Carbon-Aware Application Programming Interface (API) and Software Development Kit (SDK) Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

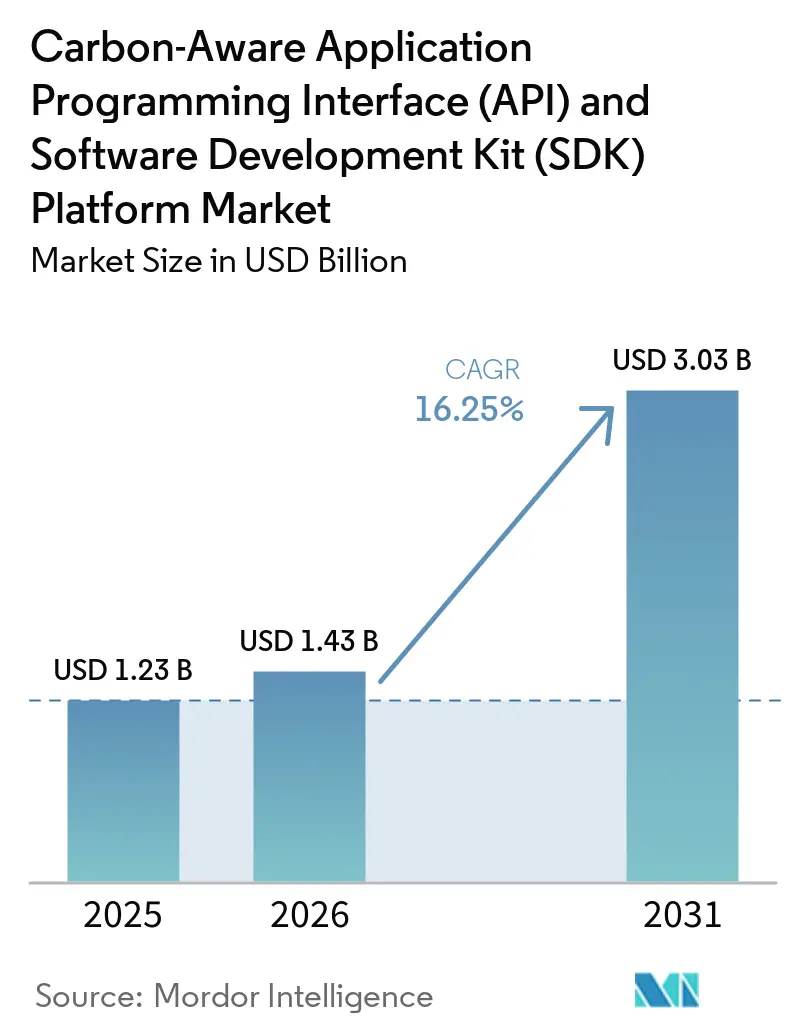

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 16.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbon-Aware Application Programming Interface (API) and Software Development Kit (SDK) Platform Market Analysis by Mordor Intelligence

The carbon-aware application programming interface (API) and software development kit (SDK) platform market size is projected to be USD 1.23 billion in 2025, USD 1.43 billion in 2026, and reach USD 3.03 billion by 2031, growing at a CAGR of 16.25% from 2026 to 2031. The carbon-aware API and SDK platform market is being shaped by tighter emissions disclosure requirements, the rising electricity burden of AI and high-performance computing workloads, and the formal adoption of common software carbon measurement standards. This cycle looks different from earlier sustainability software demand because spending is now being pulled by engineering teams that need live carbon data inside runtime, observability, and scheduling workflows. Open-source tools and formalized software carbon methods are also changing how buyers compare vendors, with more emphasis on data quality, integration depth, and audit-ready outputs than on basic dashboard functionality. The carbon-aware application programming interface (API) and software development kit (SDK) platform market is also benefiting from the link between cloud cost control and carbon control, which is widening the buyer base beyond sustainability teams. Near-term opportunity remains strongest for vendors that can support hybrid environments, simplify deployment, and help smaller suppliers meet machine-readable reporting requirements as disclosure rules move through enterprise supply chains.

Key Report Takeaways

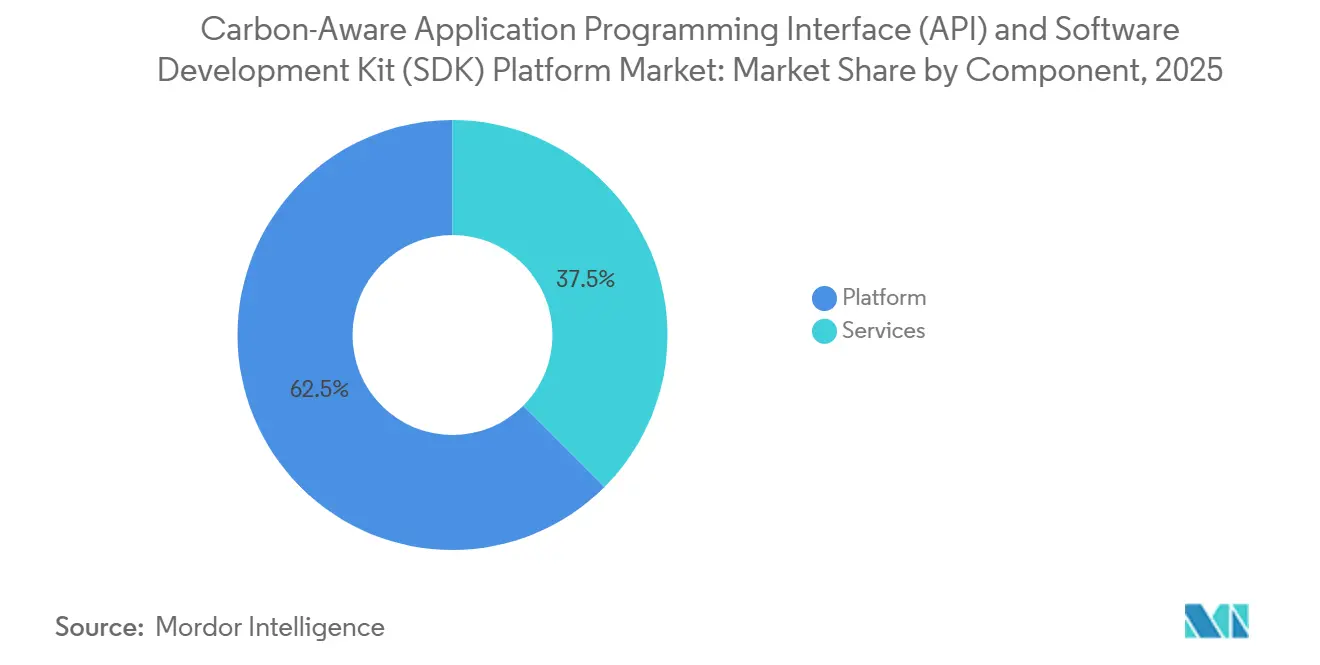

- By component, platform held 62.51% of the carbon-aware application programming interface (API) and software development kit (SDK) platform market share in 2025, while services are projected to expand at 18.15% CAGR through 2031.

- By application, carbon intensity APIs accounted for a 54.23% share of the carbon-aware API and SDK platform market in 2025, while AI and high-performance computing workload optimization are projected to grow at a 17.31% CAGR through 2031.

- By deployment mode, cloud-based deployment captured 68.12% share of the carbon-aware application programming interface and software development kit platform market in 2025, while hybrid deployment is expected to grow at a 17.84% CAGR through 2031.

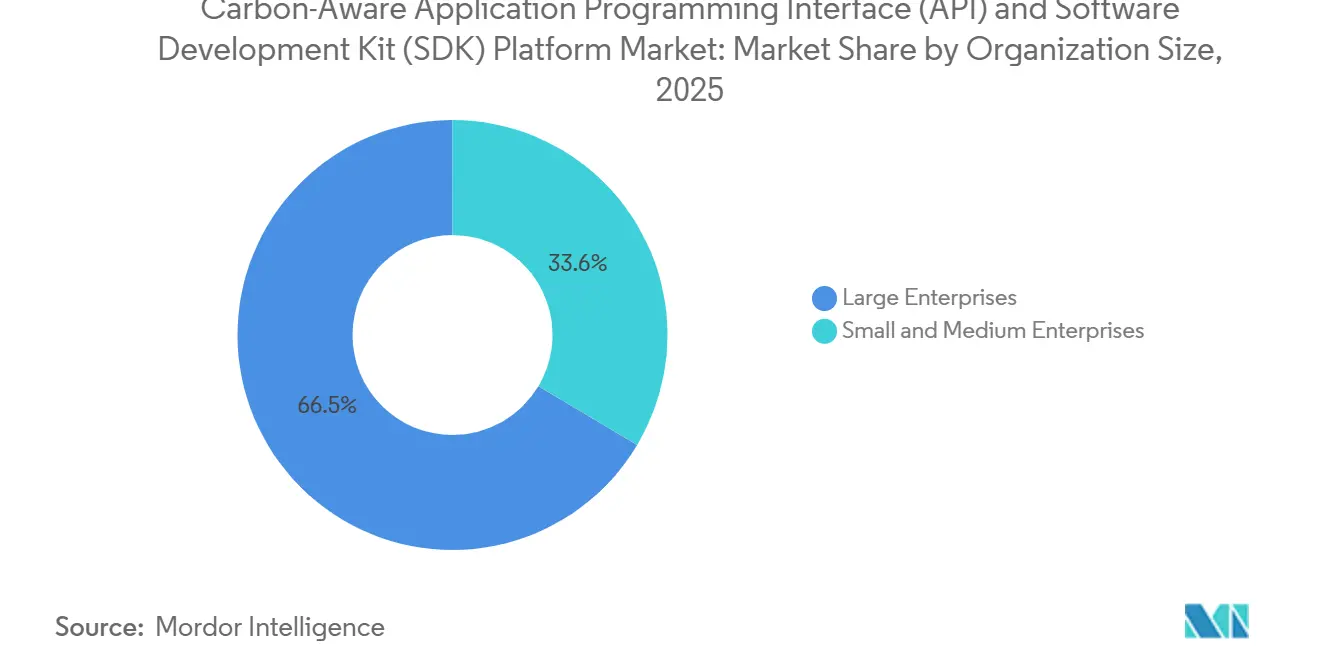

- By organization size, large enterprises held 66.45% share of the carbon-aware API and SDK platform market in 2025, while SMEs are projected to expand at 18.66% CAGR through 2031.

- By end user, information technology and telecom held 29.44% share of the carbon-aware application programming interface and software development kit platform market in 2025, while retail and e-commerce are projected to grow at 16.78% CAGR through 2031.

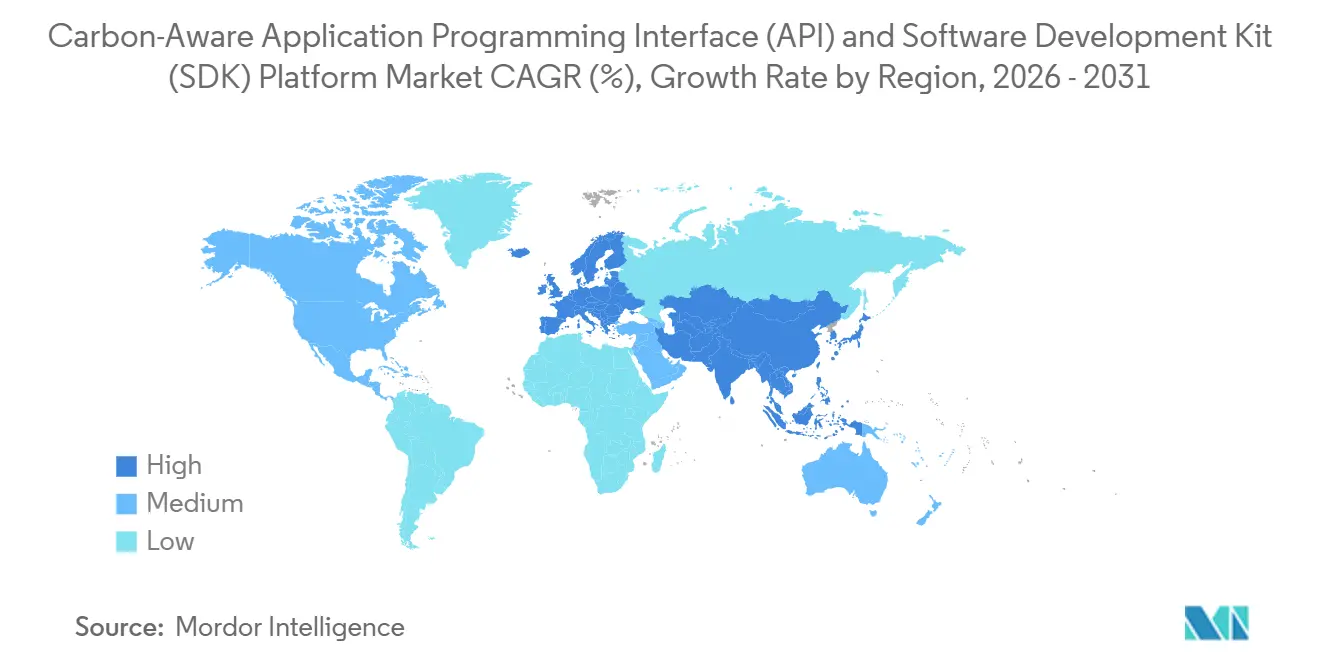

- By geography, North America held 37.29% of the carbon-aware application programming interface (API) and software development kit (SDK) platform market share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 17.04% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Carbon-Aware Application Programming Interface (API) and Software Development Kit (SDK) Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Audit-Ready Carbon Disclosure Requirements | +3.8% | Global, concentrated in Europe and North America, cascading to Asia-Pacific through supply chains | Short term (≤ 2 years) |

| AI and High-Performance Compute Workload Carbon Visibility | +3.5% | Global, core in North America and Asia-Pacific cloud regions, with spillover to Europe GPU clusters | Medium term (2-4 years) |

| FinOps and Carbon Cost Co-Optimization | +3.0% | North America and Europe primarily, extending to Asia-Pacific cloud-native adopters | Medium term (2-4 years) |

| Carbon Intensity API Adoption for Runtime Scheduling | +2.5% | Global, with early gains in North America, Germany, the United Kingdom, and Japan | Short term (≤ 2 years) |

| Standardization of Software Carbon Metrics and Tooling | +1.8% | Global, led by ISO and Green Software Foundation frameworks | Medium term (2-4 years) |

| Embedded Sustainability Controls in Engineering Workflows | +1.2% | North America and Europe primarily, with early enterprise adoption in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Audit-Ready Carbon Disclosure Requirements

The carbon-aware application programming interface (API) and software development kit (SDK) platform market is seeing its strongest commercial pull from mandatory disclosure frameworks that now require more traceable software emissions data. In 2026, many organizations across Europe are filing their first CSRD reports, and this process is raising pressure for structured, machine-readable emissions information that meets assurance requirements. The Software Carbon Intensity method maps software activity into a consistent reporting structure, which gives buyers a clearer way to request comparable carbon data from vendors and internal engineering teams. That shift matters because manual estimates are less useful when procurement teams seek application-level evidence rather than broad annual averages. The carbon-aware API and SDK platform market is therefore moving closer to core enterprise reporting infrastructure, especially for companies that sell software into Europe. State-level obligations, such as California SB 253, are adding a parallel reporting stream outside federal policy, which further broadens the compliance base addressed by these platforms.

AI and High-Performance Compute Workload Carbon Visibility

The carbon-aware application programming interface (API) and software development kit (SDK) platform market is also being driven by the rapid expansion of AI infrastructure and the need to measure its operating footprint with greater precision. Worldwide data center electricity use reached 448TWh in 2025, and current projections point to 945TWh by 2030, which keeps carbon visibility high on infrastructure roadmaps.[1]United Nations University, “Environmental Cost Of AI's Energy Use, Carbon, Water And Land Footprints,” United Nations University, unu.edu The mix of energy demand is also changing because inference accounts for 80-90% of total AI energy consumption, so the measurement problem now sits in live production environments rather than only in model training labs. The Green Software Foundation ratified SCI for AI in late 2025, providing developers with a standard way to evaluate per-inference-request carbon intensity across GPU-heavy workloads. Peer-reviewed research also showed that carbon-aware AI scheduling can cut carbon use by up to 41% while keeping latency increases within 1.1-1.7%, which weakens the argument that lower emissions must come with a material performance penalty. As a result, the carbon-aware API and SDK platform market is gaining greater prominence in AI operations stacks where teams need both visibility and control.

FinOps and Carbon Cost Co-Optimization

The carbon-aware API and SDK platform market is attracting more attention as cost and emissions optimization are increasingly handled together. Flexera reported in 2026 that, for nearly one-third of respondents, reducing cloud costs and reducing carbon emissions carried equal priority, indicating that these buying decisions are no longer the sole purview of sustainability teams. At the same time, the 2025 State of FinOps Report showed that only 3% of FinOps practices globally were making optimization decisions based on carbon, even though 53% of European practices already reported cloud carbon data, suggesting a significant execution gap. That gap creates space for vendors that can connect billing, utilization, and carbon signals within a single operating workflow rather than in separate reporting streams. The carbon-aware application programming interface (API) and software development kit (SDK) platform market benefits from this shift because APIs and SDKs are the layer that can feed both cost and carbon decisions into engineering tools. Vendors that show a joint financial and emissions outcome are likely to move through procurement faster than vendors that position only around compliance.

Carbon Intensity API Adoption for Runtime Scheduling

The carbon-aware application programming interface (API) and software development kit (SDK) platform market is expanding as carbon-intensity APIs move from pilot tools into production-grade scheduling infrastructure. WattTime released updated North America data models in March 2026 that improved the average marginal emissions forecast impact by 3.3% and expanded renewable curtailment detection across 25 additional grid regions, thereby improving temporal workload-shifting decisions. The Green Software Foundation Carbon Aware SDK has also matured into a practical normalization layer that supports API calls across providers such as WattTime and Electricity Maps, delivering unified output. Provider fragmentation still slows adoption because grid data sources differ in temporal resolution, geographic coverage, and emissions methodologies, especially when average and marginal emissions yield different scheduling signals. Vendors that package normalization and multi-region orchestration into ready-to-deploy software are in a stronger pricing position because they remove technical work that buyers do not want to handle alone. That dynamic keeps the carbon-aware application programming interface and software development kit platform market tied not only to raw data access, but also to the software layer that makes those data streams usable inside production systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Carbon Signal Data Quality Across Providers | -2.8% | Global, most acute in Asia-Pacific and South America where grid telemetry coverage is sparse | Medium term (2-4 years) |

| Integration Burden Across Cloud, DevOps, and Application Stacks | -2.2% | Global, particularly in hybrid and multi-cloud enterprise environments | Short term (≤ 2 years) |

| Performance Tradeoffs in Aggressive Carbon-Aware Scheduling | -1.5% | Global, most pronounced in latency-sensitive financial and healthcare workloads | Medium term (2-4 years) |

| Limited Buyer Readiness to Operationalize Developer-Facing Carbon Workflows | -1.0% | Emerging markets and smaller enterprises globally, with a longer adoption runway | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Carbon Signal Data Quality across Providers

The carbon-aware application programming interface (API) and software development kit (SDK) platform market still faces a major deployment barrier due to uneven data quality across carbon signal providers and regions. Coverage gaps are most visible in parts of South and Southeast Asia, Sub-Saharan Africa, and South America, where real-time marginal emissions data are limited or absent, forcing buyers to fall back on weaker annual-average proxies. Even in mature markets, the difference between average and marginal emissions intensity can lead to materially different scheduling decisions, especially in grids with high renewable penetration. WattTime and REsurety launched a free global Grid Emissions Data platform in March 2025, which improved access to hourly marginal data for qualified users but did not fully address real-time forecast quality in constrained regions. Buyers are therefore still exposed to methodology risk when they compare vendors that appear to address the same use case but differ in their underlying assumptions. This limits the pace at which the carbon-aware API and SDK platform market can move from targeted deployments to broader enterprise standardization.

Integration Burden Across Cloud, DevOps, and Application Stacks

The carbon-aware API and SDK platform market also grows more slowly, where deployment requires coordination across teams and tools that were not originally designed for sustainability instrumentation. A production-grade rollout often requires a carbon data provider, observability layers such as Prometheus or OpenTelemetry, autoscaling logic, and CI/CD controls to work together within a single operating path. The 2025 State of FinOps Report showed that reported cloud carbon data did not automatically translate into carbon-based optimization decisions, underscoring the gap between visibility and operational adoption. Carbon-aware Kubernetes frameworks help at the orchestration level, but they still require region- and workload-specific configuration, which stretches implementation timelines for mid-sized engineering teams. That burden increases demand for professional services, but it also raises the cost and complexity of production rollouts. As a result, the carbon-aware application programming interface (API) and software development kit (SDK) platform market still has a gap between technically possible pilots and enterprise-scale deployments that can last across multiple quarters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Consolidates Revenue, Services Accelerating on Implementation Demand

Platform solutions held 62.51% of the carbon-aware application programming interface (API) and software development kit (SDK) market in 2025, making the integrated delivery model the preferred choice for early enterprise adoption. Buyers favored bundled platforms because they reduce the work needed to connect API management, carbon signal normalization, and reporting dashboards across multiple teams. This preference was strongest among large organizations that could justify higher license costs in exchange for faster time-to-value and lower integration effort. Early adoption also leaned toward technically mature customers, such as hyperscalers, global banks, and large technology firms, that already had strong internal platform engineering capabilities. In that context, the carbon-aware API and SDK platform market rewarded vendors that could deliver a managed operating environment rather than a narrow point tool.

Services are projected to expand at a 18.15% CAGR through 2031, indicating that tooling alone is not enough for many new buyers. The next wave of customers includes organizations that need help translating ISO-compliant software carbon methods into client-specific pipelines and operating policies. Amadeus transferred Carmen, its production-grade carbon measurement engine, to the Green Software Foundation in January 2026, which signals that core measurement tooling is becoming easier to access while implementation expertise remains commercially valuable. The carbon-aware application programming interface (API) and software development kit (SDK) platform industry is therefore moving toward a model where license revenue and services revenue reinforce each other rather than compete.

By Application: Carbon Intensity APIs Lead, AI Workload Optimization Emerges as Strategic Priority

Carbon intensity APIs accounted for 54.23% of the carbon-aware application programming interface (API) and software development kit (SDK) platform market in 2025, reflecting their role as the primary data layer for downstream scheduling and reporting tools. This position is structural rather than temporary because most other application categories still depend on a reliable stream of carbon-intensity data before any optimization can happen. Carbon-aware Kubernetes scheduling and CI/CD workflow integration are already meaningful use cases, but they remain more fragmented because deployment logic changes across clouds, clusters, and software delivery practices. The carbon-aware API and SDK platform market, therefore, continues to center on the data layer that feeds all other application behavior. Vendors with dependable signal quality and strong normalization capabilities remain closer to the center of buyer decision-making than those that offer only narrower orchestration features.

AI and high-performance computing workload optimization is projected to grow at a 17.31% CAGR through 2031, making it the fastest-growing application area. That growth follows the shift in AI energy demand toward live inference, where scheduling decisions can be repeated at scale across high-frequency production workloads. The Green Software Foundation’s SCI for AI work provides a more formal measurement framework for that use case, making it easier for enterprise teams to justify investment in workload-level carbon controls. Other applications, such as edge scheduling and IoT telemetry, remain early, but they benefit as carbon data becomes more ambient across connected systems and developer tools.

By Deployment Mode: Cloud Dominates, Hybrid Architectures Gain Enterprise Traction

Cloud-based deployment held a 68.12% share in 2025, underscoring how closely the carbon-aware application programming interface (API) and software development kit (SDK) platform market aligns with cloud-native operating models. Most real-time carbon data flows arrive via external APIs, making cloud environments the easiest place to ingest, route, and act on those signals. Cloud deployment also supports frequent updates to emissions factor libraries and grid models without the repeated release cycles that on-premises setups would require. On-premises deployment remains relevant for organizations with data sovereignty, risk, or network routing constraints that limit how certain workloads can connect to outside services. Even so, the carbon-aware application programming interface and software development kit platform market still shows stronger revenue concentration in the cloud, as deployment friction is lower there than in tightly controlled internal environments.

Hybrid deployment is projected to record a 17.84% CAGR through 2031, making it the fastest-growing deployment mode. This pattern fits enterprises that keep latency-sensitive or regulated workloads on dedicated infrastructure while shifting flexible AI training, reporting, and batch processing into lower-carbon cloud windows. Flexera reported that cloud resource rightsizing can deliver 25-40% cost reductions and proportional carbon savings, supporting the business case for architectures that combine cloud access with tighter workload placement logic.[2]Flexera, “From Dashboard To Operating Model, A 30-60-90-Day Playbook For Cloud Sustainability In FinOps,” Flexera, flexera.com The carbon-aware API and SDK platform market has a clear opening for vendors that can consistently manage policy, carbon signals, and orchestration across public cloud, private cloud, and on-premises assets.

By Organization Size: Large Enterprises Anchor Baseline, SMEs Emerge as High-Velocity Cohort

Large enterprises held a 66.45% share in 2025, reflecting that the earliest buyers were already under mandatory disclosure pressure or running very large IT estates where small scheduling changes can matter at scale. These organizations were more willing to absorb the integration effort needed to feed carbon data into observability stacks, cloud operations tools, and internal reporting systems. They also tended to place higher value on audit-ready outputs and enterprise controls than on low initial deployment cost. In the carbon-aware application programming interface (API) and software development kit (SDK) platform market, that profile favored vendors with broader compliance support and deeper implementation. Large enterprise demand therefore built the initial revenue base even as newer buyer groups began to emerge.

SMEs are projected to grow at a 18.66% CAGR through 2031, the highest among the segmentation types covered in the input. The main trigger is the supply-chain cascade created by large customers that now want machine-readable emissions data from smaller technology suppliers. That requirement is difficult to meet with manual spreadsheets or one-off reporting, because buyers increasingly expect repeatable, API-based data exchange. The carbon-aware application programming interface (API) and software development kit (SDK) platform industry is responding with simpler integration models, but smaller customers still face procurement requirements around security, trust, and reporting reliability. As a result, SMEs are becoming the fastest-growing demand cohort, even though large enterprises remain the largest revenue pool today.

By End User: IT and Telecom Anchors the Market, Retail and E-Commerce Accelerating on Consumer Transparency Pressure

Information technology and telecom held a 29.44% share in 2025, reflecting the sector’s dual role as both a software producer and an operator of carbon-intensive digital infrastructure. That position gives the sector a stronger reason than most others to measure and optimize software-related emissions at the application and infrastructure layers. Banking, financial services, and insurance also remain a major user group because digital service delivery is extensive, and reporting pressure increasingly extends to software operations as part of broader financing and operational emissions programs. Energy and utilities use these platforms differently, often aligning internal IT optimization with generation portfolios and energy management goals. Within the carbon-aware application programming interface (API) and software development kit (SDK) platform market, this broad end-user mix reduces dependence on any single vertical, even though IT and telecom remain the largest anchors.

Retail and e-commerce are projected to grow at a 16.78% CAGR through 2031, driven by high digital transaction volumes and rising transparency expectations. Recommendation engines, order management systems, and customer-facing applications process very large volumes of API calls, so even modest reductions in carbon intensity per request can become meaningful at scale. This makes temporal and geographic workload shifting more commercially relevant for retailers than it might first appear. The carbon-aware API and SDK platform market is also gaining relevance here, as product-level sustainability claims increasingly depend on cleaner digital support systems and cleaner physical supply chains.

Geography Analysis

North America held 37.29% of the carbon-aware API and SDK platform market share in 2025, maintaining its position as the leading regional demand center. The region benefits from dense hyperscale infrastructure, large cloud-native developer communities, and early exposure to carbon-aware open-source tooling. California SB 253 and SB 261 broadened the compliance base by creating disclosure pressure that does not depend on federal climate rule continuity. The SEC proposed rescinding its climate disclosure rules in May 2026, but that change did not remove state-level obligations or address the needs of companies that still operate in stricter overseas reporting environments.[3]Securities and Exchange Commission, “Rescission Of Climate-Related Disclosure Rules,” U.S. Securities and Exchange Commission, sec.gov South America remained smaller, with Brazil providing the clearest near-term signal through its large IT sector and through subsidiaries tied to European reporting expectations.

Europe did not have a disclosed regional share figure in the input, yet it remained the most policy-dense part of the carbon-aware application programming interface (API) and software development kit (SDK) platform market. CSRD reporting in 2026 is increasing demand for application-level software emissions data that can be structured in a more consistent and auditable form. Germany, the United Kingdom, and France stood out as the largest national demand centers because they combine strong enterprise reporting maturity with large developer and cloud ecosystems. The Middle East is still early, but sovereign cloud programs in Saudi Arabia and the UAE are beginning to create a policy-led opening for carbon measurement in data center and digital infrastructure planning.

Asia-Pacific is projected to grow at a 17.04% CAGR through 2031, making it the fastest-growing regional market for the carbon-aware application programming interface and software development kit platform market. Japan is shaping much of that momentum through its evolving SSBJ disclosure guidance and NTT’s March 2026 publication of CO₂ rules for the cradle-to-grave software lifecycle. South Korea adds another policy anchor with mandatory ESG reporting for large listed companies, while India’s growth is led more by export-oriented IT services exposure than by domestic regulation. China is building a longer-term pathway through standards participation and broader carbon policy development, while Africa remains nascent, with demand concentrated in a small number of multinational-linked operations.

Competitive Landscape

The carbon-aware application programming interface (API) and software development kit (SDK) platform market remained fragmented, with open-source projects, data providers, API-first specialists, and broader enterprise sustainability platforms all competing across different layers of the stack. No single vendor dominated across carbon data provision, SDK tooling, workload integration, and compliance reporting, so buyers often evaluated vendors by layer depth rather than by total platform breadth. Commercial differentiation centered on data accuracy, connector breadth, and the ability to generate outputs aligned with recognized software carbon methods. Open-source work from the Green Software Foundation continued to widen the developer base while also making it harder for commercial vendors to compete on basic access alone.[4]Green Software Foundation, “Green-Software-Foundation Carbon-Aware-SDK,” GitHub, github.com That balance kept the carbon-aware API and SDK platform market competitive without turning it into a price-only contest.

Several strategic moves in 2025 and 2026 showed how vendors and ecosystem players were trying to deepen their position. Amadeus transferred Carmen to the Green Software Foundation in January 2026, lowering the entry barrier for SCI-aligned software measurement and pushing commercial differentiation further toward deployment and integration services. WattTime updated its North America API data models in March 2026, improving forecast accuracy and expanding curtailment visibility, thereby strengthening the value of high-quality signal providers within optimization workflows. NTT also published software lifecycle CO₂ calculation rules in March 2026, which signaled that enterprise procurement and software operations in Japan are moving toward more formalized carbon measurement expectations.

The clearest commercial gap remains in hybrid orchestration, where buyers want a carbon scheduling layer that can span bare metal, private cloud, and public cloud without heavy custom work. Smaller specialists are moving through scheduler extensions and focused integrations, while larger incumbents often rely on services-led delivery to bridge deployment complexity. Standards participation and ecosystem alignment are therefore becoming part of competitive positioning, as buyers want tools that align with a stable measurement model rather than a one-off vendor method. Overall, the carbon-aware application programming interface (API) and software development kit (SDK) platform market remains open enough for new entrants, but scale advantages now come more from integration reach and a trusted methodology than from simple carbon dashboard functionality.

Carbon-Aware Application Programming Interface (API) and Software Development Kit (SDK) Platform Industry Leaders

Watershed Technology, Inc.

Sphera Solutions, Inc.

Persefoni AI, Inc.

Normative AB

Greenly SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sweep SAS announced a complete cloud emissions measurement solution built on the AWS Sustainability service, enabling enterprise customers to automatically consolidate audit-ready Scope 1, 2, and 3 cloud emissions data into their carbon accounting workflows. The integration, developed as an AWS ISV-Accelerate partner, eliminates manual data extraction and positions Sweep's platform as a connector between hyperscaler emissions APIs and enterprise carbon reporting pipelines.

- March 2026: WattTime released new North America API data models, Model 2026-03-01, improving CO₂ MOER forecast accuracy by 3.3% on average and expanding renewable curtailment detection across 25 new grid regions in the Western Interconnect and PSCO, Colorado. The update is projected to increase the CO₂ reduction opportunity for carbon-aware scheduling workloads by 25% in North America.

- March 2026: NTT, Inc. published cradle-to-grave CO₂ emissions calculation rules for the full software product lifecycle, aligning with Japan's Ministry of Economy, Trade and Industry Carbon Footprint Guidelines. This initiative, led through the Japan Environment Club's Software Decarbonization Research Group, expands addressable software lifecycle carbon reporting from procurement and development to include operations and end-of-life, a foundational step toward green procurement mandates for software APIs in Japanese enterprise markets.

- January 2026: Amadeus transferred ownership of Carmen, its production-grade Carbon Measurement Engine integrating with Kubernetes and Prometheus, to the Green Software Foundation. The move makes a battle-tested SCI implementation tool freely available to enterprise engineering teams, lowering the barrier for organizations seeking per-application carbon measurement without building custom pipelines.

Global Carbon-Aware Application Programming Interface (API) and Software Development Kit (SDK) Platform Market Report Scope

The carbon-aware API and SDK platform market encompasses APIs and SDKs that infuse carbon intelligence into applications and developer processes. These platforms offer real-time carbon intensity metrics, emission calculation capabilities, and software-integration optimization features. They empower applications to make informed carbon decisions across areas such as routing and resource distribution. By embedding in CI/CD pipelines and development settings, these tools champion the development of eco-friendly, low-emission digital services.

The Carbon-Aware Application Programming Interface (API) and Software Development Kit (SDK) Platform Market Report is Segmented by Component (Platform, and Services [Implementation and Integration Services, and Support and Maintenance Services]), Application (Carbon-Aware Kubernetes Scheduling, Carbon Intensity APIs, AI and High-Performance Computing Workload Optimization, Continuous Integration (CI)/Continuous Delivery (CD) and Developer Workflow Integration, and Other Applications), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End User (Information Technology and Telecom, Banking, Financial Services, and Insurance, Energy and Utilities, Manufacturing, Retail and E-Commerce, Healthcare and Life Sciences, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform | |

| Services | Implementation and Integration Services |

| Support and Maintenance Services |

| Carbon-Aware Kubernetes Scheduling |

| Carbon Intensity APIs |

| AI and High-Performance Computing Workload Optimization |

| Continuous Integration (CI)/Continuous Delivery (CD) and Developer Workflow Integration |

| Other Applications |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Information Technology and Telecom |

| Banking, Financial Services, and Insurance |

| Energy and Utilities |

| Manufacturing |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Platform | |

| Services | Implementation and Integration Services | |

| Support and Maintenance Services | ||

| By Application | Carbon-Aware Kubernetes Scheduling | |

| Carbon Intensity APIs | ||

| AI and High-Performance Computing Workload Optimization | ||

| Continuous Integration (CI)/Continuous Delivery (CD) and Developer Workflow Integration | ||

| Other Applications | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End User | Information Technology and Telecom | |

| Banking, Financial Services, and Insurance | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Healthcare and Life Sciences | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the carbon-aware application programming interface (API) and software development kit (SDK) space?

The carbon-aware application programming interface (API) and software development kit (SDK) platform market size stood at USD 1.23 billion in 2025, reached USD 1.43 billion in 2026, and is projected to reach USD 3.03 billion by 2031 at a 16.25% CAGR.

Which application area leads carbon-aware API and SDK platform demand today?

Carbon intensity APIs led with a 54.23% share in 2025 because they act as the base data layer for scheduling, routing, and reporting functions across software environments.

Which customer group is expanding fastest in carbon-aware API and SDK platforms?

SMEs are projected to grow at 18.66% CAGR through 2031 as larger customers ask smaller suppliers to provide machine-readable emissions data through standardized digital interfaces.

Why is AI increasing demand for carbon-aware development tools?

AI and HPC workload optimization is projected to grow at 17.31% CAGR, supported by the rising electricity burden of inference-heavy workloads and the need for real-time carbon visibility.

Which region offers the strongest near-term demand?

North America led with 37.29% share in 2025, while Asia-Pacific is projected to expand fastest at 17.04% CAGR through 2031.

What is the biggest challenge for enterprise adoption of carbon-aware API and SDK platforms?

Data fragmentation and integration burden remain the main barriers because buyers still need to align carbon signal providers, observability tools, orchestration layers, and reporting workflows before they can scale production use.

Page last updated on: