IP DECT Phones Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

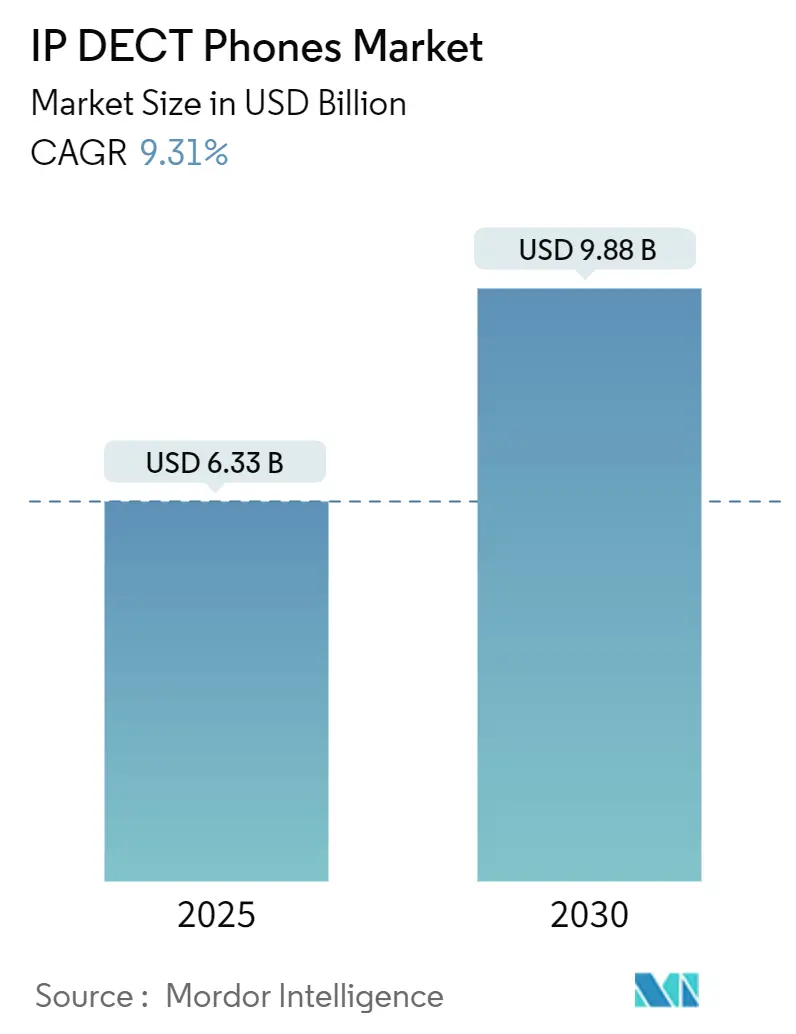

| Market Size (2025) | USD 6.33 Billion |

| Market Size (2030) | USD 9.88 Billion |

| Growth Rate (2025 - 2030) | 9.31% CAGR |

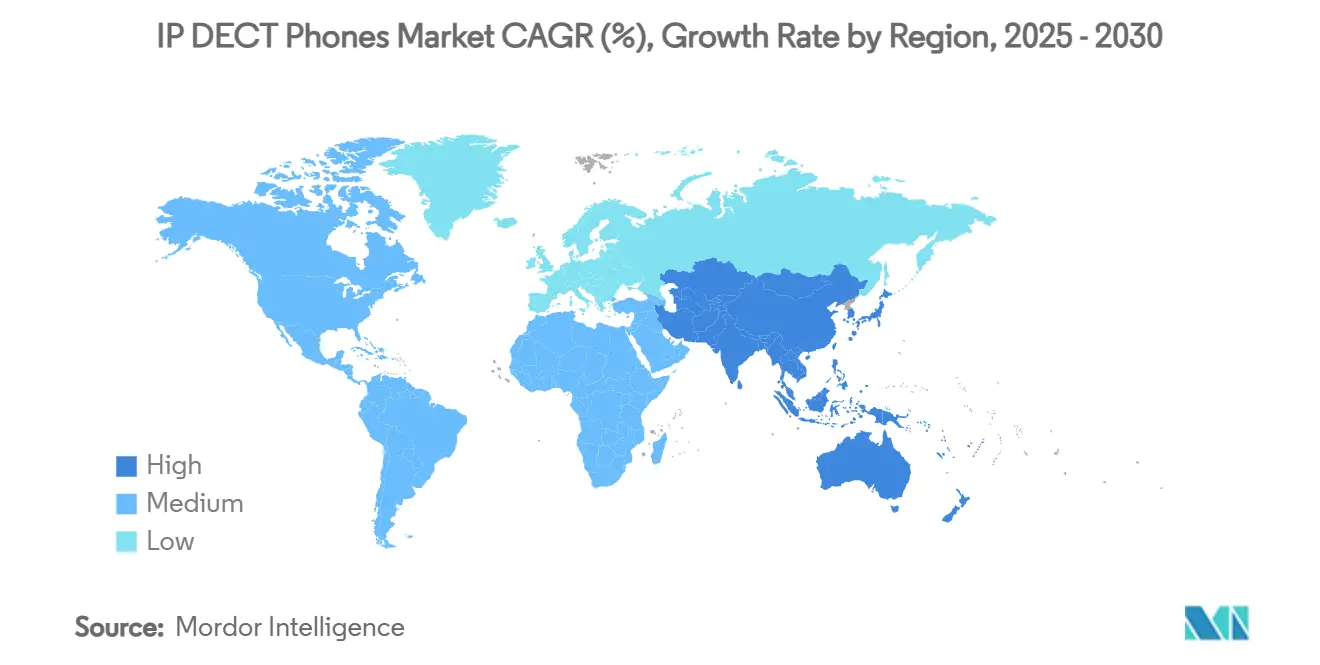

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

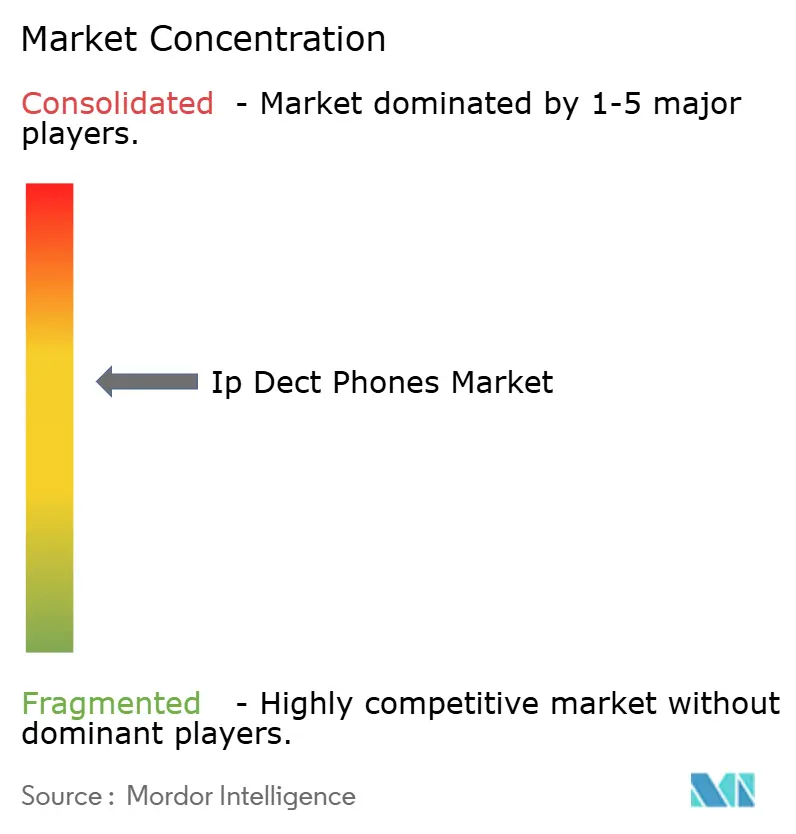

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IP DECT Phones Market Analysis by Mordor Intelligence

The IP DECT phones market size stands at USD 6.33 billion in 2025 and is projected to reach USD 9.88 billion by 2030, recording a 9.31% CAGR. Dedicated spectrum, low latency, and carrier-grade reliability keep DECT handsets indispensable for mission-critical voice even as enterprises migrate to cloud communications platforms. Accelerated replacement of legacy PBX hardware with cloud IP infrastructure, the arrival of DECT-2020 NR for integrated IoT, and factory demand for rugged mobility together underpin a healthy demand pipeline. Hybrid Wi-Fi 6 and private-5G capable handsets are broadening addressable use-cases, while antimicrobial devices safeguard clinical environments and sustain healthcare spending on specialized endpoints. Consolidation among vendors is reshaping competitive dynamics, yet a long-tail of regional specialists keeps pricing rational and innovation brisk.

Key Report Takeaways

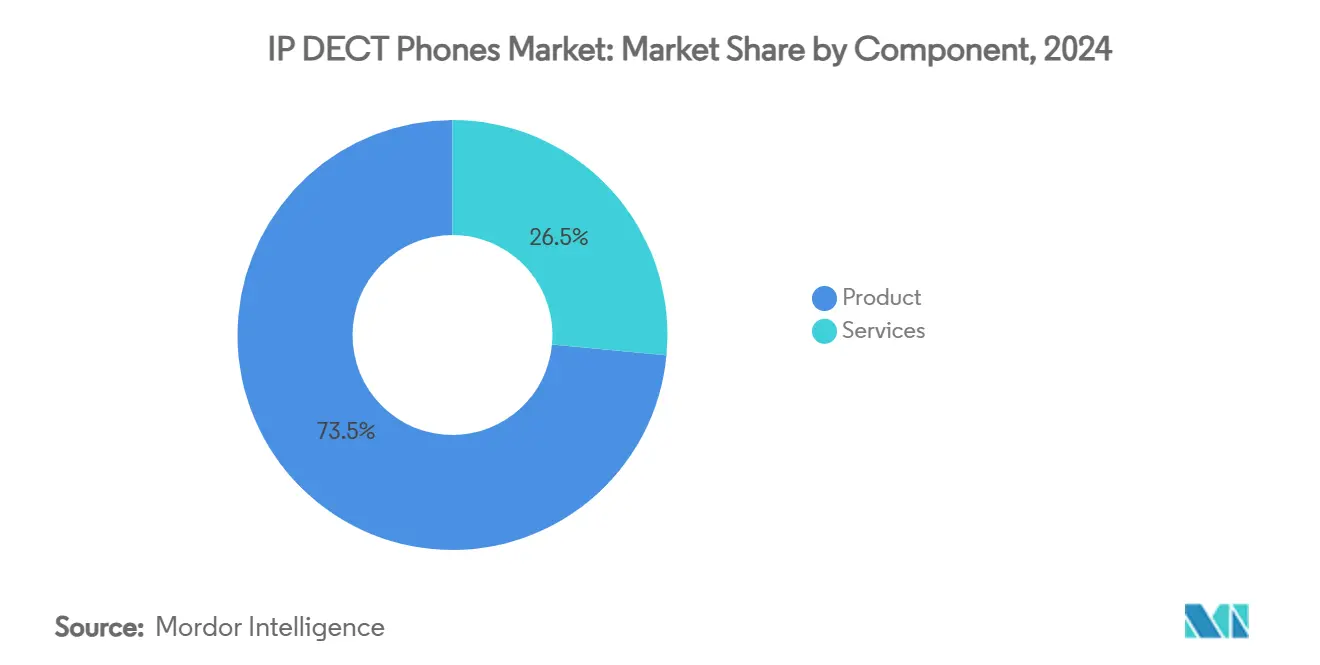

- By Component, Products retained 73.49% share of IP DECT phones market size in 2024, while services are advancing at a 9.37% CAGR through 2030.

- By Distribution Channel, B2B channels commanded 88.38% of IP DECT phones market size in 2024; B2C is on course for a 9.43% CAGR to 2030.

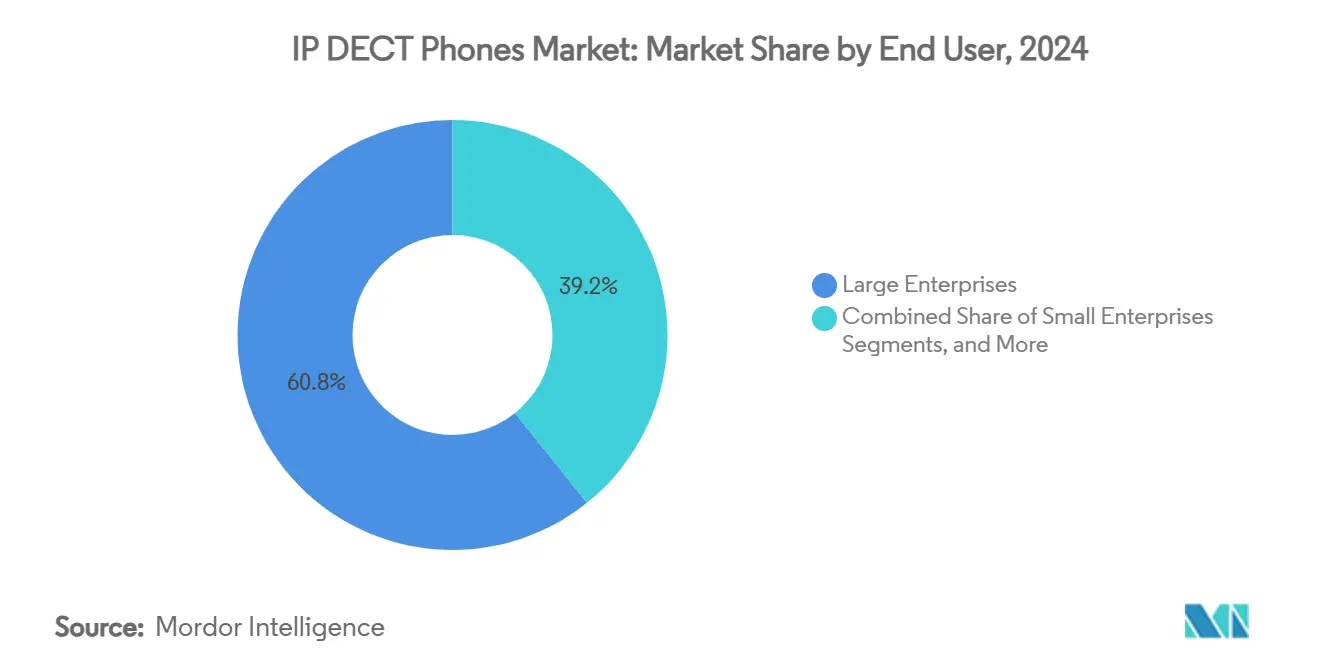

- By End User, Large enterprises captured 60.76% share of IP DECT phones market size in 2024; home users represent the fastest-growing end-user group at 9.59% CAGR to 2030.

- By Application, office communication contributed 42.29% revenue in 2024, whereas healthcare is accelerating at 9.98% CAGR through 2030.

- By geography, North America held 38.46% of IP DECT phones market share in 2024. Asia-Pacific is forecast to expand at 9.81% CAGR to 2030.

Global IP DECT Phones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid migration from legacy PBX to cloud IP | +2.1% | North America and Europe core | Medium term (2-4 years) |

| Smart-factory demand for rugged mobility | +1.8% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Roll-out of DECT-2020 NR converging voice/IoT | +1.4% | Europe first, expanding to Asia-Pacific and North America | Long term (≥ 4 years) |

| Hybrid Wi-Fi 6 / private-5G DECT handsets | +1.2% | Global early enterprise adopters | Medium term (2-4 years) |

| Infection-control healthcare handsets | +0.9% | Developed markets worldwide | Short term (≤ 2 years) |

| Ultra-low-energy DECT chipsets | +0.7% | Cost-sensitive regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Migration from Legacy PBX to Cloud IP Platforms

Organizations replacing hardware-bound PBXs with cloud services need endpoints that can register to Microsoft Teams, Zoom, and similar UCaaS suites without giving up the bullet-proof mobility long associated with DECT. Yealink’s SIP Gateway allows existing DECT bases to participate in Teams workflows, enabling call transfer, parking, and simultaneous ring on a single handset. [1]Yealink, “DECT SIP Gateway Deployment Guide,” yealink.comHospitals such as Mayotte Hospital Centre documented shorter call queues and higher staff satisfaction after shifting to cloud-integrated DECT, proving that managed mobility improves both patient care and IT overhead. Centralized administration of multi-cell systems through vendor portals reduces truck rolls and security patch delays, making cloud-ready DECT a default purchase specification in new enterprise tenders. As more PBX replacement projects go live, the IP DECT phones market registers repeat hardware upgrades as well as recurring license revenue for cloud connectors, sustaining double-digit expansion over the forecast window.

Smart-Factory Demand for Rugged On-Premise Mobility

Industry 4.0 programs place mobility at the heart of production efficiency because line supervisors, quality inspectors, and maintenance staff cannot rely on congested Wi-Fi or spotty cellular signals on a noisy shop floor. IP67-rated handsets such as Yealink’s W59R tolerate dust, moisture, and temperature swings while embedding man-down alarms and push-to-talk for safety compliance. Pharmaceutical player Siegfried Holding fitted 200 antennas across 50 buildings to combine voice, location tracking, and personal security on a single DECT backbone, illustrating the scale that factories can reach when downtime is unacceptable. The ability to layer DECT-2020 NR sensors onto the same network reduces cabling and maintenance, driving procurement managers to specify DECT in factory modernizations. Because industrial estates in China, India, and Southeast Asia are expanding floor space faster than any other region, Asia-Pacific becomes the epicenter of rugged handset demand through 2030.

Roll-out of DECT-2020 NR Converging Voice and IoT

DECT-2020 NR received ITU-R recognition as the first non-cellular 5G technology, securing global regulatory backing and ensuring spectrum protection for decades. [2]ETSI, “World's first non-cellular 5G technology, ETSI DECT-2020, gets ITU-R approval,” etsi.org With a capacity of more than 4 million devices per km² and native mesh self-healing, NR+ allows property owners to operate private networks without spectrum licensing costs typical of cellular. Nordic Semiconductor’s silicon and Wirepas 5G Mesh software already achieve 600 m link distances and multi-kilometer hop scenarios, broadening deployment economics for smart buildings and campuses. Enterprises can now roll asset-tracking tags, environmental sensors, and voice handsets onto a common infrastructure, slashing cabling budgets and accelerating payback. Vendors integrating NR+ into multi-cell base stations ship from 2025 onward, giving the IP DECT phones market a powerful, standards-backed growth engine through the end of the decade.

Hybrid Wi-Fi 6 / Private-5G DECT Handsets

Large campuses rarely rely on a single wireless technology. Zenitel’s SM-HS smartphone fuses DECT, Wi-Fi, and LTE/5G radios inside one Android device, allowing a nurse, warehouse picker, or security guard to roam across network domains without manual intervention. Alcatel-Lucent Enterprise’s alliance with Celona brings private-5G slicing into the same management console that oversees LAN and WLAN, voiding the historical trade-off between coverage, latency, and device battery life. This convergence increases addressable use-cases—think automated guided vehicles in a warehouse or staff collaboration in a convention center—where handsets negotiate the best bearer on the fly. Early adopters are paying premiums for such flexibility, and as component costs fall, hybrid capability will become a default feature that keeps the IP DECT phones market relevant against pure-play smartphone solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of UC softphone mobile apps | -1.9% | Global, especially offices | Short term (≤ 2 years) |

| SMB IT-budget contraction post-2024 | -1.1% | Worldwide small-medium businesses | Short term (≤ 2 years) |

| Possible spectrum re-allocation in Asia-Pacific/LatAm | -0.8% | Asia-Pacific and Latin America | Medium term (2-4 years) |

| Growing e-waste and sustainability scrutiny | -0.6% | Europe leading, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of UC Softphone Mobile Apps

Microsoft Teams, Zoom Phone, and countless UCaaS suites have turned every smartphone into a voice, video, and messaging endpoint, trimming the perceived need for a dedicated cordless handset. Corporations hunting for quick savings realize that softphones piggyback on consumer hardware already in employee pockets, shift updates over the air, and bundle analytics dashboards out-of-the-box. The impact lands hardest in desk-centric office settings where ruggedization or location-based alerting are not critical. Even so, DECT keeps an edge where hygiene, battery endurance, or regulated environments bar personal devices. Poly’s Rove series demonstrates how antimicrobial coatings and replaceable batteries preserve a foothold in hospitals despite the mobile-app wave. [3]tetronik GmbH, “Personal Security on an Area of 10 Hectares,” tetronik.com

SMB IT-Budget Contraction Post-2024

Inflation and higher borrowing costs have tightened cashflow for smaller firms, pushing finance teams to freeze capital outlays and favor OpEx models. A multi-cell DECT deployment involves upfront spend on bases, antennas, and handsets, making it an easy line-item to defer when a basic softphone subscription costs a few dollars per user each month. Vendors have responded with device-as-a-service contracts that spread payments and include refresh cycles, but adoption remains patchy. Where real-time staff coordination cannot rely on consumer networks—small clinics, garages, or micro-warehouses—DECT still wins, yet the volume dip from generalized belt-tightening shaves over a percentage point from the IP DECT phones market CAGR through 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand as Cloud Expertise Matters

Products continued to command 73.49% of the IP DECT phones market size in 2024, reflecting the ongoing refresh of handsets and base stations as enterprises chase DECT-2020 NR readiness and antimicrobial features. Yet the services slice is growing faster at 9.37% CAGR because organizations increasingly demand planning, spectrum surveying, and remote fleet management once deployments exceed a single building. Vendors bundle over-the-air firmware distribution, KPI dashboards, and API hooks into ITSM suites, creating annuity revenue that tempers hardware margin erosion.

The shift is visible in multi-national rollouts where centralized teams buy professional services to maintain QoS across thousands of endpoints. Poly’s cloud portal illustrates how warranty, battery health, and location data feed into predictive maintenance that cuts site visits and unplanned downtime. As cloud UC providers upsell managed mobility, integrators position DECT as a turnkey layer within broader campus networks, ensuring that services remain the growth lever within the IP DECT phones market.

By Distribution Channel: Enterprise-Centric B2B Keeps Lead

B2B channels held 88.38% of IP DECT phones market size in 2024 thanks to integrator expertise and the need for solution selling at scale. Complex site surveys, PoE switch upgrades, and VLAN segmentation mean that enterprises prefer specialist resellers or direct vendor engagement over retail outlets. Handset orders run into hundreds of units, often bundled with edge security appliances and unified communications licenses.

Nonetheless, B2C demand is climbing at 9.43% CAGR as remote workers discover that professional audio quality and interference-free calls elevate home productivity. Vendors like Gigaset package plug-and-play bases with intuitive handsets, bridging the familiarity gap between consumer cordless phones and enterprise DECT capability. E-commerce portals and electronics chains carry these kits, but average selling prices remain below enterprise levels, limiting near-term revenue impact relative to B2B volumes.

By End User: Home Users Drive the Fastest Uptake

Large enterprises accounted for 60.76% of IP DECT phones market size in 2024 because hospitals, factories, and campuses purchase thousands of units at a time and refresh on strict lifecycle calendars. Their need for fault-tolerant voice, man-down alarms, and regulatory compliance makes DECT non-negotiable. Small enterprises buy fewer units but appreciate the scalability of adding handsets without recabling offices, making them a steady mid-tier contributor.

Home users, however, represent the quickest mover at 9.59% CAGR. A hybrid workforce values dedicated voice devices that separate personal and work calls, deliver HD audio, and stand-alone during home broadband outages. Yealink’s W73P supports 10 handsets and 20 concurrent calls, letting a family run a home business and school-at-home scenarios simultaneously. As energy-efficient chipsets extend standby times into weeks, residential owners perceive tangible gains over smartphone reliance, propelling this segment upward.

By Application: Healthcare Outpaces Office Mainstay

Office communication still generates the lion’s share at 42.29% because every corporate campus and call center deploys cordless voice. Integration with Teams or Zoom softclients ensures continuity even as desk phones fade. Yet healthcare is accelerating at 9.98% CAGR owing to stringent hygiene protocols and life-safety workflows. Devices like Poly’s Rove imbued with Microban coatings reduce pathogen persistence, and dedicated spectrum avoids interference with monitoring equipment.

Retail premises equip associates with DECT clip-ons to boost aisle assistance, while residential adoption overlaps with home user demand discussed earlier. The “Others” bucket-public safety, logistics, utilities-grows steadily on the back of ruggedized handsets and DECT-2020 NR sensor fusion, adding resilience to field operations where public networks waver.

Geography Analysis

North America led the IP DECT phones market with 38.46% revenue in 2024 thanks to early cloud UC adoption, stringent clinical infection-control rules, and an active manufacturing corridor upgrading to hybrid private-5G/DECT mobility solutions. Regional healthcare systems expedited handset replacement cycles once antimicrobial and location-services became standard, while large retailers modernized in-store communication to support curbside fulfillment. Federal spectrum stability and an evolved channel ecosystem further cement vendor confidence in stocking advanced models.

Asia-Pacific, however, posts the fastest 9.81% CAGR through 2030. China and India continue to build smart factories where DECT’s deterministic latency underpins automated guided vehicles and worker safety beacons. Municipal smart-city projects in Southeast Asia adopt DECT-2020 NR to unify street-lighting, waste-management, and public Wi-Fi backhaul over a single unlicensed band. Healthcare investment in Japan and South Korea, combined with private-5G testbeds, multiplies demand for hybrid handsets that roam seamlessly between DECT and 5G slices. Because logistics hubs and ports across the region face RF hostile steel structures, DECT’s resilience offers a low-CAPEX alternative to licensed cellular repeaters.

Europe maintains a solid mid-single-digit growth trajectory anchored by DECT’s historical roots and clear CE certification regimes. Enterprises there pivot to NR+ early, encouraged by ETSI’s stewardship and government grants for energy-efficient IoT retrofits. Aging manufacturing plants in Germany and the Nordics add mesh sensors to legacy DECT bases, squeezing more value out of existing infrastructure and underpinning replacement handset demand. South America along with the Middle East and Africa trails but shows upside as telcos seek mid-band reallocations that could disrupt 1.9 GHz DECT channels; vendors therefore push interference adaptation features to protect service continuity, sustaining cautious but positive adoption curves.

Competitive Landscape

The IP DECT phones market remains moderately fragmented, with the top five vendors accounting for an estimated 55% revenue. Spectralink secures healthcare and industrial verticals through its Versity and 84-Series platforms tailored for nurse call integration and hazardous-area certifications. Yealink leverages Microsoft Teams certification to dominate cloud transition projects, bundling handsets with gateway licenses that lower softphone migration friction. Gigaset, freshly under VTech ownership, exploits strong brand equity in Europe to protect consumer and SOHO share while injecting VTech’s supply-chain efficiency into enterprise SKUs.

Alcatel-Lucent Enterprise spun off into a debt-free entity in December 2024 and is now investing in private-5G alliances, aiming to cross-sell DECT, Wi-Fi 6, and 5G radios under the same OmniVista policy umbrella. Semiconductor suppliers such as Nordic Semiconductor enter the fray by shipping NR+ reference designs, enabling ODM newcomers to launch competitively priced devices without deep RF heritage. Although UCaaS vendors threaten to displace dedicated endpoints, critical-environment requirements insulate a sizeable core market, allowing established brands to charge premiums for niche-tuned features and lifecycle services.

Strategic moves accelerated in 2024–2025. VTech bought Gigaset assets to expand European channels, while Ericsson’s USD 6.2 billion Vonage acquisition signaled renewed telecom-equipment interest in enterprise mobility APIs. Partnerships like Alcatel-Lucent Enterprise and Celona’s private-5G tie-up show hardware makers hedging against single-protocol exposure. This convergence race favors players with broad RF portfolios and software orchestration depth, nudging smaller specialists toward either vertical focus or integration alliances.

IP DECT Phones Industry Leaders

Ascom Holding AG

Spectralink Corporation

Gigaset Communications GmbH

Snom Technology GmbH

Yealink Network Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alcatel-Lucent Enterprise partnered with Celona to blend private 5G with LAN and WLAN, extending managed connectivity for warehouses and factories.

- February 2025: DECT Forum released NR+ specifications with Nordic Semiconductor silicon, delivering 600 m LOS range and 6.2 km in ideal mesh hops.

- January 2025: Ericsson finalized the USD 6.2 billion Vonage purchase, staking stronger enterprise 5G and CPaaS claims.

- January 2025: Alcatel-Lucent Enterprise named Westcoast its UK and Ireland distributor for UCaaS, CPaaS, and handset portfolio.

Global IP DECT Phones Market Report Scope

| Product |

| Services |

| B2B |

| B2C |

| Small Enterprises |

| Large Enterprises |

| Home Users |

| Healthcare |

| Retail |

| Office Communication |

| Residential |

| Other Applications |

| North America | United States |

| Rest of North America | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Middle East |

| Africa |

| By Component | Product | |

| Services | ||

| By Distribution Channel | B2B | |

| B2C | ||

| By End User | Small Enterprises | |

| Large Enterprises | ||

| Home Users | ||

| By Application | Healthcare | |

| Retail | ||

| Office Communication | ||

| Residential | ||

| Other Applications | ||

| By Geography | North America | United States |

| Rest of North America | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | |

| Africa | ||

Key Questions Answered in the Report

How large is the IP DECT phones market in 2025?

The IP DECT phones market size stands at USD 6.33 billion in 2025.

What CAGR is expected for IP DECT handsets to 2030?

Revenue is forecast to grow at a 9.31% CAGR through 2030.

Which region is expanding fastest for enterprise DECT deployments?

Asia-Pacific is projected to advance at a 9.81% CAGR as factories and smart-city projects scale mobility.

Why do hospitals prefer DECT over Wi-Fi for voice?

Dedicated spectrum avoids interference with medical devices, while antimicrobial handsets meet infection-control standards.

How is DECT-2020 NR changing deployment economics?

NR+ lets enterprises run voice and IoT sensors on the same unlicensed network, cutting cabling and license fees.

Who recently acquired Gigaset assets?

VTech purchased key Gigaset Communications assets in January 2024, expanding its European footprint.

Page last updated on: