United States Credit Agency Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

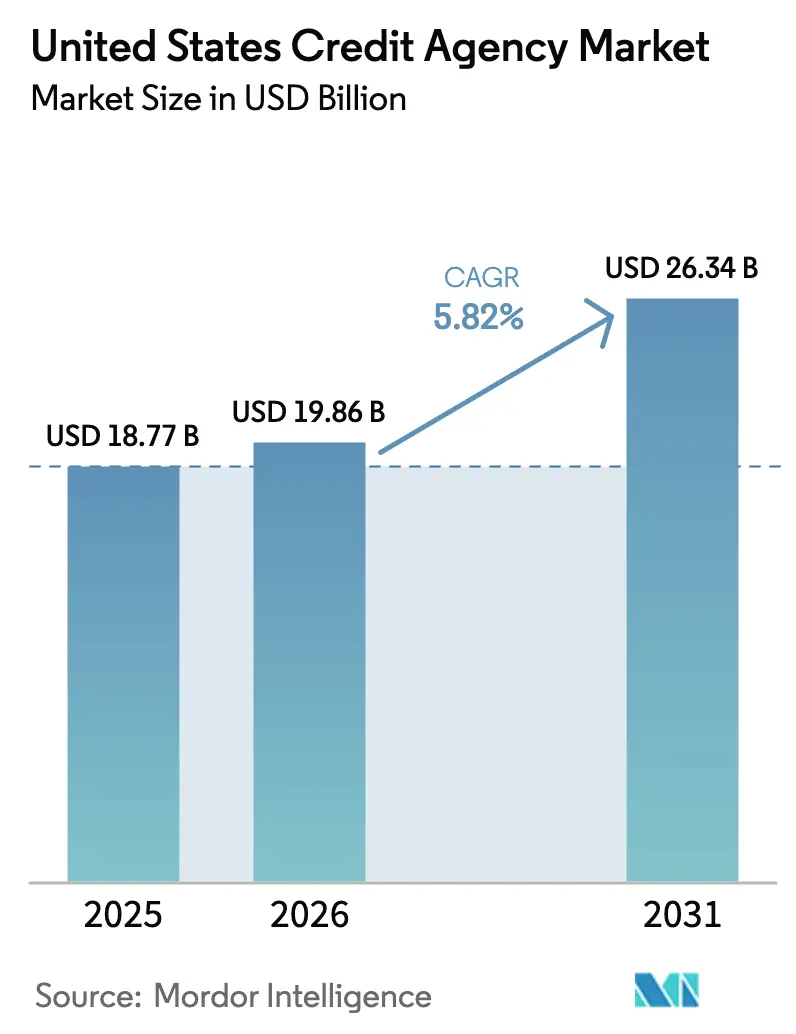

| Base Year Market Size (2025) | USD 18.77 Billion |

| Market Size (2026) | USD 19.86 Billion |

| Market Size (2031) | USD 26.34 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

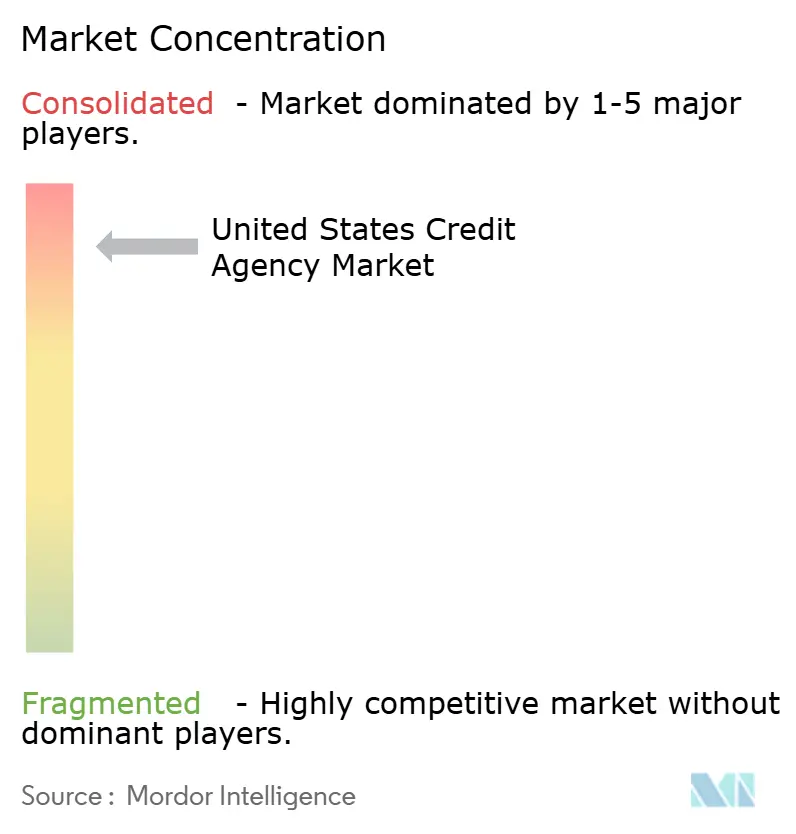

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Credit Agency Market Analysis by Mordor Intelligence

The U.S. credit agency market size was valued at USD 18.77 billion in 2025 and estimated to grow from USD 19.86 billion in 2026 to reach USD 26.34 billion by 2031, at a CAGR of 5.82% during the forecast period (2026-2031). Growth is driven by stable loan demand, increased use of alternative data, and subscription-based monitoring services, offsetting compliance costs from new Consumer Financial Protection Bureau (CFPB) and Federal Housing Finance Agency (FHFA) regulations. Lenders are adopting machine-learning models incorporating rental payments and utility bills, creating new revenue streams while meeting regulatory demands for algorithmic transparency. The CFPB’s data-broker proposal and state privacy laws are raising costs but pushing banks and fintechs toward first-party bureau files with Fair Credit Reporting Act protections. Cloud-native delivery models reduce latency, enabling instant approvals and supporting pricing stability as tri-bureau contracts shift to bi-merge formats in mortgage underwriting. The market is highly concentrated, with the top five bureaus leveraging scale to invest in AI, acquire niche platforms, and bundle identity protection with credit services. Key examples include Capital One’s acquisition of Discover, TransUnion’s OneTru launch, and Experian’s deal pipeline. Regional growth varies: the South anchors volume with a large borrower base, the West drives innovation through fintech demand, and the Northeast focuses on compliance-heavy analytics for low default variability.

Key Report Takeaways

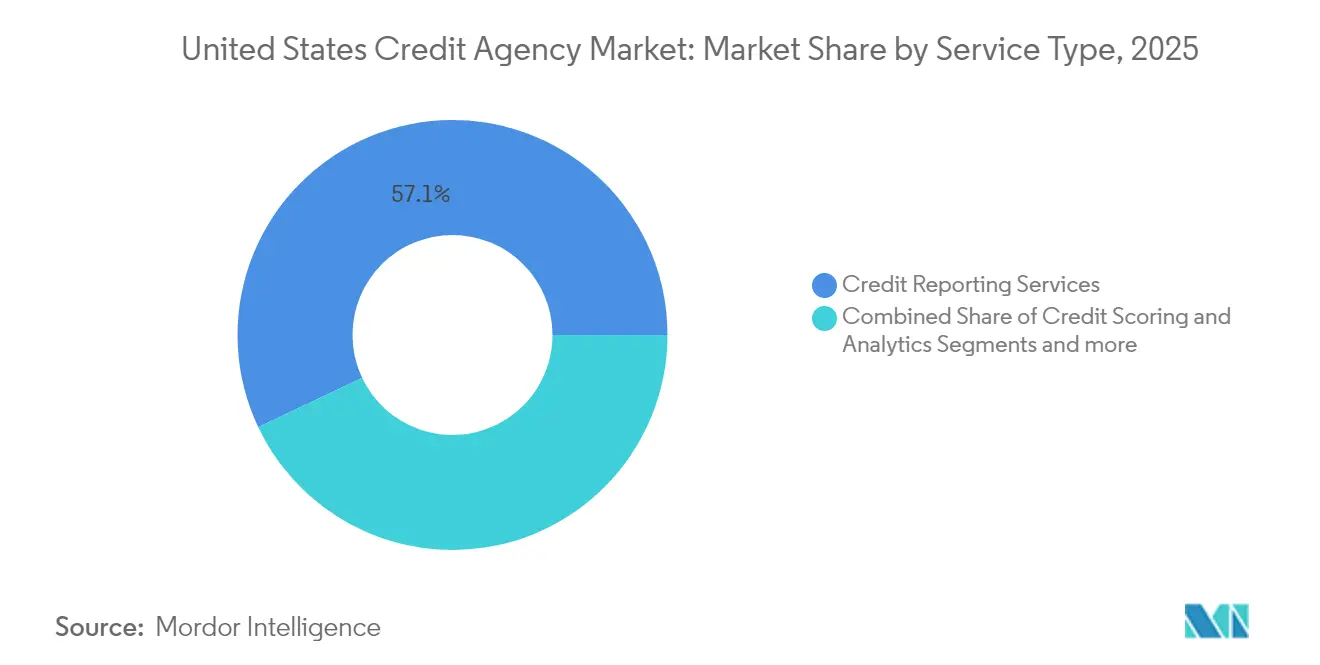

- By service type, Credit Reporting Services held 57.05% United States credit agency market share in 2025, while Credit Scoring & Analytics is projected to grow at a 6.69% CAGR to 2031.

- By end-user industry, Financial Services accounted for 38.33% of the United States credit agency market size in 2025; Media & Technology leads future expansion at an 8.47% CAGR.

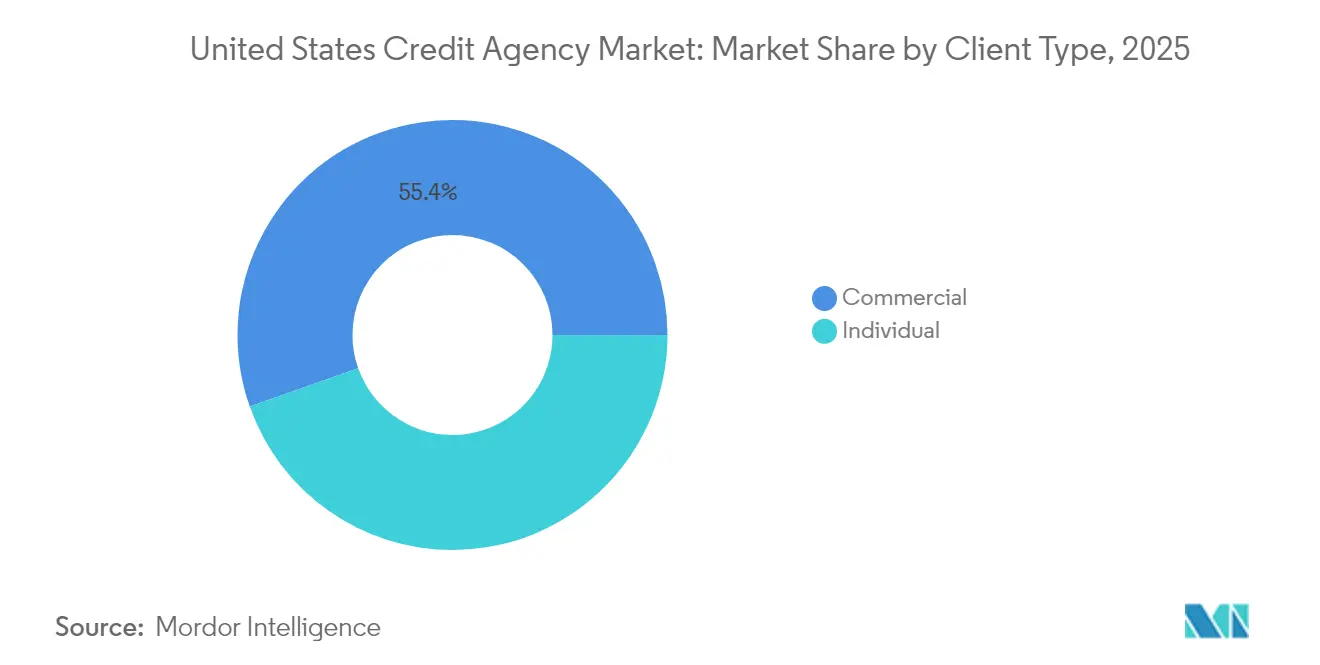

- By client type, Commercial customers represented 55.40% of the United States credit agency market size in 2025, whereas Individual services are advancing at a 6.22% CAGR.

- By geography, the South captured 37.75% revenue share of the United States credit agency market in 2025; the West region’s 6.98% CAGR through 2031 makes it the fastest-growing area.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Credit Agency Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven alternative-data scoring | +1.2% | National, early gains in West & Northeast | Medium term (2-4 years) |

| Rising BNPL & fintech lending volumes | +0.9% | National, urban focus | Short term (≤ 2 years) |

| Regulatory push for inclusive credit models | +0.8% | National, compliance hubs in Northeast | Long term (≥ 4 years) |

| Expansion of small-business credit data | +0.7% | National, strong in South & Midwest | Medium term (2-4 years) |

| Data-broker deprecation | +0.6% | California & Northeast | Medium term (2-4 years) |

| Cloud-native bureau platforms | +0.5% | National, led by West | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Driven Alternative-Data Scoring Adoption

Machine-learning engines ingest rent, utilities, and mobile-usage records to score thin-file borrowers, supplying lenders with broader coverage while satisfying CFPB goals for fairness. Citigroup estimates AI could lift global banking profits by USD 170 billion by 2028, with credit underwriting gains supplying much of that upside [1]Citigroup, “AI in Banking Profit Potential,” citigroup.com . Agencies are strategically leveraging previously untapped data assets to unlock new revenue opportunities and enhance their market positioning. They are also introducing comprehensive model-risk reports that provide in-depth analysis of bias control mechanisms, ensuring compliance with evolving regulatory standards. By prioritizing transparency in their operations, these agencies are strengthening their ability to mitigate regulatory risks and maintain credibility in the market. Moreover, this approach solidifies their role as essential facilitators of responsible AI implementation within the lending industry.

Rising BNPL and Fintech Lending Volumes

Apple began furnishing Pay Later trades to Experian in March 2024, signaling a shift from off-book installments to fully reported credit obligations [2]Experian PLC, “Apple Pay Later Data Reporting Press Release,” experian.com . CFPB research shows almost one in five BNPL users missed a payment in 2024, creating lender demand for bureau-grade oversight and loss forecasting. Agencies package BNPL attributes into specialty scores that track pay-in-four utilization and rollovers, then resell that insight to card issuers fighting share erosion. Direct-to-consumer dashboards let borrowers monitor BNPL history, generating subscription fees while easing dispute workloads. Early evidence suggests reported BNPL data raises average FICO by 10–12 points for punctual users, expanding access to mainstream credit lines.

Regulatory Push for Inclusive Credit Models

The FHFA will mandate bi-merge files and migrate to FICO 10T plus VantageScore 4.0 in Q4 2025, forcing lenders to reassess bureau mix and predictive power [3]Federal Housing Finance Agency, “Credit Score and Bi-Merge Implementation Timeline,” fhfa.gov . The CFPB’s December 2024 outline extends FCRA coverage to data brokers, channeling demand toward bureaus with established permissible-purpose workflows. State bans on medical debts under USD 500 require dynamic suppression filters that maintain file accuracy across jurisdictions. Agencies with cloud-native architectures can update exclusion rules in near real time, converting compliance into a value-added service. Inclusive scoring aligns commercial interests with public-policy goals, supporting continued growth even as fee caps loom.

Expansion of Small-Business Credit Data Products

Section 1071 of the Dodd-Frank Act compels lenders to collect demographic and geographic data on business applicants after July 2025, creating new data feeds that bureaus can sanitize and analyze. FinRegLab studies highlight persistent funding gaps for minority-owned firms, encouraging bureaus to develop alternative cash-flow and e-commerce-based scores. Initial pilot programs conducted with community banks in Texas demonstrated a significant reduction in the time and effort required for manual document reviews, while simultaneously achieving an increase in approval rates for newly established businesses. Agencies price these reports at a premium because they reduce fair-lending litigation risk and accelerate loan turnaround times. Diversifying into commercial datasets buffers revenue against consumer borrowing cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying data-privacy legislation | -0.8% | California, New York, Illinois | Medium term (2-4 years) |

| Mortgage-rate volatility | -0.7% | High-cost housing markets | Short term (≤ 2 years) |

| CFPB plan to open-source scores | -0.6% | National | Long term (≥ 4 years) |

| Tri-bureau pricing scrutiny | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Data-Privacy Legislation (US State Patchwork)

California’s Consumer Privacy Rights Act expansion, New York’s proposed Digital Fairness Bill, and Illinois’s Biometric Information Privacy Act each impose distinct consent, retention, and deletion rules. Agencies must run parallel workflows that check data provenance at state borders, inflating cloud-storage and compliance-audit spending. Delays in reconciling opt-out requests can trigger statutory fines as high as USD 7,500 per violation, eroding profit margins. Some bureaus respond by geofencing sensitive products or baking privacy surcharges into contracts. While privacy rules curb data breadth, they simultaneously heighten lender demand for vetted, FCRA-compliant sources, partially offsetting lost volume.

Mortgage-Rate Volatility Dampening Pull-Through Volumes

Thirty-year fixed mortgage rates hovered near 7% through early 2025, suppressing refinance activity and reducing tri-merge pulls by up to 35% versus 2021 peaks [4]Federal Reserve Bank of Chicago, “Mortgage Rate Impact on Credit Pulls,” chicagofed.org . Lower pull-through weakens high-margin mortgage bundles that combine reports, scores, and fraud checks. Agencies shift sales attention toward home-equity lines, cash-out refis, and construction loans to replace lost volume. Fintech startups that specialize in rate-shopping APIs still consume bureau data but negotiate tighter prices, compressing yields. As rates stabilise, purchase loans will partially offset the refi slump, yet variability remains a swing factor for near-term revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Analytics Accelerates Revenue Mix

Credit Reporting Services captured 57.05% of the U.S. credit agency market, reinforcing its position as the primary data provider for lenders. The Credit Scoring & Analytics segment is projected to expand at a 6.69% CAGR, surpassing the growth rate of traditional reporting services. This growth reflects a notable increase in the analytics-driven segment of the U.S. credit agency market. Key factors driving this expansion include regulatory requirements for AI transparency, the proliferation of Buy Now Pay Later (BNPL) offerings, and heightened demand for real-time credit approvals. Furthermore, Subscription-based Monitoring & Identity Protection services mitigate risks associated with lending cycles. These services experience demand surges during data breach events, ensuring steady revenue streams.

As scoring models mature, bureaus bolt on behavioural features such as spending volatility, pay cheque cadence, and geospatial fraud indicators, fortifying predictive power. Agencies that pilot federated-learning techniques retain consumer privacy while training networks, preserving legal compliance. Proprietary algorithmic lift underpins premium prices, yet pending CFPB algorithm-transparency moves threaten to erode that moat. To hedge, bureaus prioritise unique data ownership—public-record liens, payroll feeds, and verified cash-flow series. Cloud delivery lowers compute cost per inquiry by roughly 25% and enables pay-as-you-go bundles that attract fintech upstarts.

By End User: Technology Verticals Power Next-Wave Demand

Financial Services accounted for a substantial 38.33% share of the U.S. credit agency market size, solidifying its leading position. Growth in this base slows to steady mid-single digits as credit card and auto loans mature. Conversely, Media & Technology customers—including streaming platforms, gig-work marketplaces, and software-as-a-service vendors—purchase bureau data at an 8.47% CAGR, seeking identity verification, account-sharing analytics, and purchase fraud scores. Employment-screening rules issued under CFPB Circular 2024-06 force big tech employers to demand FCRA-grade reports for algorithmic hiring, enlarging order volumes.

Healthcare providers, utilities, and telecom firms round out niche use cases with steady requisition patterns, particularly for deposit decisions and patient-finance plans. Automotive subscription programs leverage bureau scores to calibrate mileage overage penalties. The emerging breadth reduces concentration risk and pushes bureaus to build modular APIs tailored to each vertical. Cross-selling success hinges on integrating the data once, so each additional product drop incurs marginal costs rather than bespoke projects. This scale unlocks higher operating leverage and cushions pricing pressure in legacy segments of the United States credit agency industry.

By Client Type: Individual Subscriptions Lift Margins

Commercial entities still consume 55.40% of 2025 revenue, but the Individual category grows faster at 6.22% through 2031 as privacy fears and credit-score literacy spread. Agencies convert regulatory file-disclosure rights into freemium apps that upsell score monitoring, dark-web scans, and identity-theft insurance. Customer-experience revamps—single-click freeze toggles, weekly VantageScore refresher,s and gamified credit-health tips—keep churn below 2% per month. Lifetime value rises because add-on services, such as loan-rate comparison engines and BNPL trackers, deepen wallet share.

Commercial clients remain indispensable for bulk data pulls that drive economies of scale; however, they push for rate concessions amid regulatory pressure to trim borrower fees. Agencies answer by bundling fraud, KYC, and anti-money-laundering modules that raise average revenue per unit while masking list-price declines. The individual expansion thus anchors overall margin resilience across the United States credit agency market.

Geography Analysis

Southern states captured 37.75% of 2025 bureau revenue, propelled by population inflows, robust mortgage origination, and extensive community-bank networks. Florida and Texas show double-digit growth in fintech loan applications, and lenders in those states purchase enhanced cash-flow analytics to accommodate non-traditional employment patterns. Housing inflation in Atlanta, Miami and Dallas heightens payment-shock risk, prompting demand for location-aware scoring rules. Agencies also partner with regional universities to test rental-payment data feeds, anticipating CFPB inclusivity mandates.

The Western region, while currently dominating turnover, is projected to achieve a significant compound annual growth rate (CAGR) of 6.98% by 2031. California’s Consumer Privacy Rights Act pushes companies toward privacy-by-design bureau APIs, allowing agencies to charge compliance premiums. Silicon Valley startups embed split-second decision tools into in-app finance offers, consuming high-frequency bureau calls that lift transaction counts. Oregon and Washington contribute as e-commerce hubs that utilise identity verification to stop account takeovers. Western adoption of rental, subscription, and buy-now-pay-later datasets provides fertile ground for new score variants tuned to gig-economy cash flows.

The Northeast combines longstanding financial-services depth with low delinquency risk. Regulatory proximity accelerates pilot programs on explainable AI scoring; agencies run model-risk user groups in New York and Massachusetts to solicit feedback before nationwide rollout. Midwestern demand remains moderate but steady. Community banks navigating industrial transitions buy commercial bureau files enriched with supplier-payment histories that gauge small-manufacturer resilience. These diverse regional patterns allow bureaus to tailor pricing and data-depth tiers, maximising value capture across the United States credit agency market.

Competitive Landscape

The five national players—Equifax, Experian, TransUnion, Dun & Bradstreet and LexisNexis Risk Solutions—command major market revenue, resulting in near-textbook oligopoly status. Their dominance is reinforced by vast historical datasets, lender integrations and compliance certifications that create formidable entry barriers. CFPB Director Rohit Chopra labelled the cohort a “credit bureau cartel” after observing report prices rise fourfold since 2022. This scrutiny accelerates platform upgrades designed to show audit trails, bias dashboards and dispute-resolution tracking.

Strategic moves underscore vertical expansion. TransUnion’s April 2025 Monevo acquisition plugs instant pre-qualification into its OneTru cloud, capturing referral lead revenue while reinforcing data moats. Equifax invests heavily in Workforce Solutions to cross-sell income verification as lenders embrace ability-to-repay rules. Experian pilots Buy-Now-Pay-Later performance scores, bundling them with mainstream FICO offerings to stay relevant with younger demographics. Dun & Bradstreet exploits Section 1071 datasets to revamp its small-business PAYDEX model. LexisNexis integrates public-record liens with consumer tradelines, arming insurers with combined property-credit insights.

Competitive intensity revolves around latency, model explainability, and depth of alternative assets rather than simple file count. Cloud migration chops average response times below 300 milliseconds and lowers the marginal cost of new data attributes. Agencies that achieve sub-second turnaround win embedded-finance contracts with fintech apps. However, concentration fuels antitrust talk; proposed anticompetitive-conduct cases could mandate data portability or pricing remedies. Bureaus prepare by lobbying on cybersecurity grounds and highlighting the systemic risk reduction they provide.

United States Credit Agency Industry Leaders

Equifax Inc.

Experian PLC

TransUnion

Dun & Bradstreet Holdings

Fair Isaac Corp. (FICO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Capital One completed its USD 35.3 billion Discover acquisition, creating the largest US card issuer and bolstering proprietary network rails.

- April 2025: TransUnion acquired Monevo, giving it a marketplace that links 150+ lenders to comparison sites across the US and UK.

- December 2024: CFPB proposed Regulation V updates that extend FCRA coverage to data brokers and tighten permissible-purpose rules.

- February 2024: Experian began adding Apple Pay Later loans to consumer files, marking the first major BNPL reporting arrangement.

United States Credit Agency Market Report Scope

A credit agency is a for-profit entity that gathers data on individuals' and businesses' debts. It then evaluates this data to generate a credit score, a numerical representation of the borrower's creditworthiness. United States credit agencies are segmented by client type and vertical. By client type, the market is segmented into individual and commercial, and by vertical, the market is segmented into direct-to-consumer, government and public sector, healthcare, financial services, software and professional services, media and technology, automotive, telecom and utilities, retail and e-commerce, and other vertical types. The report offers market size and forecasts for the United States credit agency market in terms of value (USD) for all the above segments.

| Credit Reporting Services |

| Credit Scoring & Analytics |

| Credit Monitoring & Identity Protection |

| Direct-to-Consumer |

| Government and Public Sector |

| Healthcare |

| Financial Services |

| Software and Professional Services |

| Media and Technology |

| Automotive |

| Telecom and Utilities |

| Retail and E-Commerce |

| Other Verticals |

| Individual |

| Commercial |

| Northeast |

| Midwest |

| South |

| West |

| By Service Type | Credit Reporting Services |

| Credit Scoring & Analytics | |

| Credit Monitoring & Identity Protection | |

| By End User | Direct-to-Consumer |

| Government and Public Sector | |

| Healthcare | |

| Financial Services | |

| Software and Professional Services | |

| Media and Technology | |

| Automotive | |

| Telecom and Utilities | |

| Retail and E-Commerce | |

| Other Verticals | |

| By Client Type | Individual |

| Commercial | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the projected size of the United States credit agency market by 2031?

The market is forecast to reach USD 26.34 billion by 2031, growing at a 5.82% CAGR.

Which service type is growing fastest?

Credit Scoring & Analytics leads with a 6.69% CAGR through 2031 as lenders seek AI-driven risk assessment tools.

Why is the West region expected to outpace others?

Technology-sector expansion and stringent data-privacy laws drive 6.98% CAGR growth in the West, boosting demand for advanced compliance and alternative-data solutions.

How will FHFA’s bi-merge requirement affect bureaus?

It reduces tri-bureau dependence, rewarding agencies that can prove higher predictive accuracy under FICO 10T and VantageScore 4.0 models.

What role does BNPL data play in bureau revenue?

Reporting BNPL trades, as Apple did with Pay Later, broadens consumer credit files and enables agencies to sell new analytics products to lenders monitoring short-term installment risk.

Are individual subscriptions becoming more important?

Yes. Identity-protection and credit-monitoring packages for consumers are expanding at a 6.22% CAGR, adding a higher-margin revenue stream beyond institutional clients.

Page last updated on: