Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

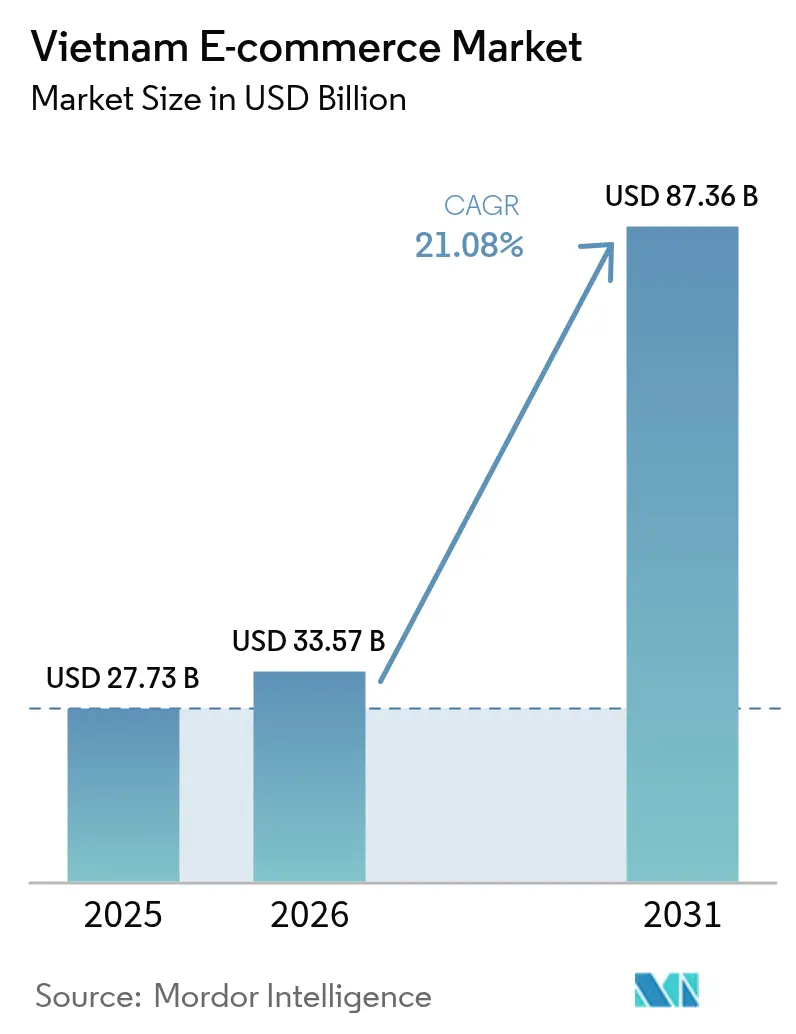

| Base Year Market Size (2025) | USD 27.73 Billion |

| Market Size (2026) | USD 33.57 Billion |

| Market Size (2031) | USD 87.36 Billion |

| Growth Rate (2026 - 2031) | 21.08% CAGR |

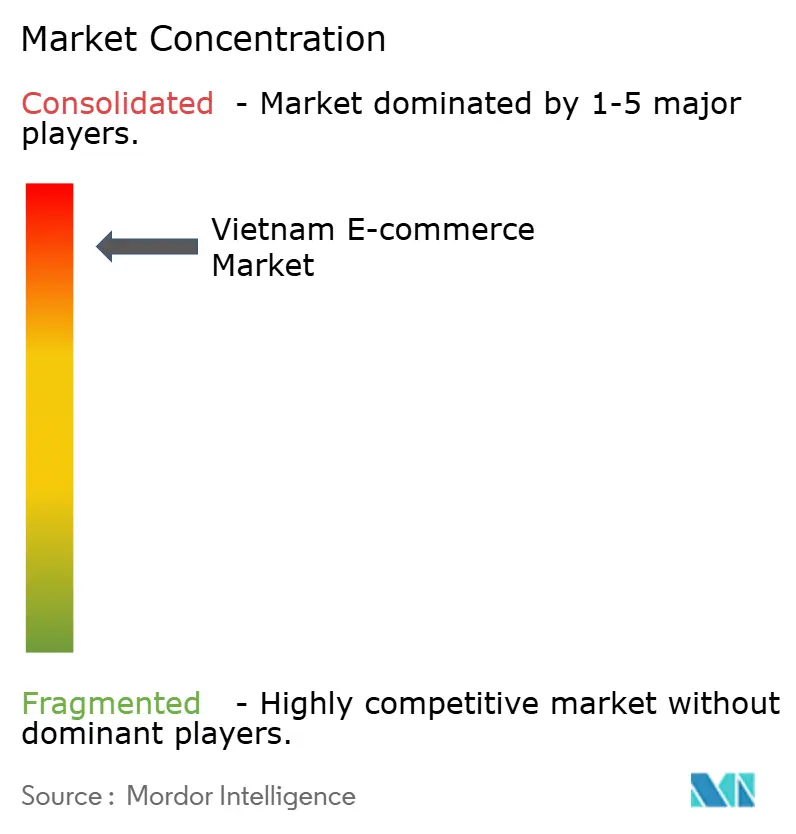

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam E-commerce Market Analysis by Mordor Intelligence

The Vietnam e-commerce market size is expected to grow from USD 27.73 billion in 2025 to USD 33.57 billion in 2026 and is forecast to reach USD 87.36 billion by 2031 at 21.08% CAGR over 2026-2031. Digital commerce now commands about 9% of total retail sales, underscoring how swiftly online channels are displacing traditional store formats.[1]Ministry of Industry and Trade, “Vietnam's E-Commerce Market Exceeds 25 Billion USD,” vietnamplus.vn Ongoing expansion springs from rapid mobile adoption, rising consumer trust in cash-free payments, and an ecosystem where social-commerce and short-video content have turned product discovery into entertainment. Government policies—most notably the National Cashless Payment Development Project—are accelerating non-cash transactions, while free-trade pacts such as the CPTPP and RCEP are drawing in a wave of cross-border sellers. Competitive intensity is sharpening as content-driven commerce narrows the field to a handful of dominant platforms, forcing smaller merchants to refine niche strategies or exit. On the infrastructure side, last-mile investments in tier-2 cities are shrinking delivery windows, further broadening the addressable base for the Vietnam e-commerce market.

Key Report Takeaways

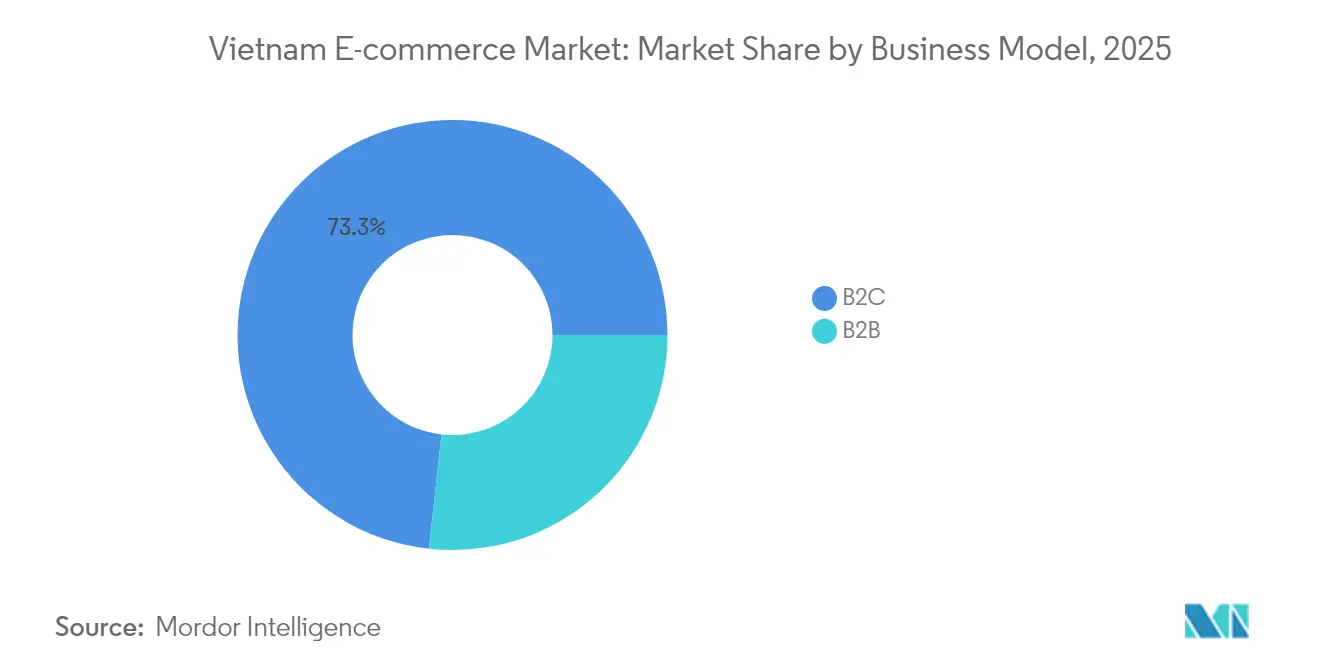

- By business model, B2C controlled 73.25% of Vietnam e-commerce market share in 2025, while B2B is forecast to compound at 21.75% through 2031.

- By device type, smartphones captured 71.10% revenue share of the Vietnam e-commerce market size in 2025; the mobile segment is advancing at an 18.1% CAGR to 2031.

- By payment method, credit and debit cards accounted for 29.40% share of the Vietnam e-commerce market size in 2025; BNPL is projected to grow at a 26.85% CAGR to 2031.

- By B2C product category, consumer electronics led with 26.35% of Vietnam e-commerce market share in 2025, while Food & Beverages is expanding at a 27.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide Adoption of Cashless Payments via National Cashless Payment Development Project 2021-2025 | +4.2% | National, with early gains in Hanoi, Ho Chi Minh City | Medium term (2-4 years) |

| Expansion of Last-mile Delivery Infrastructure into Tier-2 Cities | +3.8% | Tier-2 cities (Da Nang, Can Tho, Hai Phong, Nha Trang) | Medium term (2-4 years) |

| Surge in Social-Commerce Transactions via Short-Video Platforms | +5.1% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| Entry of Cross-border Sellers Leveraging CPTPP & RCEP FTAs | +2.9% | National | Long term (≥ 4 years) |

| Government-backed E-Invoicing Mandate (Circular 78) Boosting Trust | +1.5% | National | Medium term (2-4 years) |

| Rapid Growth in Quick-commerce Online Grocery | +3.2% | Urban centers (Ho Chi Minh City, Hanoi, Da Nang) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Nationwide adoption of cashless payments via the National Cashless Payment Development Project 2021-2025

Card-less transactions soared 63.3% in volume and 41.45% in value in early 2024, while QR code usage leapt nearly ten-fold.[2]Government of Vietnam, “Cashless Payment on the Rise in Viet Nam,” baochinhphu.vn Retail acceptance is now commonplace, with 79% of food-service outlets and 74% of stores offering digital options. Linking the National Population Database to payment rails streamlines checkout, lifting conversion rates and widening the Vietnam e-commerce market. By 2025, authorities expect e-commerce to account for half of all cashless payments, embedding a structural trust factor that reduces cart abandonment.

Expansion of last-mile delivery infrastructure into tier-2 cities

Logistics providers are rolling out urban consolidation centres that trim delivery times by up to 40% and support same-day service outside major hubs.[3]ITF-OECD, “Urban Logistics in Six Case Studies,” itf-oecd.org Trucks remain the backbone for inter-city hauls, while motorbikes excel in dense streets. Local authorities prioritise eco-friendly vehicles and digital route planning to relieve congestion. As delivery reliability improves, consumer confidence in the Vietnam e-commerce market strengthens, unlocking new cohorts in Da Nang and Can Tho that previously relied on cash-on-delivery.

Surge in social-commerce transactions via short-video platforms

TikTok Shop generated VND 36 trillion (USD 3.9 billion) of GMV in Q1 2025, a 113.8% jump year-on-year. Eighty-one percent of users say creator content directly shapes purchase decisions. Fashion and beauty dominate, showing how “shoppertainment” shifts engagement from keyword search to real-time discovery—an evolution propelling the Vietnam e-commerce market into a content-first era.

Entry of cross-border sellers leveraging CPTPP & RCEP free-trade agreements

Cross-border imports climbed 43% in 2024 to 324.1 million items valued at USD 568 million. Reduced tariffs and simplified customs are drawing brands that previously bypassed Vietnam. For domestic merchants, the same FTAs expand export reach, encouraging SMEs to list on global marketplaces and further integrate the Vietnam e-commerce market into regional supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Return Rates Elevating Fulfilment Costs | -2.1% | National, with higher impact in rural areas | Medium term (2-4 years) |

| Fragmented Cold-chain Logistics Limiting Fresh-Food Penetration | -1.8% | National, with higher impact outside major cities | Long term (≥ 4 years) |

| Escalating Digital-ad Costs Squeezing SME Margins | -2.4% | National | Short term (≤ 2 years) |

| Rural Broadband Reliability Causing Checkout Drop-offs | -1.9% | Rural areas, particularly in mountainous regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating digital-ad costs squeezing SME margins

Capturing just 1% of the Vietnam e-commerce market demands annual media spend near USD 6 million, a figure well beyond most local sellers. Active storefronts fell 6.2% between early 2023 and late 2024 as marketing bids spiralled on dominant marketplaces, lowering product variety and throttling innovation. SMEs are pivoting to micro-influencers, first-party data and community-led channels to stretch budgets, yet the near-term drag on growth remains.

Fragmented cold-chain logistics limiting fresh-food penetration

Cold storage is concentrated in top cities, leaving tier-2 regions underserved and fuelling post-harvest losses of 25–30% for fruit and vegetables. Ten structural gaps—ranging from workforce skills to IT traceability—curb reliable temperature control during last-mile fulfilment. Unless integrated solutions emerge, the food segment’s projected 28.4% CAGR could moderate, tempering the overall Vietnam e-commerce market outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B platforms accelerate beyond B2C leadership

B2C retained 73.25% of Vietnam e-commerce market share in 2025, yet the B2B segment is compounding at 21.75%-well above headline growth. Digital financing, ASEAN supply-chain integration and omnichannel procurement tools are persuading manufacturers and wholesalers to migrate spend online. The Vietnam E-commerce and Digital Economy Agency notes that MRO buyers in industrial zones are doubling their online order values each year, a trend that augments the Vietnam e-commerce market size for enterprise transactions.

Rising demand from tier-2 industrial parks is reshaping fulfilment. Sellers bundle financing and inventory-led models that guarantee delivery within two days, a timeline once reserved for B2C orders. Cross-border sourcing through CPTPP channels gives Vietnamese SMEs direct access to components at competitive terms, sharpening cost structures across export value chains. As adoption matures, the Vietnam e-commerce industry is poised to see B2B’s share climb toward 30% by decade-end.

By Device Type: Mobile commerce dominates user experience

Smartphones accounted for 71.10% of all orders in 2025 and are scaling at an 18.1% CAGR, ensuring mobile retains primacy in the Vietnam e-commerce market. Average data use per handset topped 12 GB a month, and 84% of residents held 4G connectivity. App-first strategies-lighter code, one-tap payments and embedded loyalty-translate directly into basket expansion.

Desktop traffic still matters for complex goods such as high-value electronics, but its relative weight is waning. Meanwhile, wearables and smart-TV commerce sit below 3% share yet exhibit promising double-digit growth as 5G rolls out. This multi-device environment pushes platforms to unify session data, creating cohesive experiences that nurture retention across the Vietnam e-commerce market.

By Payment Method: BNPL disrupts traditional mix

Cards commanded the largest stake at 29.40%, but BNPL’s 26.85% CAGR positions it as the game-changer for checkout flexibility. Gross merchandise value under BNPL reached USD 4.05 billion in 2025, thanks to partnerships such as Fundiin-Pharmacity and MoMo-Grab. Low credit-card penetration and a youthful demographic intersect to push alternative credit forward, broadening the Vietnam e-commerce market size for discretionary spending.

Regulators remain watchful, demanding clearer disclosure of fees and interest-equivalent charges. Providers counter by integrating repayment via automated wallet debits, lowering delinquency risks. For merchants, BNPL lifts average order values by 30-40%, counteracting the higher marketing costs that compress margins elsewhere in the Vietnam e-commerce industry.

By B2C Product Category: Food & Beverages lead digital transformation

Although consumer electronics held the largest 26.35% slice of Vietnam e-commerce market share in 2025, Food & Beverages is surging ahead at 27.25% CAGR. Quick-commerce models promise 30- to 60-minute delivery, converting habitual corner-store trips into online staples. Grocery basket frequency grew 72.8% in 2025, signalling mainstream comfort with chilled logistics reliability in top cities.

Beauty and personal-care categories thrive on creator-led tutorials, while cross-border consumer electronics vendors use tariff relief to extend price advantages. Fashion retains a natural home on video platforms, generating VND 23.4 trillion (USD 900 million) on TikTok Shop in Q1 2025 alone. Export-oriented furniture sellers are experimenting with augmented-reality fit-outs, reflecting how product-specific innovation keeps the Vietnam e-commerce market vibrant.

Geography Analysis

Ho Chi Minh City and Hanoi dominate transaction value, yet dynamic growth pockets are emerging in Da Nang, Can Tho, Hai Phong and Nha Trang as infrastructure matures. The Vietnam e-commerce market exceeded USD 27.73 billion in 2025, rising 19.4% year-on-year. Analysts foresee the Vietnam e-commerce market size reaching USD 33.57 billion by 2026 and USD 87.36 billion by 2031.

Urban adoption remains strongest: 60% of metropolitan households bought FMCG online in 2024, up from 29% in 2019. Rural zones still encounter checkout drop-offs tied to inconsistent broadband, yet a government-backed rural fibre programme promises to narrow gaps by 2028. Household internet access correlates with higher disposable income, indirectly widening the Vietnam e-commerce market’s consumer base.

Regionally, Vietnam stands third in Southeast Asia behind Indonesia and Thailand but boasts the region’s fastest compound growth. Trade pacts reposition the country as an export staging ground: nearly 400,000 Vietnamese sellers now list on cross-border platforms, logging 20-30% monthly sales expansion. The National E-Commerce Development Master Plan (2026-2030) targets USD 5.5 billion in online exports by 2027, a policy thrust that will further globalise the Vietnam e-commerce market.

Competitive Landscape

The Vietnam e-commerce market is now a two-horse race: Shopee and TikTok Shop jointly controlled 97% of GMV in Q1 2025. Shopee’s share slid from 68% to 62%, even as revenue climbed 11.3%, while TikTok Shop leapt to 35% through “shoppertainment” tactics. Domestic pioneer Tiki, hampered by capital constraints, now hovers near zero share after VNG’s strategic retreat.

Competitive levers are shifting from price subsidies to ecosystem services: next-day promises, loyalty wallets and creator-commerce studios. Shopee is co-launching YouTube Shopping to blunt TikTok’s influence, merging Google’s video reach with its logistics backbone. Government-backed niche portals such as Vietnam Post’s nongsan.buudien.vn target underserved agricultural segments, adding vertical depth without challenging incumbents head-on.

M&A chatter centres on logistics integration rather than marketplace consolidation, as fulfilment scale now underpins cost leadership. Cross-border challengers Temu and Shein are exploring local warehouses to shave delivery from weeks to days, testing the resilience of entrenched players. Against this backdrop, the Vietnam e-commerce market rewards platforms that combine captive media reach with embedded payments, creating sticky networks that deter multihoming.

Vietnam E-commerce Industry Leaders

Tiki Corporation

FPT Retail JSC (FPT Shop)

Shopee Pte. Ltd. (Sea Ltd)

Mobile World Investment Corp. (The Gioi Di Dong)

Lazada South East Asia Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Decree 70/2025 introduced new electronic invoicing rules, expanding compliance requirements for foreign e-commerce suppliers.

- February 2025: VNG exited management of Tiki after a VND 510 billion (USD 19 million) loss, though it retains a major shareholding.

- February 2025: The State Bank of Vietnam issued Directive 01/CT-NHNN to promote cashless payments and digital transformation in banking .

- January 2025: Vietnam's five largest e-commerce platforms (Shopee, Lazada, TikTok Shop, Tiki and Sendo) reported a combined GMV of VND 318.9 trillion (USD 12.6 billion) in 2024, a 37.36% increase from 2023.

Vietnam E-commerce Market Report Scope

E-commerce involves establishing connections and selling products, services, and information using computer communication networks. E-commerce often refers to the online trade of goods and services, which denotes a larger scale of economic activity. Internal organizational transactions that enable B2B and B2C transactions are included in e-commerce.

The Vietnam E-commerce market is segmented by b2c e-commerce (beauty and personal care, consumer electronics, fashion and apparel, food and beverage, furniture and home, Others [Toys, DIY, Media, etc.]), B2B e-commerce. The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

Key Questions Answered in the Report

What is the current value of the Vietnam e-commerce market?

The Vietnam e-commerce market size stands at USD 33.57 billion in 2026 and is forecast to reach USD 87.36 billion by 2031.

Which business model is growing fastest?

B2B platforms are expanding at a 21.75% CAGR, outpacing the traditional B2C segment even though B2C still holds 73.25% of market share.

How dominant is mobile commerce in Vietnam?

Smartphones generated 71.10% of 2025 transactions and are set to maintain leadership with an 18.1% CAGR through 2031.

Why is BNPL important in Vietnam’s payment mix?

With low credit-card penetration, BNPL offers flexible financing and is projected to grow at 26.85% CAGR, boosting average order values for merchants.

What challenges limit e-commerce growth in rural areas?

Intermittent broadband reliability and sparse cold-chain infrastructure lead to checkout drop-offs and restrict fresh-food delivery outside major cities.

Who are the main players in Vietnam’s e-commerce market?

Shopee and TikTok Shop dominate with a combined 97% share, while local platforms such as Tiki and Sendo now operate in specialised or niche segments.

Page last updated on: