Rice Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rice Flour Market Analysis by Mordor Intelligence

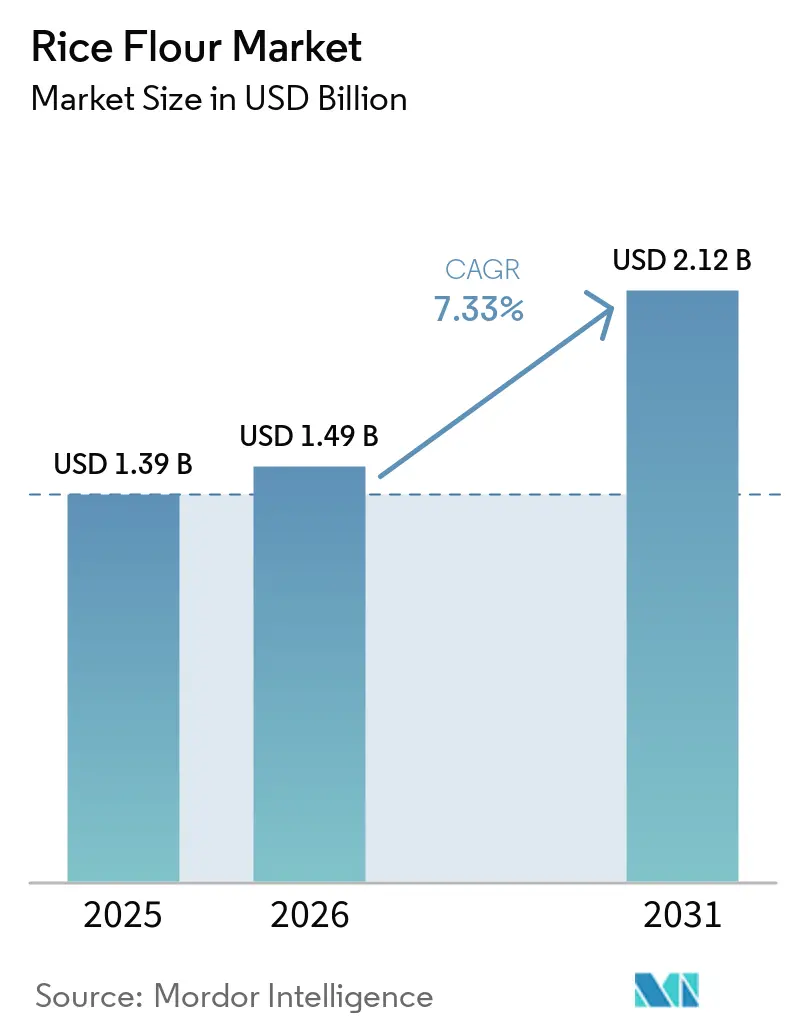

The rice flour market size is expected to grow from USD 1.39 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 2.12 billion by 2031 at 7.33% CAGR over 2026-2031. The global rice flour market is experiencing significant growth, driven by increasing consumer demand for gluten-free staples, clean-label formulations, and organic-certified products. Regulatory frameworks focused on allergen labeling and food safety are prompting reformulations, while government initiatives promoting organic agriculture are enhancing supply availability. Product innovations are expanding the market's scope, with soluble, ultra-fine, and fortified blends gaining traction in bakery, beverage, and convenience food applications. Key market players are investing in capacity expansions, proprietary milling technologies, and direct-to-consumer strategies, while smaller brands are leveraging e-commerce platforms to target niche segments. This convergence of health-conscious demand, regulatory support, and technological advancements positions rice flour as a dynamic market segment that integrates everyday consumption with premium, functional, and sustainable solutions.

Key Report Takeaways

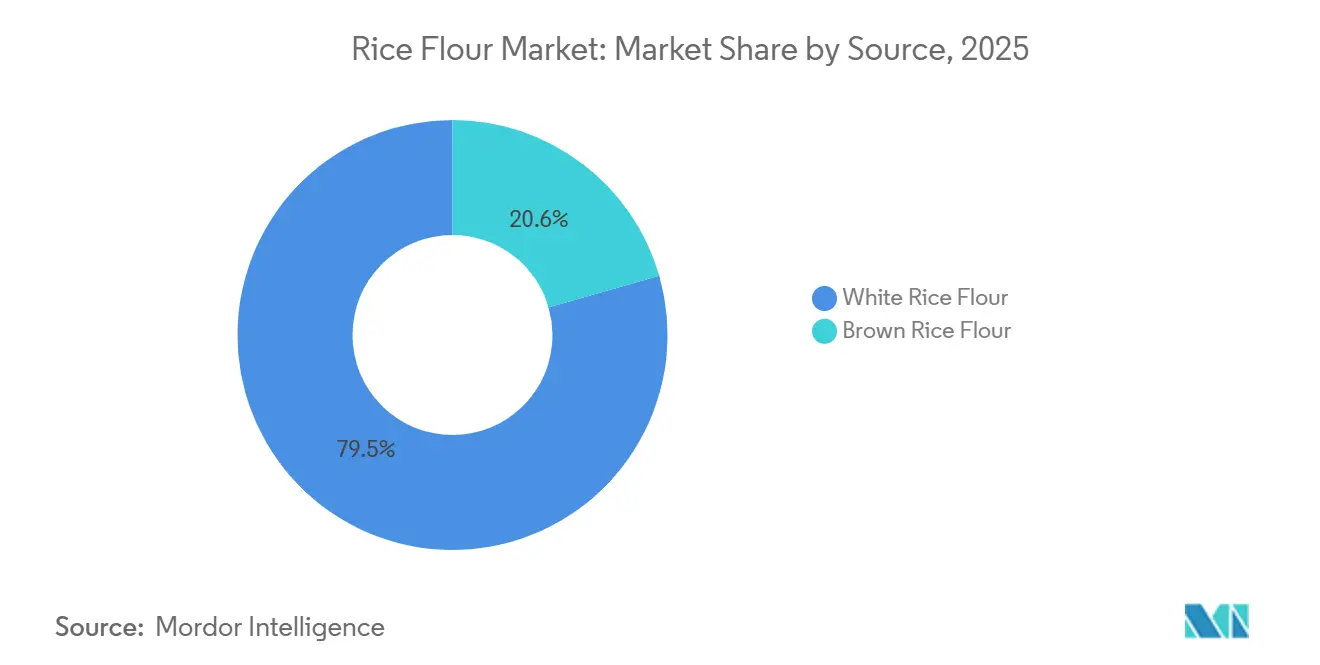

- By source, white rice flour accounted for a 79.45% share of the rice flour market in 2025, whereas brown rice flour is projected to expand at a 7.98% CAGR through 2031.

- By nature, conventional variants dominated with 86.29% of the rice flour market share in 2025; organic products are rising fastest at 8.54% CAGR through 2031.

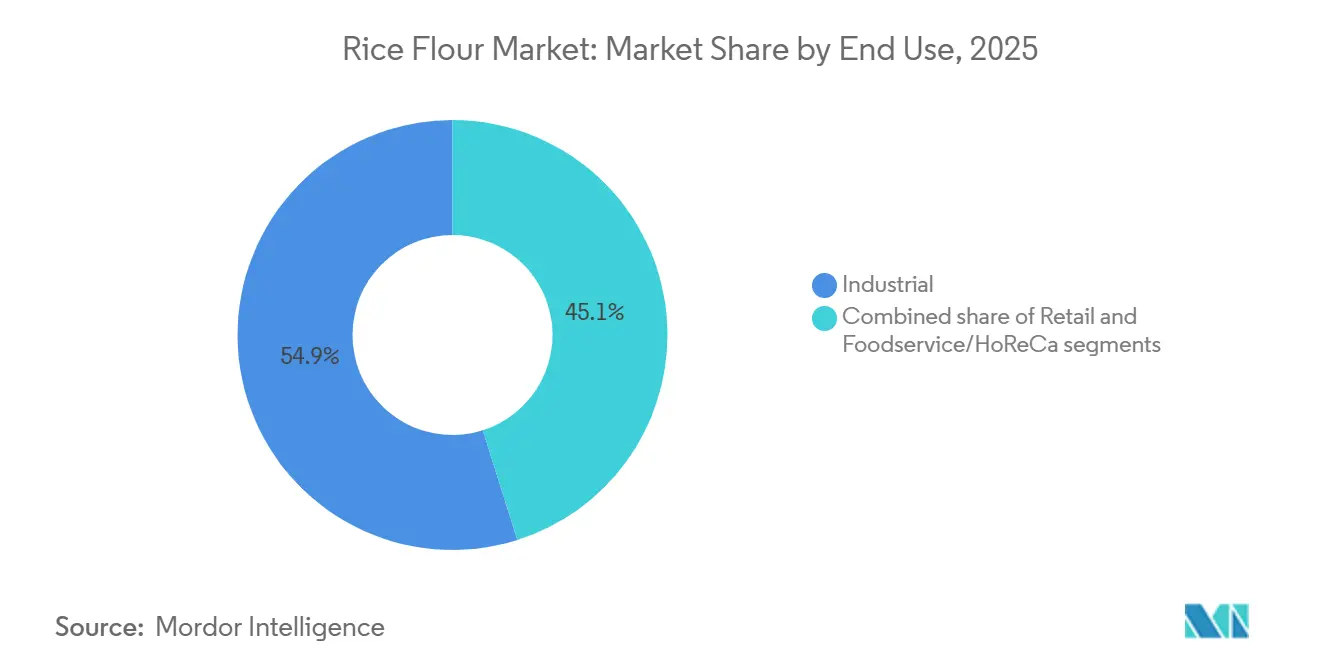

- By end use, industrial applications held 54.88% of the 2025 demand within the rice flour market, while the retail segment leads growth at 8.23% CAGR during 2026-2031.

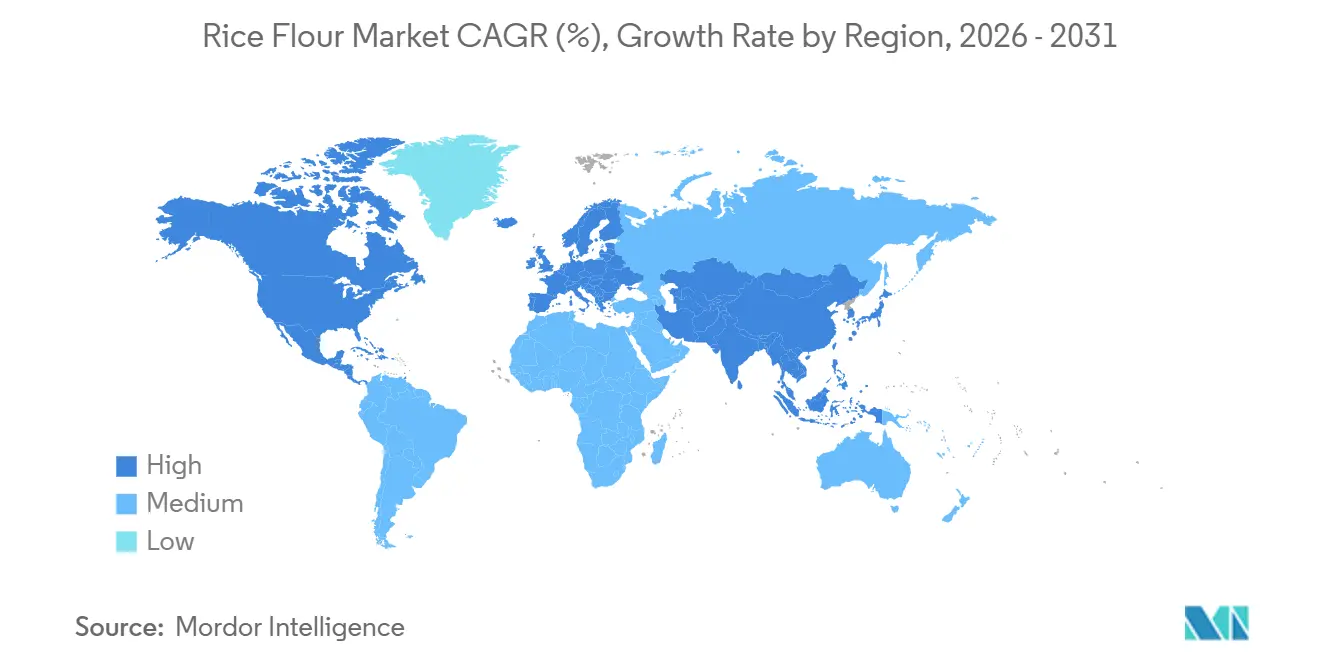

- By geography, Asia-Pacific commanded 56.21% of the global rice flour market share in 2025 and remains the fastest-growing region at 7.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rice Flour Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of gluten intolerance and celiac disease | +1.2% | Global, with elevated seroprevalence in Asia (1.8%) and Europe (1.3%) | Medium term (2-4 years) |

| Growth of clean-label and organic rice flour | +1.5% | North America & European Union, spillover to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Surge in popularity of instant and processed food products | +1.0% | Asia-Pacific core, Latin America, Middle East | Short term (≤ 2 years) |

| Growing popularity of asian cuisine worldwide | +0.8% | North America, Europe, Middle East | Medium term (2-4 years) |

| Government support for sustainable agriculture and organic farming | +1.3% | United States, European Union, select Asia-Pacific markets (Japan, South Korea) | Long term (≥ 4 years) |

| Emergence of ultra-fine and specialty rice flours | +1.0% | Global, early adoption in Japan, North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of gluten intolerance and celiac disease

The global rice flour market is experiencing significant growth, driven by the increasing prevalence of gluten intolerance and celiac disease, alongside a strong consumer shift toward clean-label and organic products. According to Beyond Celiac, an estimated 1 in 133 Americans, or about 1% of the population, has celiac disease[1]Source: Beyond Celiac, "Celiac Disease: Facts and Figures," beyondceliac.org. With a substantial portion of celiac cases remaining undiagnosed, the actual demand for gluten-free staples like rice flour exceeds reported figures. Rice flour's hypoallergenic properties and neutral flavor position it as a preferred alternative. This demand has spurred product innovation, particularly in pediatric formulations and family-oriented baking mixes. Additionally, clean-label trends are prompting manufacturers to replace synthetic additives with rice flour-based solutions that offer both functionality and transparency. Government initiatives supporting organic certification and supply chain development are further accelerating the adoption of certified rice flour. These health-driven demands, regulatory support, and evolving consumer preferences are collectively driving market growth, establishing rice flour as a versatile ingredient aligned with wellness, authenticity, and sustainability.

Growth of clean-label and organic rice flour

The increasing demand for clean-label and organic rice flour is being driven by consumers' preference for recognizable and minimally processed ingredients, aligning with transparency and wellness trends. According to the Organic Trade Association (OTA), United States sales of certified organic products grew by 5.2% in 2024, exceeding the overall marketplace growth of 2.5% during the same period[3]Source: Organic Trade Association (OTA), "Organic Trade Association reports sales of organic products at $71.6 billion with growth rate more than doubling overall marketplace," ota.com. This growth indicates a fundamental shift in consumer preferences, particularly among younger consumers who emphasize ethical and sustainable food choices. Regulatory and policy frameworks are providing structured support for organic rice flour production. The European Union has set a target of 25% organic farming by 2030, creating incentives for sustainable agricultural practices and organic rice cultivation[4]Source: European Commission, "Action plan for organic production in the EU," europa.eu. Consumers are actively avoiding products containing synthetic additives. In response, manufacturers are adopting rice flour-based solutions that provide functionality while maintaining a simple and familiar label appearance. Soluble and specialty rice flours are gaining prominence as natural alternatives to modified starches and emulsifiers, fostering innovation in the bakery, beverage, and convenience food markets. Simultaneously, government programs subsidizing organic certifications and expanding supply chains are reducing barriers for producers, ensuring broader availability of certified organic rice flour in mainstream markets. These factors collectively position rice flour as a reliable and versatile ingredient, meeting the demands for health, authenticity, and sustainability.

Surge in popularity of instant and processed food products

Urbanization, increasing disposable incomes, and time-constrained lifestyles are driving the demand for convenient meal solutions, thereby fueling the growth of the global rice flour market. Rice flour has established itself as a key functional ingredient in products such as instant noodles, extruded snacks, rice cakes, and pre-mixed baking formulations, owing to its rapid gelatinization properties, neutral flavor, and compatibility with modern processing technologies. Continuous research and development are further strengthening its market position by introducing innovations that enhance texture, improve reconstitution speed, and increase nutritional value, including low-glycemic-index formats and resistant starch enrichment. These advancements solidify rice flour's role as a clean-label, versatile alternative to wheat-based and synthetic binders, aligning with consumer demand for healthier, reliable, and convenient instant food products.

Growing popularity of asian cuisine worldwide

The increasing global demand for Asian cuisine is driving significant growth in the rice flour market. Traditional products such as mochi, rice noodles, rice cakes, tempura batters, and gluten-free flatbreads are experiencing widespread adoption beyond their regions of origin. In key markets such as North America, Europe, and the Middle East, consumers are increasingly seeking authentic flavors and textures, which is fueling the integration of rice flour into both foodservice applications and ready-to-cook product offerings. Exporting nations, particularly Thailand, are capitalizing on this trend by implementing targeted trade initiatives and promotional campaigns to enhance the visibility and appeal of rice-based products in premium and high-value markets. These efforts are further supported by the growing presence of Asian restaurants, meal kits, and convenience-focused food formats, which are driving sustained demand for rice flour as a core ingredient. Moreover, the global diffusion of Asian culinary traditions is positioning rice flour as a versatile and culturally significant ingredient that meets modern consumer preferences. Its ability to bridge authenticity with the rising demand for diverse, health-oriented, and gluten-free food options makes it a strategic component in the evolving food and beverage industry. This trend underscores the importance of rice flour in catering to shifting consumer behaviors and expanding opportunities in the global market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative gluten-free flours | -0.6% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Stricter arsenic residue limits in EU infant cereals | -0.8% | Europe, spillover to export-oriented Asia-Pacific producers | Short term (≤ 2 years) |

| Price volatility of rice as a raw material | -0.5% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Regulatory and labeling challenges associated with GMO | -0.3% | United States, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from alternative gluten-free flours

The growth of the rice flour market is being constrained by increasing competition from alternative gluten-free flours. Options such as cassava, almond, coconut, chickpea, and soy flours are gaining market share in both retail and foodservice channels, driven by consumer demand for dietary solutions aligned with trends like paleo, keto, and high-protein diets. These alternatives often provide superior protein content, enhanced fat profiles, and improved technical performance in applications such as encapsulation and emulsification. In comparison, rice flour's high starch content and lower protein levels limit its functional versatility. As specialty flours continue to expand, rice flour suppliers are under pressure to differentiate through advancements in processing, product fortification, and cost optimization. These strategies are essential to maintain competitiveness in a market where consumers increasingly prioritize both authenticity and added nutritional benefits in gluten-free products.

Stricter arsenic residue limits in European Union (EU) infant cereals

Stricter arsenic residue limits imposed by the European Union are creating significant challenges for the rice flour market, particularly in infant and young-child food applications. The new regulations, which mandate extremely low arsenic thresholds, require producers to implement rigorous testing protocols, source low-arsenic rice varieties, or reformulate products to reduce rice flour content. These compliance requirements are driving up production costs and complicating supply chain operations. Additionally, they are enabling alternative cereals such as oat, millet, and quinoa to capture market share in these sensitive categories. To remain competitive in the premium infant food segment, rice flour suppliers must invest in advanced quality assurance measures and certification strategies to navigate the increasingly stringent regulatory environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: White Rice Dominance Faces Brown Rice Innovation

White rice flour maintains a dominant market share of 79.45% in 2025. Its established use in gluten-free baking, noodles, batters, and convenience foods underscores its market leadership. The neutral flavor, fine texture, and high starch content of white rice flour make it highly compatible with industrial-scale processing techniques such as extrusion and spray-drying, ensuring consistent quality and operational efficiency in instant food production. Additionally, advancements like enzyme-treated soluble rice flour are enhancing its value proposition, enabling manufacturers to replace synthetic bulking agents while maintaining clean-label standards. Supported by superior milling yields and extended shelf life, white rice flour remains the preferred choice across mainstream applications.

Conversely, brown rice flour is emerging as the fastest-growing segment, with a projected CAGR of 7.98% from 2026 to 2031. This growth is driven by increasing consumer demand for whole-grain, fiber-rich alternatives that align with health and wellness trends. Retaining the bran and germ, brown rice flour offers a higher nutritional profile, including fiber, vitamins, and antioxidants, while delivering a lower glycemic response compared to white rice flour. Despite challenges such as shorter shelf life and coarser texture, advancements in particle-size reduction, fermentation, and blending are improving its functionality in bakery and snack applications. These innovations are narrowing the performance gap with white rice flour, positioning brown rice flour as a premium option for health-conscious consumers and expanding its role in the global gluten-free product market.

By Nature: Conventional Scale Meets Organic Acceleration

Conventional rice flour accounted for 86.29% of the market share in 2025 and continues to dominate the market. Its leadership is driven by established supply chains, cost efficiency, and widespread adoption across industrial, foodservice, and retail channels. The product's scalability and affordability make it the preferred choice for high-volume applications, such as noodle manufacturing, institutional foodservice, and export markets. Supported by robust infrastructure and consistent yields, conventional rice flour ensures reliability for manufacturers and distributors focused on operational efficiency and price competitiveness. This entrenched position reinforces its role as the foundation of the market, sustaining its leadership in mainstream applications.

In contrast, organic rice flour is the fastest-growing category, projected to achieve a CAGR of 8.54% from 2026 to 2031. Growth is fueled by increasing consumer demand for clean-label products, government subsidies, and retailer initiatives to expand organic product portfolios. While organic rice flour faces higher production costs and certification challenges, it commands a premium price due to its perceived health benefits, environmental sustainability, and traceability. Certifications such as United States Department of Agriculture Organic, European Union Organic, halal, and kosher enhance its credibility in the market. Furthermore, advancements in processing technologies and supply chain expansion are improving product availability. Despite challenges such as supply constraints and stringent testing requirements, organic rice flour is establishing a strong foothold in premium retail, specialty bakery, and health-focused packaged goods, positioning itself as a key growth driver within the segment.

By End Use: Industrial Foundation Enables Retail Innovation

In 2025, industrial end-use dominated the market with a 54.88% share. This stronghold was bolstered by rice flour's functional properties, cost efficiency, and seamless integration into high-volume production lines. Key players, including noodle manufacturers, bakery suppliers, snack producers, and processed food formulators, anchor this segment. Rice flour's neutral flavor and gluten-free nature position it as a versatile ingredient across various applications. Established procurement relationships and economies of scale solidify its market dominance, ensuring rice flour remains a staple in industrial food manufacturing and export-oriented supply chains.

Retail channels, however, are set to outpace others, boasting a projected CAGR of 8.23% from 2026 to 2031. This surge is fueled by the rise of direct-to-consumer gluten-free baking mixes, instant rice-flour products, and certified allergen-free formulations. Growing consumer interest in home baking, coupled with dietary restrictions and a preference for clean-label products, is driving demand. E-commerce platforms and specialty health food stores are enhancing accessibility. Moreover, innovations like rice-flour-based bread mimicking wheat textures and allergen-free mixes are spurring adoption. As more consumers whip up gluten-free meals at home and explore diverse cuisines, retail channels are emerging as the market's growth engine, balancing industrial scale with personalized, health-centric offerings.

Geography Analysis

Asia-Pacific, holding 56.21% of the market share in 2025. This leadership is bolstered by Thailand's robust export infrastructure, India's vast production capabilities, and a surge in domestic consumption in nations like China, Japan, and South Korea. The region's established supply chains, coupled with government initiatives, not only bolster rice exports but also pivot towards health-centric and specialty products. Furthermore, leading ingredient processors are expanding their capacities, cementing Asia-Pacific's supremacy and ensuring a steady flow of innovations, especially in clean-label and gluten-free segments.

Simultaneously, Asia-Pacific is projected to maintain its rapid ascent, boasting a CAGR of 7.59% through 2031. This growth is fueled by urbanization, rising disposable incomes, and heightened health consciousness. The demand for gluten-free bakery items, noodles, and whole-grain rice flour products is on the rise, driven by a societal shift towards healthier eating and proactive government campaigns on health. This dual distinction as both the largest and the fastest-growing region highlights Asia-Pacific's pivotal role in steering the global rice flour market.

While Asia-Pacific takes center stage, North America and Europe are also witnessing steady growth. This expansion is largely attributed to the prevalence of celiac disease, a preference for clean-label products, and the surging popularity of Asian cuisine. Retail outlets and specialty foodservice channels are buzzing with activity, driven by innovations in organic certifications, allergen-free products, and the rising adoption of soluble rice flour. On the other hand, regions like South America, the Middle East, and Africa are emerging as new frontiers. Here, urbanization, a burgeoning middle class, and initiatives aimed at food security are spurring demand. Moreover, policy decisions and trade dynamics in these areas are shaping product availability and pricing, marking them as significant growth zones alongside the more established markets.

Competitive Landscape

The global rice flour market exhibits a moderately fragmented competitive landscape, with key players such as Ingredion, Cargill, ADM, and Ebro Foods leveraging extensive production networks, proprietary processing technologies, and established partnerships with food and beverage manufacturers. These companies are strategically focusing on capacity expansion in rice-producing regions, innovation in soluble and ultra-fine rice flours, and vertical integration to secure organic and non-genetically modified organism (GMO) sourcing. These initiatives enable them to address the growing demand for clean-label and functional ingredients while maintaining strong positions in industrial and specialty applications.

Simultaneously, emerging opportunities are creating space for disruptors and mid-tier players. New cooperatives and specialty millers are differentiating themselves by offering traceability, origin-based narratives, and certified organic or heirloom rice varieties, which appeal to premium retail and direct-to-consumer markets. Additionally, technological advancements are reshaping the competitive dynamics, with digital agriculture platforms enhancing traceability and advanced milling equipment enabling functional customization, thereby opening new avenues for market differentiation.

Smaller players are increasingly utilizing e-commerce, subscription-based models, and partnerships with health-focused brands to capture niche segments. In response, established players are strengthening their innovation pipelines and pursuing strategic expansions. The interaction between global market leaders and agile regional disruptors is driving a dynamic competitive environment, where differentiation through clean-label innovation, sustainability credentials, and premium positioning is becoming as critical as scale and cost efficiency. This equilibrium ensures the rice flour market remains conducive to both consolidation and entrepreneurial growth.

Rice Flour Industry Leaders

-

Archer-Daniels-Midland Company (ADM)

-

Ingredion Incorporated

-

KRBL Limited

-

BENEO GmbH

-

Burapa Prosper

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Riceland Foods, the U.S.'s largest rice miller and marketer, teamed up with ODW Logistics to launch a new 64,000 sq ft warehouse in Memphis, Tennessee. This facility, compliant with FDA standards and accessible by rail, was strategically located after an in-depth logistics network analysis. This move aims to boost distribution efficiency and cater to rising customer demand. With the Memphis hub, Riceland can better redistribute inventory, ramp up production capacity, and enhance supply chain flexibility. The company is leveraging the rail infrastructure and expanding its operations at plants in Arkansas and Missouri.

- April 2025: Quinn Snacks partnered with Ralston Family Farms, a women-led, third-generation farm championing regenerative agriculture. Together, they're turning broken rice grains into premium regenerative brown rice flour. This collaboration not only transforms potential waste into a valuable product but also bolsters sustainable farming and ensures economic stability for the farm. The move is in line with Quinn's commitment to promoting regenerative agriculture, creating opportunities for farmers, refining ingredient sourcing, and boosting transparency in the supply chain.

- November 2024: LT Foods Ltd., a global FMCG giant and the force behind brands like DAAWAT, Hadeel, and Mufaddal, set up shop in Saudi Arabia, inaugurating a new office in Riyadh. With an eye on the Kingdom's USD 2 billion rice and rice-based foods market, LT Foods is channeling SAR 185 million over the next five years into warehousing, inventory, and personnel. The ambitious company targets a revenue of SAR 435 million in the same timeframe.

Global Rice Flour Market Report Scope

Rice flour is a finely milled powder made from rice grains, commonly used as a gluten-free alternative in baking, cooking, and food processing. It offers a neutral flavor, smooth texture, and versatile functionality, making it suitable for noodles, batters, snacks, and specialty health-focused products.

The global rice flour market is segmented by source, nature, end use, and geography. Based on the source, the market is segmented into White Rice Flour and brown rice flour. Based on the source, the market is segmented into conventional and organic. Based on the source, the market is segmented into retail, industrial, and foodservice/HoReCa. Based on the geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

| White Rice Flour |

| Brown Rice Flour |

| Conventional |

| Organic |

| Retail |

| Industrial |

| Foodservice/HORECA |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | White Rice Flour | |

| Brown Rice Flour | ||

| By Nature | Conventional | |

| Organic | ||

| By End Use | Retail | |

| Industrial | ||

| Foodservice/HORECA | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the rice flour market?

The rice flour market size is USD 1.39 billion in 2025 and is projected to reach USD 2.12 billion by 2031.

Which region leads the rice flour market?

Asia-Pacific holds 56.21% of 2025 revenue and is also the fastest-growing region at 7.59% CAGR.

Why is brown rice flour gaining popularity?

Brown rice flour grows at 7.98% CAGR owing to whole-grain fiber, micronutrient retention, and alignment with clean-label trends.

How are arsenic regulations affecting market growth?

EU limits of 0.25 mg/kg increase compliance costs, restricting supply in infant cereal channels but enhancing consumer confidence.

Page last updated on: