Cloud Telephony Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.17 Billion |

| Market Size (2031) | USD 45.57 Billion |

| Growth Rate (2026 - 2031) | 9.32% CAGR |

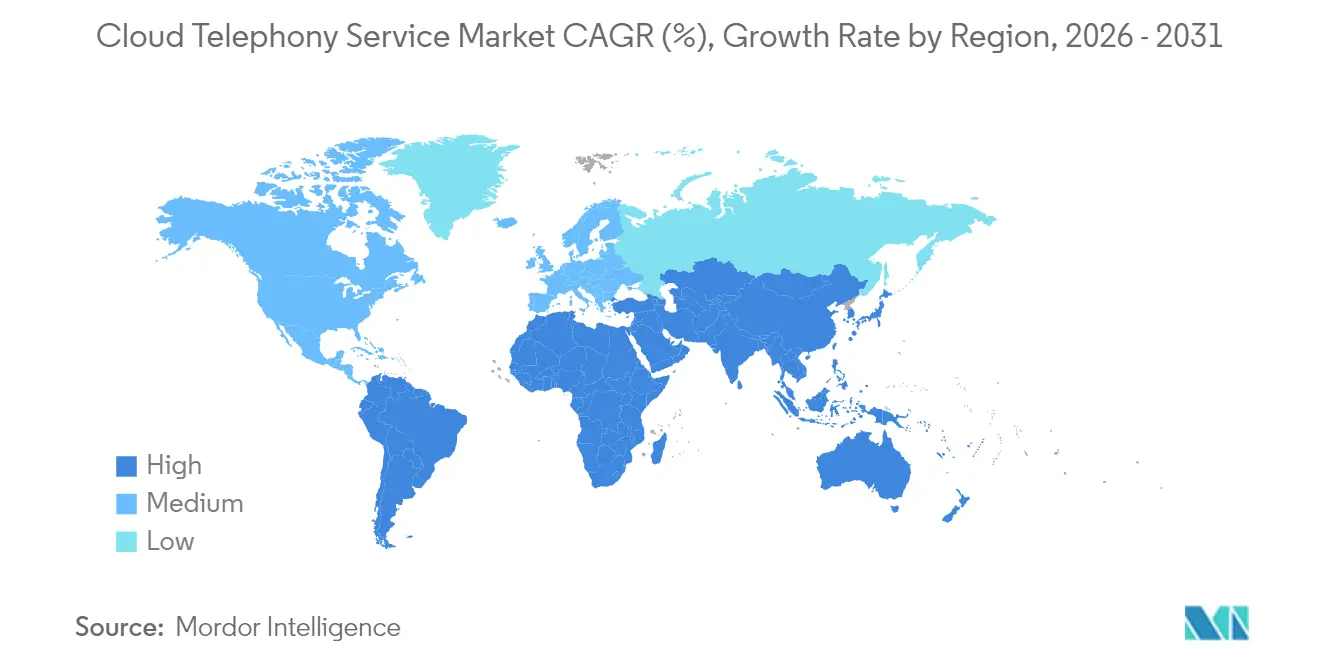

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

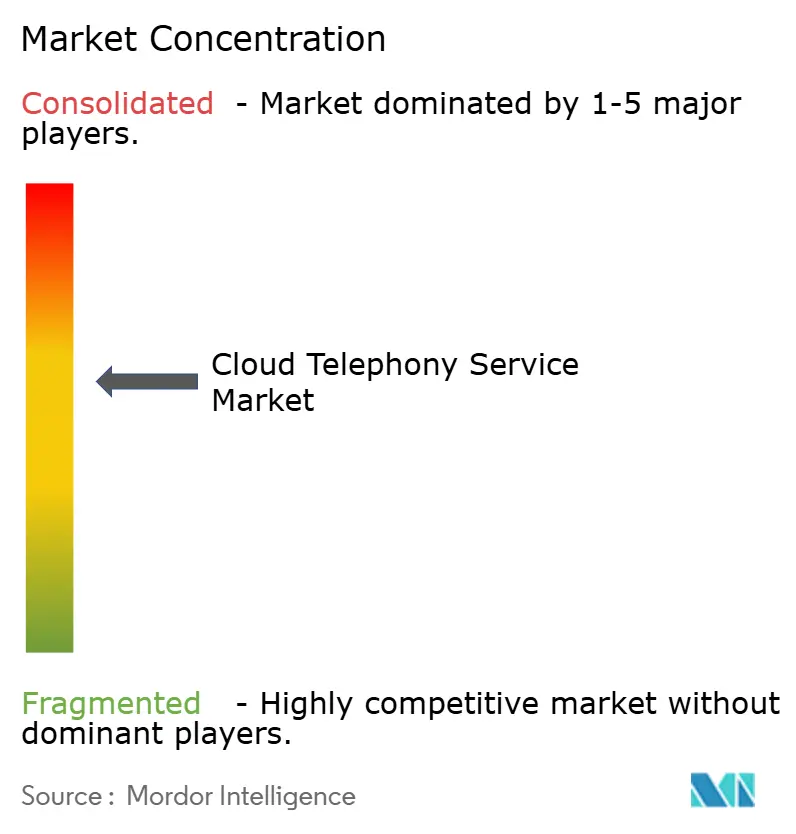

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Telephony Services Market Analysis by Mordor Intelligence

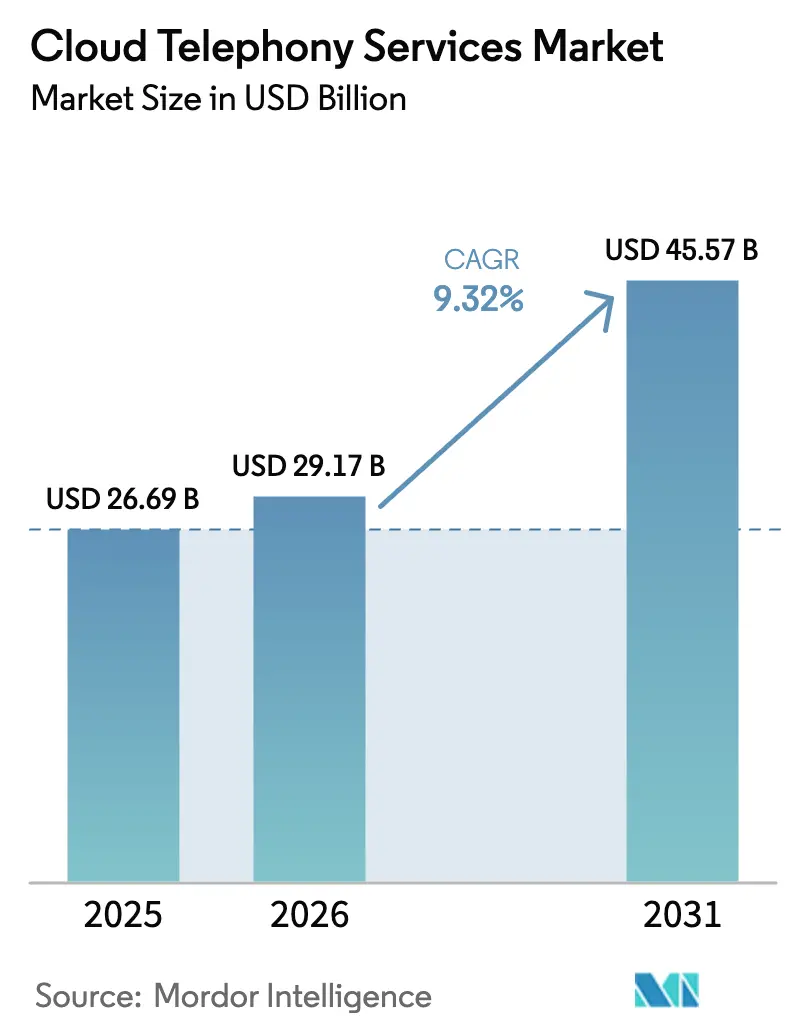

The Cloud Telephony Services Market size was valued at USD 26.69 billion in 2025 and estimated to grow from USD 29.17 billion in 2026 to reach USD 45.57 billion by 2031, at a CAGR of 9.32% during the forecast period (2026-2031).

This period of sustained expansion mirrors a global migration from hardware-based PBX estates toward cloud-native unified communications, where enterprises gain lower operating costs, on-demand scalability, and simplified global reach. Adoption momentum is reinforced by AI-infused contact-center productivity tools, expanding telco API ecosystems, and intensifying green data-center mandates that favor virtualized voice workloads over on-premises switching. Competitive intensity rises as traditional telecom carriers pivot to software, hyperscale clouds court voice traffic, and pure-play vendors differentiate through vertical packages and developer-centric platforms. While security and bandwidth reliability still temper uptake in heavily regulated and emerging markets, the overwhelming trend signals a decisive long-term tilt toward cloud-first telephony architectures in every major region.

Key Report Takeaways

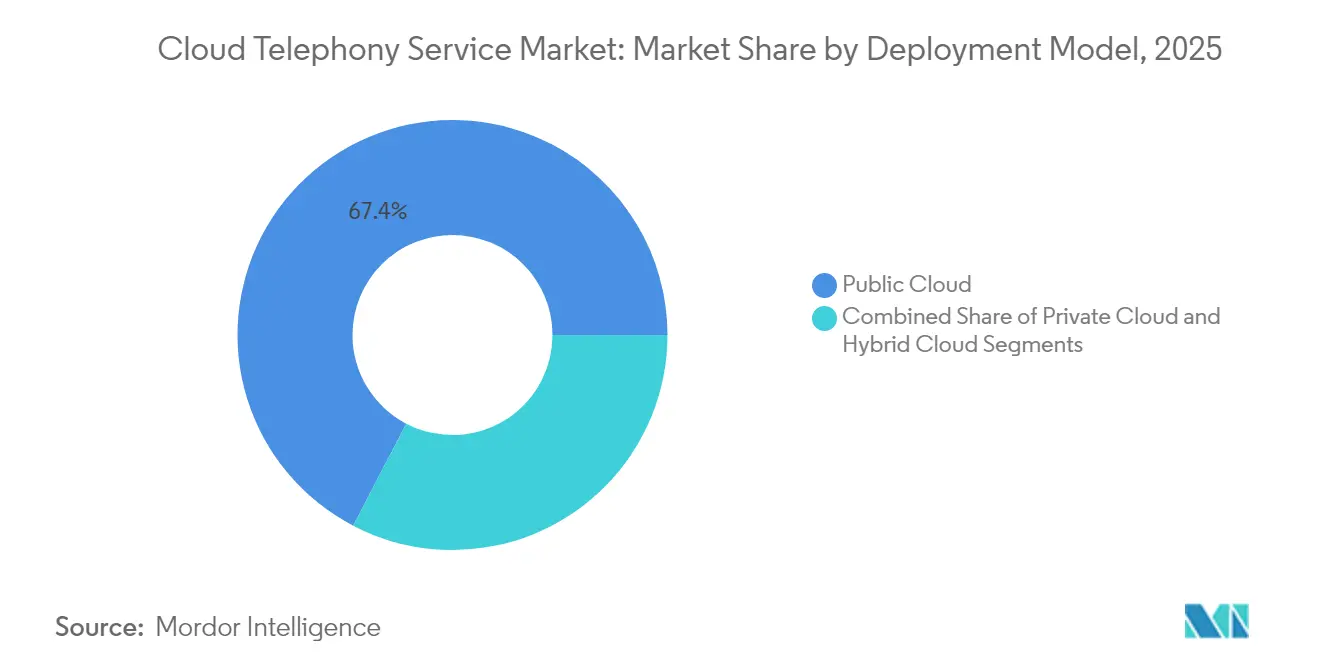

- By deployment model, the public cloud captured 67.35% of the cloud telephony services market share in 2025, whereas hybrid configurations are expanding at a 10.12% CAGR through 2031.

- By service type, UCaaS held 41.05% of the cloud telephony service market size in 2025, while CPaaS is advancing at an 10.78% CAGR over the same horizon.

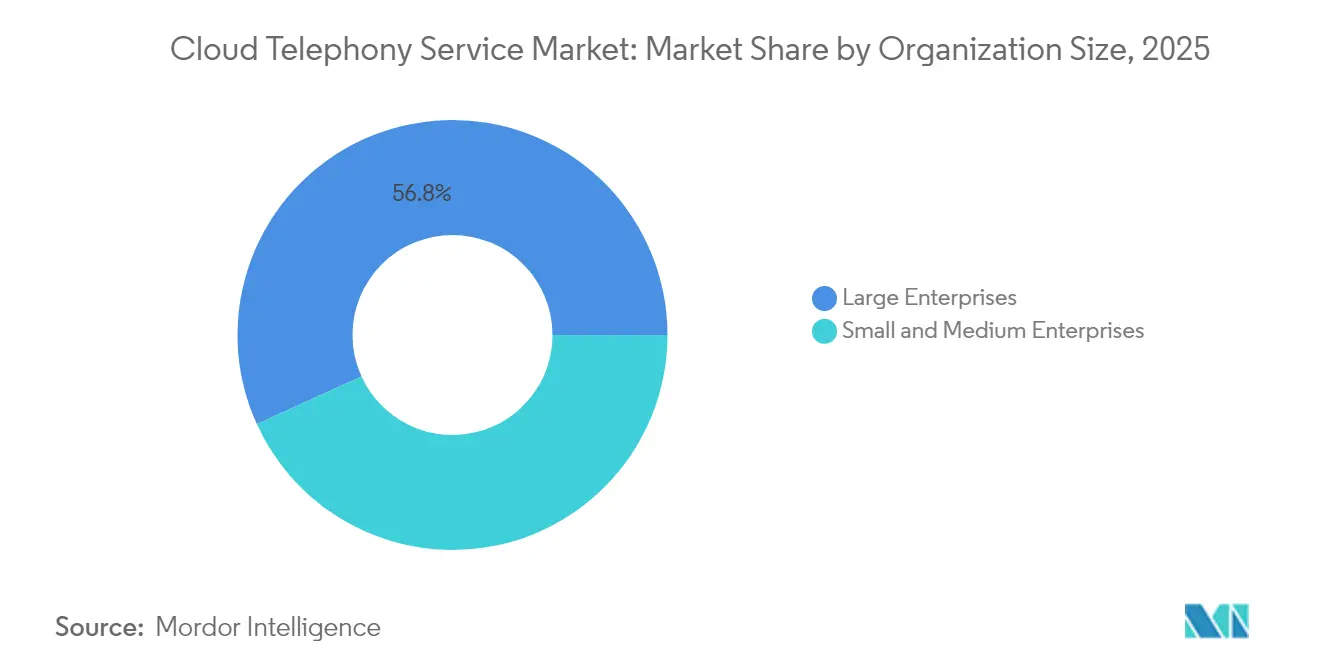

- By organization size, large enterprises controlled 56.80% of the cloud telephony services market in 2025; small and medium enterprises are growing at a 10.28% CAGR to 2031.

- By end-user vertical, IT and telecom commanded 24.05% of the cloud telephony service market size in 2025, but healthcare is projected to deliver an 10.95% CAGR.

- By geography, North America led with 36.95% revenue share in 2025; Asia Pacific is set to post a 10.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Telephony Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy PBX transition to cloud UC | +2.1% | Global with emphasis on North America and Europe | Medium term (2-4 years) |

| Persistent remote & hybrid work culture | +1.8% | Urban centers worldwide | Short term (≤ 2 years) |

| Public-cloud OPEX and elastic scalability | +1.2% | Cost-sensitive SME segments globally | Long term (≥ 4 years) |

| AI-enhanced contact-center productivity | +0.9% | North America and Europe early, APAC following | Medium term (2-4 years) |

| Telco API monetization in SaaS ecosystems | +0.6% | Developed markets across all regions | Long term (≥ 4 years) |

| Green data-center mandates | +0.4% | European Union leading; North America and APAC catching up | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy PBX Transition to Cloud UC

Enterprises are resigning aging PBX equipment in favor of unified communications clouds that remove hardware refresh cycles, specialized telephony talent, and capacity-planning overheads. Microsoft Teams Phone illustrates this shift by embedding global voice inside existing productivity suites and cutting total cost of ownership by up to 30%.[1]Microsoft Corporation, “Microsoft Teams Phone,” microsoft.comDecision makers increasingly treat voice workloads as part of a broader digital platform, using analytics, AI services, and mobile interoperability that simply are not feasible on premises. Depreciation schedules of physical PBX assets align neatly with five-year cloud migration plans, encouraging wholesale replacement projects. As licensing bundles include voice, messaging, and video under one predictable subscription, financial controllers favor the subscription model. Collectively, these factors add 2.1 percentage points to overall CAGR, making the transition the single most important accelerator for the cloud telephony service market.

Remote and Hybrid Work Culture Surge

Hybrid work is now a structural, not temporary, feature of global employment. Knowledge workers expect the same call quality at home, in coworking spaces, and in headquarters, forcing IT teams to prioritize location-agnostic voice solutions. Cisco Webex Calling routes PSTN traffic through cloud-connected providers to secure compliance while letting roaming employees retain their existing extensions. Organizations also use mobility-optimized softphones that integrate calendars and CRM records, ensuring workflow continuity. The cultural change touches every industry, so demand spikes across enterprise size bands rather than being restricted to technology firms. The result adds 1.8 percentage points to cloud telephony services market growth, especially in North America, Europe, and rapidly urbanizing APAC hubs.

Public-Cloud OPEX & Elastic Scalability

Public-cloud voice eliminates up-front hardware spend, spreads costs through per-user models, and lets operators dial capacity up or down in minutes. This economic flexibility resonates with SMEs that cannot afford over-provisioned PBX trunks during seasonal peaks. Real-time billing dashboards enable CFOs to cross-charge usage back to business units, creating transparent cost governance. For multinationals, geographic expansion becomes a matter of licensing rather than building local exchanges. These factors collectively inject 1.2 percentage points into the CAGR and cement public clouds as the default backbone of the cloud telephony services market.

AI-Enhanced Contact-Center Productivity

AI is redefining agent workflows by offering sentiment scoring, intent routing, and contextual coaching. NICE CXone Mpower now processes more than 100 million interactions each month, surfacing real-time insights that shorten handle times and lift first-call resolution. Voicebots triage routine queries, freeing human agents for complex tasks. Predictive models allocate staff in line with forecasted call volumes, eliminating idle time. The productivity gains feed straight into ROI calculations, adding 0.9 percentage points to growth and pushing enterprises to adopt cloud telephony platforms that already bundle AI frameworks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VoIP security and compliance hurdles | -1.3% | Global, highest in regulated verticals | Short term (≤ 2 years) |

| Broadband QoS gaps in emerging markets | -0.8% | APAC emerging, Latin America, Africa | Medium term (2-4 years) |

| Hyperscale cloud egress-fee lock-in risk | -0.7% | Multiregional multi-cloud adopters | Long term (≥ 4 years) |

| Feature-parity limits in vertical workflows | -0.5% | Healthcare and financial services | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

VoIP Security & Compliance Hurdles

The rising threat surface of IP communications puts encryption, fraud prevention, and lawful interception back on executive agendas. New California VoIP licensing rules illustrate increasingly stringent oversight, compelling providers to secure separate authorizations and report traffic metrics. In multi-jurisdiction deployments, enterprises juggle overlapping privacy statutes that stipulate domestic call recording or data residency. Board-level risk committees often demand third-party audits before approving contracts, which lengthens procurement cycles. The resulting headwinds remove 1.3 percentage points from the CAGR, especially in healthcare, finance, and public sector accounts.

Broadband QoS Gaps in Emerging Markets

In parts of Southeast Asia, Latin America, and sub-Saharan Africa, last-mile connectivity struggles to maintain consistent jitter and packet-loss thresholds. Voice degradation damages brand perception, causing local subsidiaries to defer migrations. Service-level agreements rarely guarantee enterprise-grade MOS scores outside metropolitan cores, so organizations keep fall-back analog trunks. Network-upgrade roadmaps are improving, but the deficiency still subtracts 0.8 percentage points from market growth over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Strategies Balance Control and Agility

Hybrid cloud deployments represent the fastest-expanding configuration at a 10.12% CAGR, even as the public cloud owns 67.35% of the 2025 cloud telephony services market size. Enterprises blend private data centers for sensitive workloads with elastic public capacity for standard traffic, mitigating both latency and sovereignty risks. Banking, healthcare, and defense institutions often keep compliance-critical recordings inside national borders while routing overflow through regional hubs. The model also supports phased migrations, letting IT teams move country offices one cluster at a time without service disruption.

Private cloud installations serve narrower use cases. Government agencies operating classified networks or stock exchanges that cannot tolerate shared infrastructure rely on dedicated environments. Although capital intensive, these rollouts lock down physical access, permit hardware cryptography modules, and comply with bespoke certification regimes. Growth in the cloud telephony service market remains modest but stable as such institutions modernize legacy PBX hardware on a one-for-one basis. Conversely, the public cloud continues to seduce mid-market enterprises with plug-and-play provisioning, global numbering pools, and rapid feature drops. Expect the public tier to retain a majority share yet see incremental dilution as hybrid gains traction through 2031.

By Service Type: CPaaS Unlocks Programmable Connectivity

UCaaS anchored 41.05% of the cloud telephony services market in 2025, cementing its role as the default replacement for desk phones, voicemail, and conferencing. Vendors enrich suites with task management, whiteboarding, and intranet-quality video, making the bundle a one-stop collaboration stack. Contact-center-as-a-service (CCaaS) claims a healthy slice thanks to AI tooling that automates agent workflows. Cloud PBX and SIP trunking persist for organizations wishing to retain physical handsets or protect existing investments while still routing calls through the cloud.

The breakout performer is communications-platform-as-a-service, which is growing at 10.78% annually as developers stitch voice, SMS, video, and authentication functions directly into customer applications. Retailers embed click-to-call widgets at checkout, while logistics apps auto-dispatch driver alerts in local languages. CPaaS also fuels two-factor authentication and KYC verification, aligning with fintech compliance demands. This programmability narrative feeds straight into digital transformation budgets, making CPaaS a strategic pillar of the broader cloud telephony service market.

By Organization Size: SMEs Accelerate Through Simplicity

Large enterprises still represent 56.80% of 2025 revenue, leveraging multilayered feature sets, global compliance matrices, and legacy integration toolkits. Migration waves often coincide with office lease renewals or ERP upgrades, enabling clean technological breakpoints. Complex governance frameworks favor vendors offering secure admin portals, audit tracing, and role-based access control, locking in high-value, long-duration contracts.

Small and medium enterprises, however, post a 10.28% CAGR as user-friendly onboarding, freemium trials, and per-seat billing resonate strongly. Dialpad surpassing USD 300 million ARR underscores rising SME appetite for AI-powered calling, transcription, and coaching tools previously restricted to large contact centers. For budget-constrained firms, the elimination of maintenance fees and software patching unlocks funds for core business expansion. The SME segment therefore injects fresh volume into the cloud telephony service market, increasing competitive pressure for streamlined pricing and support models.

By End-User Vertical: Healthcare Moves from Reactive to Proactive Care

IT and telecom companies remain the single largest buyers, holding 24.05% of the 2025 cloud telephony service market size as they standardize internal operations and resell cloud minutes through wholesale channels. BFSI institutions adopt voice analytics for fraud detection and advisory meetings, while retail blends automated IVR with live agent escalations to manage holiday spikes. Government offices digitize citizen hotlines to reduce queue times, and universities deploy cloud PBX extensions to unite campuses and e-learning cohorts. Manufacturing turns to ruggedized SIP endpoints integrated with MES platforms, tying floor alerts directly into supervisor softphones.

Healthcare is forecast to grow at an 10.95% CAGR, spurred by telemedicine, remote patient monitoring, and secure clinician collaboration. HIPAA-grade encryption, audit-ready call logs, and EHR integration rank high on procurement checklists. Video consultations align with reimbursement codes, driving hospitals to integrate voice inside clinical portals rather than rely on separate consumer apps. The COVID-era surge in virtual visits cemented patient expectations for omnichannel access, pushing providers to refresh voice infrastructure quickly.

Geography Analysis

North America’s 36.95% share mirrors a mature adoption curve characterized by large-scale enterprise consolidation projects, extensive fiber penetration, and a vibrant partner ecosystem. United States federal agencies release multi-billion dollar modernization contracts that include cloud-based voice, while Fortune 500 corporations bake global numbering pools into hybrid-work policies. Canada leverages provincial broadband initiatives to extend coverage into remote resource extraction zones, giving mining and energy operators reliable VoIP options.

Europe charts steady expansion as GDPR compliance and digital sovereignty remain central purchase criteria. The cloud telephony services market benefits from pan-EU initiatives advocating energy-efficient data centers and cross-border interoperability. In the United Kingdom, financial-services firms migrate trading-desk turrets to the cloud, improving resilience and reducing square-footage costs. Germany’s Mittelstand manufacturers shift to hybrid deployments that couple plant-floor SIP phones with public-cloud collaboration hubs. France’s “cloud de confiance” framework encourages locally hosted voice nodes, leading to a rise in sovereign partnership models.

Asia Pacific posts the fastest trajectory at a 10.54% CAGR and is reshaping the long-term center of gravity for the cloud telephony service market. China’s aggressive cloud-computing blueprint drives provincial governments and state enterprises to standardize on domestic UC stacks. India’s Digital India and BharatNet projects extend fiber to rural districts, facilitating a leapfrog from analog lines to cloud softphones in small businesses. Japan’s enterprise base prioritizes disaster-resilient voice following seismic events, choosing geographically redundant clouds.

Competitive Landscape

The competitive map is moderately fragmented, with established software suites intersecting specialist voice providers and telecom incumbents. Microsoft exploits its Microsoft 365 footprint to bundle Teams Phone lines, enabling one-click provisioning inside familiar admin consoles and accelerating seat growth among existing productivity customers. RingCentral continues to broker carrier partnerships that embed its UCaaS stack into incumbent telco offerings, broadening reach and diluting direct-sales costs. Cisco leans on network-hardware relationships, offering Webex Calling as an add-on that utilizes existing QoS policies and SD-WAN deployments.

Amazon Web Services reinforces Amazon Connect with AI agent assist, sentiment analysis, and CRM connectors, monetizing compute cycles and storage along the way. NICE expands beyond contact-center voice into end-to-end experience orchestration, absorbing MindTouch to infuse knowledge-management content directly into agent desktops. Emerging vendors differentiate with developer-friendly GraphQL APIs, pay-per-conversation billing, and vertical compliance modules. Telecommunications carriers, wary of revenue erosion, cultivate private-label UCaaS offerings hosted in regional data centers to retain enterprise contracts. M&A activity remains brisk as players acquire AI analytics startups, regional SIP trunk brokers, and workflow automation tools. Looking ahead, platform breadth, pre-built integrations, and transparent pricing will likely overshadow raw call quality as decisive buyer criteria.

Cloud Telephony Services Industry Leaders

RingCentral

8x8 Inc.

Microsoft (Teams Phone)

Cisco (Webex Calling)

Vonage (incl. Ericsson)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NICE showcased CXone Mpower innovations, including Disney and H&R Block deployments that highlight AI-driven automation at scale.

- May 2025: NICE reported 12% year-over-year cloud revenue growth, reaching USD 700.2 million and authorizing a USD 500 million share-repurchase plan.

- February 2025: Dialpad crossed USD 300 million in annual recurring revenue, underscoring momentum in AI-centric SME cloud calling.

- January 2025: Five9 released bidirectional presence sync for Microsoft Teams, allowing agents to view expert availability in real time.

Global Cloud Telephony Services Market Report Scope

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| UCaaS |

| CCaaS |

| Cloud PBX |

| CPaaS |

| SIP Trunking |

| IVR / Auto-Attendant |

| Voice and Messaging APIs |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare |

| Retail and E-commerce |

| Government and Public Sector |

| Education |

| Manufacturing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Service Type | UCaaS | ||

| CCaaS | |||

| Cloud PBX | |||

| CPaaS | |||

| SIP Trunking | |||

| IVR / Auto-Attendant | |||

| Voice and Messaging APIs | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Vertical | IT and Telecom | ||

| BFSI | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Government and Public Sector | |||

| Education | |||

| Manufacturing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | Nigeria | ||

| South Africa | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the cloud telephony service market?

The cloud telephony service market size is valued at USD 29.17 billion in 2026.

How fast is the market expected to grow?

It is forecast to record a 9.32% CAGR, reaching USD 45.57 billion by 2031.

Which deployment model is growing the quickest?

Hybrid cloud deployments are expanding at a 10.12% CAGR as firms balance security with scalability.

Why is Asia Pacific attracting attention from vendors?

The region’s 10.54% CAGR is fueled by rapid digitization, expanding broadband, and the popularity of developer-friendly CPaaS APIs.

How are small and medium enterprises benefiting?

SMEs eliminate hardware costs, adopt pay-as-you-go pricing, and access AI-powered features that level the playing field with large enterprises.

What are the major barriers to adoption?

VoIP security compliance, inconsistent broadband quality in emerging markets, and concerns over hyperscale egress fees are the primary restraints.

Page last updated on: