Trade Credit Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.87 Billion |

| Market Size (2031) | USD 30.94 Billion |

| Growth Rate (2026 - 2031) | 9.26% CAGR |

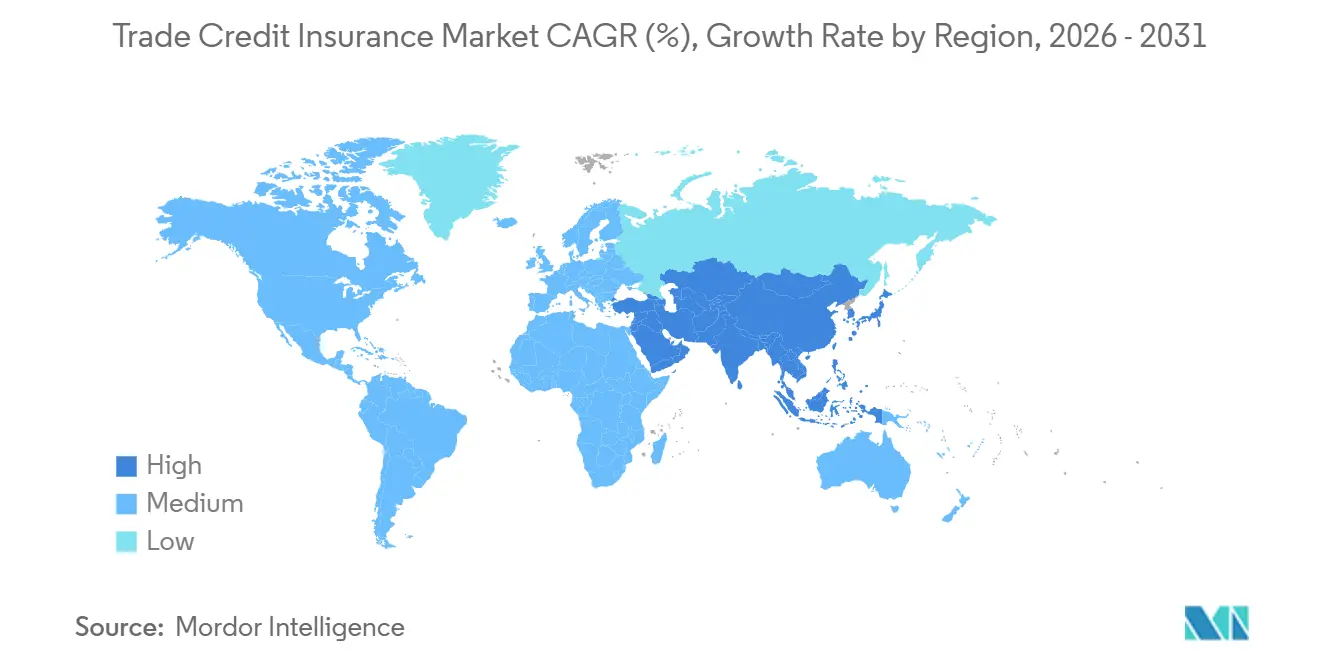

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

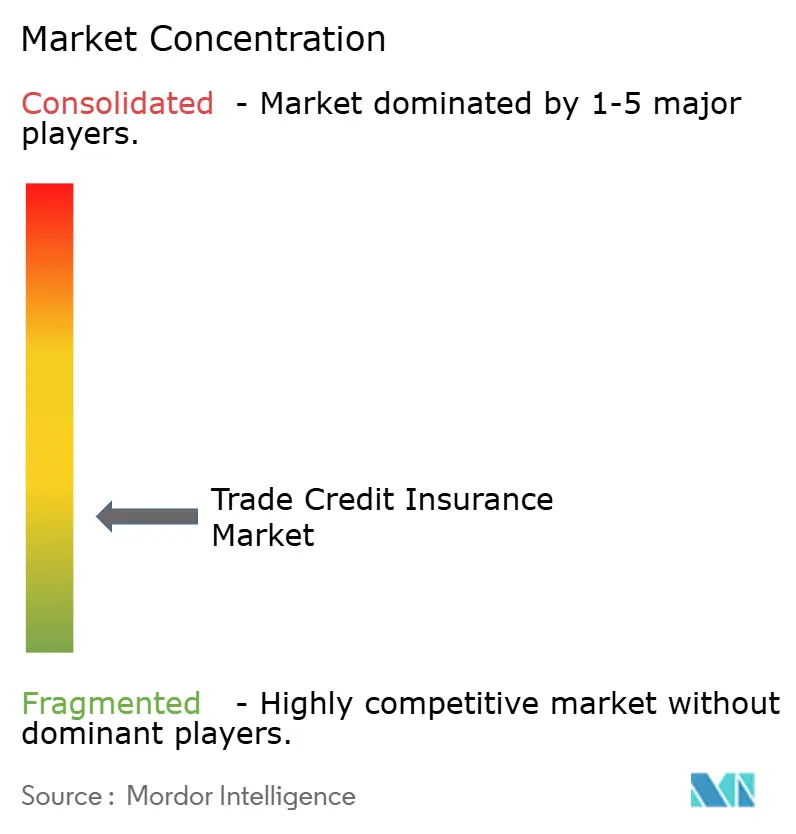

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trade Credit Insurance Market Analysis by Mordor Intelligence

The Trade Credit Insurance Market size is projected to expand from USD 18.52 billion in 2025 and USD 19.87 billion in 2026 to USD 30.94 billion by 2031, registering a CAGR of 9.26% between 2026 to 2031.

Growth in the trade credit insurance market is closely tied to a prolonged insolvency cycle, with global business insolvencies expected to rise by 3% to 6% in 2026 and bankruptcy counts already standing 24% above pre-pandemic levels. This setting is changing how policyholders use cover, because receivables protection is now being used not only to protect balance sheets but also to support receivables-based financing and working capital access. Claims activity increased sharply by late 2025, yet pricing for new entrants remained competitive, which shows that underwriting pressure and pricing response are no longer moving in the same direction across the trade credit insurance market. Europe remained the largest regional base in 2025, while Asia-Pacific is set to expand the fastest through 2031, as export diversification, SME formalization, and stronger support from export credit agencies continue to expand the addressable base of the trade credit insurance market. The leading global carriers still control the core of premium volume, but lower penetration in North America and product access barriers for smaller companies leave clear room for broader channel innovation and simpler policy design.

Key Report Takeaways

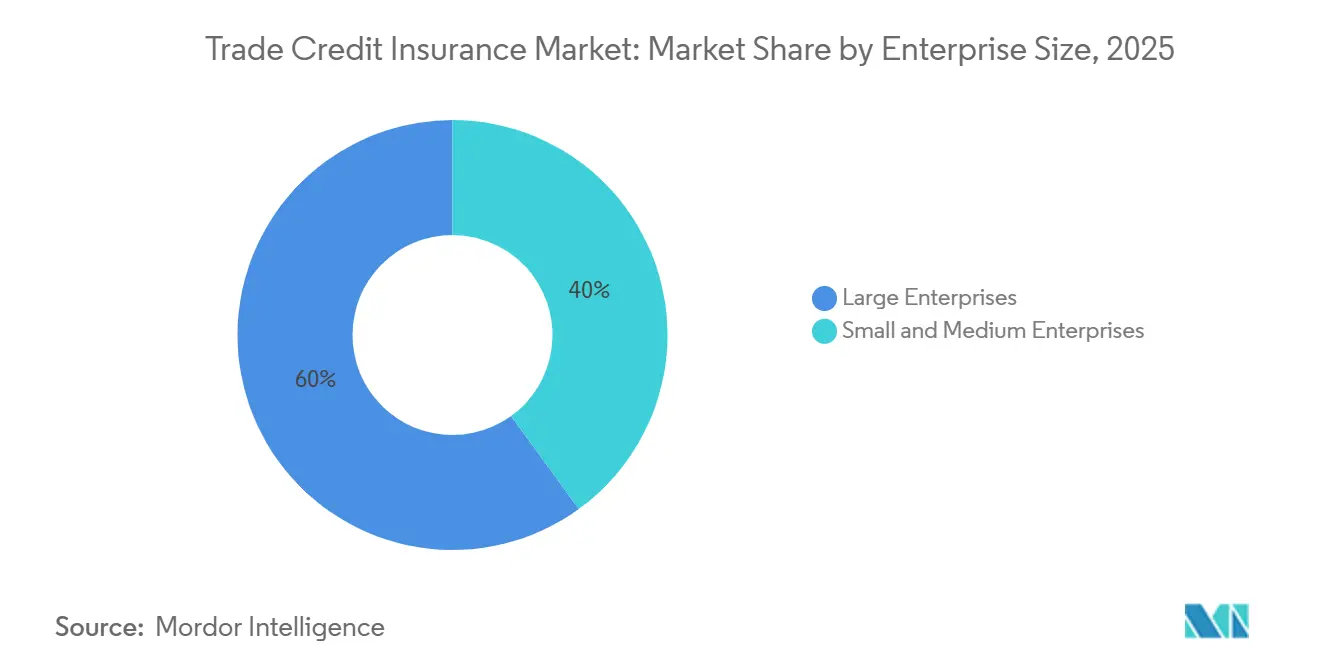

- By enterprise size, large enterprises held 60.00% of the trade credit insurance market share in 2025, while SMEs are projected to grow at 10.90% CAGR through 2031.

- By coverage, whole turnover coverage accounted for 56.40% of the trade credit insurance market share in 2025, while single buyer coverage is projected to grow at a 12.00% CAGR through 2031.

- By application, cross-border business captured 58.70% of the trade credit insurance market share in 2025, while domestic coverage is projected to grow at a 11.80% CAGR through 2031.

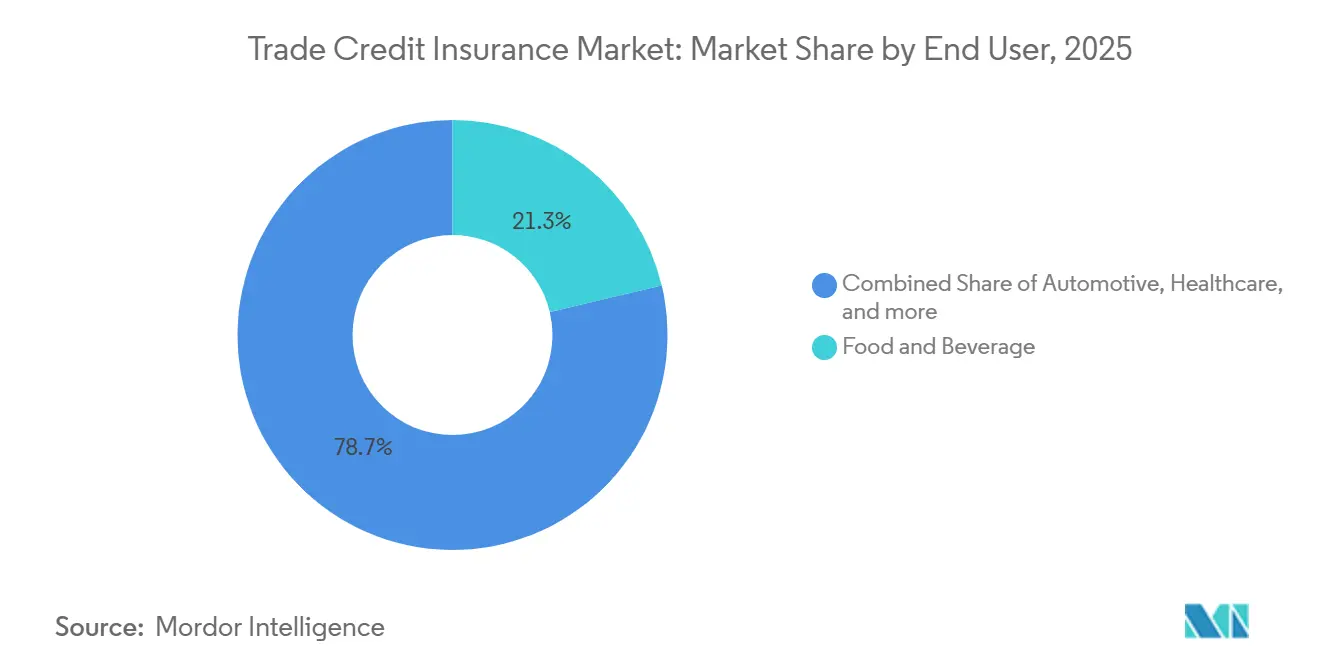

- By end use, food and beverage accounted for 21.30% of the trade credit insurance market share in 2025, while automotive is projected to grow at a 12.80% CAGR through 2031.

- By geography, Europe captured 31.70% of global premiums in the trade credit insurance market share in 2025, while Asia-Pacific is projected to grow at 11.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trade Credit Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Buyer Insolvency Exposure | +2.0% | Global | Short term (≤ 2 years) |

| Embedded Finance Adoption | +1.6% | Global, with early concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Cross-Border Payment Risk | +1.3% | Global, with the highest intensity in Europe, Asia-Pacific, the Middle East, and Africa | Medium term (2-4 years) |

| Sanctions and Counterparty Screening | +1.0% | North America and the EU, spill-over to the Asia-Pacific | Medium term (2-4 years) |

| Broker-Bank Distribution Integration | +0.8% | Global, with leading adoption in Europe and North America | Medium term (2-4 years) |

| SME Credit Limit Accessibility | +0.7% | Asia-Pacific core, spill-over to South America and Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Buyer Insolvency Exposure Accelerates Policy Uptake

The trade credit insurance market is seeing stronger policy demand because insolvency risk has stayed elevated for 5 straight years. Allianz Trade projected global business insolvencies would rise by 6% in 2025 and by a further 3% to 6% in 2026, taking cumulative bankruptcies to 24% above pre-pandemic levels[1][1] ALLIANZ-TRADE.COM Allianz Trade Insolvency report 2025. Germany added further weight to that pattern, with 24,064 corporate insolvencies recorded in 2025, up 10.3% year on year and the highest level since 2014. Sellers now face a clearer need to protect receivables before losses flow into cash flow pressure, funding stress, and covenant strain. In the trade credit insurance market, this has moved cover from a selective treasury tool toward a more routine part of customer risk control, especially in sectors with concentrated buyer books and tariff exposure. The result is firmer demand for policies even when headline premium competition still appears intact for lower-risk new buyers.

Embedded Finance Adoption Expands the Distribution Frontier

The trade credit insurance market is expanding into platforms where invoicing, financing, and payment workflows already sit on a single digital path. Munich Re’s Talaria model shows how credit insurance and receivables finance can be embedded through API-based distribution, using payment behavior and machine learning to support invoice-level decisions[2][2] MUNICHRE.COM Talaria Solutions | Munich Re. That operating model matters because many smaller firms do not buy annual portfolio policies through traditional channels, but they will use protection if it is placed inside their financing or accounts receivable workflow. Allianz Trade has responded with its digital B2B payment solution, which combines credit insurance, buyer checks, and fraud controls into a single process. Its April 2026 partnership with Klear in North America took the same idea into insurance-backed receivables financing for growth suppliers, demonstrating that incumbent carriers are moving quickly to protect their relevance in the next distribution layer of the trade credit insurance market. As more transaction data stays with platforms rather than brokers, control over the client interface is becoming almost as important as pricing strength.

Cross-Border Payment Risk Intensifies Demand for Export Cover

The trade credit insurance market continues to draw demand from exporters because cross-border payment risk remains high across several trade corridors. Atradius noted that geopolitics, financing pressure, and rerouted supply chains are reshaping credit limit activity in 2026, including the creation of new buyer relationships through route substitution in locations such as Oman[3][3] ATRADIUS.CH How geopolitics, financing, and AI redefine credit insurance in 2026. That matters because first-time buyer risk is harder to assess when sellers lack a long payment history with newly onboarded buyers. In Brazil, trade credit insurance premiums rose 6.2% to BRL 2.3 billion in 2025, while export-focused premiums rose 45% to BRL 161.6 million, indicating that exporters moved to protect exposures on more volatile trade routes. The trade credit insurance market is therefore benefiting not only from a rise in trade risk, but also from the speed with which firms now have to approve unfamiliar counterparties and shipping paths. This keeps single-buyer cover and export-focused structures relevant even where whole-turnover programs remain the base product.

Sanctions and Counterparty Screening Drive Integration Demand

The trade credit insurance market is also being shaped by stricter counterparty review requirements in cross-border underwriting. Sanctions screening is becoming routine in credit limit workflows because insurers must now assess ownership structures, practical control signals, and transaction patterns before approving international buyers. The United Kingdom Financial Conduct Authority found that stronger firms rely on vessel tracking, corporate structure analysis, and multi-source data cross-checking when managing sanctions controls. Those practices are moving from internal compliance functions into commercial insurance propositions, especially for exporters without large in-house screening teams. As a result, the trade credit insurance market is adding greater service value around underwriting intelligence, not only balance-sheet protection. This is especially relevant for small- and mid-sized exporters willing to pay more for faster access to pre-vetted buyer pools and cleaner onboarding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Premium Burden | -1.4% | Global, most acute in SME segments across all regions | Short term (≤ 2 years) |

| Policy Exclusion Complexity | -1.1% | Global, with highest friction in emerging-market buyers | Medium term (2-4 years) |

| Underwriting Data Fragmentation | -0.9% | Asia-Pacific core, spill-over to South America and the Middle East, and Africa | Long term (≥ 4 years) |

| Reinsurance Capacity Sensitivity | -0.8% | Global, with concentration risk in Lloyd’s treaty market | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Premium Burden Limits SME Adoption

The trade credit insurance market still faces a basic access problem because smaller firms often see protection as expensive relative to their margin base. Atradius reported that 30% of SMEs in France, Germany, and the Netherlands cited high premiums as the main reason for not buying policies, while 45% cited product complexity as another major barrier. That pressure is amplified when claims trends worsen in tariff-affected sectors such as automotive and steel, because blended pricing then moves upward for buyers with far less bargaining power. Standard premium ranges of 0.25% to 1% of insured turnover, combined with minimum premium thresholds and broker costs, can make cover difficult to justify for firms below the lowest revenue tiers. The trade credit insurance market, therefore, grows more slowly in the part of the customer base where payment risk is often most painful in working capital terms. More flexible invoice-level pricing is the clearest answer to this restraint, but adoption remains uneven across regions and channels.

Policy Exclusion Complexity Creates Coverage Gaps

The trade credit insurance market also loses demand when policy language does not align with what corporate credit teams expect it to cover. Exclusions tied to pre-existing debt, disputed goods or services, related-party transactions, and unresolved contractual obligations affect a meaningful share of real payment failures. Sanctions-related carve-outs and exclusions linked to dual-use goods or restricted sectors add another layer of uncertainty in cross-border books. This means the buyers causing the most concern are often the hardest to insure in practice, especially in stressed sectors or difficult jurisdictions. The trade credit insurance market remains exposed to this confidence gap until documentation standards, digital invoicing practices, and claims interpretation become more consistent across markets. That issue is particularly relevant for exporters operating across several legal systems where recoveries, documentation rules, and buyer disputes do not move on the same timetable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: Large Corporates Anchor Premiums, SMEs Drive Volume Growth

Large enterprises held 60.00% of global premiums in 2025, which kept them as the leading buyer group in the trade credit insurance market and the largest base of recurring premium volume. Their position comes from scale, because large corporate accounts often place whole-turnover programs, structured credit solutions, and lender-linked facilities across multiple geographies and buyer groups. The same scale also improves negotiating leverage, allowing multinational insureds to arrange syndicated credit limits across several carriers and secure broader coverage architecture than smaller firms can usually access. In the trade credit insurance industry, this segment also benefits from closer alignment with bank underwriting requirements and treasury planning. That large-account strength does not remove pressure, because claims severity, tariff disruption, and sector concentration still affect portfolio design and pricing discipline. Large insureds increasingly want layered solutions that combine primary capacity, top-up support, and financing compatibility rather than a single annual policy with static terms. They also expect fast limit responses, because buyer turnover, supplier relocation, and market entry plans change more quickly than legacy underwriting cycles were built to handle. The trade credit insurance market therefore relies on this group not only for premium scale, but also for product development that later moves down into the mid-market. This keeps large enterprises at the center of product design even while the next wave of policy count growth comes from smaller firms.

SMEs are the fastest-growing enterprise cohort, with a 10.90% CAGR through 2031, which gives this group the clearest expansion role in the trade credit insurance market. Payment delays remain a serious operating issue for that customer set, and trade credit accounted for 52% of all B2B transactions in Western Europe in 2026 as tighter bank lending pushed more financing pressure into supplier relationships. That trend raises the cost of a single buyer default for smaller firms because working capital buffers are thinner and alternative funding lines are usually narrower. API-based models such as Munich Re’s Talaria are starting to lower entry barriers by pricing per invoice rather than requiring a long portfolio history before cover becomes available. The SME segment still carries structural friction that goes beyond price alone. Simpler wording, faster onboarding, and embedded financing links matter because many smaller companies do not have internal insurance specialists or dedicated credit teams. Capital frameworks such as Solvency II and the broader move toward stronger insurance capital standards also shape insurer appetite for SME books, since correlated defaults in one sector can consume capital quickly. That makes portfolio quality, transaction data, and distribution efficiency central to whether SME growth can remain profitable. The trade credit insurance market has clear demand in this segment, but conversion depends on whether the product can be sold and serviced in a lighter format.

By Application: International Business Stays Core, Domestic Segment Gains Momentum

Cross-border business captured 58.70% of global premiums in 2025, giving it the largest application base in the trade credit insurance market size for that year. This remained the core use case because exporters face slower legal recourse, more documentation friction, and greater recovery uncertainty when buyers are located in another jurisdiction. Tariff disruption and trade route changes reinforced that demand in 2025 and 2026, especially where suppliers had to enter new corridors quickly or shift customer mixes with little payment history in place. In Brazil, export-focused premiums rose 45% to BRL 161.6 million in 2025, which showed how firms responded when buyer exposures became harder to assess through normal commercial channels. The international segment also keeps a large open gap in the United States, where policy penetration among exporters remains far below European levels. That lower penetration in the United States is important because it points to distribution opportunity rather than weak need. Many exporters still rely on internal credit control or selective customer vetting rather than formal insurance-backed receivables protection. As tariff shifts, sanctions checks, and corridor volatility persist, that approach becomes harder to scale without stronger external support. The trade credit insurance market should therefore keep seeing cross-border demand from both mature exporters and first-time policy buyers. The base use case remains export protection, but the operating need has widened into financing support, compliance screening, and faster onboarding for unfamiliar counterparties. This keeps the international application segment central even as domestic use grows faster.

Domestic coverage is the fastest-growing application segment, with an 11.80% CAGR through 2031, as the trade credit insurance market moves deeper into internal supply chain finance and factoring structures. That growth is tied to how domestic receivables are now being financed and monitored through more digitized accounts receivable systems. Benelux and the Nordics have shown especially strong domestic penetration because insurers have been integrated into receivables management workflows sold directly to corporate credit functions. In Brazil, the 2026 reform path around export credit insurance and insurer eligibility also points to a wider role for private capacity in adjacent receivables protection channels. This faster domestic growth also reflects a change in how lenders and corporates think about local buyer risk. Domestic receivables are easier to document than export claims, but that does not make them safer when sectors are under margin pressure or when payment cycles lengthen. Banks serving mid-market clients increasingly want cover that can sit inside domestic receivables-backed lending, especially when customer concentration is high. That channel is helping domestic business grow from a secondary use case into a more meaningful premium stream. The trade credit insurance market is therefore broadening beyond its original export identity without losing the export-led base that still defines the largest application share.

By End Use: Food and Beverage Holds the Largest Share, Automotive Faces a Repricing Cycle

Food and beverage held 21.30% of global premiums in 2025, making it the largest end-use base in the trade credit insurance market. The segment’s size comes from high transaction volumes, thin operating margins, and a buyer structure that often concentrates sales into large retailers, wholesalers, and foodservice groups. Commodity volatility, climate-linked supply disruptions, and energy cost pass-through have increased payment risk along the distribution chain, especially where annual credit reviews cannot keep pace with buyer stress. WTW noted that insurer appetite for wholesalers and grocers improved after 2022, and several carriers were offering top-up support as food inflation pushed turnover above older policy ceilings. That mix of high-frequency sales and tight margins explains why food and beverage remains a durable anchor segment inside the trade credit insurance market. The sector also benefits from the fact that cover can support financing discipline as much as it protects against insolvency. A missed payment in food distribution can quickly affect inventory turns, supplier commitments, and seasonal purchasing decisions. Insurers, therefore, remain relevant not only because the sector is risky, but because coverage helps keep receivables finance usable when buyer quality becomes uneven. Healthcare, IT, and telecom also hold meaningful positions in the portfolio mix, with IT and telecom supported by the rising use of real-time payment behavior data in platform-driven business-to-business transactions. That wider end-use mix gives the trade credit insurance market a stable premium base even when one sector experiences abrupt pricing pressure. It also helps carriers balance portfolios between higher-volume mature lines and more selective specialized exposures.

Automotive is projected to grow at a 12.80% compound annual growth rate (CAGR) through 2031, making it the fastest-growing end-use segment in the trade credit insurance market. That pace reflects both genuine demand growth and a repricing cycle, as tariff actions and supply chain realignment have raised buyer stress among tier-1 and tier-2 suppliers. WTW highlighted the importance of credit insurance for businesses exposed to tariff-linked trade disruption, especially where policyholders needed protection against changed risk conditions in global supply chains. Atradius also placed auto and transportation under active credit risk review in 2026, supporting the view that underwriting attention is rising across the segment. This means premium growth in automotive comes partly from higher need and partly from more careful pricing of exposures that had previously been underwritten under easier conditions. Other end uses continue to broaden the demand base. The energy segment benefits from infrastructure and project cycles in the Gulf and sub-Saharan Africa, where lenders increasingly expect risk protection before funding trade-linked transactions. Metals and mining, construction, and agriculture also add specialized demand for single-buyer and political risk extensions in more volatile corridors. These are not always the largest premium pools, but they matter because they stretch product design and support higher-value structured placements. The trade credit insurance market therefore remains diversified by use case even though food and beverage and automotive draw most of the current attention.

By Coverage: Whole Turnover Dominates, Single Buyer Gains on Structured Deal Flow

Whole turnover coverage retained 56.40% of global premiums in 2025, making it the main coverage structure across the trade credit insurance market. Its role remains strong because exporters and distributors with large buyer rosters prefer to transfer portfolio-level debtor risk rather than assess each account individually. That format works especially well for insureds with hundreds of active credit relationships, broad regional exposure, and frequent turnover changes across customers. It also fits companies that use cover alongside factoring, receivables financing, and internal working capital controls. In the trade credit insurance industry, whole-turnover programs remain the most familiar and scalable way to align underwriting, policy administration, and financing in a single arrangement. The product also benefits from integrating habits and processes within treasury departments. In markets such as Germany, France, and the United States, trade credit insurance is often handled as a routine part of receivables management rather than an occasional response to stress. Whole-turnover structures help firms spread buyer risk across a larger book, thereby improving coverage efficiency and reducing dependence on a small number of named debtors. They also provide a cleaner framework for regular limit management when turnover changes across many buyers at once. That is why the trade credit insurance market still uses this structure as the base layer even as more specialized products gain traction. The stability of the whole-turnover segment therefore reflects both product utility and deep corporate process integration.

Single buyer coverage is the fastest-growing coverage segment, with a 12.00% CAGR through 2031, as the trade credit insurance market takes on more structured financing deals. Banks and lenders prefer named-debtor structures when a financing line is tied to a specific high-value buyer, because the coverage maps directly to one receivable concentration. That alignment is especially useful in receivables-backed funding, top-up placements, and bank-led risk transfer where the policy must support a defined exposure rather than an entire trade book. AXA XL noted in 2025 that top-up demand has risen as inflation-led turnover growth and new buyer onboarding push insureds beyond existing policy ceilings. This keeps single buyer products attractive even for firms that already maintain a broader whole-turnover program underneath. The growth of single buyer cover also reflects how financing channels now shape product design more directly. Insureds do not always replace portfolio policies when a limit gap appears, and many instead add ring-fenced capacity on a concentrated debtor. That creates a blended structure where the core book stays on whole-turnover terms while high-value concentrations move into separate layers. The trade credit insurance market is therefore developing a more modular product set, driven less by legacy form and more by how lenders, brokers, and corporate treasurers want risk packaged. This is one of the clearest signs that coverage architecture is becoming more flexible than it was in earlier underwriting cycles.

Geography Analysis

Europe accounted for 31.70% of global premiums in 2025, giving it the largest regional share of the trade credit insurance market and the deepest carrier infrastructure. The region hosts Allianz Trade, Atradius, Coface, and the Lloyd’s market, which together support both standard portfolio business and more specialized structured credit placements. Germany remained the continent’s largest national market, with credit insurers covering EUR 506 billion in trade receivables in 2025, while corporate insolvencies rose to 24,064, the highest count since 2014. France, the United Kingdom, Italy, Spain, and Benelux also contribute major premium volumes, supported by mature broker relationships and long-established use of credit insurance in receivables management. Europe’s policy environment still matters globally because changes in e-invoicing, bank capital treatment, and claims documentation standards can influence how quickly structured demand returns.

Asia-Pacific is the fastest-growing region, with a 11.50% CAGR through 2031, making it the strongest expansion engine in the trade credit insurance market. Growth is concentrated in China, India, South Korea, Japan, and high-momentum Southeast Asian markets such as Vietnam, Indonesia, and Thailand. A key support factor is the presence of established export credit agencies, including Sinosure, ECGC, K-Sure, and NEXI, because they provide a public foundation that private carriers can co-insure or reinsure around. That structure allows capacity to expand without forcing commercial carriers to absorb all of the capital burden alone. The regional story is therefore not only about export growth, but also about a wider institutional framework that helps new policy demand convert into insurable volume.

North America remains in an earlier penetration phase, but its runway is meaningful within the trade credit insurance market. The United States still sits well below Europe on exporter policy penetration, which leaves substantial room for conversion if distribution and product simplicity improve. Tariff disruption has pushed more mid-market manufacturers and distributors to formalize customer risk review, which is helping the product move from occasional purchase to more routine treasury planning. Canada and Mexico are also benefiting from reshoring and near-shore supply chain integration, because closer production networks create more domestic and regional receivable exposures that can be financed or insured. This catch-up path is likely to keep North America central to medium-term channel innovation.

The Middle East and Africa, along with South America, remain the next tier of growth areas in the trade credit insurance market. Gulf economies led by Saudi Arabia and the UAE are widening usage as construction, oil and gas, and trade finance volumes expand alongside national diversification programs. Atradius strengthened that direction in April 2026 by establishing a regulated hub in the Dubai International Financial Centre to serve the Gulf, the wider Middle East, and Africa more directly[4][4] DIFC.COM Atradius Expands Middle East Presence with New DIFC Hub | DIFC. In Africa, the African Continental Free Trade Area is helping create more structured intra-regional trade flows, while Allianz Trade’s 2026 Country Risk Atlas pointed to improving conditions in parts of South America that may draw additional underwriting capacity.

Competitive Landscape

The trade credit insurance market remains moderately fragmented. Allianz Trade, Atradius, and Coface are among the key players, leveraging broad distribution networks, deep buyer databases, long-standing bank relationships, and the ability to syndicate capacity across large multinational accounts. The largest carriers also have an advantage in structured business because lenders prefer highly rated counterparties that can respond quickly to large single-name or portfolio placements. At the same time, the market is not closed, as specialty Lloyd’s syndicates, regional export credit agencies, and fintech-backed platforms are expanding the ways protection can be distributed. This leaves the trade credit insurance market fragmented in terms of core premium ownership but more open in product delivery and niche capacity creation.

Competition is now being shaped as much by operating model as by underwriting appetite. Atradius launched its Arcade unified pricing platform in Connecticut in 2026 to replace legacy infrastructure and standardize quoting by combining customer and internal credit risk data. Allianz Trade has focused on digital workflows through Allianz Trade pay and then extended that logic into North American receivables financing through its Klear partnership in April 2026. These moves show that the trade credit insurance market is rewarding carriers that can combine balance-sheet capacity with fast data processing, embedded onboarding, and financing compatibility. Carriers that cannot modernize those layers risk losing access to the fastest-growing channels, even if their core underwriting capabilities remain strong.

Another important shift is consolidation via adjacent risk-transfer platforms. Swiss Re Corporate Solutions agreed in February 2026 to acquire QBE Insurance Group’s Global Trade Credit and Surety business, which showed how reinsurers are moving closer to primary premium streams and direct client access. That logic matters because ownership of underwriting data, client relationships, and policy origination is becoming more valuable as embedded finance scales. The trade credit insurance market also remains exposed to reinsurance concentration, because treaty capacity is held by a limited group of providers and that can tighten quickly after systemic losses. This means competitive intensity can rise at the front end even while capacity discipline in the background still constrains how far primary growth can run.

Smaller entrants continue to matter even if they do not yet challenge the top tier on aggregate premium. Their pressure is strongest in the mid-market, where faster onboarding, lower minimum premiums, and API integration can be more decisive than brand scale. That matters for SME access, domestic applications, and newer geographies where corporate buyers are still forming purchasing habits. The trade credit insurance market is therefore likely to stay top-heavy in premium share while becoming broader and more diverse in distribution structure.

Trade Credit Insurance Industry Leaders

Allianz Trade

Atradius N.V.

Coface SA

American International Group, Inc.

Zurich Insurance Group Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Allianz Trade and Klear (a capital intelligence platform for high-growth companies) announced a landmark insurance-backed receivables financing partnership in North America. The programme provides comprehensive credit insurance on receivables from non-investment-grade buyers, enabling Klear to extend capital against a broader invoice universe. This represents one of the first purpose-built TCI-secured receivables programmes for growth-stage companies in North America.

- April 2026: Atradius established operations at the Dubai International Financial Centre (DIFC), regulated by the Dubai Financial Services Authority (DFSA), marking a formal expansion into the MENA region. The hub strengthens Atradius's capacity to deliver credit insurance and debt collection solutions across the Gulf, broader Middle East, and Africa.

- February 2026: Swiss Re Corporate Solutions agreed to acquire QBE Insurance Group's Global Trade Credit and Surety business, subject to regulatory approvals. The transaction strengthens Swiss Re Corporate Solutions' primary credit and surety capabilities, marking a strategic move by a leading reinsurer to capture upstream premium income and expand its corporate client risk management suite.

- January 2026: Coface entered a partnership with LSEG Risk Intelligence to enhance corporate compliance and buyer screening capabilities. The collaboration integrates LSEG's financial crime and counterparty risk data into Coface's credit limit issuance workflows, creating a combined compliance-and-insurance decision layer for multinational clients.

Global Trade Credit Insurance Market Report Scope

| Large Enterprises |

| Small and Medium Enterprises |

| Single Buyer Coverage |

| Whole Turnover Coverage |

| International |

| Domestic |

| Food and Beverage |

| Automotive |

| IT and Telecom |

| Healthcare |

| Energy |

| Other End Uses |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Coverage | Single Buyer Coverage | |

| Whole Turnover Coverage | ||

| By Application | International | |

| Domestic | ||

| By End Use | Food and Beverage | |

| Automotive | ||

| IT and Telecom | ||

| Healthcare | ||

| Energy | ||

| Other End Uses | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected size of trade credit insurance by 2031?

The trade credit insurance market is projected to reach USD 30.94 billion by 2031, rising from USD 19.87 billion in 2026 at a CAGR of 9.26%.

Which region leads global premiums in 2025?

Europe leads with 31.70% of global premiums in 2025, supported by mature carrier networks and strong use of credit insurance in bank-linked receivables management.

Which customer group is expanding the fastest?

SMEs are the fastest-growing enterprise segment, with a forecast CAGR of 10.90% through 2031, driven mainly by embedded and platform-based distribution.

Why is demand increasing across exporters?

Demand is rising because insolvency risk remains elevated, trade routes are changing, and firms need receivables protection that can also support financing and buyer screening.

Which coverage structure still dominates premiums?

Whole turnover coverage remains the largest structure with 56.40% of premiums in 2025, because it fits diversified buyer books and established treasury processes.

Which end-use segment shows the fastest growth?

Automotive is projected to expand at a 12.80% CAGR through 2031, reflecting both stronger demand and more careful pricing as tariff and supply chain pressures raise buyer stress.

Page last updated on: