Banana Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

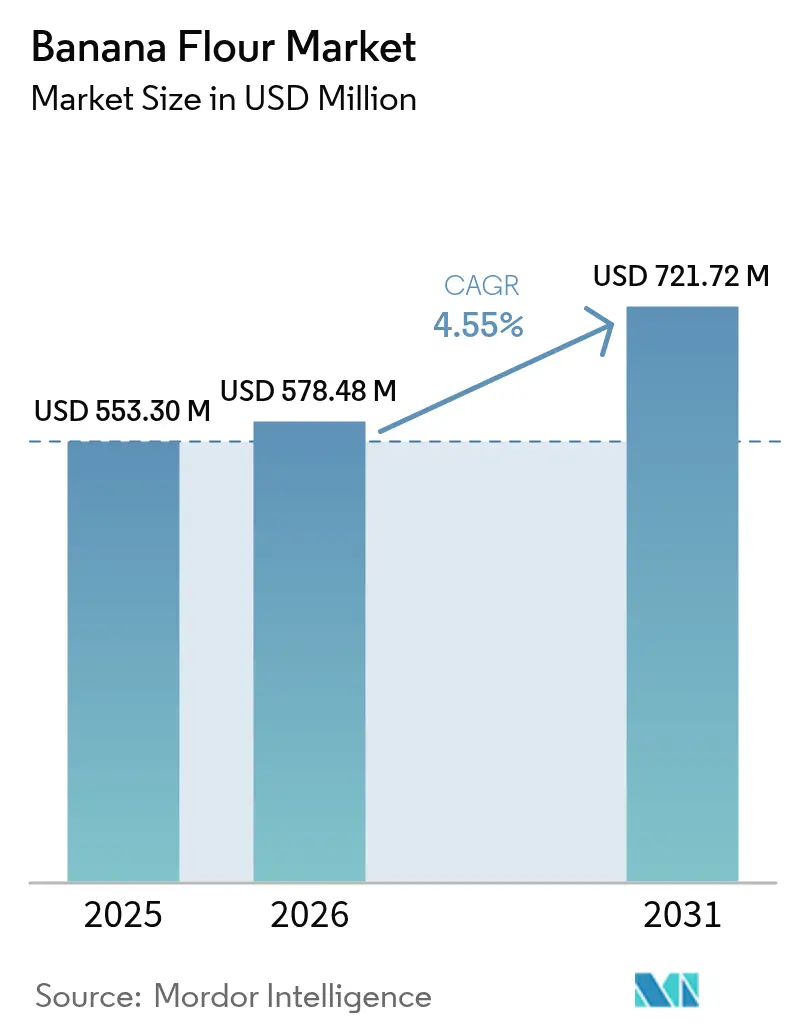

| Market Size (2026) | USD 578.48 Million |

| Market Size (2031) | USD 721.72 Million |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Banana Flour Market Analysis by Mordor Intelligence

The banana flour market size in 2026 is estimated at USD 578.48 million, growing from 2025 value of USD 553.3 million with 2031 projections showing USD 721.72 million, growing at 4.55% CAGR over 2026-2031. The banana flour market is witnessing substantial growth, primarily driven by the increasing demand for gluten-free and resistant-starch ingredients, coupled with a rising consumer inclination toward clean-label products. This trend reflects a broader shift in consumer preferences toward healthier and more transparent food options. Manufacturers are increasingly leveraging banana flour due to its ability to meet critical consumer needs, including improved digestive health, effective blood sugar management, and enhanced sustainability. Furthermore, regulatory initiatives, such as the FDA's phased removal of synthetic food dyes, are accelerating the transition toward natural ingredients, creating additional growth opportunities for the market. The competitive landscape is further shaped by supply-side advantages in the Asia-Pacific region, which ensure a steady raw material supply, and significant advancements in functional food innovation across North America and Europe, driving product diversification and market expansion.

Key Report Takeaways

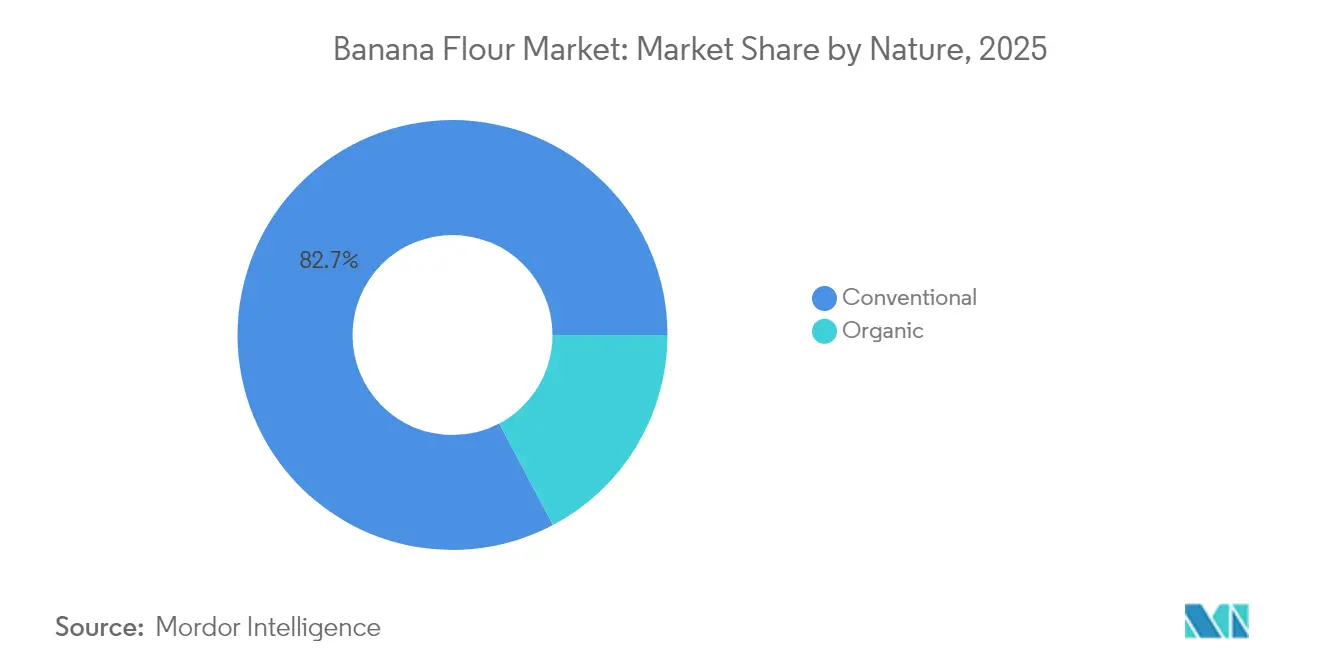

- By nature, the conventional segment held 82.74% of the banana flour market share in 2025, while organic flour is advancing at a 5.52% CAGR to 2031.

- By source, green unripe bananas accounted for 91.42% of the banana flour market size in 2025; the ripe-banana segment is projected to grow at 5.55% CAGR through 2031.

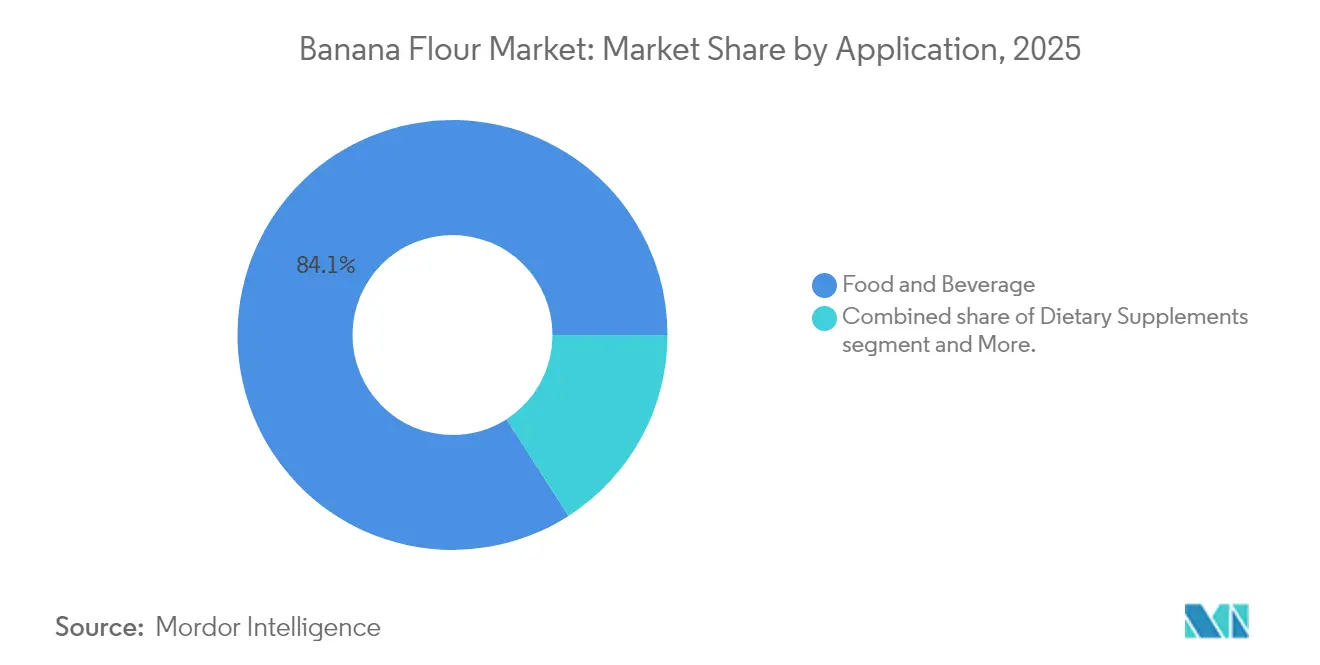

- By application, food and beverage commanded 84.08% of the banana flour market size in 2025, whereas dietary supplements are expanding at 7.21% CAGR through 2031.

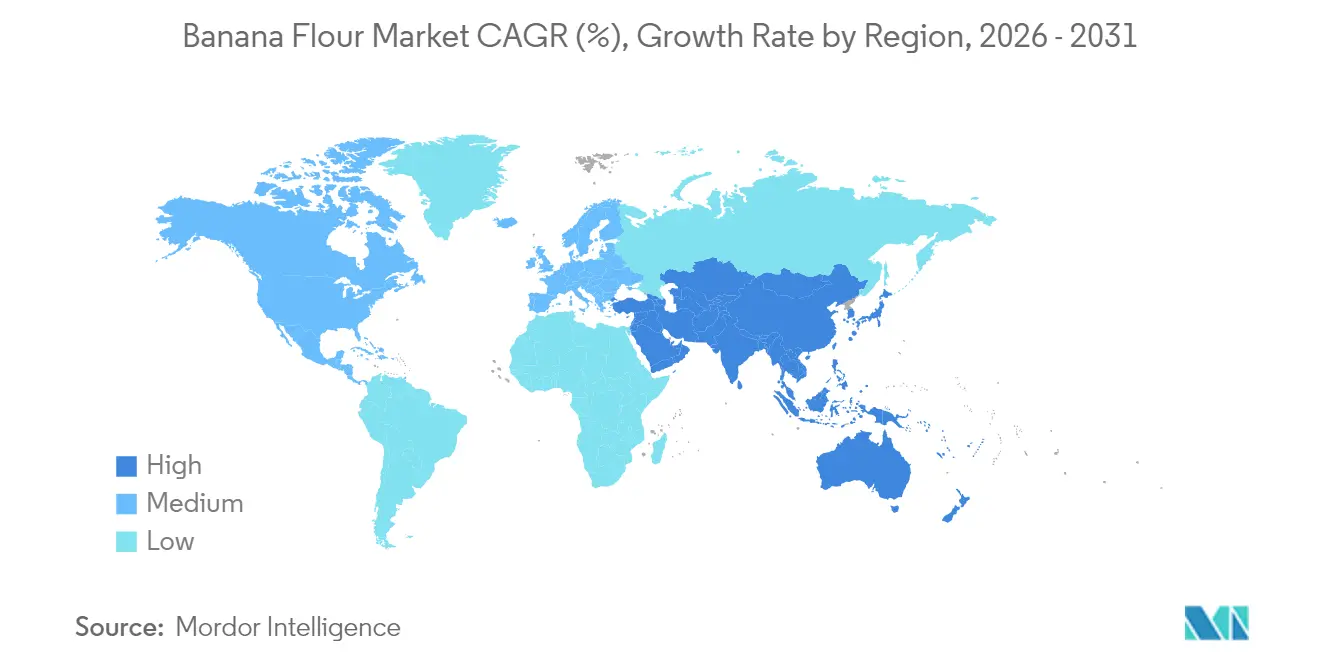

- By geography, Asia-Pacific led with 38.27% revenue share in 2025; Middle East and Africa is the fastest-growing region at a 6.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Banana Flour Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating demand for gluten-free products | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Surging vegan and plant-based diet trends | +0.9% | Global, led by North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Rising preference for clean-label and natural food ingredients | +0.8% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Expansion in functional food and beverage segment | +0.7% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Increasing adoption of banana flour in the food processing industry | +0.6% | Global, with early adoption in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Growing adoption of resistant starch-rich flours in baking | +0.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating demand for gluten-free products

The gluten-free food movement has transitioned from being solely focused on managing celiac disease to encompassing a broader emphasis on digestive health and wellness. This paradigm shift has driven a sustained and growing demand for innovative alternative flour solutions. Among these, banana flour has emerged as a premium option in bakery applications due to its naturally gluten-free composition and superior binding capabilities compared to traditional rice or corn-based alternatives. Additionally, banana flour offers significant functional benefits, such as enhanced moisture retention and improved structural integrity in gluten-free formulations. These attributes effectively address the longstanding technical challenges that have historically constrained the quality and appeal of gluten-free products. Furthermore, current dietary trends reveal that Australians consume only 3-9 grams of resistant starch daily, which is significantly below the recommended intake of 15-20 grams[1]Source: Commonwealth Scientific and Industrial Research Organisation (CSIRO), “Resistant Starch: Why You Need It,” csiro.au . This nutritional shortfall presents a substantial market opportunity for banana flour, as it can bridge this gap while aligning with clean-label requirements. For food manufacturers, incorporating banana flour into their product offerings not only enhances the nutritional value of gluten-free products but also strengthens their positioning in the health-conscious consumer segment.

Surging vegan and plant-based diet trends

The growing adoption of plant-based foods is significantly driving the demand for ingredients that combine high nutritional value with functional performance. Banana flour has emerged as a pivotal ingredient in the formulation of vegan products, offering a strategic advantage to manufacturers. Its inherent natural sweetness reduces the dependency on added sugars, while its prebiotic properties promote digestive health, addressing two critical consumer demands in the plant-based nutrition market. Reflecting the increasing institutional support for plant-based ingredients, the USDA has allocated a USD 500 million investment in 2024 to enhance local food sourcing for school meal programs[2]Source: United States Department of Agriculture (USDA), “Local Food for Schools Cooperative Agreement Program,” usda.gov. This initiative not only creates new market opportunities for banana flour suppliers but also strengthens connections between local farmers and producers. Furthermore, banana flour's versatility across both sweet and savory applications empowers manufacturers to develop comprehensive and diverse plant-based product portfolios using a single, multifunctional ingredient. The market's shift toward delivering complete plant-based nutritional profiles, rather than merely substituting animal-based products, positions banana flour as a key ingredient that simultaneously delivers multiple nutritional and functional benefits, aligning with evolving consumer preferences.

Rising preference for clean-label and natural food ingredients

As consumer preferences increasingly shift toward transparency and recognizable ingredients, food formulation strategies are undergoing significant transformation. Banana flour emerges as a key ingredient in this landscape due to its straightforward, single-ingredient composition, which eliminates the need for chemical processing or synthetic additives. Concurrently, the FDA's directive to phase out synthetic food dyes by 2026, including Blue No. 1 and 2, Green 3, Red 40, and Yellow No. 5 and 6, presents a substantial opportunity for natural alternatives that deliver both functional and aesthetic advantages. With its natural pale yellow color and mild flavor profile, banana flour is well-positioned to meet the demands of clean-label reformulations, where maintaining product appearance and taste is critical to consumer acceptance. Additionally, banana flour's multifunctionality, serving as both a flour substitute and a natural thickening agent, enables manufacturers to reduce the use of multiple additives. This simplification of ingredient lists aligns with the growing industry focus on reducing complexity while ensuring product quality, performance, and shelf stability. Such attributes make banana flour a strategic choice for manufacturers aiming to address evolving consumer demands and regulatory requirements effectively.

Expansion in functional food and beverage segment

As the functional food market continues to prioritize scientifically validated health benefits, there is a growing demand for ingredients with demonstrated physiological advantages. Banana flour, recognized for its high resistant starch content, is strategically positioned to capitalize on this trend due to its significant metabolic health benefits. Resistant starch undergoes fermentation in the colon, resulting in the production of short-chain fatty acids, particularly butyrate. Butyrate plays a critical role in enhancing gut barrier integrity and exhibits potent anti-inflammatory properties, making banana flour a valuable ingredient in addressing gut health. Additionally, its ability to positively influence insulin sensitivity and regulate appetite aligns with the increasing consumer focus on managing metabolic health, a key driver in the functional food market. Japan's regulatory framework for functional foods, which emphasizes rigorous scientific substantiation of health claims, serves as a benchmark for positioning banana flour in premium functional food applications. This regulatory model highlights the potential for banana flour to be marketed as a scientifically backed ingredient in high-value product categories. Furthermore, the beverage segment presents a significant growth opportunity. Banana flour's excellent solubility and neutral taste profile make it an ideal component for incorporation into protein shakes, smoothies, and other functional beverages, ensuring compatibility with sensory expectations while enhancing nutritional value.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price volatility of raw bananas limits the growth | -0.8% | Global, most acute in import-dependent regions | Short term (≤ 2 years) |

| Intensifying competition from established alternative flours | -0.6% | Global, particularly in mature markets | Medium term (2-4 years) |

| Higher production costs compared to traditional flours | -0.4% | Global | Medium term (2-4 years) |

| Limited consumer awareness in developing regions | -0.6% | Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price volatility of raw bananas limits the growth

Flour processors face significant margin pressures due to fluctuations in raw banana prices. These price variations are further intensified by climate change and plant diseases, such as Fusarium Tropical Race 4, which threaten production stability in key cultivation regions. According to the FAO, global banana production is increasingly exposed to risks from adverse weather conditions and escalating production costs. Major exporters, including Ecuador, the Philippines, and Costa Rica, are experiencing notable supply chain disruptions. Additionally, the production of banana flour relies on specific banana varieties and precise ripeness levels, limiting processors' ability to switch to lower-cost alternatives during price hikes. In 2023, global banana exports were highly concentrated, with Ecuador accounting for USD 3.79 billion, followed by the Philippines at USD 1.22 billion and Costa Rica at USD 1.19 billion[3]Source: World Bank, “Commodity Trade Statistics,” worldbank.org. This concentration creates supply chain vulnerabilities, directly impacting flour pricing stability. To address these challenges, processors are increasingly adopting vertical integration strategies and entering long-term supply contracts. However, these approaches require substantial capital investment, making them less viable for smaller market participants.

Intensifying competition from established alternative flours

The alternative flour market has reached a stage of maturation, attracting established industry players equipped with extensive distribution networks and significant marketing resources. This development has intensified competitive dynamics, particularly impacting the growth trajectory of banana flour's market share. Almond flour, coconut flour, and other nut-based alternatives continue to leverage their well-established supply chains and strong consumer recognition, providing them with a competitive edge. Meanwhile, emerging alternatives such as cricket flour and algae-based proteins are striving to capture a share of the same functional food applications, adding further complexity to the competitive landscape. Additionally, the regulatory environment for novel food approvals in critical markets, such as the European Union, presents significant challenges. Recent updates to regulatory guidelines now mandate more comprehensive safety and nutritional data, creating substantial barriers to entry. These regulatory hurdles tend to favor companies with advanced regulatory expertise and substantial resources, enabling them to navigate the complexities more effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Organic Premium Drives Innovation

In 2025, conventional banana flour commands a dominant 82.74% market share, establishing itself as a cost-effective substitute for wheat flour in mainstream culinary applications. Its widespread adoption owes much to efficient supply chains and lower production costs, making it a go-to choice for large-scale food manufacturers attuned to price sensitivity. Bakery and snack producers, on the hunt for gluten-free ingredients that won't break the bank, consistently turn to conventional banana flour. Its versatility across a myriad of products cements its status as a staple in the industry. This affordability resonates with both mass-market consumers and manufacturers, ensuring the flour's continued prominence. In essence, the conventional segment stands as the cornerstone of the banana flour market, striking an optimal balance between price and performance.

While the organic banana flour segment holds a smaller market share, it boasts the title of the fastest-growing segment, with projections indicating a compound annual growth rate (CAGR) of 5.52% through 2031. This growth trajectory underscores a strategic shift towards premium positioning, fueled by consumers' readiness to invest more in certified organic ingredients. The momentum is especially strong in developed markets, where the demand for clean labels dovetails with sustainability ideals, allowing brands to set premium prices. Yet, the organic segment grapples with supply chain challenges, primarily due to the scarcity of certified organic bananas. This limitation poses a hurdle but simultaneously presents a golden opportunity for suppliers who can secure dependable sources. With backing from initiatives like the USDA’s USD 300 million Organic Transition Initiative, which aims to assist farmers in transitioning to organic farming, there's potential for an expanded supply. This interplay of limited supply and surging demand not only accentuates competitive advantages but also paves the way for premiumization in the organic banana flour market throughout the forecast period.

By Source: Green Banana Dominance Reflects Processing Advantages

In 2025, green unripe bananas command a dominant 91.42% market share, thanks to their superior resistant starch content and processing stability, making them the top choice for flour production. Resistant starch not only enhances the nutritional profile of the flour but also improves its shelf life and functionality in various applications. On the other hand, the ripe banana segment, though smaller, is set to expand at a 5.55% CAGR from 2026 to 2031. Manufacturers are tapping into the fruit's natural sweetness and enhanced flavor for value-added applications, such as baked goods and snacks, which cater to evolving consumer preferences for natural and flavorful ingredients. This segmentation underscores the technical nuances of flour production, with green bananas offering higher yields and consistent nutritional quality, while ripe bananas provide opportunities for innovation in product development.

Green banana flour maintains market leadership due to its higher resistant starch content, with unripe bananas containing 50-60% resistant starch compared to less than 1% in fully ripe bananas. This nutritional advantage aligns with increasing consumer demand for digestive health and blood sugar management solutions, creating opportunities for premium product positioning. Ripe banana flour, however, caters to niche markets that value natural sweetness and flavor, particularly in baking mixes and specialty food products. The segment's growth is fueled by advancements in processing technologies that preserve nutritional integrity while enhancing the sensory appeal of ripe bananas. From a supply chain perspective, green bananas are preferred due to their longer shelf life and lower transportation risks, although ripe banana utilization presents opportunities to minimize waste in banana processing operations.

By Application: Dietary Supplements Drive Premium Growth

Food and beverage applications dominate with 84.08% market share in 2025, reflecting banana flour's primary role as a functional ingredient in mainstream food manufacturing. Although the dietary supplements segment currently represents a smaller portion of the market, it is projected to grow at a robust 7.21% CAGR through 2031, signaling the market's strategic shift toward nutraceutical applications. This diversification in usage reflects banana flour's transition from a commodity ingredient to a specialized product with a health-focused value proposition. Within the food and beverage sector, the bakery and confectionery subsegment leads, driven by banana flour's superior binding capabilities and moisture retention properties, particularly in gluten-free formulations.

The increasing consumer awareness regarding the health advantages of resistant starch, particularly its critical role in enhancing digestive health and supporting metabolic functions, is driving the robust growth of the dietary supplements segment. This segment leverages premium pricing strategies to position banana flour as a high-value functional health ingredient, distinguishing it from its traditional use as a conventional flour substitute. Such strategic positioning aligns seamlessly with the growing global demand for innovative and health-focused products, further solidifying its appeal in the competitive marketplace.

Geography Analysis

In 2025, the Asia-Pacific region captured a dominant 38.27% share of the banana flour market. This leadership is attributed to abundant raw material availability, a rapidly growing processed-food industry, and cost-effective labor. The region leverages India's extensive banana production and the advanced food manufacturing infrastructure in countries like Japan and South Korea. In China, snack manufacturers are increasingly utilizing banana flour to enhance fiber content in product labeling. Furthermore, Japan's "Foods with Function Claims" system supports high-resistant-starch positioning, enabling products to secure premium pricing.

The Middle East and Africa is forecasted to achieve the highest growth, with a CAGR of 6.66% through 2031. In South Africa, retail chains are expanding their gluten-free product portfolios with banana-flour-based baked goods, while wellness cafés in Saudi Arabia are incorporating banana-flour pancakes into their menus. Regional growth is further driven by government initiatives aimed at enhancing food security and reducing import dependency, creating opportunities for local processing of imported raw materials.

North America and Europe are anticipated to witness steady but moderate growth. These mature markets demonstrate high penetration of gluten-free products and a consumer base that prioritizes supply chain transparency. The FDA has approved several resistant-starch ingredients under its Generally Recognized as Safe (GRAS) pathway. However, brands are differentiating themselves through organic and fair-trade certifications. In Europe, the EFSA's updated novel-food regulations mandate more transparent but cost-intensive dossiers, which are expected to benefit compliant exporters over time. South America, with its proximity to raw-banana production clusters, is positioning itself as an emerging processing hub. Ecuadorian cooperatives are piloting solar-assisted drying technologies to reduce energy costs, while Brazilian start-ups are targeting fitness centers with banana-flour smoothie bases. Although challenges such as infrastructure gaps and currency volatility persist, government-backed loan programs indicate a positive outlook for growth in the region.

Competitive Landscape

The global banana flour market is moderately fragmented, with companies focusing on leveraging online platforms to improve the visibility and reachability of their products. Key players differentiate their offerings and compete on different factors, including product offerings, ingredients, packaging, price, and functionality, to gain a competitive advantage. Key players operating in the market are KADAC Pty Ltd, Sol Organica, S.A., Griffith Foods Worldwide Inc. (Terova), SV Agrofood, and Kanegrade Ltd. Most of them focus on effective marketing promotional strategies and the extension of their gluten-free offerings portfolio. Moreover, mergers and acquisitions targeting global expansion will remain a key strategy for several companies in the banana flour market.

Processors maintain a dominant position in national distribution channels, with private-label contracts undergoing annual renegotiations. Regional mills located in the Philippines, India, and Indonesia primarily supply local snack industry leaders, whereas Western specialty brands often depend on contract manufacturing to meet their production needs. Vertical integration has emerged as a critical strategy, enabling firms to secure plantations, thereby stabilizing raw material costs and ensuring compliance with pesticide control standards. Investments in advanced technologies are focused on optimizing production processes, such as low-temperature drying techniques to preserve resistant starch content and automated sieving systems to achieve consistent granulation quality.

Significant growth opportunities exist in niche segments, including infant-nutrition blends, pharmaceutical binders, and animal-nutrition pellets. Market disruptors are actively pursuing proprietary enzymatic treatment technologies designed to enhance amylose content beyond conventional levels. These advancements are being marketed as “super-resistant” banana flour, specifically targeting clinical nutrition brands seeking innovative and high-performance ingredients.

Banana Flour Industry Leaders

KADAC Pty Ltd

Sol Organica, S.A.

Kanegrade Ltd.

Griffith Foods Worldwide Inc. (Terova)

SV Agrofood

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Flowers Foods acquired Simple Mills, a prominent player in natural snacks and baking mixes. This strategic acquisition enhances Flowers Foods' position in the better-for-you food market and unlocks new distribution opportunities for alternative flour ingredients.

- February 2025: Dole, the multinational known for its fruits and vegetables, has partnered with Givaudan to distribute its green banana powder. This green banana powder, an innovative recycled ingredient, is crafted by Dole Specialty Ingredients (DSI), a branch of Dole Asia Holdings.

- September 2024: Symrise and Shan Foods launched a state-of-the-art production facility in Pakistan to strengthen local manufacturing capabilities and address the increasing demand in the savory food market.

- July 2024: International Agriculture Group (IAG), a start-up specializing in ingredient technology, has unveiled its latest offering, NuBana N200 Green Banana Flour, boasting a minimum of 65% RS2 resistant starch. The natural products industry is eyeing NuBana N200 Green Banana Flour for diverse applications, spanning powders, beverage mixes, cold-fill drinks, and energy bars.

Global Banana Flour Market Report Scope

Banana flour refers to a form of a powder that is made from green bananas and is known to be rich in dietary fibers, carbohydrates, cellulose, essential amino acid, hemicellulose, and starch. These are also used as gluten-free products in various baked food. Banana flour has come up as an alternative to regular wheat flour. Banana flour is made by milling dehydrated green bananas, resulting in high levels of resistant starch.

The global banana flour market is segmented by type (conventional and organic) and application (food & beverage, dietary supplements, and other applications). The food and beverage segment is further bifurcated into bakery & confectionery, soups & dressings, functional beverages, and other applications. The study also covers the global analysis of the major regions, including North America, Europe, Asia-Pacific, South America, and the Middle-East and Africa.

The market sizing and forecasts have been done for each segment based on value (in USD Million).

| Conventional |

| Organic |

| Green (Unripe) Banana |

| Ripe Banana |

| Food and Beverage | Bakery and Confectionery |

| Snacks and Cereals | |

| Beverages | |

| Sauces, Soups and Dressings | |

| Others | |

| Dietary Supplements | |

| Animal Feed and Pet Food | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Nature | Conventional | |

| Organic | ||

| By Source | Green (Unripe) Banana | |

| Ripe Banana | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Snacks and Cereals | ||

| Beverages | ||

| Sauces, Soups and Dressings | ||

| Others | ||

| Dietary Supplements | ||

| Animal Feed and Pet Food | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current market size of banana flour?

The banana flour market stands at USD 578.48 million in 2026 and is set to reach USD 721.72 million by 2031.

Which region leads global demand?

Asia-Pacific commands 38.27% of worldwide revenue, supported by abundant raw materials and established food-processing capacity.

Which application segment grows the fastest?

Dietary supplements register a 7.21% CAGR through 2031 as consumers look for resistant-starch products that support digestive and metabolic health.

Why is green-banana flour dominant?

Green bananas deliver higher resistant-starch levels and better processing stability, capturing 91.42% share of source-based sales in 2025.

Page last updated on: