lightweight storage, and simple rehydration or cooking. These attributes make them suitable for ready-to-eat or ready-to-cook meal solutions, meal-prep kits, and on-the-go consumption. This trend is evident in market data; for example, according to the Federal Statistical Office, the German convenience food processing industry generated approximately EUR 6.04 billion in revenue in 2024 [1]Source: Federal Statistical Office "Revenue in the convenience food manufacturing sector in Germany", destatis.de. This highlights that a significant portion of consumers in one of Europe’s largest economies is prioritizing convenience-focused food products. The notable revenue of this segment demonstrates how convenience and time-saving preferences are influencing food consumption patterns, positioning dehydrated foods to benefit from this shift in dietary habits.

Clean-label/organic minimally processed food demand

The demand for clean-label, organic, and minimally processed foods is profoundly driving growth in the Europe dehydrated food market. Consumers are increasingly seeking products that are natural, transparent, and free from artificial additives, preservatives, and excessive processing. Dehydrated foods, including fruits, vegetables, herbs, and meal components, perfectly align with these preferences due to their minimal processing, retention of nutrient content, and simple ingredient lists. This strong shift in consumer focus toward health, wellness, and clean-label attributes is compelling manufacturers to innovate and actively promote dehydrated products that meet these expectations, thereby significantly enhancing their market appeal. As a result, the rising emphasis on organic, natural, and minimally processed foods is becoming a pivotal growth driver, substantially expanding the market for dehydrated products across retail, foodservice, and industrial segments in Europe.

Increasing outdoor activities and travelling

Increasing outdoor activities and travel are key drivers of the Europe dehydrated food market. Consumers engaged in sports, hiking, camping, and other on-the-go activities require portable, lightweight, and long-shelf-life food options that are easy to carry and consume without preparation. Dehydrated foods, such as fruits, vegetables, snacks, and meal kits, effectively meet this demand by offering convenient nutrition in compact forms suitable for travel, outdoor adventures, and active lifestyles. For example, Sport England reported that in 2024, 30 million adults in England participated in sports or physical activities weekly, representing a significant population with active lifestyles that depend on convenient, nutrient-dense food options [2]Source: Sport England, "Sport England see record numbers playing sport", sportengland.org. This growing participation in outdoor and recreational activities directly drives the demand for dehydrated foods, positioning them as an essential choice for consumers seeking quick, portable, and health-conscious meal solutions during travel, exercise, or other active pursuits.

Sustainability awareness and eco-conscious consumer behavior

Sustainability awareness and eco-conscious consumer behavior are significantly influencing the growth of the Europe dehydrated food market. Consumers increasingly prefer products that minimize environmental impact, reduce food waste, and encourage responsible consumption. Dehydrated foods align with these preferences due to their extended shelf life, reduced spoilage, and ability to utilize surplus or seasonal produce that might otherwise be wasted, thereby contributing to circular and sustainable food systems. Furthermore, many producers in the market are adopting eco-friendly packaging and energy-efficient processing methods, which resonate with environmentally conscious consumers. Consequently, the combination of reduced food waste, lower transportation weight, and sustainable production practices is driving consumer preference for dehydrated products, positioning sustainability awareness as a critical factor for market growth across retail, foodservice, and industrial segments in Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and processing costs | -0.9% | Energy-intensive regions (Germany, Netherlands, Belgium), impacting all manufacturing hubs | Short term (≤ 2 years) |

| Competition from alternative foods | -0.6% | Pan-European, particularly in urban centers with access to fresh and frozen alternatives | Medium term (2-4 years) |

| Regulatory hurdles and compliance issues | -0.4% | EU-wide, with stricter enforcement in Germany, France, Netherlands | Long term (≥ 4 years) |

| Supply chain volatility | -0.5% | Southern Europe (Italy, Spain) for raw materials, Northern Europe for energy inputs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High production and processing costs

High production and processing costs remain a significant restraint for the Europe dehydrated food market, impacting both growth and profitability for manufacturers. Advanced dehydration methods, including freeze-drying, vacuum drying, and spray-drying, require specialized equipment, consume substantial energy, and demand strict quality control measures, all of which contribute to increased production expenses. These elevated costs often lead to higher retail prices, reducing the competitiveness of dehydrated products compared to fresh, frozen, or canned alternatives, particularly among price-sensitive consumers. For smaller producers and new entrants, the need for substantial capital investment and high operational costs creates barriers to entry and limits scalability, thereby restricting overall market growth. As a result, the high cost of production and processing continues to pose a significant challenge, slowing adoption and constraining the growth potential of dehydrated foods in Europe.

Regulatory hurdles and compliance issues

Regulatory hurdles and compliance issues pose a significant challenge for the Europe dehydrated food market. Manufacturers must address complex food safety, labeling, and quality standards that differ across countries. Compliance with these stringent regulations necessitates extensive documentation, testing, certification, and adherence to hygiene and processing standards, leading to increased operational costs and potential delays in product launches or market expansion. This is particularly burdensome for smaller producers or companies aiming for pan-European distribution, as navigating diverse regulatory requirements across multiple countries adds complexity and risk. For example, according to the Federal Office of Consumer Protection and Food Safety (BVL), as of May 2024, 109 warnings were issued regarding food products in Germany, reflecting the strict monitoring and enforcement environment manufacturers face [3]Source: Federal Office of Consumer Protection and Food Safety (BVL), "Number of published warnings about food products in Germany", bvl.bund.de. Such regulatory scrutiny highlights the risks and barriers associated with compliance, making regulatory challenges a significant restraint on the growth of the dehydrated food market in Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drying Technology: Freeze-Dried Gains on Premium Positioning

Spray-dried formats dominate the Europe dehydrated food market, accounting for 39.15% of total revenue in 2025. This reflects their widespread acceptance in both industrial and consumer-oriented applications. Spray drying is extensively used due to its ability to enable efficient, large-scale production of powders and granules with consistent quality. This method is particularly suitable for dehydrated dairy ingredients, fruit and vegetable powders, flavorings, seasonings, instant beverage mixes, and functional food components. Its capability to preserve aroma, color, and nutritional value, while producing shelf-stable and easy-to-handle ingredients, has made it the preferred choice for manufacturers seeking cost-effective and versatile dehydration solutions. Furthermore, many European food and beverage processors depend on spray-dried ingredients for reformulation, clean-label product development, and convenience-focused offerings, further driving its market share.

Freeze-dried products are projected to grow at a rate of 5.58% from 2026 to 2031, driven by their increasing appeal among European consumers who value high-quality, nutrient-retentive, and premium dehydrated food options. Freeze-drying is highly effective in preserving flavor, texture, color, and nutritional value compared to most other dehydration methods. This makes freeze-dried products particularly attractive to health-conscious consumers, premium food brands, specialty retailers, and industries such as sports nutrition, outdoor foods, and functional snacks. As clean-label and minimally processed trends gain momentum across Europe, freeze-dried fruits, vegetables, herbs, and ready-meal components are being increasingly incorporated into cereals, snacks, beverages, and convenience foods.

By Product Type: Nutraceuticals Surge as Functional Demand Escalates

In 2025, fruits and vegetables accounted for 37.62% of total sales, emphasizing their significant role in the Europe dehydrated food market. This dominance is attributed to strong consumer demand for natural, nutrient-rich, and versatile ingredients used in various applications, including snacks, bakery products, cereals, soups, ready meals, and health-focused beverages. Dehydrated fruits and vegetables align with macro-trends such as clean-label preferences, plant-based diets, convenience-driven consumption, and sustainability awareness. These products offer a long shelf life, reduced waste, and minimal processing while retaining much of their nutritional value. As consumers increasingly prioritize healthier and more natural food options, the substantial market share of dehydrated fruits and vegetables underscores their enduring relevance and growing applications across both retail and industrial segments.

Nutraceutical and functional powders are projected to grow at a rate of 6.44% through 2031, marking them as one of the fastest-growing product categories in the Europe dehydrated food market. This growth is driven by rising consumer interest in health optimization, immunity support, natural supplements, and performance nutrition. These trends have gained momentum as Europeans seek convenient, science-backed solutions to enhance overall wellness. Dehydrated functional powders, including herbal blends, protein powders, and micronutrient-enriched formulations, provide concentrated nutrition in easily consumable formats suitable for smoothies, supplements, sports drinks, and ready-to-mix functional beverages. Their long shelf life, portability, and alignment with clean-label and plant-based preferences further contribute to their increasing demand.

By Nature: Organic Accelerates Despite Conventional Dominance

In 2025, conventional products accounted for 86.43% of the market share, underscoring their dominance in the Europe dehydrated food market. This significant share is attributed to their widespread availability, cost-effectiveness, and well-established supply chains, making them the preferred choice for large-scale food manufacturers and mainstream retail consumers. Conventional dehydrated fruits, vegetables, and herbs remain highly competitive due to their lower production costs compared to organic alternatives. This cost advantage enables manufacturers to offer affordable pricing while maintaining consistent quality and volume. These products are extensively used as core ingredients in soups, sauces, snacks, ready meals, bakery formulations, and industrial food processing, ensuring steady and high-volume demand.

Organic dehydrated foods are projected to grow at a rate of 6.6% from 2026 to 2031, driven by the increasing consumer preference in Europe for clean-label, sustainably produced, and minimally processed food options. This growth is fueled by rising health consciousness, greater scrutiny of ingredient lists, and a preference for foods free from synthetic pesticides, additives, and GMOs. Organic dehydrated fruits, vegetables, herbs, and meal components align well with these consumer expectations, as they retain natural nutrition while offering long shelf life and versatility for use in snacks, cereals, beverages, baby food, and ready-to-cook applications. Additionally, the expanding retail availability, improved certification systems, and increased investment by food manufacturers in organic sourcing and processing are contributing to the growing mainstream acceptance of organic dehydrated products.

By End User: Retail Channels Outpace Industrial as E-Commerce Expands

By end user, the industrial packaged food segment accounted for 48.75% of total demand in 2025, underscoring its significant role in shaping the Europe dehydrated food market. This substantial share highlights the reliance of large food manufacturers on dehydrated ingredients, including fruit powders, vegetable flakes, and functional blends, for various applications. Dehydrated ingredients provide consistent quality, extended shelf life, ease of handling, and cost-effective storage, making them well-suited for high-volume industrial production where efficiency and uniformity are essential. Their ability to deliver concentrated flavor, color, and nutrition without additives aligns with the clean-label and reformulation trends prevalent in Europe’s packaged food industry. As manufacturers continue to expand offerings in convenience foods, plant-based products, and functional food categories, the demand for high-quality dehydrated inputs remains robust, solidifying the industrial packaged food segment as the largest and most influential end-user group.

Retail channels are projected to grow at a compound annual growth rate (CAGR) of 6.55% through 2031, driven by increasing consumer demand for accessible, shelf-stable, and versatile dehydrated food products across Europe. This growth is supported by the rising availability of dehydrated fruits, vegetables, herbs, snacks, and meal components in supermarkets, hypermarkets, organic stores, and specialty retailers. Additionally, the broader shift toward convenient home cooking, clean-label preferences, and healthier snacking habits is contributing to this trend. Retailers are allocating more shelf space to dehydrated and freeze-dried products as consumers seek natural, minimally processed options with extended shelf life and convenient storage. Innovations in packaging, flavor varieties, and premium product lines such as organic, functional, or gourmet dehydrated foods are further attracting a wider consumer base.

Geography Analysis

Germany accounted for 20.32% of 2025 revenue, underscoring its position as the largest and most technologically advanced contributor to Europe’s dehydrated food market. This dominance is supported by a well-established food-processing infrastructure and export-oriented manufacturing clusters, particularly in Bavaria and North Rhine-Westphalia, which host many of Europe’s leading food producers and ingredient processors. Germany's proximity to abundant raw-material suppliers, as Europe’s largest producer of potatoes and dairy, ensures a steady supply of high-quality inputs for dehydration processes. Additionally, advanced automation, robotics, and energy-efficient processing systems enhance competitiveness by mitigating high labor costs and enabling large-scale, precise production.

Italy is projected to grow at the fastest rate of 6.02% through 2031, fueled by strong consumer demand for premium, organic, and clean-label dehydrated products. The country’s rich culinary and agri-food traditions further support this growth. France and Spain maintain mid-tier positions in the market, supported by robust food manufacturing sectors, expanding retail distribution networks, and growing consumer interest in healthy, natural, and portable food formats. These factors contribute to consistent growth in both countries.

The United Kingdom, Sweden, Belgium, and the Rest of Europe collectively contribute a balanced share to the market. Their growth is driven by rising consumer demand for convenience foods, premium freeze-dried snacks, and functional ingredients. These regions also benefit from increasing retail penetration, niche product innovations, and a growing focus on health-oriented and sustainable food solutions. Together, these areas create a geographically diverse European market with distinct competitive strengths across each subregion.

Competitive Landscape

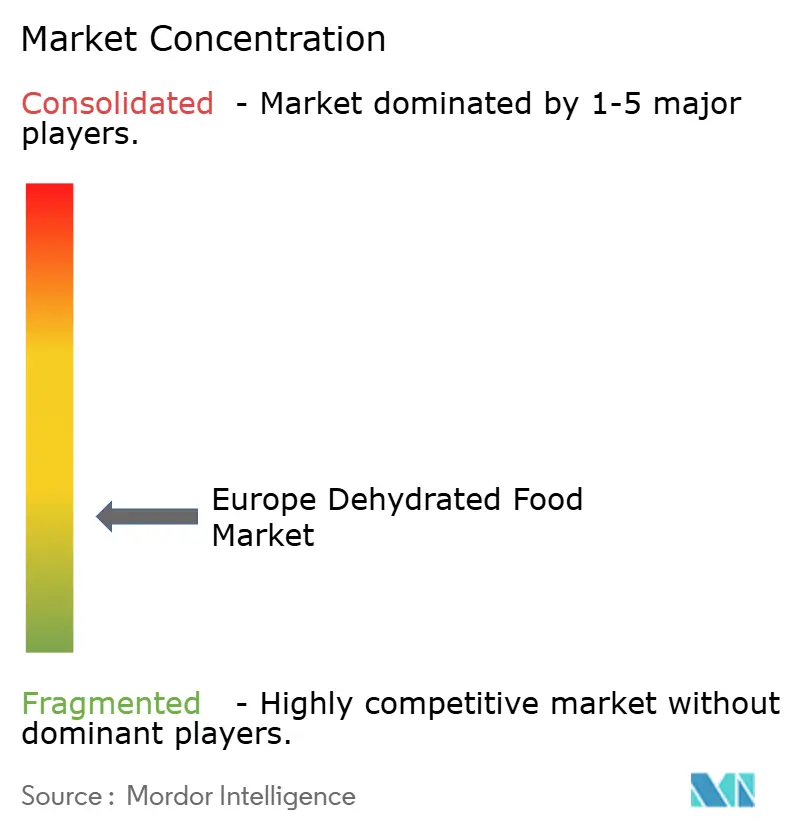

The Europe Dehydrated Food Market is moderately fragmented, with competition involving both large multinational ingredient suppliers and specialized regional processors. Key players in the market include Arla Foods amba, Asahi Group Holdings Ltd., Nestlé S.A., European Freeze Dry Ltd., and Lyo Food Sp. z o.o. These companies leverage their strengths in technology, sourcing, and distribution to maintain competitive positions. Market concentration is particularly high in commodity-driven segments such as spray-dried milk powders, instant coffee, and foundational vegetable powders. In these areas, economies of scale in procurement, energy efficiency, logistics, and global distribution enable established players to maintain cost advantages and influence pricing structures.

Specialized producers in niche segments compete by focusing on innovations in freeze-drying efficiency, nutritional preservation, and gourmet flavor profiles. These innovations often appeal to outdoor enthusiasts, health-conscious consumers, and the premium retail segment. Such firms emphasize sustainability and artisanal processing to build customer loyalty and justify premium pricing. Meanwhile, multinational conglomerates leverage their existing retail and foodservice relationships to cross-sell dehydrated ingredients alongside their core product offerings. These companies employ bundling strategies to secure shelf space and enhance promotional visibility.

Significant growth opportunities are emerging in the dehydrated seafood and egg powder segments, particularly for foodservice and industrial applications. Dehydrated seafood and egg ingredients offer advantages such as portability, safety, shelf stability, and waste reduction, making them well-suited to address current foodservice challenges. As major incumbents have underinvested in these categories, agile mid-sized processors and innovators have a unique opportunity to establish early leadership. This is particularly relevant as European manufacturers seek cost-stable, versatile protein options for ready meals, sauces, bakery products, and travel-oriented foods.

Europe Dehydrated Food Industry Leaders

-

Arla Foods amba

-

Asahi Group Holdings Ltd.

-

Nestlé S.A.

-

European Freeze Dry Ltd.

-

Lyo Food Sp. z o.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Soul Kitchen has introduced a new line of single-serve, clean-label soups. The initial offerings include Super Greens and Lion’s Mane Mushroom. These soups are made using gently dehydrated vegetable powders, herbs, and spices, without the use of gums, emulsifiers, palm oil, or artificial flavorings.

- October 2025: JDE Peet’s has introduced a newly upgraded innovation laboratory in Utrecht, the Netherlands, dedicated to its coffee products. The facility features high-precision grinders, capsule fillers for single-serve espresso, and advanced freeze-drying systems.

- July 2025: British confectionery company Langtins has launched a new range of freeze-dried sweets, including Fruit Bites, Fruit Bears, Lemon Bites, Mini Rocks, Drift Rocks, Jelly Rings, Rain Burst, and Sour Bites. All products are Halal certified and come in resealable pouches.

- November 2024: Del Monte has introduced a new range of dried fruit snacks in the United Kingdom. The range includes four products: Lemon Apple Sticks, Strawberry Apple Sticks, Spiced Apple Crisps, and Naked Apple Crisps.

Europe Dehydrated Food Market Report Scope

Dehydrated food refers to the types of food that have been dried to remove most of their natural moisture to preserve the food, thus reducing the potential problems which can occur as fresh foods mold or become fermented. The European dehydrated food market is segmented by type, product, distribution channel, and geography. Based on the type, the market is segmented into freeze-dried, spray-dried, vacuum-dried, sun-dried, and other types. Based on the product, the market is segmented into dairy products, vegetables and fruits, meat and seafood, and other product types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retailing, and other distribution channels. Based on geography, the market is segmented into the United Kingdom, Germany, France, Russia, Italy, Spain, and the Rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Drying Technology

| Spray-dried |

| Freeze-dried |

| Vacuum-dried |

| Sun / Solar-dried |

| Other Drying Technologies |

By Product Type

| Fruits and Vegetables |

| Meat and Seafood |

| Dairy and Eggs |

| Instant Coffee and Other Beverages |

| Prepared Meals and Soups |

| Spices, Herbs, and Seasonings |

| Nutraceutical and Functional Powders |

By Nature

| Conventional |

| Organic |

By End User

| Industrial Packaged Food | |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Drying Technology | Spray-dried | |

| Freeze-dried | ||

| Vacuum-dried | ||

| Sun / Solar-dried | ||

| Other Drying Technologies | ||

| By Product Type | Fruits and Vegetables | |

| Meat and Seafood | ||

| Dairy and Eggs | ||

| Instant Coffee and Other Beverages | ||

| Prepared Meals and Soups | ||

| Spices, Herbs, and Seasonings | ||

| Nutraceutical and Functional Powders | ||

| By Nature | Conventional | |

| Organic | ||

| By End User | Industrial Packaged Food | |

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe Dehydrated Food market in 2026?

The market stands at USD 72.91 billion and is projected to reach USD 95.55 billion by 2031.

Which drying technology is growing fastest in Europe?

Freeze-drying is advancing at a 5.58% CAGR as processors target premium applications and nutrient retention benefits.

Which product category shows the strongest growth momentum?

Nutraceutical and functional powders are expected to rise at 6.44% annually as consumers adopt immunity and gut-health formulations.

Why is Italy forecast to outpace other countries?

Artisanal producers are freeze-drying protected designation of origin tomatoes and herbs, aligning with premium export demand and outdoor tourism growth.

Page last updated on: