E-commerce App Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

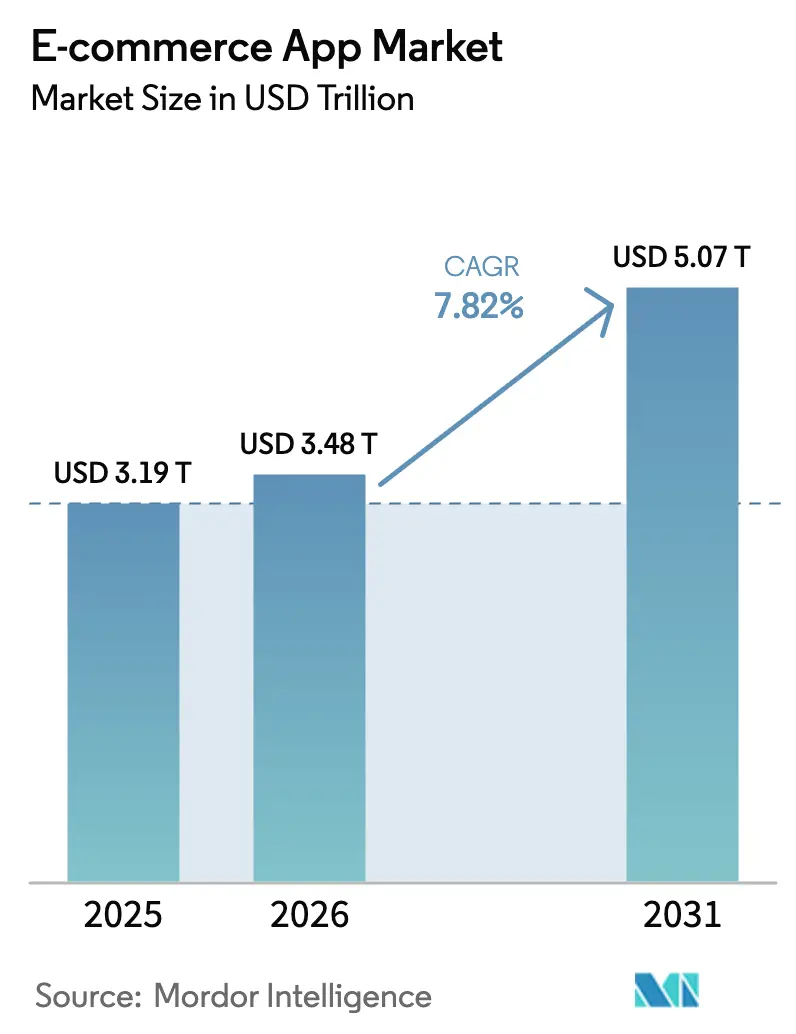

| Market Size (2026) | USD 3.48 Trillion |

| Market Size (2031) | USD 5.07 Trillion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-commerce App Market Analysis by Mordor Intelligence

The e-commerce app market size is projected to be USD 3.19 trillion in 2025, USD 3.48 trillion in 2026, and reach USD 5.07 trillion by 2031, growing at a CAGR of 7.82% from 2026 to 2031. Immersive augmented-reality try-ons, enabled by 5G networks that cut median page-load times by 40%, have raised conversion rates by 18% to 22% in fashion and home-furnishing categories. Subscription models are gathering momentum as consumers trade one-off fees for all-you-can-ship memberships, a shift that shields platforms from cyclical spending dips. Social-commerce integrations on short-video platforms now collapse discovery and checkout into 90 seconds, prompting brands to redirect 15% to 20% of search-advertising budgets toward creator partnerships. Meanwhile, mobile-money interoperability in Africa and instant-payment rails in India compress settlement friction, broadening addressable demand and stimulating competitive entry.

Key Report Takeaways

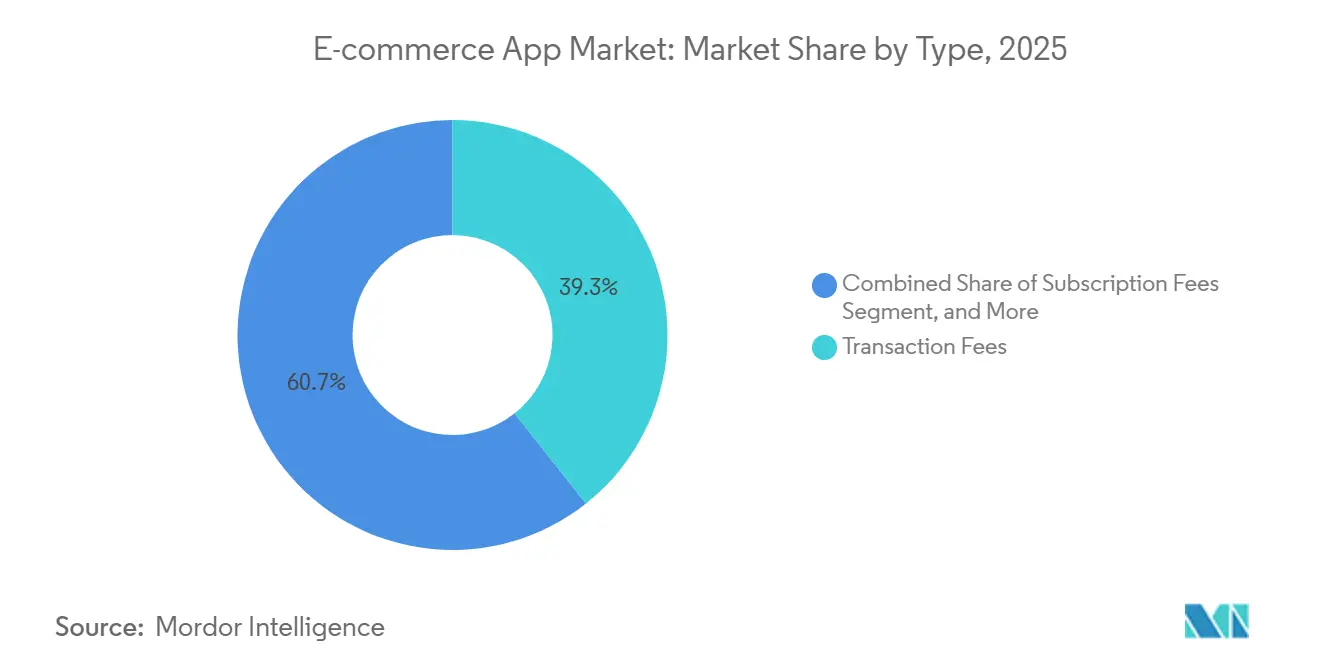

- By type, transaction fees led with 39.34% revenue share in 2025 while subscription fees are forecast to expand at an 8.82% CAGR to 2031.

- By platform, android held 72.67% of the e-commerce app market share in 2025, whereas super-app mini-programs post the highest projected CAGR at 8.24% through 2031.

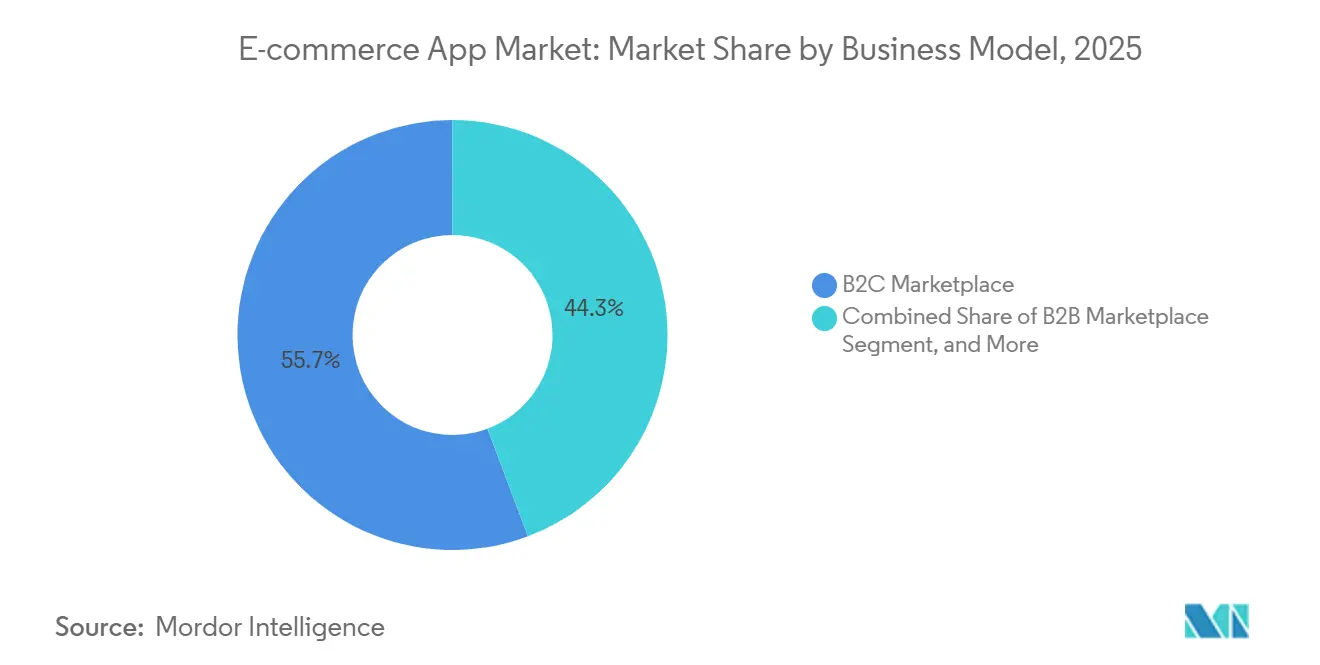

- By business model, business-to-consumer marketplaces accounted for 55.71% of the e-commerce app market in 2025, and peer-to-peer resale is advancing at an 8.41% CAGR through 2031.

- By product category, fashion and apparel commanded a 28.66% share in 2025, while grocery and FMCG are set to grow at a 9.11% CAGR through 2031.

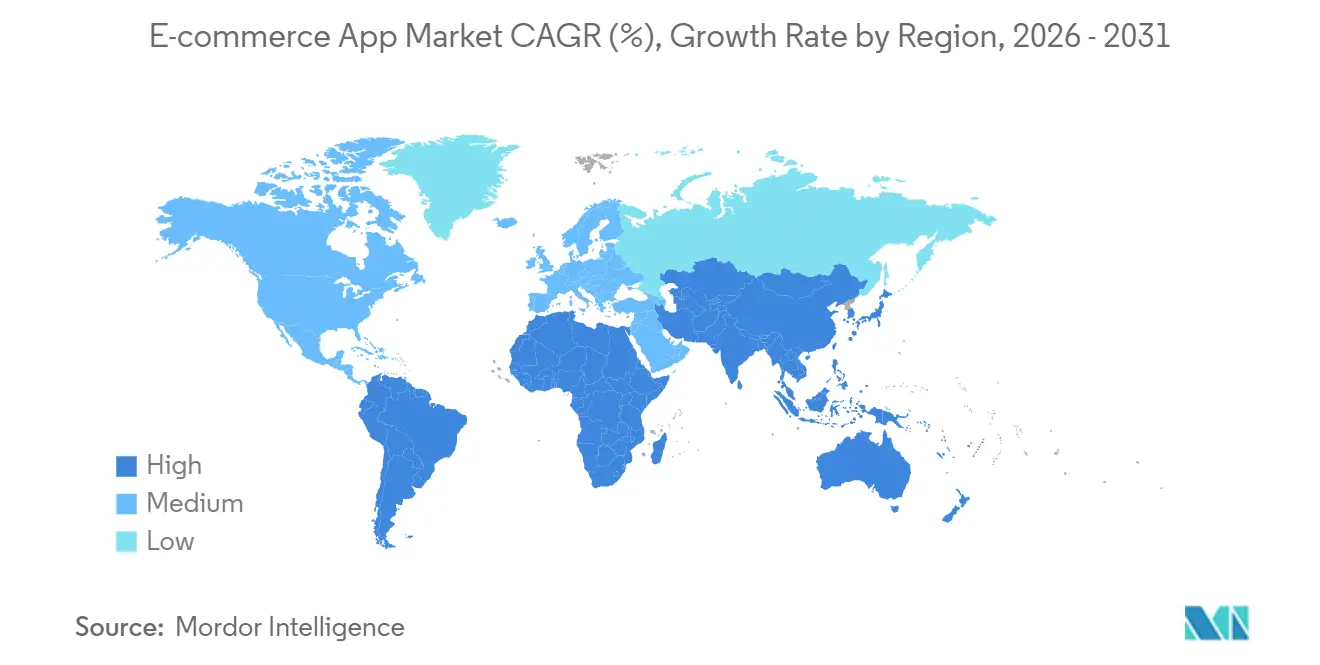

- By geography, Asia-Pacific accounted for 42.48% of 2025 revenue, and Africa is the fastest-growing region, with an 8.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-commerce App Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G Enhancing Mobile-Commerce Experiences | +1.2% | Global, with early density in South Korea, United States, China | Medium term (2-4 years) |

| Rapid Expansion of Buy-Now-Pay-Later Integrations | +1.4% | North America, Europe, Australia | Short term (≤ 2 years) |

| Growing Social-Commerce Convergence via Short-Video Platforms | +1.6% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| AI-Driven Personalization Increasing Average Order Value | +1.3% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Penetration of Affordable Smartphones in Emerging Economies | +1.5% | Africa, South Asia, Southeast Asia | Long term (≥ 4 years) |

| Government Push for Digital Payments and e-Invoices | +1.0% | India, Brazil, Middle East, with pilot programs in Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Enhancing Mobile-Commerce Experiences

Single-digit-millisecond latency on 5G enables rich product visualization that had stalled on 4G. In South Korea, 5G penetration reached 50% in 2024, and AR-enabled listings achieved a 2.3x click-through rate compared to static images.[1]Samsung Electronics, “AR Features Drive Engagement,” news.samsung.com Retailers exploit network slicing to guarantee sub-50-millisecond checkout during flash sales, curbing the USD 18 billion in annual losses from cart abandonment. Telcos are also bundling zero-rated data plans that subsidize app usage in price-sensitive markets across Southeast Asia and Latin America, thereby boosting e-commerce app adoption.

Rapid Expansion of Buy-Now-Pay-Later Integrations

BNPL accounted for 9.8% of U.S. e-commerce transactions in 2024, but its reclassification as credit card lending now imposes Regulation Z dispute-resolution obligations that may inflate compliance costs by USD 1.2 billion annually. Despite tighter oversight, PayPal disclosed that BNPL users exhibit a 35% higher lifetime value than one-time buyers, validating installment flexibility as a demand catalyst.[2]PayPal Holdings, “Annual Report 2025,” pypl.com Incumbents able to underwrite risk with proprietary data will likely widen moats as the e-commerce app market evolves.

Growing Social-Commerce Convergence via Short-Video Platforms

TikTok Shop processed USD 20 billion GMV across Southeast Asia in 2024, demonstrating that shoppable live streams can compress the purchase funnel to under 90 seconds. Instagram’s 2025 rollout of in-app checkout to 27 additional countries removed redirect friction that had caused 40% of social-referred traffic to leak.[3]Meta Platforms, “Form 10-K 2025,” meta.com Brands now allocate up to 20% of their performance spend to influencer partnerships that convert at 3x the rate of traditional algorithmic recommendations. Logistics APIs that auto-populate shipping addresses have cut abandonment rates by 22 percentage points, reinforcing social video as a durable demand driver.

AI-Driven Personalization Increasing Average Order Value

Recommendation engines surpassing 85% accuracy raise average order values by 12% to 15%, a benchmark confirmed in Amazon’s 2025 shareholder letter. Shopify merchants enabling dynamic bundling saw carts expand 18% after a June 2025 AI upgrade. Return rates fell 23% among retailers deploying predictive sizing tools, expanding gross margins while easing logistics pressure. Heightened privacy rules are now channeling investment toward first-party data capture through loyalty programs, cementing personalization as a pivotal capability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Regulatory Scrutiny on App Tracking Transparency | -0.9% | Global, with strictest enforcement in European Union, United States | Short term (≤ 2 years) |

| Escalating Cross-Border Logistics Costs for SMEs | -0.7% | Global, acute in Africa, Latin America, Southeast Asia | Medium term (2-4 years) |

| Heightened Consumer Concerns Around Data Privacy Breaches | -0.6% | North America, Europe, with rising awareness in Asia-Pacific | Medium term (2-4 years) |

| Talent Shortage in Mobile Cyber-Security Engineering | -0.5% | Global, most severe in North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Regulatory Scrutiny on App Tracking Transparency

Opt-in rates for Apple’s App Tracking Transparency framework slipped to 25% by 2024, severing cross-app identifier graphs that powered retargeting and costing Meta an estimated USD 10 billion in mobile-ad revenue. The European Union levied EUR 2.1 billion in GDPR fines on non-compliant e-commerce apps during 2023-2024, forcing developers to rebuild consent flows that capture 40% less first-session data. Platforms now pivot toward contextual ads and first-party loyalty schemes, yet short-term revenue pressure persists across the e-commerce app market.

Escalating Cross-Border Logistics Costs for SMEs

Small-parcel shipping rates rose 18% in 2024, shrinking margins for SMEs lacking volume to negotiate contracts. Customs digitization delays under Europe’s Import Control System 2 held 22% of inbound parcels for more than five days during its October 2024 rollout. Flexport and other freight-aggregation platforms pool SME shipments to secure container rates 25% below spot, but access remains uneven in Africa and Southeast Asia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Subscription Models Counter Fee Fatigue

Transaction fees accounted for 39.34% of revenue share in 2025, as marketplaces monetized every completed sale, yet subscription fees are on track to expand at an 8.82% CAGR through 2031. Amazon Prime exemplifies the model with 230 million members who contributed USD 40 billion in annual fees during 2025, cushioning revenue against discretionary slowdowns. Rising subscription uptake indicates that predictable logistics perks and exclusive drops outweigh the perceived loss of flexibility for many shoppers, a trend expected to deepen as the e-commerce app market matures.

Recurring billing is increasingly supported by the regulatory framework. Europe's Digital Markets Act prohibits the mandatory use of proprietary payment systems, thereby reducing the dominance of in-app commissions associated with transaction fees. E-commerce applications that integrate transaction income with subscription models experience a 30% decrease in revenue volatility, emphasizing the benefits of diversification.

By Platform: Mini-Programs Chip Away at the Duopoly

Android maintained 72.67% of the installed base in 2025, propelled by sub-USD 100 devices popular in Asia and Africa. iOS captured just 19% of downloads but 45% of GMV, driven by affluent user cohorts in North America and Europe. In 2025, WeChat boasted 4.5 million mini-programs on its super-app platform, collectively handling transactions worth USD 420 billion, marking an impressive 8.24% CAGR for the segment.

Mini-programs inherit parent-app credentials and payment methods, boosting retention compared with standalone apps, which lose 70% of new installs within 30 days. China’s regulators now require business license displays in mini-programs, raising compliance overhead while solidifying consumer trust. Although North American antitrust scrutiny chills super-app expansion, mini-program traction across Asia positions the format as a durable growth pillar in the e-commerce app market.

By Business Model: Resale Platforms Power Circular Growth

Business-to-consumer marketplaces accounted for 55.71% of 2025 revenue, offering an unmatched breadth of assortment but razor-thin seller margins of 3% to 5%. Peer-to-peer resale, advancing at an 8.41% CAGR, counters this dynamic by monetizing authentication services and carbon-offset badges rather than listing fees. In 2025, Depop's carbon-neutral checkout boosted average order values by 11%, highlighting the positive impact of sustainable initiatives on consumer spending behavior.

Business-to-business platforms are streamlining procurement processes. They utilize ERP APIs that automatically trigger reorders whenever inventory levels fall below set thresholds. However, regulatory duties vary across the board. For instance, resale applications bear the brunt of liabilities when it comes to counterfeit products. This challenge prompted Poshmark to implement advanced computer-vision filters, achieving an impressive 92% accuracy rate, ensuring listings are vetted before going live. Collectively, these models shed light on the fragmentation of value pools within the e-commerce application market.

By Product Category: Quick-Commerce Redefines Convenience

Fashion and apparel accounted for 28.66% of revenue in 2025, buoyed by frequent replenishment and social media-inspired loops. Grocery and FMCG, however, are forecast to post a 9.11% CAGR as 10-minute delivery compresses last-mile costs through hyper-local dark stores. By late 2025, Zepto and Blinkit, both hailing from India, had set up 800 micro-fulfillment centers, seizing 12% of the grocery expenditure in Mumbai and Bengaluru.

Trade-in programs play a significant role in facilitating the recovery of secondary-market value for electronics and media sales within brand ecosystems. These programs not only enhance the lifecycle of products but also contribute to sustainable practices by encouraging reuse and recycling. Each vertical strategically adapts technology to address specific challenges and consumer needs, thereby underscoring the segmentation depth and innovation within the e-commerce app market.

Geography Analysis

Asia-Pacific generated 42.48% of 2025 revenue, as China’s super-app ecosystems embedded retail, payments, and social networking into a single platform, processing 4.5 million daily mini-program transactions. India’s Unified Payments Interface cleared 11.6 billion monthly transactions, enabling even street vendors to accept QR-code payments through Paytm and PhonePe. Southeast Asia’s live-stream commerce hit USD 180 billion in GMV, compressing discovery-to-purchase cycles to sub-100 seconds.

North America held a 28% share in 2025, with the United States contributing USD 820 billion as Amazon Prime’s 180 million domestic members fueled one-day shipping economics. Mexico’s app penetration jumped to 48% on the back of MercadoPago micro-loans that extend credit to unbanked consumers. California’s Consumer Privacy Act curtailed third-party data sharing, forcing a pivot toward contextual ad strategies across the e-commerce app market.In accordance with the Digital Markets Act, Europe mandated interoperable payments, resulting in an 8 to 12 percentage point reduction in gatekeeper take rates, thereby benefiting third-party developers. Following Brexit, customs frictions extended delivery times in the United Kingdom by 5 days, necessitating dual-fulfillment footprints and consequently increasing logistics costs. While Russia encountered challenges due to payment-network sanctions, these were partially mitigated by the country's domestic Mir rails.

Africa is the fastest-growing region at an 8.89% CAGR, propelled by mobile-money interoperability that cuts cross-border fees from 7% to under 1%. Jumia adopted a 60% cash-on-delivery model in Nigeria and Egypt, deploying GPS-tagged drop-off points where formal addresses are scarce. Implementation lags under the African Continental Free Trade Area still leave customs clearance at 7-10 days, a barrier ripe for digital brokers. Brazil’s Pix processed 3.2 billion monthly instant-payment transactions, evaporating three-day settlement lags. MercadoLibre’s 1,800 fulfillment sites now enable next-day delivery in major metros, raising service expectations across the region. Argentina’s consumers lean on installment plans to hedge against inflationary erosion, underscoring macro volatility’s sway over the e-commerce app market.

Middle East markets reached 48% penetration in 2025, buoyed by mandates requiring businesses with annual revenue above SAR 1 million to accept digital payments. Noon and Amazon.ae compete on same-day service despite the 45-degree Celsius summers that challenge perishable logistics. The UAE's VAT-refund app allows tourists to instantly reclaim taxes on eligible purchases, providing a seamless and efficient process. This initiative has significantly contributed to a 14% increase in luxury app purchases, highlighting its positive impact on consumer spending within the country.

Competitive Landscape

Moderate fragmentation defines the e-commerce app market. The top five players - Amazon, Alibaba, Shopify, Walmart, and JD - command 38% of 2025 revenue, while regional champions such as MercadoLibre, Jumia, and Flipkart dominate local niches by tailoring logistics and payment rails to on-the-ground realities. Horizontal super-apps aggregate ride-hailing, food, and retail under a single login, whereas vertical specialists own farm-to-doorstep supply chains.

Alibaba’s unified commerce protocol synchronizes 1.2 billion SKU updates daily, routing orders to the nearest node within 80 milliseconds, a scale that erects technical barriers for newcomers. Quick-commerce disruptors Zepto and Blinkit exploit 15-minute grocery windows to capture urban top-up missions, compelling traditional grocers to launch comparable offerings. Shopify’s AI discovery tool, rolled out mid-2025, lifted cart sizes by 18% without incremental acquisition spend, highlighting the technology’s leverage for margin expansion.

Privacy-by-design architectures now separate leaders from laggards in markets where data stewardship sways consumer trust. Platforms that encrypt data in transit and trim retention windows post 22% higher trust scores in shopper surveys and face 40% lower legal exposure to privacy fines. As regulations tighten in the e-commerce app market, this compliance advantage may expand, providing companies adhering to these standards with a stronger competitive position and increased consumer trust.

E-commerce App Industry Leaders

Amazon.com, Inc.

eBay Inc.

Walmart Inc.

Alibaba Group Holding Limited

Shopify Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Shopify and TikTok enabled one-click checkout for TikTok Shop merchants across North America and Europe, reducing manual reconciliation by 85%.

- November 2025: Alibaba invested USD 1.2 billion to add 120 Southeast Asian fulfillment centers, cutting last-mile costs by 18%.

- October 2025: Walmart acquired Zeekit for USD 340 million, integrating virtual try-ons that lowered apparel return rates 14 percentage points.

- September 2025: MercadoLibre launched MercadoPago credit cards with 3% cashback, enrolling 4.2 million customers in 90 days.

Global E-commerce App Market Report Scope

The E-commerce App Market Report is Segmented by Type (In-app Purchases, Advertisements, Subscription Fees, Transaction Fees, Freemium Upsell), Platform (Android, iOS, Super-App Mini-Programs), Business Model (B2C Marketplace, B2B Marketplace, C2C/Peer-to-Peer, Direct-to-Consumer Brand App), Product Category (Fashion and Apparel, Electronics and Media, Grocery and FMCG, Home and Furniture, Health and Beauty, Other Product Categories), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| In-app Purchases |

| Advertisements |

| Subscription Fees |

| Transaction Fees |

| Freemium Upsell |

| Android |

| iOS |

| Super-App Mini-Programs |

| B2C Marketplace |

| B2B Marketplace |

| C2C / Peer-to-Peer |

| Direct-to-Consumer Brand App |

| Fashion and Apparel |

| Electronics and Media |

| Grocery and FMCG |

| Home and Furniture |

| Health and Beauty |

| Other Product Categories |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Type | In-app Purchases | ||

| Advertisements | |||

| Subscription Fees | |||

| Transaction Fees | |||

| Freemium Upsell | |||

| By Platform | Android | ||

| iOS | |||

| Super-App Mini-Programs | |||

| By Business Model | B2C Marketplace | ||

| B2B Marketplace | |||

| C2C / Peer-to-Peer | |||

| Direct-to-Consumer Brand App | |||

| By Product Category | Fashion and Apparel | ||

| Electronics and Media | |||

| Grocery and FMCG | |||

| Home and Furniture | |||

| Health and Beauty | |||

| Other Product Categories | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the e-commerce app market in 2026 and what growth is expected?

The e-commerce app market size stood at USD 3.48 trillion in 2026 and is projected to reach USD 5.07 trillion by 2031, reflecting a 7.82% CAGR.

Which platform leads global installs?

Android dominated with 72.67% of installs in 2025, benefiting from low-cost smartphones across Asia, Africa and Latin America.

What segment is growing fastest by revenue model?

Subscription fees are forecast to expand at an 8.82% CAGR through 2031 as consumers opt for all-you-can-ship memberships and ad-free browsing.

Which region shows the highest growth momentum?

Africa posts the fastest regional CAGR at 8.89%, propelled by interoperable mobile-money systems that slash cross-border fees.

How are 5G networks influencing mobile commerce?

5G’s single-digit-millisecond latency enables augmented-reality try-ons and sub-50 millisecond checkout windows, raising conversion rates up to 22% in visual categories.

What regulatory change most impacts advertising revenues?

Apple’s App Tracking Transparency framework cut global opt-in rates to 25%, reducing cross-app targeting and costing major platforms billions in ad revenue.

Page last updated on: