Functional Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

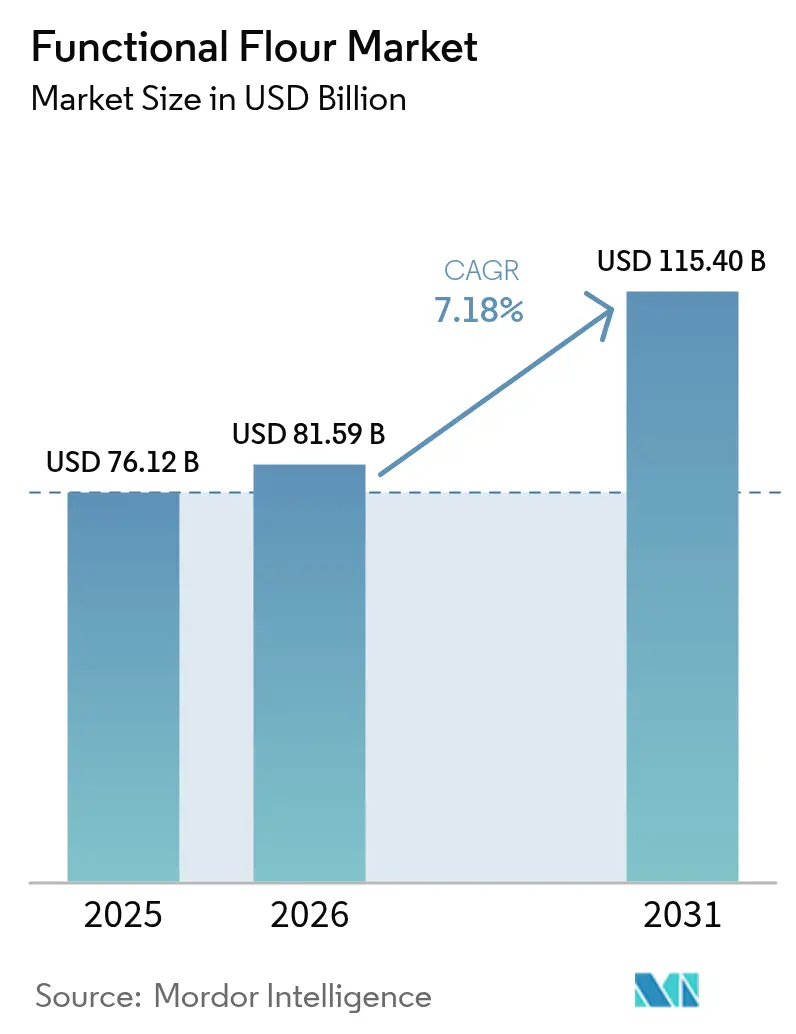

| Market Size (2026) | USD 81.59 Billion |

| Market Size (2031) | USD 115.40 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Functional Flour Market Analysis by Mordor Intelligence

The functional flour market size is expected to increase from USD 76.12 billion in 2025 to USD 81.59 billion in 2026 and reach USD 115.40 billion by 2031, growing at a CAGR of 7.18% over 2026-2031. Accelerated demand for clean-label texturizers, fortification mandates in staple foods, and sustained growth of plant-based protein formats keep the functional flour market on an upward trajectory. Legume-based ingredients are gaining share because they supply protein concentrations above 20% while remaining free from the top eight allergens, enabling formulators to diversify beyond wheat. Precision extrusion and heat-moisture treatment let processors tailor gelatinization profiles, cutting reliance on hydrocolloids and opening cost-effective reformulation pathways. At the same time, side-stream upcycling creates new profit pools by turning oat-milk pulp, okara, and brewers’ spent grain into high-fiber functional flours, meeting corporate sustainability targets and retailer scorecards. Supply-chain resilience is now a strategic differentiator as drought-linked yield swings in Canada and Europe raise input-price volatility and heighten the need for diversified sourcing contracts.

Key Report Takeaways

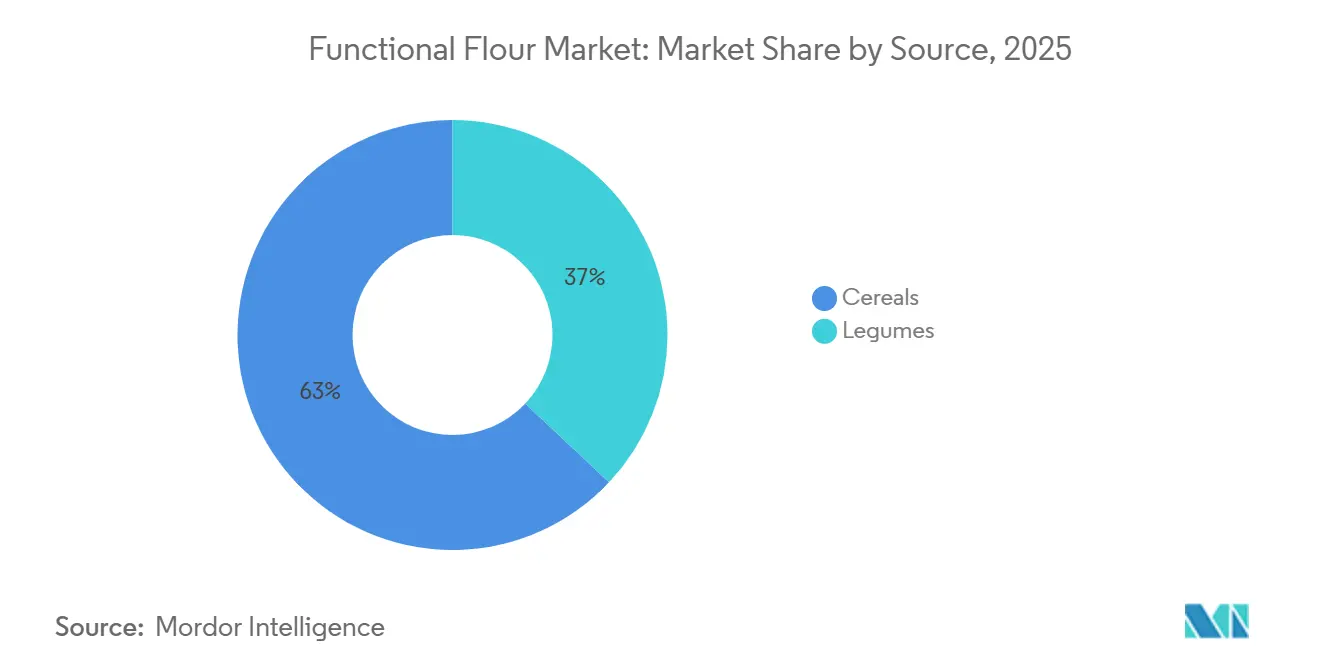

- By source, cereals commanded 62.98% of functional flour market share in 2025, while legumes are poised to grow at an 8.74% CAGR through 2031.

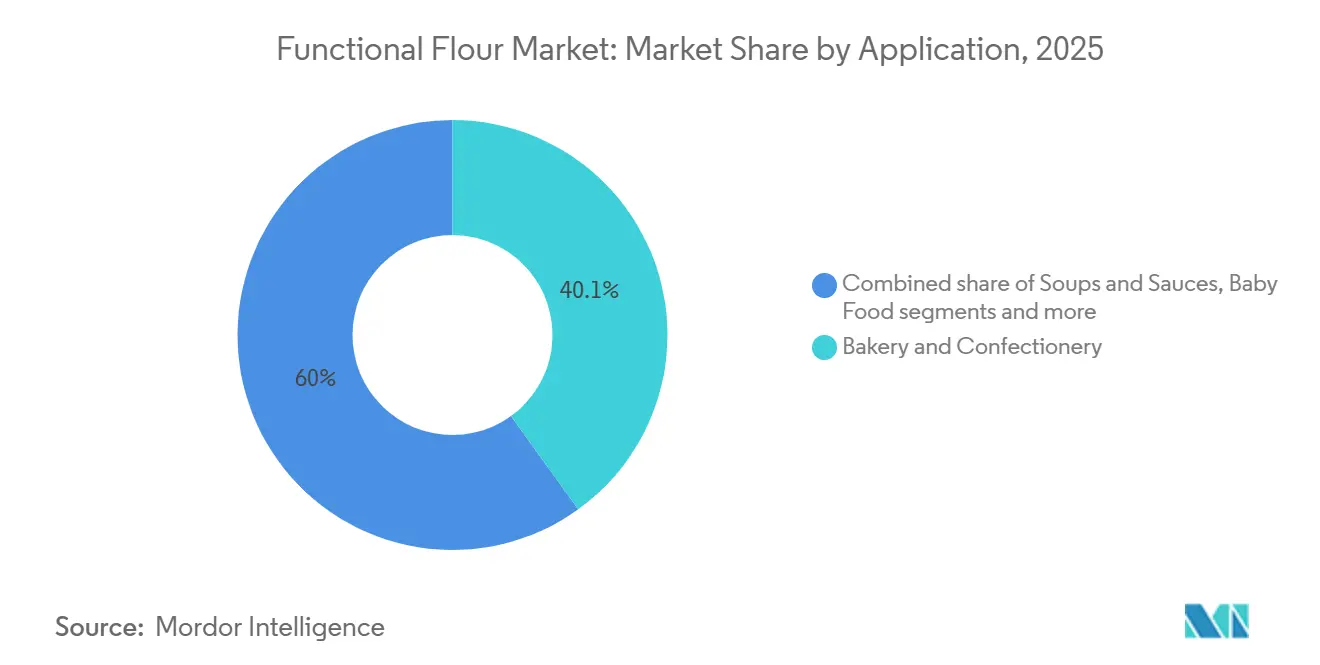

- By application, bakery and confectionery accounted for 40.05% share of the functional flour market size in 2025, whereas meat alternatives are set to register a 7.63% CAGR to 2031.

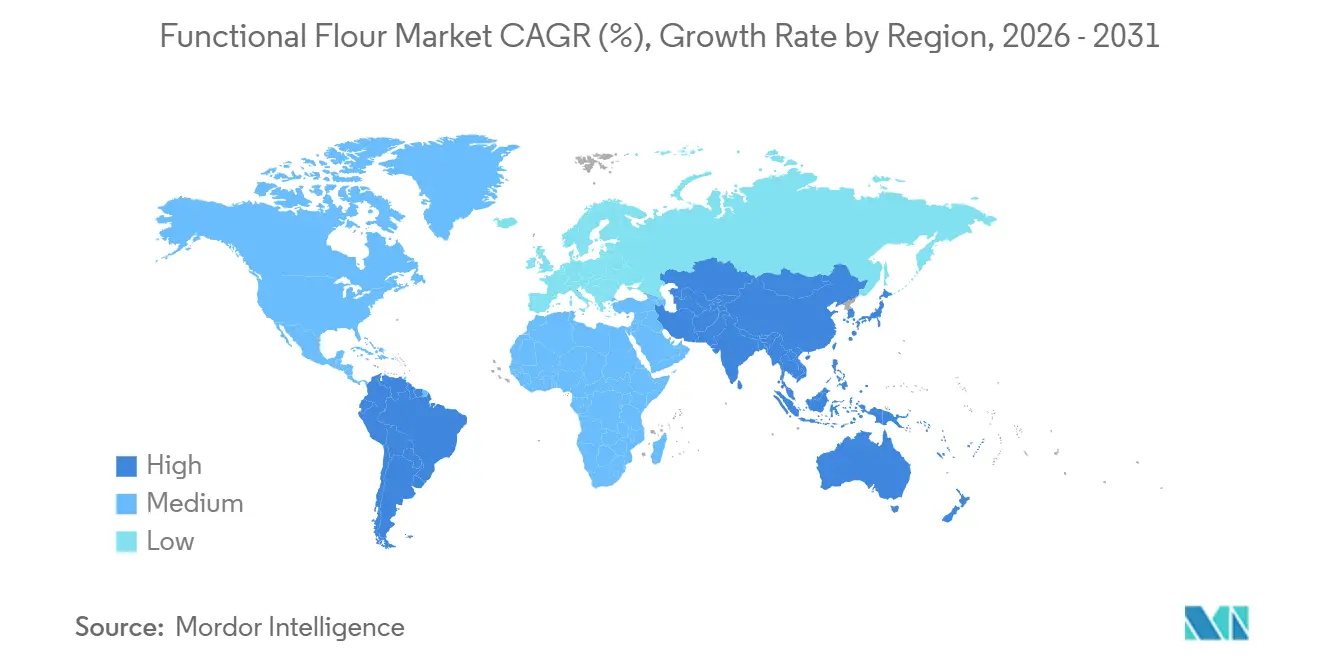

- By geography, North America led with a 33.22% revenue share in 2025, while Asia-Pacific is projected to advance at an 8.79% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Functional Flour Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bakery and snack industry demand for texture control and shelf-stability | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing use in specialty and high-margin segments (sports nutrition, baby foods, fortified staples) | +1.5% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth in plant-based food and alternative proteins | +2.1% | North America, Europe, Asia-Pacific core markets | Long term (≥4 years) |

| Adoption of precision extrusion and heat-moisture treatment unlocking customized functional traits | +1.2% | Global, led by North America and Western Europe | Short term (≤2 years) |

| Up-cycling of food-processing side-streams into high-fiber flours | +0.9% | Europe, North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Regulatory support and food-safety standards harmonization | +0.7% | Global, particularly Europe, Asia-Pacific, Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Bakery and snack industry demand for texture control and shelf-stability

The bakery and snack industry is witnessing a growing emphasis on texture control and shelf stability, driven by shifting consumer preferences and market demands. Manufacturers are striving to deliver consistent sensory quality, such as soft bread crumbs or crisp crackers, while addressing the increasing demand for nutritional and functional benefits in staple products. This trend is reflected in the rising expenditure of United Kingdom households on bread and cereals, which reached GBP 23.38 billion in 2025, up from GBP 22.32 billion in 2022, as per the Office for National Statistics (UK), underscoring robust demand for high-quality products [1]Source: Office for National Statistics (UK), "Consumer Trends: Chained Volume Measure, Seasonally Adjusted," ons.gov.uk . To meet these expectations, industrial bakers and snack producers are collaborating with ingredient suppliers like Archer Daniels Midland Company and Cargill, Incorporated. These suppliers are innovating functional flours that enhance water absorption, dough rheology, and product texture, while also incorporating health-focused attributes such as higher fiber, protein content, or gluten-free functionality. This collaboration enables manufacturers to balance clean-label claims with technical performance, ensuring products remain fresher for longer without compromising on mouthfeel or structural integrity. Such advancements are critical in a competitive market environment characterized by heightened consumer expectations and supply chain challenges.

Growing use in specialty and high-margin segments (sports nutrition, baby foods, fortified staples)

Shifting lifestyle and health priorities are driving growth in the functional flour market, particularly in specialty and high-margin segments such as sports nutrition, baby foods, and fortified staples. With 21.5% of United States adults expected to participate in sports, exercise, and recreational activities daily in 2024, up from 20.1% in 2022, there is increasing demand for nutrient-enhanced sports nutrition that support performance and recovery [2]Source: Bureau of Labor Statistics, "American Time Use Survey - 2023 Results," bls.gov . Concurrently, heightened parental focus on nutrient-dense baby foods and fortified staples is encouraging food manufacturers to source specialized functional flours that provide tailored nutritional profiles, improved digestibility, and enhanced processing performance. Key suppliers, including Ardent Mills and Swedish Oat Fiber, are innovating with fiber-enriched flours that help formulators meet protein and clean-label requirements while maintaining texture and processability in finished products. These developments reflect how consumer health trends are reshaping ingredient strategies across the value chain. Furthermore, the market is expanding as customers increasingly seek differentiated, higher-margin products that align with active and preventive health objectives, reinforcing the role of functional flours in addressing evolving consumer demands.

Growth in plant-based food and alternative proteins

Rising consumer interest in sustainable, animal-free diets is driving significant changes in the functional flour market, as demand grows for flours that enhance texture, protein content, and functional performance in plant-based applications. Data reveals that 6 in 10 or 59% of U.S. households purchased plant-based foods in 2024, reflecting widespread adoption [3]Source: The Good Food Institute, "U.S. Retail Market Insights for the Plant-Based Industry," gfi.org. This trend, as highlighted by The Good Food Institute and the Plant Based Food Association, is encouraging food manufacturers to reformulate bakery, snack, and meat-alternative products with ingredients that replicate the mouthfeel and structure of traditional options. To meet these evolving needs, companies such as Scoular and Ingredion Incorporated are developing tailored solutions, including pea protein-fortified flours, chickpea and lentil flours with enhanced emulsification properties, and tapioca or rice flour blends engineered for specific viscoelastic characteristics. These innovations enable brands to address consumer expectations for sustainability, nutrition, and sensory quality without compromising product performance. The interplay between the growth of plant-based foods and advancements in functional flour underscores the market's focus on delivering ingredient solutions that align with current consumer preferences and industry demands.

Adoption of precision extrusion and heat-moisture treatment unlocking customised functional traits

Manufacturers in the functional flour market are increasingly adopting precision extrusion and heat-moisture treatment technologies to develop ingredients with specific performance characteristics. These methods enable the customization of functional traits such as water absorption, controlled gelatinization, and targeted digestibility, addressing evolving product standards and complex processing requirements. By refining starch, protein, and fiber structures, these technologies help bakers and food formulators achieve consistent texture, extended shelf life, and reliable processing in finished products. Additionally, these advanced techniques allow for the creation of flours with tailored functional profiles, such as enhanced emulsification for vegan pâtés, modified pasting properties for gluten-reduced breads, and improved gel strength for high-protein bars. This capability is critical as brands compete on both performance and clean-label attributes. Leading ingredient suppliers, including Ardent Mills (a joint venture of Conagra Brands, Cargill, and CHS) and MGP Ingredients, Inc., are leveraging these technologies to produce engineered functional flours that reduce reliance on chemical additives while delivering targeted nutritional and sensory outcomes. As formulators demand predictable and customizable ingredient functionality across bakery, snack, and specialty applications, the integration of precision extrusion and heat-moisture treatment is becoming a cornerstone of innovation, linking end-product quality with upstream ingredient design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of raw materials and production | -1.4% | Global, acute in North America and Europe | Short term (≤2 years) |

| Supply-chain volatility and limited scalability | -1.1% | Global, concentrated in pulse-producing regions (Canada, India, Australia) | Medium term (2-4 years) |

| Potential allergen and cross-contamination risks | -0.6% | North America, Europe, Asia-Pacific urban markets | Medium term (2-4 years) |

| Functional-performance drift across crop varieties hindering standardization | -0.8% | Global, particularly affecting legume-based flours | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High cost of raw materials and production

The high cost of raw materials and production poses a significant challenge in the functional flour market. Specialty grains, ancient seeds, and legume sources are inherently more expensive than conventional wheat due to limited cultivation areas, premium sourcing requirements, and volatile supply dynamics. These higher raw material costs are further amplified by processing expenses, including specialized milling, quality control, and targeted fortification methods, which enhance the ingredient's functionality compared to standard flour. This cost burden directly impacts B2B suppliers and food manufacturers. For example, The Scoular Company invests in advanced processing for high-protein and pulse-based flours but faces premium input costs for peas and chickpeas, along with the capital-intensive nature of air classification equipment required to ensure consistent functional traits. Food formulators often weigh the technical benefits of functional flours against conventional alternatives, particularly in price-sensitive segments where higher ingredient costs can compress margins and slow adoption. Additionally, supply chain challenges, such as seasonal availability and transportation cost fluctuations, further increase production expenses. These factors make it difficult for manufacturers to scale niche functional flours without passing costs to customers or accepting reduced margins. This underscores the importance of cost management, grower partnerships, and process efficiencies for B2B functional flour manufacturers aiming to remain competitive.

Potential allergen and cross-contamination risks

Allergen and cross-contamination risks are critical challenges in the functional flour market. Functional flours, often derived from pulses, nuts, seeds, and alternative grains, carry inherent allergen profiles such as pea, soy, and nut flours. When processed in facilities handling wheat or gluten, the need for stringent segregation, cleaning, and testing protocols becomes essential to prevent cross-contact, which could lead to health risks and regulatory complications. To address these concerns, ingredient suppliers and food manufacturers invest in specialized allergen management systems and traceability measures, adding complexity and cost. For example, Avena Foods employs dedicated production lines and certification processes to mitigate cross-contamination risks, particularly for gluten-free and allergen-free claims, ensuring safety alongside functionality. In a market driven by clean-label and health-focused demands, managing allergen risks is integral to quality control, as even minor contamination can result in recalls, brand damage, or regulatory scrutiny. These challenges necessitate close collaboration between manufacturers and producers to implement robust segregation, testing, and certification practices. Balancing ingredient innovation with rigorous risk mitigation strategies is essential to maintaining consumer trust and ensuring compliance across bakery, snack, and specialty food applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Legumes Outpace Cereals on Protein Demand

Cereal-based functional flours hold the largest share in the market, contributing 62.98% to overall expansion. Staples such as rice, corn, and wheat remain essential in Asia-Pacific diets and global bakery systems. Oat flour is increasingly favored for its beta-glucan content, which supports cholesterol-reduction claims approved by the U.S. Food and Drug Administration. Barley flour, traditionally linked to brewing and malt-extract industries, is now being adapted for soups and ready meals through low-beta-glucan variants to meet convenience-driven consumption trends. Quinoa and buckwheat flours bolster gluten-free premiumization strategies, while rye flour retains regional importance in Scandinavian and Eastern European bakery traditions, where sourdough fermentation addresses its dense crumb structure. These factors collectively underscore the foundational role of cereal-based flours in both heritage and volume-driven applications.

Legume-based functional flours are projected to grow at a faster CAGR of 8.74% through 2031, driven by the rising demand for plant-based protein formulations that emphasize amino acid completeness and allergen avoidance. Pea flour leads this segment with its neutral flavor and 20–25% protein concentration, making it ideal for dairy alternatives and meat analogues. Lentil flour is gaining traction in gluten-free bakery applications due to its binding properties and high iron content, exceeding 7 mg per 100 g, supporting anemia-reduction initiatives in South Asia. Soybean flour remains relevant in cost-sensitive applications, while chickpea and fava-bean flours cater to premium niches tied to clean-label and ethnic formulations. Advanced milling and air-classification technologies from suppliers like Bühler Group enable tailored protein functionality, supporting growth and diversification within this segment.

By Application: Meat Alternatives Drive Fastest Expansion

The bakery and confectionery segment accounts for the largest share of the functional flour market, contributing 40.05% to projected 2025 revenue. This growth is attributed to the increasing demand for clean-label reformulation and gluten-free products, which are transforming bread, cakes, and sweet goods to meet consumer expectations for transparent ingredient lists. Manufacturers are replacing chemical improvers with enzyme-treated and specialty flours to enhance crumb softness, moisture retention, and shelf stability while maintaining clean-label standards. Savory snacks are also utilizing functional flours to reduce fat absorption and increase protein content, as demonstrated by lentil-flour tortilla chips delivering 18% protein compared to 6% in corn-based alternatives. Additionally, soups, sauces, and ready-to-eat products are adopting pre-gelatinized and resistant-starch flours to improve efficiency and nutritional value, addressing the needs of convenience-driven categories.

The meat alternatives segment represents the fastest-growing application, with a projected CAGR of 7.63% through 2031. This expansion is driven by the rising popularity of plant-based meat and the need to replicate the texture and juiciness of animal protein using functional-flour blends. Pea and soy flours form the protein base, while wheat gluten and modified starches provide elasticity and moisture retention. Suppliers such as Roquette Frères are supporting this trend by offering pulse-derived functional flours and texturizing solutions tailored for advanced processing techniques, enabling manufacturers to enhance product quality and scalability.

Geography Analysis

North America is expected to account for 33.22% of the global functional flour market revenue by 2025, driven by its integrated ecosystem spanning raw material supply to value-added ingredient innovation. The United States' mature plant-based food sector and Canada’s position as the largest global exporter of pulses underpin this dominance. The demand for pea and soy flours in meat analogues and dairy alternatives is reinforced by the strong presence of alternative-protein brands in the United States, while Canada’s pulse infrastructure ensures reliable export flows of lentils and peas for functional milling. Companies like SunOpta Inc. capitalize on this regional strength by processing and supplying pulse-based functional flours tailored for protein fortification and gluten-free systems, aligning agricultural scale with formulation-driven demand.

The Asia-Pacific region is projected to grow at a CAGR of 8.79% through 2031, supported by rapid urbanization, rising disposable incomes, and government-led fortification mandates. In China, younger consumers adopting flexitarian diets are driving demand for pea- and soy-based flours in meat analogues and dairy alternatives. Japan’s aging population is increasing interest in high-protein, easy-to-digest flour systems for senior nutrition, while Australia’s gluten-free bakery segment is incorporating chickpea and lentil flours. The 2024 approval of lupin flour as a novel ingredient with mandatory allergen labeling by Food Standards Australia New Zealand further supports ingredient diversification. These factors position Asia-Pacific as a high-growth consumption hub and an innovation corridor for fortified and specialty flour solutions.

Europe maintains steady revenue contributions, driven by clean-label expectations and advanced regulatory frameworks that encourage minimally processed, transparently sourced functional flours. The region’s bakery culture and demand for gluten-free premium products sustain interest in oat, rye, and pulse-derived flours. Meanwhile, South America and the Middle East and Africa are witnessing growth due to national fortification programs and expanding middle-class populations seeking affordable protein-enriched staples. Soy, corn, and pulse flours dominate mass-market applications, with B2B innovators like Cosucra Groupe Warcoing supporting protein standardization and fiber enrichment strategies across these regions.

Regulatory Landscape

Functional flours sit between staple-flour composition requirements and ingredient-authorization pathways, so compliance depends on both fortification mandates and safety assessments for novel or modified fractions. In the United Kingdom, amendments to the Bread and Flour regime move non-wholemeal common wheat flour to mandatory folic acid fortification, with the requirement taking effect in December 2026 in England and Wales after a transition period for existing stocks. In China, GB/T 21122-2025 codifies technical requirements, classification, and labeling for fortified wheat flour, reinforcing country-specific formulation and label adaptation for global suppliers.

For functional fibers, protein-enriched fractions, and upcycled or modified flour components, approvals and notifications shape market access. In the United States, the FDA GRAS Notice Inventory remains a key route for commercial use of functional-flour-related ingredients, illustrated by the February 2026 no-questions response for Comet Biorefining Corporation (GRN 1266) covering wheat fiber extract from wheat (Triticum aestivum). In the European Union, use of certain functional ingredients may rely on EU rules for food additives and the Novel Food framework (Regulation (EU) 2015/2283), keeping dossiers, traceability, and exposure evidence central to commercialization, while draft proposals such as NAFDACs 2026 wheat and durum semolina fortification regulations in Nigeria highlight continuing divergence across emerging fortification markets.

Value Chain Analysis

The functional flour value chain begins with grain and pulse origination (wheat, rice, corn, oats, peas, lentils, soy, fava) and moves through cleaning, conditioning, milling, and functionalization steps such as pre-gelatinization, heat-moisture treatment, enzyme treatment, and air classification. Large agribusinesses and millers secure supply via grower programs and trading networks, while specialized processors tailor functionality (water binding, viscosity, emulsification, protein concentration) to application needs in bakery, snacks, soups and sauces, ready-to-eat products, baby food, and meat alternatives. Quality assurance is also closely tied to allergen management and specification control, particularly where facilities handle both gluten-containing cereals and gluten-free or pulse-based functional flours.

Distribution and application support increasingly influence competitive differentiation, with regional technical service and logistics helping customers manage reformulation and local regulatory requirements. In April 2026, DKSH signed an exclusive distribution agreement with Limagrain Ingredients covering Southeast Asia (including Malaysia, the Philippines, Singapore, Thailand, Vietnam, and Indonesia), bundling marketing, sales, logistics, and application services to shorten time-to-market for functional flour portfolios. Co-development partnerships also shape midstream value capture, including the April 2026 multi-year strategic alliance between Casillo and Puratos Italia in Italy to develop and market new functional baking ingredients, and collaborations such as MartinoRossi and Molini Bongiovanni (November 2025) that integrate protein extraction with custom milling for plant-based protein mixes for industrial savory bakery formats.

Competitive Landscape

The functional flour market is moderately fragmented, with vertically integrated grain merchants such as Cargill, ADM, and Bunge playing a dominant role. These companies manage significant commodity volumes through their global sourcing networks and multi-modal logistics, helping to stabilize input costs despite volatile grain prices and climate-related disruptions anticipated in 2026. By supplying flours with consistent specifications, they support multinational food manufacturers in producing bakery staples and snacks. Their operational scale ensures cost-efficient handling of high-volume orders for pre-cooked and fortified flours, meeting the growing demand driven by increasing household expenditures on staple foods across regions like North America and Asia-Pacific.

Cargill utilizes proprietary milling and modification technologies to deliver uniform gluten-free and high-fiber flours, which are essential for multinational snack producers seeking texture consistency in extruded products. ADM complements this by offering pulse- and cereal-based blends optimized for fortified staples, supported by multi-site logistics to address regional shortages. Bunge further strengthens the market by providing additive-free, stable flours for pasta and ready-to-eat foods, ensuring cost predictability and enabling manufacturers to maintain margins despite economic pressures and raw material price fluctuations expected in 2026.

Specialized processors like Ingredion and Associated British Foods focus on high-margin segments by delivering application-specific solutions. Ingredion’s texturizing flour systems enable precise viscosity control in plant-based patties, helping brands differentiate in the expanding alternative protein market while adhering to organic certifications demanded by premium consumers. Associated British Foods enhances this segment by offering certified organic pulse flours for hypoallergenic baby foods and gluten-free mixes. These efforts foster innovation and long-term partnerships, positioning these companies as key contributors to specialty growth within the evolving functional flour market.

Functional Flour Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Associated British Foods plc

-

Ingredion Incorporated

-

Bunge Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and route-to-market whitespace shows up where functional flours address multiple constraints at once, including clean-label bulking and texture replacement, protein and fiber fortification, and allergen or gluten-free positioning. Ingredient suppliers are commercializing label-friendly carbohydrate and starch solutions to replace additives like maltodextrin, as illustrated by Cargills SimPure soluble rice flour positioning for bakery, dairy, beverages, sauces, snacks, and seasonings. At the same time, fortification mandates and standards in large wheat-flour systems, including the UK folic acid requirement effective in December 2026 and Chinas GB/T 21122-2025 fortified wheat flour standard, support opportunities for premix-ready and specification-controlled functional flour systems that reduce compliance friction for bakers and food manufacturers.

Capacity buildouts and regional partnerships are expanding access to protein-forward and specialty flour formats, particularly in plant-based and gluten-free applications. BENEO inaugurated a pulse-processing plant in Offstein, Germany in April 2025 following a 50 million euro investment by the Suedzucker Group, adding industrial scale for faba bean-based functional ingredients, while Bankom completed a soybean processing expansion in Serbia in July 2026 that includes high-protein textured soy protein and expanded soy flour output. Commercial localization is also advancing, such as Eshbal Functional Food Inc. commencing commercial production in Canada in January 2026 for gluten-free flour blends, and distribution-led expansion, including the April 2026 DKSH and Limagrain Ingredients arrangement to broaden Southeast Asia coverage. Processing innovation continues to feed the pipeline, with research reporting progress in dry separation approaches for wheat flour fractionation that reduce energy intensity versus wet routes, which aligns with corporate sustainability scorecards and supports upcycling and side-stream valorization programs already influencing ingredient procurement.

Recent Industry Developments

- June 2026: Ingredion completed the acquisition of Benicaros, a prebiotic fiber ingredient produced from upcycled carrot pomace, broadening its fiber fortification toolkit. The move strengthens Ingredions positioning in clean-label functional ingredients that can be paired with functional flours in bakery, snacks, and nutrition-focused formulations.

- December 2025: Protein Industries Canada, Maia Farms, and Phytokana Ingredients announced a CAD 32.5 million project to process Canadian-grown fava beans into ingredients including fava flour, starch flour, and protein concentrate using a process designed to avoid heat and chemicals. The project adds supply-side momentum for pulse-based functional flours that target taste, texture, and nutrition requirements in plant-based dairy and meat applications.

- July 2024: Cargill launched SimPure 92260, a soluble rice flour positioned as a recognizable-ingredient alternative with functionality comparable to 10 DE maltodextrin. This expands clean-label formulation options for functional flour systems used in reduced-sugar bakery, powdered beverages, sauces, dressings, snacks, cereals, and flavor carrier applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the functional flour market covers food-grade flours that are processed or formulated to deliver added functionality in finished foods, such as better texture, higher fiber or protein, gluten-free performance, or improved shelf life.

Scope exclusions: We exclude non-food industrial flour uses and retail-ready mixes where flour is not the main value driver.

Segmentation Overview

-

By Source

-

Cereals

- Rye

- BuckWheat

- Oats

- Barley

- Quinoa

- Others (Rice, Corn, Sorghum)

-

Legumes

- Pea

- Lentil

- Soybean

- Others (Chickpea, Fava Bean)

-

Cereals

-

By Application

- Bakery and Confectionery

- Savory Snacks

- Soups and Sauces

- Ready To Eat Products

- Baby Food

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the market boundary and build an initial set of demand indicators that can be checked year to year. We reviewed public agriculture and food-manufacturing statistics such as USDA, FAO, and national statistical offices, then cross-referenced trade data (for example, UN Comtrade) to understand cross-border flour and cereal ingredient movements.

To keep inputs aligned with regulatory and formulation realities, we also referenced standards and nutrition guidance from sources such as the FDA and EFSA, plus peer-reviewed papers on hydrothermal treatment, extrusion, and fortification effects in bakery and prepared foods. Company filings, investor presentations, and reputable press were used to place functional flour within wider ingredient portfolios, and a paid subscription for company financials and a patent database supported checks on new claims and process directions. The sources listed here are illustrative and not exhaustive, and additional references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually sold as functional flour across regions, and how pricing and use rates shift by application (bakery, savory snacks, soups and sauces, and ready-to-eat products). We spoke with a mix of ingredient suppliers, processors, distributors, and food manufacturers, then used follow-ups to close gaps on typical inclusion rates, product substitution behavior, and regional labeling expectations.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 50% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 30% |

| Smaller Players: 15% | Managers: 57% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started from a top-down build where cereal and pulse processing output, trade flows, and downstream packaged food production were used to reconstruct the addressable flour pool. We then filtered that pool through functional-flour penetration by application and region. After the structure was in place, we used selective bottom-up checks such as sampled supplier revenue bands, typical price ranges by flour type, and volume-to-value conversions to confirm the totals and adjust outliers.

A few practical inputs were tracked because they explain most of the movement in this market, including bakery and snack production growth, consumer shifts toward high-protein and high-fiber labeling, the adoption rate of gluten-free and clean-label formulations, relative pricing versus conventional flour, and regional fortification or labeling rules that shape what can be marketed as functional. For forecasting, scenario analysis was used so the model can reflect different adoption speeds across regions, and then primary expert views were used to settle on a base-case path for penetration and pricing progression. Where bottom-up data was thin in smaller countries, we filled gaps using region-level ratios and per-capita packaged food indicators, then rechecked the implied volumes for reasonableness.

Data Validation & Update Cycle

Outputs were tested through triangulation across independent signals, and we reworked the model when growth rates or implied volumes moved outside normal food ingredient patterns. Any large variance by region or application triggered a second review, followed by re-contact with selected interviewees to confirm whether the change came from pricing, reformulation, or a genuine demand shift.

Before sign-off, the full chain of assumptions is reviewed in steps so that a change in one input does not quietly distort totals elsewhere. The report is refreshed annually, and interim updates are done when material events occur that can impact supply, pricing, or labeling. Prior to delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Functional Flour Market Estimate Compared With Other Published Estimates

Published market sizes for functional flour often do not match because firms draw the product boundary differently, and then apply different conversion choices for volume, pricing, and what qualifies as functional. The year chosen as the current point also matters because grain-linked pricing can swing and create big value shifts even when consumption is steadier.

Trade flow checks for cereal and pulse-derived ingredients, plus application-level consumption signals in bakery and ready-to-eat foods, are the evidence points that keep Mordor Intelligence's estimate tied to functional flour used as an ingredient in food manufacturing, rather than including standard flour volumes sold without functional positioning. Differences usually come from whether estimates fold in conventional flour sold into similar applications, how specialty flour premiums are applied across regions, and how quickly penetration is assumed to rise in emerging markets when clean-label and gluten-free adoption is still uneven.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 81.59 B (2026) | |

| Regional Consultancy A | USD 83.44 B (2024) | Uses an earlier current-year anchor and appears to group a wider set of specialty and fortified flours together, which can pull in volumes that are not consistently positioned as functional in end products. |

| Industry Publisher B | USD 70.80 B (2025) | Likely applies more conservative penetration and price-premium assumptions for gluten-free and protein-enriched flours, and may treat functional flour as a narrower subset focused on select health claims. |

The spread in the table is mainly explained by what gets counted as functional, how premiums are applied, and how base-year pricing is handled. By keeping assumptions tied to observable demand signals and then cross-checking value against practical price bands, the model stays transparent and repeatable for decision-making.

Key Questions Answered in the Report

What is the forecast value of global functional flour sales by 2031?

They are projected to reach USD 115.40 billion, reflecting a 7.18% CAGR from 2026 to 2031.

Which ingredient type is growing fastest within functional flours?

Legume-based flours, spearheaded by pea and lentil variants, are advancing at an 8.74% CAGR to 2031.

Why are functional flours important in plant-based meat?

They create cohesive protein matrices during high-moisture extrusion, replacing hydrocolloids while improving juiciness and bite in meat analogues.

Which region is expected to post the fastest growth?

Asia-Pacific, supported by fortification mandates and a shift toward flexitarian diets, is forecast to expand at an 8.79% CAGR through 2031.

Page last updated on: