North America Stone Plastic Composite Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

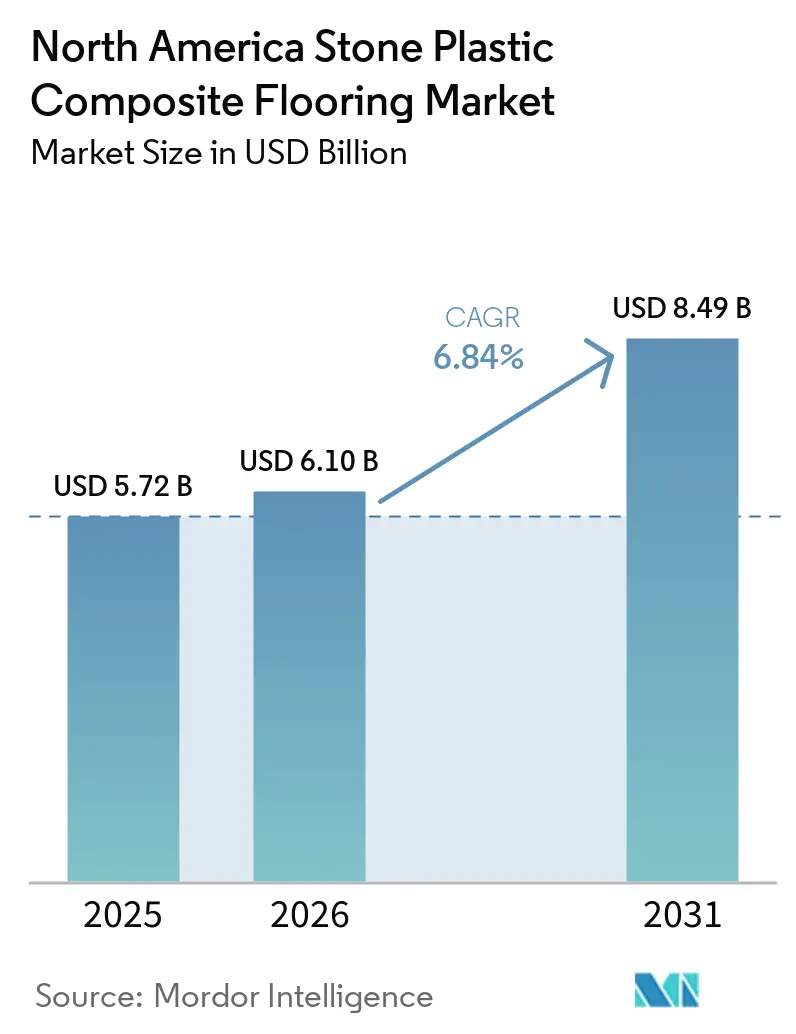

| Base Year Market Size (2025) | USD 5.72 Billion |

| Market Size (2026) | USD 6.10 Billion |

| Market Size (2031) | USD 8.49 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

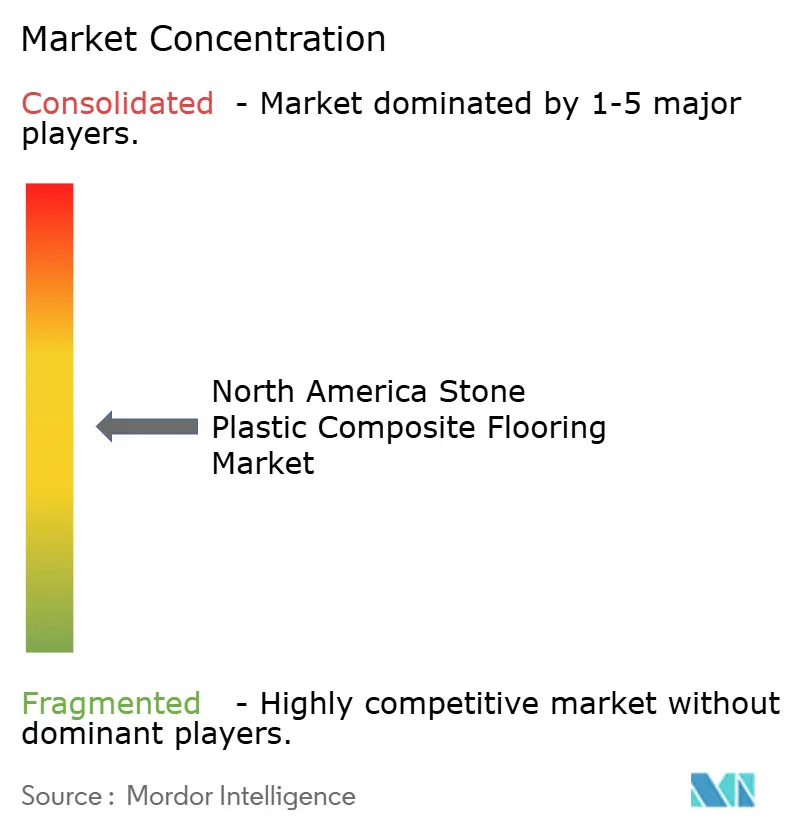

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Stone Plastic Composite Flooring Market Analysis by Mordor Intelligence

The North America stone plastic composite flooring market size stood at USD 6.10 billion in 2026, up from USD 5.72 billion in 2025, and is projected to reach USD 8.49 billion by 2031 at a 6.84% CAGR. Momentum is shaped by renovation and multifamily retrofit activity that favors fast, clean floating installs over glue-down formats, thereby shortening downtime for homes and hospitality assets. Domestic and nearshore capacity has improved schedule reliability compared with trans-Pacific routes, helping buyers reduce change orders and inventory buffers as compliance expectations rise. Tightening certification requirements, including the ASSURE program update that adds an edge fracture resistance test, is lifting product quality baselines and screening out weak locking geometries. Residential buyers continue to select stone plastic composite (SPC) for its waterproofing and scratch resistance in kitchens, basements, and laundry rooms. At the same time, commercial operators use click-lock SPC to accelerate room turn cycles, protecting revenue in hotels and senior living. Online visualization and direct-to-consumer selling support faster color and pattern decisions, reinforcing the channel shift toward digital consideration and purchase paths in the North American SPC flooring market.

Key Report Takeaways

- By product type, SPC planks led with 72.10% of the North America SPC flooring market share in 2025; SPC tiles are projected to expand at a 7.10% CAGR through 2031.

- By product thickness, 5.1–6.0 mm accounted for 34.80% of the North America SPC flooring market share in 2025; products above 6.5 mm are projected to grow at a 7.45% CAGR through 2031.

- By installation method, interlocking/click-lock accounted for 85.72% of the North America SPC flooring market share in 2025; the segment is also projected to grow at a 6.84% CAGR through 2031.

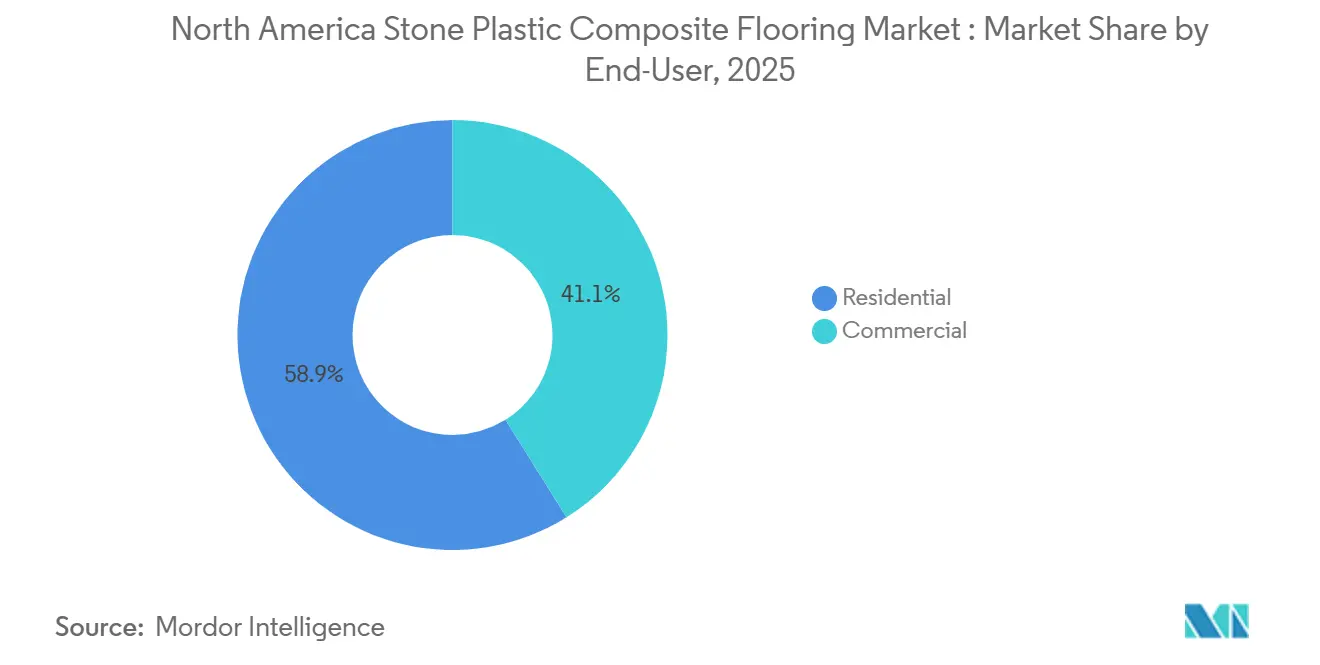

- By end user, residential accounted for 58.90% of the North America SPC flooring market share in 2025; commercial is projected to grow at a 7.05% CAGR through 2031.

- By distribution channel, home centers within B2C/retail captured 42.51% of the North America SPC flooring market share in 2025; online is projected to grow at an 8.60% CAGR through 2031.

- By geography, the United States commanded 82.50% of the North American SPC flooring market share in 2025; Mexico is projected to grow at a 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Stone Plastic Composite Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation and DIY preference for waterproof rigid core | +1.2% | United States, Canada | Short term (≤ 2 years) |

| Shift from flexible LVT/WPC to SPC on performance-to-price | +1.1% | United States, Canada, and spillover to Mexico | Medium term (2-4 years) |

| Retail push: home centers and specialty expanding SPC access | +0.9% | United States, Canada | Medium term (2-4 years) |

| Commercial uptake in hospitality and multifamily retrofits | +1.3% | United States, Canada, Mexico | Medium term (2-4 years) |

| Locking-system advances reduce install time and recalls | +0.7% | North America-wide | Short term (≤ 2 years) |

| Nearshoring and domestic SPC capacity lower lead time and compliance risk | +1.4% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renovation and DIY Preference for Waterproof Rigid Core

SPC addresses a practical problem in wet or variable-temperature interior spaces because its stone-plastic core does not swell like wood-based products under moisture exposure. Homeowners value click-lock floating installation that avoids adhesives, shortens project duration, and lowers labor costs compared with glue-down jobs, helping the North American SPC flooring market capture a larger share of renovation budgets. SPC adoption is supported by measurable shifts in renovation behavior and material performance needs. According to the National Association of Realtors, existing homes account for roughly 85–90% of annual housing transactions, sustaining a large renovation base. The Home Improvement Research Institute notes that over 60% of homeowners undertake at least one DIY project annually, with flooring among the most common upgrades. SPC also maintains structural stability over a temperature range of approximately -20°C to 60°C, minimizing expansion gaps in sunlit or semi-conditioned spaces. These performance characteristics translate into lower maintenance frequency and reduced lifecycle costs, reinforcing repeat purchases among landlords and owner-occupiers.

Shift from Flexible LVT/WPC to SPC on Performance to Price

SPC’s higher core density and compression tolerance improve resistance to rolling loads and furniture legs compared to softer WPC or flexible LVT, supporting wider use in high-traffic zones at accessible price points. Property owners who switch from carpet or flexible LVT to SPC in busy corridors and living areas report fewer expansion and contraction issues, which cuts callbacks for replacements and repairs. The North American SPC flooring market also benefits from the perception that rigid core formats deliver greater value per dollar due to their durability, scratch resistance, and water tolerance in daily use. The transition toward SPC is driven by quantifiable improvements in mechanical performance relative to flexible LVT and WPC. According to ASTM International, SPC’s rigid core density typically exceeds 1,900–2,100 kg/m³, compared with 800–1,200 kg/m³ for WPC, resulting in significantly higher resistance to indentation and rolling loads.

Retail Push: Home Centers and Specialty Expanding SPC Access

National home centers merchandise waterproof rigid core next to laminate and engineered wood, which makes it easy for shoppers to compare moisture protection and care requirements in one visit. Specialty flooring stores lean into premium SPC assortments and installation services that address subfloor prep and acoustics, which support higher average selling prices and customer satisfaction. The online channel adds augmented reality visualization that helps users preview plank colors and patterns at home, which speeds decisions and reduces the need for multiple sample runs. As e commerce grows, direct to consumer brands can offer certified products with clear documentation of emissions and materials, which builds trust among remote buyers. This multi channel expansion broadens reach and supports steady gains for the North America SPC flooring market as digital journeys complement in store advice.

Commercial Uptake in Hospitality and Multifamily Retrofits

Hotels and senior living facilities favor SPC to reduce room downtime because click lock installs move faster and avoid adhesive cure times, which improves revenue protection during phased renovations. Hospitality operators also cite easier care regimes and reduced stain risk versus carpet, which lowers maintenance labor and chemical use across housekeeping schedules. In multifamily buildings, thicker SPC with acoustic underlayment helps meet IIC and STC targets in many assemblies, which simplifies approvals where code officials require minimum impact sound reduction. Commercial specifiers often prefer certified products that meet emissions and composition criteria, which aligns with ASSURE and FloorScore requirements in RFPs [1]SCSGLOBALSERVICES.COM https://cdn.scsglobalservices.com/files/program_documents/SCS%20Standard_111_V2.0%20%282025%29%20%281%29.pdf. These patterns are expanding the installed base across corridors, lobbies, and unit interiors, which adds a durable growth vector for the North America SPC flooring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tariffs, UFLPA scrutiny, and PVC input price volatility | -1.0% | United States, spillover to Canada and Mexico | Medium term (2-4 years) |

| Quality issues from ultra‑thin SPC erode trust | -0.6% | United States national retail | Short term (≤ 2 years) |

| IP enforcement on interlocking systems raises costs | -0.3% | United States, Canada | Long term (≥ 4 years) |

| Tightening standards and fracture testing add retooling burden | -0.4% | United States, partial Canada adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tariffs, UFLPA Scrutiny, and PVC Input Price Volatility

Importers adjust sourcing and documentation to show clean supply chains because enforcement tools now require higher confidence evidence and end-to-end traceability. According to U.S. Customs and Border Protection, enforcement under the Uyghur Forced Labor Prevention Act led to over 3,500 shipment detentions valued at over USD 900 million in its first year, increasing compliance costs and clearance times. Buyers weigh landed cost scenarios that include tariff exposure, Section 301 tariffs on Chinese vinyl flooring products remain at up to 25%, and potential detentions, which can extend port dwell times by 2–4 weeks and add storage and demurrage costs of USD 100–USD 300 per container per day. PVC resin remains a significant share of SPC cost, and swings in resin pricing create margin pressure when retail price points are tightly managed. Some brands diversify production footprints to Southeast Asia or North America to balance tariff grids and streamline audits, which shifts how volumes are allocated to the United States and Canada [2]STARSPLAS.COM https://www.starsplas.com/spc-flooring-industry-and-sino-us-tariffs-impact/. These cross-currents make planning more complex and temper near-term growth for the North American SPC flooring market.

Quality Issues from Ultra Thin SPC Eroding Category Trust

Entry-price products with thinner cores can struggle on imperfect subfloors, increasing the risk of gapping, ledging, and profile damage after installation. Industry installation guidelines from the National Wood Flooring Association indicate that subfloor flatness deviations greater than 3/16 inch over 10 feet significantly increase joint stress, a condition in which thin SPC (typically <4 mm) shows higher failure rates. Overfilled mineral content in the core can also increase brittleness and cause locking-tongue failures under point loads, which drive callbacks and dent consumer confidence. Retailers and contractors mitigate this by steering buyers toward wear-layer and thickness thresholds that demonstrate consistent field performance in residential and light commercial settings. The fracture resistance test introduced under the Resilient Floor Covering Institute ASSURE certification program establishes minimum edge strength benchmarks, helping filter out products prone to failure under normal vertical deflection forces of 250–300 lbs. These steps support a healthier long-term trajectory for the North America SPC flooring market as buyers align product specs with expected use conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Planks Dominate, Yet Tiles Capture Design‑Forward Hospitality

SPC planks held 72.10% in 2025, and SPC tiles are projected to post a 7.10% CAGR through 2031 as design-driven projects gain scale in the North America SPC flooring market. Planks benefit from realistic wood visuals, embossed textures, and familiar room layouts that align with residential preferences and DIY installation flows. Tile formats expand use cases in hospitality and mixed-use spaces where geometric layouts or larger modules reduce grout lines and speed maintenance routines. Installers cite consistent click lock performance and flatness as critical for large format tiles, which supports the selection of certified systems in higher traffic locations. This balance of aesthetics and practicality positions both formats to contribute to steady growth in the North America SPC flooring market.

SPC tiles improve differentiation against laminate and flexible vinyl because tiles enable visual narratives not easily created with plank-only assortments. Product teams add slip-resistant finishes and thicker wear layers to tile SKUs aimed at public spaces, which helps preserve appearance under daily cleaning and rolling traffic. As home centers and specialty stores adjust planograms to include more statement tile options, tiles can capture incremental share without displacing core plank volume in the North America SPC flooring market. Visualizer tools also help household buyers evaluate tile looks at home, which lowers decision friction for pattern rich spaces.

By Product Thickness: 5.0–5.5 mm Balances Cost, while >6.5 mm Unlocks Acoustic Compliance

The 5.1-6.0 mm class accounted for 34.80% of the North America SPC flooring market share in 2025, while planks thicker than 6.5 mm are projected to post a 7.45% CAGR through 2031. Mid-range constructions balance rigid core stability with competitive cost, making them a good fit for most residential rooms and many light commercial spaces. Thicker builds integrate attached pads that support impact sound reduction, helping satisfy building code targets in many assemblies when paired with appropriate subfloors. Contractors highlight edge strength and profile precision as keys to long-term performance across all thicknesses, a claim reinforced by the fracture resistance test adopted in the ASSURE standard. These attributes inform fit-for-purpose selections across projects in the North America SPC flooring market.

Thin, entry-level products can work for quick cosmetic refreshes, yet they are more sensitive to subfloor flatness and heavy point loads, which increases the risk in high-traffic spaces. Premium >6.5 mm products suit hospitality corridors and multifamily units above grade because acoustics and indentation resistance carry more weight in those applications. Installers who standardize on a thickness band reduce training complexity and minimize profile transition issues at doorways, which improves job outcomes in the North America SPC flooring industry [3]LANHEFLOORING.COM https://lanheflooring.com/optimizing-flooring-supply-chains-b2b-best-practices-for-importing-spc-flooring-from-china-in-2026/. Buyers weigh total installed cost and code alignment, which keeps mid range SKUs central to the North America SPC flooring market.

By Installation Method: Click-Lock Dominance Reshapes Labor Economics and Quality Gates

Interlocking click-lock systems commanded 85.72% of the North American SPC flooring market share in 2025 and are projected to expand at a 6.84% CAGR through 2031, indicating that the portion of the North American SPC flooring market tied to floating assemblies will continue to grow. Click assemblies eliminate wet adhesives, which removes an entire cost line item and enables do it yourself workflows where competent homeowners can install 150 to 300 square feet per day in straightforward rooms, a pattern that underpins labor savings cited by market participants. Licensed click systems from Unilin, Välinge, and i4F carry price premiums near the upper end of assortments but deliver tight profile tolerances and meet ASSURE v2.0 requirements that include the ASTM F3781 profiled edge fracture resistance minimum of 17 pounds force. i4F’s December 2025 acquisition of Beaulieu International Group’s rigid core and LVT patent portfolio consolidated intellectual property and expanded the licensing base for interlocking technologies across North America.

Regulatory and sustainability factors reinforce the click lock advantage because floating floors avoid wet adhesives subject to volatile organic compound limits under rules such as South Coast AQMD Rule 1168 and help projects meet LEED low emitting materials criteria when adhesives are minimized or specified within compliant thresholds. Interlocking construction enables intact plank removal at the end of life, aligning with manufacturer take-back programs, including Shaw’s reTURN Reclamation, which collects eligible resilient flooring streams above defined volume thresholds. Hospitality and multifamily renovations specify click lock SPC more frequently in 2026 because faster installations shorten room downtime and preserve occupancy revenue during phased refreshes, an advantage manufacturers highlight in installation guidance and product messaging.

By End User: Residential Renovation Leads Volume, Commercial Hospitality Drives Growth

Residential accounted for 58.90% of the North America SPC flooring market size in 2025, while commercial is projected to grow at a 7.05% CAGR through 2031. Homeowners pick SPC for busy kitchens, basements, and bathrooms because it resists moisture, scratches, and everyday wear. DIY friendly floating installs save labor dollars and time, which encourages adoption in cost sensitive renovation plans. Residential buyers also value easy cleaning and the ability to refresh spaces without sanding or refinishing, which supports word of mouth referrals. These traits keep SPC central to household flooring upgrades in the North America SPC flooring market.

Commercial operators value speed to reopen rooms and the durability to handle rolling traffic, luggage, and spills, which makes SPC a strong fit for hotel corridors and units. Many multifamily and senior living developers specify products with thicker wear layers and acoustic pads to improve comfort and reduce noise complaints, which supports tenant satisfaction. Certification requirements in bids help screen for material safety and performance, which supports reliable outcomes across large properties in the North America SPC flooring industry. As hospitality development resumes and deferred renovations proceed, commercial uses are set to add steady growth to the North America SPC flooring market.

By Distribution Channel: B2C Retail Anchors Volume, Online Accelerates with Visualization

Home centers within B2C/retail captured 42.51% of the North America SPC flooring market share in 2025, while online is projected to grow at an 8.60% CAGR as visualization and fulfillment improve. Home centers offer strong opening price points and broad access, which helps awareness and drives trial in entry segments. Specialty stores differentiate with premium SKUs, installation services, and extended warranties, which support higher average selling prices and fewer callbacks. Online brands leverage FloorScore and other certifications to build trust at a distance and remove friction in sample selection with room visualizer experiences. These channel roles complement each other and support a broad reach for the North America SPC flooring market.

Contractor focused B2B distributors maintain sticky relationships through job site delivery, credit terms, and access to trims and underlayments, which boosts repeat purchases. Developers and large property managers also expand centralized procurement, which can bypass retail and support direct mill relationships for volume buys. Turnkey manufacturing solutions in North America create options for regional brands that want a made-in-local supply and faster replenishment, which deepens the ecosystem in the North America SPC flooring market. As online and offline models continue to blend, buyers gain more transparent access to specs and certifications, which supports confident choices.

Geography Analysis

The United States commanded 82.50% of the North America SPC flooring market size in 2025, supported by strong retail penetration, multifamily retrofits, and broader commercial specifications. Buyers focus on products that meet indoor air quality and performance thresholds, which align with multi attribute certifications used in institutional and hospitality procurements. The United States also benefits from equipment know how and supplier networks that support rigid core production, which allows faster turns on local color ranges and formats. Retailers and contractors value reliable click systems and durable edge profiles, which help reduce callbacks and protect brand equity in the North America SPC flooring market. Evolving import compliance screens sharpen the focus on traceable inputs, which motivates some buyers to shift volumes to domestic or regional sources.

Canada continues to adopt SPC in residential renovation and light commercial use, with attention to testing and performance documentation for building and environmental standards. Access to North American manufacturing and warehousing shortens lead times to major hubs, which supports replenishment stability for retailers. Specialty dealers in Canada lean on premium wear layers and acoustics to differentiate from entry price imports, which supports long term satisfaction and referrals. These factors underpin stable growth in the North America SPC flooring market as Canadian distributors broaden assortments tied to local needs.

Mexico is projected to grow at a 7.25% CAGR as nearshore manufacturing and cross border logistics improve access to the U.S. and Canada, which lowers freight times and eases planning. Hospitality developments in resort corridors favor waterproof rigid core in guest rooms and common areas because it speeds installation and simplifies cleaning [4]UNITEDHOTELSUPPLY.COM https://unitedhotelsupply.com/blog/why-hotels-choose-spc-flooring. Producers also evaluate regional value content strategies for tariff planning, which supports competitive landed costs for North American orders. These conditions support a rising contribution from Mexico within the North America SPC flooring market as distribution and manufacturing footprints expand.

Competitive Landscape

The North America SPC flooring market features a set of large brands and OEMs alongside many regional and online entrants, which keeps pricing and innovation competitive. Branded lines continue to emphasize installation speed, surface realism, and acoustic comfort, while certification coverage and clear specs build trust with architects and facility managers. Companies differentiate through licensed click systems, wear layer thickness, and design libraries that include tiles and wide plank options. In parallel, turnkey manufacturing options enable regional distributors to explore local production, which can yield faster line changes and custom runs for retailers. These moves sustain a steady cadence of product refreshes aligned to real world install and maintenance needs in the North America SPC flooring market.

Strategic activity centers on three themes. The first is installation technology and profile durability, where clear performance thresholds limit failure risk and improve field outcomes. The second is format variety, as hexagon and large format tiles give designers alternatives to wood look planks, which broadens commercial placements. The third is supply chain reliability, in which nearshoring reduces transit variability and supports frequent replenishment and promotions. Together, these initiatives anchor differentiation on speed, quality, and design in the North America SPC flooring market.

Digital first brands are also expanding, using visualization to compress decision timelines and certifications to validate safety and emissions to remote buyers. Specialty retailers defend share with bundled services and premium SKUs that align with demanding use cases, which helps maintain margins. Equipment providers also expand their footprints to support new lines in North America, which spreads manufacturing know how and adds capacity options for brands. These factors keep competitive pressure high while supporting steady product improvements in the North America SPC flooring market.

North America Stone Plastic Composite Flooring Industry Leaders

Shaw Industries

Mohawk Industries

HMTX Industries

AHF Products

Mannington Mills

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Axiscor Performance Floors launched its Ascend SPC flooring collection targeting both residential and commercial applications. The line features seven colorways in 7×60-inch planks with a total thickness of 6 mm, a 28-mil wear layer with antimicrobial protection, and 1 mm of IXPE attached underlayment for sound absorption. Installation integrates i4F technology to simplify click-lock engagement. Warranties span lifetime residential, 15-year light commercial, and 10-year commercial coverage.

- January 2026: The Resilient Floor Covering Institute and SCS Global Services announced an update to the ASSURE Certified® certification for rigid core resilient flooring, incorporating a new testing requirement: ASTM F3781, Standard Test Method for Measurement of the Fracture Resistance of a Modular Resilient Flooring's Profiled Edge(s) to an Applied Vertical Force. Products must now demonstrate profiled edges meet or exceed 17 pounds force (lbf) of vertical deflection strength, as measured by independent laboratory testing. The revision strengthens the multi-attribute certification, which already covers indoor air quality, composition, size tolerance, product thickness, wear-layer thickness, heavy metal content, and ortho-phthalate content.

- December 2025: i4F acquired Beaulieu International Group's rigid core and LVT patent portfolio, comprising over 100 patents covering drop-lock, angle-tap, and edge-profiling innovations. The transaction consolidates i4F's technology base for rigid-core and SPC flooring, expanding its licensing revenue stream and strengthening enforcement capabilities against unlicensed manufacturers. The acquisition followed i4F's May 2025 licensing agreement with Milat Floor, enabling the latter to use i4F's drop-lock system in new SPC flooring ranges for global distribution.

North America Stone Plastic Composite Flooring Market Report Scope

| SPC Tiles |

| SPC Planks |

| 4.0–5.0 mm |

| 5.1–6.0 mm |

| 6.1–6.5 mm |

| Above 6.5 mm |

| Self-Adhesive |

| Glue-Down |

| Interlocking/Click-lock |

| Others |

| Residential |

| Commercial |

| B2C / Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B / Contractors |

| United States |

| Canada |

| Mexico |

| By Product Type | SPC Tiles | |

| SPC Planks | ||

| By Product Thickness | 4.0–5.0 mm | |

| 5.1–6.0 mm | ||

| 6.1–6.5 mm | ||

| Above 6.5 mm | ||

| By Installation Method | Self-Adhesive | |

| Glue-Down | ||

| Interlocking/Click-lock | ||

| Others | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B / Contractors | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the North America SPC flooring market?

The North America SPC flooring market size is projected to expand from USD 5.72 billion in 2025 and USD 6.10 billion in 2026 to USD 8.49 billion by 2031, registering a 6.84% CAGR from 2026 to 2031.

Which formats are gaining the most traction in North America?

SPC planks led with 72.10% share in 2025 for familiar wood visuals and DIY installs, while SPC tiles are projected to grow at a 7.10% CAGR on design‑forward hospitality projects.

How are building code and certification trends shaping specifications?

Thicker SPC with acoustic underlayment helps many assemblies meet IIC and STC targets, while the ASSURE update adds edge fracture‑resistance testing that strengthens click‑system performance baselines.

Which end-user segments are driving demand in 2026?

Residential leads volume at 58.90% for waterproof and low‑maintenance needs, while commercial is projected to post a 7.05% CAGR on hospitality and multifamily retrofits.

What role is nearshoring playing in the North America SPC flooring market?

Turnkey line deployments and regional production shorten replenishment cycles, reduce compliance risks tied to complex import routes, and support custom runs for retailers and developers.

How is e‑commerce changing the SPC purchase journey?

Online brands use visualization tools and clear certifications to build trust and accelerate decisions, which supports the channel’s projected 8.60% CAGR through 2031.

Page last updated on: