Cloud Workload Efficiency and Carbon-Aware Scheduling Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

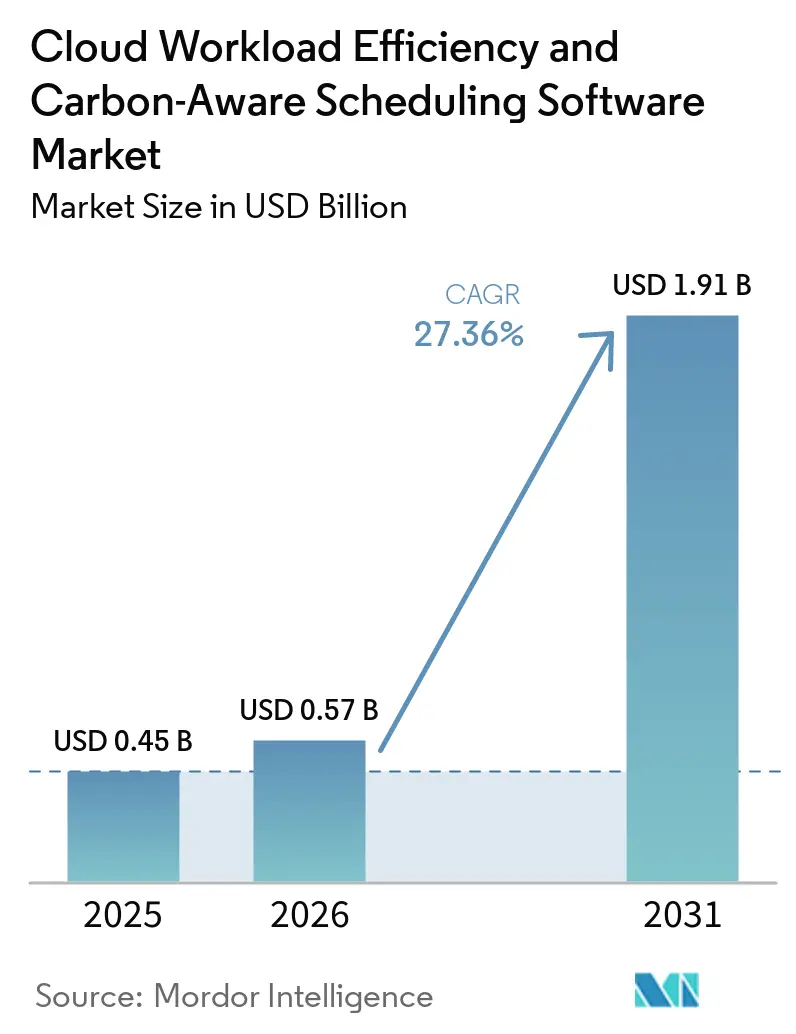

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 27.36% CAGR |

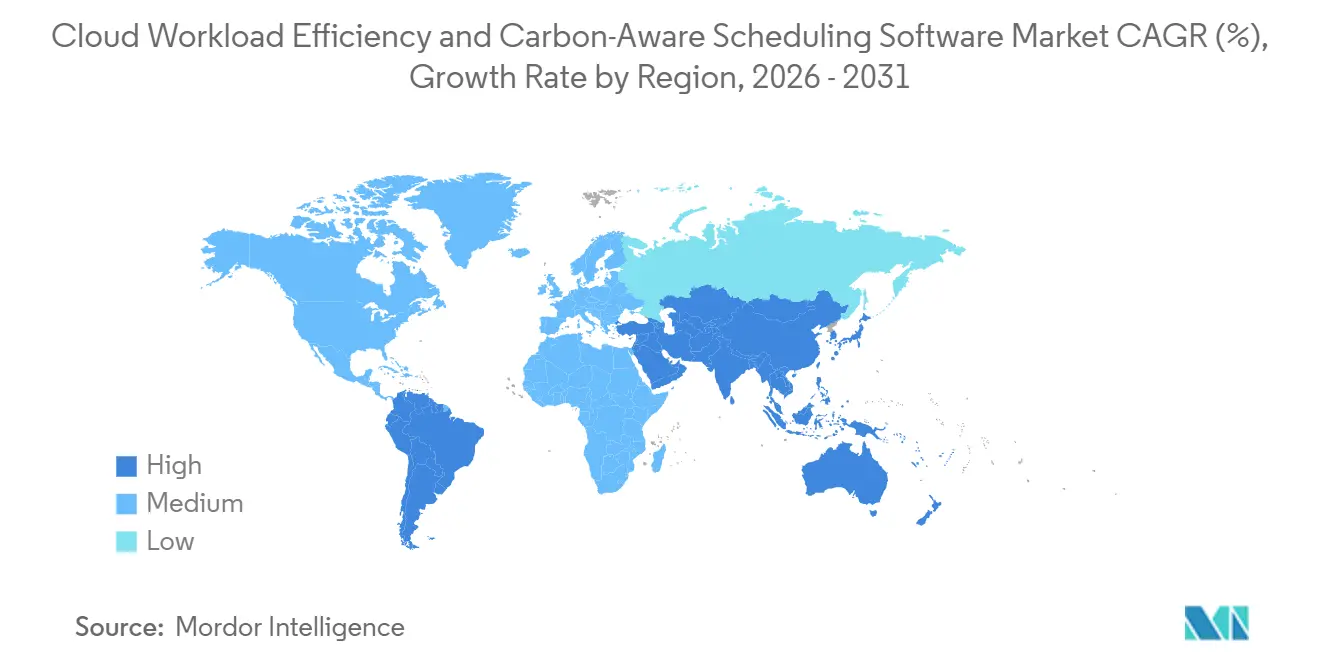

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Workload Efficiency and Carbon-Aware Scheduling Software Market Analysis by Mordor Intelligence

The cloud workload efficiency and carbon-aware scheduling software market size is projected to be USD 0.45 billion in 2025, USD 0.57 billion in 2026, and reach USD 1.91 billion by 2031, growing at a CAGR of 27.36% from 2026 to 2031. The cloud workload efficiency and carbon-aware scheduling software market is expanding because enterprises now want a single operating layer that can cut cloud waste and lower compute-related emissions simultaneously, which makes spending discipline and sustainability reporting part of the same decision process. The cloud workload efficiency and carbon-aware scheduling software market is also benefiting from closer alignment among FinOps, platform engineering, and sustainability teams, as buyers increasingly prefer tools that turn infrastructure optimization into measurable reporting outputs. AI training and inference demand is adding another growth tailwind because GPU-heavy environments create visible power spikes, high utilization variance, and larger savings opportunities than general-purpose compute. The cloud workload efficiency and carbon-aware scheduling software market is drawing intense vendor activity from carbon data providers, Kubernetes optimization vendors, FinOps platforms, and infrastructure automation firms, which is pushing competition toward unified control planes rather than stand-alone tools. Growth still faces friction from the complexity of multi-cloud integration and uneven carbon measurement standards across providers, yet those same gaps also create room for vendors to simplify deployment, normalize data, and deliver audit-ready reporting.

Key Report Takeaways

- By geography, North America accounted for 34.85% of the cloud workload efficiency and carbon-aware scheduling software market in 2025, while Asia-Pacific is projected to expand at a 28.67% CAGR through 2031.

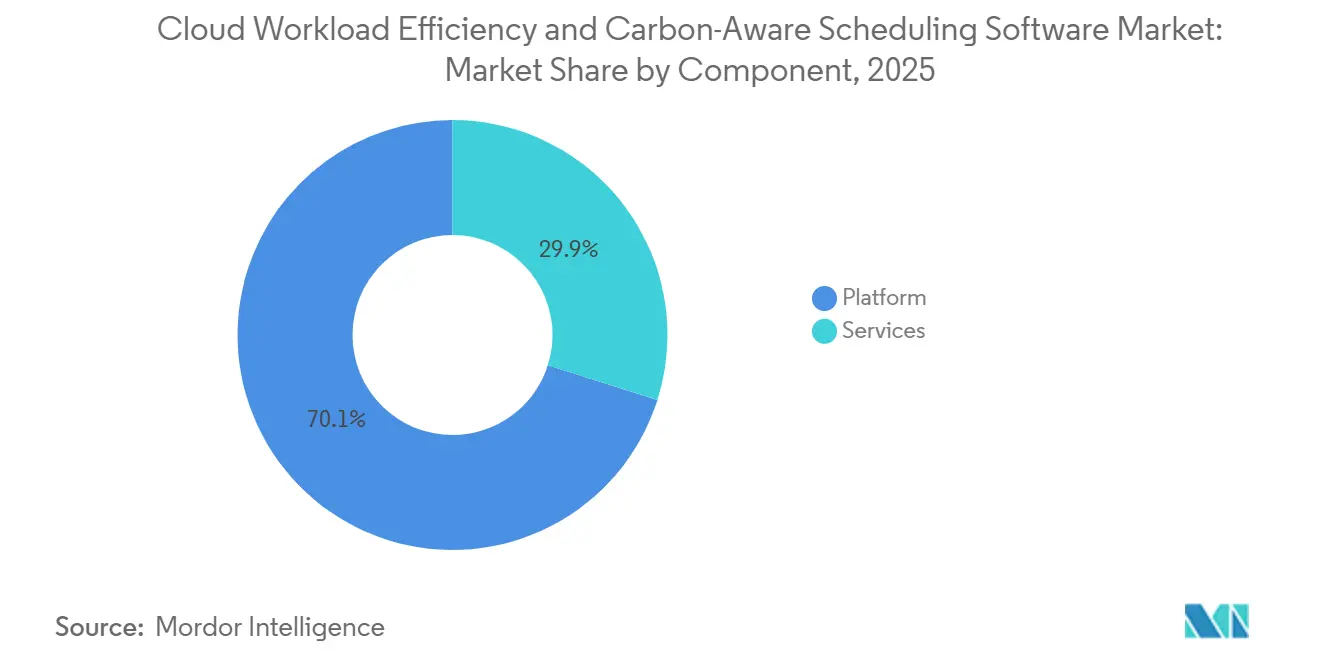

- By component, platform solutions led with 70.12% share in 2025, while services are projected to expand at 28.45% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 67.34% of the market in 2025, while hybrid deployment is projected to grow at a 27.89% CAGR through 2031.

- By enterprise size, large enterprises held 65.41% share in 2025, while SMEs are projected to grow at 28.12% CAGR through 2031.

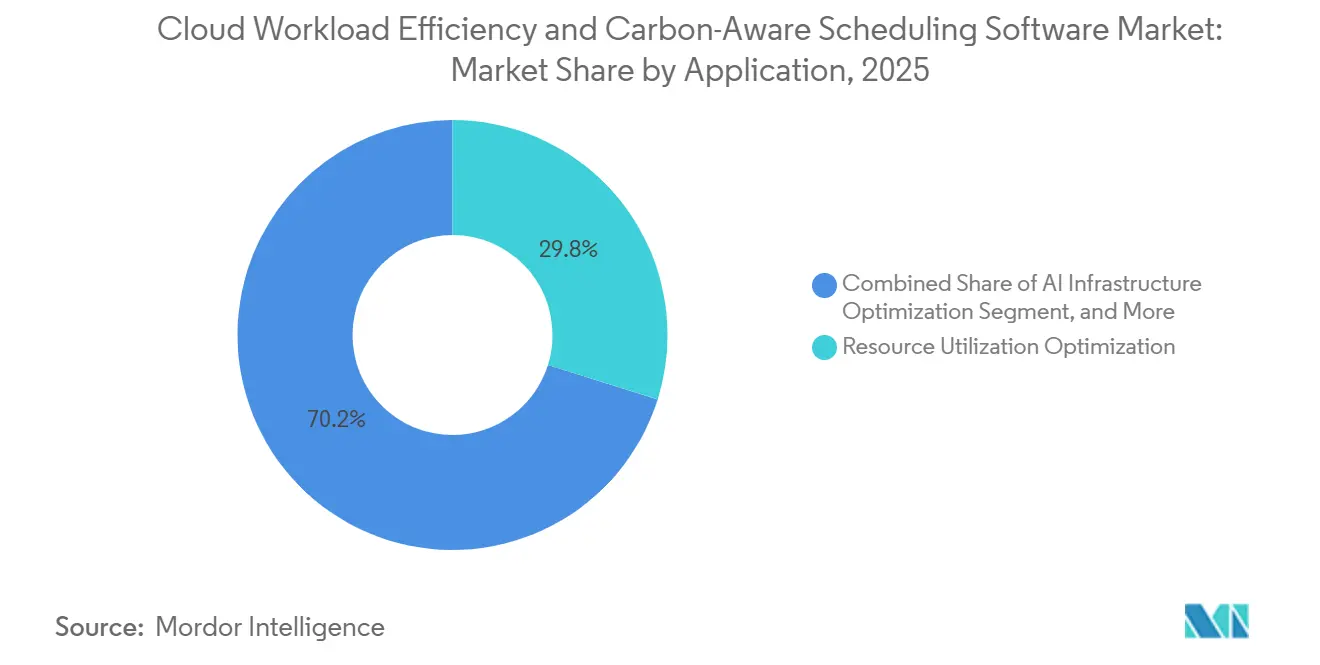

- By application, resource utilization optimization captured 29.84% share in 2025, while AI infrastructure optimization is projected to expand at 29.56% CAGR through 2031.

- By end-user industry, IT and Telecom accounted for 26.74% share in 2025, while Retail and Consumer Goods are projected to grow at 27.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud Workload Efficiency and Carbon-Aware Scheduling Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising FinOps Adoption for Cloud Cost and Carbon Co-Optimization | +5.8% | Global, with strongest traction in North America and Western Europe | Medium term (2-4 years) |

| Grid Carbon Intensity APIs Enabling Real-Time Workload Placement | +4.7% | Global, core adoption in North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Kubernetes-Native Automation Demand Across Cloud-Native Enterprises | +4.3% | Global, with accelerated uptake in North America, Europe, and APAC tech hubs | Short term (≤ 2 years) |

| Mandatory Sustainability Reporting Increasing Audit-Ready Emissions Controls | +3.8% | EU, North America, spill-over to APAC and Middle East and Africa | Medium term (2-4 years) |

| Multi-Cloud Expansion Creating Region-Aware Scheduling Demand | +3.1% | Global, particularly APAC, North America, and EU sovereign cloud zones | Medium term (2-4 years) |

| AI and GPU Workloads Increasing Elasticity and Energy Efficiency Needs | +2.6% | Global, led by North America, APAC, and emerging AI corridors in Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising FinOps Adoption for Cloud Cost and Carbon Co-Optimization

The cloud workload efficiency and carbon-aware scheduling software market is benefiting from the shift of carbon tracking into the same operating model that already governs cloud cost control. The State of FinOps 2026 showed that 78% of FinOps practices were embedded within CTO or CIO organizations, indicating that optimization decisions are now handled closer to engineering teams than to stand-alone finance groups.[1]FinOps Foundation, “State of FinOps 2026 Report,” FinOps Foundation, data.finops.org The same 2026 FinOps dataset showed that 98% of respondents already managed AI spend within the FinOps scope, up from 63% in 2025, underscoring the need for tools that can consistently govern volatile compute demand. The FinOps Foundation also formally designated cloud sustainability as an official framework capability in 2026, providing enterprises with a common structure for integrating carbon metrics into multi-cloud cost management practices. That shift matters for the cloud workload efficiency and carbon-aware scheduling software market because buyers no longer see emissions visibility as a separate dashboard purchase; they see it as part of the control layer for cloud operations. As organizations combine financial accountability with cloud emissions reporting, the cloud workload efficiency and carbon-aware scheduling software market is moving from discretionary tooling toward a more standard procurement requirement.

Grid Carbon Intensity APIs Enabling Real-Time Workload Placement

The cloud workload efficiency and carbon-aware scheduling software market is also supported by the rapid improvement in external grid data, which can now be fed directly into scheduler logic. Electricity Maps expanded its API coverage to more than 200 countries and territories and introduced 72-hour grid forecasts across more than 100 zones, giving platforms a longer planning window for batch and flexible workloads.[2]Electricity Maps, “New 72-Hour Grid Forecasts, Advanced Load Optimization for Greater Carbon and Cost Savings,” Electricity Maps, electricitymaps.com WattTime updated its North American model in 2025 with more granular signals for gas and coal generation and said the release enabled 25% more carbon-reduction impact than earlier API versions. Fraunhofer ISST found that shifting workloads spatially from Germany to lower-carbon grids such as Sweden, Norway, or France could reduce electricity carbon intensity by up to 96%, while temporal shifting toward cleaner windows could cut emissions by 21%. IBM Research reported that its Caspian scheduler reduced carbon emissions by 33% while completing 98% of workloads on schedule, providing a strong proof point for the cloud workload efficiency and carbon-aware scheduling software market. As forecast quality improves and geographic coverage deepens, the cloud workload efficiency and carbon-aware scheduling software markets benefit, as automated placement becomes more practical than manual intervention.

Kubernetes-Native Automation Demand Across Cloud-Native Enterprises

The cloud workload efficiency and carbon-aware scheduling software market is closely tied to Kubernetes because that environment has become the common operating layer for modern cloud-native applications and a large share of enterprise AI workloads. The CNCF Annual Cloud Native Survey, released in January 2026, found that 82% of container users ran Kubernetes in production, up from 66% in 2023, and that 66% of organizations hosting generative AI models used Kubernetes for some or all of their inference workloads.[3]CNCF, “Kubernetes Established as the De Facto Operating System for AI as Production Use Hits 82% in 2025 CNCF Annual Cloud Native Survey,” CNCF, cncf.io As clusters grow in node count, team counts, and workload diversity, manual right-sizing and scheduling become harder to sustain, which pushes enterprises toward policy-driven optimization and continuous automation. The Green Software Foundation released Carbon Aware SDK v1.8.0 with unified support for Electricity Maps data and updated compatibility with WattTime v3 signals, making it easier to embed carbon-aware behavior into existing cloud-native workflows. This matters for the cloud workload efficiency and carbon-aware scheduling software market because carbon-aware scheduler extensions can be adopted within existing Kubernetes operations rather than requiring broad application rewrites. That lower integration barrier shortens testing cycles, supports faster onboarding, and widens the addressable market for cloud workload efficiency and carbon-aware scheduling software.

Mandatory Sustainability Reporting Increasing Audit-Ready Emissions Controls

The cloud workload efficiency and carbon-aware scheduling software market is also being driven by regulation, as buyers increasingly need workload-level data that can withstand formal emissions reporting. California’s Climate Corporate Data Accountability Act set an initial Scope 1 and Scope 2 reporting deadline of August 10, 2026, for companies with annual revenue above USD 1 billion that do business in California, underscoring the value of tools that connect operational activity with auditable emissions records. Directive (EU) 2026/470, adopted in February 2026, maintained structured disclosure obligations for large enterprises under the EU reporting framework and reinforced demand for granular Scope 2 information from cloud operations. In this environment, dashboard visibility alone is no longer sufficient, as procurement teams want data models and reporting outputs that can withstand assurance review. That changes the buying criteria in the cloud workload efficiency and carbon-aware scheduling software market, because vendors need to deliver evidence of quality, not just optimization recommendations. The result is a steadier demand base for the cloud workload efficiency and carbon-aware scheduling software market across regulated sectors such as BFSI, government, healthcare, and large enterprise IT.[4]California Air Resources Board, “California Corporate Greenhouse Gas Reporting and Climate Related Financial Risk Disclosure Programs,” California Air Resources Board, arb.ca.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across Heterogeneous Cloud and Legacy Environments | -3.4% | Global, most acute in North America and EU for multi-cloud enterprises | Medium term (2-4 years) |

| Limited Carbon Data Standardization and Forecast Accuracy | -2.8% | Global, with greatest impact in APAC and Middle East and Africa where grid data granularity is low | Medium term (2-4 years) |

| Data Residency and Compliance Constraints Restricting Cross-Region Scheduling | -2.1% | EU, Brazil, China, India, Middle East and Africa | Long term (≥ 4 years) |

| Workload Performance Risk From Aggressive Carbon-Aware Deferral Policies | -1.6% | Global, amplified in latency-sensitive verticals such as BFSI and Healthcare | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across Heterogeneous Cloud and Legacy Environments

The cloud workload efficiency and carbon-aware scheduling software market still faces slower adoption cycles as enterprises try to integrate public cloud, private cloud, on-premises virtual infrastructure, and legacy scheduling systems into a single optimization layer. Many organizations run AWS, Azure, and GCP alongside VMware estates, bare-metal systems, and older enterprise software environments, creating real data normalization problems before scheduling logic can even begin. The CNCF survey showed that Kubernetes production use is broad, yet it also identified a group of organizations still in early or non-cloud-native stages, underscoring how uneven infrastructure maturity remains across the installed base. In the cloud workload efficiency and carbon-aware scheduling software market, the uneven maturity of the market lengthens procurement cycles because buyers often need connectors, data mapping, and governance alignment before they can move into active optimization. The issue is more visible in industrial manufacturing, healthcare, and government, where older batch systems and compliance-heavy infrastructure coexist with newer containerized environments. Demand does not disappear under these conditions, but deployment timelines stretch and initial ownership costs rise, which slows near-term scale-up in the cloud workload efficiency and carbon-aware scheduling software market.

Limited Carbon Data Standardization and Forecast Accuracy

The cloud workload efficiency and carbon-aware scheduling software market also faces a measurement problem, as there is no single, universal method for calculating workload-level carbon intensity across providers and regions. Electricity Maps discontinued its marginal emissions data offering in 2025 due to verifiability concerns, underscoring that even leading data providers are still refining methodological choices that matter to enterprise buyers. WattTime improved regional granularity in its v3 API, yet the company’s own release notes make clear that data quality is much stronger in North America than in many parts of Asia-Pacific, Africa, and South America. The Green Software Foundation’s Carbon Aware SDK is useful as an open standard, but its results still depend on upstream sources that vary in coverage, timing, and underlying assumptions. For the cloud workload efficiency and carbon-aware scheduling software market, that means two platforms can produce materially different emissions estimates for the same workload in the same region, which weakens buyer confidence in reported savings. Until providers publish more auditable workload-level carbon figures that align more closely with accepted reporting standards, this issue will remain a meaningful brake on the cloud workload efficiency and carbon-aware scheduling software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Depth Keeps The Software Layer Central

Platform solutions captured 70.12% of the cloud workload efficiency and carbon-aware scheduling software market in 2025, which showed that buyers still preferred integrated orchestration environments over fragmented point tools. Within the cloud workload efficiency and carbon-aware scheduling software industry, platforms remain the primary decision-making center because they combine carbon data ingestion, scheduling logic, cost visibility, and policy control in a single environment. That position is important because enterprises want measurable outcomes from a single operational layer rather than separate products for spend control, sustainability tracking, and workload placement. The largest vendor focus inside this category remains carbon-aware schedulers, workload orchestration engines, and AI-based placement tools, since those functions connect most directly with daily infrastructure decisions. In practice, the component mix shows that the cloud workload efficiency and carbon-aware scheduling software markets still favor software-led control, even when services are attached later to support rollout and tuning.

Services are projected to grow at a 28.45% CAGR through 2031, making them the fastest-growing component of the cloud workload efficiency and carbon-aware scheduling software market. That growth reflects demand for implementation consulting, managed optimization programs, training, and governance support, especially among buyers that lack deep internal platform engineering teams. IBM expanded Turbonomic to include energy consumption and carbon footprint reporting for virtual machines, and that kind of enhancement shows why services often sit alongside platform adoption rather than replace it. In many enterprise accounts, the initial consulting engagement becomes an ongoing managed service contract, which improves retention and increases the long-term value of the installed customer base. The cloud workload efficiency and carbon-aware scheduling software market, therefore, shows a clear pattern where platform products open the account, while services deepen adoption and stabilize usage over time.

By Deployment Mode: SaaS Delivery Leads While Hybrid Use Cases Broaden

Cloud-based deployment commanded a 67.34% share in 2025, making it the default operating model across the cloud workload efficiency and carbon-aware scheduling software market. This structure reflects buyer preference for SaaS tools that can ingest fresh grid data, update optimization models, and push policy changes without requiring local software maintenance. It also aligns with the purchasing profile of enterprises that already run significant workloads in the public cloud and want minimal infrastructure overhead from the optimization layer itself. In deployment terms, the cloud workload efficiency and carbon-aware scheduling software market size remained centered on cloud delivery because it offered the fastest route from data collection to active control. That lead position is likely to remain firm because cloud-native buyers continue to favor subscription-based tools that can scale with usage and evolve quickly with scheduler logic.

Hybrid deployment is projected to record a 27.89% CAGR through 2031, making it the fastest-growing mode in the cloud workload efficiency and carbon-aware scheduling software market. The main demand comes from regulated industries and public-sector environments that still keep sensitive workloads on-premises while expanding selected functions to the public cloud. These buyers need a single policy layer that can view carbon intensity, cost exposure, and placement constraints across both sides of the estate. Hybrid growth also reflects data residency needs, because enterprises often want carbon-aware optimization without giving up local control over restricted workloads or sovereign infrastructure requirements. On-premises deployment will remain smaller, but it will continue to serve air-gapped and critical infrastructure settings where external connectivity is limited and live scheduling signals must be replaced with cached data and local rule sets.

By Enterprise Size: Large Accounts Dominate Revenue While SMEs Accelerate Adoption

Large enterprises accounted for 65.41% of the cloud workload efficiency and carbon-aware scheduling software market in 2025, reflecting the sheer scale of their cloud spending and the financial impact of small efficiency gains across large environments. Large organizations in IT and Telecom, BFSI, and industrial manufacturing often operate complex multi-cloud estates and large Kubernetes footprints, making manual optimization impractical early on. They also face more direct reporting pressure under major sustainability frameworks, which makes cloud emissions visibility part of a broader enterprise control requirement. From the buyer perspective, the cloud workload efficiency and carbon-aware scheduling software market still leaned heavily toward large enterprises because those customers had the strongest economic case and the strongest compliance motivation. That combination kept large accounts at the center of present revenue even as adoption patterns started to broaden.

SMEs are projected to expand at a 28.12% CAGR through 2031, making them the fastest-growing segment in the cloud workload efficiency and carbon-aware scheduling software market. The adoption threshold is falling because SaaS pricing tiers, open-source tooling, and pre-integrated bundles reduce the need for a large in-house engineering team at the start of deployment. Another important factor is that smaller suppliers in consumer and retail value chains increasingly face requests from larger customers for auditable emissions disclosures, which shifts cloud efficiency from a cost-only topic to a commercial requirement. FinOps Foundation data showed that FinOps practices now extend across organizations of all sizes and that AI spend management is now common well beyond the largest enterprises. That broadening of operational maturity means the cloud workload efficiency and carbon-aware scheduling software market is moving down-market faster than legacy cloud management tools were designed to support.

By Application: Core Optimization Remains Largest While AI Workloads Drive New Demand

Resource utilization optimization accounted for 29.84% of the cloud workload efficiency and carbon-aware scheduling software market in 2025, which kept the category anchored in the most direct and measurable form of savings. Enterprises already understand right-sizing, idle capacity recovery, autoscaling, and better bin-packing, so this application still provides the easiest entry point for procurement and proof of value. The dominance of this use case also shows that many buyers begin with cost control and only later extend the same tooling into formal emissions tracking and carbon-aware placement. In application terms, this share meant that the cloud workload efficiency and carbon-aware scheduling software market size remained grounded in core infrastructure efficiency rather than in experimental sustainability workflows. That installed base matters because it gives vendors a strong cross-sell path into broader workload governance after the initial savings case is accepted.

AI infrastructure optimization is projected to grow at 29.56% CAGR through 2031, making it the fastest-growing application in the cloud workload efficiency and carbon-aware scheduling software market. GPU-intensive training and inference jobs create larger power swings, greater per-unit cost exposure, and more wasted capacity than conventional compute, making the improvement opportunity easier for buyers to see. Research posted on arxiv.org showed that GPU cluster workloads often enter execution-idle states that still consume meaningful baseline power, further strengthening the case for specialized schedulers and automated downscaling logic. The cloud workload efficiency and carbon-aware scheduling software market is therefore moving beyond general right-sizing into a more specialized layer of GPU orchestration, placement, and carbon-aware deferral. Multi-cloud placement, sustainable DevOps and testing, carbon-aware scheduling, and energy-efficient data processing remain important adjacent applications because they expand vendor relevance across more steps in the cloud operations cycle.

By End-User Industry: IT And Telecom Leads While Retail Builds Momentum

IT and Telecom captured 26.74% of the cloud workload efficiency and carbon-aware scheduling software market in 2025, giving it the largest end-user position among all industry groups. The sector leads because it combines high cloud intensity, strong platform engineering capabilities, mature FinOps adoption, and large Kubernetes operator communities that are already comfortable with continuous optimization tools. Cloud-native software companies and telecom infrastructure providers also run some of the most complex multi-cloud environments, which makes recurring cost and efficiency tuning a routine operational need rather than an occasional project. In share terms, IT and Telecom represented the clearest expression of cloud workload efficiency and carbon-aware scheduling software market share, as this vertical had both the scale of spending and the operational readiness to adopt early. That lead position should remain important because the sector continues to absorb AI workloads, distributed services, and data-heavy applications that benefit from policy-based scheduling.

Retail and Consumer Goods is projected to grow at 27.43% CAGR through 2031, making it the fastest-growing end-user vertical in the cloud workload efficiency and carbon-aware scheduling software market. Consumer-facing brands are under rising pressure to demonstrate credible progress on Scope 3 reduction programs, and that pressure is increasingly extending to the digital infrastructure used for commerce, analytics, and supply-chain visibility. The segment also benefits from flexible batch workloads in recommendation engines, campaign analytics, and demand planning, which are easier to shift across regions or time windows than many transaction-critical systems. Industrial Manufacturing, Energy and Utilities, Healthcare and Life Sciences, BFSI, Government and Public Sector, and Transportation and Logistics all represent significant demand pools as their cloud estates become more data-intensive and policy-sensitive. As those sectors scale digital operations, the cloud workload efficiency and carbon-aware scheduling software industry is finding more vertical entry points where cost control, operational resilience, and emissions visibility need to work together.

Geography Analysis

North America held 34.85% of the cloud workload efficiency and carbon-aware scheduling software market share in 2025, which made it the leading regional contributor. That position reflected early FinOps maturity, deep hyperscaler infrastructure, and a large installed base of enterprises already running multi-cloud and Kubernetes-heavy environments. California SB 253 raised the region’s urgency by setting an initial Scope 1 and Scope 2 reporting deadline of August 10, 2026, for qualifying companies that do business in the state. The United States also remains the main focus for several competing vendors in cost optimization, Kubernetes automation, and carbon-aware operations, keeping the regional buying environment active and competitive. Canada and Mexico remain smaller contributors, but adoption is widening in financial services and manufacturing as regional subsidiaries align with enterprise-wide sustainability and infrastructure policies.

Asia-Pacific is projected to grow at 28.67% CAGR through 2031, making it the fastest-growing geography in the cloud workload efficiency and carbon-aware scheduling software market. The region’s momentum comes from rapid hyperscale cloud build-out across India, South Korea, Australia and New Zealand, Japan, and China, where enterprise cloud capacity and AI workloads are both increasing. The cloud workload efficiency and carbon-aware scheduling software market is growing rapidly in Asia-Pacific as buyers increasingly need region-aware workload placement that can respond to cost, capacity, and data location constraints simultaneously. The March 2026 Wirtschaftsrat report on data centers described AI-guided workload energy management as a strategic issue for data center operations, and that logic maps directly to the large and expanding digital estates seen across Asia-Pacific. Growth is also supported by digital policy developments and the rise of local cloud regions, which make it easier to combine performance requirements with region-specific scheduling rules.

Europe remains a structurally important part of the cloud workload efficiency and carbon-aware scheduling software market because it operates under the most mature reporting framework among major regions. Directive (EU) 2026/470 reinforced the regulatory framework for large-enterprise sustainability disclosures, keeping demand focused on auditable, granular cloud emissions data. The Climate Neutral Data Center Pact also kept attention on renewable matching targets, which strengthened the practical value of tools that can shift flexible compute toward cleaner power windows. South America, led by Brazil, and the Middle East and Africa remain earlier-stage opportunities, yet sovereign cloud investment, data residency rules, and expanding hyperscaler footprints are gradually improving the case for the cloud workload efficiency and carbon-aware scheduling software market across those regions.

Competitive Landscape

The cloud workload efficiency and carbon-aware scheduling software market has a moderately concentrated upper tier and a fragmented middle layer, with no single vendor controlling all the important capabilities across cost optimization, carbon data, Kubernetes automation, and sustainability reporting. Full-platform providers such as IBM Turbonomic, Cast AI, Harness, and CloudBolt compete against specialist vendors that focus more narrowly on data signals, container optimization, or reporting depth. That structure keeps the cloud workload efficiency and carbon-aware scheduling software market competitive because buyers can achieve similar outcomes through multiple vendor combinations rather than a single dominant suite. It also means differentiation depends less on simple feature breadth and more on how well each vendor integrates scheduling logic, cloud economics, and reporting quality within a single control plane. The cloud workload efficiency and carbon-aware scheduling software market, therefore, rewards vendors that can simplify deployment and prove measurable results across mixed infrastructure estates.

A clear strategic pattern in the cloud workload efficiency and carbon-aware scheduling software market is consolidation around broader platform capabilities. CloudBolt acquired StormForge in March 2025 and integrated machine learning-based Kubernetes resource optimization into its FinOps platform, which strengthened its position in continuous cost and carbon control for container environments. Cast AI moved further in the same direction in January 2026, launching OMNI Compute as a unified control plane for cross-provider GPU consumption by Kubernetes workloads, directly targeting the fast-growing AI infrastructure optimization opportunity. IBM also extended Turbonomic to include energy consumption and carbon footprint reporting for virtual machines, helping connect workload optimization with broader ESG workflows in enterprise IT environments. These moves show that the cloud workload efficiency and carbon-aware scheduling software market is shifting away from isolated optimization features and toward broader operational platforms that can support cost, sustainability, and AI infrastructure governance together.

Another competitive theme is the growing role of open frameworks and shared tooling in shaping buyer expectations. The Green Software Foundation’s Carbon Aware SDK gives developers a practical way to embed carbon-aware logic into cloud-native environments, lowering the barrier to experimentation and compressing pricing power for some commercial add-ons. At the same time, open tools can expand awareness and create upgrade paths for vendors that offer stronger enterprise controls, reporting quality, and multi-environment support. A large white space remains for vendors that can provide verified workload-level carbon accounting within the scheduler itself, rather than as a later reporting layer, leaving room for further product expansion and future acquisitions in the cloud workload efficiency and carbon-aware scheduling software market.

Cloud Workload Efficiency and Carbon-Aware Scheduling Software Industry Leaders

Cast AI

Densify, Inc.

GramLabs, Inc. d/b/a StormForge

Spot Software, Inc.

Fairwinds, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Harness released AI Cost Management as an integrated feature within its Cloud and AI Cost Management platform, enabling FinOps teams to attribute AI spend at the model, token, and agent level alongside existing cloud cost data; the release consolidates AI and cloud cost governance in a single platform, directly targeting the 98% of enterprises that now manage AI spend within their FinOps programs.

- January 2026: Cast AI Group, Inc. achieved a valuation exceeding USD 1 billion following a strategic investment from Pacific Alliance Ventures, the US venture arm of Shinsegae Group; simultaneously, the company launched OMNI Compute, a unified multi-cloud GPU compute control plane that enables Kubernetes workloads to access GPU capacity across providers without code changes, directly addressing AI infrastructure optimization demand.

- March 2026: CloudBolt Software acquired StormForge (formerly GramLabs, Inc. d/b/a StormForge) from Insight Partners, integrating StormForge's patent-pending machine learning-based Kubernetes resource optimization into CloudBolt's FinOps platform; the acquisition enables continuous cost and carbon optimization across container environments at the node and pod levels, closing a key capability gap in the FinOps for Kubernetes workflow.

- March 2026: WattTime and REsurety jointly launched the Grid Emissions Data platform, a free, open-access resource providing high-quality hourly marginal emissions data on a global scale covering the prior three complete years in CSV format; the platform broadens carbon intensity data access for developers integrating scheduling logic into cloud workload platforms.

Global Cloud Workload Efficiency and Carbon-Aware Scheduling Software Market Report Scope

The Cloud Workload Efficiency and Carbon-Aware Scheduling Software market refers to platforms and services that optimize cloud computing workloads for both performance and sustainability. These solutions integrate carbon-aware schedulers, workload orchestration engines, cloud optimization platforms, carbon-intensity analytics, multi-cloud optimization systems, AI-based workload placement tools, and sustainability automation engines to reduce energy consumption and minimize carbon footprints in cloud environments.

The Cloud Workload Efficiency and Carbon-Aware Scheduling Software market report is segmented by Component (Platform [Carbon-Aware Schedulers, Workload Orchestration Engines, Cloud Optimization Platforms, Carbon-Intensity Analytics, Multi-Cloud Optimization Systems, AI-Based Workload Placement Tools, Sustainability Automation Engines], and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Carbon-Aware Workload Scheduling, Resource Utilization Optimization, Multi-Cloud Workload Placement, AI Infrastructure Optimization, Sustainable DevOps and Testing, Energy-Efficient Data Processing), End-user Industry (Industrial Manufacturing, Energy and Utilities, BFSI, Retail and Consumer Goods, IT and Telecom, Healthcare and Life Sciences, Government and Public Sector, Transportation and Logistics, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform | Carbon-aware schedulers |

| Workload orchestration engines | |

| Cloud optimization platforms | |

| Carbon-intensity analytics | |

| Multi-cloud optimization systems | |

| AI-based workload placement tools | |

| Sustainability automation engines | |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Carbon-Aware Workload Scheduling |

| Resource Utilization Optimization |

| Multi-Cloud Workload Placement |

| AI Infrastructure Optimization |

| Sustainable DevOps and Testing |

| Energy-Efficient Data Processing |

| Industrial Manufacturing |

| Energy and Utilities |

| BFSI |

| Retail and Consumer Goods |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Transportation and Logistics |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Platform | Carbon-aware schedulers |

| Workload orchestration engines | ||

| Cloud optimization platforms | ||

| Carbon-intensity analytics | ||

| Multi-cloud optimization systems | ||

| AI-based workload placement tools | ||

| Sustainability automation engines | ||

| Services | ||

| By Deployment | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Carbon-Aware Workload Scheduling | |

| Resource Utilization Optimization | ||

| Multi-Cloud Workload Placement | ||

| AI Infrastructure Optimization | ||

| Sustainable DevOps and Testing | ||

| Energy-Efficient Data Processing | ||

| By End-user Industry | Industrial Manufacturing | |

| Energy and Utilities | ||

| BFSI | ||

| Retail and Consumer Goods | ||

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Transportation and Logistics | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size outlook for the cloud workload efficiency and carbon-aware scheduling software market?

The cloud workload efficiency and carbon-aware scheduling software market was valued at USD 0.45 billion in 2025, reached USD 0.57 billion in 2026, and is forecast to reach USD 1.91 billion by 2031 at a 27.36% CAGR.

Which region leads adoption of cloud workload efficiency and carbon-aware scheduling software?

North America led in 2025 with 34.85% share, supported by mature FinOps programs, a dense hyperscaler base, and rising disclosure requirements.

Which regional opportunity is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing geography with a projected 28.67% CAGR, driven by hyperscale expansion, AI compute growth, and stronger regional scheduling needs.

Which application area is creating the strongest new demand?

AI infrastructure optimization is the fastest-growing application at 29.56% CAGR because GPU-heavy workloads create large cost swings, energy waste, and scheduling complexity.

Why are enterprises buying these platforms now instead of relying on existing cloud cost tools?

Buyers increasingly want one control layer that can reduce spend and produce auditable emissions records, especially as AI cost governance and sustainability reporting move into the same operating model.

Which customer groups are shaping current demand the most?

Large enterprises still dominate revenue with 65.41% share, while SMEs are growing faster at 28.12% CAGR as SaaS pricing, open-source tools, and bundled deployments reduce adoption barriers.

Page last updated on: