Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

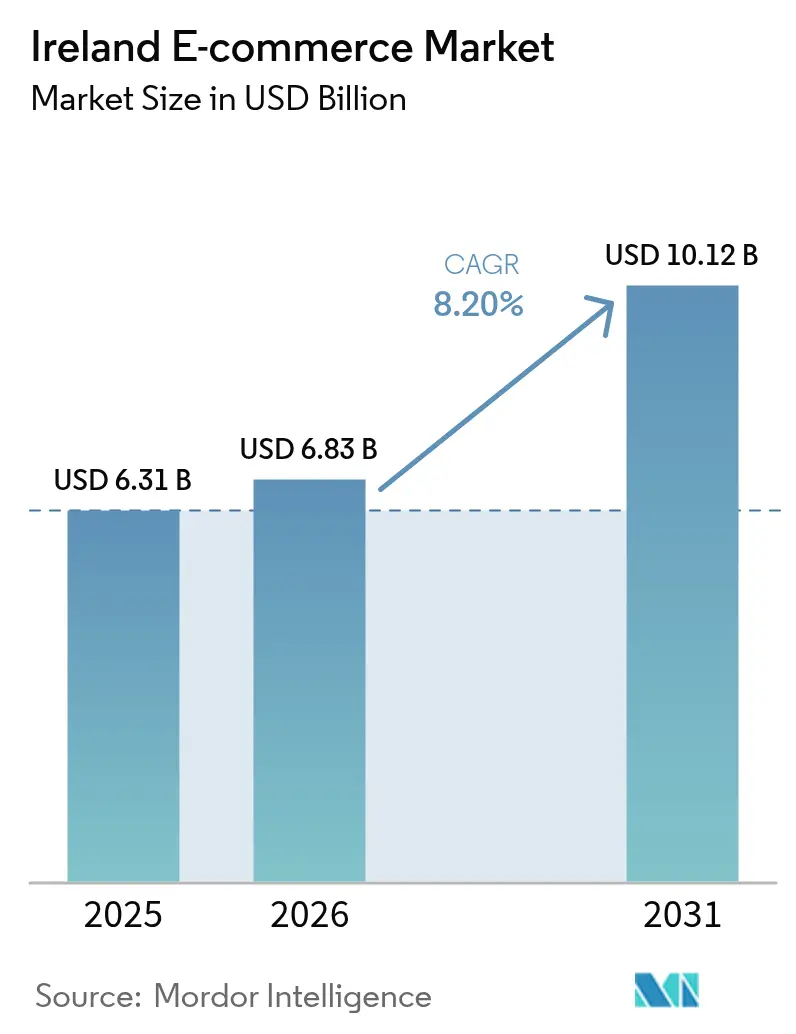

| Base Year Market Size (2025) | USD 6.31 Billion |

| Market Size (2026) | USD 6.83 Billion |

| Market Size (2031) | USD 10.12 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

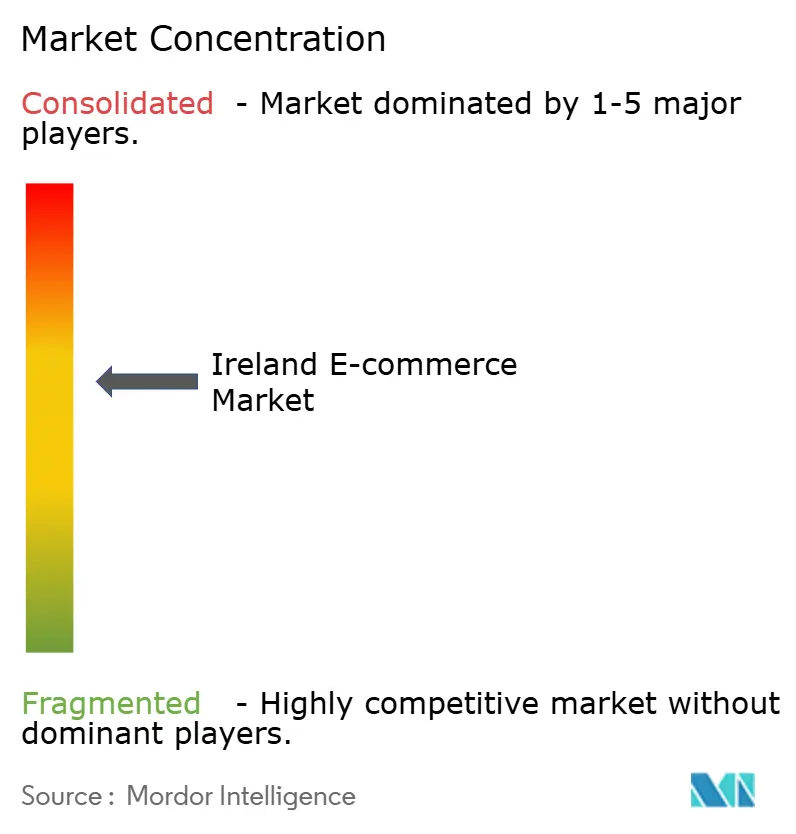

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland E-commerce Market Analysis by Mordor Intelligence

The Ireland e-commerce market size is expected to grow from USD 6.31 billion in 2025 to USD 6.83 billion in 2026 and is forecast to reach USD 10.12 billion by 2031 at 8.2% CAGR over 2026-2031. Demand momentum is underpinned by government programs that treat the digital economy as a strategic growth pillar worth the equivalent of 13% of national GDP.[1]International Trade Administration, “Ireland - Digital Economy,” trade.gov Ireland’s unique position as an English-speaking, euro-denominated gateway between the EU and the UK adds further upside, especially after Brexit complicated direct UK-to-EU e-commerce flows. Same-day delivery roll-outs by An Post and global players such as Amazon have reset consumer expectations around speed, pushing average order values higher and encouraging omnichannel investments by domestic retailers.[2]An Post, “Online Shopping and Returns,” anpost.com An SME-focused policy mix—led by Grow Digital vouchers, tax credits and advisory hubs—is rapidly closing the technology adoption gap, with two-thirds of small firms now at basic digital intensity and almost the same share experimenting with AI and cloud tools. On the consumer side, raised contactless limits and the surge of Buy-Now-Pay-Later (BNPL) options are translating into larger basket sizes and materially lower cart-abandonment rates, while tighter EU consumer-rights rules have pushed trust indicators to historic highs.

Key Report Takeaways

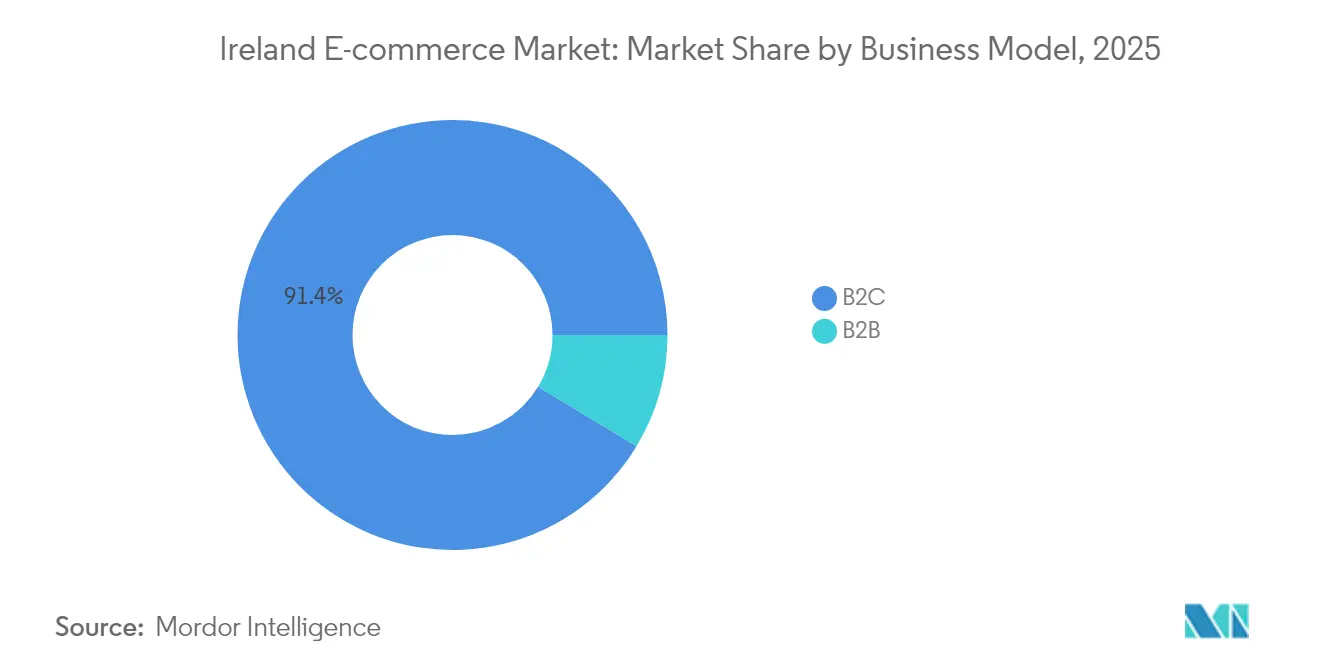

- By business model, the B2C segment held 91.35% of the Ireland e-commerce market share in 2025; B2B is projected to expand at a 12.4% CAGR to 2031.

- By device type, smartphones and tablets accounted for 67.10% of the Ireland e-commerce market size in 2025, with a 10.3% CAGR outlook through 2031.

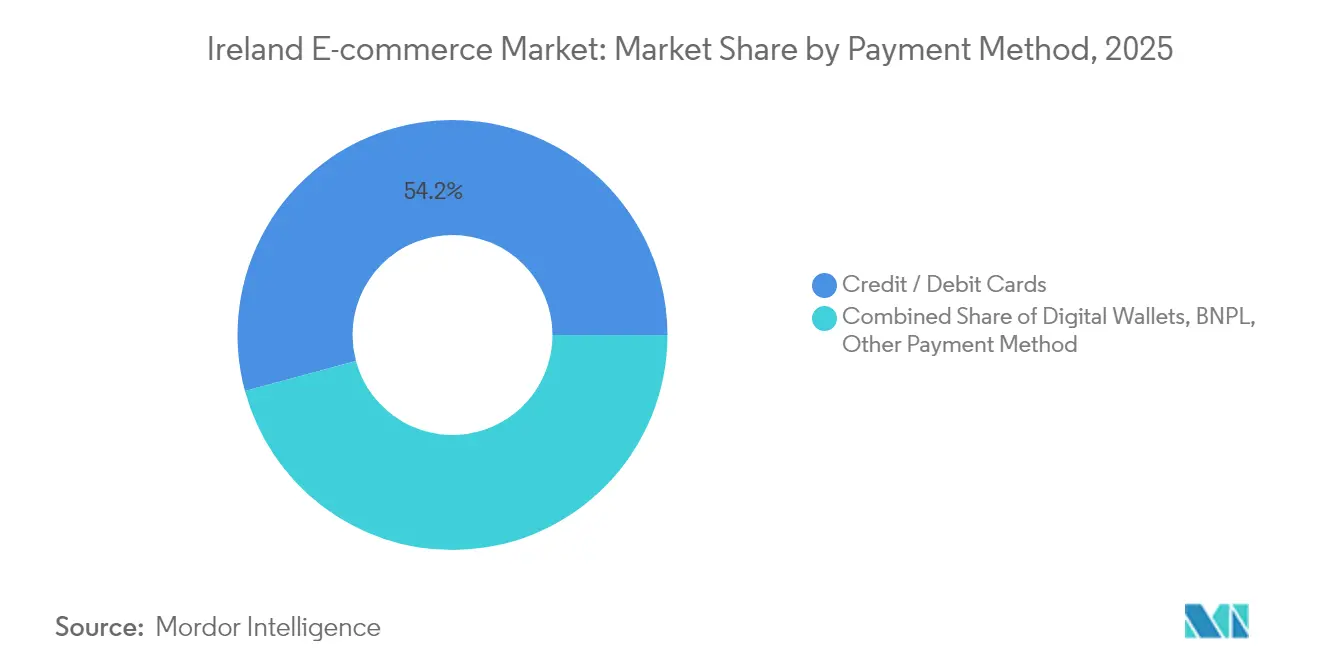

- By payment method, credit and debit cards retained 54.20% share of the Ireland e-commerce market size in 2025, while BNPL is advancing at a 13.1% CAGR to 2031.

- By B2C product category, fashion & apparel led with 26.40% revenue share in 2025, whereas beauty & personal care is the fastest-growing segment at a 11.8% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ireland E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of same-day delivery infrastructure across Irish urban centres | +1.8% | Dublin, Cork, Galway metropolitan areas | Short term (≤ 2 years) |

| Revised EU Digital Consumer Rights Directive boosting online consumer trust | +1.2% | National, with stronger impact in rural areas | Medium term (2-4 years) |

| Rapid increase in contactless debit-card limits driving higher AOV | +0.9% | National, concentrated in urban centers | Short term (≤ 2 years) |

| National Digital Strategy 2030 grants accelerating Irish SME webshop onboarding | +1.5% | National, prioritizing rural and underserved regions | Long term (≥ 4 years) |

| Buy-Now-Pay-Later adoption among millennials and Gen-Z shoppers | +1.1% | National, skewing toward 18-35 demographic clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Same-Day Delivery Infrastructure Across Irish Urban Centres

An Post, DPD and Fastway jointly operate 47 automated sortation sites and 312 parcel lockers, enabling retailers to promise same-day fulfilment to 2.1 million households that place orders before 14:00. Average order value for these orders is 23% higher than standard-delivery baskets, pushing omnichannel incumbents such as SuperValu to pilot micro-fulfilment robotics for inventory accuracy. The Ireland e-commerce market therefore enjoys metropolitan service levels comparable to the most advanced EU peers, yet rural customers remain on 2-3-day lead times, preserving scope for further growth.

Revised EU Digital Consumer Rights Directive Boosting Online Consumer Trust

The post-2024 rollout of the Digital Services Act (DSA) increased Irish consumer trust in online shopping to 78%, up from 65% a year earlier, as dispute-resolution times fell and chargebacks dropped 31%.[3]European Commission, “A Europe Fit for the Digital Age,” ec.europa.eu Oversight is split between media-regulator Coimisiún na Meán and the Competition & Consumer Protection Commission, providing a dual-layer enforcement structure that international platforms now view as a competitive advantage rather than a compliance cost. The Ireland e-commerce market thereby benefits from a trust dividend that directly lowers acquisition spend.

Rapid Increase in Contactless Debit-Card Limits Driving Higher AOV

Bank of Ireland data show a 34% surge in contactless volumes after the limit moved to EUR 50 (USD 54) in 2025. Instant settlement rails championed by the Central Bank have removed payment-friction points that historically deterred large online purchases. Digital wallets already represent 29% of all card transactions, and their mobile-first UX delivers conversion rates 18% above static card entry flows.

National Digital Strategy 2030 Grants Accelerating Irish SME Webshop Onboarding

Grow Digital vouchers distributed EUR 47 million (USD 51 million) to 9,400 SMEs in 2024, covering platform build-outs and digital marketing spend. Enterprise Ireland’s Digital-for-Business advisory added technical expertise to 3,200 firms, with 85% launching live web shops within six months. As a result, Ireland e-commerce market participation among SMEs now generates 30% of their total sales, outpacing the EU benchmark of 20%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Brexit customs frictions raising delivery cost & transit time from UK sellers | -1.4% | National, with higher impact on border counties | Long term (≥ 4 years) |

| High last-mile logistics cost in rural West & Northwest counties | -0.8% | Connacht and Ulster regions primarily | Medium term (2-4 years) |

| Recurrent e-commerce cyber-breaches eroding shopper confidence | -0.6% | National, concentrated in high-value transaction segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-Brexit Customs Frictions Raising Delivery Cost & Transit Time From UK Sellers

Extra customs paperwork and EUR 8-15 (USD 9-16) handling fees per shipment add 2-4 days of latency on UK orders, cutting UK-to-Ireland cross-border volumes 27% since 2024. Many UK merchants have exited the market rather than navigate VAT thresholds below EUR 135 (USD 146), leading Irish consumers to source more goods from EU suppliers.

High Last-Mile Logistics Cost in Rural West & Northwest Counties Hinders Market

Despite the National Broadband Plan’s rollout to 544,000 premises, parcel carriers face 40-60% higher per-stop costs in Leitrim and neighbouring counties because of low drop densities and difficult terrain. Shared-delivery pilots remain fragmented, prolonging a two-speed Ireland e-commerce market in which rural cart conversion lags urban norms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Acceleration Outpaces B2C Maturation

B2C transactions continued to dominate with a 91.35% share in 2025, yet B2B volumes are on course for a 12.4% CAGR through 2031 as manufacturing and services firms digitalise procurement. This interplay suggests that the Ireland e-commerce market size for B2B could approach a fifth of total GMV by decade-end. Enterprise Ireland subsidies and high SME cloud adoption rates underpin the trend, while Applied Nutrition’s 39% European growth demonstrates how digital wholesale channels bypass legacy distributors.

B2C growth is steady rather than explosive, helped by mobile checkout speeds that already capture 65% of all consumer orders. Government white-paper progress reports show 85% of digital-transformation milestones on track, implying further efficiency gains for both sides of the marketplace.

By Device Type: Mobile Dominance Drives Infrastructure Investment

Smartphones and tablets owned 67.10% traffic share in 2025 and are set to expand at 10.3% CAGR as 5G coverage matures. That places the device segment on course to account for roughly 74% of the Ireland e-commerce market size by 2031. The drive for low-latency commerce has spurred edge-computing nodes in metropolitan clusters, while desktop remains relevant for large-ticket B2B orders where specification review is more involved.

Voice assistants and smart TVs are still niche, but early adopters are experimenting with conversational commerce, pointing to new touchpoints for marketers who need to reach screen-agnostic consumers.

By Payment Method: BNPL Disrupts Traditional Card Dominance

Cards still process 54.20% of 2025 GMV, yet BNPL’s 13.1% CAGR outlook would move its share into the mid-teens by 2031, fuelled by transparent fee structures and embedded checkout UX. Digital wallets benefit from PSD2 open-banking rails, while the coming digital euro promises instant transactions that could compress merchant fees further. The Ireland e-commerce market share held by legacy cards will remain sizeable but less dominant as multi-rail payment orchestration becomes the norm.

By B2C Product Category: Beauty Emerges as Growth Leader

Fashion & apparel delivered 26.40% of consumer GMV in 2025, but beauty & personal care is the volume-weighted growth engine at a 11.8% CAGR. Hybrid work lifestyle keeps consumer electronics resilient, while on-demand food delivery platforms widen the addressable market for groceries. The Ireland e-commerce market size for discretionary categories therefore rides both self-care premiumisation and convenience demand, with omnichannel loyalty programs such as Levi’s Red Tab creating stickier customer relationships.

Geography Analysis

The domestic market boasts internet penetration above 95%, placing Ireland in the EU’s top quartile. Dublin alone generates roughly 40% of online turnover thanks to multinational tech clusters, a deep talent pool and dense last-mile networks. Cork and Galway form the next tier, aided by university ecosystems that accelerate digital-native consumption patterns.

Rural regions benefit from high-speed broadband but still pay 40-60% delivery premiums, a pricing delta that depresses transaction frequency. The Ireland e-commerce market size measured on a per-capita basis is therefore materially higher in Leinster versus Connacht and Ulster, reinforcing the case for logistics partnerships that aggregate rural demand onto shared routes.

On the cross-border front, 38% of Irish consumers still buy internationally despite post-Brexit frictions, helped by EU Digital Markets Act harmonisation that makes continental purchases seamless. Amazon’s Irish domain launch in March 2025, with EUR-priced inventory and one-day delivery promises, underscores the island’s producer-and-consumer role as a UK-EU bridge.

Competitive Landscape

Competition remains intense but not yet winner-takes-all. Amazon’s local launch has escalated service-level expectations, yet domestic banners such as Tesco.ie and Currys.ie still defend share through click-and-collect convenience and local merchandising. SuperValu’s adoption of Tally shelf-scanning robots illustrates how traditional grocers weaponise technology to keep pace on stock accuracy and fulfilment speed.

Fintech innovation has become a battlefield differentiator. Wayflyer’s revenue-based financing model injects working capital into high-potential merchants, while Fiserv’s full takeover of AIB Merchant Services signals accelerating payment-stack consolidation. Market white space persists in rural fulfilment, B2B procurement and niche verticals that demand regulatory expertise, giving agile Irish startups room to manoeuvre before global giants pivot into those micro-segments.

Strategic moves now centre on ecosystem building rather than pure sales volume: parcel-locker alliances, embedded finance plays and multi-tenant marketplace platforms all feature prominently. The Ireland e-commerce market therefore trends toward service bundling, with logistics, payments and data analytics offered as integrated solutions that lock in both merchants and shoppers.

Ireland E-commerce Industry Leaders

Amazon.co.uk

Argos Distributors (Ireland) Limited

Tesco Ireland

Currys Ireland Limited

Littlewoods Ireland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fiserv completed its acquisition of AIB Merchant Services, combining acquiring, POS and value-added payment services under one roof to streamline merchant onboarding and strengthen cross-border processing capability.

- March 2025: Amazon launched a dedicated Irish e-commerce site, listing more than 200 million products in euros and pledging one-day delivery nationwide, a move that localises fulfilment and reduces currency-conversion friction for Irish shoppers.

- March 2025: Wayflyer acquired B2B marketplace MadeMeBuyIt for USD 1 billion, integrating transaction data from both sides of the buyer–supplier equation and boosting its risk-scoring accuracy for revenue-based lending.

- February 2025: Levi Strauss & Co. rolled out the Red Tab Member Programme in Ireland across 12 European markets, aiming to capture first-party data and drive repeat purchases via exclusive perks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Ireland eCommerce market as every domestic or cross-border purchase of goods and digitally delivered services completed by Irish consumers or enterprises through internet-enabled devices, valued at point of payment in US dollars (mordorintelligence.com).

Scope Exclusion: We exclude peer-to-peer classifieds, online gambling, and digital advertising revenues.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

We conduct structured interviews with marketplace operators, parcel integrators, payment processors, and SME web-store owners across Dublin, Cork, and Galway, which confirm average basket size, return rates, and BNPL uptake, and help us close gaps left by desktop work.

Desk Research

Our analysts first gather baseline metrics from tier-one public sources such as the Central Statistics Office, Eurostat Digital Economy tables, and ComReg connectivity releases, which show internet access, card usage, and broadband reach. Complementary insights come from trade associations like eCommerce Europe, Irish consumer sentiment trackers, and Volza shipment logs that hint at inflow peaks for apparel and electronics.

We then tap paid repositories including D&B Hoovers for merchant revenues and Dow Jones Factiva for news flows that flag flash-sales or VAT rule shifts, thereby sharpening growth inflection points. The sources noted are illustrative; many additional references inform data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down spend pool is built from national household outlays, eCommerce penetration, and cross-border leakage, and is then validated with sampled merchant gross merchandise value roll-ups. Key variables like smartphone share of checkouts, parcel density per capita, VAT changes, interchange caps, and euro-dollar shifts feed a multivariate regression that extends the model to 2030. Where bottom-up tallies diverge, we interpolate to align with reconciled totals.

Data Validation & Update Cycle

Outputs face two-tier analyst audits; anomalies trigger source re-runs, and the model is refreshed each year, with interim updates when policy or macro shocks alter demand.

Why Mordor's Ireland E-commerce Baseline Commands Reliability

Published estimates diverge, and we acknowledge that scope, currency choice, and refresh cadence drive those gaps. External studies put 2024 values between USD 6.17 billion and USD 18 billion, while a statistics portal lists USD 6.20 billion for 2025.

Our disciplined scope, transparent variables, and yearly updates keep Mordor's view steady for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.31 bn (2025) | Mordor Intelligence | |

| USD 6.17 bn (2024) | Regional Data Platform A | Counts only web-shop revenue, omits in-app sales |

| USD 18 bn (2024) | Global Consultancy B | Bundles B2B portals and ticketing spend |

| USD 6.20 bn (2025) | Statistics Portal C | Uses constant euros, lacks cross-border adjustment |

The comparison shows that once differing inclusions and currency treatments are stripped away, Mordor's balanced build, anchored to verifiable consumption indicators and refreshed every year, delivers the most repeatable baseline for investors and planners.

Key Questions Answered in the Report

What is the current value of the Ireland e-commerce market?

The Ireland e-commerce market is valued at USD 6.83 billion in 2026 and is projected to hit USD 10.12 billion by 2031.

Which business model is expanding fastest?

B2B e-commerce is forecast to grow at a 12.4% CAGR to 2031, outpacing the mature but still dominant B2C segment.

Why is BNPL important in Ireland?

BNPL solutions are expanding at a 13.1% CAGR as millennials and Gen Z favour interest-free instalments over traditional revolving credit.

How significant is mobile commerce?

Smartphones and tablets account for 67.10% of online transactions today and are on course for a 10.3% CAGR, driven by 5G and mobile-wallet adoption.

What barriers limit rural e-commerce adoption?

Higher last-mile delivery costs—up to 60% above urban rates—and fewer parcel-locker locations keep rural conversion rates below urban benchmarks.

How has Brexit affected Ireland’s online retail?

Customs fees and longer transit times have reduced UK-origin orders by 27%, pushing Irish shoppers toward EU suppliers and domestic platforms.

Page last updated on: