VoIP Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

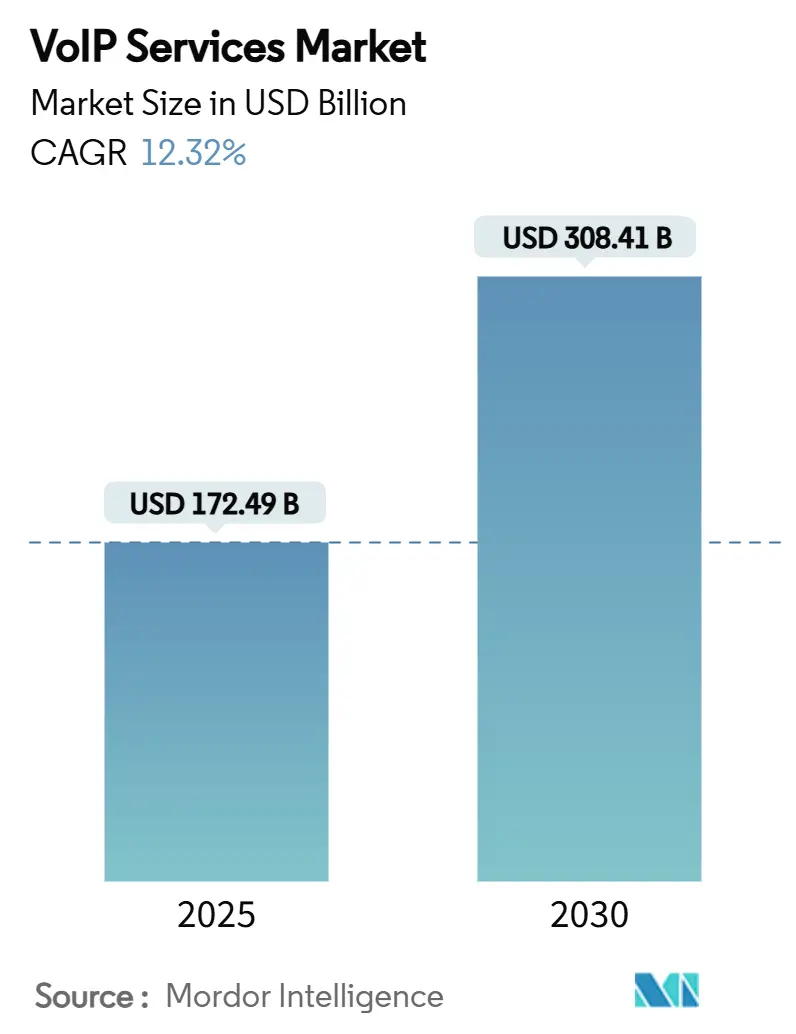

| Market Size (2025) | USD 172.49 Billion |

| Market Size (2030) | USD 308.41 Billion |

| Growth Rate (2025 - 2030) | 12.32% CAGR |

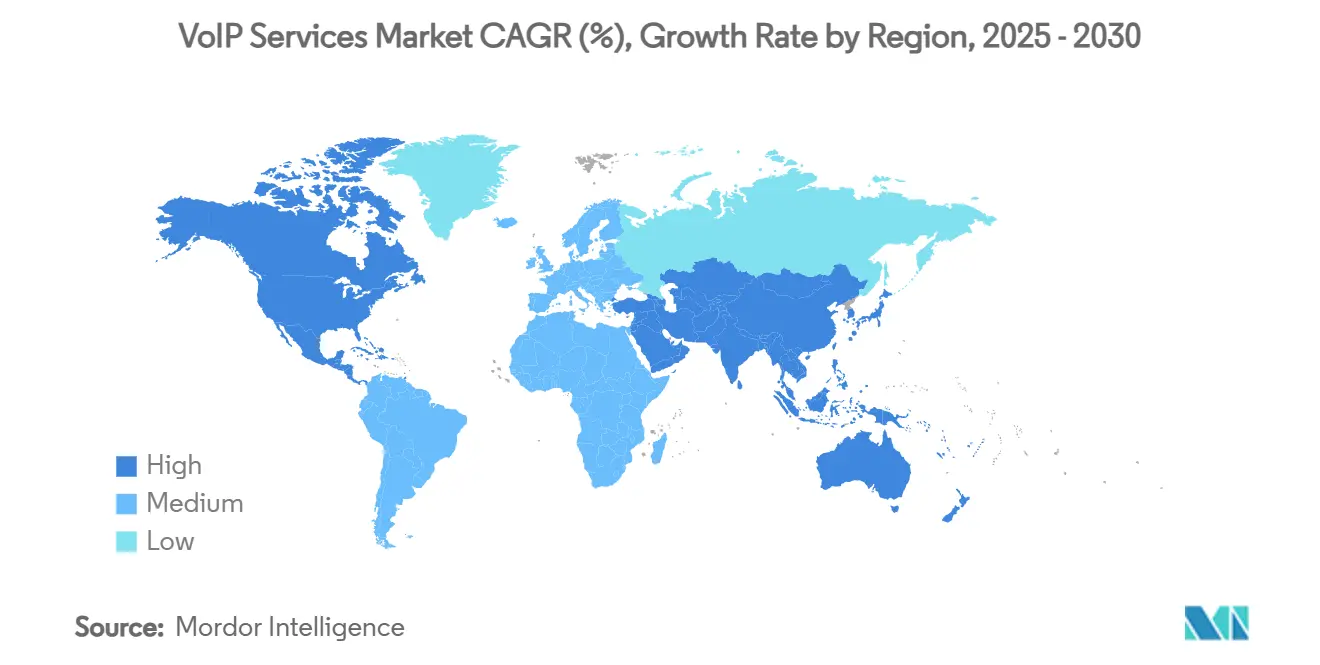

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

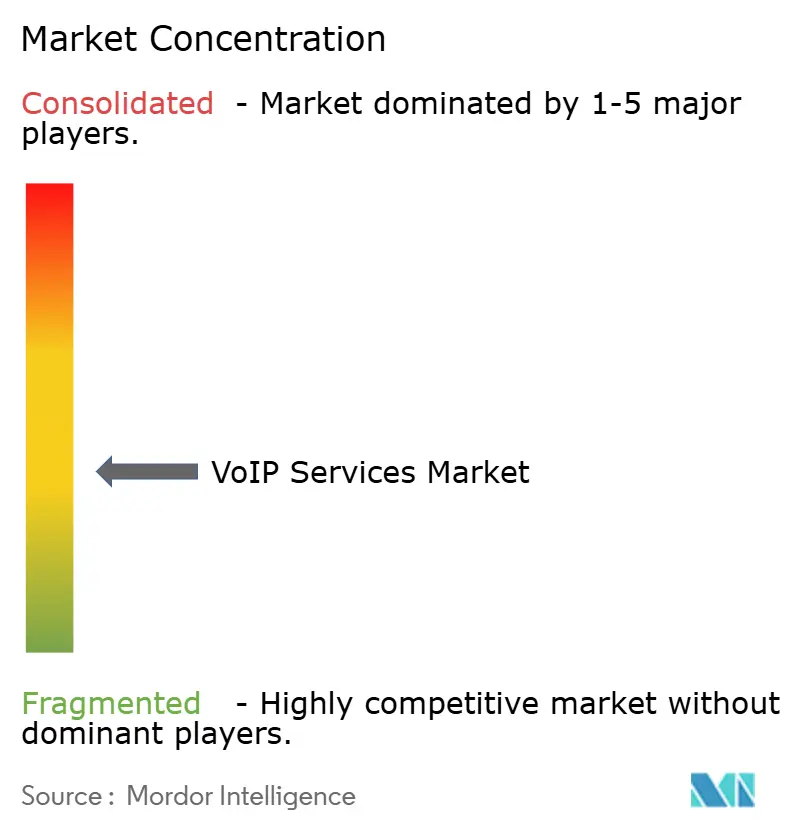

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

VoIP Services Market Analysis by Mordor Intelligence

The VoIP services market size stands at USD 172.49 billion in 2025 and is forecast to expand to USD 308.41 billion by 2030, reflecting a 12.32% CAGR through the period. Rapid migration from circuit-switched telephony to internet-based voice, the normalisation of hybrid work patterns, and enterprise cloud-first mandates accelerate adoption. Rising 5G coverage improves mobile VoIP quality, while artificial-intelligence analytics lift average revenue per user by automating call insights and customer interactions. Government-backed broadband programmes and falling equipment costs further widen addressable subscriber bases, especially in rural and emerging areas. Competitive dynamics show moderate fragmentation, yet high-value acquisitions by Tier-1 carriers signal a pivot toward vertically integrated, cloud-native voice ecosystems.

Key Report Takeaways

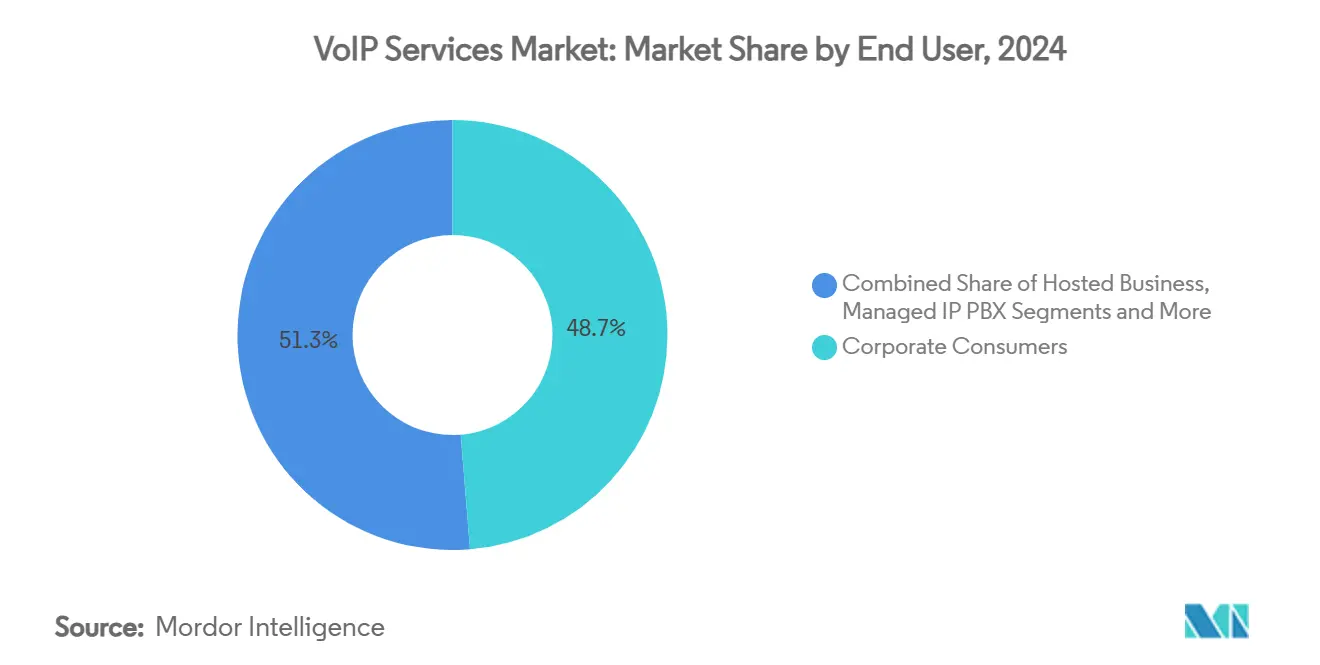

- By end user, corporate consumers held 48.7% of the VoIP services market share in 2024, while the hosted business sub-segment is advancing at a 12.5% CAGR through 2030.

- By call type, international long-distance traffic accounted for 60.1% of the VoIP services market size in 2024; mobile VoIP international services are climbing at a 13.1% CAGR to 2030.

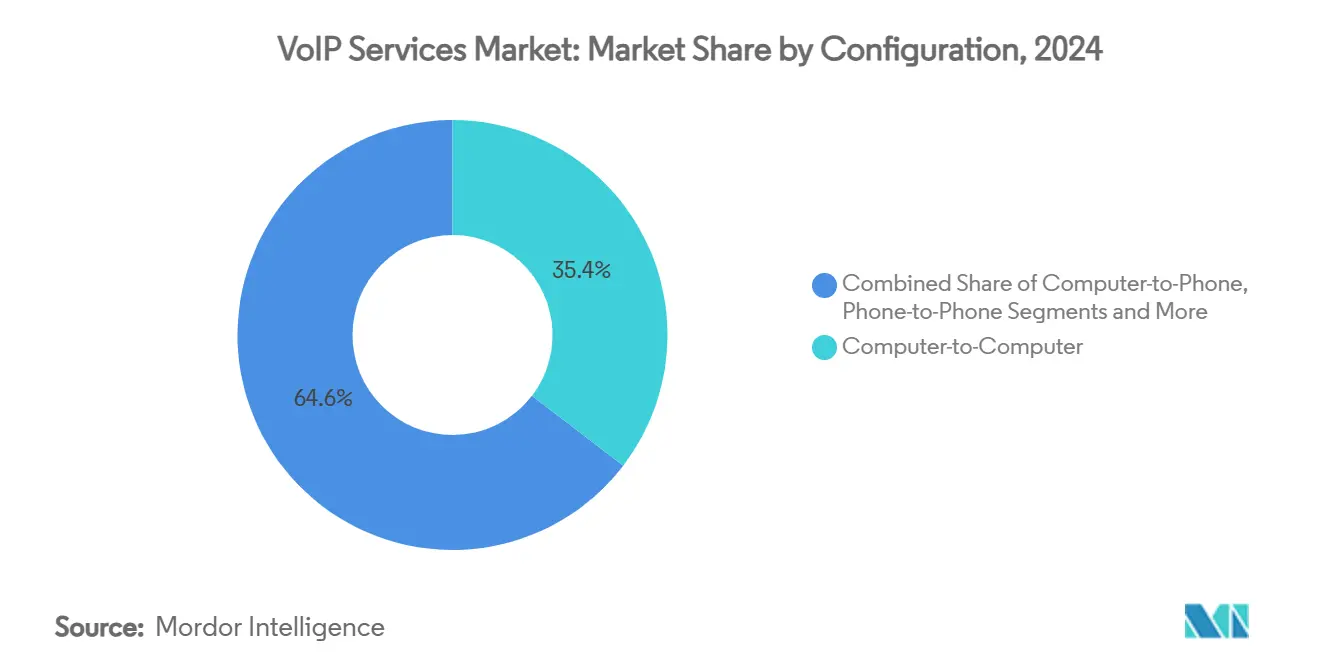

- By configuration, computer-to-computer retained 35.4% share of the VoIP services market size in 2024 and mobile softphone applications are expanding at 13.2% CAGR through 2030.

- By deployment model, hosted and cloud PBX captured 52.3% of the VoIP services market share in 2024 and is projected to grow at 12.8% CAGR to 2030.

- By geography, North America commanded 40.9% share in 2024, whereas Asia Pacific is forecast to post the fastest 12.6% CAGR between 2025-2030.

- AT&T, Verizon, Microsoft, Cisco, RingCentral and 8x8 collectively controlled 37% of global revenue in 2024.

Global VoIP Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote/hybrid work and UCaaS uptake | +2.1% | North America, Europe | Medium term (2-4 years) |

| Cost advantages versus PSTN | +1.8% | Global, emerging markets strong | Short term (≤ 2 years) |

| 5G rollout elevating mobile VoIP quality | +1.5% | Asia Pacific, North America | Long term (≥ 4 years) |

| SMB appetite for hosted PBX | +1.2% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| AI-driven voice analytics revenue | +0.9% | Global, led by US enterprises | Long term (≥ 4 years) |

| Rural broadband funding | +0.7% | US, UK, selected APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Remote Work and UCaaS Adoption

Unified communications as a service became the default enterprise communications architecture once hybrid work normalised. Eighty-four percent of organisations now view integrated UCaaS and contact-centre-as-a-service as their long-term model, citing fewer vendor touchpoints and improved customer retention after past communication failures. Microsoft’s Teams Phone tie-up with AT&T illustrates how cloud voice, video and messaging converge on single platforms that sustain corporate compliance and device roaming. [1]AT&T, "AT&T Announces AT&T Cloud Voice with Microsoft Teams Phone Mobile," about.att.comProviders monetise this convergence through tiered subscriptions that replace disparate licences, lifting average revenue per user and compressing churn.

Cost Advantages versus PSTN amid Rising Telecom OPEX

Legacy wireline divisions continue to post double-digit revenue declines, creating price tension as incumbents manage ageing copper assets. Subscription VoIP models answer by lowering upfront installation costs by up to 90% and slashing ongoing toll fees, a benefit that resonates most with SMEs seeking enterprise functionality without capital expenditure. Traditional carriers, in turn, sunset legacy services, leaving service gaps rapidly filled by agile VoIP specialists.

5G Rollout Boosting Mobile-VoIP Voice Quality

Voice over New Radio capitalises on standalone 5G cores to deliver end-to-end packetised voice with sub-20 ms latency. T-Mobile extended VoNR coverage to 100 million subscribers, while AT&T signed a multi-year voice-core modernisation deal with Nokia. Improved error rates remove the historical reliability ceiling that curtailed mobile enterprise adoption and enable new latency-sensitive applications such as real-time translation and AI coaching.

SMB Preference for Hosted PBX Solutions

Cloud-first procurement now dominates small-business spending, with 85% of firms prioritising hosted deployments by 2025. Providers like RingCentral and Ooma bundle scalable voice with CRM connectors, allowing companies without in-house IT skills to enjoy zero-touch upgrades and pay-as-you-grow seat pricing. This dynamic shortens sales cycles and speeds churn-influenced switching.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and VoIP fraud escalation | -1.4% | North America, Europe | Short term (≤ 2 years) |

| OTT calling regulatory uncertainty | -0.8% | Asia Pacific, MEA | Medium term (2-4 years) |

| QoS issues on congested public links | -0.6% | High-density urban zones | Short term (≤ 2 years) |

| Climate-driven power and fibre outages | -0.5% | Global coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cybersecurity and VoIP-Fraud Incidents

More than half of enterprises report an uptick in voice-channel attacks since 2021, with finance seeing a 90% surge. Deep-fake audio and spoofed CLI techniques undermine trust and trigger compliance penalties. Providers invest in STIR/SHAKEN call authentication and AI-based anomaly detection but must pass added costs to customers, raising acquisition hurdles for smaller accounts.

Regulatory Uncertainty Around OTT Calling in Emerging Markets

India’s Telecom Act 2023 proposal to license OTT voice apps illustrates policy flux that could mandate local servers, licence fees and emergency-service obligations. Similar restrictions in China and parts of the Gulf force providers to operate through state-controlled partners, diluting margins and complicating market entry. Continuous lobbying and compliance spend divert cash from product innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Corporate Stronghold with Hosted Momentum

Corporate buyers generated 48.7% of 2024 revenue, confirming that enterprise workflows still anchor the VoIP services market. Multi-site rollouts and global call routing keep switching barriers high. Yet the hosted business sub-segment is forecast to log a 12.5% CAGR to 2030, reflecting CFO preference for operational rather than capital budgets. The VoIP services market size attributable to corporate contracts is set to exceed USD 150 billion by 2030, while subscription bundles trim provisioning lead times from weeks to hours.

Managed IP PBX solutions act as midway steps for firms that desire hardware control but outsource software upkeep. Elastic SIP trunking also remains attractive; Twilio posted three consecutive years of double-digit trunking customer growth. The VoIP services market share for individual consumers is maturing in developed economies, yet growth lingers in mobile-first emerging markets where VoIP replaces costly GSM international tariffs.

By Call Type: International Long-Distance Dominance Amid Mobile Surge

International long-distance traffic represented 60.1% of 2024 call volume, driven by globalised supply chains and distributed talent pools. This slice of the VoIP services market size continues to benefit from carrier-OTT partnerships that bypass legacy settlement fees. Mobile VoIP international minutes, facing a 13.1% CAGR, illustrate rising smartphone dependency and improvements in roaming data pricing.

Domestic VoIP substitution also progresses as businesses retire TDM trunks. Juniper Research projects operators could capture USD 20 billion in incremental revenue by 2028 through internet voice bundles that integrate cloud PBX with unlimited national minutes. Integration of SMS, chat and presence data blurs call-type boundaries, reinforcing platform stickiness.

By Configuration: Desktop Leadership Meets Mobile Softphone Growth

Computer-to-computer sessions held 35.4% of 2024 traffic thanks to entrenched desktop collaboration suites. High-resolution webcams, headsets and content-sharing tools strengthen this format’s office relevance. However, mobile softphone adoption is the fastest-growing at 13.2% CAGR as employees demand parity between desk and handset experiences. AI features such as real-time transcription in 8x8 softphones widen functional gaps with legacy desktop phones.[2]Morris, Tricia, “2024 State of Business Communications,” 8x8.com

Traditional phone-to-phone VoIP remains viable for conservative verticals but loses ground in greenfield deployments. SIP trunk configurations bridge legacy PBXs during phased cloud migrations, preserving sunk costs while granting IP advantages.

By Deployment Model: Hosted Cloud PBX Commands Trajectory

Hosted and cloud PBX services already account for 52.3% of global revenue and will sustain a 12.8% CAGR, cementing cloud as the de-facto enterprise voice core. Microsoft, Cisco and RingCentral promote API-rich ecosystems where voice becomes one micro-service among many.

The VoIP services market share for on-premise systems declines as security certifications ease cloud concerns. Hybrid deployments offer gradual transition paths; Pure IP documents thousands of lines moved to Teams Phone with direct routing while keeping local survivability gateways.

Geography Analysis

North America retained 40.9% revenue share in 2024, supported by early UCaaS uptake, abundant fibre backhaul and clear regulatory frameworks. The USD 42.45 billion Broadband Equity, Access and Deployment programme funds last-mile infrastructure that brings modern voice options to underserved US counties. [3]National Telecommunications and Information Administration, “BEAD Program Overview,” ntia.gov Canada benefits from cross-border enterprise traffic, while Mexico’s near-shoring boom lifts demand for bilingual VoIP support centres. Extreme weather remains a risk, with more than 4,000 miles of coastal fibre conduit flagged as vulnerable to sea-level rise over the next 15 years. [4]Department of Homeland Security, “Implications of Extreme Weather Events on U.S. Telecommunications Infrastructure,” dhs.gov

Asia Pacific is the fastest-growing region at 12.6% CAGR, fuelled by mobile economy contributions worth USD 880 billion in 2023 and ongoing 5G rollouts. China and India drive volume through mass-market handset upgrades, while Japan, South Korea and Australia capitalise on AI-based voice analytics for customer-experience gains. Regulatory ambiguity in markets such as India, however, tempers absolute upside.

Europe shows stable progression underpinned by cross-border commerce and 5G coverage targets like Germany’s 90% goal by 2025. The United Kingdom’s EUR 5 billion (USD 5.88 billion) Project Gigabit aims to extend gigabit broadband to 312,000 premises, indirectly lifting rural VoIP availability. Ongoing mobile-carrier consolidation talks may influence pricing and service diversity. The Middle East, Africa and South America trail in penetration but exhibit focused hotspots where fibre and data-centre builds intersect with startup ecosystems.

Competitive Landscape

Moderate fragmentation defines the VoIP services industry, yet marquee acquisitions are redrawing boundaries. Ericsson sealed its USD 6.2 billion Vonage takeover in January 2025, integrating API-driven voice services with 5G network slices. Verizon announced a USD 20 billion move on Frontier Communications that brings 9.6 million fibre premises under its wing. These integrations aim to pair last-mile ownership with cloud UC platforms, creating end-to-end service guarantees competitors without physical networks cannot match.

Platform breadth and AI capabilities now outweigh per-minute tariffs in buying decisions. RingCentral leads the UCaaS revenue league with around 20% share, aided by AI summarisation and agent-assist modules. Microsoft leverages its 42.8% collaboration foothold via Teams Phone add-ons, while Cisco invests in real-time media models that auto-correct jitter. Twilio scales programmable voice APIs for developers, extending market reach beyond traditional enterprise buyers.

Niche opportunities persist in compliance-heavy verticals such as healthcare, where HIPAA mandates create barriers that favour specialised providers. White-label and wholesale channels also grow as regional ISPs bundle cloud PBX to offset declining broadband ARPU.

VoIP Services Industry Leaders

-

Microsoft (Skype / Teams Voice)

-

Cisco Systems (Webex / BroadWorks / CUCM)

-

AT&T

-

Vonage Holdings

-

RingCentral

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: AT&T extended its Nokia voice-core pact to deploy cloud-native IMS and Voice over New Radio across its 5G footprint.

- January 2025: Ericsson finalised the USD 6.2 billion Vonage acquisition, returning the vendor to enterprise communications.

- January 2025: RingCentral introduced a next-generation POTS replacement that modernises copper lines with cloud lines.

- December 2024: Zadarma bought US-based VoIPVoIP to expand North American reach and add speech analytics.

Global VoIP Services Market Report Scope

| Corporate Consumers |

| Hosted Business |

| Managed IP PBX |

| IP Connectivity (SIP Trunking) |

| Individual Consumers |

| International Long-Distance VoIP Calls |

| Domestic VoIP Calls |

| Computer-to-Phone |

| Computer-to-Computer |

| Phone-to-Phone |

| Mobile Softphone |

| SIP Trunk Access |

| Hosted / Cloud PBX |

| On-Premise (Self-Hosted) |

| Hybrid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By End User | Corporate Consumers | ||

| Hosted Business | |||

| Managed IP PBX | |||

| IP Connectivity (SIP Trunking) | |||

| Individual Consumers | |||

| By Call Type | International Long-Distance VoIP Calls | ||

| Domestic VoIP Calls | |||

| By Configuration | Computer-to-Phone | ||

| Computer-to-Computer | |||

| Phone-to-Phone | |||

| Mobile Softphone | |||

| SIP Trunk Access | |||

| By Deployment Model | Hosted / Cloud PBX | ||

| On-Premise (Self-Hosted) | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the VoIP services market in 2025?

The VoIP services market size is USD 172.49 billion in 2025, with a projected 12.32% CAGR to 2030.

Which region is growing the fastest?

Asia Pacific is expected to post the highest regional CAGR of 12.6% between 2025-2030, propelled by 5G rollouts and smartphone adoption.

What deployment model leads global revenue?

Hosted and cloud PBX accounts for 52.3% of 2024 revenue and is forecast to expand at 12.8% CAGR through 2030.

Why are enterprises shifting from PSTN to VoIP?

Companies save up to 50% on call costs, avoid legacy hardware upkeep and gain AI features such as real-time transcription.

What is the main security concern for VoIP?

Rising deep-fake and caller-ID spoofing attacks increase fraud risk, prompting wider use of STIR/SHAKEN and AI fraud analytics.

Which companies dominate the competitive landscape?

AT&T, Verizon, Microsoft, Cisco, RingCentral and 8x8 collectively hold roughly 37% of global revenue, with ongoing consolidation shaping market dynamics.

Page last updated on: