Telecom Cloud Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

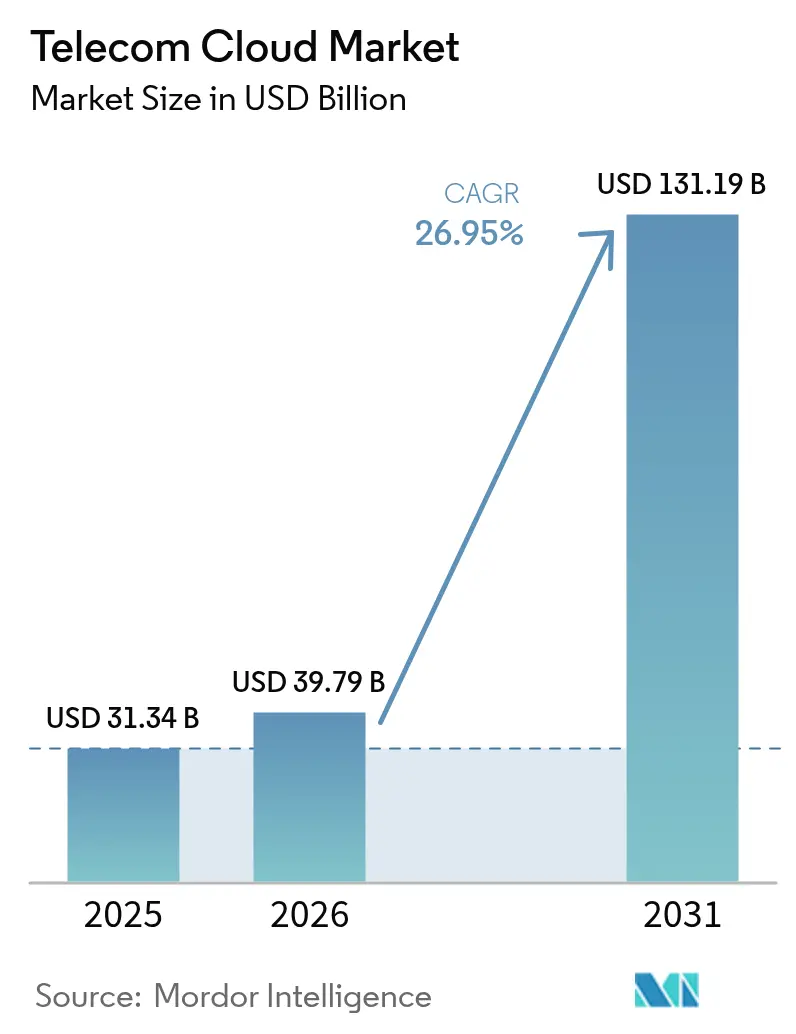

| Market Size (2026) | USD 39.79 Billion |

| Market Size (2031) | USD 131.19 Billion |

| Growth Rate (2026 - 2031) | 26.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Cloud Market Analysis by Mordor Intelligence

The telecom cloud market size is expected to grow from USD 31.34 billion in 2025 to USD 39.79 billion in 2026 and is forecast to reach USD 131.19 billion by 2031 at 26.95% CAGR over 2026-2031. Operators are steering capital toward cloud-native core networks that unlock 5G monetization, accelerate edge computing, and compress operating costs. Converging trends-Open RAN deployment, network-functions virtualization, and hybrid-cloud adoption-are altering how connectivity is engineered and sold. Spending commitments such as AT&T’s USD 14 billion Open RAN deal with Ericsson underscore the scale of transition. Vodafone’s USD 1.5 billion pact with Microsoft highlights how multi-cloud frameworks address performance, sovereignty, and compliance expectations. Verizon’s multi-access edge computing trials cutting latency in half exemplify how edge-cloud federation positions carriers for Industry 4.0 revenue pools.

Key Report Takeaways

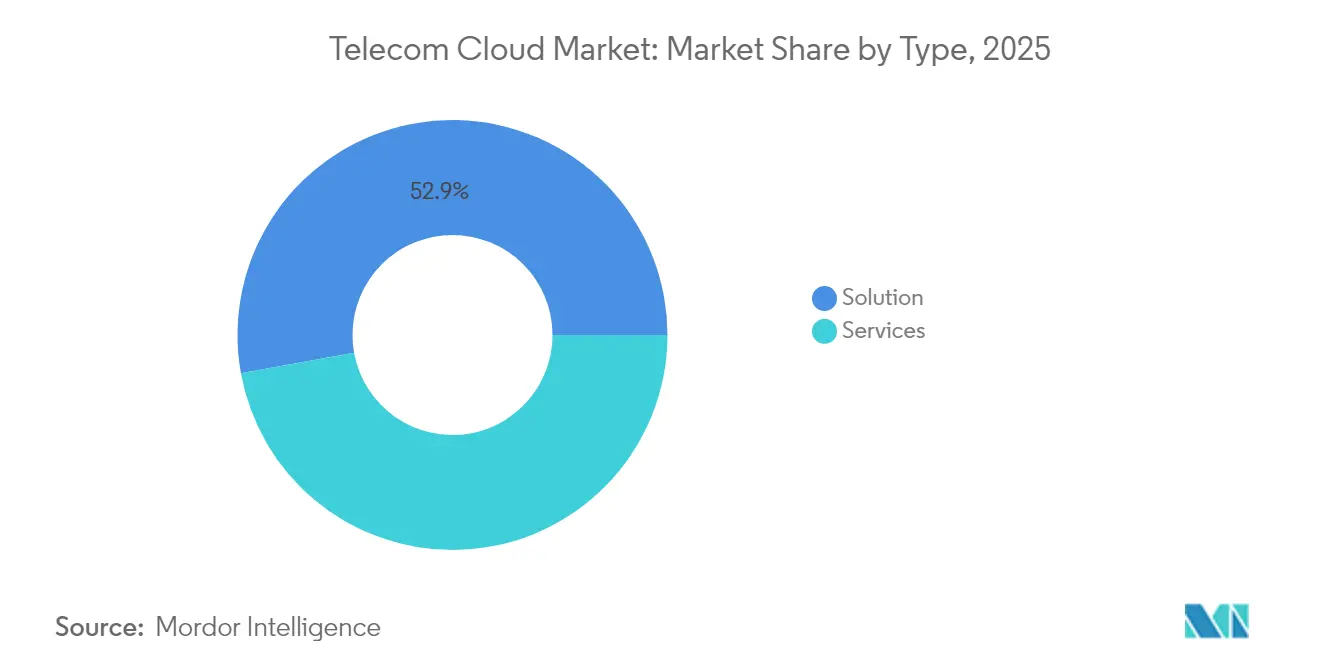

- By solution type, Solution offerings led with 52.85% revenue share of the telecom cloud market in 2025; Services are projected to expand at a 27.25% CAGR through 2031.

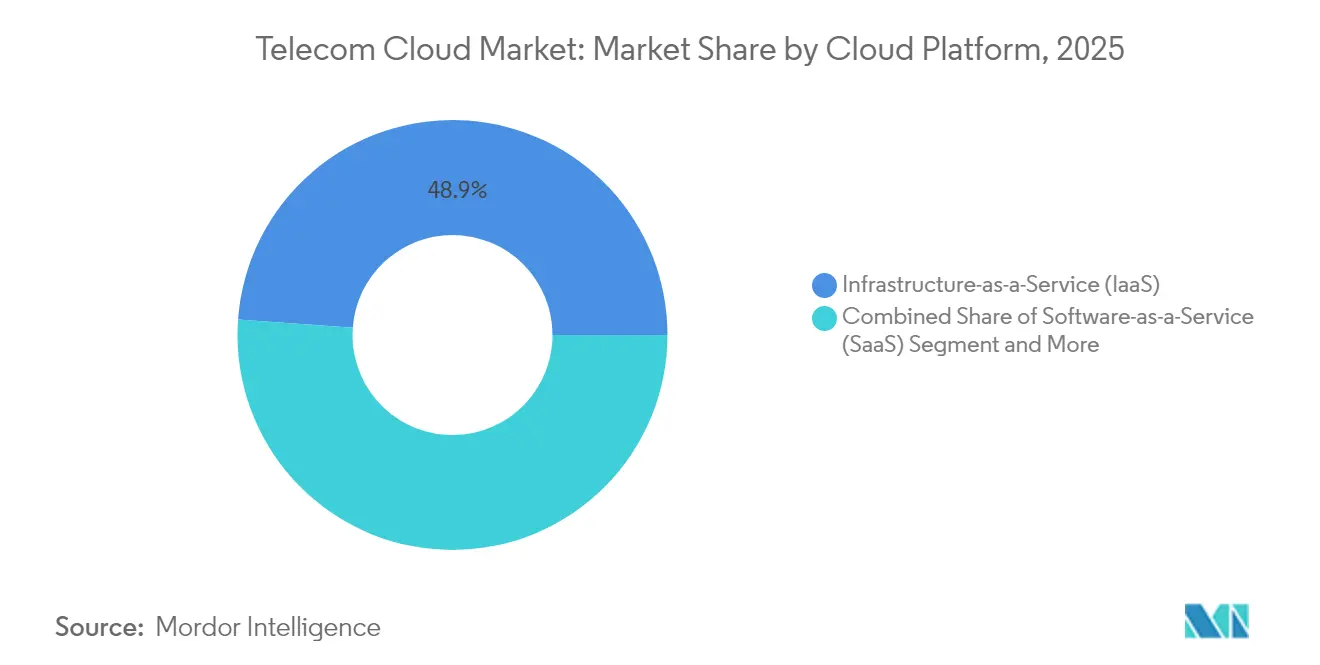

- By platform, Infrastructure-as-a-Service captured 48.85% telecom cloud market share in 2025, whereas Platform-as-a-Service is forecast to climb at a 28.65% CAGR to 2031.

- By application, Billing and Provisioning held 45.10% share of the telecom cloud market size in 2025, while Traffic Management is poised for a 27.6% CAGR to 2031.

- By end user, BFSI commanded 32.15% of telecom cloud market share in 2025; Healthcare exhibits the fastest expansion at a 28.1% CAGR through 2031.

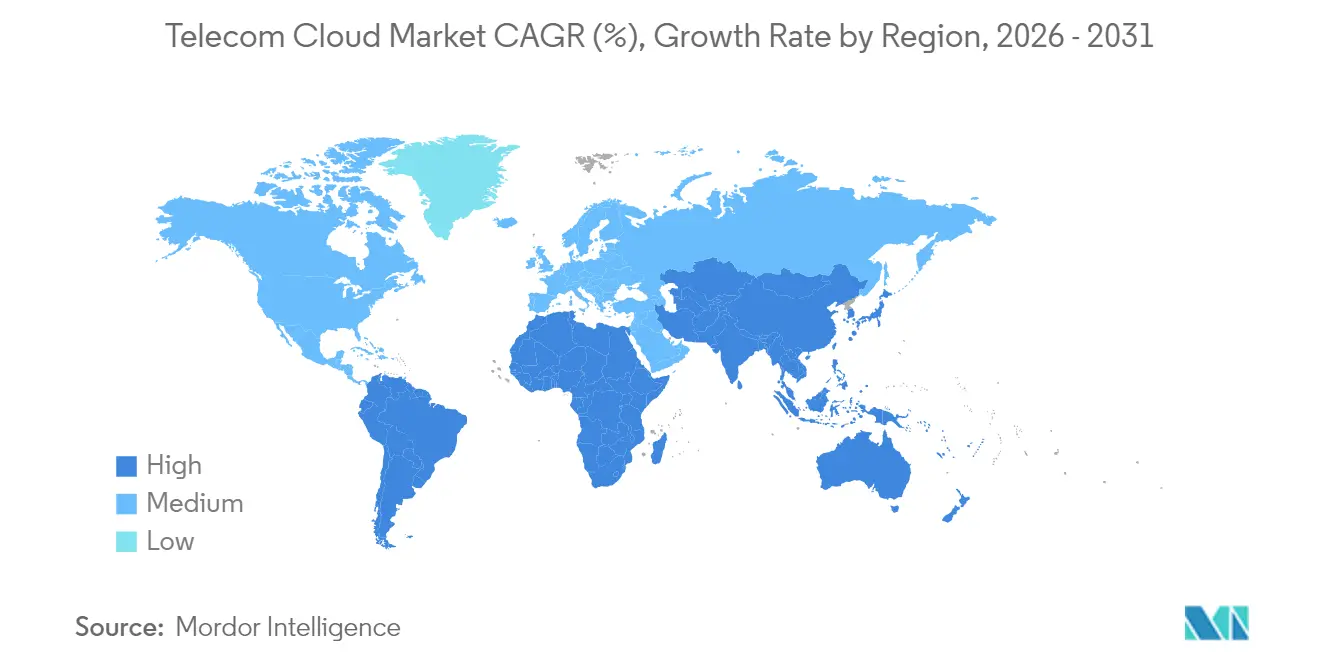

- By region, North America accounted for 34.90% of revenue in 2025, yet Asia-Pacific is on track for a 26.85% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Telecom Cloud Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G roll-outs demanding cloud-native core networks | +6.5% | Global, with early gains in North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Growing adoption of hybrid and multi-cloud by telecom operators | +2.7% | Global, particularly strong in North America and EU | Short term (≤ 2 years) |

| Cost efficiency via NFV-enabled OPEX savings | +2.8% | Global, with higher impact in mature markets | Medium term (2-4 years) |

| Convergence of Open RAN accelerating RAN-cloudification | +1.9% | North America and EU leading, Asia-Pacific following | Long term (≥ 4 years) |

| Edge-cloud federation enabling ultra-low-latency enterprise 4.0 | +1.5% | Global, concentrated in industrial regions | Medium term (2-4 years) |

| Sustainability pledges shifting telcos to green public clouds | +1.2% | EU and North America leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in 5G roll-outs demanding cloud-native core networks

Standalone 5G mandates cloud-native cores, dismantling monolithic architectures in favor of micro-services that enable automated network slicing and real-time provisioning. Deutsche Telekom’s work with Google Cloud on AI-driven RAN orchestration proves that automation is now indispensable to manage the scale and complexity of 5G traffic. Telefónica Germany migrated 45 million subscribers to Ericsson’s cloud-native 5G core, cutting service-activation times and fortifying network agility.[1]Deutsche Telekom AG, “Telefónica Germany Migrates 45 Million Subscribers to Cloud-Native Core,” ericsson.comThese transformations signal that 5G revenue relies on cloud-native capabilities deployed at carrier grade.

Growing adoption of hybrid and multi-cloud by telecom operators

Rakuten Symphony’s multi-cloud blueprint showcases workload portability across providers while guarding sovereignty obligations. Hybrid architectures allow latency-sensitive network functions to remain on-premise while scalable workloads burst to public clouds. Cisco finds 82% of enterprises now run hybrid models, validating the strategy for resilience and cost optimization. This dual-environment adoption is accelerating as operators link compliance with innovation velocity.

Edge-cloud federation enabling ultra-low-latency enterprise 4.0

Verizon’s multi-access edge computing trials halved latency, a prerequisite for real-time automation in factories and logistics hubs. [2]Verizon Communications, “MEC Trials Cut Latency by 50%,” verizon.com Federated edge-cloud models stitch central clouds with metro-edge zones, opening fresh revenue from Industry 4.0, AR/VR, and autonomous mobility use cases.

Convergence of Open RAN accelerating RAN-cloudification

AT&T plans 70% of wireless traffic on Open-capable platforms by 2026 through a USD 14 billion Ericsson alliance, illustrating how disaggregated hardware-software deployments are entering production scale. Google Cloud’s O-RAN Alliance membership shows hyperscalers racing to inject their software prowess into radio networks.[3]Google Cloud, “Ericsson On-Demand Launch Announcement,” cloud.google.com Cloud RAN centralizes processing, bolstering spectrum efficiency and reducing energy draw, outcomes aligned with operator cost and sustainability goals.

Restraints Impact Analysis of Telecom Cloud Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and security compliance hurdles | -3.2% | Global, particularly acute in EU, China, and emerging markets | Long term (≥ 4 years) |

| Integration complexity with legacy BSS/OSS stacks | -2.1% | Global, higher impact in mature markets with extensive legacy infrastructure | Medium term (2-4 years) |

| Shortage of cloud-native skills in telco ops teams | -1.8% | Global, most severe in North America and EU | Short term (≤ 2 years) |

| High cross-border cloud exit-cost risk exposures | -1.4% | Global, particularly affecting multi-national operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty and security compliance hurdles

Google Cloud’s telecom-specific compliance frameworks attest to the maze of regional privacy rules carriers must meet. Localization mandates inflate compute costs by up to 60%, eroding the telecom cloud market’s cost-saving allure. VMware sovereign-cloud blueprints show architecture complexity rises when carriers enforce in-country residency and encryption at rest. Evolving statutes constrain deployment flexibility and lengthen project timelines.

Integration complexity with legacy BSS/OSS stacks

Netcracker outlines multi-stage remediation paths for cloud migrations, spotlighting extensive custom integrations that resist lift-and-shift approaches netcracker.com. Ericsson stresses that outdated BSS silos impede digital-service rollout speeds.[3] Technical debt and change-management hurdles combine to slow momentum, particularly in mature markets with decades of customization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Telecom Cloud Market Segment Analysis

By Type:

Services Gain Momentum as Managed Models ScaleIn 2025 solution segment held 52.85% share, reflecting operators’ first-wave focus on foundational cloud stacks. Yet Services are accelerating at a 27.25% CAGR, forecast to close the gap as carriers outsource operations to specialist partners. Unified communication, CDN, and security workloads continue to lift Solution revenues, but managed hosting, professional services, and network-as-a-service contracts are growing faster.

Operators increasingly adopt managed models to de-risk transformation and redeploy staff toward customer innovation. Colocation footprints give carriers proximity to edge zones, while professional-service engagements address skills shortages. This trend signals a structural shift toward opex-based consumption, aligning telco spending with traffic elasticity and subscriber seasonality across the telecom cloud market.

By Application:

Traffic Management Outpaces Traditional OSS PillarsBilling and Provisioning retained 45.10% of telecom cloud market size in 2025, underpinning revenue assurance activities critical to every carrier. Traffic Management, however, is projected to grow 27.6% annually as 5G data surges strain networks. Cisco’s Ultra Traffic Optimization and Opanga’s RAIN AI showcase AI-driven congestion relief that boosts QoE without fresh spectrum buys.

AI-infused engines that predict congestion and reroute packets in real time are becoming must-have capabilities. HCL’s Augmented Network Automation illustrates 20% capacity lifts alongside OPEX cuts, explaining the outsized growth. Ancillary workloads such as security analytics and customer-experience portals also migrate to cloud in lockstep, reinforcing application-layer diversification within the telecom cloud market.

By Cloud Platform:

PaaS Captures Developer MindshareInfrastructure-as-a-Service retained 48.85% telecom cloud market share in 2025 because virtual machines and bare-metal servers remain baseline for VNFs and legacy workloads. Platform-as-a-Service is rising 28.65% a year as micro-services, containers, and CI/CD pipelines move center stage. Ericsson and Google Cloud’s 5G Core-as-a-Service lets operators instantiate slices in minutes, proving PaaS can meet telecom grade SLAs.

Container orchestration and serverless models lower development overhead and shorten release cycles, magnetizing network application teams toward PaaS. SaaS remains niche for now because carriers prefer control over network layers, though targeted SaaS offerings in analytics and compliance are emerging. The shift underscores how the telecom cloud market is aligning with mainstream cloud-native tooling.

By End User:

Healthcare Surges Behind BFSI LeadershipBFSI dominated with 32.15% share of telecom cloud market size in 2025 as digital banking, trading, and fraud analytics depend on low-latency secure infrastructure. Healthcare, though smaller, is advancing 28.1% CAGR as telehealth, imaging, and remote monitoring scale. AT&T’s medical-imaging service exemplifies how centralized cloud repositories improve diagnostic workflows.

Manufacturing is adopting private LTE and edge clouds for smart factories, evidenced by Dow Chemical’s Industry 4.0 rollouts. Retail leans on omnichannel and real-time inventory, while government and smart-city projects focus on public safety and mobility. Media and Entertainment continues to push CDN capacity and live streaming, diversifying demand across the telecom cloud market.

Geography Analysis

North America Telecom Cloud Market

North America accounted for 34.90% revenue in 2025 as early 5G roll-outs, established hyperscaler partnerships, and favorable regulations aligned. Carriers monetized edge services and enterprise connectivity, strengthening regional leadership in the telecom cloud market. Federal funding streams for rural 5G also bolster investment momentum.

APAC Telecom Cloud Market

Asia-Pacific is projected to expand at 26.85% CAGR through 2031, supported by government digitalization programs and massive data-center investments. AWS’s USD 15 billion commitment and Microsoft’s USD 2.9 billion plan in Japan illustrate capital intensity, while Huawei’s 77% cloud-service revenue jump in 2023 signals domestic demand acceleration. China’s USD 9.2 billion 2023 cloud-infrastructure spend positions its carriers and local providers for growth.

EMEA and LATAM Telecom Cloud Market

Europe remains a sizeable market, where stringent sovereignty mandates foster sovereign-cloud builds and spark Open RAN experiments. Energy-efficiency goals align with cloud consolidation, giving European carriers strategic imperatives to modernize networks. Middle East and Africa and Latin America show rising adoption curves fueled by smart-city initiatives, fintech penetration, and mobile-first demographics, though regulatory gaps and skills shortages temper near-term scale.

Regulatory Landscape

Telecom cloud deployments are increasingly shaped by overlapping telecom-security, cloud-sovereignty, and certification initiatives that influence where network functions can run and which controls operators must evidence. In Europe, the Gigabit Infrastructure Act entered into force on May 11, 2024 and reached general application by Nov 12, 2025, supporting accelerated gigabit rollouts that pull more core and edge workloads into cloud platforms. BEREC also published an Oct 2024 report on cloud and edge computing services, pointing to regulatory focus on dependency, resilience, and governance for telecom-critical cloud services.

In 2026, policy and standards activity tightened around sovereignty and security assurance for carrier-grade cloud. The European Commission published a proposal for the Digital Networks Act in January 2026 to harmonize EU telecom rules, and the EU also progressed cloud sovereignty mechanisms through its Cloud Sovereignty Framework, including an April 2026 sovereign cloud services contract for EU institutions. Security and assurance requirements continued to formalize through ETSI (GS NFV-SOL 023 V5.4.1 released April 2026 for NFV certificate management), ITU-T (Y.3165 in Aug 2025 and Y.3169 in Dec 2025 for confidential computing and containerized UPF orchestration), and national measures such as the UK DSIT Draft Revised Telecommunications Security Code of Practice 2026 (June 2026) and Nigeria's National Cloud Policy 2025 (Oct 2025) administered by NITDA, including data classification and residency expectations.

Competitive Landscape

Competition centers on alliances rather than head-to-head battles. Vodafone’s decade-long USD 1.5 billion collaboration with Microsoft typifies how operators secure hyperscaler innovation while hyperscalers access carrier distribution. Ericsson, Nokia, and Samsung embed cloud APIs into RAN portfolios, ensuring relevance as network functions shift to software. Google Cloud, AWS, and Microsoft Azure tailor carrier-grade PaaS stacks, competing on automation, AI, and sovereignty guardrails.

Pure-play vendors fill niches-Mavenir in cloud-native IMS, Metaswitch in virtual session border control-while systems integrators handle complex multicloud choreography. The Global Telco AI Alliance reveals consortium models aimed at diluting hyperscaler dominance by co-developing multilingual LLMs. Competitive intensity is moderate; value creation hinges on ecosystem orchestration rather than zero-sum share grabs across the telecom cloud market.

Telecom Cloud Industry Leaders

AT&T Inc

BT Group PLC

Telefonaktiebolaget LM Ericsson

Verizon Communications Inc.

Telstra Corporation Ltd.

- *Disclaimer: Major Players sorted in no particular order

Telecom Cloud Market Companies Covered in this Report

- ATandT Inc.

- Verizon Communications Inc.

- BT Group plc

- Deutsche Telekom AG

- NTT Communications Corp.

- China Telecommunications Corp.

- Telstra Corp. Ltd

- Telefonaktiebolaget LM Ericsson

- CenturyLink (Lumen Technologies)

- Singapore Telecommunications Ltd

- Telus Corp.

- Swisscom AG

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- IBM Cloud

- Oracle Communications Cloud

- Huawei Cloud

- VMware (Telco Cloud Platform)

- Cisco Systems (Telco Cloud)

Market Opportunities and Future Outlook

A near-term opportunity is carrier-grade hybrid cloud that keeps production network functions under operator control while using hyperscaler tooling for automation and lifecycle management. O2 Telefonica moved production-scale 5G Core network functions onto AWS Outposts in its own data center with Nokia (March 2026), showing how operators can address sovereignty and latency constraints while still relying on public-cloud platforms. This supports demand for integrated offerings that combine NF/CNF onboarding, observability, security controls, and workload portability across distributed sites, particularly for core, traffic management, and edge workloads tied to 5G Standalone and enterprise use cases.

Another opportunity centers on interoperability and federation layers that reduce integration friction across multi-vendor telco clouds and speed up API exposure to application ecosystems. ETSI released OpenOP Version 1 in March 2026 as an open-source operator platform for telco cloud federation and capability exposure using CAMARA APIs, while Europe's EU Cloud Alliance published a Telco Cloud Reference Architecture (March 2025) to standardize integration patterns. Together, these initiatives support productization of common orchestration, policy, and service-exposure blueprints across private, public, and sovereign clouds, reinforcing addressable demand for PaaS-led developer platforms and managed services to help operators industrialize cloud operations under evolving sovereignty and security requirements.

Recent Industry Developments in Telecom Cloud Market

- June 2026: BT Group and Verizon signed an agreement to combine their international enterprise operations into a 50:50 joint venture serving more than 3,000 customers. The deal consolidates global connectivity platforms and operational assets, strengthening the bundle of network and cloud-adjacent services multinationals procure from telecom providers.

- March 2026: BT Group renewed and expanded its core network partnership with Ericsson, including deployment of a dual-mode 5G Core on BT Network Cloud with capabilities such as NSSF and NEF to support 5G Standalone functions. The expanded scope reinforces cloud-native core modernization and deepens the operator-vendor roadmap around programmable, API-exposed core services.

- June 2024: The EU Gigabit Infrastructure Act entered into force, setting a policy foundation to accelerate gigabit network rollouts across Member States. Faster access-network build activity increases the need for scalable core and edge capacity, supporting ongoing migration of telecom workloads toward cloud-based infrastructure and operations.

Telecom Cloud Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the telecom cloud market is defined as spending on cloud-based infrastructure, platforms, and software used by telecom operators to run network functions and related workloads (including virtualized and cloud-native functions), plus the services needed to deploy and operate them.

Scope exclusions: We exclude pure colocation or data-center space leasing revenue when it is not tied to telecom cloud workloads or telecom network-function delivery.

Segments Covered in This Report

- By Type

- Solution

- Unified Communication and Collaboration

- Content Delivery Network

- Other Solutions

- Service

- Colocation Services

- Network Services

- Professional Services

- Managed Services

- Other Types

- Solution

- By Application

- Billing and Provisioning

- Traffic Management

- Other Applications

- By Cloud Platform

- Software-as-a-Service (SaaS)

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- By End User

- BFSI

- Retail

- Manufacturing

- Transportation and Distribution

- Healthcare

- Government

- Media and Entertainment

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Taiwan

- Rest of Asia-Pacific

- Middle-East and Africa

- Middle-East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle- East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle-East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand picture and to set practical boundaries for what should be counted as telecom cloud spending versus adjacent IT or connectivity revenue. We referred to public sources such as the ITU, the World Bank, OECD broadband statistics, national telecom regulators, and standards and architecture references from bodies such as ETSI and 3GPP, since these help anchor operator rollout timelines and virtualization progress.

To pressure-test the operating assumptions, we also reviewed operator annual reports, earnings call transcripts, investor presentations, and reputable press coverage on 5G core modernization, cloud-native network functions, and network automation. In addition, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases to track comparable product positioning and to sanity-check the direction of ASP movement over time. The desk sources listed here are illustrative, and many other public and paid references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to confirm how telecom cloud budgets are split across infrastructure layers, virtualized and cloud-native network functions, and supporting services, and then to test whether the implied spend levels match what buyers and suppliers see in the field. We spoke with telecom operators, system integrators, cloud infrastructure and software providers, and channel partners across major regions so assumptions around adoption timing, migration pace, and pricing were checked against procurement patterns that respondents reported from ongoing deals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 40% |

| Mid tier: 61% | Functional/Unit leaders: 33% | EMEA: 33% |

| Smaller Players: 14% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where operator cloud migration activity and network modernization signals were used to reconstruct the addressable spend pool, and then allocations were applied across the telecom cloud stack based on adoption and deployment patterns. To keep the totals realistic, the output was corroborated using selective bottom-up approximations, such as sampled ASP times deployed capacity ranges, supplier revenue sampling where disclosures exist, and partner channel checks, which were then used to adjust outlier estimates.

Key inputs used in the model included the pace of 5G core rollouts, the share of network functions moving from physical to virtualized and cloud-native form factors (VNF to CNF progression), cloud deployment mix (public, private, and hybrid), capacity expansion signals for carrier-grade compute and storage, and services intensity during migration waves. For forecasting, scenario analysis was used to reflect differences in operator capex and opex cycles, with the scenario weights refined through expert feedback so the final curve fits what industry participants expect over the next few years. Where bottom-up visibility was limited for smaller countries or smaller suppliers, gaps were handled by using proxy adoption ratios tied to operator scale indicators and then re-checked against regional spending patterns.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including operator investment commentary, virtualization milestones, and observed pricing direction for cloud infrastructure and network-function software. If any country or region showed a sudden jump that did not align with rollout timing or procurement feedback, the assumptions were revisited and, when needed, follow-up calls were triggered to close the gap.

Before sign-off, the model is reviewed in multiple steps so arithmetic checks, scope checks, and year-on-year consistency checks are completed by more than one analyst. The report is refreshed annually, and interim updates are made when material events occur, such as major changes in operator cloud strategies or a visible shift in pricing. Right before delivery, a final review pass is completed so the published view reflects the latest available inputs.

Mordor Intelligence's Telecom Cloud Market Size Compared Against Other Published Estimates

Published telecom cloud market values often differ because the spending boundary is not identical across studies, and because the timing of currency conversion and pricing assumptions can shift the same underlying volumes into different USD totals. Differences also show up when one estimate leans on a single-year snapshot, while another spreads migrations more evenly across the forecast window.

The biggest gap drivers we see are how VNFs and CNFs are counted (and whether related services are bundled into the same total), whether colocation-style revenue is mixed into the number, and how ASP changes are treated as cloud infrastructure costs trend downward, while software and services intensity can rise. When FX rates are applied using different cutoffs and when assumptions are not revalidated after major operator announcements, the resulting market size can move noticeably, which is why a refresh-led model with consistent currency timing and rechecks is critical, a discipline applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.79 B (2026) | |

| Industry Research Publisher A | USD 22.10 B (2024) | The scope appears broader on deployment and application labels, but it is less explicit on excluding colocation-only revenue, and the earlier base year can understate later migration waves if ramp-up timing is spread differently. |

| Global Publisher B | USD 22.43 B (2024) | This estimate uses a 2024 base and may reflect a narrower interpretation of telecom-operator network cloud spend, with less emphasis on carrier-grade workload validation signals that shift spend recognition into later years. |

The table shows that year selection and what gets bundled into telecom cloud are the main reasons totals spread out across sources. By keeping inclusions tied to operator network cloud workloads, applying consistent FX timing, and revisiting ASP and adoption assumptions when field feedback changes, the result stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the telecom cloud market?

The telecom cloud market is valued at USD 39.79 billion in 2026.

How fast is the telecom cloud market expected to grow?

It is forecast to register a 26.95% CAGR, reaching USD 131.19 billion by 2031.

Which region is growing the quickest?

Asia-Pacific is projected to advance at a 26.85% CAGR thanks to heavy infrastructure spending and digital-government programs.

Why are services outpacing solutions in growth?

Operators increasingly outsource cloud operations to managed-service providers, driving the Services segment at a 27.25% CAGR as they focus internal resources on innovation.

What is the biggest restraint facing telecom cloud adoption?

Data-sovereignty and security compliance hurdles subtract 3.2 percentage points from forecast CAGR, particularly in regions with strict localization laws.

Page last updated on: