Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The North America Mobile Cloud Market Report is Segmented by User Type (Enterprise, and Consumer), End-User Industry (Individual Users, Small and Medium Enterprises, and Large Enterprises), Deployment Model (Public Cloud, Private Cloud, and Hybrid/Multi-Cloud), Application Type (mCommerce, Content Streaming, Productivity and Collaboration, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

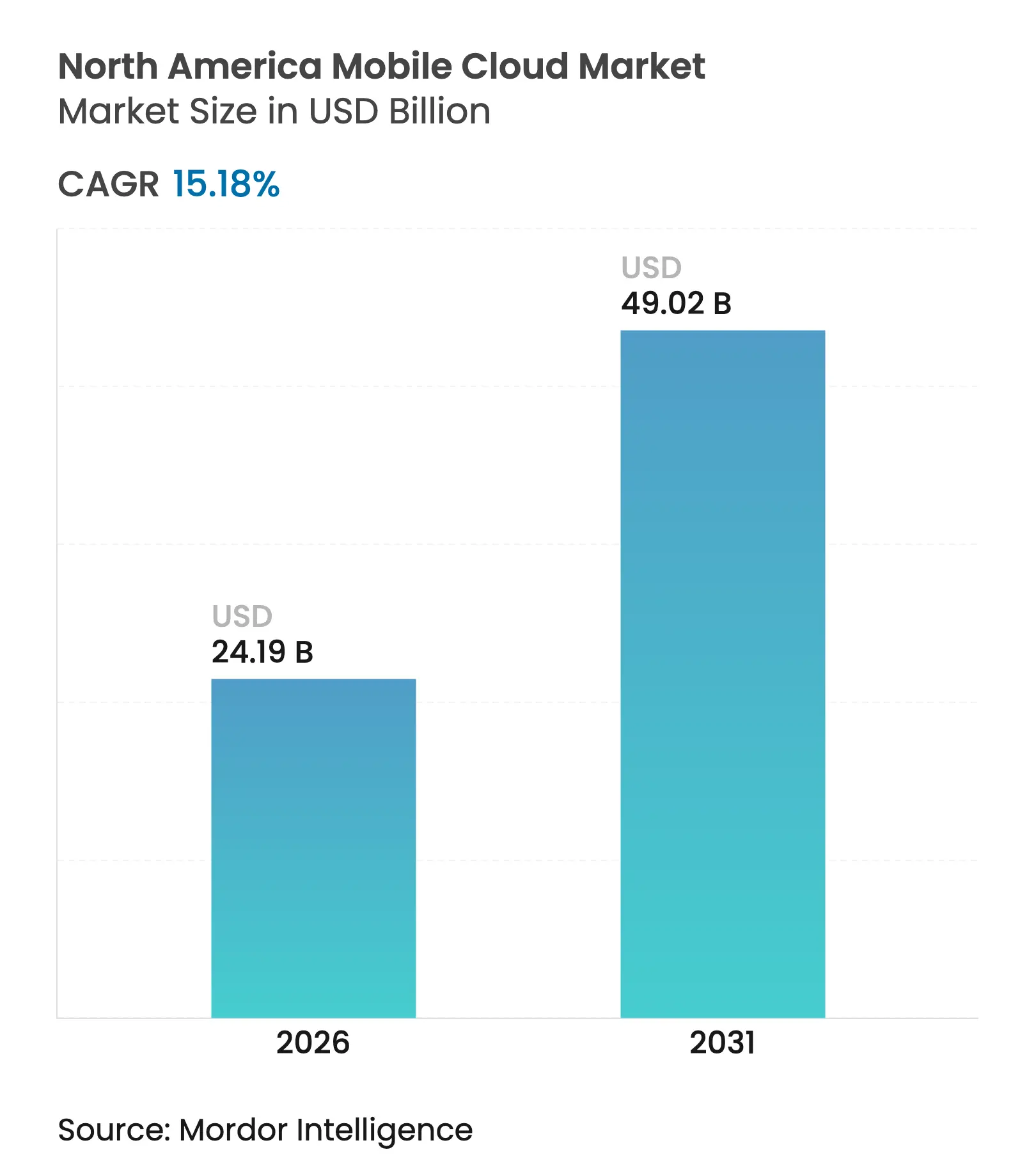

| Market Size (2026) | USD 24.19 Billion |

| Market Size (2031) | USD 49.02 Billion |

| Growth Rate (2026 - 2031) | 15.18 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The North America mobile cloud market size was valued at USD 21 billion in 2025 and estimated to grow from USD 24.19 billion in 2026 to reach USD 49.02 billion by 2031, at a CAGR of 15.18% during the forecast period (2026-2031). Edge-ready 5G build-outs, led by T-Mobile’s nationwide 5G Advanced footprint, have moved low-latency compute from core data centers to neighbourhood cell sites, opening fresh revenue streams for mobile-first workloads. Enterprises are prioritizing cloud-native network functions that process generative-AI inference close to subscribers, accelerating demand for container orchestration and serverless platforms. Consumer adoption is being catalysed by eSIM-only smartphones and direct-to-device satellite links that push always-on connectivity into previously unreachable areas. Meanwhile, hyperscalers are racing to extend programmable edge zones so customers can avoid expensive backhaul and data-egress fees. Mobile-specific zero-trust requirements, though essential, continue to impose latency overheads that vendors must engineer around.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

5G densification and edge POP build-out 5G densification and edge POP build-out | +4.20% | North America core, expanding to rural areas | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+4.20% | Geographic Relevance:North America core, expanding to rural areas | Impact Timeline:Medium term (2-4 years) |

Generative-AI-led mobile workload explosion Generative-AI-led mobile workload explosion | +3.80% | Global, with concentration in US tech hubs | Short term (≤ 2 years) | |||

BYOD security mandates (CISA and NIST SP-800-124 r2) BYOD security mandates (CISA and NIST SP-800-124 r2) | +2.10% | US federal and enterprise sectors, spillover to Canada | Medium term (2-4 years) | |||

ESIM-only smartphone design wave ESIM-only smartphone design wave | +1.90% | North America consumer markets | Long term (≥ 4 years) | |||

Low-orbit satellite backhaul integration Low-orbit satellite backhaul integration | +1.40% | Rural North America, remote industrial sites | Long term (≥ 4 years) | |||

Mobile app carbon-budget scrutiny Mobile app carbon-budget scrutiny | +1.10% | Global, with regulatory focus in North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

5G Densification and Edge POP Build-out

5G densification is transforming network topologies by relocating compute resources to micro-edge sites that sit one or two hops from the radio. T-Mobile’s 5G Advanced rollout delivers the sub-10 ms round-trip latency that cloud gaming and augmented-reality apps demand.[1]5G Americas, “T-Mobile Reaches 5G Advanced Nationwide Milestone,” 5gamericas.org Partnerships such as Vapor IO and NVIDIA in Las Vegas show how edge points of presence now function as mini data centers with GPU acceleration rather than simple packet gateways. Cloud providers are off-loading content caching, AI inference, and security inspection to these nodes, trimming backhaul expenses and meeting stringent data-residency rules. Fixed-wireless access has already connected roughly 9 million homes, widening the addressable base for mobile cloud subscriptions. The ongoing spectrum refarming in 6 GHz bands is set to intensify small-cell deployment and propel new service tiers for ultra-reliable low-latency communication.

Generative-AI-led Mobile Workload Explosion

Generative-AI chat, translation, and video-creation tools are ballooning per-user data volumes beyond historical forecasts. Ericsson expects AI-based video interactions to sustain traffic momentum even as traditional streaming plateaus.[2]Ericsson, “5G in the North America Region – Mobility Report,” ericsson.com Qualcomm estimates that cloud-only processing of multimodal AI queries could inflate infrastructure spend by billions, pushing vendors toward device-edge hybrids that trim compute cycles and power draw. Akamai’s Cloud Inference service promises 60% lower latency and 86% lower cost compared with centralized inference, underscoring how specialized silicon at the edge is rewriting cost curves. Enterprises are embracing bring-your-own-model strategies, running proprietary LLMs in secure mobile backends to preserve IP while meeting data-sovereignty mandates. These dynamics are redefining capacity planning, turning burstable GPU pools at the metro edge into a core buying criterion for cloud contracts.

BYOD Security Mandates (CISA and NIST SP-800-124 r2)

Revised guidelines from NIST and CISA require continuous posture assessment, zero-trust segmentation, and real-time threat feeds for any cloud that backs mobile endpoints.[3]National Institute of Standards and Technology, “SP 800-124 Rev 2: Guidelines for Managing the Security of Mobile Devices,” csrc.nist.gov FedRAMP inheritance gives established hyperscalers an advantage, but smaller providers are closing gaps through managed-security partnerships. Containerized workspaces that split corporate and personal data have become table stakes, influencing procurement cycles in healthcare, banking, and defense. Demand for dynamic policy engines that factor user behaviour, geolocation, and device health is accelerating SaaS adoption within the North America mobile cloud market. Vendors able to surface compliance dashboards and automated audit trails are winning multi-year framework agreements.

eSIM-only Smartphone Design Wave

Apple’s and Google’s moves to ship eSIM-only flagships remove the physical-SIM bottleneck, enabling users to switch carriers on demand and optimize network performance without a store visit. Roland Berger projects eSIM penetration hitting 75% of smartphone lines by 2030, up from 10% in 2023. For cloud providers, eSIM opens dynamic traffic-steering, letting apps pick the cheapest or fastest network in real time. New MVNOs are aligning with hyperscalers to offer programmable connectivity tiers integrated directly into developer toolchains. Thales highlights that eSIM and emerging iSIM place cryptographic keys in tamper-resistant hardware, simplifying zero-trust onboarding for enterprise devices.[4]Thales Group, “Weighing ‘Soft SIM’ and ‘Cloud SIM’ as IoT Connectivity Choices,” thalesgroup.com These advances will reshape roaming economics and encourage location-aware microservices that spin up region-specific edge containers as users move.

Restrain Impact Table

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Mobile-specific cloud egress costs Mobile-specific cloud egress costs | -2.30% | Global, with higher impact in multi-region deployments | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-2.30% | Geographic Relevance:Global, with higher impact in multi-region deployments | Impact Timeline:Short term (≤ 2 years) |

Zero-trust latency penalties Zero-trust latency penalties | -1.80% | Enterprise-focused markets in US and Canada | Medium term (2-4 years) | |||

Multi-jurisdiction data-residency conflicts Multi-jurisdiction data-residency conflicts | -1.50% | Cross-border operations between US, Canada, Mexico | Long term (≥ 4 years) | |||

Mobile app carbon-budget scrutiny Mobile app carbon-budget scrutiny | -1.20% | Global, with regulatory enforcement in North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Mobile-specific Cloud Egress Costs

Data-out fees slice 10-15% from many mobile application budgets, because frequent state sync and media uploads traverse multiple availability zones. AWS lists USD 0.05 per GB for internet egress from US East, a charge that accumulates rapidly for high-resolution video or AI model updates. Google Cloud’s recent decision to drop egress fees for customer-owned data hints at a forthcoming price war, yet inconsistent policies complicate forecasting. Startups that cannot negotiate volume discounts often refactor architectures, pushing content to regional edge nodes to avoid inter-region transfers. These pressures accelerate demand for multi-cloud routers and overlay networks that steer traffic toward the least-cost path without impacting user experience.

Zero-trust Latency Penalties

Service-mesh overlays insert additional TLS handshakes and policy lookups that stretch round-trip times by several milliseconds. Real-time gaming and AR sessions, which target sub-20 ms end-to-end delays, feel the impact first. DoD’s Zero Trust Architecture 2.0 concedes that CPU overhead rises along with encryption depth, prompting interest in data-plane acceleration offload cards. Mobile clients worsen the challenge because wireless jitter stacks on top of server-side processing, occasionally breaching UX thresholds. Vendors are experimenting with lightweight attestation protocols and hardware-anchored identity to cut authentication hops, but broad adoption remains a mid-term goal.

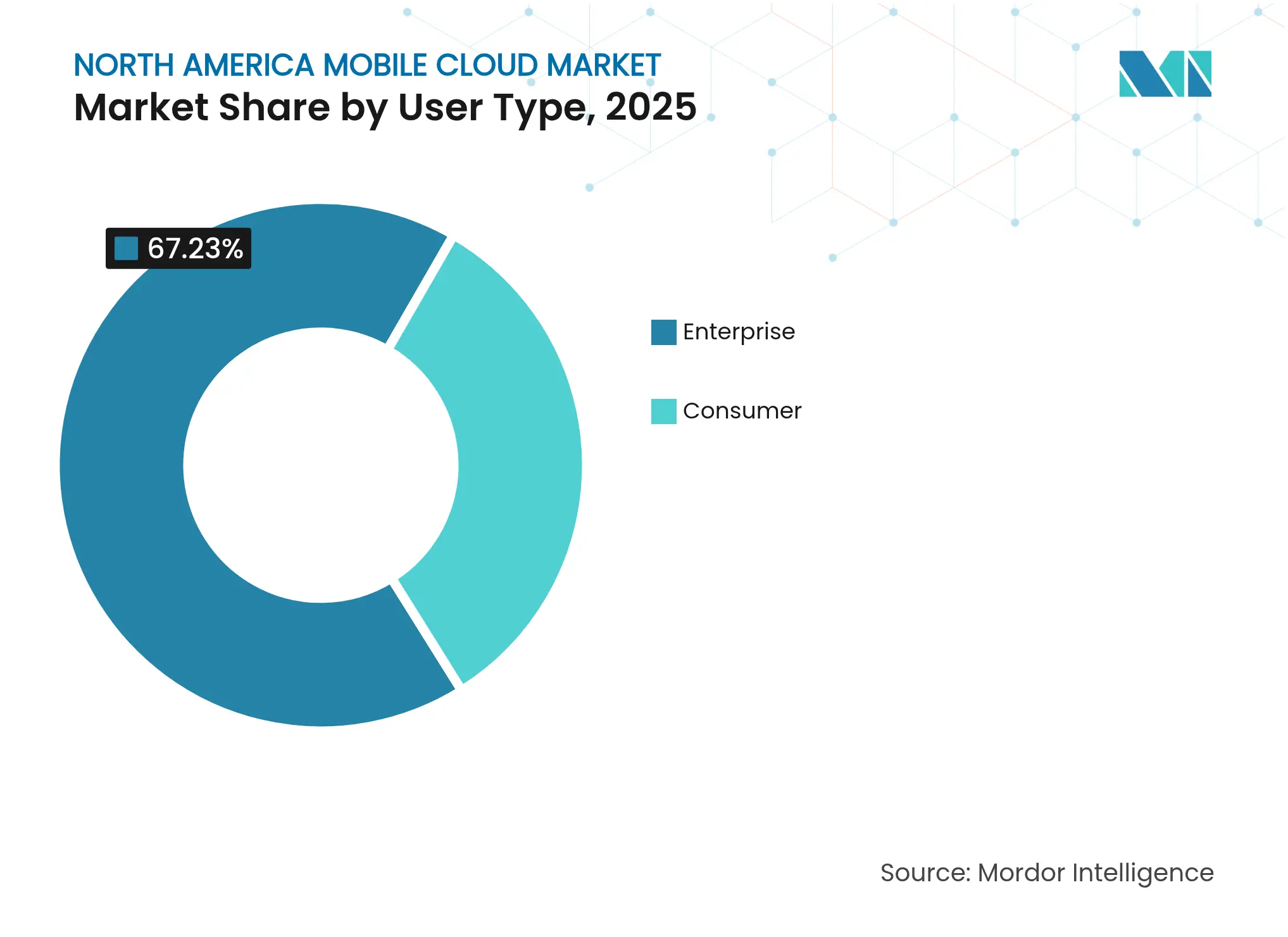

By User Type: Enterprise Dominance Drives Security Innovation

Enterprise customers generated USD 14.12 billion, equal to 67.23% of the North America mobile cloud market size in 2025. Federal contractors, healthcare networks, and global banks poured budget into mobile management suites that integrate zero-trust and AI-driven threat analytics. Consumer revenue, while smaller, is forecast to outpace enterprise at 19.08% CAGR, propelled by creator-economy apps that harness edge GPUs for live content rendering. Enterprises lean on FedRAMP-authorized SaaS and managed detection services that expose unified audit logs for regulators. In contrast, consumers chase low-friction signup flows and bundled data plans that hide complexity. Cloud vendors therefore segment product lines: hardened control planes with granular policy for enterprise buyers and lightweight, usage-based models for the gig-economy crowd.

The divergence encourages tiered infrastructure. Enterprise workloads land on private clusters with dedicated interconnects, while consumer traffic rides on shared multitenant fleets optimized for cost elasticity. Security mandates such as NIST SP-800-124 r2 motivate enterprises to adopt mobile application containers that isolate personal data, spurring demand for back-end identity brokers. At the same time, consumer adoption of eSIM-enabled roaming and on-device AI pushes edge capacity planning. This cross-pollination is blurring boundaries, with vendors like DigitalOcean courting both indie developers and mid-market IT teams under one portal, foreshadowing convergence across the North America mobile cloud market.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Individual Users Challenge Enterprise Assumptions

Large enterprises controlled 53.68% share in 2025, yet individual creators and freelancers are expanding at a 20.58% CAGR, a pace that will add fresh pressure on platform usability. Enterprises favour integrated access governance, centralized billing, and lengthy service-level commitments. Individual users prioritize pay-as-you-go compute bursts that spin up alongside a weekend coding sprint, often selecting simpler control panels over full-stack observability. This dichotomy forces providers to build dual personas into their consoles while unifying billing across roles.

Individual prosumers increasingly demand the same GPU clusters, low-code pipelines, and API gateways available to Fortune 500 accounts. The resulting traffic variability drives interest in autoscaling micro-VMs that boot in under a second. For the North America mobile cloud market, the implication is clear: back-end schedulers must juggle enterprise reservations and bursty consumer spikes within the same physical clusters. Providers that master this balancing act surface higher utilization without compromising SLA guarantees.

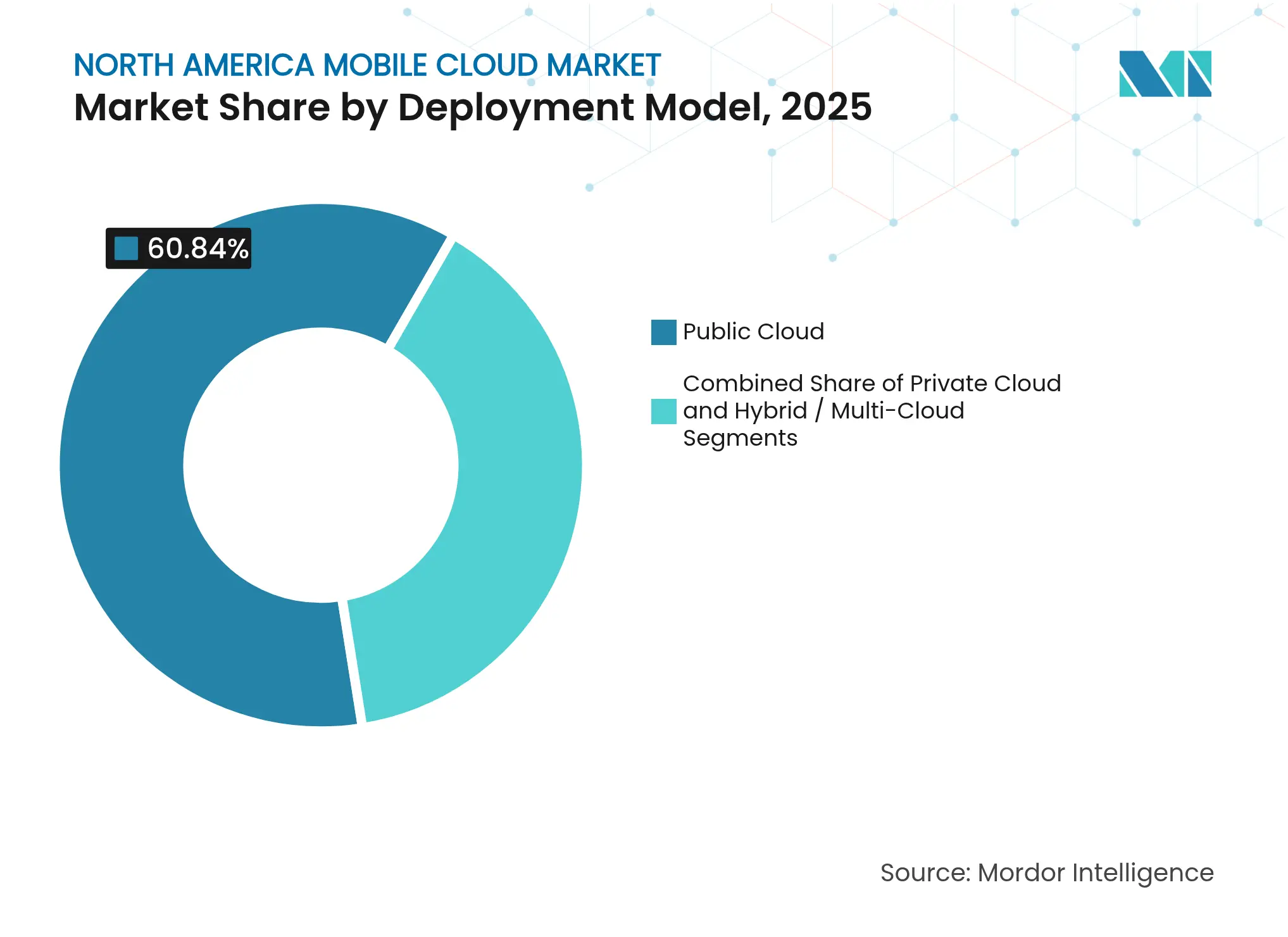

By Deployment Model: Hybrid Architectures Gain Strategic Importance

Public cloud services gathered 60.84% of the North America mobile cloud market share in 2025 by offering predictable pricing and friction-free onboarding. However, hybrid patterns are growing fastest at 22.03% CAGR as organizations blend colocation racks, telco edges, and hyperscale regions. Data-sovereignty laws and egress-cost discipline push sensitive tables and media libraries into nearby private clouds, leaving stateless microservices on public endpoints. DigitalOcean’s Partner Network Connect exemplifies this posture by tunnelling 1-10 Gbps links between multiple providers to slash cross-cloud transfer fees.

Hybrid adoption is reinforced by multicloud disaster-recovery playbooks that replicate databases across vendor boundaries. Telcos, meanwhile, package compute alongside network slices, creating a unified fabric that auto-steers packets to the nearest function instance. This model positions the North America mobile cloud market as an orchestration canvas rather than a monolithic stack, rewarding platforms that provide consistent policy controls regardless of location.

Note: Segment shares of all individual segments available upon report purchase

By Application Type: Gaming Leads While Health Emerges

Mobile gaming produced USD 5.74 billion, or 27.33% of 2025 revenue, benefiting from latency budgets that shrink to single-digit milliseconds inside 5G Advanced clusters. Cloud-rendered AAA titles rely on edge GPU pools that eliminate device heat and battery drain. In parallel, mobile health logged the highest growth rate at 23.62% CAGR, catalysed by FDA guidance that clarifies paths to clearance for diagnostic apps. Clinics deploy HIPAA-compliant video consult services hosted at metropolitan colocation sites to secure protected health information while minimizing lag.

Beyond these anchors, AI-assisted productivity suites and short-form video editors stretch platform capabilities by mixing compute-intensive inference with bursty storage. Retailers piloting cashier-less stores stream inference models to camera arrays, using mobile cloud back-ends for real-time stockkeeping. Gaming’s predictable peak periods contrast with health and retail which deliver always-on workloads, prompting providers to layer reservation-based capacity alongside spot pricing. Thus, application diversity reinforces the architectural flexibility crucial to the North America mobile cloud market.

The United States generated 81.92% of 2025 revenue, underpinned by extensive 5G coverage, dense edge colocation, and early-adopter enterprises that fund proof-of-concept pilots. AWS expanded its Outposts catalogue with new racks built for telco-grade environments, letting carriers run cloud stacks inside central offices while maintaining hybrid control panels. Microsoft, Google, and Akamai followed suit with metro-edge rollouts so developers can latch compute within 30 km of subscribers. Federal mandates on mobile security accelerate domestic spending because agencies must modernize legacy remote-access portals.

Canada, though smaller today, is pacing at an 17.93% CAGR. Regulatory reforms compel BCE and Telus to open fibber loops to competitors, spurring bandwidth price declines and carrier differentiation around value-added cloud. CAD 11.4 billion invested in 2024 upgraded rural towers and laid dark fiber to northern territories. Over 90% population enjoys 5G availability, giving app developers a national sandbox for testing low-latency features. Immigration-led labour force growth fuels digital service uptake, translating to double-digit subscription gains for cloud video, fintech, and telehealth platforms.

Mexico sits at an earlier stage yet posts compelling momentum. Its technology sector expanded 4.9% in 2024, and cloud services are projected to rise 12.6% in 2025 as Microsoft commits USD 1.3 billion to new zones and Google Cloud opens a Queretaro region. With 6.6 million 5G lines and e-commerce forecast to crest USD 29.6 billion, demand for scalable back-ends is accelerating. Government forecasts cite USD 3.36 billion GDP lift from 5G health use cases by 2030, implying robust tailwinds for medical-grade mobile apps. Collectively, these dynamics illustrate how infrastructure maturity and policy regimes dictate adoption velocity across the North America mobile cloud market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

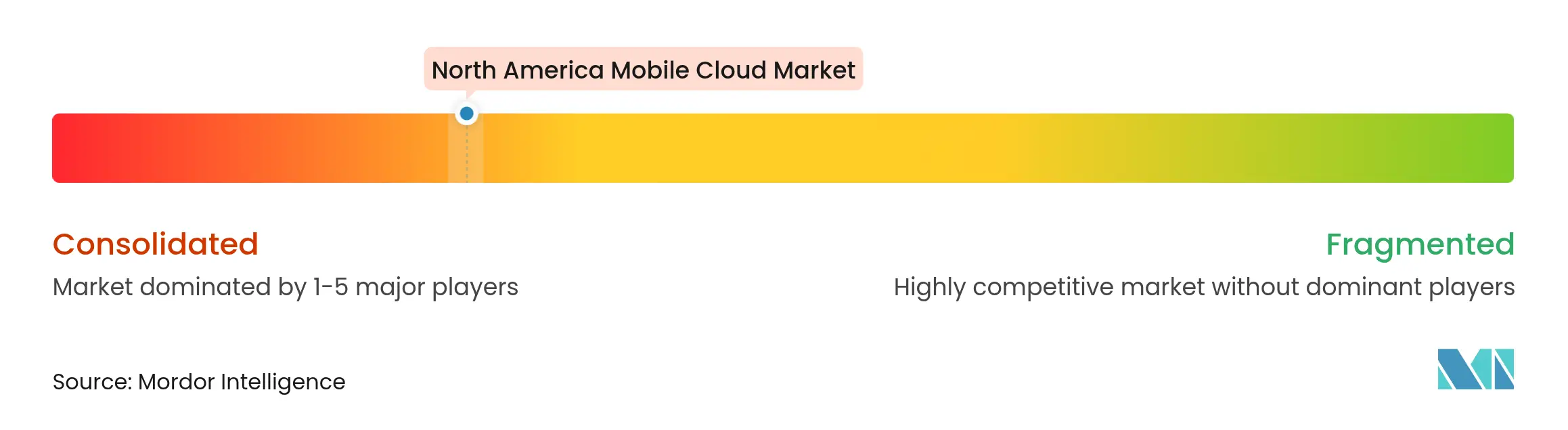

Market Concentration

Competition is moderate and intensifying as hyperscalers broaden edge coverage while specialized providers carve out performance-sensitive niches. AWS leads through an end-to-end portfolio that bundles silicon, managed services, and partner marketplaces. Its USD 230 million Generative AI Accelerator attracts early-stage mobile-first startups, locking workloads into its ecosystem. Microsoft counters with strategic regional investments and Azure-OpenAI integrations, courting enterprises that desire ChatGPT-style capabilities while meeting compliance obligations. Google Cloud differentiates via data-analytics tooling and cost-optimized multicloud ingress.

Akamai, historically a CDN, now positions as a full-stack cloud after acquiring Edgio assets and unveiling compute services across 4,200 edge sites. This footprint resonates with mobile gaming studios that crave predictable sub-20 ms latency. DigitalOcean targets developers seeking simplicity: one-click GPU instances, transparent outbound traffic pricing, and grants up to USD 100,000 for GenAI startups. Qualcomm, NVIDIA, and Snowflake form the enabling layer, supplying edge accelerators and data-mesh fabrics that mobile clouds embed as managed offerings. Partnerships flourish: IBM aligns watsonx with Salesforce’s Einstein 1 to furnish turnkey AI for mobile workforce apps, while telcos team with hyperscalers to wrap network slices in programmable APIs.

Consolidation remains likely as capital-intensive edge rollouts test smaller providers’ balance sheets. Yet fragmentation persists in vertical use cases such as regulated health, where boutique clouds with HITRUST certifications retain loyal tenants. Overall, vendor differentiation hinges on three pillars: egress cost policy, developer experience, and proximity to users. Providers that optimize all three stand to capture disproportionate share of the evolving North America mobile cloud market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The North America Mobile Cloud Market Report is Segmented by User Type (Enterprise, and Consumer), End-User Industry (Individual Users, Small and Medium Enterprises, and Large Enterprises), Deployment Model (Public Cloud, Private Cloud, and Hybrid/Multi-Cloud), Application Type (mCommerce, Mobile Gaming, Content Streaming, Productivity and Collaboration, and Other Application Types), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.