Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

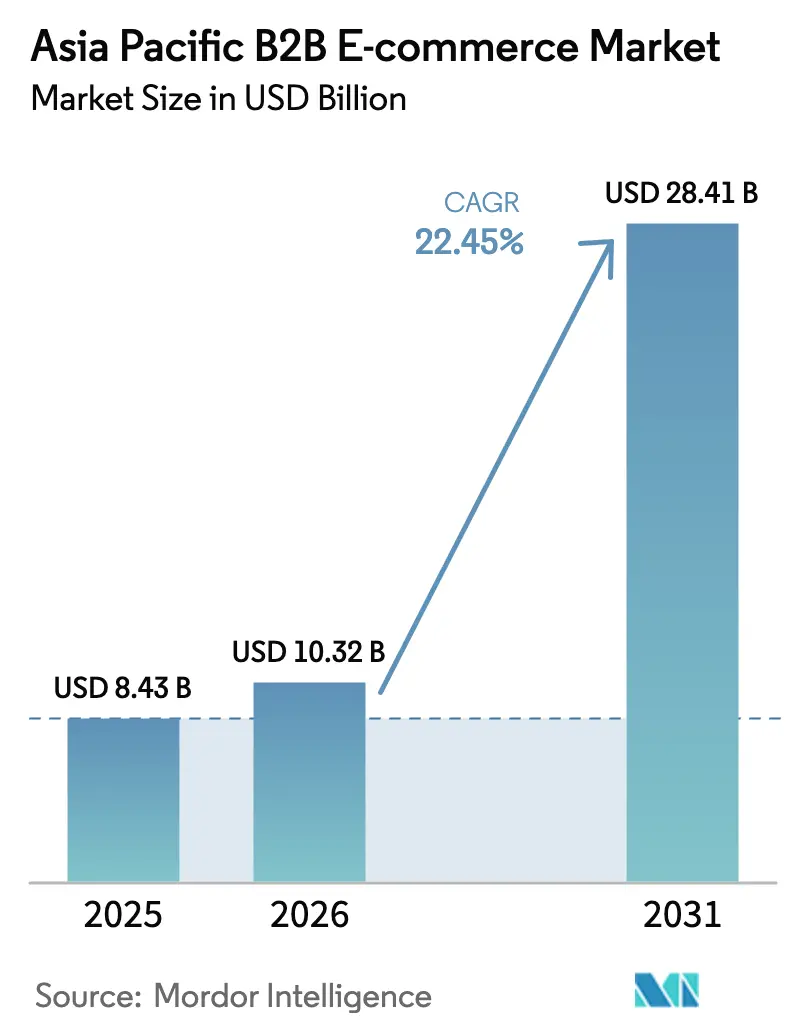

| Base Year Market Size (2025) | USD 8.43 Billion |

| Market Size (2026) | USD 10.32 Billion |

| Market Size (2031) | USD 28.41 Billion |

| Growth Rate (2026 - 2031) | 22.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific B2B E-commerce Market Analysis by Mordor Intelligence

Asia-Pacific B2B e-commerce market size in 2026 is estimated at USD 10.32 billion, growing from 2025 value of USD 8.43 billion with 2031 projections showing USD 28.41 billion, growing at 22.45% CAGR over 2026-2031. This rapid expansion reflects an irreversible pivot by enterprise buyers toward digital procurement and payment flows, supported by embedded-finance rails that unlock USD 242 billion of fresh working-capital capacity for small and medium enterprises (SMEs). Digitization momentum is further amplified by mandatory e-invoicing regimes across several economies, fiber-to-factory connectivity breakthroughs, and rising pressures to de-risk supply chains after pandemic-era disruptions. As corporations chase cost savings and cycle-time reductions, digital marketplaces are evolving into platforms that meld procurement, financing, and logistics-all in real time. Nevertheless, structural frictions around tax compliance, cross-border documentation, and payment-trust gaps in Tier-2/3 cities temper the market’s otherwise steep growth curve.

Key Report Takeaways

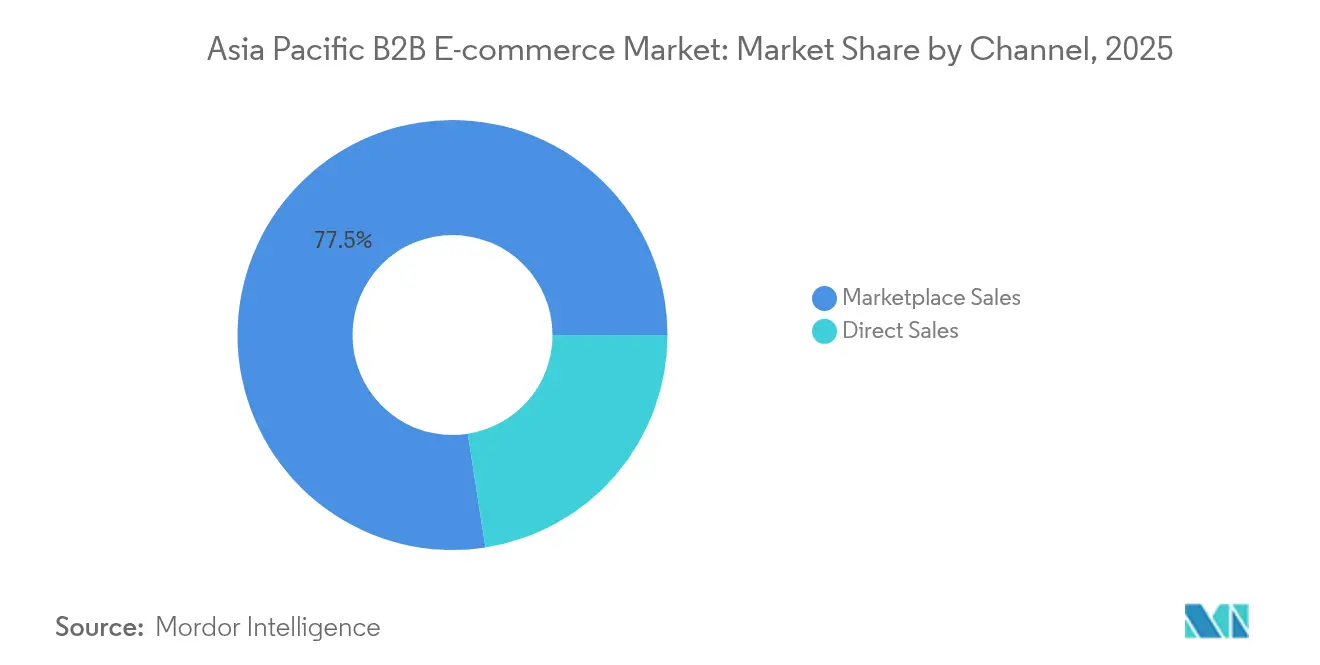

- By channel, marketplace sales accounted for 77.45% of the Asia-Pacific B2B e-commerce market share in 2025, while direct sales channels are advancing at a 24.8% CAGR through 2031.

- By transaction model, domestic orders controlled 69.20% of the Asia-Pacific B2B e-commerce market size in 2025; cross-border flows are expanding at 26.1% CAGR to 2031.

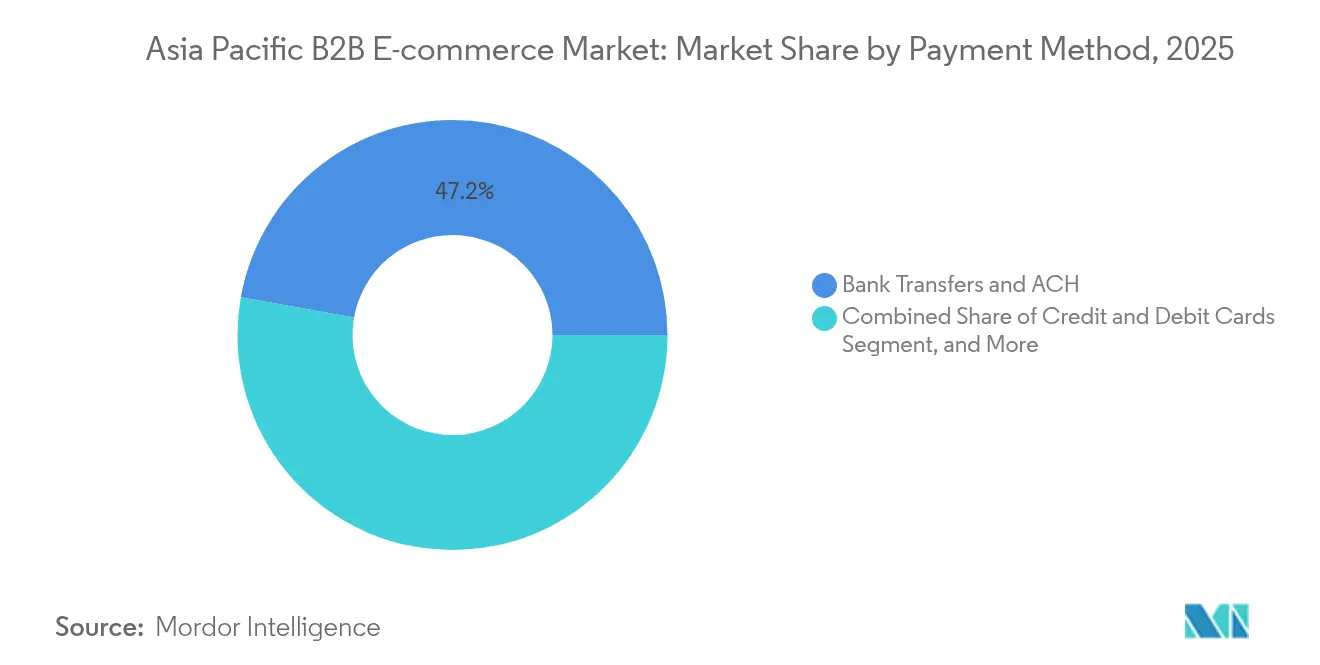

- By payment method, bank transfers held 47.20% of the Asia-Pacific B2B e-commerce market size in 2025; e-wallets, BNPL, and embedded-finance options are the fastest-rising cluster at 23.9% CAGR.

- By industry vertical, manufacturing led with 27.40% Asia-Pacific B2B e-commerce market share in 2025, whereas healthcare and life sciences will post the strongest 26.9% CAGR to 2031.

- By country, China dominated with 61.10% Asia-Pacific B2B e-commerce market share in 2025; India is forecast to post a 24.7% CAGR and emerge as the principal share-gainer by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific B2B E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital procurement adoption among APAC manufacturing SMEs | +3.8% | China, India, Southeast Asia manufacturing hubs | Medium term (2-4 years) |

| Government-led e-invoicing mandates (PEPPOL, GST) | +2.9% | Singapore, Australia, Japan, India | Short term (≤ 2 years) |

| 5G & fiber roll-out enabling real-time marketplaces | +2.4% | South Korea, Japan, urban China, Singapore | Medium term (2-4 years) |

| Embedded finance APIs de-risking B2B credit | +3.1% | India, Southeast Asia, emerging APAC markets | Long term (≥ 4 years) |

| Sustainability-driven paperless procurement targets | +1.6% | Japan, Australia, multinational corporations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital procurement adoption among APAC manufacturing SMEs

Manufacturing SMEs are abandoning manual requisition and phone-based ordering workflows as raw-material price volatility averaged 15-20% during 2024, forcing tighter spend controls. Vendors such as ProcMart lifted revenue from INR 2.2 billion (USD 0.026 billion) to INR 6.2 billion (USD 0.072 billion) in FY 2024 by delivering catalog search, spend analytics, and dynamic contract updates that trim purchase-order cycle times by up to 60%. While Tier-1 industrial corridors digitize at speed, penetration lags in Tier-2/3 districts where relationship-based buying remains entrenched.

Government-led e-invoicing mandates drive market acceleration

Singapore’s nationwide PEPPOL network processed 1.2 million invoices from 50,000 firms by 2024, turning compliance into a catalyst for platform onboarding. India’s GST e-invoicing clauses create a similar domino effect, pushing even micro-enterprises onto digital rails to remain eligible suppliers. Interoperable frameworks under the coming ASEAN.[1]Asia-Pacific Economic Cooperation, “Paperless Trade Platforms in the Post-COVID-19 Era,” apec.org Digital Economy Framework Agreement aim at USD 1 trillion digital-economy value by 2030, with e-invoicing interoperability as a pillar. Network externalities will intensify as large buyers refuse non-compliant paper invoices.

5G infrastructure enables real-time marketplace dynamics

Ultra-low latency 5G networks are transforming B2B marketplaces from static catalog platforms into dynamic pricing environments that mirror financial trading systems. South Korea's advanced 5G deployment enables real-time inventory visibility across supply chains, allowing manufacturers to adjust procurement strategies based on live supplier capacity data.[2]GSMA, “Mobile Economy Asia-Pacific 2023,” gsma.com This technological capability is particularly valuable for just-in-time manufacturing models where procurement timing directly impacts production efficiency. Real-time marketplaces also enable sophisticated auction mechanisms for commodity procurement, where suppliers can bid dynamically based on current capacity and input costs. The infrastructure investment is substantial, with mobile operators across APAC investing heavily to support 5G coverage that will account for 41% of total mobile connections by 2030. However, the B2B applications extend beyond connectivity to encompass IoT-enabled supply chain monitoring and automated procurement triggers based on inventory sensors.

Embedded finance APIs democratize B2B credit access

Real-time transaction scoring allows marketplaces to extend instant net-30 or net-60 terms without bearing direct credit exposure. HSBC’s API ties into platform checkout flows so that trade-finance limits auto-populate at cart confirmation, shrinking paperwork from weeks to minutes. The democratization is most visible in Southeast Asia, where mobile-first fintech uptake is projected to pass 60% by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented ASEAN tax & import compliance | -2.1% | ASEAN member states, cross-border operations | Medium term (2-4 years) |

| Low digital-payment trust in Tier-2/3 markets | -1.7% | Rural India, Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| High logistics cost for bulky MRO goods | -1.4% | Industrial manufacturing regions, remote areas | Medium term (2-4 years) |

| Vendor lock-in concerns among Japanese conglomerates | -0.9% | Japan, South Korea enterprise markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented ASEAN tax and import compliance creates operational friction

Each ASEAN jurisdiction runs independent VAT rules, e-services levies, and invoice-clearance models. Marketplaces must embed jurisdiction-specific logic, inflating overheads and delaying vendor onboarding. Indonesia insists on real-time tax clearance for every invoice, whereas Singapore’s PEPPOL flow stays voluntary, forcing platforms to juggle two integration tracks. These disparities blunt the scale economies that typically accelerate network-effect growth.

Digital-payment trust deficits constrain Tier-2/3 market penetration

Procurement officers in rural districts still regard online escrow or wallet mechanisms as risky, preferring bank transfers or cash-on-delivery even for high-value B2B orders. Limited recourse options if disputes arise reinforce this caution. Research on Southeast Asian SMEs reveals that such trust gaps curb marketplace usage despite smartphone penetration approaching 80%. Platforms respond with localized field-sales teams and deferred-payment guarantees, but uptake remains slower outside metro areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Marketplace Dominance Faces Direct-Sales Disruption

Marketplace sales controlled 77.45% of the Asia-Pacific B2B e-commerce market in 2025, a legacy of buyer dependence on aggregated supplier directories. Direct-sales portals, however, are accelerating at 24.8% CAGR as procurement leaders pursue deeper integration with ERP and logistics systems. Large manufacturers launch private portals that permit granular price negotiations, minimizing marketplace fees and data leakage.

The shift also reflects embedded-finance adoption within supplier-managed storefronts, enabling flexible settlement terms identical to marketplace offerings without ceding margin. While discovery remains easier on horizontal marketplaces, strategic items with recurring volumes increasingly migrate to direct rails for tighter quality control. Over the forecast horizon, marketplaces will likely pivot toward value-added financing and fulfillment services to defend relevance.

By Transaction Model: Cross-Border Growth Outpaces Domestic Expansion

Domestic orders still account for 69.20% of the Asia-Pacific B2B e-commerce market size in 2025, but cross-border flows will rise faster at 26.1% CAGR, encouraged by tariff concessions under the Regional Comprehensive Economic Partnership. Paperless trade protocols now shave 3.8% off administrative costs per shipment and cut border-clearance time by 6.7%.

Currency-hedging tools and automated duty calculators embedded within platforms lower the operational barrier for SMEs to sell regionally. Nevertheless, multidimensional compliance across VAT, import licensing, and data-localization laws remains burdensome, particularly for micro-exporters lacking legal resources. Thus, service providers offering bundled customs brokerage and tax-filing APIs stand to capture incremental revenue.

By Payment Method: Digital Wallets Reshape B2B Transaction

Traditional bank transfers and automated clearing house rails preserved a 47.20% share of the Asia-Pacific B2B e-commerce market in 2025 thanks to audit-trail familiarity and bank-ledger integration. Yet e-wallets, BNPL, and invoice-financing options will compound at 23.9% CAGR through 2031, mirroring consumer-grade expectations among millennial procurement managers. Real-time fraud engines and ISO 20022 messaging improve reconciliation accuracy, nudging CFOs to embrace wallet-based flows for mid-ticket purchases.

Bank-sponsored virtual-account solutions bridge the trust gap by combining wallet UX with traditional bank safeguards. Regulatory ambiguity over cross-border e-money passports still limits volume in conservative sectors such as defense or public procurement, but fintech sandboxes across Hong Kong, Singapore, and Australia are progressively clarifying licensing paths.

By Industry Vertical: Manufacturing Leadership Challenged by Healthcare Acceleration

Manufacturing maintained 27.40% Asia-Pacific B2B e-commerce market share in 2025 on the back of electronics, machinery, and automotive procurement complexity. Multi-tier BOM structures and frequent engineering changes make digital cataloging a necessity, which platforms like Zetwerk address through CAD-file matching and supplier qualification engines.

Healthcare and life sciences, however, will expand at 26.9% CAGR as regulators demand end-to-end traceability for devices, reagents, and pharmaceuticals. Digital platforms provide serialized tracking, temperature-controlled logistics visibility, and compliance documentation that manual workflows cannot match. Investment flows into med-tech hubs in Singapore and South Korea are catalyzing specialized B2B portals focusing on lab consumables and clinical-trial supplies.

Geography Analysis

China’s leadership stems from policy-driven digitization that integrated industrial parks with cross-border e-commerce channels and customs fast lanes. The Belt and Road Initiative broadens its supplier reach across Central and South Asia, reinforcing platform scale advantages. Heightened geopolitical scrutiny triggers supply-chain diversification, yet domestic consumption upgrades and enterprise procurement automation preserve double-digit growth.

India’s trajectory is propelled by policy nudges like compulsory GST e-invoicing, statewide fiber penetration, and the open-network movement that encourages interoperable digital commerce. SME onboarding accelerates as low-cost smartphones and vernacular interfaces lower entry barriers. The confluence of demographic dividend and manufacturing formalization will shift regional share to India by the end of the decade.

Japan, South Korea, Australia, and New Zealand represent mature nodes where penetration already hovers around 40-50%. Here, incremental growth derives from AI-driven demand forecasting, IoT-sourced automatic replenishment, and ESG-linked procurement scorecards. Meanwhile, the Rest of Asia–Pacific, particularly Indonesia, Vietnam, and the Philippines, provides the next wave of volume as regulatory frameworks approach convergence under the ASEAN Digital Economy Framework Agreement.

Competitive Landscape

Regional fragmentation characterizes the Asia-Pacific B2B e-commerce market. Alibaba’s 1688.com and Made-in-China.com dominate mainland flows, leveraging vertically integrated logistics and domestic financing instruments. IndiaMART and Zetwerk anchor the Indian sphere with deep roots in manufacturing clusters and localized compliance know-how. In Japan and South Korea, incumbents differentiate via high-fidelity data exchange and integration toolkits demanded by keiretsu and chaebol procurement teams.

Strategic competition is shifting from simple catalog breadth toward end-to-end workflow orchestration. Players invest in embedded-finance APIs, cross-border duty calculators, and AI-driven sourcing engines that suggest optimal suppliers based on lead-time volatility. Platform-native logistics capacity and ESG score-tracking modules are emerging as new battlegrounds.

Market-wide consolidation remains moderate because ASEAN tax heterogeneity erects natural borders. Yet capital-rich platforms pursue bolt-on acquisitions in niche verticals such as healthcare consumables or construction materials to gain specialized compliance capabilities. Successful acquirers are expected to merge disparate data silos, unlocking unified dashboards that underpin regional procurement centers of excellence.

Asia Pacific B2B E-commerce Industry Leaders

Alibaba Group Holding Ltd

Amazon.com, Inc.

Flipkart Online Services Pvt. Ltd.

IndiaMart InterMesh Ltd

eBay Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tata Technologies posted INR 51.68 billion (USD 620 million) in revenue with a 1% uptick, underscoring its pivot to software-defined manufacturing solutions that feed data into OEM-run B2B portals. The move aims to lock Tata’s automotive clients into integrated design-to-procurement ecosystems.

- April 2025: Avia Solutions Group reported EUR 2.7 billion (USD 2.92 billion) turnover, with 28.5% stemming from Asia-Pacific freight and MRO contracts. The company is bundling aviation logistics with e-commerce fulfillment to capture rising cross-border parts demand.

- February 2025: VTEX accelerated international rollout while upgrading its unified B2B/B2C commerce engine with AI-based catalog normalization, positioning it to serve multinational brands seeking single-stack deployments across APAC.

- December 2024: Sonepar divested Vallen Asia via management buy-out, freeing resources to double down on core electrical-distribution markets while giving Vallen autonomy to specialize in industrial consumables e-commerce across Southeast Asia.

Asia Pacific B2B E-commerce Market Report Scope

Business-to-business or B2B e-Commerce platforms allow buyers and suppliers to interact and arrange the deliverables leveraging the services offered by the platform. The scope of the report includes sales made through B2B e-commerce sites and e-procurement channels. However, EDI sales are not included as part of the scope.

The Asia Pacific B2B E-commerce market is segmented by Channel (Direct sales and Marketplace sales) and Country.

By Channel

| Direct Sales |

| Marketplace Sales |

By Transaction Model

| Domestic |

| Cross-border |

By Payment Method

| Bank Transfers and ACH |

| Credit and Debit Cards |

| Other Payment Methods |

By Industry Vertical

| Manufacturing |

| Retail and Wholesale |

| Healthcare and Life Sciences |

| Automotive |

| Construction and Building Materials |

| Other Industry Verticals |

By Country

| China |

| Japan |

| India |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Channel | Direct Sales |

| Marketplace Sales | |

| By Transaction Model | Domestic |

| Cross-border | |

| By Payment Method | Bank Transfers and ACH |

| Credit and Debit Cards | |

| Other Payment Methods | |

| By Industry Vertical | Manufacturing |

| Retail and Wholesale | |

| Healthcare and Life Sciences | |

| Automotive | |

| Construction and Building Materials | |

| Other Industry Verticals | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific B2B e-commerce market today?

The market is valued at USD 10.32 billion in 2026 and is tracking toward USD 28.41 billion by 2031, implying a 22.45% CAGR.

Which country contributes most to regional B2B e-commerce revenue?

China holds 61.10% of regional revenue owing to government-backed digitization and well-developed logistics corridors.

What is the fastest-growing segment within the market?

Cross-border transactions show the highest momentum at a 26.1% CAGR as RCEP tariff reductions and paperless trade standards take hold.

Why are embedded-finance tools critical to B2B platforms?

They enable real-time credit decisions, extend supplier payment terms, and unlock an estimated USD 242 billion in SME working-capital opportunity.

What are the key regulatory accelerators for adoption?

Mandatory e-invoicing frameworks such as PEPPOL and India’s GST network push suppliers to digitize invoices, driving broader platform onboarding.

Where do trust gaps still limit digital B2B payments?

Tier-2 and Tier-3 cities in India, Indonesia, and the Philippines show persistent skepticism of wallet-based payments, slowing adoption relative to metro areas.

Page last updated on: