Pulse Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

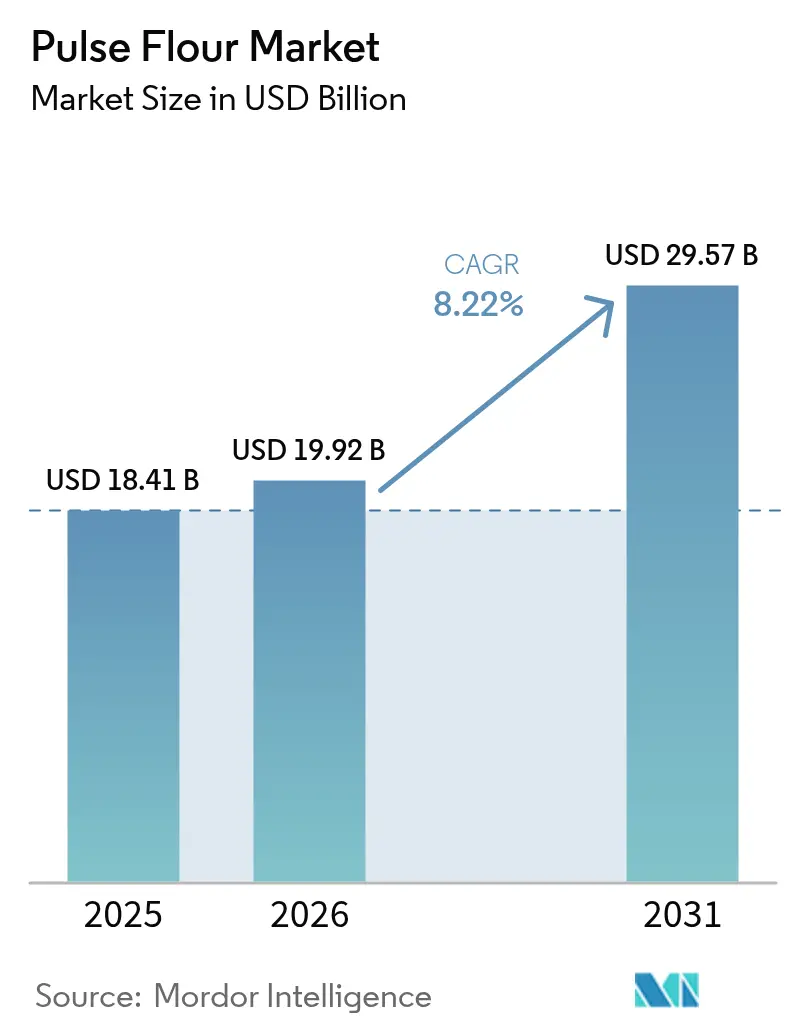

| Market Size (2026) | USD 19.92 Billion |

| Market Size (2031) | USD 29.57 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

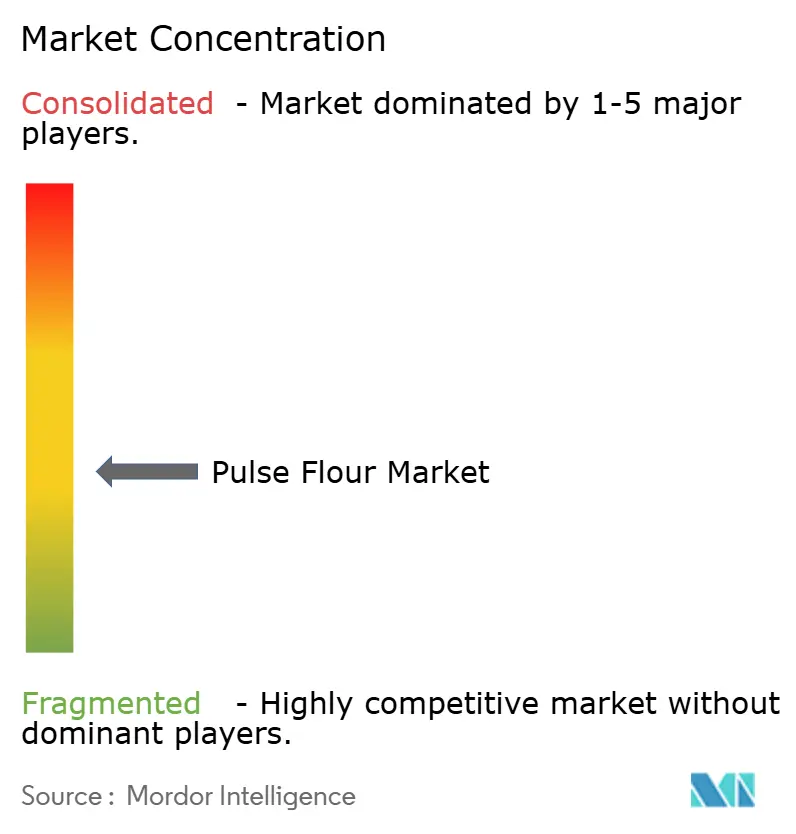

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pulse Flour Market Analysis by Mordor Intelligence

The pulse flour market size is expected to grow from USD 18.41 billion in 2025 to USD 19.92 billion in 2026 and is forecast to reach USD 29.57 billion by 2031 at 8.22% CAGR over 2026-2031. This robust expansion reflects the convergence of health-conscious consumer behavior, technological processing advancements, and regulatory support for plant-based protein alternatives across major food systems. Macro forces driving this growth trajectory include the escalating prevalence of celiac disease and gluten intolerance, which has intensified the demand for gluten-free alternatives beyond traditional wheat-based products. The clean-label movement has simultaneously elevated pulse flour as a minimally processed ingredient that delivers both nutritional density and functional versatility. Supply chain dynamics present both opportunities and constraints, with weather-dependent crop yields creating price volatility that processors must navigate through strategic sourcing and inventory management[1]Source: World Bank, "Risks and challenges in global agricultural markets", blogs.worldbank.org . The resilient expansion reflects consumers’ shift to plant-based proteins, new dry-fractionation and wet-milling methods that improve functionality, and supportive labeling regulations.

Key Report Takeaways

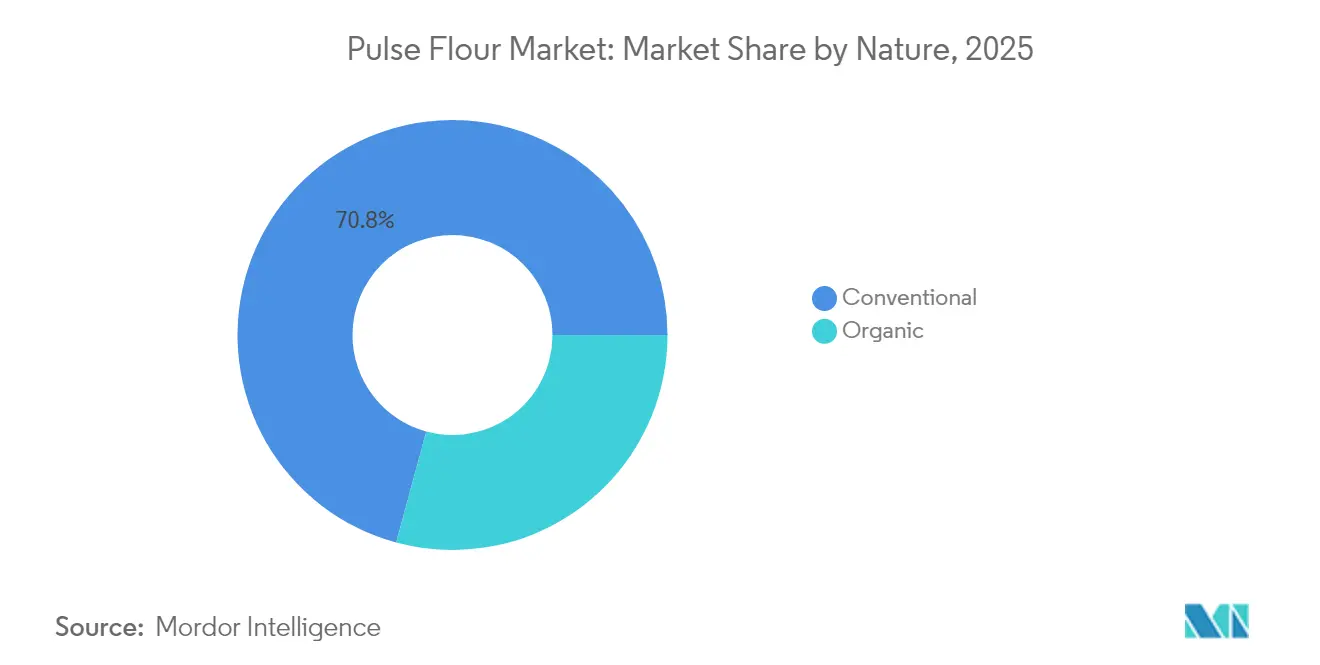

- By nature, conventional grades accounted for 70.78% of the pulse flour market size in 2025, while organic grades are expanding at a 10.39% CAGR.

- By pulse type, chickpea flour held 38.21% of the pulse flour market share in 2025; pea flour is forecast to grow the fastest at 9.12% CAGR through 2031.

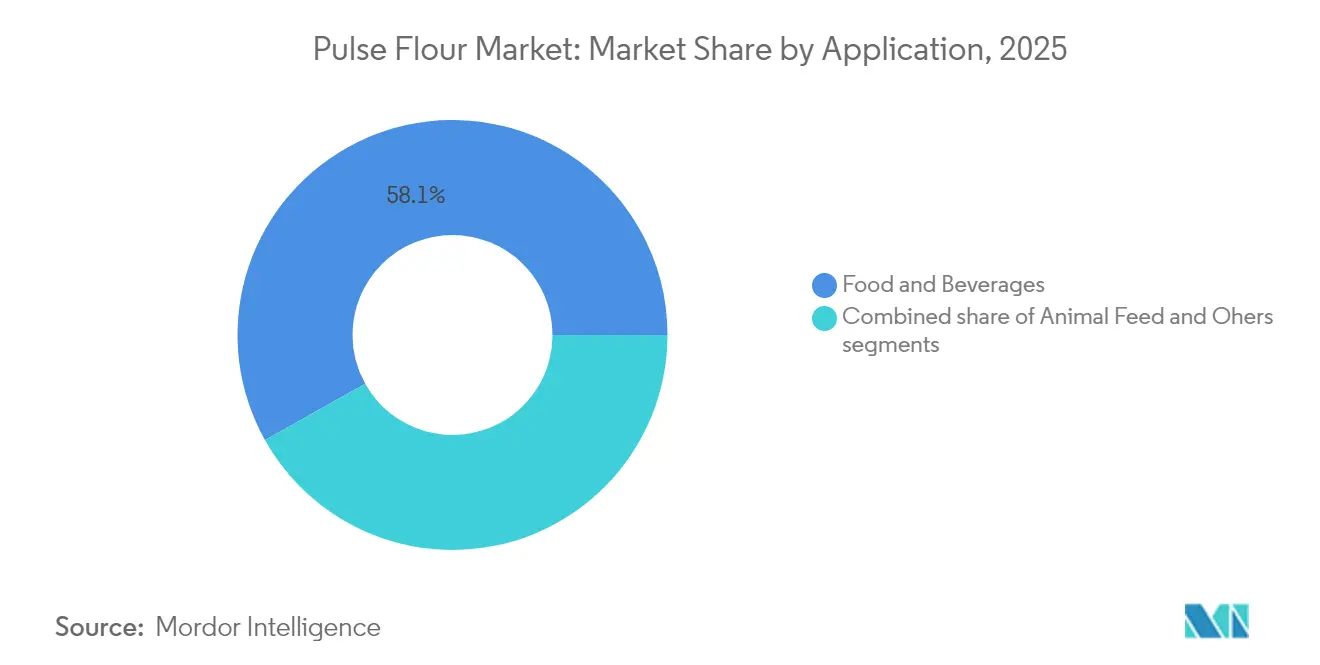

- By application, food and beverages commanded 58.12% of the pulse flour market size in 2025 and are advancing at a 10.18% CAGR to 2031.

- By geography, North America led with 32.54% revenue share in 2025; Asia-Pacific is projected to record the highest regional CAGR at 9.06% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pulse Flour Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened awareness and adoption of gluten-free and plant-based diets | +2.1% | Global; strongest in North America & Europe | Medium term (2-4 years) |

| Increasing incidence of celiac disease and gluten intolerance | +1.8% | Global; primarily developed markets | Long term (≥ 4 years) |

| Growing demand for clean-label, natural, and minimally processed ingredients | +1.5% | North America & Europe; growing in Asia-Pacific | Medium term (2-4 years) |

| Rising consumption of protein-rich and ready-to-eat (RTE) foods | +1.3% | Global; Asia-Pacific pacing volume growth | Short term (≤ 2 years) |

| Widening adoption of pulse flour in bakery and snack products | +1.0% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Expanding applications in food fortification and nutritional enhancement | +0.8% | Global, with focus on developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Awareness and Adoption of Gluten-Free and Plant-Based Diets

Consumer dietary preferences have fundamentally shifted toward plant-based proteins, with pulse flour emerging as a cornerstone ingredient in this transformation. The gluten-free market expansion has created unprecedented demand for functional alternatives that maintain textural integrity in baked goods and processed foods. Pulse flours deliver superior protein content ranging from 16-30% compared to traditional wheat flour, while providing essential amino acids that complement plant-based dietary patterns [2]Source: Cereals & Grains Association, "Challenges and Opportunities in Formulating with Pulse Ingredients", www.cerealsgrains.org .This nutritional advantage has prompted food manufacturers to reformulate existing products and develop new categories specifically targeting flexitarian and vegetarian consumers. The trend extends beyond individual health choices to encompass environmental sustainability concerns, as pulse cultivation requires significantly less water and generates lower carbon emissions than animal protein production. Regulatory bodies have responded by establishing clearer labeling standards for plant-based products, reducing market entry barriers for pulse flour applications.

Increasing Incidence of Celiac Disease and Gluten Intolerance

Medical diagnosis rates for celiac disease and non-celiac gluten sensitivity continue escalating across developed markets, creating a medically-driven demand base that transcends lifestyle preferences. Healthcare providers increasingly recommend pulse-based alternatives as nutritionally superior substitutes that address both gluten avoidance and protein adequacy requirements. The demographic expansion of diagnosed cases has shifted from predominantly adult populations to include pediatric patients, broadening the market scope to include specialized infant and child nutrition products. Food service establishments have responded by incorporating pulse flour into menu items to accommodate medical dietary restrictions while maintaining operational efficiency. This medical necessity creates price-inelastic demand that provides revenue stability for pulse flour processors during commodity price fluctuations. The trend has also stimulated research into pulse flour processing techniques that eliminate cross-contamination risks, leading to dedicated production facilities and certification programs.

Growing Demand for Clean-Label, Natural, and Minimally Processed Ingredients

Consumer scrutiny of ingredient lists has intensified demand for recognizable, minimally processed components that align with clean-label positioning strategies. Pulse flour satisfies this requirement as a single-ingredient product that requires minimal processing beyond milling and sieving operations. The absence of chemical additives, preservatives, and artificial enhancement agents positions pulse flour as a premium ingredient that commands higher margins while meeting consumer transparency expectations. Food manufacturers leverage pulse flour's clean-label credentials to differentiate products in competitive categories where ingredient transparency drives purchasing decisions. This trend has accelerated the adoption of pulse flour in organic and natural product lines, where conventional wheat flour alternatives may not meet certification requirements. The regulatory environment supports this shift through labeling requirements that favor simple, recognizable ingredient names over complex chemical designations.

Rising Consumption of Protein-Rich and Ready-to-Eat (RTE) Foods

Lifestyle changes have accelerated demand for convenient, protein-dense food options that support active lifestyles and busy schedules. Pulse flour enables manufacturers to enhance protein content in ready-to-eat products without compromising taste, texture, or shelf stability characteristics. The protein fortification capability of pulse flour allows food processors to target specific demographic segments, including athletes, elderly consumers, and health-conscious individuals seeking convenient nutrition solutions. Ready-to-eat applications benefit from pulse flour's water absorption properties and binding characteristics, which improve product cohesion and reduce manufacturing complexity. The trend has expanded beyond traditional snack categories to include breakfast cereals, nutrition bars, and meal replacement products where pulse flour serves both functional and nutritional roles. Market research indicates that protein-enhanced products command premium pricing, creating favorable economics for pulse flour incorporation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent supply of raw materials due to weather-dependent crop yields | -1.2% | Global, concentrated in major pulse-producing regions | Short term (≤ 2 years) |

| Price volatility of raw pulse crops | -0.9% | Global, especially affecting cost-sensitive processors | Short term (≤ 2 years) |

| Taste and texture differences affecting consumer acceptance | -0.7% | North America & Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Allergenic concerns associated with certain pulse varieties | -0.5% | Global; heightened scrutiny in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inconsistent Supply of Raw Materials Due to Weather-Dependent Crop Yields

Agricultural production volatility presents the most significant operational challenge for pulse flour processors, with weather patterns increasingly unpredictable due to climate change impacts. Drought conditions in major pulse-producing regions can reduce crop yields, creating supply shortages that force processors to source from alternative regions at premium prices. The concentration of pulse production in specific geographic areas amplifies this vulnerability, as adverse weather events can simultaneously impact multiple suppliers within the same region. Processing facilities must maintain larger inventory buffers to ensure consistent production schedules, increasing working capital requirements and storage costs. The supply inconsistency also affects product quality standardization, as different growing regions produce pulses with varying protein content, moisture levels, and functional characteristics. Long-term contracts with growers provide some stability but limit processors' ability to capitalize on favorable spot market conditions during abundant harvest periods.

Price Volatility of Raw Pulse Crops

Commodity price fluctuations create margin pressure for pulse flour processors who face challenges in passing cost increases to price-sensitive food manufacturers. Raw pulse prices can vary within a single crop year, driven by factors including weather conditions, export demand, and currency exchange rates affecting international trade. This volatility complicates long-term supply agreements with food manufacturers who require predictable ingredient costs for budgeting and pricing strategies [3]Source: Farm Credit Canada, " 2024 Grains, oilseeds and pulses sector outlook", www.fcc-fac.ca . Processors must implement sophisticated hedging strategies and flexible pricing mechanisms to maintain profitability while preserving customer relationships. The price sensitivity is particularly acute in animal feed applications, where pulse flour competes directly with lower-cost alternatives like soybean meal and corn gluten. Market participants have responded by developing value-added products with enhanced functionality that justify premium pricing relative to commodity pulse ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Organic Segment Drives Premium Growth

Conventional pulse flour maintains market leadership with 70.78% share in 2025, reflecting established supply chains and cost-competitive positioning across mainstream food applications. However, the organic segment demonstrates exceptional growth momentum at 10.39% CAGR through 2031, driven by premium positioning and sustainability-focused procurement strategies. The organic certification process requires dedicated processing facilities and supply chain segregation, creating barriers to entry that protect margins for established organic processors according to the World of Organic Agriculture. Conventional pulse flour benefits from economies of scale and established distribution networks, making it the preferred choice for large-volume applications in commercial bakery and food service sectors.

The organic segment's growth trajectory reflects consumer willingness to pay premium prices for certified organic ingredients, with price premiums ranging above conventional alternatives. Processing innovations have reduced the cost differential between organic and conventional pulse flour production, making organic options more accessible to mid-market food manufacturers. The regulatory environment supports organic growth through clear certification standards and labeling requirements that enable premium positioning. Organic pulse flour processors increasingly focus on direct relationships with certified organic farmers to ensure supply security and quality consistency, creating vertically integrated supply chains that enhance profitability.

By Pulse Type: Pea Flour Emerges as Growth Leader

Chickpea flour commands the largest market share at 38.21% in 2025, benefiting from established culinary traditions and superior functional properties in gluten-free applications. The dominance reflects chickpea flour's versatility across diverse food categories, from traditional flatbreads to modern protein bars and meat alternatives. Pea flour, however, exhibits the strongest growth momentum at 9.12% CAGR through 2031, driven by its neutral flavor profile and exceptional protein content that appeals to mainstream food manufacturers. Lentil flour occupies a specialized niche in premium applications, while bean flour serves primarily industrial and animal feed markets. The growing consumer preference for plant-based proteins and gluten-free alternatives continues to drive chickpea flour adoption in new product developments.

The competitive dynamics between pulse types reflect their distinct functional characteristics and application suitability. Pea flour's rapid adoption stems from its ability to enhance protein content without significantly altering taste profiles, making it ideal for products targeting mainstream consumers rather than specialty dietary segments. Processing innovations have improved pea flour's water absorption and binding properties, expanding its utility in bakery applications where it previously faced limitations. The supply chain for pea flour benefits from concentrated production in North America, providing processors with reliable sourcing and reduced transportation costs compared to other pulse types that require international procurement.

By Application: Food and Beverages Segment Maintains Dominance

The food and beverages segment captures 58.12% market share in 2025 and is projected to grow at 10.18% CAGR through 2031, reflecting pulse flour's expanding integration into mainstream food products. Within this segment, bakery products represent the largest sub-category, followed by extruded snacks and breakfast cereals that leverage pulse flour's protein enhancement capabilities. The segment's growth is driven by product innovation in gluten-free alternatives and protein-fortified foods that address evolving consumer preferences. Animal feed applications maintain steady demand but face margin pressure from alternative protein sources and commodity price volatility.

Recent innovations in food applications include pulse flour integration into pasta and noodles, where it enhances protein content while maintaining acceptable texture characteristics. The meat and meat analogs sub-segment represents a high-growth opportunity, as pulse flour provides both protein content and binding properties essential for plant-based meat alternatives. Processing technology advances have enabled pulse flour incorporation into previously challenging applications like dairy alternatives and beverages, expanding the addressable market beyond traditional baked goods. The regulatory environment supports food applications through established safety standards and nutritional labeling requirements that facilitate market entry.

Geography Analysis

North America commands 32.54% market share in 2025, leveraging established agricultural infrastructure and consumer familiarity with plant-based proteins to maintain regional leadership. The United States and Canada benefit from concentrated pulse production in the northern Great Plains, providing processors with reliable raw material access and reduced transportation costs that enhance competitiveness in global markets. Processing facilities in this region have invested heavily in advanced milling and fractionation technologies that produce high-purity protein concentrates and specialized flour grades for premium applications. The regulatory environment supports market growth through clear labeling standards and food safety protocols that facilitate product development and market entry.

Asia-Pacific emerges as the fastest-growing region with 9.06% CAGR through 2031, driven by expanding food processing industries and increasing protein consumption in developing markets. India's food processing sector is projected to rise, creating substantial demand for protein-rich ingredients like pulse flour in packaged foods and ready-to-eat products. China's growing middle class and urbanization trends drive demand for convenient, protein-enhanced foods that incorporate pulse flour as a functional ingredient. The region benefits from government initiatives promoting food processing infrastructure development and nutritional enhancement programs that support pulse flour adoption.

Europe represents a mature market characterized by premium positioning and organic product focus, with steady growth driven by sustainability concerns and clean-label preferences. The European Union's agricultural policies aim to boost local pulse production and reduce import dependence, potentially affecting supply chain dynamics and pricing structures for pulse flour processors. Germany, France, and the United Kingdom lead regional consumption, with established distribution networks and consumer acceptance of plant-based proteins supporting market stability. The region's stringent food safety and labeling requirements create barriers to entry but also protect established players from low-cost competition. Recent acquisitions like DSM's purchase of Vestkorn Milling for EUR 65 million (USD 70 million) in November 2021 demonstrate continued consolidation and investment in pulse-based protein capabilities

Note: Segment shares of all Individual segments will be available upon report purchase

Regulatory Landscape

Pulse flour regulation is shaped by food safety, contaminant-control, and ingredient-authorization frameworks that increasingly treat milled pulse ingredients with the same specificity as whole pulses. In India, the Food Safety and Standards Authority of India (FSSAI) notified amendments to the Food Safety and Standards Regulations on June 3, 2026, explicitly expanding heavy-metal limits to cover Pulse and Pulse flours and reinforcing contaminant monitoring across processing lots.

In the United States, FDA oversight follows FSMA preventive controls and GRAS pathways, with post-market action such as the May 2024 FDA determination that tara flour did not meet the GRAS standard and was an unapproved food additive. In the European Union, Regulation (EU) 2015/2283 (Novel Foods) governs market access, and EFSA activity continues to define conditions with the January 2024 safety assessment for bambara groundnut flour as a traditional food from a third country.

Competitive Landscape

The pulse flour market, marked by moderate concentration, includes established agricultural processors and specialized ingredient companies. This market structure presents opportunities for consolidation and scale advantages through strategic acquisitions and capacity expansions. Prominent players in the market include Tate & Lyle PLC, Ingredion Inc., Xinghua Lianfu Food Co., Ltd, Buhler Holding AG, and Avena Foods Limited.

Leading companies adopt vertical integration strategies that span raw material sourcing, processing, and distribution. These strategies enable them to capture value across the supply chain while maintaining consistent quality and ensuring supply security. The adoption of advanced technologies further strengthens competitive positioning. Techniques such as dry fractionation and wet milling facilitate the production of high-purity protein concentrates and specialized flour grades, which often command premium pricing.

Processing innovations remain a key focus area, with companies working to enhance functional properties like water absorption, binding capacity, and flavor neutrality. These advancements support the expansion of pulse flour applications in mainstream food products. Patent activity in the market centers on processing methods and product formulations, with recent filings addressing challenges such as debittering in chickpea protein concentrate production. Additionally, strategic partnerships between processors and food manufacturers foster preferred supplier relationships, providing revenue stability and enabling market access for new product development initiatives.

Pulse Flour Industry Leaders

-

Tate & Lyle PLC

-

Xinghua Lianfu Food Co.,Ltd

-

Ingredion Inc.

-

Buhler Holding AG

-

Avena Foods Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product development targeting texture, binding, neutral taste, and gluten-free functionality remains a key whitespace for pulse flour suppliers, particularly in high-volume bakery, batters and breadings, breakfast cereals, and snack systems. Evidence of this shift includes ADM launching a pea flour product in May 2026 for applications such as batters, breadings, baked goods, and cereals across North America and Europe, signaling continued commercialization of application-specific pulse flours rather than generic commodity milling.

Localization of pulse processing and tighter identity-preserved supply chains create additional opportunity, especially where customers demand traceability and consistent functional performance. BENEO inaugurated its first pulse-processing plant in Germany in April 2025, adding regional capacity aligned with European clean-label and protein-enrichment demand, while USDA ERS reported US dry pulse availability rising 7% in 2024 to 11 pounds per person (April 2025 release), supporting broader use of pea and other pulse flours in North American reformulation programs.

Recent Industry Developments

- July 2026: Ingredion showcased next-generation pulse-derived ingredient solutions at IFT FIRST 2026, highlighting application-ready platforms for bakery and snack applications.

- June 2026: Buhler Group announced the acquisition of Endeco and its subsidiary Endeco Protein and Food, strengthening its plant-based processing technology capabilities for pulse-based proteins and related flour lines.

- April 2025: BENEO inaugurated its first pulse-processing plant in Germany, adding regional capacity aligned with European clean-label and protein-enrichment demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the pulse flour market covers flour produced by milling pulses (such as chickpeas, peas, lentils, and beans) and sold for food, beverage, and feed-related uses across major regions, measured in value terms (USD).

Scope exclusions: whole pulses, pulse protein isolates or concentrates, and ready-to-eat finished foods made with pulse flour are not counted as market revenue.

Segmentation Overview

-

By Nature

- Organic

- Conventional

-

By Pulse Type

- Chickpea

- Peas

- Lentil

- Bean

- Others

-

By Application

-

Food and Beverages

- Bakery Products

- Extruded Snacks

- Breakfast Cereals

- Pasta and Noodles

- Meat and Meat Analogs

- Others

- Animal Feed

- Others

-

Food and Beverages

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

To set the market frame, we first pulled established public data series that describe pulse supply, processing, and downstream demand signals. Common inputs came from sources such as FAOSTAT for pulse production trends, UN Comtrade for trade flows of pulses and flour-type products where classifications allow, and USDA and similar agriculture agencies for crop outlook and price direction.

Next, the desk work was used to translate those signals into usable assumptions for the model, including regional pulse availability, typical conversion from pulses to flour, and key end-use patterns in bakery, snacks, and gluten-free foods. We also reviewed company filings and investor presentations for capacity additions and product mix, along with association websites and peer-reviewed food science journals on pulse flour adoption, plus reputable press for new launches. When needed, subscription datasets were used for company financials and for patent tracking to confirm activity and timing. The desk sources listed here are illustrative only, and other public references were used to cross-check and clarify inputs during the study.

Primary Interviews and Surveys

Primary work was used to test what the desk signals could not fully explain, especially pricing logic, channel mix, and how much pulse flour is being substituted for wheat flour in different recipes. We spoke with participants across milling, ingredient supply, food manufacturing, and distribution. We then triangulated feedback across APAC, EMEA, and the Americas so regional differences in availability and adoption were reflected in the final sizing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | APAC: 45% |

| Mid tier: 54% | Functional/Unit leaders: 33% | EMEA: 35% |

| Smaller Players: 19% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

The main sizing logic starts from the demand pool, then builds the value using a top-down approach based on pulse processing and food consumption signals, converted into pulse flour usage with realistic penetration and conversion assumptions. To keep totals grounded, the results were checked with selective bottom-up approximations, such as sampling supplier revenues where disclosed, using channel checks on typical pack sizes, and multiplying observed price ranges by estimated volumes for key applications.

A few inputs mattered most: pulse crop output and trade availability by region, milling and fractionation capacity announcements, the share of gluten-free and high-protein product launches that use pulse flour, substitution rates in bakery and extruded snacks, and regional price movements for pulses and flour. Where interview feedback showed inconsistent pricing, we used a simple price ladder by application (for example, retail packs versus bulk industrial supply) and then normalized to the same currency timing.

For forecasting, we relied on scenario analysis supported by expert consensus, since adoption often moves in steps when new formulations scale and when raw pulse prices shift. Growth rates were adjusted by region based on expected capacity additions, food labeling and nutrition trends, and observed import dependence. Data gaps in any one country were handled by mapping to similar markets using per-capita pulse consumption and trade reliance, then reviewing against regional totals.

Data Validation & Update Cycle

Model outputs were validated through multiple checks so single-source bias did not drive results. We compared implied volumes and values against independent signals like pulse production, trade movements, and visible pricing in key channels, then flagged outliers for a second analyst review.

When a variance was material, assumptions were revisited and selected experts were re-contacted to confirm whether the change was real, timing-related, or caused by a scope mismatch. Reports are refreshed annually, and interim updates are made when major events occur, such as large capacity starts, sharp raw material price swings, or policy changes affecting trade. Before delivery, a final pass is completed so the published view reflects the latest available public data and confirmed market feedback.

Mordor Intelligence's Pulse Flour Market Size Compared Against Other Published Estimates

Published pulse flour market values can look far apart because the scope is not always consistent, and the underlying pricing logic can be handled in different ways. Differences usually come from what is counted as pulse flour revenue, which end uses are included, and whether the estimate is anchored to realistic volume signals or mainly to broad food spending.

Pulse protein isolates and concentrates sit outside Mordor Intelligence's scope, which is one reason the 2025 value can be lower than estimates that blend multiple pulse ingredients into one number. In addition, some sources rely heavily on retail-priced equivalents across all channels, which can inflate totals if industrial bulk pricing and feed applications are not treated separately or validated with capacity and trade checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.41 B (2025) | |

| Global Consultancy A | USD 49.55 B (2024) | Often reflects a broader ingredient or flour basket and can lean on retail price equivalents across channels, which raises implied value if bulk industrial pricing and conversion factors are not normalized. |

| Industry Publisher B | USD 24.70 B (2025) | May apply a more aggressive adoption curve and wider inclusion of adjacent pulse-based ingredients, and it typically provides fewer explicit checks against capacity additions and trade-based availability. |

The spread in the table is mainly explained by what each estimate includes and how prices are applied across channels. By keeping the scope tied to milled pulse flour revenue and then validating the totals with realistic demand indicators and pricing ladders, the sizing steps stay easier to follow and repeat when the market is updated.

Key Questions Answered in the Report

What is the current value of the pulse flour market?

The pulse flour market is valued at USD 19.92 billion in 2026.

How fast is the pulse flour market expected to grow?

It is projected to expand at an 8.22% compound annual growth rate, reaching USD 29.57 billion by 2031.

Which pulse type dominates the market?

Chickpea flour leads with 38.21% of 2025 revenue.

Which region shows the strongest growth momentum?

•Asia-Pacific is forecast to record the highest regional CAGR at 9.06% through 2031, fueled by rising protein demand in India and China.

Page last updated on: