Conversational Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

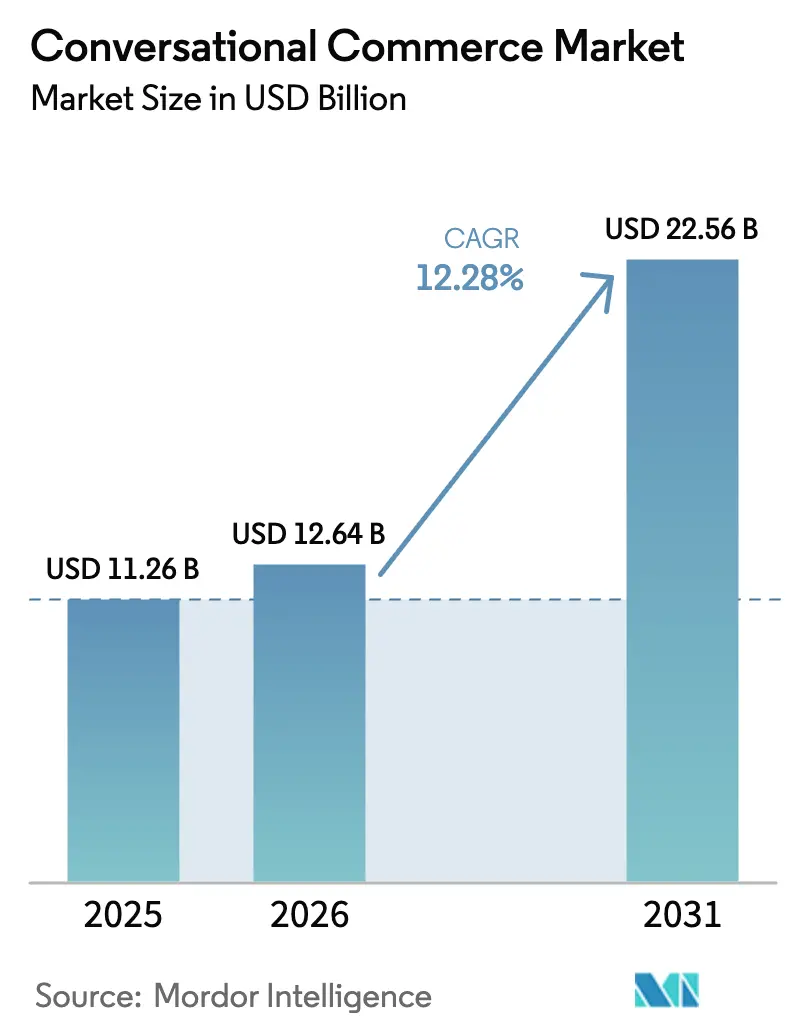

| Market Size (2026) | USD 12.64 Billion |

| Market Size (2031) | USD 22.56 Billion |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conversational Commerce Market Analysis by Mordor Intelligence

The conversational commerce market size is projected to be USD 11.26 billion in 2025, USD 12.64 billion in 2026, and reach USD 22.56 billion by 2031, growing at a CAGR of 12.28% from 2026 to 2031. Real-time, context-aware dialogues inside familiar messaging and voice platforms are replacing static web forms, collapsing the steps from intent to purchase and reducing cart abandonment. Smartphone-first regions and pro-interoperability regulation are amplifying adoption, while live-video shopping, in-chat payments, and voice-enabled checkout continue to blur the line between marketing interaction and transaction moment. Vendors that pair low-code tooling with large-language-model APIs are lowering entry barriers for small businesses, and cloud deployment remains the default as brands seek elastic infrastructure that scales during promotional spikes without capital expense.

Key Report Takeaways

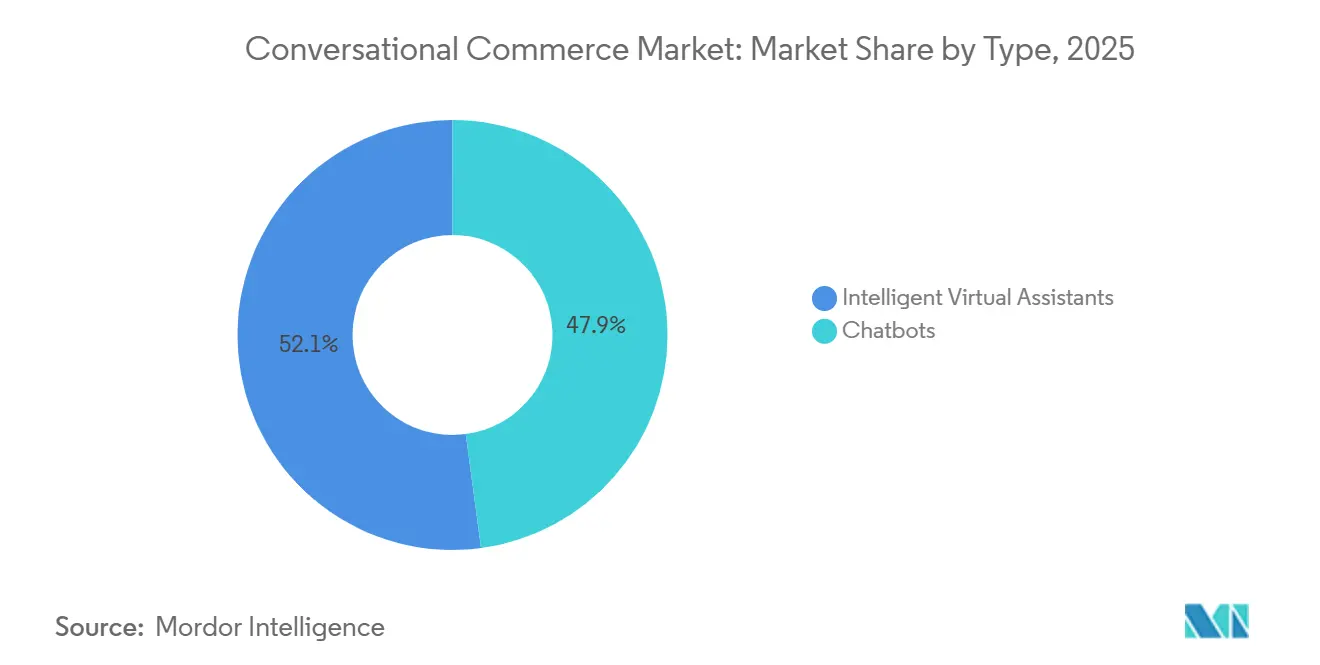

- By type, chatbots held 47.89% of the conversational commerce market share in 2025, while intelligent virtual assistants are projected to register a 12.74% CAGR through 2031.

- By component, software and solutions led with a 72.46% revenue share in 2025; services are forecast to expand at a 12.71% CAGR to 2031.

- By deployment mode, cloud installations accounted for 83.66% of the conversational commerce market size in 2025 and are expected to grow at a 12.62% CAGR through 2031.

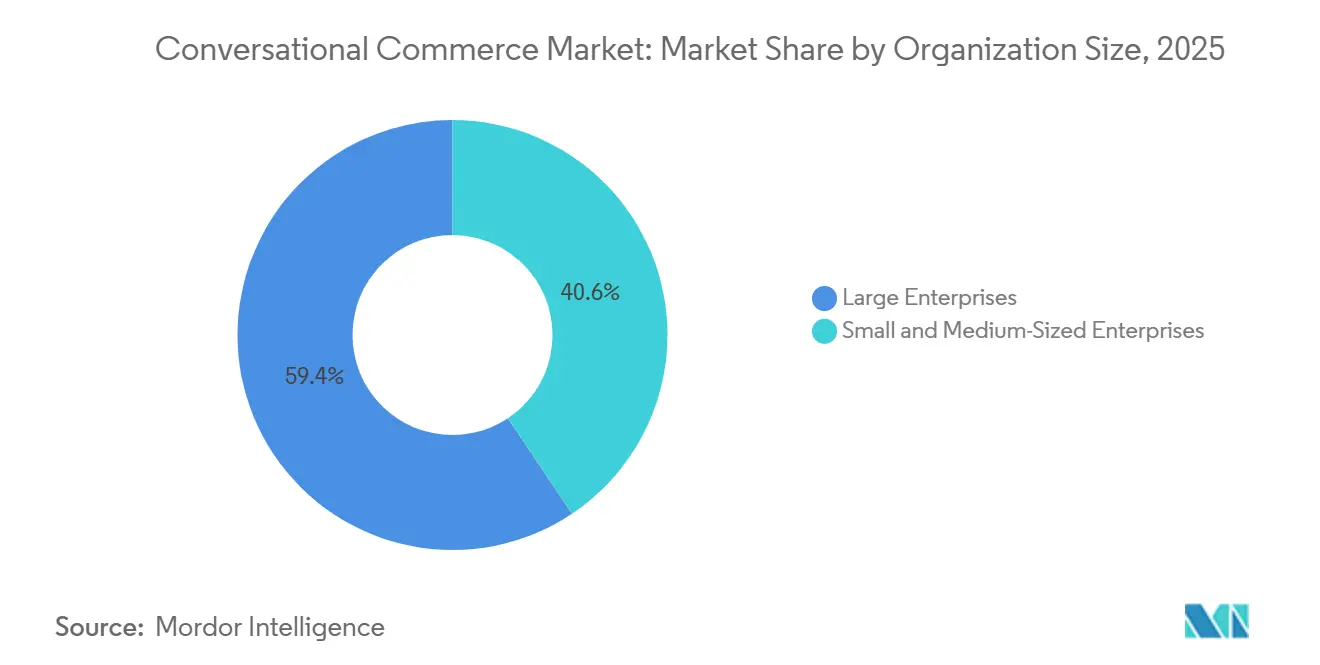

- By organization size, large enterprises captured 59.37% of 2025 spending, whereas small and medium-sized enterprises are set to rise at a 12.67% CAGR to 2031.

- By end-user industry, retail and e-commerce accounted for 27.84% of the conversational commerce market in 2025, while healthcare is advancing at a 13.44% CAGR through 2031.

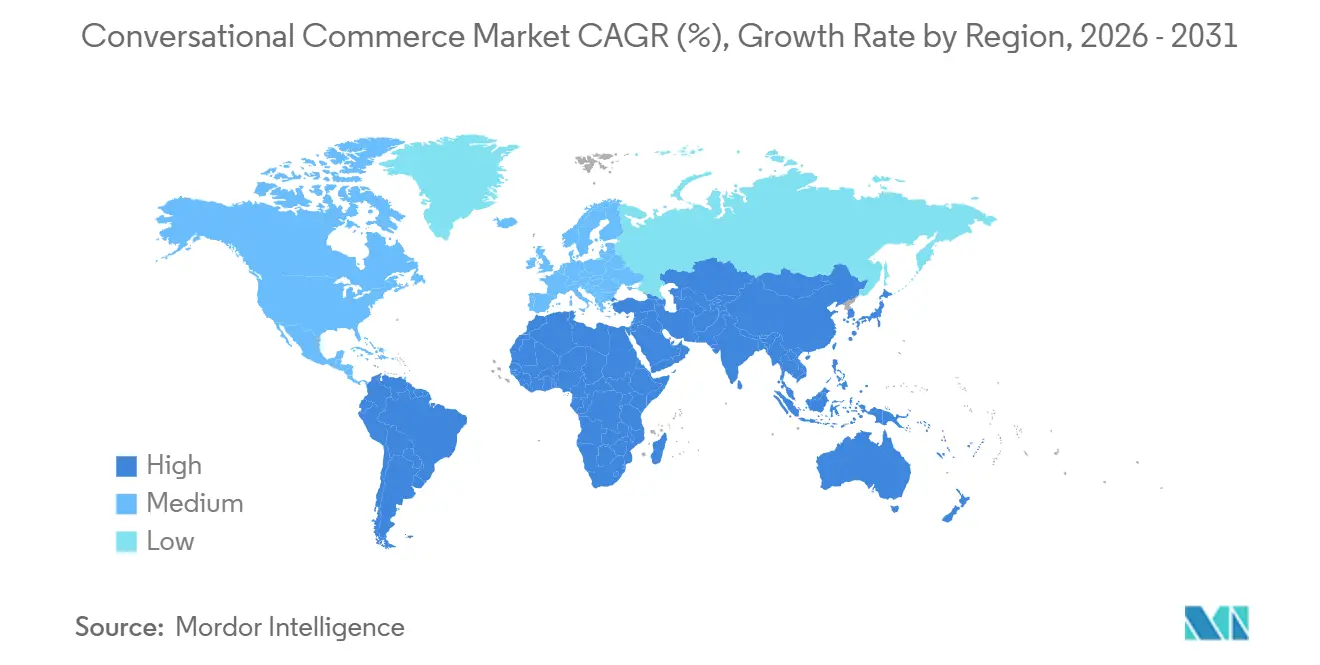

- By geography, Asia-Pacific commanded 38.91% of the conversational commerce market share in 2025, and Africa is projected to post a 13.27% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Conversational Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Roll-Out of WhatsApp Business in India and Brazil Enabling In-Chat Payments | +2.3% | Asia-Pacific (India core), South America (Brazil core) | Medium term (2-4 years) |

| Live-Video Social Commerce in China Catalysing Transactable Chat Sessions | +2.1% | Asia-Pacific (China core, spill-over to Southeast Asia) | Short term (≤ 2 years) |

| Foundation-Model APIs Lowering SME Chatbot Build Cost | +2.4% | Global, with accelerated uptake in emerging markets | Medium term (2-4 years) |

| Mandatory RCS Roll-Outs by European MNOs Unlocking Rich Messaging Commerce | +1.6% | Europe (EU27 and United Kingdom) | Long term (≥ 4 years) |

| Voice-Enabled Smart-Speaker Check-Out Penetration Across US Households | +1.5% | North America (United States core) | Medium term (2-4 years) |

| Bank-Grade KYC Plug-Ins for Messaging Apps Driving Regulated BFSI Use Cases in North America | +1.3% | North America (United States, Canada) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rollout of WhatsApp Business in India and Brazil Enabling In-Chat Payments

Meta reported business-messaging revenue at a USD 1 billion annual run rate in 2024, and India and Brazil accounted for a disproportionately high share of chat volume.[1]China Internet Network Information Center, “Statistical Report on Internet Development in China,” cnnic.net.cn India’s Unified Payments Interface processed 16.73 billion transactions in December 2025, and WhatsApp Pay completes those payments without redirecting users, reducing cart abandonment by 30% when compared with mobile-web flows. Brazil counted 5 million active WhatsApp Business accounts by mid-2025, and its Pix network handled 4.4 billion transfers in November 2025, with a growing share initiated within messaging threads. High smartphone penetration, low card usage, and pro-interoperability regulation make chat-native checkout especially attractive to micro-merchants. Similar conditions in Indonesia, Mexico, and Nigeria point to further geographic spillover for this model.

Live-Video Social Commerce in China Catalysing Transactable Chat Sessions

China’s livestreaming ecosystem generated CNY 4.9 trillion (USD 690 billion) in 2024 merchandise value, and platforms such as Douyin and Taobao Live now embed one-to-one chat that lets viewers negotiate, request demos, and pay without leaving the video.[2]National Payments Corporation of India, “UPI Transaction Statistics December 2025,” npci.org.in Alibaba disclosed that sessions with real-time chat converted 40% better than prerecorded video ads in fiscal 2025. Douyin processed more than 1 billion live-commerce orders during 1H 2025, validating the format at a national scale. Southeast Asian marketplaces such as Shopee and Lazada are piloting similar features, signalling imminent regional expansion. Western platforms are also prototyping shoppable video to offset advertising-only revenue streams.

Foundation-Model APIs Lowering SME Chatbot Build Cost

OpenAI cut GPT-4 API pricing from USD 0.03 to USD 0.01 per 1,000 tokens between 2023 and January 2025, trimming inference expense by 67%. Google’s Gemini API introduced a free tier offering qualifying startups 1 million tokens per month, intensifying price pressure.[3]Google Cloud, “Gemini API Free Tier,” cloud.google.com Lower input costs have reduced total ownership expense for conversational AI by roughly 60%, allowing small retailers and clinics to deploy production-grade bots without data-science hires. A 2025 PwC survey shows 48% of SMEs in North America and Europe intend to adopt conversational AI within 12 months, more than double the 2023 level. Emerging-market merchants gain even more as cloud APIs let them leapfrog call-center outsourcing in both cost and deployment speed.

Mandatory RCS Rollouts by European MNOs Unlocking Rich Messaging Commerce

European carriers adopted the GSMA Universal Profile in 2024, and by early 2026, more than 80% of Android devices in the EU ship with RCS active by default. Deutsche Telekom, Orange, Telefónica, and Vodafone launched a joint RCS business hub that lifted click-through rates 25% above SMS in retail and travel pilots. Rich cards, payment buttons, and verified sender IDs make the channel suitable for checkout experiences that once required native apps. The forthcoming EU eIDAS 2.0 wallet will enable in-message authentication for regulated payments, further boosting credibility. Together, these shifts position carrier-grade messaging as a standards-based alternative to proprietary platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Apple iOS Privacy Updates Reduce 3rd-Party Conversion Tracking in Messages | -1.4% | Global, with pronounced impact in North America and Europe | Short term (≤ 2 years) |

| EU Digital Markets Act Limits Platform Self-Preferencing of Commerce Flows | -1.2% | Europe (EU27 gatekeepers: Apple, Meta, Google, Amazon) | Medium term (2-4 years) |

| NLP Accuracy Gaps in Low-Resource Asian Languages Hinder the Market | -0.9% | Asia-Pacific (Southeast Asia, South Asia excluding India) | Long term (≥ 4 years) |

| Fragmented Payment Standards in Africa Depress Completion Rates | -0.8% | Africa (sub-Saharan Africa core) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Apple iOS Privacy Updates Reduce 3rd-Party Conversion Tracking in Messages

Apple’s App Tracking Transparency, enforced since iOS 14.5, requires explicit opt-in for cross-app tracking, and global consent stabilized near 25% by mid-2024. Without deterministic links between chat engagements and iOS purchases, brands struggle to prove return on ad spend. Meta confirmed in its 2024 earnings call that targeting accuracy and attribution declined materially, prompting product shifts toward in-chat payments that retain first-party data. The measurement gap is most acute in North America and Europe, where iOS market share tops 50% in several countries. Probabilistic models fill some gaps, but at the cost of precision and higher acquisition budgets.

EU Digital Markets Act Limits Platform Self-Preferencing of Commerce Flows

The Digital Markets Act, enforceable since March 2024, bars designated gatekeepers from favoring in-house payment rails or ranking their own services above rivals. Merchants on WhatsApp or Google Business Messages can now steer EU buyers to third-party gateways, yet early compliance data show conversion rates lag native checkout by 15-20% because users face extra redirects and unfamiliar payment pages. While the rule expands payment choice and trims platform fees, it fragments user journeys that once felt seamless. Gatekeepers are redesigning interfaces to remain compliant without losing engagement, but near-term revenue per conversation is expected to dip until shoppers grow comfortable with multistep flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Intelligent Virtual Assistants Gain Ground On Established Chatbots

Chatbots captured 47.89% of the conversational commerce market share in 2025, reflecting their dominance in order tracking and FAQ automation. Intelligent virtual assistants, however, are projected to advance at a 12.74% CAGR through 2031 as large-language-model reasoning, sentiment analysis, and proactive outreach grow more affordable. Enterprises see assistants shorten average handle time and increase cross-sell rates by surfacing contextual offers rather than rigid menu prompts. Banking, insurance, and healthcare providers appreciate assistants that parse policy text or triage symptoms, tasks that scripted bots cannot perform reliably. The shift signals a gradual migration from static decision trees toward generative, multi-turn engagement.

Growth momentum rests on richer data pipelines and on-device speech processing that trims latency. Voice shopping benefits most because assistants can disambiguate products, negotiate delivery windows, and upsell complementary items, whereas chatbots force users through keyword sequences that inflate abandonment. Vendors package retrieval-augmented generation and conversation memory so assistants remember prior interactions across channels, further widening the capability gap. At the same time, chatbots remain cost-effective for high-volume flows in regulated settings that demand strict audit trails. The coexistence of both tools lets brands match complexity to use case while nudging high-value journeys toward assistants.

By Component: Services Expand As Integrations Outpace Off-The-Shelf Licenses

Software and solutions accounted for 72.46% of the conversational commerce market size in 2025, fueled by platform licenses, API calls, and pre-built templates. Yet services are forecast to grow at a 12.71% CAGR through 2031 as enterprises wrestle with legacy CRM, payment, and inventory integrations that shrink the appeal of plug-and-play deployments. Consulting teams configure encryption, compliance logging, and multi-language tuning that regulated sectors cannot skip. Financial services implementations often require alignment with SOC 2 and PCI-DSS, which generic cloud dashboards lack. As a result, service revenue now attaches to most enterprise licenses.

The consulting surge also comes from iterative optimization once a bot is live. Brands rely on managed services for A/B testing prompts, refining intents, and mining conversation transcripts for product feedback. Health providers contract specialists to map electronic health records and pharmacy systems into HIPAA-compliant chat flows. Platform vendors respond with tiered support bundles that add training credits and dedicated success managers, converting one-time deals into subscription-like revenue. Over time, the rising share of wallet from services balances price compression on core software seats.

By Deployment Mode: Cloud Dominates As Elasticity And Fast Releases Trump Control

Cloud installations held 83.66% of the conversational commerce market share in 2025 and are expected to climb at a 12.62% CAGR through 2031. Brands favor pay-as-you-go elasticity that absorbs seasonal traffic spikes without capital budgets. Hyperscalers roll out new features every few weeks, so customers can access the latest large-language-model integrations without scheduling downtime. Regional data-center expansion and certifications such as FedRAMP High ease sovereignty concerns that once blocked federal and financial workloads. On-premises projects now center on air-gapped defense systems and nations with strict residency laws.

Operational advantages compound over time. Deloitte found that cloud reduced the five-year total cost of ownership by 45% compared with on-premises hardware, thanks to avoided depreciation and labor overhead. Continuous delivery also means faster remediation of compliance findings and security patches, shrinking breach windows. On-premises users, by contrast, face annual upgrade cycles that lag cloud feature sets and analytics dashboards. As foundation-model inference costs fall, the scale economies of multitenant infrastructure grow stronger, tilting future migrations even further toward the cloud.

By Organization Size: SMEs Close The Gap With No-Code Tools And Usage-Based Fees

Large enterprises accounted for 59.37% of the conversational commerce market in 2025, leveraging volume discounts, global rollouts, and custom analytics. Small and medium-sized enterprises are projected to grow at a 12.67% CAGR through 2031, as no-code builders and pay-per-conversation pricing eliminate high upfront fees. Shopify Inbox, for example, attracted hundreds of thousands of merchants with a free chat layer embedded in storefront dashboards. WhatsApp Business added rich catalog and quick-reply widgets at zero cost, letting micro-retailers sell inside a familiar interface. Lower financial and technical barriers shift adoption from experiment to necessity for neighborhood stores.

SMEs use templates for appointment booking, delivery tracking, and lead qualification that go live in days, not months. Falling API prices let them offer human-like dialog without machine-learning talent, while marketplaces provide plug-and-play payment gateways. Enterprises still outspend on multilingual assistants, governance, and advanced analytics that require dedicated teams. Yet as suppliers release vertical starter kits and usage-based tiers, the capability gap narrows. Over the forecast period, incremental growth will disproportionately come from first-time SME buyers entering the channel.

By End-User Industry: Healthcare Emerges As The Fastest-Expanding Vertical

Retail and e-commerce accounted for 27.84% of the conversational commerce market share in 2025, leveraging chat to rescue abandoned carts, automate returns, and personalize recommendations. However, healthcare is slated to record the highest CAGR of 13.44% between 2026 and 2031. Telemedicine providers merge symptom checkers, appointment slots, and prescription refills into unified threads that cut call-center load and improve patient compliance. HIPAA-ready encryption and audit trails are now shipped by default on many cloud platforms, unlocking large hospital networks. Insurers experiment with claim intake bots that collect documents and verify coverage in chat, accelerating settlement cycles.

Other industries follow distinct paths. Banks embed biometric KYC plugins and fraud alerts to protect high-value transfers, while telecom operators automate tier-one troubleshooting for connectivity issues. Travel brands push real-time rebooking options via chat when flights change, bundling hotels and cars to drive incremental revenue. Manufacturing and logistics remain early-stage but show upside as supplier portals and shipment tracking migrate from email to conversational interfaces. Across verticals, success correlates with the ability to combine transactional data, identity verification, and payment rails into a single dialogue that finishes the sale.

Geography Analysis

Asia-Pacific contributed 38.91% of 2025 conversational-commerce revenue, anchored by China’s live-video shopping and India’s in-chat UPI payments. Douyin’s one-to-one chat inside livestreams now sets the conversion benchmark that TikTok is adapting for Western markets, while Taobao Live’s 40% uplift over prerecorded video demonstrates the power of real-time engagement. Southeast Asian super-apps such as Grab and Gojek fold ride-hailing, food delivery, and chat commerce into unified wallets, compressing the customer journey to a few taps. Japan and South Korea are showing slower migration from app-centric buying to chat-native flows, yet voice assistants embedded in smart TVs and cars are opening a new entry point for conversational checkout.

Africa is forecast to expand at a 13.27% CAGR through 2031 as the ubiquity of mobile money meets falling API costs for foundation models. Kenya’s M-Pesa exceeded 2 billion transactions in 2024, and Nigerian fintechs are embedding WhatsApp bots to handle peer payments and bill pay under the Central Bank’s open-banking rules. South Africa and Egypt are piloting RCS commerce with local carriers, but fragmented payment standards still depress completion rates. In North America, more than 100 million U.S. households own Alexa devices, and voice shopping queries rose 37% in 2024, though image-poor interfaces cap conversion. Canadian banks mirror U.S. patterns, adding bilingual chatbots that comply with PIPEDA data rules.

Europe’s trajectory is shaped by the Digital Markets Act and GDPR, which enforce interoperability while raising deployment complexity. The United Kingdom, Germany, France, and Italy lead enterprise rollouts, and RCS reaches more than 80% of EU Android phones, boosting click-through rates by 25% over SMS. Spain and the Nordics focus on sustainability-minded shoppers who value transparent data practices. South America relies on Brazil, where 5 million merchants use WhatsApp Business and Pix logs 4.4 billion monthly transfers inside chat threads. Argentina, Colombia, and Chile follow, though macro volatility influences spend. In the Middle East, the UAE’s Smart Dubai chatbot processed 500,000 interactions in its first year, and Saudi Vision 2030 funds Arabic large-language models for citizen services. Regional growth ultimately hinges on 4G-5G rollout, interoperable payments, and public-sector digital mandates.

Competitive Landscape

The market remains moderately concentrated, with hyperscalers and specialists splitting share, with the top five providers holding roughly 40-45%. Meta’s WhatsApp Business API surpassed 200 million monthly business interactions in 2025 and now layers catalogs, payments, and real-time inventory into chat, aiming to become a merchant operating system for mobile-first markets. Google Business Messages funnels Maps searches into transactable threads and crossed the one-billion-conversation mark in 2024, leveraging search intent to shorten the path to purchase.

Specialist vendors carve out niches where compliance or vertical depth trumps scale. LivePerson ties sentiment scoring to secure handoff, winning U.S. bank and insurer deals that demand audit-grade transcripts. Sprinklr’s 2025 Botsify acquisition adds 10,000 SMEs and no-code templates, widening reach beyond enterprise clients. Glia’s ChannelLess Architecture enables financial institutions to move customers from web chat to voice without losing authentication, solving a pain point that generic platforms often overlook. IBM patents on cross-channel memory position Watson Assistant to keep context as users switch devices, addressing a key driver of abandonment.

White-space opportunities persist in manufacturing, logistics, and education, where conversational tools remain nascent. Regional disruptors in Africa and Southeast Asia bundle local language, mobile money, and pay-as-you-go pricing, undercutting Western licensing models. Hyperscalers answer by embedding newer foundation models, multimodal search, and auto-translation, compressing feature gaps but not always matching local nuance. Mergers and partnerships accelerate as vendors seek breadth; LivePerson partnered with Salesforce to route chats by lifetime value, unlocking a USD 50 million pipeline in 90 days. As platform APIs converge on similar core functions, differentiation shifts to packaged use cases, privacy guarantees, and ecosystem depth, leaving room for both global giants and nimble vertical specialists.

Conversational Commerce Industry Leaders

Amazon Web Services, Inc.

Meta Platforms, Inc.

Google LLC

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Meta expanded WhatsApp Business API to support multi-agent routing and real-time inventory, cutting post-purchase cancellations 19%.

- January 2026: Google launched Dialogflow CX 2.0 with native Gmail and Google Chat integration, trimming CRM bot deployment time 40%.

- December 2025: AWS released Amazon Lex V3 with 24-language support and noise-robust speech recognition, 38% of new deployments came from Asia-Pacific and the Middle East.

- November 2025: Microsoft closed its USD 16 billion acquisition of Nuance’s conversational-AI unit, bolstering healthcare virtual assistants.

Global Conversational Commerce Market Report Scope

The Conversational Commerce Market Report is Segmented by Type (Chatbots, and Intelligent Virtual Assistants), Component (Software and Solutions, and Services), Deployment Mode (Cloud, and On-Premises), Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), End-User Industry (Banking, Financial Services and Insurance, Information Technology and Telecom, Healthcare, Travel and Hospitality, Retail and E-Commerce, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Chatbots |

| Intelligent Virtual Assistants |

| Software and Solutions |

| Services |

| Cloud |

| On-Premises |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance |

| Information Technology and Telecom |

| Healthcare |

| Travel and Hospitality |

| Retail and E-Commerce |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Chatbots | ||

| Intelligent Virtual Assistants | |||

| By Component | Software and Solutions | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| By Organization Size | Small and Medium-Sized Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | Banking, Financial Services and Insurance | ||

| Information Technology and Telecom | |||

| Healthcare | |||

| Travel and Hospitality | |||

| Retail and E-Commerce | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will global conversational commerce spending be by 2031?

It is projected to reach USD 22.56 billion, expanding from USD 12.64 billion in 2026 at a 12.28% CAGR.

Which region contributes the most revenue today?

Asia-Pacific led with 38.91% of 2025 revenue, driven by China’s live-video shopping and India’s in-chat payments.

What segment is growing fastest within the market?

Healthcare deployments are forecast to post a 13.44% CAGR as telemedicine integrates symptom checking and prescription flows into chat.

Why do enterprises favor cloud deployment for conversational commerce?

Cloud offers elastic scaling, rapid feature releases, and 45% lower five-year total cost of ownership versus on-premises setups.

How are privacy regulations affecting conversational commerce?

Apple’s App Tracking Transparency and the EU Digital Markets Act limit tracking and self-preferencing, reducing conversion measurement accuracy and raising compliance complexity.

Are small businesses adopting conversational AI?

Yes, SME adoption is rising at a 12.67% CAGR due to no-code builders and pay-per-conversation pricing that lower entry barriers.

Page last updated on: