Dry Fruits Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

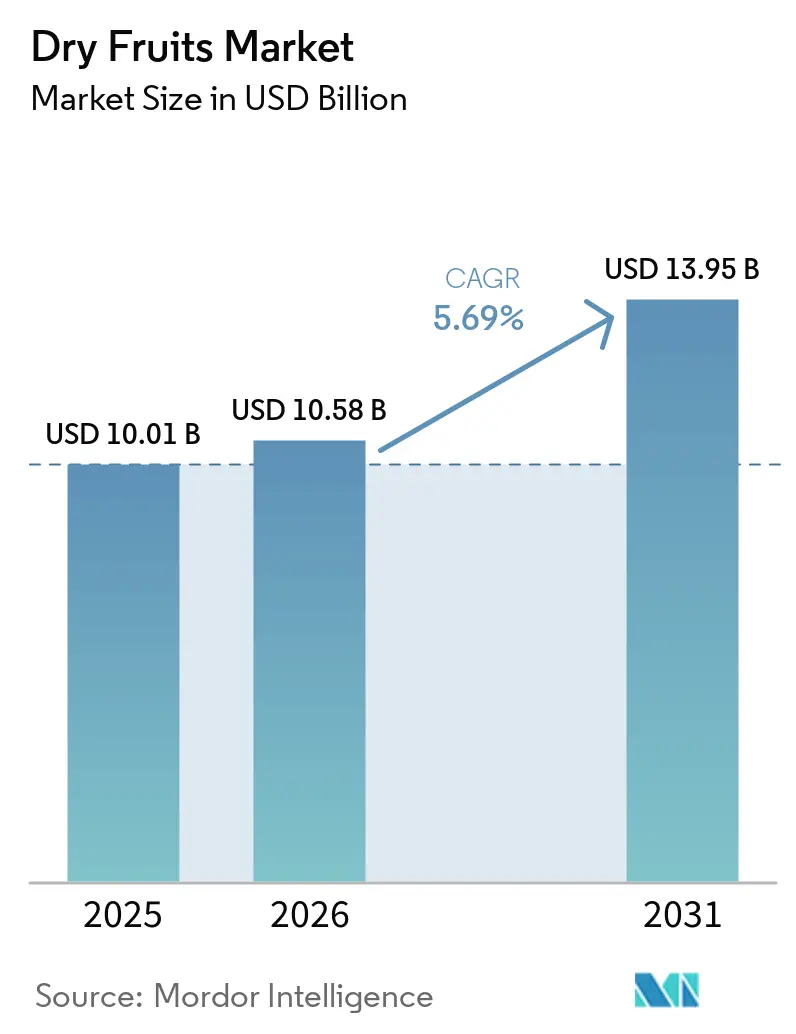

| Market Size (2026) | USD 10.58 Billion |

| Market Size (2031) | USD 13.95 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dry Fruits Market Analysis by Mordor Intelligence

The dry fruits market size is expected to grow from USD 10.01 billion in 2025 to USD 10.58 billion in 2026 and is forecast to reach USD 13.95 billion by 2031 at 5.69% CAGR over 2026-2031. Demand is shifting from seasonal confectionery use toward everyday snacking and functional food consumption. This change is being supported by stronger interest in clean-label food, convenient pack formats, and fitness-oriented eating habits. Gifting occasions across emerging markets are also widening household purchase frequency and premium pack demand. The dry fruits market is being shaped at the same time by tight agricultural supply in weather-sensitive origin countries, which is keeping pricing firm and raising the value of stable sourcing and compliance systems. Competition remains fragmented, so companies that combine dependable procurement, food safety discipline, and brand-led premium positioning are better placed to capture growth in the dry fruits market.

Key Report Takeaways

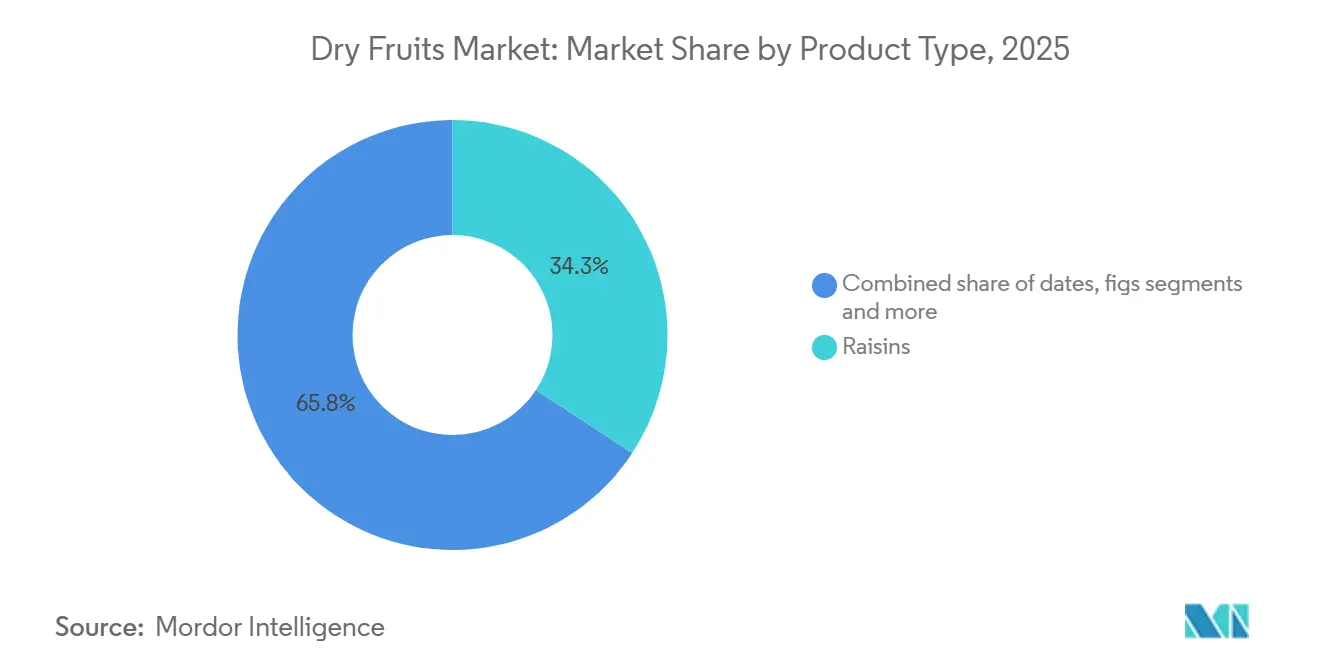

- By product type, raisins held 34.25% of dry fruits market share in 2025, while the dry fruits market size for dates is projected to expand at 6.34% CAGR through 2031.

- By category, conventional dried fruits accounted for 88.39% of revenue in 2025, while Natural & Organic is forecast to advance at 7.11% CAGR through 2031.

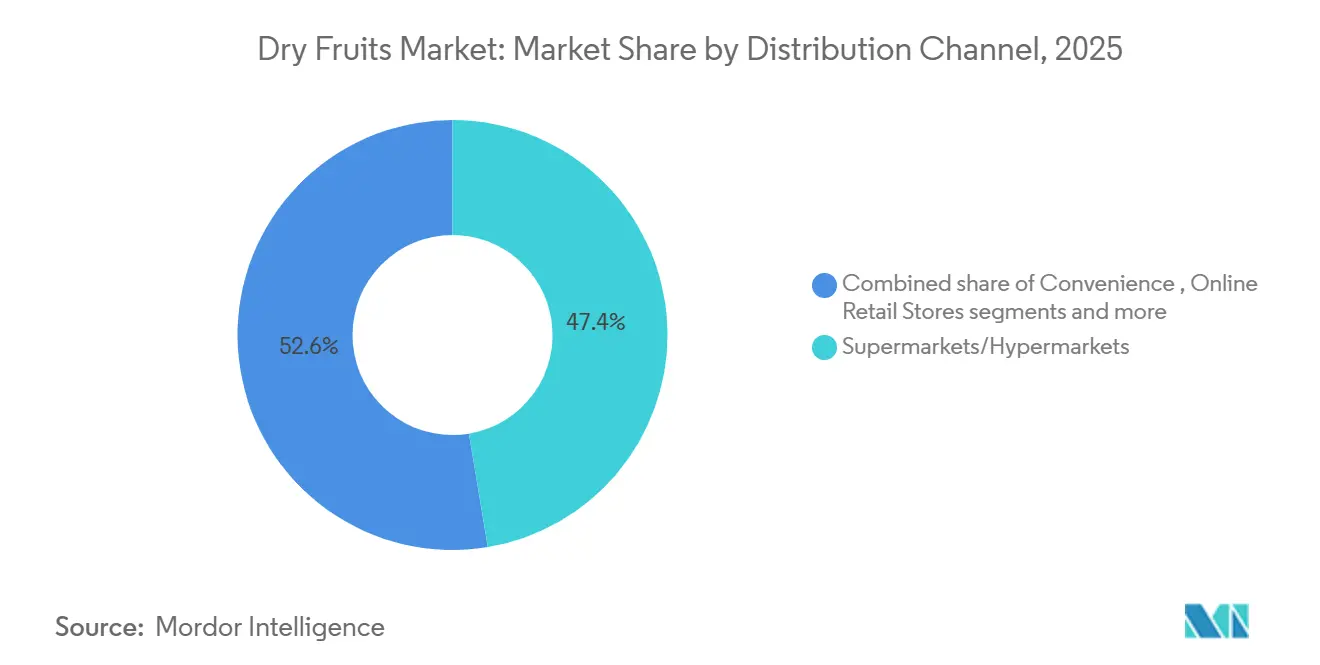

- By distribution channel, supermarkets and hypermarkets captured 47.38% of the dry fruits market size in 2025, while online retail stores are projected to grow at 7.34% CAGR through 2031.

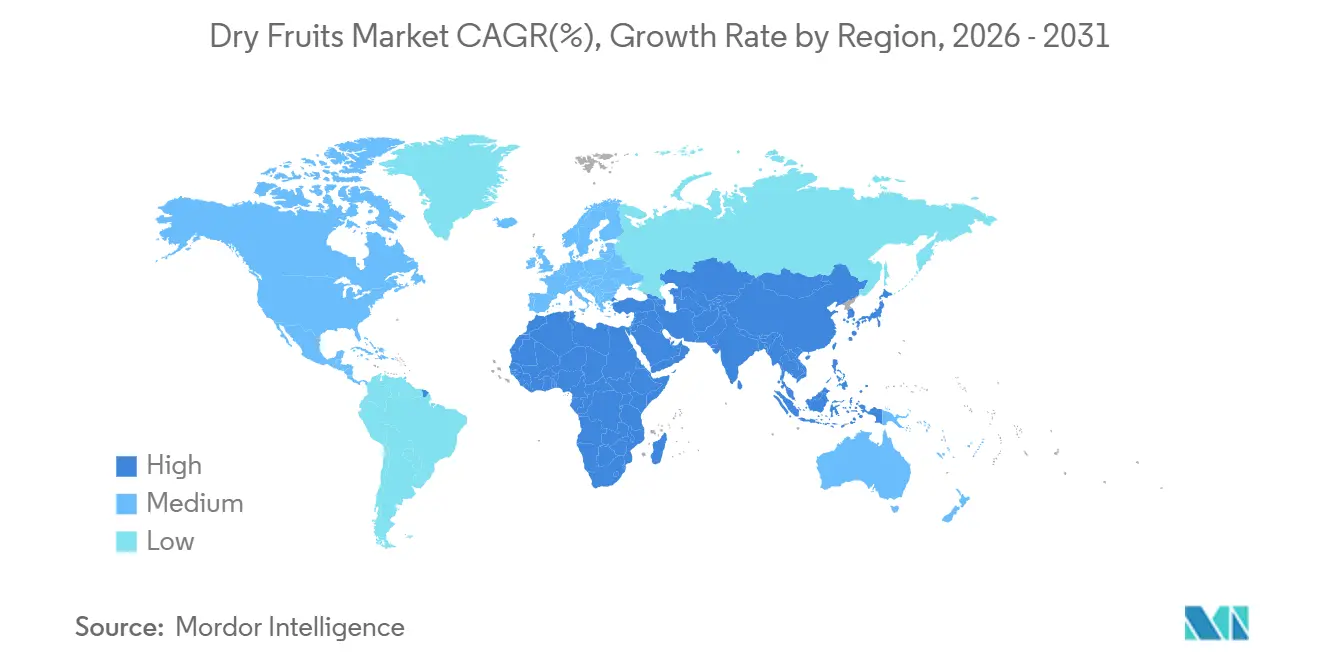

- By geography, Asia-Pacific held 38.45% of dry fruits market share in 2025, while Middle East and Africa is forecast to expand at 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dry Fruits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for convenient and healthy snack options | +1.0% | Global, highest in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing awareness about immunity and nutritional benefits | +0.8% | Global, with concentrated gains in South Asia and Southeast Asia | Short term (≤ 2 years) |

| Higher spending on premium and organic food products | +0.9% | North America, Europe core, Australia | Medium term (2-4 years) |

| Surging adoption of fitness, wellness, and weight-management diets | +0.7% | North America, Europe, urban Middle East | Medium term (2-4 years) |

| Higher demand during festive seasons and gifting occasions | +0.5% | South Asia, Middle East and Africa, East Asia | Short term (≤ 2 years) |

| Rising influence of social media and health influencers promoting nutritious snacking | +0.6% | Global, highest in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for convenient and healthy snack options

The dry fruits market is being significantly driven by the rising consumer preference for convenient and healthy snack options. Modern consumers are increasingly seeking ready-to-eat foods that offer both nutritional value and ease of consumption, positioning dry fruits as an ideal snacking solution.In addition, consumers are shifting away from heavily processed snacks toward products perceived as healthier and minimally processed, which is further supporting demand for dried fruits such as almonds, raisins, pistachios, walnuts, and dates. The convenience factor of dry fruits appeals across various income groups as shoppers increasingly prefer snacks that require no preparation while delivering functional health benefits. According to the Glanbia Nutrition Report 2024, more than half of U.S. consumers are actively trying to consume more protein (56%), more fiber (53%), or less sugar (58%), reflecting the growing demand for nutrient-dense snack alternatives[1]Source: Glanbia Nutrition, “What Americans are snacking on today”, glanbianutrition.com. This evolving consumer behavior is encouraging manufacturers and retailers to expand their portfolios of packaged, flavored, organic, and portion-controlled dry fruit products, thereby accelerating overall market growth.

Increasing awareness about immunity and nutritional benefits

Consumers are increasingly recognizing the benefits of fiber, potassium, magnesium, and natural energy content in products like dates and raisins, which is driving growth in the dry fruits market. This trend is particularly evident in South and Southeast Asia, where consumers are shifting their perception of dried fruits from occasional treats to essential nutrient-dense foods. Manufacturers in the dry fruits market are responding by developing product mixes that use dates and raisins as natural sweeteners in bars, clusters, and beverages, catering to this growing demand. In India, the annual demand for dry fruits exceeds 1.43 million tons. However, shipments dropped by 15% to 25% in early 2026 due to disruptions along the Iran-Afghanistan corridor, which restricted supplies and increased prices. These supply chain challenges are pushing stakeholders to accelerate domestic procurement strategies and diversify sourcing options to stabilize the dry fruits market.

Higher spending on premium and organic food products

The dry fruits market is experiencing a surge in premium growth as certification, packaging formats, and origin stories become more prominent on retail shelves. This trend drives demand for organic supply, as certified dried fruits attract consumers who associate premium products with cleaner production methods and improved traceability. In 2024, the European Union increased its imports of organic nuts and dried fruits from non-EU countries by 26%, reflecting this growing preference[2]Source: Republique Francaise, “Organic Agriculture in the European Union”, agencebio.org. Additionally, private-label brands in Western Europe are expanding their presence in the dry fruits market, creating significant volume opportunities for certified suppliers, even as branded products face tighter profit margins. The European Union’s stringent compliance rules are raising export standards, favoring processors who consistently maintain proper documentation, ensure residue control, and uphold certification requirements in the dry fruits market.

Surging adoption of fitness, wellness, and weight-management diets

The dry fruits market is being strongly driven by the surging adoption of fitness, wellness, and weight-management diets among consumers worldwide. Health-conscious individuals are increasingly incorporating dry fruits such as almonds, walnuts, pistachios, raisins, and dates into their daily diets due to their high protein, fiber, healthy fat, and antioxidant content. These products are widely perceived as nutritious snack alternatives that support energy management, muscle recovery, digestive health, and overall wellness. In addition, the growing popularity of gym culture, sports nutrition, keto diets, plant-based eating patterns, and clean-label food consumption is further accelerating demand for dry fruits across multiple consumer groups. Consumers following weight-management programs are also preferring portion-controlled and nutrient-dense snacks that help promote satiety while reducing the intake of heavily processed foods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price volatility of raw materials and imported products | -1.1% | Global, most acute in South Asia and Middle East and Africa import-dependent markets | Short term (≤ 2 years), Medium term (2-4 years) |

| Risk of fungal contamination and aflatoxin issues | -0.7% | Europe, Turkey, North Africa, West Asia | Medium term (2-4 years) |

| Supply chain disruptions due to climate and trade regulations | -0.9% | Turkey, Iran, India, California supply corridors | Long term (≥ 4 years) |

| High storage and transportation costs for premium quality products | -0.4% | North America, Europe, East Asia long-haul import routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High price volatility of raw materials and imported products

Crop risks, conflicts, and trade bottlenecks are simultaneously disrupting several major supply corridors, causing persistent price fluctuations in the dry fruits market. In early 2026, disruptions along the Iran-Afghanistan trade corridor triggered a 20% to 30% increase in the prices of raisins, dates, and pistachios in India. Additionally, a heatwave in 2025 severely damaged raisin crops in Nasik and Sangli, sharply reducing yields and driving wholesale prices in India up from INR 280 per kg to INR 400 per kg. The geographic concentration of these supply shocks exacerbates the situation, as alternative sources cannot quickly replace the missing volumes. This dynamic significantly increases procurement risks for processors, retailers, and importers operating in the dry fruits market.

Risk of fungal contamination and aflatoxin issues

Exporters targeting the European Union actively address quality risks in the dry fruits market, particularly those posed by aflatoxins and ochratoxin A. The EU enforces strict regulations, setting a maximum aflatoxin level of 4.0 µg/kg for dried fruits intended for direct consumption and 10.0 µg/kg for pre-sorted lots. For ochratoxin A, the EU caps levels at 8.0 µg/kg for dried vine fruits and figs, and 2.0 µg/kg for other dried fruits[3]Source: European Union, "COMMISSION REGULATION (EU) 2022/1370", eur-lex.europa.eu. In 2024, Turkey reported compliance data showing ochratoxin A levels in dried figs reaching 14.85 µg/kg. As a result, exporters destroyed 1,400 tons of contaminated figs in 2025 to meet regulatory standards. The Codex Alimentarius continues to develop a code of practice for ochratoxin A in dried fruits, with the process expected to extend until 2028. This prolonged timeline forces exporters to operate within a fragmented compliance framework for the foreseeable future. These challenges increase costs related to testing, sorting, and traceability in the dry fruits market, while also strengthening the competitive position of processors that have established robust food safety systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dates Gain Ground on Raisins' Volume Lead

Raisins accounted for 34.25% of the global dry fruits market share in 2025, making them the leading product type within the industry. The segment’s dominance is primarily supported by the widespread use of raisins across bakery, confectionery, dairy, breakfast cereals, and snack applications. Raisins are highly preferred by consumers due to their natural sweetness, long shelf life, affordability, and nutritional benefits, including fiber, antioxidants, and essential minerals. The product also enjoys strong demand in both household consumption and industrial food processing sectors across North America, Europe, and Asia-Pacific. In addition, the increasing popularity of healthy snacking trends and natural sugar alternatives has further strengthened raisin consumption globally. Food manufacturers are increasingly incorporating raisins into energy bars, trail mixes, and functional food products to cater to health-conscious consumers.

The dates segment is projected to register the fastest growth in the dry fruits market, expanding at a CAGR of 6.34% through 2031. The growth is largely driven by rising consumer preference for natural sweeteners, clean-label food ingredients, and nutrient-rich snack products. Dates are increasingly being used as sugar substitutes in bakery products, energy bars, dairy alternatives, and sports nutrition applications due to their natural sweetness and high nutritional value. The segment is also benefiting from growing awareness regarding the health benefits associated with dates, including digestive health support, energy enhancement, and high antioxidant content. Strong consumption across Middle Eastern countries, along with rising adoption in Europe, North America, and Asia-Pacific, is further supporting market expansion.

By Category: Organic Commands a Premium but Conventional Anchors Volume

Conventional dried fruits accounted for 88.39% of the global dry fruits market revenue in 2025, making them the dominant category within the industry. The strong market position of conventional products is primarily driven by their wide availability, lower pricing compared to organic alternatives, and extensive consumer acceptance across both developed and emerging markets. Conventional dried fruits are heavily utilized in bakery, confectionery, dairy, breakfast cereals, snacks, and foodservice applications due to their cost-effectiveness and consistent supply. Large-scale food manufacturers and retail brands continue to prefer conventional dried fruits to maintain competitive product pricing and high-volume production capabilities. In addition, supermarkets, hypermarkets, and convenience stores offer a broad range of conventional dried fruit products, improving accessibility for mass-market consumers.

The Natural & Organic segment is forecast to register the fastest growth in the dry fruits market, expanding at a CAGR of 7.11% through 2031. The increasing consumer preference for clean-label, chemical-free, and sustainably sourced food products is significantly contributing to the growth of this segment. Health-conscious consumers are increasingly shifting toward organic dried fruits due to concerns regarding pesticide residues, artificial additives, and overall food quality. The segment is also benefiting from the rising popularity of plant-based diets, functional nutrition, and premium healthy snacking trends across North America and Europe. In addition, growing awareness regarding environmental sustainability and ethical farming practices is encouraging consumers to purchase certified organic and naturally processed dried fruit products.

By Distribution Channel: Online Retail Outpaces Physical Formats

Supermarkets and hypermarkets accounted for the largest share of the dry fruits market in 2025, contributing 47.38% of the total market revenue. The dominance of this distribution channel is supported by the strong consumer preference for one-stop shopping experiences, where buyers can access a wide variety of packaged and branded dry fruit products under a single roof. Large retail chains provide extensive shelf visibility, promotional discounts, and bulk purchasing options, which encourage higher product sales across urban and semi-urban regions. Consumers also prefer supermarkets and hypermarkets due to the assurance of product quality, freshness, and availability of multiple domestic and international brands. In addition, organized retail stores frequently introduce attractive packaging formats, private-label offerings, and seasonal promotions that further strengthen consumer engagement.

Online retail stores are projected to register the fastest growth in the dry fruits market, expanding at a CAGR of 7.34% through 2031. The rapid growth of this segment is primarily driven by increasing internet penetration, rising smartphone usage, and the growing adoption of e-commerce platforms among consumers. Online channels provide convenience through doorstep delivery, easy product comparison, subscription-based purchases, and access to a broader assortment of dry fruit products than traditional retail outlets. Consumers are increasingly shifting toward digital shopping platforms due to attractive discounts, flexible payment options, and the availability of premium and organic dry fruit varieties.

Geography Analysis

Asia-Pacific dominated the global dry fruits market in 2025, accounting for 38.45% of the overall market share. The region’s strong market position is primarily supported by its large population base, rising disposable income levels, and long-standing cultural consumption of dry fruits in countries such as India, China, and Japan. Dry fruits are widely consumed across the region during festivals, religious occasions, and as part of traditional diets, which continues to drive steady product demand. In addition, increasing health awareness among consumers has encouraged the adoption of nutrient-rich snacks, further boosting the consumption of almonds, cashews, pistachios, raisins, and walnuts. The rapid expansion of organized retail networks, supermarkets, and e-commerce platforms across developing Asian economies has also improved product accessibility and visibility.

The Middle East and Africa region is projected to witness the fastest growth in the dry fruits market, expanding at a CAGR of 7.05% through 2031. The growth of the market in this region is supported by increasing urbanization, changing dietary habits, and rising awareness regarding the nutritional benefits of dry fruits. Consumers across Gulf countries and several African economies are increasingly incorporating healthy snack alternatives into their daily diets, which is driving demand for premium and packaged dry fruit products. The region also benefits from strong cultural and religious associations with dry fruit consumption, particularly during Ramadan and other festive occasions when dates, almonds, pistachios, and raisins experience significant demand.

Other regions, including North America, Europe, and South America, also contribute significantly to the growth of the global dry fruits market. North America represents a mature market characterized by high consumer awareness regarding healthy eating habits, strong demand for organic and premium dry fruits, and increasing incorporation of dry fruits into snack bars, breakfast cereals, and bakery products. Europe continues to witness stable demand due to the growing popularity of plant-based diets, clean-label food products, and functional snacks, particularly in countries such as Germany, the United Kingdom, France, and Italy. Meanwhile, South America is emerging as a developing market with increasing consumption of packaged food products and rising retail penetration in countries including Brazil and Argentina.

Competitive Landscape

The dry fruits market is highly fragmented, with the presence of numerous international, regional, and local manufacturers competing across various product categories and distribution channels. Market competition is largely influenced by product quality, pricing strategies, sourcing capabilities, packaging innovation, and brand recognition. Leading companies are increasingly focusing on expanding their product portfolios by introducing organic, flavored, roasted, and value-added dry fruit variants to attract health-conscious consumers. In addition, companies are investing in advanced processing, sorting, and packaging technologies to improve product shelf life and maintain quality standards. The growing demand for premium and clean-label food products has also encouraged manufacturers to strengthen their certification standards and traceability practices.

Competition in the dry fruits market is further intensified by the rapid expansion of organized retail channels and e-commerce platforms. Major players are strengthening partnerships with supermarkets, hypermarkets, specialty stores, and online retailers to improve product availability and market penetration. E-commerce platforms, in particular, have enabled smaller and regional brands to directly reach consumers, thereby increasing pricing competition and product differentiation within the market. Companies are also focusing on attractive packaging formats, convenient portion sizes, and premium gifting packs to target urban consumers and festive demand.

Regional dynamics play a significant role in shaping the competitive landscape of the dry fruits market. Countries with strong dry fruit production and export capabilities, such as the United States, India, Turkey, Iran, and China, remain highly influential in terms of supply chain control and pricing competitiveness. Local and regional manufacturers often compete effectively by leveraging lower production costs, strong domestic distribution networks, and consumer familiarity with traditional dry fruit varieties. At the same time, multinational companies are emphasizing sustainability initiatives, ethical sourcing, and premium branding to differentiate themselves in highly competitive markets.

Dry Fruits Industry Leaders

-

Sun-Maid Growers of California

-

Sunsweet Growers Inc.

-

National Raisin Company

-

Ocean Spray Cranberries, Inc.

-

Bergin Fruit and Nut Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Ocean Spray Cranberries unveiled new formats for its Craisins® Dried Cranberries. These include a Sour Watermelon variant in a 6 oz resealable pack, a limited-edition Fireworks Cranberry Mix (20 oz, exclusively at Sam's Club), and single-serve multipacks of Strawberry and Raspberry Lemonade (1 oz pouches in 5-packs). With these launches, Ocean Spray is positioning Craisins as a go-to everyday snack, moving away from their traditional role as mere recipe toppings.

- May 2026: Joolies introduced its Organic DATE SOURS at Sprouts Farmers Market across the nation. These candy-inspired, no-added-sugar snacks, made from whole dates, come in four enticing flavors: Blue Raspberry, Watermelon, Cherry Cola, and Peachy. Aimed at candy lovers, the product offers a fruit-based alternative and boasts distribution in over 12,000 retail locations.

- March 2026: Apis India Limited's MISK brand debuted Masala Dates in New Delhi. These seedless, pre-sliced dates, available in three Indian masala flavors - Achari, Imli, and Chilli-Lime - are marketed as a ready-to-eat superfood snack. Targeting urban consumers seeking convenient snacking, the product is available nationwide through retail, modern trade, and e-commerce channels, highlighting the rising trend of flavor innovation in the dates sub-category.

Global Dry Fruits Market Report Scope

Dry fruits are fruits that have had most of their natural water content removed either through natural drying methods, such as sun drying, or through mechanical drying processes. The dry fruits market is segmented by product type, category, distribution channel and geography. Based on product type, the market is segmented into raisins, dates, apricots, figs, prunes and other product types. Based on category, the market is segmented into conventional, natural and organic. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million) and volume (tons).

| Raisins |

| Dates |

| Apricots |

| Figs |

| Prunes |

| Other Product Types |

| Conventional |

| Natural & Organic |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East & Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Raisins | |

| Dates | ||

| Apricots | ||

| Figs | ||

| Prunes | ||

| Other Product Types | ||

| By Category | Conventional | |

| Natural & Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East & Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of dry fruits sales by 2031?

The dry fruits market is forecast to reach USD 13.95 billion by 2031, rising from USD 10.58 billion in 2026 at a 5.7% CAGR.

Which product type leads global demand for dried fruit?

Raisins led with 34.25% of 2025 revenue because they remain deeply embedded in bakery, cereal, confectionery, and snack applications.

Which product type is growing the fastest through 2031?

Dates are the fastest-growing product type, with a projected 6.34% CAGR through 2031, supported by demand for natural sweeteners and better-for-you snacks.

Which sales channel is expanding the fastest?

Online retail stores are forecast to grow at 7.34% CAGR through 2031, helped by wider grocery e-commerce adoption and digital-first product launches.

Which region holds the largest share, and which one is growing the fastest?

Asia-Pacific held the largest share at 38.45% in 2025, while Middle East and Africa is expected to grow the fastest at 7.05% CAGR through 2031.

Page last updated on: