Cornmeal Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

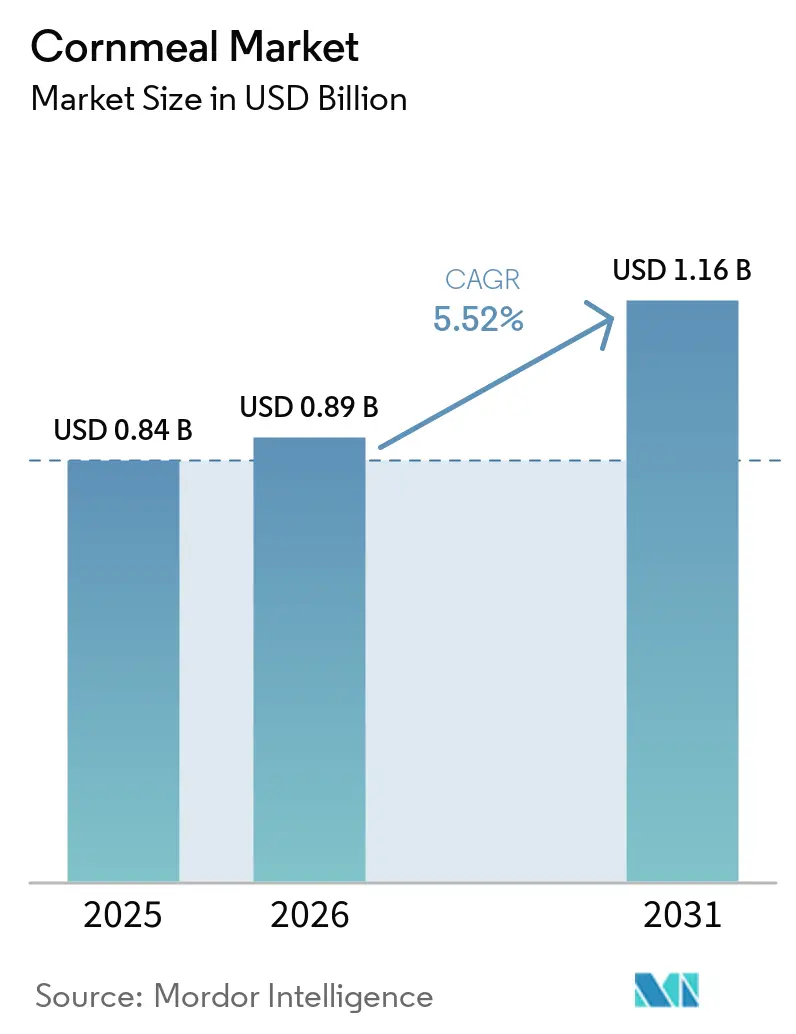

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cornmeal Market Analysis by Mordor Intelligence

The cornmeal market size was valued at USD 0.84 billion in 2025 and estimated to grow from USD 0.89 billion in 2026 to reach USD 1.16 billion by 2031, at a CAGR of 5.52% during the forecast period (2026-2031). Rising consumer preference for naturally gluten-free staples, accelerating adoption of ethnic dishes that rely on masa, polenta, and grits, and steady industrial demand for coating and breading blends continue to anchor the cornmeal market. Regulatory focus on gluten-cross contact, mycotoxin limits, and transparent labeling is nudging manufacturers toward dedicated, certified milling lines. Robust U.S. corn harvests and comparatively stable 2026 futures pricing are giving processors cost visibility, while contract farming of blue and organic varieties is helping premium brands secure differentiated supply. At the same time, food-service chains are standardizing cornmeal-based coatings across regions, deepening penetration in quick-service and convenience formats.

Key Report Takeaways

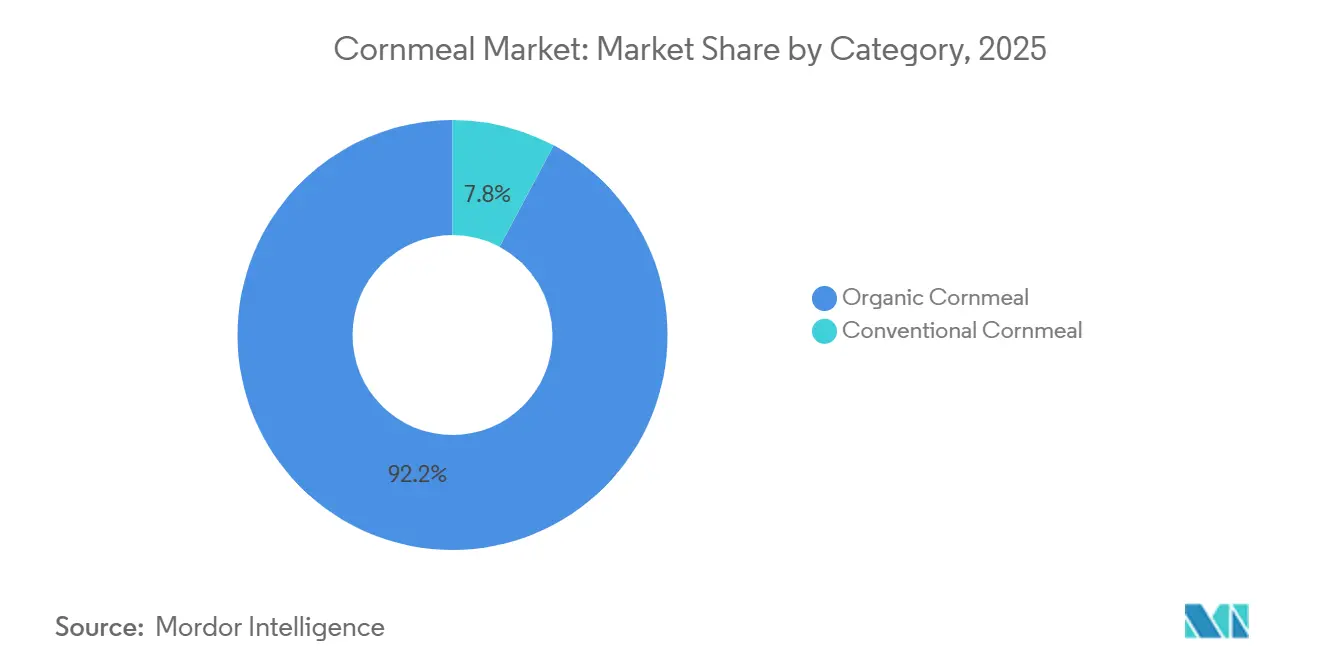

- By category, conventional formats held 92.25% of the cornmeal market share in 2025, whereas organic variants are advancing at a 7.46% CAGR through 2031.

- By product type, yellow cornmeal led with 59.08% revenue share in 2025, while blue cornmeal is forecast to expand at a 6.68% CAGR between 2026 and 2031.

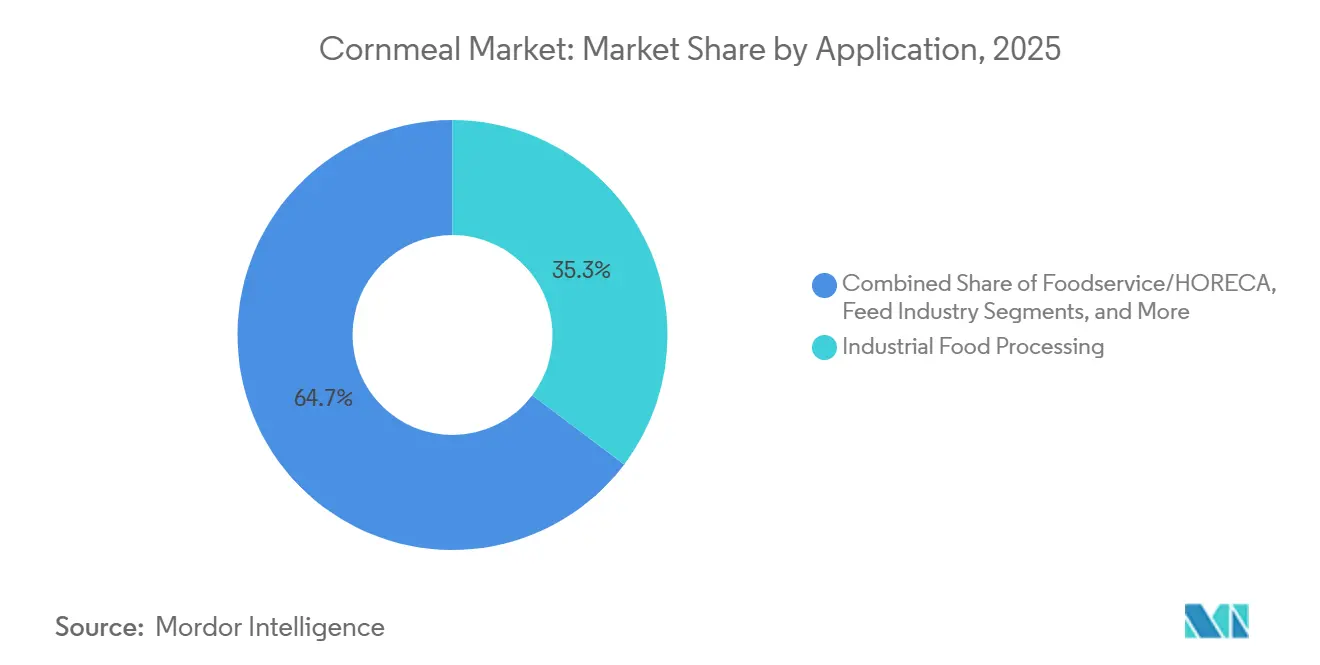

- By application, industrial food processing accounted for 35.28% of the cornmeal market in 2025; the retail segment is projected to post the fastest growth at a 6.84% CAGR through 2031.

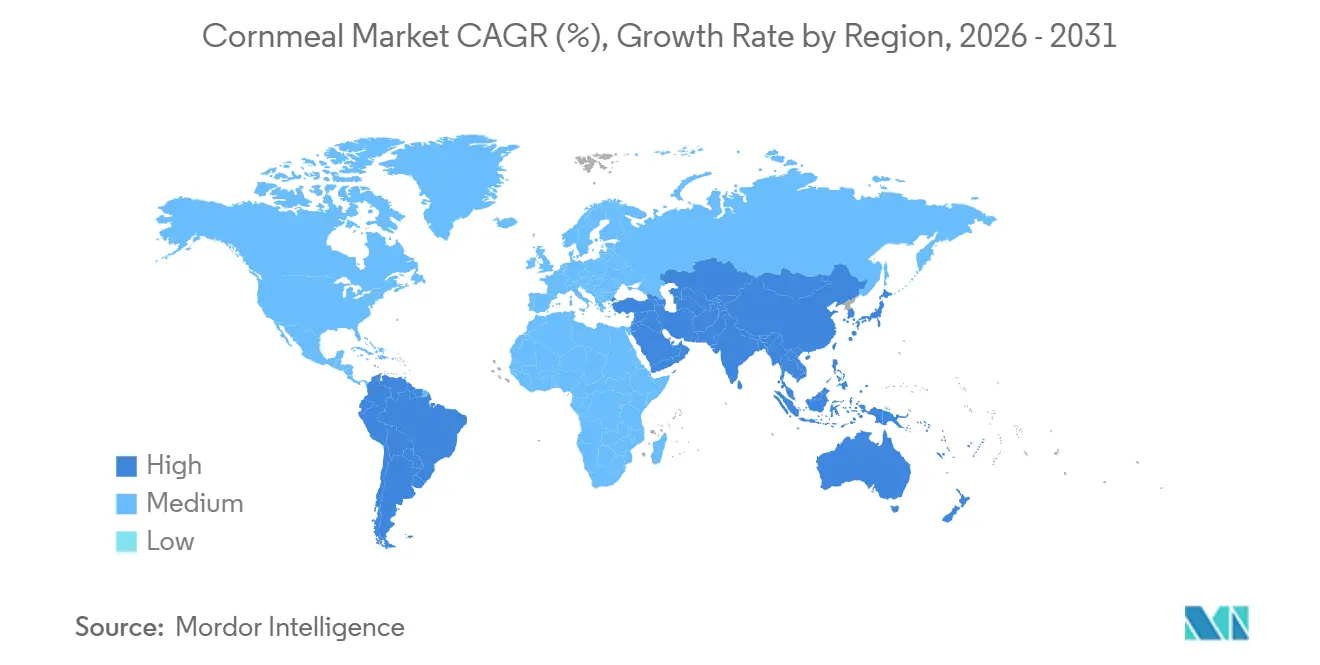

- By geography, North America accounted for 32.22% of revenue in 2025, while Asia-Pacific is on track to be the fastest-growing region at a 6.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cornmeal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Gluten-free Staple Ingredients | +0.9% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of Ethnic and Regional Cuisine Consumption | +0.7% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Growth in Ready-to-cook and Instant Meal Mixes | +0.6% | North America, Europe, Asia-Pacific metro areas | Medium term (2-4 years) |

| Increased Use in Coating and Breading Applications | +0.5% | Global, led by North America and Europe foodservice | Short term (≤ 2 years) |

| Expansion of Snack Industry Using Corn-based Inputs | +0.8% | Global, with Asia-Pacific and Latin America growth | Medium term (2-4 years) |

| Growth of Organic and Non-GMO Cornmeal Products | +0.4% | North America and Europe premium retail channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for gluten-free staple ingredients

Celiac disease prevalence and non-celiac gluten sensitivity are driving regulatory and commercial momentum for gluten-free labeling. The FDA issued a Request for Information in January 2026 addressing gluten cross-contact prevention and ingredient disclosure, responding to a citizen petition that sought mandatory listing of all gluten-containing ingredients and inclusion of gluten on the allergen list in the FDA Compliance Policy Guide Section 555.250[1]Source: U.S. Food and Drug Administration, “Compliance Policy Guide: Sec. 555.400 Aflatoxins in Human Food,” fda.gov. USDA Food Safety and Inspection Service Directive 7230.1, effective September 2025, added gluten to the list of ingredients requiring accurate control and labeling under the "Big 9" allergen framework, signaling heightened scrutiny across federal agencies. Cornmeal benefits as a naturally gluten-free flour substitute with established supply chains and processing infrastructure. Retail penetration accelerates as manufacturers reformulate baked goods, coatings, and snack bases to meet gluten-free claims, leveraging cornmeal's functional properties, binding, texture, and neutral flavor that wheat flour traditionally provided. The regulatory tightening on cross-contact also elevates compliance costs for wheat-based facilities, indirectly favoring dedicated corn milling operations that can certify gluten-free status without extensive facility segregation.

Expansion of ethnic and regional cuisine consumption

Mexican food consumption among U.S. adults rose, with tacos the most preferred item and nachos driving additional corn chip demand. Grocery stores accounted for the majority of Mexican foods consumed by adults overall and by Hispanic consumers, indicating robust retail demand for corn tortillas, masa harina, and cornmeal used in home preparation. Hispanic adults exhibited a 2-to 3-fold higher prevalence of Mexican food consumption than other demographic groups, and this cohort's purchasing power and population growth underpin sustained demand for corn-based staples. Mexican food accounted for approximately 30% of daily energy intake on days it was eaten, with dinner accounting for 48% of consumption occasions, suggesting meal-centric usage that drives volume per capita, according to USDA FSRG. Beyond Mexican cuisine, regional preferences for polenta in Italy, arepa flour in Colombia and Venezuela, and fermented corn porridges in sub-Saharan Africa create diverse demand vectors. Migration patterns and urbanization in Asia-Pacific and Middle East markets are introducing corn-based products to new consumer segments, though penetration remains nascent compared to wheat and rice staples.

Growth in ready-to-cook and instant meal mixes

Convenience-driven consumption is reshaping cornmeal demand as meal kit services and ready-to-cook formats proliferate. Cornmeal's shelf stability, quick cooking time, and versatility in breading, batters, and side dishes align with time-pressed households seeking semi-prepared ingredients. Industrial food processors are incorporating finer cornmeal grades into instant polenta, cornbread mixes, and coating systems that require minimal preparation. The shift toward e-commerce grocery channels, accelerated and sustained through 2025, has expanded distribution reach for specialty cornmeal products, organic, stone-ground, and heirloom varieties that previously faced limited retail shelf space. Foodservice operators, particularly quick-service restaurants, are adopting pre-mixed cornmeal coatings for chicken tenders, fish fillets, and vegetable fritters to standardize quality and reduce labor costs. Cargill's April 2026 partnership with Saatvik Agro to establish a 500-tonne-per-day corn milling plant in Madhya Pradesh, India, with scalability to 1,000 tonnes per day, reflects strategic positioning to serve rising domestic demand for starch derivatives and processed corn ingredients in ready-to-eat and instant food segments, according to Agro Spectrum India. The facility targets the North and West India markets, where urbanization and dual-income households are driving the adoption of convenience foods.

Increased use in coating and breading applications

Cornmeal's coarse texture and adhesion properties make it a preferred ingredient in coating systems for fried and baked proteins. Foodservice and industrial food processing segments leverage cornmeal to achieve crispy exteriors on chicken, seafood, and vegetables, with particle sizes tailored to application: coarser grades for rustic coatings and finer grades for uniform breading. The global expansion of quick-service restaurant chains, particularly in Asia-Pacific and Middle East markets, is standardizing coating formulations that incorporate cornmeal alongside wheat flour and starches. Regulatory pressure to reduce trans fats and acrylamide formation in fried foods has prompted reformulation efforts; cornmeal's lower protein content compared to wheat flour can reduce acrylamide precursors when combined with optimized frying protocols. Additionally, gluten-free coating systems for allergen-sensitive consumers and Halal-certified foodservice operators increasingly specify cornmeal as a base ingredient. Industrial processors are investing in automated bread lines that require consistent particle-size distribution and moisture content, driving demand for degerminated cornmeal with a fat content below 2.25% to meet the FDA fumonisin guidance of 2 ppm for degermed products, according to the National Grain and Feed Association. This specification creates a quality premium for millers capable of precise fractionation and mycotoxin control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Susceptibility to Mycotoxin Contamination in Corn Supply | -0.6% | Global, acute in humid/tropical regions and improper storage | Short term (≤ 2 years) |

| Price Fluctuations Driven by Corn Commodity Market Volatility | -0.5% | Global, transmission via futures markets and export flows | Short term (≤ 2 years) |

| Competition from Alternative Flours (Wheat, Rice, Oat, Almond) | -0.4% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Vulnerability to Climate Impacts on Corn Harvest Yields | -0.3% | Central Plains U.S., parts of Latin America, sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Susceptibility to mycotoxin contamination in corn supply

Aflatoxins and fumonisins pose persistent quality and regulatory risks to cornmeal supply chains. FDA's Compliance Policy Guide Section 555.400 sets a 20 parts per billion action level for total aflatoxins in human food, while fumonisin guidance specifies 2 ppm for degermed dry-milled cornmeal (fat content below 2.25%) and 4 ppm for whole or partially degermed products. FDA updated its mycotoxin surveillance program in September 2024, adopting the multi-mycotoxin LC-MS/MS method C-003 to simultaneously detect 12 analytes, including aflatoxins, fumonisins, deoxynivalenol, ochratoxin A, zearalenone, and T-2/HT-2 toxins, thereby increasing detection sensitivity and enabling enforcement actions. Import Alert 23-14, published April 10, 2026, mandates Detention Without Physical Examination for corn flour and bolted meal shipments from multiple countries, including recent additions from India, Mexico, Ghana, and Guatemala, that failed to meet mycotoxin thresholds, requiring Laboratory Accreditation for Analyses of Food (LAAF)-accredited testing for release, according to the U.S. Food and Drug Administration. Mycotoxin contamination is climate-dependent: hot, dry conditions followed by high humidity favor fumonisin-producing Fusarium species, while aflatoxin-producing Aspergillus thrives in warm, humid environments during pre-harvest, harvest, and post-harvest storage. A three-year North Carolina State University study found that biocontrol strains AF36 and Afla-Guard applied at 7.5-10 pounds per acre reduced aflatoxin levels, and Bt hybrid Viptera (N78S-3111) significantly lowered both aflatoxin and fumonisin contamination, though fungicide applications yielded inconsistent results, according to the NC State Extension. Millers face trade-offs between sourcing low-cost corn from regions with higher contamination risk and premium-priced corn from suppliers implementing biocontrol and hybrid selection, with testing and rejection costs adding 2-5% to raw material expenses.

Price fluctuations driven by corn commodity market volatility

Corn commodity prices directly influence cornmeal production costs, yet 2026 exhibits relative stability. USDA Risk Management Agency's February 2026 price discovery set the projected price for December 2026 corn futures at USD 4.62 per bushel, down USD 0.08 from 2025's USD 4.70, with a volatility factor of 0.15, the lowest in 15 years, reducing revenue protection premiums and signaling market expectations of ample supply. USDA's May 2025 Feed Outlook projected 2025/26 season-average farm prices at USD 4.20 per bushel, supported by record U.S. corn production of 15.820 billion bushels and a stocks-to-use ratio of 11.6%, though strong export demand of 2.675 billion bushels and elevated feed use of 5.900 billion bushels temper downside price risk, according to USDA ERS. Ethanol demand remains stable at 5.500 billion bushels, consuming approximately one-third of U.S. corn production and limiting availability for food-grade milling despite large aggregate supplies, according to the USDA ERS. International price dynamics introduce volatility: Brazil's 1.8% grain export tax and potential additional fees of USD 0.40 per 60-kilogram bag raise export prices and reduce competitiveness, while Argentina lowered export taxes to boost shipments, and China lifted some tariff exemptions on U.S. agricultural imports, shifting demand toward South American origins, according to the Agricultural and Processed Food Products Export Development Authority. Cornmeal processors with limited hedging programs face margin compression when corn prices spike due to weather shocks or export surges, though Archer Daniels Midland's 2024 10-K disclosed hedging 9-26% of anticipated monthly corn grind over 12 months, illustrating industry practices to mitigate short-term price swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Gains Traction Despite Conventional Dominance

Conventional cornmeal accounted for 92.25% of the market in 2025, underpinned by well-established supply chains, cost advantages, and widespread acceptance across foodservice, industrial processing, and retail channels. Its dominance is supported by economies of scale in milling, lower raw material costs, and flexibility across multiple applications ranging from animal feed to human consumption, allowing processors to optimize capacity utilization and mitigate commodity price volatility. However, the segment operates in a mature, fragmented supplier landscape, leading to sustained pricing pressure. Margins are further constrained by competing demand from ethanol production, which diverts approximately 5.5 billion bushels of U.S. corn annually, thereby tightening the availability of food-grade corn, according to the USDA ERS. Non-GMO cornmeal, while often perceived similarly to organic products, faces structural supply constraints in regions where genetically modified crop cultivation dominates. In India, where corn production is largely non-GMO by default and reached 43-44 million metric tons in 2025/26, domestic ethanol blending policies redirected 7-9 million metric tons toward biofuel, reducing exportable volumes to key markets such as Nepal, Bhutan, Bangladesh, and Vietnam, as reported by the USDA FAS India. In China, high import tariffs on corn flour, 59% within quota and 90% outside quota, support domestic conventional producers but increase input costs for manufacturers reliant on non-GMO imports, according to the USDA FAS Beijing. Despite these pressures, conventional cornmeal maintains resilience due to its versatility, with applications spanning coatings, breading, and extruded snacks in industrial processing, staple uses such as polenta and cornbread in foodservice, and inclusion in livestock feed, which helps stabilize demand during periods of surplus.

Organic cornmeal, while representing a smaller share of the market, is projected to expand at a CAGR of 7.46% from 2026 to 2031, driven by certification standards such as the USDA National Organic Program and increasing retailer requirements for non-GMO Project Verified ingredients. Supply growth remains constrained by inherent production challenges, including yield reductions of 10-20% compared to conventional hybrids due to limitations on synthetic inputs and pest control methods, which in turn sustain farm-gate price premiums of 30-50%. Demand is primarily concentrated in North America and Europe, where retailers such as Whole Foods, Sprouts, and specialty grocers actively allocate shelf space to organic offerings. Strategic initiatives by major food companies further support category development; for instance, General Mills’ November 2025 commitment to significantly expand the use of Kernza perennial grain in Cascadian Farm cereals highlights efforts to scale sustainability-oriented ingredients through collaborations with academic institutions and farmer incentive programs—an approach that may be extended to organic cornmeal. Nevertheless, the requirement for a three-year transition period for organic certification, during which producers incur higher costs without access to premium pricing, continues to limit the pace of acreage expansion.

By Product Type: Yellow Cornmeal Leads, Blue Variant Commands Premium

Yellow cornmeal accounted for 59.08% of the market in 2025, supported by the widespread cultivation of yellow dent corn hybrids, strong consumer familiarity, and versatility across baking, frying, and industrial applications. Its leading position is reinforced by agronomic benefits, as hybrid yellow dent corn offers stable yields, resistance to lodging, and compatibility with mechanized harvesting, thereby lowering production costs and ensuring a consistent supply. From a processing perspective, millers favor yellow corn due to its uniform kernel size, lower moisture variability, and reliable starch-to-protein ratios, which facilitate standardized production and compliance with industrial specifications. In contrast, white cornmeal serves markets with more regional concentration, particularly in Central and South America, sub-Saharan Africa, and the Southern United States, where it is traditionally used in products such as tortillas, grits, and porridges. While it competes with yellow cornmeal in applications such as gluten-free baking mixes and polenta due to its milder flavor and lighter color, it lacks the carotenoid content, including lutein and zeaxanthin, found in yellow corn that supports eye health positioning. Other varieties, including red and multicolored heirloom cornmeal, remain limited to artisanal and specialty retail channels, where their distinct flavor profiles and origin narratives appeal to niche consumers, although inconsistent supply and higher costs restrict broader market penetration.

Blue cornmeal is projected to grow at a CAGR of 6.68% between 2026 and 2031, driven by its nutritional differentiation and premium positioning. It contains anthocyanin antioxidants, exhibits 8–20% higher protein content compared to commercial yellow hybrids, and has a lower glycemic index due to differences in starch digestibility, as noted by New Mexico State University. However, production constraints remain significant, with yields ranging from 1,000 to 4,000 pounds per acre compared to 8,000 to 10,000 pounds for hybrid dent corn, necessitating contract farming arrangements with strict quality parameters, including kernel color intensity, moisture levels below 13%, stress cracks under 10%, and off-type kernels below 2%[2]Source: Lois Grant, “Blue Corn Production and Marketing in New Mexico,” New Mexico State University, nmsu.edu. Kernel size also influences product quality, as smaller kernels produce a more pronounced flavor and deeper color, while larger kernels contain higher proportions of white starchy endosperm, reducing color intensity and leading to grading differentials. Blue cornmeal is primarily targeted at health-conscious consumers, specialty food producers, and ethnic markets seeking authentic Southwestern U.S. and Mexican heritage products. Although anthocyanins support antioxidant-related positioning, scientific evidence regarding their bioavailability and health benefits remains limited, and no qualified health claims have been approved by the FDA. Additionally, the open-pollinated nature of blue corn allows farmers to retain and selectively breed seeds for desired traits, but this genetic variability introduces challenges for large-scale processing and necessitates post-harvest sorting to maintain product consistency.

By Application: Industrial Scale Meets Retail Growth

Industrial food processing accounted for 35.28% of the market share in 2025, driven by coating and breading systems, extruded snacks, and ingredient blends for baked goods. Industrial food processors prioritize degerminated cornmeal with a fat content below 2.25% to meet the FDA's fumonisin guidance of 2 ppm, as germ fractions concentrate mycotoxins and shorten shelf life, according to the National Grain and Feed Association. Coating systems for quick-service restaurant chains require consistent particle size distribution, typically 300-600 microns for meal and 212-300 microns for fine meal, to ensure uniform adhesion and frying performance, according to the National Library of Medicine. Cargill's April 2026 partnership with Saatvik Agro to establish a 500-tonne-per-day corn milling plant in Madhya Pradesh, India, with scalability to 1,000 tonnes per day, targets starch derivatives for the food industry, reflecting strategic positioning to serve processed food manufacturers in North and West India, according to Agro Spectrum India. Foodservice/HORECA (hotels, restaurants, catering) relies on cornmeal for polenta, cornbread, and frying batters, with demand tied to dining traffic and menu innovation. The feed industry absorbs off-grade cornmeal and corn gluten meal as protein and energy sources for poultry, swine, and aquaculture, providing a demand floor during oversupply periods. Other applications include pet food, industrial starches, and fermentation substrates, though volumes are modest compared to food uses.

Retail is expanding at 6.84% CAGR through 2026-2031, benefiting from e-commerce penetration, meal kit adoption, and consumer interest in gluten-free and ethnic cooking. Retail cornmeal sales concentrate in North America, where 44% of Mexican food consumed by U.S. adults is sourced from grocery stores, translating to sustained demand for masa harina, cornmeal, and corn flour for home preparation of tortillas, tamales, and cornbread, according to the USDA FSRG. E-commerce platforms enable specialty cornmeal brands, stone-ground, organic, heirloom, to reach niche consumers without competing for limited retail shelf space, though logistics costs and product fragility (stone-ground cornmeal's higher fat content reduces shelf life) constrain profitability. Foodservice operators face labor cost pressures and menu simplification trends that favor pre-mixed coatings and batters over bulk cornmeal requiring on-site preparation, shifting demand toward value-added industrial products. Feed industry demand for corn gluten meal and off-grade cornmeal provides price support during periods of human-food oversupply, though feed prices are sensitive to soybean meal and DDGS (distillers dried grains with solubles) competition, with India's DDGS supply projected to rise from 3.2 million metric tons in 2024/25 to 4.2 million metric tons in 2025/26 as ethanol production expands, according to the USDA FAS India.

Geography Analysis

North America accounted for 32.22% of global cornmeal revenue in 2025, supported by a record U.S. corn harvest of 16.75 billion bushels and a season-average farm price of USD 4.00 per bushel, which improved feedstock affordability, according to the USDA. Export volumes of 2.675 billion bushels maintained relatively tight but stable supply conditions, while ethanol production absorbed approximately one-third of total output, indirectly supporting prices for degermed cornmeal. In Mexico, strong cultural demand for tortillas continues to drive consumption of both white and yellow cornmeal through domestic production and imports, while Canada’s 4% increase in corn acreage has yet to generate significant exportable surpluses, sustaining the region’s reliance on imports for specialized milling products. Additionally, North America leads in the adoption of certified gluten-free milling infrastructure, reflecting compliance with stringent FDA regulations and providing processors with a competitive advantage in international markets.

Asia-Pacific is expected to record the fastest growth, with a projected CAGR of 6.45% through 2031. India produced approximately 43 million metric tons of corn in 2025/26; however, government ethanol blending policies diverted up to 9 million metric tons toward biofuel production, thereby tightening supply for food-grade processing, as reported by the USDA[3]Source: Santosh K. Singh, “Grain and Feed Update,” USDA Foreign Agricultural Service New Delhi, usda.gov. Investments such as Cargill’s 500-tonne-per-day milling facility in Madhya Pradesh highlight the region’s growing demand for processed and convenience foods. In China, high import tariffs, 59% within quota and 90% outside quota, continue to protect domestic producers and limit import penetration despite rising demand for snack products, according to the USDA. Across Southeast Asia, corn usage remains largely concentrated in animal feed, although the rapid expansion of foodservice formats such as bubble tea outlets and fried snack vendors is gradually increasing the use of cornmeal-based coatings, indicating potential growth opportunities for specialty imports.

In Europe increasing dependence on imports, particularly to meet demand from Italy’s polenta producers and Germany’s gluten-free bakery segment. While policy initiatives promoting regenerative agriculture may support future production of specialty corn, short-term market stability remains closely tied to supply from key exporters such as Ukraine and Brazil. In Latin America, Brazil’s production of 132 million metric tons underscores its role as a major global supplier; however, the region remains exposed to weather-related risks, including delays in safrinha planting that can influence global price dynamics. In Africa, corn continues to be primarily utilized for staple foods such as porridge, with industrial milling capacity still at an early stage of development. Nevertheless, improvements in post-harvest infrastructure and the implementation of regional trade agreements are facilitating the emergence of packaged cornmeal and instant grits, positioning the continent as a prospective long-term growth market.

Competitive Landscape

The cornmeal market demonstrates moderate concentration, with both large, vertically integrated processors and numerous regional milling companies. Major players continue to scale operations and manage input cost volatility through structured procurement and risk mitigation strategies. For instance, Archer Daniels Midland processed 18.541 million metric tons of corn in 2024 through its Carbohydrate Solutions segment, generating USD 11.234 billion in revenue, while employing hedging strategies that cover approximately 9-26% of its anticipated monthly corn grind to manage price fluctuations. Strategic portfolio realignment is also evident, as reflected in Bunge’s July 2025 divestiture of its North American dry corn and masa milling assets to Grain Craft, including six facilities and around 600 employees, enabling Bunge to focus on global value chains while supporting Grain Craft’s expansion into corn-based ingredients. Similarly, Cargill’s April 2026 partnership with Saatvik Agro to establish a 500-tonne-per-day milling facility in Madhya Pradesh, scalable to 1,000 tonnes per day, highlights efforts to capture growing demand for processed corn derivatives in emerging urban markets.

Downstream integration and brand positioning remain key competitive strategies across the value chain. PepsiCo’s Frito-Lay division benefits from vertically integrated sourcing and processing capabilities to support its tortilla chip and corn snack portfolio, while companies such as Goya Foods and Empresas Polar (P.A.N.) maintain strong positions in the masa harina segment across Latin America and U.S. Hispanic markets. At the same time, regional and specialty millers, including Bob’s Red Mill, Heartland Mill, and Shagbark Seed & Mill, differentiate themselves through organic certification, stone-ground production methods, and the use of heirloom corn varieties, enabling them to capture higher-margin retail niches. Across the industry, strategic priorities include vertical integration, geographic expansion, and product diversification. In addition, investments in agricultural inputs and quality control, such as biocontrol methods and Bt hybrid adoption, are being utilized to reduce mycotoxin contamination; research from North Carolina State University indicates that approaches such as AF36 biocontrol and Viptera hybrids can significantly lower aflatoxin and fumonisin levels, thereby supporting regulatory compliance and reducing testing costs.

Emerging growth opportunities are centered on product innovation and supply chain differentiation. These include scaling blue cornmeal production through contract farming and hybrid development, expanding non-GMO cornmeal exports to Asia-Pacific markets with restrictions on genetically engineered crops, and developing value-added retail offerings such as organic stone-ground cornmeal and ready-to-cook polenta kits. New entrants and smaller players are increasingly leveraging e-commerce channels to bypass traditional retail limitations, while emphasizing traceability, regenerative agriculture, and heritage grain narratives to appeal to premium consumers. Technological advancements are also shaping the competitive landscape, with a focus on precision milling to achieve consistent particle size for industrial applications, adoption of multi-mycotoxin testing methods such as LC-MS/MS to meet regulatory standards, and the use of blockchain for traceability in organic and non-GMO supply chains. Furthermore, regulatory developments, such as the U.S. FDA’s September 2024 update to Compliance Program 7307.001, which requires Laboratory Accreditation for Analyses of Food (LAAF)-certified testing for mycotoxin compliance and removal from Import Alert 23-14, are increasing compliance requirements and favoring processors with access to accredited laboratory capabilities.

Cornmeal Industry Leaders

Archer Daniels Midland Company

PepsiCo, Inc.

Bunge Global SA

Cargill, Incorporated

Shagbark Seed & Mill

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cargill inaugurated a corn milling plant in Gwalior, Madhya Pradesh, India, in partnership with Saatvik Agro Processors, with an initial capacity of 500 tonnes per day, scalable to 1,000 tonnes per day.

- July 2025: Grain Craft completed the acquisition of Bunge's North American dry corn milling assets, including six facilities, a transload/packaging facility, and a distribution warehouse.

- July 2025: Bunge and Viterra finalized their merger, creating an enlarged agribusiness with enhanced grain-origination reach.

- January 2025: Cargill acquired two U.S. feed mills from Compana Pet Brands to strengthen its animal nutrition distribution capacity.

Global Cornmeal Market Report Scope

Cornmeal is a coarse flour made from dried maize (corn), widely used as a staple ingredient in food processing, culinary applications, and animal feed. The cornmeal market is segmented by category, product type, application, and geography. By category, the market includes organic cornmeal and conventional cornmeal. By product type, the market is segmented into yellow cornmeal, white cornmeal, blue cornmeal, and other variants. Based on application, the market covers industrial food processing, foodservice/HORECA, feed industry, retail, and other uses. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been conducted on a value basis (USD million).

| Organic Cornmeal |

| Conventional Cornmeal |

| Yellow Cornmeal |

| White Cornmeal |

| Blue Cornmeal |

| Others |

| Industrial Food Processing |

| Foodservice/HORECA |

| Feed Industry |

| Retail |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Organic Cornmeal | |

| Conventional Cornmeal | ||

| By Product Type | Yellow Cornmeal | |

| White Cornmeal | ||

| Blue Cornmeal | ||

| Others | ||

| By Application | Industrial Food Processing | |

| Foodservice/HORECA | ||

| Feed Industry | ||

| Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the cornmeal market today and where is it heading?

The cornmeal market size stood at USD 0.89 billion in 2026 and is projected to reach USD 1.16 billion by 2031, registering a 5.52% CAGR.

Which region grows the fastest in cornmeal demand?

Asia-Pacific is forecast to expand at a 6.45% CAGR through 2031, lifted by India’s convenience-food boom and China’s tariff-protected local processing base.

Which segment leads and which one grows quickest within the cornmeal category split?

Conventional cornmeal captured 92.25% share in 2025, while the organic segment is the fastest gainer at a 7.46% CAGR to 2031.

Why is blue cornmeal attracting attention despite small volumes?

Blue cornmeal carries anthocyanin antioxidants, 8-20% higher protein, and a compelling heritage story, factors driving its 6.68% CAGR even though low field yields limit supply.

How are regulators influencing cornmeal manufacturing?

FDA’s tighter mycotoxin surveillance and ongoing work on gluten-cross contact labeling are pushing mills toward certified gluten-free lines and rigorous toxin testing, raising technical barriers to entry.

Page last updated on: