Personal Cloud Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 38.69 Billion |

| Market Size (2031) | USD 82.06 Billion |

| Growth Rate (2026 - 2031) | 16.23% CAGR |

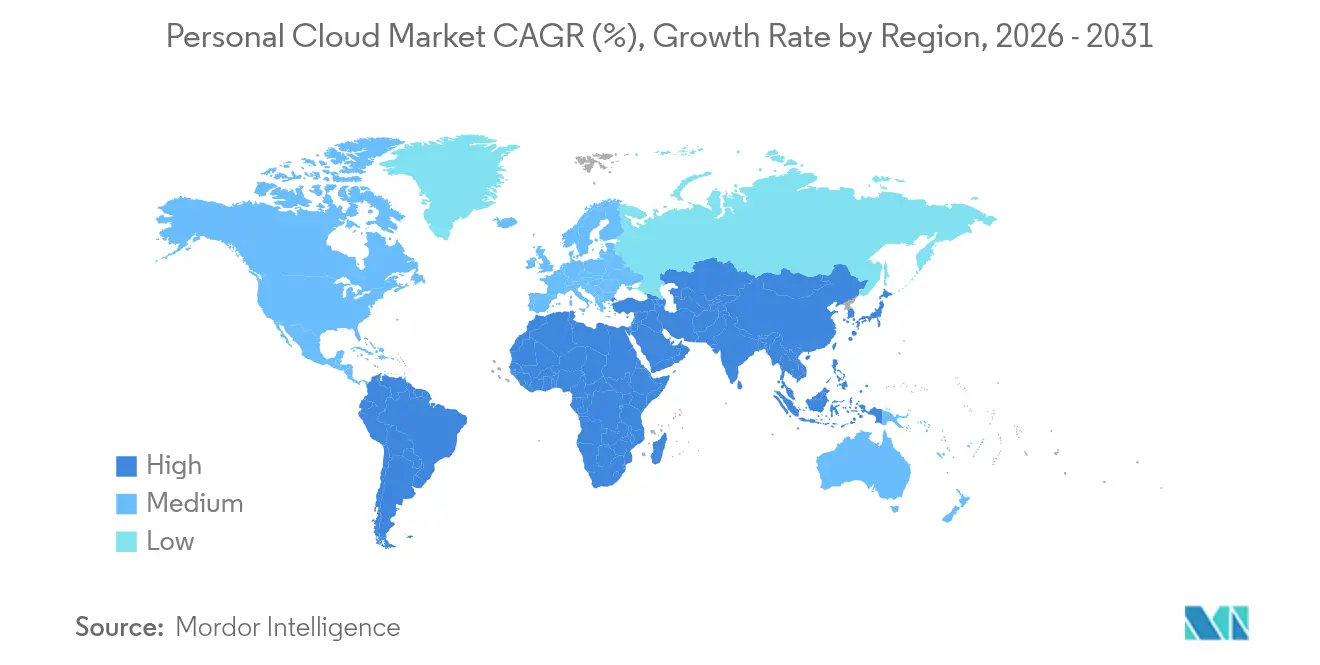

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Cloud Market Analysis by Mordor Intelligence

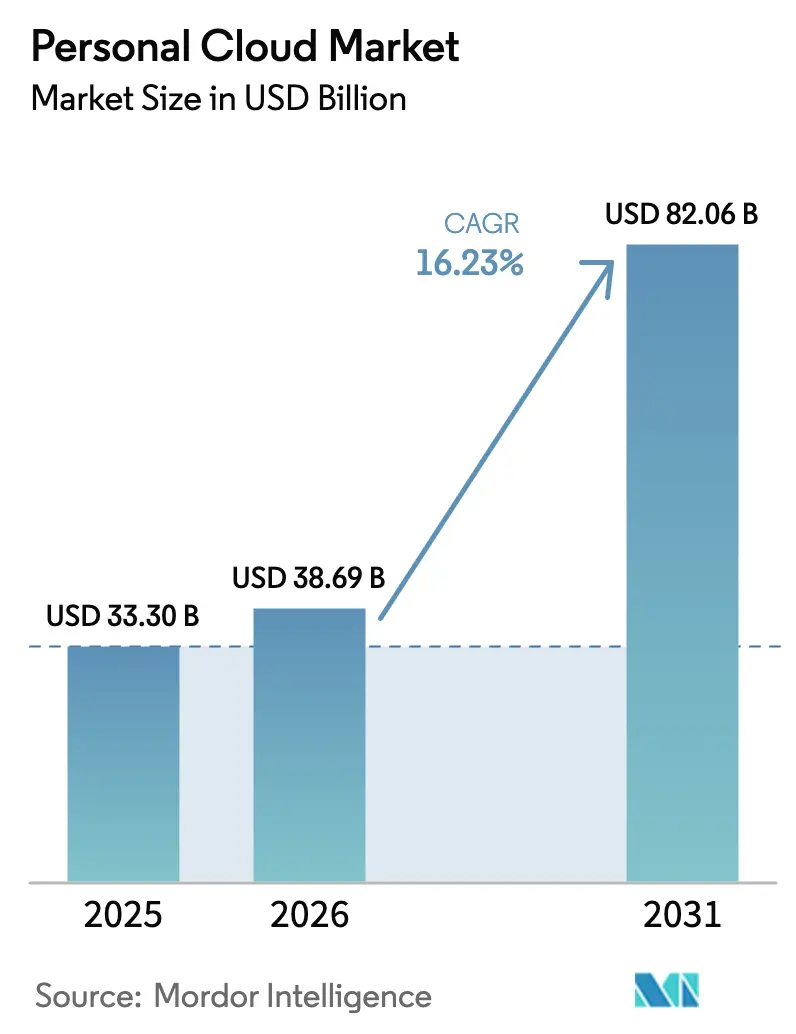

The personal cloud market size is expected to grow from USD 33.3 billion in 2025 to USD 38.69 billion in 2026 and is forecast to reach USD 82.06 billion by 2031 at 16.23% CAGR over 2026-2031. Sustained double-digit expansion reflects a decisive transition from local storage toward cloud-first data management, underpinned by 5G roll-outs, rapid AI infusion across consumer applications, and cross-device demand for friction-free content access. Telecom operators are bundling storage with connectivity to address subscription fatigue and reduce churn, while data-sovereignty regulations are steering providers toward regional infrastructure investments. Intensifying privacy expectations are shifting the conversation from capacity to control, pushing providers to differentiate through encryption, zero-knowledge architectures, and hybrid deployment options. Finally, AI-powered curation, search, and memory-re-engagement tools are transforming cloud storage from a passive utility into an experiential service layer, expanding the addressable pool of paying users.

Key Report Takeaways

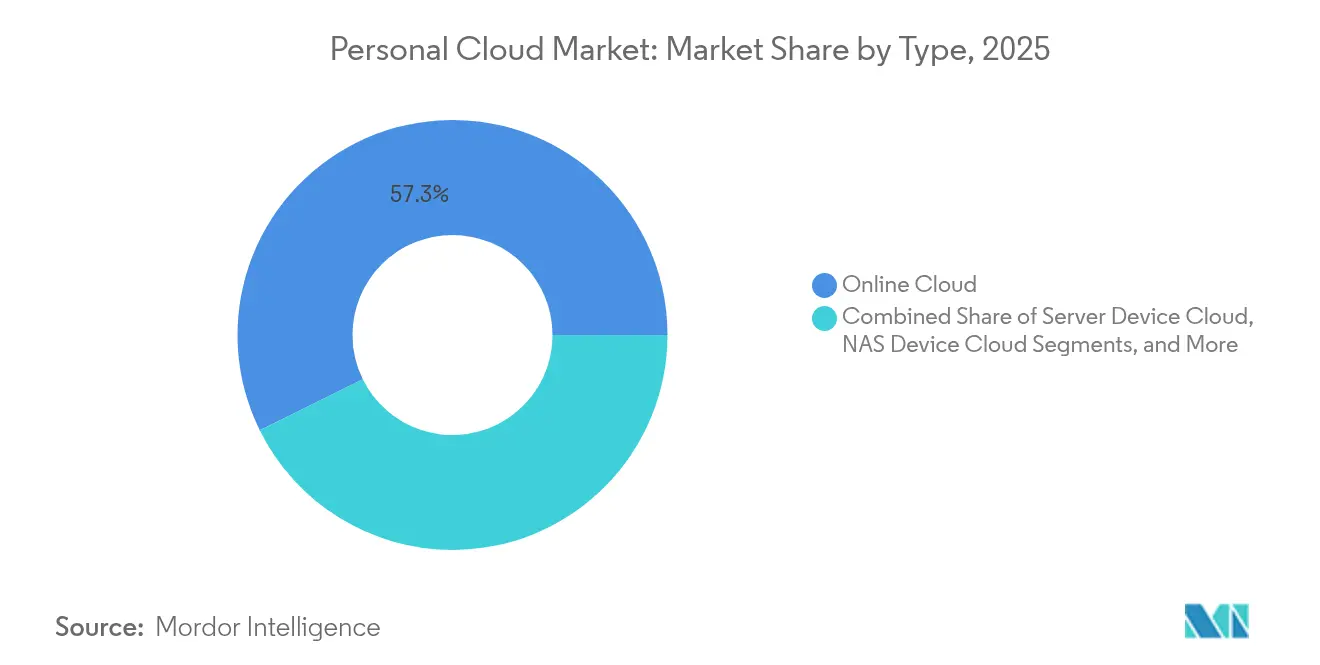

- By type, Online Cloud accounted for 57.30% of personal cloud market share in 2025, whereas NAS Device Cloud is on track to grow at an 18.02% CAGR through 2031.

- By hosting model, Provider Hosting dominated with 80.25% revenue share in 2025, while User/Self Hosting is projected to expand at 17.42% CAGR to 2031.

- By revenue type, Direct streams (subscriptions and one-time licenses) captured 64.10% in 2025; Indirect models are set to grow at 20.45% CAGR between 2026-2031.

- By pricing model, the Freemium tier held 53.20% in 2025, yet Tiered Subscription is the fastest-growing approach at 19.12% CAGR.

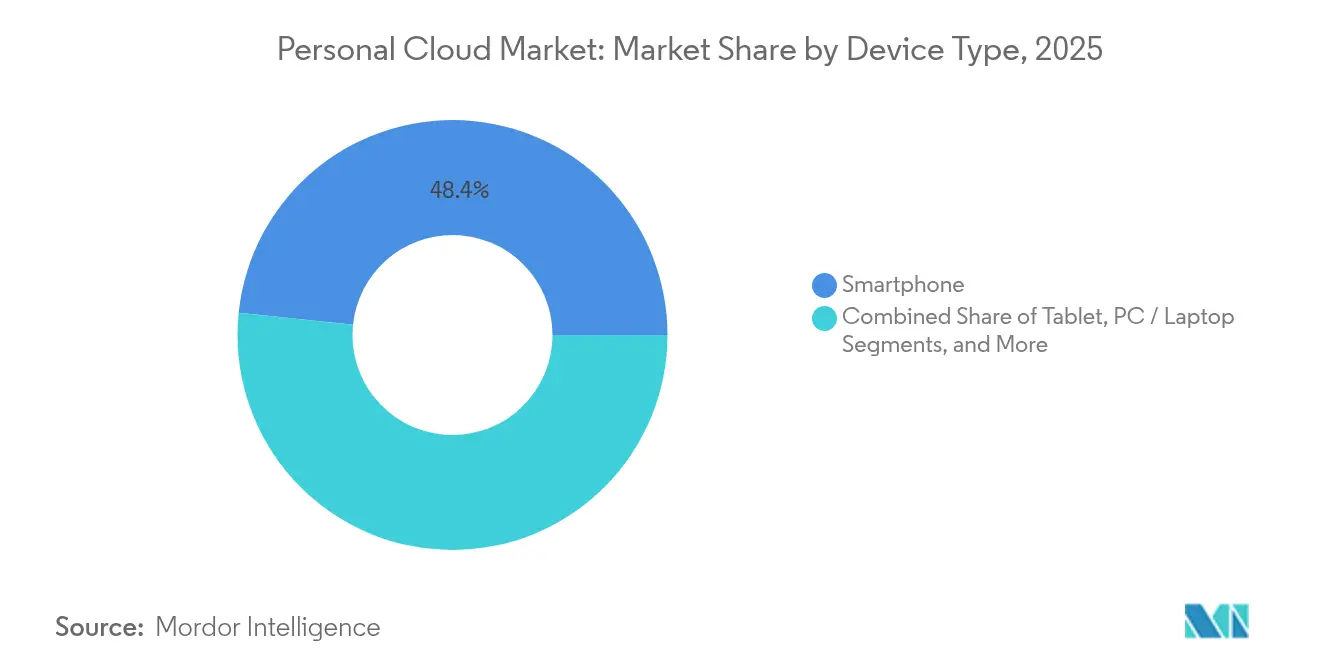

- By device type, smartphones remained the leading access point with 48.35% in 2025, but smart-home devices are poised for 16.78% CAGR through 2031.

- By end-user, consumers generated 71.40% of 2025 revenue, while the SME segment will grow at 19.66% CAGR on the back of hybrid-work adoption.

- By geography, North America retained regional leadership with 33.60% of 2025 revenue, whereas Asia is forecast to record an 18.25% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation of 5G Smartphones Boosting Personal Cloud Usage in Asia | +3.20% | Asia, with spillover to North America and Europe | Medium term (2-4 years) |

| Telecom-Operator Bundled Personal Cloud Services Raising ARPU in North America | +2.50% | North America, with emerging impact in Europe | Short term (≤ 2 years) |

| AI-powered Content Curation and Memory Re-engagement Features Driving Paid Upgrades | +4.10% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Data-Residency Mandates in Europe Accelerating Operator-Hosted Personal Cloud Nodes | +2.80% | Europe, with spillover to Asia and North America | Medium term (2-4 years) |

| Smart-Home Ecosystem Integration Expanding Use Cases Beyond Storage | +1.90% | North America and Europe | Long term (≥ 4 years) |

| SME Shift from On-prem NAS to Subscription Personal Cloud for Hybrid Workforce | =3.60% | Global, with stronger impact in North America and Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid proliferation of 5G smartphones boosting uptake

Asia’s accelerated 5G build-out is eliminating latency bottlenecks that once discouraged mobile cloud use. Higher upstream bandwidth allows lossless real-time photo backup, RAW video uploads, and contiguous device-to-device sync. Regional handset makers are embedding on-device AI inferencing that cooperates with cloud engines for privacy-preserving personalization, a model showcased during MediaTek’s 2025 Generative AI Gateway launch [1]MediaTek, “MediaTek Showcases AI Vision From Edge to Cloud at Computex 2025”, mediatek.com. Operator metrics already indicate that 5G users generate 2.4 × the cloud-bound traffic of 4G cohorts, positioning personal cloud market services as a default companion feature of next-generation mobility plans.

Telecom-operator bundles raising ARPU

North American carriers now package 1-2 TB of encrypted storage inside premium 5G plans, elevating stickiness while adding USD 2-4 blended ARPU. Verizon and AT&T report churn reductions approaching 30% among cloud-enabled subscribers, validating the bundling thesis. Synchronoss’ 2025 platform refresh supports more than 11 million active telecom customers, processes 50 million photos daily, and underpins operators’ brand-labeled offerings at scale. As the model spreads to Europe, bundled propositions are expected to offset downward pressure on standalone pricing.

AI-powered curation accelerating premium conversion

Algorithmic clustering of photos, auto-generation of “memory reels,” and voice-activated media search have moved storage beyond commoditized gigabytes. Providers using on-device object detection combined with cloud-side large-language-model processing report conversion lifts of up to 40 % from free to paid tiers. Deloitte finds that half of consumers aged 24-45 would accelerate upgrades if AI utilities are present. The value narrative pivots toward emotionally resonant experiences, reinforcing willingness to pay even as headline capacity prices decline.

Data-residency mandates creating regional nodes

More than 80 countries enforce some form of data-localization law, a trend most mature in Europe where GDPR, DSA, and emerging digital sovereignty initiatives require in-region processing. Operators with domestic data center estates are capitalizing by offering compliance-ready storage, while hyperscalers establish sovereign cloud zones or partner with carriers for host-country nodes. This regulatory undercurrent rewards providers able to demonstrate auditable locality and accelerates multi-geography rollout road-maps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer-Privacy Litigation Against Big-Tech Cloud Platforms in EU | -1.80% | Europe, with spillover to North America | Medium term (2-4 years) |

| Price Wars and Freemium Conversions Depressing ARPU | -2.30% | Global | Short term (≤ 2 years) |

| Rural Broadband Gaps Limiting Uptake in South America and Africa | -0.70% | South America, Africa, and rural areas globally | Long term (≥ 4 years) |

| Hardware Supply-Chain Volatility Raising BOM Cost for On-prem Appliances | -0.90% | Global, with stronger impact in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer-privacy litigation in the EU

Ongoing class actions on data-harvesting practices have forced providers to re-architect consent flows, adopt privacy-by-design frameworks, and localize processing. The European Commission’s updated Standard Contractual Clauses add compliance overhead for cross-border transfers [2]European Commission, “New Standard Contractual Clauses – Questions and Answers overview”, commission.europa.eu. Providers incur higher legal and engineering costs, and risk revenue slowdowns if data-driven monetization models are curtailed.

Price wars depressing ARPU

Aggressive capacity giveaways and headline price cuts drive user acquisition yet constrain profitability. Freemium conversion rates stay in the low-single-digit range, pressuring providers to upsell via differentiated feature bundles. Sustained discounting risks training consumers to expect free storage, complicating monetization unless value-added services command clear willingness to pay.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Balance shifts toward hybrid control

The personal cloud market continues to be led by Online Cloud services, which commanded 57.30% of revenue in 2025 by virtue of zero-hardware onboarding and ubiquitous mobile integration. However, NAS Device Cloud alternatives are growing fastest at an 18.02% CAGR to 2031 as privacy-minded users pursue greater ownership of encryption keys and physical disks. This niche overlaps consumer and prosumer segments, and suppliers are embedding AI-level metadata tagging so that smart-albums and contextual search remain comparable to online rivals. Growth in NAS adopters signals that perceptions of convenience versus control are evolving, especially for high-resolution creators who prefer local throughput yet require cloud redundancy. Enterprises meanwhile maintain Server Device Cloud deployments when regulatory or performance needs call for single-tenant instances. The trajectory suggests convergence: online providers add optional local cache appliances, while NAS vendors integrate seamless remote-access portals, blurring formerly discrete categories.

Yet Online Cloud incumbents enjoy powerful network effects through integrated productivity suites, cross-device photo viewers, and zero-touch sharing links. Their sizeable install bases enable continuous telemetry-driven product iteration, keeping churn low. NAS entrants counter by highlighting offline-first resilience, customizable retention policies, and subscription avoidance. Providers at both ends are investing in federated identity and Open API approaches so that hybrid workflows do not trap data in silos. Over the forecast horizon, differentiation will pivot less on raw capacity and more on orchestration sophistication, ransomware recovery guarantees, and verifiable encryption methods that underpin user trust in the personal cloud market.

By Hosting Model: Sovereignty concerns spur self-hosting

Provider Hosting captured 80.25% of 2025 spending owing to friction-free sign-up, elastic scale, and continuous updates delivered by hyperscalers. Nonetheless the User/Self Hosting category is set to widen at 17.42% CAGR as CIOs re-evaluate data-sovereignty exposure. Industry research indicates that 86% of technology leaders plan partial repatriation of workloads to private environments in 2025. Self-hosting resonates with regulated sectors and privacy-oriented consumers who prefer to hold encryption keys on premise. Containerized installer stacks, automatic patch pipelines, and subscription-based support contracts are lowering the entry threshold, making this path viable beyond highly technical enthusiasts.

Hybrid adoption is becoming mainstream: data frequently accessed for collaboration resides with the provider, whereas archival or sensitive content is parked in the user’s datacenter. Vendors respond by offering orchestration dashboards that surface both pools under a unified namespace, shielding users from topological complexity. Provider-hosted services still dominate because of cost efficiencies at scale, but growth in self-hosting underscores a broader theme of digital autonomy that increasingly shapes buying criteria in the personal cloud market.

By Revenue Type: Beyond storage monetization

Direct subscriptions and perpetual licenses delivered 64.10% of revenue in 2025, yet stakeholder interviews reveal tightening ceiling effects as freemium saturation rises. Indirect channels—advertising, in-app merchandising, and operator bundles—are accelerating at 20.45% CAGR, allowing providers to monetize large free cohorts without aggressive upsell tactics. Operators view cloud bundles as stickiness levers, subsidizing capacity from connectivity margins. Advertising-funded tiers, though sensitive to privacy optics, appeal to price-sensitive audiences when consent frameworks are transparent.

Subscription-based revenue remains reliable, but its architecture is evolving toward modular packs rather than monolithic plans. Providers cluster AI editing, smart-home device sync, and advanced recovery under premium add-ons, generating incremental ARPU while honoring granularity. Successful indirect monetization balances data ethics with experiential value, underscoring the strategic complexity of revenue diversification within the personal cloud market.

By Pricing Model: Tiering refines value capture

Freemium offerings delivered 53.20% of 2025 downloads and remain the gateway for audience expansion. However, Tiered Subscription pricing is rising at 19.12% CAGR as providers fine-tune feature stratification and align paywalls with clear experiential leaps. Typical designs retain a free safety-net tier (5-15 GB) while positioning mid-range plans around family sharing, vault encryption, and AI storytelling. Business-grade tiers incorporate compliance attestations such as ISO 27001 and SOC 2, attracting SME administrators who need audit readiness.

Usage-based billing is starting to surface for professional creators whose storage spikes episodically. Bundled pricing inside telecom or device ecosystems offers another vector, converting hardware margins into recurring cloud revenue. Across models, clarity and predictability trump complexity; providers that articulate benefit-led tiers while minimizing surprise fees stand to capture the highest lifetime value in the personal cloud market.

By Device Type: Smart-home endpoints catalyze data flows

Smartphones retained 48.35% access share during 2025 because they generate the bulk of personal media. Yet smart-home devices—security cameras, speakers, thermostats—are projected to climb at 16.78% CAGR. Continuous 4K footage and event logs stream directly to the cloud, demanding robust ingest and tiered retention policies. Providers are experimenting with edge-AI filtering that stores motion-triggered highlights while cold-archiving raw video to lower-cost tiers, balancing bandwidth and economics.

PCs and laptops continue to matter for batch content management and creative workflows that involve large assets, whereas tablets bridge casual consumption. As device diversity expands, the overriding product requirement is seamless cross-context identity recognition so that actions taken on one screen synchronize instantaneously elsewhere. Device growth patterns therefore intensify the importance of orchestration intelligence within the personal cloud market.

By End-User: SME momentum reshapes design priorities

Consumers generated 71.40% of 2025 turnover, but SMEs represent the fastest-growing cohort at 19.66% CAGR. Hybrid work has converted personal cloud services into quasi-file-servers that provide version control, ransomware rollback, and zero-trust sharing links without the administrative burden of traditional file servers. Managed Service Providers report that outsourcing storage cuts SME IT costs by 20-30%. Large enterprises continue to align personal cloud deployments within broader multi-cloud strategies, treating them as user-focused complements to object-storage back-ends.

Product road maps are adapting: role-based access control, audit trails, and integration with SaaS productivity stacks now headline marketing material. Simultaneously, consumer tiers double down on automatic photo stories and family vaults. The bifurcation obliges vendors to maintain dual emphasis—consumer delight on one side, business-grade rigor on the other—while reusing core storage engines, sustaining economies of scale across the personal cloud market.

Geography Analysis

North America captured 33.60% of 2025 spending, supported by high broadband penetration, early 5G adoption, and entrenched subscription behaviors. Providers leverage sophisticated billing infrastructure to experiment with micro-tiers and AI-enhanced upsells. Regulatory attention is intensifying but remains less prescriptive than Europe’s, giving operators greater room for service innovation. The rise of operator-bundled storage, typified by Verizon’s myHome plan, demonstrates how connectivity incumbents convert network differentiation into cloud stickiness. Growth prospects revolve around AI-driven feature expansion and deeper smart-home integration.

Asia is the fastest-growing territory at an 18.25% CAGR through 2031. Massive smartphone penetration and large-scale data-center investments are the dual engines of expansion. KPMG forecasts regional data-center capacity doubling to 37,580 MW by 2030. Chinese platforms integrate personal cloud directly inside super-apps, fusing storage with payments and social feeds. Localization laws in India and China create niches for domestic providers with sovereign stacks, compelling international firms to form joint ventures or license models. Fast-moving consumer expectations—driven by short-video and gaming cultures—translate into higher per-user storage creation, reinforcing the importance of regional edge nodes.

Europe’s landscape is uniquely shaped by GDPR, SCC frameworks, and an active antitrust agenda. The Competition and Markets Authority’s cloud services investigation signals scrutiny of contract lock-ins and data-egress pricing . Providers address data sovereignty by building EU-specific clusters or partnering with telecom operators who already host in-country facilities. Privacy-aware consumers are willing to pay premium increments for demonstrable compliance, supporting monetization of value-added encryption and audit-logging features. While regulatory friction elevates cost structure, it also protects providers that excel in transparency and local trust, sustaining healthy profitability within the regional slice of the personal cloud market.

Competitive Landscape

The personal cloud market shows moderate concentration among large platform providers, yet persistent room for differentiation. Alphabet, Microsoft, and Apple leverage integrated ecosystems—mobile OS, productivity suites, hardware—to deliver frictionless storage add-ons. Telecom operators are emerging challengers, converting network assets and billing relationships into turnkey cloud bundles. Synchronoss underpins many of these white-label offerings, illustrating a vendor-partner model that scales rapidly inside carrier channels. Start-ups target privacy and decentralization niches through zero-knowledge cryptography and blockchain-anchored metadata, positioning as antidotes to perceived hyperscale overreach.

Strategic vectors center on AI, security, and ecosystem breadth. Microsoft’s FY25 Q3 results highlighted 20% year-on-year cloud revenue expansion, affirming AI-linked premium tiers as growth engines. Dropbox pivots toward enterprise collaboration while retaining consumer mindshare through AI search and automated transcription, securing a differentiated foothold in the content-centric subset of the personal cloud market. Hardware vendors such as Hewlett Packard Enterprise advance private-cloud appliance stacks that bridge on-prem control with public cloud elasticity, addressing the hybrid demands of regulated industries.

Competitive intensity is expected to rise as generative AI democratizes advanced media tooling, making time-to-market and GPU partnerships critical. Providers that master seamless multi-cloud orchestration, transparent pricing, and regulator-friendly architectures will consolidate leadership while niche innovators exploit privacy micro-segments and regional compliance gaps.

Personal Cloud Industry Leaders

Google LLC

Microsoft Corporation

Apple Inc.

Dropbox, Inc.

Amazon Web Services, Inc. (AWS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hewlett Packard Enterprise launched an advanced private-cloud portfolio anchored by HPE Morpheus VM Essentials, promising 90% savings on VM licence costs and 2.5× lower TCO to strengthen its hybrid-IT value proposition.

- April 2025: Microsoft reported USD 42.4 billion in Q3 FY25 cloud revenue, a 20% year-on-year increase, underscoring cloud and AI as primary levers for productivity and security differentiation.

- March 2025: Dell Tech World spotlighted the dual imperative of generative AI adoption and flexible hypervisor choice, culminating in the Dell Private Cloud and Automation Platform aimed at simplifying multi-hypervisor estates.

- January 2025: Synchronoss introduced its next-generation Personal Cloud platform featuring AI-powered photo editing, supporting 11 million subscribers and 230 PB of managed data, bolstering carrier-bundled service capacity.

Global Personal Cloud Market Report Scope

A personal cloud is a collection of digital content and services that are accessible from any device through the internet. It is the individual's collection of digital content, services and apps which are seamlessly accessible across any device.

The personal cloud market is segmented by type (server device cloud, NAS device cloud, home-made cloud, online cloud), by hosting (provider hosting, user/self hosting), by end-user (consumer, enterprises), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Server Device Cloud |

| NAS Device Cloud |

| Self-hosted Cloud |

| Online Cloud |

| Provider Hosting |

| User / Self Hosting |

| Direct (Subscription, One-time) |

| Indirect (Advertising, Bundled) |

| Freemium |

| Tiered Subscription |

| One-time License |

| Bundled with Device / Telco Plan |

| Smartphone |

| Tablet |

| PC / Laptop |

| Smart-Home Device |

| Consumers |

| Small and Medium Enterprises |

| Large Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Type | Server Device Cloud | ||

| NAS Device Cloud | |||

| Self-hosted Cloud | |||

| Online Cloud | |||

| By Hosting Model | Provider Hosting | ||

| User / Self Hosting | |||

| By Revenue Type | Direct (Subscription, One-time) | ||

| Indirect (Advertising, Bundled) | |||

| By Pricing Model | Freemium | ||

| Tiered Subscription | |||

| One-time License | |||

| Bundled with Device / Telco Plan | |||

| By Device Type | Smartphone | ||

| Tablet | |||

| PC / Laptop | |||

| Smart-Home Device | |||

| By End-User | Consumers | ||

| Small and Medium Enterprises | |||

| Large Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What factors are driving the fastest growth in the personal cloud market?

5G expansion, AI-enhanced curation features, and telecom-operator bundles are the primary catalysts, jointly increasing global adoption and accelerating premium conversion rates.

How do data-residency laws affect market strategy?

Localized storage requirements encourage providers to deploy in-region nodes or partner with telecom operators, turning compliance into a competitive differentiator rather than a pure cost burden.

Why are SMEs moving away from on-premises NAS?

Subscription clouds cut capex, improve collaboration for hybrid teams, and embed enterprise-grade security controls, supporting a 19.66% CAGR for SME adoption through 2031.

Which pricing model is most successful today?

Tiered subscriptions are scaling fastest at 19.12% CAGR because they map premium features—AI editing, smart-home sync, compliance vaults—to users’ specific willingness to pay.

How large is the Personal Cloud market in 2026?

The Personal Cloud Market size is expected to increase from USD 33.30 billion in 2025 to USD 38.69 billion in 2026 and reach USD 82.06 billion by 2031, growing at a CAGR of 16.23% over 2026-2031.

Page last updated on: